Global Greenhouse Horticulture Market Size, Share, Trends & Growth Forecast Report, Segmented By Covering Material (Plastic Greenhouses and Glass Greenhouses), Product (Ornamentals and Edibles), Application (Greenhouse Films, Grow Bags, Wind Break and Shelter Nets, Horticulture Twines and Others) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis (2026 to 2034)

Market Size, 2025

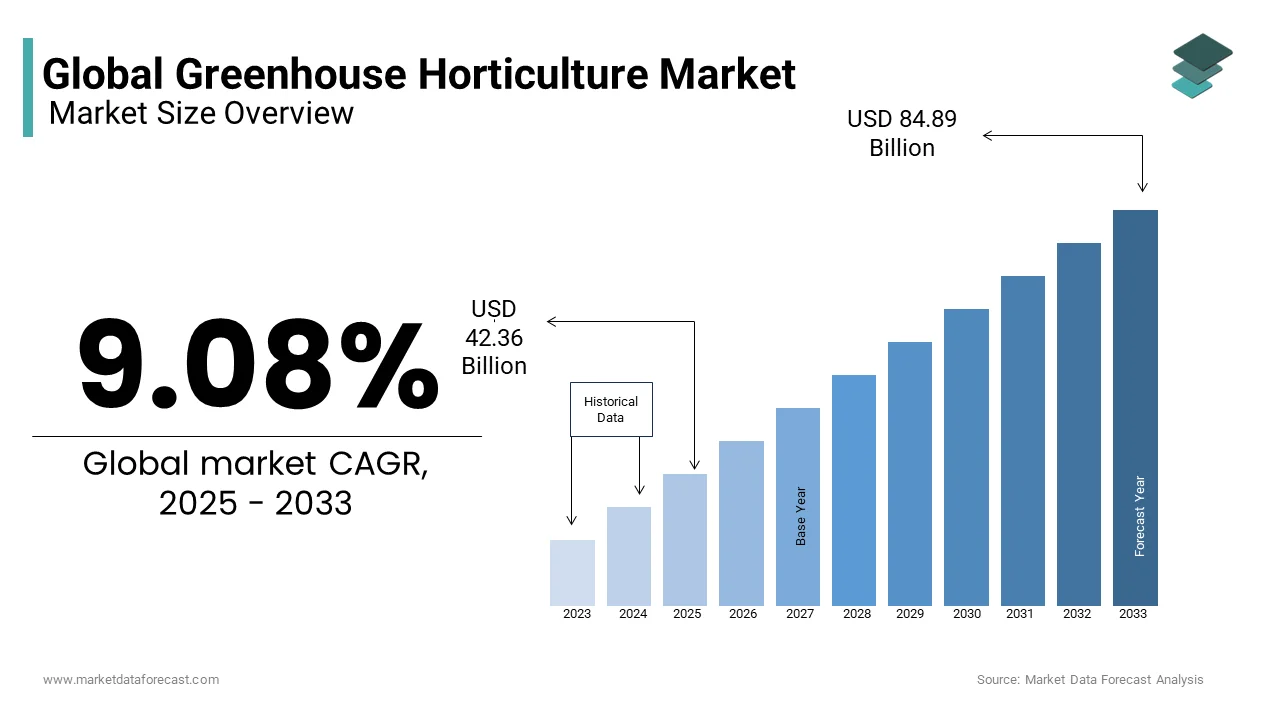

$42.36 BnMarket Estimate, 2026

$46.21 BnMarket Forecast, 2034

$92.61 BnCAGR, 2026–2034

9.08%Global Greenhouse Horticulture Market Report Summary

The global greenhouse horticulture market was valued at USD 42.36 billion in 2025, is estimated to reach USD 46.21 billion in 2026, and is projected to expand to USD 92.61 billion by 2034, growing at a CAGR of 9.08% during the forecast period from 2026 to 2034. The growth of the global greenhouse horticulture market is driven by rising demand for pesticide-free and high-quality produce, increasing pressure on arable land, and the need for climate-resilient agricultural systems. Controlled-environment agriculture enables year-round production, higher yields per square meter, and efficient use of water and nutrients, making greenhouses an attractive solution amid urbanization and climate variability. Furthermore, growing adoption of advanced technologies such as precision climate control, hydroponics, and automation is accelerating market expansion across developed and emerging economies.

Key Market Trends

Increasing consumer preference for safe, traceable, and residue-free fruits and vegetables. Rising adoption of plastic-covered greenhouses is due to their cost-effectiveness, flexibility, and ease of installation. Growing deployment of advanced greenhouse films to improve light diffusion, thermal insulation, and crop productivity. Expansion of urban and peri-urban greenhouse farming to reduce food miles and support local food systems. Integration of renewable energy solutions and smart technologies to improve energy efficiency and sustainability of greenhouse operations.

Segmental Insights

- Based on the covering material, the plastic greenhouses segment dominated the market in 2024. The segment’s leadership is attributed to lower capital costs, adaptability across diverse climatic conditions, and suitability for both small- and large-scale commercial operations.

- Based on product, the edibles segment held a prominent share of the global greenhouse horticulture market in 2024. Strong demand for greenhouse-grown vegetables, fruits, and herbs, driven by year-round availability and consistent quality, continues to support this segment’s dominance.

- Based on application, the greenhouse films segment led the market by capturing 44.3% of the share in 2024. Growth in this segment is driven by continuous innovation in film materials that enhance durability, light transmission, and energy efficiency.

Regional Insights

The global greenhouse horticulture market demonstrates strong regional dynamics.

- North America was the largest contributor in 2024, accounting for 32.4% of the global market share, supported by advanced agricultural infrastructure, high technology adoption, and strong demand for premium produce.

- Europe ranked second, holding a significant share in 2024, driven by stringent food safety regulations, sustainability mandates, and widespread adoption of high-tech greenhouses.

- The Asia-Pacific region is witnessing rapid growth, fueled by high population density, rising food demand, and government-led food security initiatives.

- Latin America is expanding steadily, led by Brazil and Mexico.

- Middle East and Africa region is expected to grow due to heavy investments in high-tech greenhouse projects to address water scarcity and food self-sufficiency.

Competitive Landscape

The global greenhouse horticulture market is competitive, with the presence of greenhouse solution providers, technology companies, and integrated project developers. Market players are focusing on innovation in climate control systems, automation, irrigation, and sustainable materials to strengthen their market positions. Prominent companies operating in the global greenhouse horticulture market include Richel Group, Hoogendoorn Growth Management B.V., Certhon, Dalsem Horticulture Projects B.V., HortiMaX B.V., Harnois Greenhouses, Priva B.V., Ceres Greenhouse Solutions, Van der Hoeven, Oritech Solutions, Netafim Ltd., Ridder Holding Harderwijk B.V., Rough Brothers Inc., and T.M. Greenhouses Ltd., among others.

Global Greenhouse Horticulture Market Size

The global greenhouse horticulture market was valued at USD 42.36 billion in 2025 and is anticipated to reach USD 46.21 billion in 2026 from USD 92.61 billion by 2034, growing at a CAGR of 9.08% from 2026 to 2034.

The Greenhouse Horticulture is the controlled cultivation of high-value horticultural crops such as vegetables, fruits, ornamental plants, and herbs within enclosed, climate-regulated structures designed to optimize plant growth regardless of external environmental conditions. These systems employ advanced technologies, including hydroponics, automated irrigation, supplemental lighting, and integrated pest management, to enhance yield, quality, and production consistency. Greenhouse cultivation, particularly in peri-urban zones, addresses this spatial challenge by enabling year-round production with reduced water and land consumption.

MARKET DRIVERS

Rising Demand for Pesticide-Free and Nutrient-Rich Produce Driving the Greenhouse Horticulture Market

The escalating global demand for pesticide-free and nutritionally dense produce due to rising consumer health consciousness and regulatory pressure on chemical residues, es is a major factor bolstering the growth of the Greenhouse Horticulture Market. According to the World Health Organization, over 200,000 annual deaths are attributed to acute pesticide poisoning, predominantly in agricultural communities, prompting stricter controls on field pesticide use. Greenhouse systems inherently limit pest intrusion, allowing producers to significantly reduce chemical inputs through integrated biological control methods. Furthermore, closed-loop hydroponic systems minimize leaching, protecting groundwater quality. Consumers in North America and Europe increasingly associate greenhouse-grown vegetables with safety and consistency, as evidenced by the Organic Trade Association noting a 12% year-on-year increase in demand for certified low-residue produce.

Arable Land Scarcity and High-Yield Greenhouse Systems Driving the Greenhouse Horticulture Market

The increasing scarcity and degradation of arable land, which is forcing agricultural innovation toward spatially efficient and environmentally resilient production models, is also expected to leverage the growth of the Greenhouse Horticulture Market. According to Wageningen University & Research, Dutch greenhouses produce up to 70 kg of tomatoes per square meter annually, compared to 10 kg in traditional open-field farming. This productivity leap is achieved through precision climate control, LED lighting, and CO₂ enrichment.

MARKET RESTRAINTS

High Capital and Energy Costs Restricting Growth of the Greenhouse Horticulture Market

The prohibitively high capital and operational costs associated with advanced climate-controlled facilities in low- and middle-income regions are restraining the growth of the greenhouse horticulture market. According to the International Energy Agency, energy accounts for up to 30% of operating costs in temperate climate greenhouses, where supplemental lighting and heating are essential during winter months. In developing economies such as India and Nigeria, where smallholder farmers dominate agriculture, such investments are financially unviable without substantial government or private sector subsidies.

Technical Complexity and Skills Shortages Hindering Growth of the Greenhouse Horticulture Market

The technical complexity and specialized knowledge required to manage modern greenhouse operations, which create a significant barrier to entry and scalability, ty are also hindering the growth of the greenhouse horticulture market. Effective greenhouse management demands expertise in plant physiology, climate control systems, nutrient formulation, and data-driven decision-making. According to a 2023 assessment by the Food and Agriculture Organization, only 18% of agricultural extension officers in developing countries have received training in controlled environment agriculture. Mismanagement of humidity or nutrient balance can lead to crop loss, with fungal outbreaks such as Botrytis costing growers up to 30% of yield, as documented by the European and Mediterranean Plant Protection Organization.

MARKET OPPORTUNITIES

Renewable Energy Integration and Urban Greenhouse Farming: Creating New Opportunities in the Greenhouse Horticulture Market

The integration of renewable energy systems with greenhouse operations by enabling sustainable, off-grid cultivation and reducing long-term operational dependencies is creating new opportunities for the growth of the greenhouse horticulture market. Solar photovoltaic panels, geothermal heating, and biomass energy are increasingly being deployed to power climate control and lighting systems.

The rise of urban and peri-urban greenhouse farms that supply hyper-local produce to densely populated cities by reducing food miles and enhancing freshness is greatly influencing the growth of the greenhouse horticulture markets. Vertical farms and rooftop greenhouses are being integrated into city infrastructure to meet the demands of urban consumers for traceable, low-carbon food. According to C40 Cities, urban agriculture could supply up to 10% of global vegetable demand if scaled effectively. In Singapore, where only 1% of land is designated for agriculture, the government’s “30 by 30” initiative aims to produce 30% of the nation’s nutritional needs locally by 2030, with greenhouse farms like Sustenir Agriculture already supplying supermarkets with indoor-grown kale and strawberries.

MARKET CHALLENGES

Energy Supply Dependence and Price Volatility Restricting Growth of the Greenhouse Horticulture Market

The heavy reliance on consistent energy supply in regions with unstable grids or high fossil fuel dependence may hinder the growth of the greenhouse horticulture market. In colder climates, maintaining optimal temperatures requires continuous heating, often from natural gas or electricity. As per Eurostat, greenhouse horticulture in the Netherlands consumed 7.2 billion cubic meters of natural gas in 2022, representing 10% of the nation’s industrial gas use. Energy price volatility, such as the 2022 European energy crisis, led to temporary shutdowns of 15% of Dutch greenhouse operations, according to the Netherlands Greenhouse Horticulture Association.

Plastic Waste and Environmental Impact of Greenhouse Materials Restraining the Greenhouse Horticulture Market

The environmental footprint associated with non-biodegradable construction materials and plastic waste generated by greenhouse operations is expected to fuel the growth of the greenhouse horticulture market. Most commercial greenhouses utilize polyethylene films, polycarbonate panels, and PVC piping, which degrade slowly and are rarely recycled. According to the United Nations Environment Programme, over 4.8 million tons of agricultural plastic are usedeach year globally, with less than 30% being collected for recycling. While biodegradable mulch films and recyclable cladding materials are emerging, their adoption remains limited due to higher costs and performance inconsistencies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.08% |

| Segments Covered | By Covering Material, Application, Product, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Richel Group, Hoogendoorn Growth Management B V, Certhon Inc, Dalsem Horticulture Projects B V, HortiMaX B V, Harnois Greenhouses, Priva B V, Ceres Greenhouse Solutions |

SEGMENTAL ANALYSIS

By Covering Material Insights

The plastic greenhouses segment was the largest by accounting for a dominant share of the greenhouse horticulture market in 2024, with its cost-effectiveness and adaptability in emerging agricultural economies. The initial construction cost of plastic greenhouses is up to 60% lower than that of glass-based structures, making them accessible to small and medium-scale growers. According to the International Fund for Agricultural Development, over 80% of greenhouse farmers in India, Turkey, and Morocco rely on polyethylene-covered tunnels due to their affordability and ease of assembly. Additionally, advancements in multilayer poly films with anti-drip and UV-blocking properties have significantly improved light transmission and durability.

The glass greenhouse segment is expected to grow with an emerging CAGR of 9.3% during the forecast period, with the rising deployment of energy-efficient, climate-smart glasshouses in high-income countries focused on sustainable intensification. Modern glass greenhouses integrate semi-transparent photovoltaic panels by enabling simultaneous solar energy generation and crop cultivation. According to the Joint Research Centre of the European Commission, agrivoltaic glasshouses can reduce grid dependency by up to 40% while maintaining 90% of photosynthetic active radiation transmission. Furthermore, their superior thermal mass and light diffusion properties support year-round production of high-value crops such as tomatoes and peppers.

By Product Insights

The edibles segment was the largest and held a prominent share of the global greenhouse horticulture market in 2024, with the growing imperative to ensure food security and nutritional availability in urbanized and land-constrained regions. Greenhouse-grown vegetables such as tomatoes, cucumbers, and leafy greens offer a consistent supply, reduced spoilage, and higher nutrient retention compared to open-field alternatives.

The ornamentals segment is swiftly emerging with a CAGR of 10.7% during the forecast period, with rising disposable incomes, urban beautification initiatives, and the expansion of commercial floral markets. Greenhouses enable year-round production of high-value flowers such as roses, orchids, and chrysanthemums, which are sensitive to climatic fluctuations. The Netherlands, the world’s largest flower exporter, produces over 9 billion cut roses annually in climate-controlled glasshouses, as reported by the Dutch Flower Council. The integration of LED lighting and CO₂ enrichment has further enhanced bloom quality and growth cycles by making greenhouse cultivation the preferred method for premium ornamental production.

By Application Insights

The greenhouse films segment was the largest by capturing 44.3% the share in 2024, with the primary covering material in low-cost, scalable greenhouse structures across Asia, the Middle East, and Latin America. Polyethylene (PE) and ethylene-vinyl acetate (EVA) films are widely adopted due to their high light diffusion, thermal insulation, and resistance to UV degradation. According to the Indian Agricultural Research Institute, multilayer greenhouse films can increase crop yield by up to 35% by optimizing photosynthetic efficiency. Additionally, innovations such as anti-fog and infrared-retaining films have extended the operational lifespan and energy efficiency of these structures.

The horticulture twines segment is likely to witness a CAGR of 12.1% throughout the forecast period with the increasing adoption of vertical crop training systems in high-density greenhouse farming, particularly for vining crops like tomatoes, cucumbers, and beans. Modern twines made from polypropylene and biodegradable polymers offer superior tensile strength and plant compatibility, reducing stem damage during growth. The shift toward automation has further boosted demand for pre-cut, pre-attached twines compatible with robotic planting systems.

REGIONAL ANALYSIS

North American Market Analysis

North America was the largest contributor to the global greenhouse horticulture market by occupying 32.4% of the share in 2024. The growth of the market in this region is driven by the advanced technological integration and strong consumer demand for locally grown, pesticide-free produce. The United States alone operates over 3,500 commercial greenhouses, with California, Florida, and Ontario (Canada) serving as key production hubs. The rise of vertical farms in urban centers like Chicago and New Jersey reflects a strategic shift toward reducing food miles.

Europe Market Analysis

Europe greenhouse horticulture market was positioned second by holding 38.3% of the market share in 2024. Germany and France are expanding their greenhouse capacity to reduce dependency on food imports, with Germany’s Federal Ministry of Food and Agriculture investing 150 million euros in protected horticulture by 2025. The European Green Deal and Farm to Fork Strategy further incentivize pesticide reduction and circular resource use, favoring greenhouse systems.

Asia Pacific Market Analysis

The Asia-Pacific greenhouse horticulture market growth is driven by the rapid expansion, fueled by population density and food security imperatives. China operates over 4 million hectares of greenhouse structures, the largest area globally, primarily for vegetable production, according to the Chinese Academy of Agricultural Sciences. India is witnessing accelerated adoption, with the Ministry of Agriculture promoting greenhouse clusters in states like Maharashtra and Karnataka through subsidy schemes covering up to 50% of setup costs. Japan has pioneered energy-efficient, multi-tiered greenhouses in urban areas, with Tokyo’s Pasona Urban Farm producing 100 kg of vegetables daily within a downtown office complex.

Latin America Market Analysis

Latin America greenhouse horticulture market growth is driven by Brazil and Mexico, leading regional development. Brazil’s greenhouse vegetable production grew by 18% between 2020 and 2023, driven by demand from urban centers like São Paulo and Brasília, according to the Brazilian Institute of Geography and Statistics. In Mexico, the Sinaloa and Baja California regions have expanded greenhouse exports of tomatoes and berries to the U.S., with protected cultivation now covering over 12,000 hectares, as per the National Institute of Statistics and Geography. Government-backed irrigation projects and private-sector investments in hydroponic systems are accelerating modernization, although access to financing and technical expertise remains uneven across rural areas.

Middle East And Africa Market Analysis

The Middle East and Africa greenhouse horticulture market growth is likely to be driven by the huge investments heavily in high-tech greenhouses as part of its National Food Security Strategy 2051, with indoor farms now producing 30% of domestic leafy greens, according to the Ministry of Climate Change and Environment. Saudi Arabia’s NEOM project includes a 330-hectare vertical farm using AI and hydroponics to grow vegetables in desert conditions. In South Africa, commercial greenhouse operations in the Western Cape supply supermarkets with year-round produce, with output increasing by 14% annually since 2020, as reported by Statistics South Africa.

COMPETITIVE LANDSCAPE

The competitive dynamics of the greenhouse horticulture market are defined by a convergence of agritech innovation, regional scalability, and ecosystem integration. While traditional equipment manufacturers maintain strong positions, new entrants specializing in AI, IoT, and vertical farming technologies are redefining performance benchmarks. Competition is shifting from standalone product superiority to holistic system optimization, where interoperability between climate control, irrigation, and lighting determines market preference. Regional disparities in infrastructure and policy create both barriers and opportunities, prompting firms to adopt localized strategies rather than one-size-fits-all models.

KEY MARKET PLAYERS

Some of the key players in the global greenhouse horticulture market include

- Richel Group

- Hoogendoorn Growth Management B.V

- CerthInc Ic.c

- Signify (formerly Philips Lighting)

- Rijk Zwaan

- Dalsem HorticultureProject B.VV...V

- HortiMaXB.V.V

- Harnois Greenhouses

- Priva BB.V.

- Ceres Greenhouse Solutions

- Van Der Hoeven

- Oritech Solutions

- Netafim Ltd

- Ridder Holding Harderwijk B.V.

- Rough Brothers Inc.

- TInc reenhouses Ltd

Top Players In The Market

- Rijk Zwaan has established a robust footprint in the Asia Pacific greenhouse horticulture sector by delivering high-performance vegetable seeds specifically bred for controlled environment agriculture. The company operates regional research centers in India, China, and Thailand, where it develops climate-resilient tomato, pepper, and cucumber varieties optimized for hydroponic and soilless cultivation. In 2023, it launched a proprietary tomato hybrid in Japan engineered for extended shelf life and enhanced Brix levels, catering to premium retail and restaurant supply chains. Rijk Zwaan also collaborates with local greenhouse operators to conduct on-site trials, ensuring genetic suitability under region-specific humidity and light conditions. Its digital seed performance platform, Seedlink, enables real-time monitoring of crop development, supporting data-driven farming decisions.

- Signify has become a pivotal enabler of advanced greenhouse horticulture in the Asia Pacific region through its targeted LED grow lighting solutions that enhance photosynthetic efficiency and crop uniformity. In 2023, Signify partnered with Sky Greens, a vertical farm in Singapore, to optimize light recipes for leafy greens, achieving a 30% reduction in energy consumption while increasing yield. Its research collaboration with Chiba University in Japan has led to customized spectral formulations for strawberries and herbs grown in multi-tiered urban farms. Signify also provides lighting design services and energy audits, helping growers maximize return on investment.

- Netafim has significantly influenced the Asia Pacific greenhouse horticulture landscape by advancing precision irrigation and fertigation systems tailored for high-density, soilless cultivation. The company has implemented its drip irrigation and hydroponic solutions in large-scale greenhouse clusters in India, Vietnam, and Australia, where water conservation is a strategic priority. It also established a demonstration farm in Hyderabad to showcase sustainable greenhouse practices for Indian farmers transitioning from open-field cultivation. Netafim’s partnership with government agricultural agencies in Indonesia supports training programs on drip-based greenhouse farming for smallholders.

Top Strategies Used By The Key Market Participants

Key players in the greenhouse horticulture market are leveraging technological innovation, strategic partnerships, regional customization, digital integration, and sustainability-driven product development to consolidate their market presence. Companies are investing in R&D to create crop-specific lighting spectra, climate-adaptive covering materials, and smart irrigation algorithms. Collaborations with research institutions and local governments enable field validation and policy alignment. Firms are tailoring product portfolios to regional needs, such as drought-resistant systems in arid zones or compact designs for urban farms.

RECENT MARKET NEWS

- In January 2024, Rijk Zwaan launched a climate-resilient tomato hybrid in Japan specifically designed for hydroponic greenhouse systems by enhancing flavor profile and disease resistance to meet premium market demands.

- In May 2024, Signify partnered with Sky Greens in Singapore to deploy advanced LED grow lights in a vertical farm, which is optimizing light recipes for leafy greens and reducing energy use by 30% while increasing yield consistency.

- In August 2024, Netafim inaugurated a demonstration greenhouse in Hyderabad, India, showcasing drip irrigation and fertigation solutions for smallholder farmers transitioning to protected cultivation.

- In February 2024, Rijk Zwaan initiated a multi-year collaboration with Chiba University in Japan to refine seed performance under controlled LED lighting conditions, bridging plant genetics with smart horticulture.

- In June 2024, Signify introduced a new spectral lighting module for strawberry cultivation in South Korean greenhouses by improving fruit color, sweetness, and harvest uniformity through tailored light wavelengths.

MARKET SEGMENTATION

This research report on the global greenhouse horticulture market has been segmented and sub-segmented based on covering material, application, product, and region.

By Covering Material

- Plastic

- Glass

By Application

- Greenhouse Films

- Grow Bags

- Windbreak

- Shelter Nets

- Horticulture Twines

- Others

By Product

- Ornamentals

- Edibles

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the current size of the global greenhouse horticulture market?

The market was valued at around USD 38.83 billion in 2024 and is steadily growing due to rising demand for fresh, year-round produce.

What is driving growth in the greenhouse horticulture market?

Key drivers include food security concerns, climate change resilience, urbanization, and technological advancements in controlled environment agriculture.

Which region leads the greenhouse horticulture market globally?

Europe holds the largest market share, driven by strict food safety regulations and a strong preference for sustainable farming practices.

What is the expected growth rate of this market?

The market is projected to grow at a CAGR of about 7.6% to 9.2% from 2025 to 2033, reflecting increasing adoption worldwide.

How do greenhouses benefit crop production?

Greenhouses create controlled environments that protect crops from weather and pests, enabling higher yields and extended growing seasons.

What role do technological innovations play in this market?

Innovations like automation, hydroponics, and smart systems enhance efficiency, reduce resource use, and improve crop quality.

Why is the demand for greenhouse horticulture increasing?

Population growth, urban land limits, and consumer preference for fresh, pesticide-free produce boost greenhouse cultivation worldwide.

What major challenges does the greenhouse horticulture industry face?

Challenges include high initial costs, energy consumption, and the need for skilled labor to manage advanced technologies.

How does government support impact this market?

Subsidies, grants, and incentives for modern farming techniques significantly encourage investment and adoption of greenhouse horticulture.

What future trends are expected in greenhouse horticulture?

The market will see smart greenhouses, sustainable materials, and precision farming to meet evolving environmental and consumer demands.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com