Europe Post Harvest Treatment Products Market Size, Share, Trends & Growth Forecast Report By Type, By Application, and By Country (Germany, France, Spain, Italy, United Kingdom & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Post-Harvest Treatment Products Market Report Summary

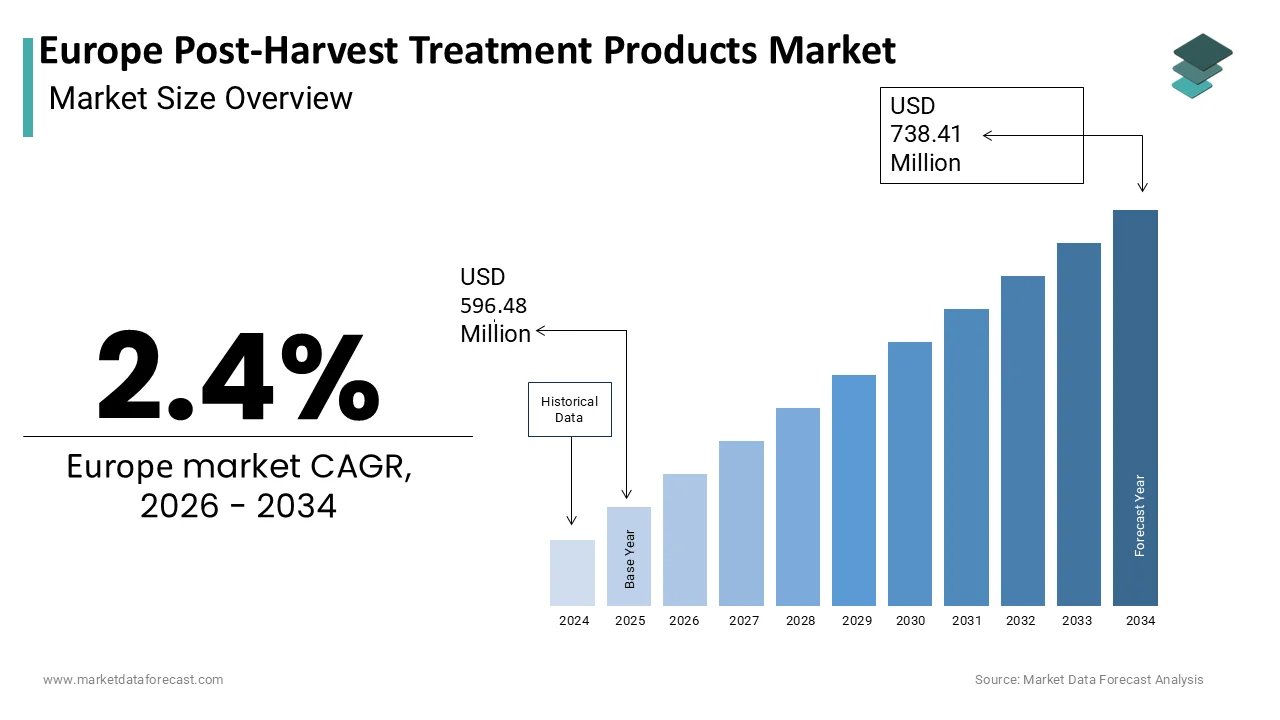

he Europe Post-Harvest Treatment Products Market was valued at USD 596.48 million in 2025 and is projected to reach USD 738.41 million by 2034, growing from USD 610.80 million in 2026 at a CAGR of 2.4% during the forecast period. Growth is driven by rising consumer demand for fresh, high-quality produce, stringent EU food safety and waste-reduction regulations, and integration of digital monitoring and smart storage solutions. High operational costs and limited adoption among small-scale farmers are shaping market dynamics.

Key Market Trends

- Rising adoption of IoT-enabled smart storage with real-time spoilage prediction

- Growing demand for natural edible coatings like chitosan and alginate films

- Increasing shift toward plant-based and biodegradable preservation alternatives

- Expansion of blockchain traceability for post-harvest treatment compliance

- Rising regulatory pressure under EU Packaging and Packaging Waste Regulation

Segmental Insights

- Based on type, fungicides held the largest share in 2025, driven by their critical role in preventing fungal spoilage in high-value crops.

- Based on application, fruits held the majority share in 2025, driven by high perishability and premium pricing incentivizing preservation investment.

- Coatings and wax is the fastest-growing type segment, projected at a CAGR of 6.8%, driven by consumer preference for natural, chemical-free preservation.

Regional Insights

- Germany led the market in 2025, supported by strict retail quality standards from chains like Aldi and Lidl.

- France holds a significant share, driven by its status as a leading agricultural exporter requiring specialized post-harvest care.

- Spain is a prominent market supported by its year-round production and role as a major European export hub.

- Italy contributes notably due to its premium fruit and vegetable production requiring targeted preservation.

- Vegetables is the fastest-growing application segment, projected at a CAGR of 5.9%, driven by rising plant-based dietary habits.

Competitive Landscape

The market is highly competitive, with multinational corporations and specialized regional players competing on chemical innovation, biological preservation methods, and regulatory compliance. Companies are investing in bio-based preservatives and digital monitoring tools to align with EU sustainability goals.

Prominent players in the market include Bayer AG, BASF SE, Syngenta AG, UPL Limited, Corteva Agriscience, Nufarm Limited, Eastman Chemical Company, JBT Corporation, Pace International LLC, Decco Worldwide Post-Harvest Holdings B.V., Xeda International S.A., and Agrofresh Solutions Inc.

Europe Post-Harvest Treatment Products Market Size

The Europe Post-Harvest Treatment Products Market is projected to grow from USD 596.48 million in 2025 to USD 610.80 million in 2026 and reach USD 738.41 million by 2034, registering a CAGR of 2.4% during the forecast period from 2026 to 2034.

Post-harvest treatment refers to the practices applied to agricultural produce immediately after harvesting. This critical phase bridges the gap between farm production and consumer consumption, addressing physiological decay and microbial contamination. In Europe, where stringent food safety regulations govern the supply chain, these treatments are indispensable for maintaining the integrity of fresh fruits, vegetables, and grains. According to Eurostat, the European Union generates approximately 58 million tons of food waste annually, with household consumption serving as the single largest structural contributor to the total volume. This substantial loss underscores the urgency for effective preservation methods. Furthermore, as per sources, the European agricultural sector yields roughly 270 million tons of major cereal crops during standardized annual tracking cycles, forming the baseline requirements for regional storage and distribution infrastructure. The integration of advanced cooling systems, edible coatings, and controlled atmosphere storage has become standard practice among European distributors. Consumer demand for year-round availability of seasonal produce further amplifies the need for these technologies. As urbanization increases and supply chains lengthen, the role of post-harvest treatment evolves from mere preservation to a strategic component of food security. The market is thus driven by the dual imperative of reducing waste and meeting the high-quality expectations of European consumers who prioritise freshness and nutritional value in their dietary choices.

MARKET DRIVERS

Rising Consumer Demand for Fresh and High Quality Produce

European consumers exhibit an unwavering preference for fresh, nutrient-rich, and visually appealing produce, which propels the growth of the Europe post harvest treatment market. This directly fuels the adoption of advanced post-harvest treatments. The European retail sector faces immense pressure to deliver products that meet rigorous aesthetic and safety standards, as shoppers increasingly reject items showing signs of wilting or discolouration. According to the Food Waste Index Report by the United Nations, identifying baseline handling losses along early post-harvest nodes highlights a critical worldwide challenge for standard preservation networks. To combat this, retailers rely on treatments such as ethylene inhibitors and antimicrobial washes to maintain firmness and colour. As per macroeconomic consumption data compiled by Eurostat, collective spending on overall food and non-alcoholic beverages constitutes one of the largest foundational segments of total household expenditure across the European Union. This consumer behavior compels suppliers to invest in technologies that slow down respiration rates and delay senescence. For instance, the use of modified atmosphere packaging has seen widespread adoption across major supermarkets in Germany and France to extend the viability of leafy greens and berries. The expectation for consistent quality regardless of seasonal variations drives continuous innovation in preservation techniques. Consequently, the market for post-harvest solutions expands as stakeholders strive to align supply chain capabilities with the exacting standards of modern European shoppers who view freshness as a non-negotiable attribute of their purchases.

Stringent Regulatory Frameworks Ensuring Food Safety and Waste Reduction

The European Union enforces some of the world’s most comprehensive food safety and environmental regulations, which further drive the expansion of the Europe post harvest treatment market. According to the environmental framework established under the European Commission's Farm to Fork Strategy, binding regional targets demand coordinated action across member states to systematically scale down waste volumes across both retail and household levels by 2030. As per the European Environment Agency (EEA), food waste generates significant lifecycle greenhouse gas emissions, underscoring the urgent climate necessity of integrating preventative management into broader national climate strategies. These regulations require strict adherence to hygiene standards during processing and storage, thereby increasing the reliance on approved sanitizers and coating agents that prevent microbial growth without compromising safety. According to the European Commission, statutory maximum residue limits for agricultural substances are routinely updated in the EU database to safeguard consumers while providing parameters for post-harvest treatments. This regulatory scrutiny drives investment in compliant technologies such as ozone treatment and biological control agents. Additionally, the EU’s circular economy action plan encourages the minimization of losses at every stage of production, further incentivizing the use of advanced storage solutions. Companies operating within this framework must continuously adapt their processes to meet evolving legal requirements, which creates a sustained demand for innovative and compliant post-harvest treatments. The regulatory landscape thus not only ensures consumer protection but also fosters a market environment where technological advancement in preservation is both necessary and rewarded.

MARKET RESTRAINTS

High Operational Costs Associated with Advanced Preservation Technologies

The implementation of sophisticated post-harvest treatment systems involves substantial capital expenditure and ongoing operational costs, which are a significant restraint for many participants in the European market. Advanced technologies such as controlled atmosphere storage facilities, automated sorting lines, and precision cooling systems require heavy initial investment that may be prohibitive for small- and medium-sized enterprises. According to the European Investment Bank (EIB), deploying advanced capital upgrades across rural supply chains depends heavily on increasing targeted knowledge transfer and supporting regional infrastructure programs. Furthermore, the energy consumption associated with maintaining optimal storage conditions is considerable, with refrigeration accounting for a large portion of operational expenses in cold chain logistics. The recent volatility in energy prices across Europe has exacerbated this burden, forcing some operators to reconsider the extent of their preservation efforts. Maintenance of specialized equipment also demands skilled labor and regular servicing, adding to the overall cost structure. Small-scale farmers and local distributors often lack the financial resources to integrate these high-cost solutions, leading to disparities in market access and product quality. This economic barrier restricts the uniform application of post-harvest treatments across the region, particularly in Eastern European countries where agricultural margins are thinner. Consequently, while the technology exists to significantly reduce waste, its high cost prevents universal adoption, leaving a segment of the market reliant on less effective and traditional methods that result in higher spoilage rates.

Limited Awareness and Adoption Among Small-Scale Farmers

A significant portion of regional agriculture consists of small-scale farming operations, which hinders the expansion of the Europe post harvest treatment market. These farms frequently lack the awareness or resources to implement modern post-harvest treatments. As per Eurostat, the vast majority of agricultural enterprises in the European Union operate as small-scale family holdings, creating distinct structural challenges for regional supply chain consolidation and localized resource optimization. The knowledge gap regarding the benefits and application of advanced preservation techniques remains wide in rural areas, where extension services may be underfunded or inaccessible. Many small farmers are unaware of cost-effective solutions such as natural coatings or simple ventilation improvements that could significantly reduce their post-harvest losses. This lack of technical know-how is compounded by limited access to training programs and demonstration projects that showcase the efficacy of modern treatments. The fragmented nature of small-scale production also makes it difficult to achieve economies of scale, rendering individual investments in technology financially unviable. Consequently, a large volume of produce from these farms suffers from premature spoilage before reaching broader markets. The absence of coordinated efforts to educate and support these farmers hinders the overall efficiency of the European food supply chain. Without targeted initiatives to bridge this awareness gap, post-harvest treatments remain underutilized. Consequently, their potential to enhance food security and farmer incomes is lost, perpetuating agricultural waste and economic inefficiency.

MARKET OPPORTUNITIES

Integration of Digital Monitoring and Smart Storage Solutions

The advent of Internet of Things technology offers a transformative opportunity for the Europe post harvest treatment market. This enables real-time monitoring and precise control of storage conditions. Smart sensors can track temperature, humidity, and ethylene levels within storage facilities, allowing for immediate adjustments that optimize preservation outcomes. According to the European Commission's Common Agricultural Policy (CAP), significant financial support is directed toward precision agriculture and data-driven infrastructure to accelerate the green transition in rural areas. This digital shift enables predictive analytics that forecast spoilage risks and recommend proactive interventions, thereby reducing waste and improving inventory management. Large distribution centers in countries like the Netherlands and Belgium are already adopting these smart systems to enhance their logistical efficiency. The ability to collect and analyze data from multiple points in the supply chain provides valuable insights into product behavior under various conditions, facilitating continuous improvement in treatment protocols. Furthermore, blockchain technology offers transparency in tracking the history of post-harvest treatments, assuring consumers and regulators of compliance with safety standards. This digital integration not only enhances operational efficiency but also opens new revenue streams through data-driven services. As connectivity improves across rural Europe, the scalability of these smart solutions increases, offering a pathway for broader adoption. The convergence of digital innovation and post-harvest science thus creates a dynamic environment where technology drives sustainability and profitability in equal measure.

Expansion of Organic and Sustainable Treatment Methods

The growing consumer preference for organic produce paves the way for the development and adoption of sustainable post-harvest treatment methods, which is likely to boost the expansion of the European market. Traditional chemical preservatives are often incompatible with organic certification standards, driving demand for natural alternatives such as plant-based extracts, essential oils, and biodegradable coatings. As per the Research Institute of Organic Agriculture (FiBL), the total volume of farmland under organic management and European retail sales continues to show steady long-term growth. This trend encourages innovation in biopreservation techniques that utilize the antimicrobial properties of natural substances to extend shelf life without synthetic additives. Companies are investing in research to identify effective organic compounds that can replace conventional chemicals while maintaining efficacy against pathogens and spoilage organisms. The European Green Deal further supports this shift by promoting sustainable agricultural practices and reducing reliance on synthetic inputs. Opportunities exist for startups and established firms to develop proprietary formulations that meet organic standards while delivering comparable performance to traditional treatments. Additionally, the use of renewable energy sources in storage facilities aligns with the sustainability goals of organic producers, creating a holistic approach to post-harvest management. This alignment with consumer values and regulatory directions positions sustainable treatments as a key growth area, offering a competitive advantage to those who can successfully navigate the technical challenges of natural preservation.

MARKET CHALLENGES

Complexity of Supply Chain Coordination Across Multiple Jurisdictions

The complexity of coordinating supply chains across multiple countries with varying regulations and infrastructure capabilities impedes the growth of the Europe post harvest treatment market. Each member state may have specific requirements for food safety inspections, labelling, and transportation standards, creating administrative burdens for cross-border trade. According to the European Shippers' Council (ESC), resolving regulatory barriers and infrastructure gaps across regional freight corridors is necessary to reduce delays for intermodal logistics operators. The fragmentation of the market means that treatments approved in one country may face additional scrutiny or rejection in another, complicating the distribution of perishable goods. This regulatory heterogeneity requires companies to maintain multiple compliance protocols, increasing operational complexity and risk. Furthermore, differences in infrastructure quality, such as cold chain reliability, vary significantly between Western and Eastern European regions, affecting the consistency of treatment outcomes. The lack of harmonized standards for certain emerging technologies also creates uncertainty for investors and innovators. Coordinating timely deliveries across borders while maintaining strict temperature controls is logistically challenging, especially during peak seasons when capacity is strained. These coordination issues can lead to bottlenecks that compromise product quality and increase waste, undermining the effectiveness of post-harvest treatments. Addressing these systemic challenges requires greater collaboration among regulatory bodies and industry stakeholders to streamline processes and ensure seamless movement of treated produce across the continent.

Environmental Concerns Regarding Chemical Residues and Waste Disposal

Environmental sustainability concerns remain a growing challenge for the European post-harvest treatment market. This applies particularly to the disposal of chemical residues and packaging materials. While treatments are essential for preservation, the accumulation of non-biodegradable packaging and chemical runoff from washing facilities raises ecological alarms. As per the statutory frameworks established under the EU Packaging and Packaging Waste Regulation (PPWR), strict, legally binding targets demand that all packaging materials circulating in the market be fully recyclable to reduce commercial plastic waste. Consumers and regulators are increasingly scrutinizing the environmental footprint of these practices, pressuring companies to adopt eco-friendly alternatives. The challenge lies in finding treatments that are both effective and environmentally benign, as many natural alternatives currently lack the longevity or potency of synthetic options. Additionally, the disposal of wastewater containing sanitizers and preservatives requires specialized treatment to prevent contamination of local water bodies, adding to operational costs. The transition to circular economy principles demands that companies rethink their waste management strategies, investing in recycling infrastructure and biodegradable materials. However, the high cost and limited availability of sustainable alternatives hinder rapid adoption. Balancing the need for effective preservation with environmental responsibility remains a complex dilemma for industry players. Failure to address these concerns can result in reputational damage and regulatory penalties, making environmental stewardship a critical challenge that must be navigated carefully to ensure long-term market viability.

SEGMENTAL ANALYSIS

By Type Insights

The fungicides segment was the largest in the Europe post harvest treatment market and occupied a commanding share in 2025. This supremacy of the segment was supported by its critical role in preventing microbial spoilage and extending the shelf life of perishable goods. The dominance of this segment is also driven by the high susceptibility of fruits and vegetables to fungal infections during storage and transport, which results in significant economic losses if left untreated. According to ScienceDaily, post-harvest fungal infections routinely wipe out 10% to 20% of harvested crops globally, with changing weather patterns driving a critical industry shift toward multi-functional biocontrol and non-chemical preservation strategies. The widespread adoption of fungicides is further supported by their cost-effectiveness and proven efficacy in controlling common diseases such as grey mould and blue mould in apples and citrus fruits. Regulatory approvals for specific active ingredients ensure that these treatments meet safety standards while providing reliable protection. The extensive cultivation of high-value crops in countries like Spain and Italy, which are prone to fungal attacks in humid conditions, amplifies the demand for these chemicals. Additionally, the integration of fungicides with other preservation methods enhances their performance, making them indispensable for large-scale distributors. The consistent need to maintain visual appeal and prevent decay in retail environments ensures that fungicides remain the primary choice for producers seeking to minimize waste and maximize marketability. This entrenched reliance on fungal control mechanisms solidifies the segment's leadership position in the regional market landscape.

On the other hand, the coatings and wax segment is on the rise and is expected to be the fastest-growing segment in the market, with a CAGR of 6.8% over the forecast period. This rapid growth of the segment is fueled by increasing consumer preference for natural and edible preservation methods that avoid synthetic chemical residues. As per the Research Institute of Organic Agriculture (FiBL), the long-term retail volume and distribution networks for certified organic foods continue to demonstrate stable European market maturation. These coatings create a protective barrier that reduces moisture loss and respiration rates, effectively extending freshness without altering taste or texture. Innovations in chitosan- and alginate-based films have gained traction due to their antimicrobial properties and environmental compatibility. The European Green Deal’s emphasis on reducing plastic waste also favours coatings that replace traditional plastic packaging, aligning with sustainability goals. Major retailers in Germany and France are increasingly adopting coated produce to meet eco-conscious consumer expectations, further accelerating market penetration. The versatility of coatings across various fruit and vegetable types allows for broad application, enhancing their appeal among diverse agricultural stakeholders. Continuous research into improving the durability and effectiveness of natural coatings ensures sustained innovation, positioning this segment as a dynamic growth engine within the broader post-harvest treatment industry.

By Application Insights

In 2025, the fruits segment held the majority share of the Europe post harvest treatment market because of its high perishability and significant economic value in the regional food supply chain. The delicate nature of fruits such as berries, apples, and citrus makes them highly susceptible to physical damage and microbial decay, necessitating intensive preservation efforts. According to Eurostat, monitoring the structural supply chain infrastructure for fresh produce categories is essential to mitigating product losses between harvest fields and regional consumer markets. The premium pricing of many fruit varieties incentivizes producers to invest in advanced treatments to maintain quality and reduce shrinkage. Retailers prioritize the visual appeal of fruits, driving the use of wax coatings and ethylene blockers to preserve color and firmness during extended distribution cycles. The seasonal variability of fruit production also demands storage solutions that allow for year-round availability, further boosting treatment adoption. Countries like Spain and Italy, which are major exporters of fresh fruits, rely heavily on these technologies to meet international quality standards. The high sensitivity of fruits to temperature fluctuations and handling errors makes post-harvest treatments essential for minimizing losses. This critical dependence on preservation technologies to safeguard revenue and consumer satisfaction cements the leading position of the fruits segment in the market.

However, the vegetables segment is expected to exhibit a noteworthy CAGR of 5.9% from 2026 to 2034 due to rising health consciousness and increased dietary inclusion of fresh produce. This reflects shifting consumer habits towards plant-based diets. As per Freshfel Europe, average fresh produce intake across the European Union measures roughly 355.71 grams per day per person, tracking below the minimum daily target of 400 grams recommended by the World Health Organization. Leafy greens and cruciferous vegetables are particularly prone to rapid wilting and microbial contamination, requiring specialized treatments such as antimicrobial washes and controlled atmosphere storage. The expansion of ready-to-eat vegetable products in urban markets has intensified the demand for effective preservation methods that ensure safety and longevity. Retailers are investing in advanced cooling and packaging technologies to maintain the crispness and nutritional value of vegetables throughout the supply chain. The growth of organic vegetable farming also drives the adoption of natural preservation techniques, aligning with consumer preferences for clean-label products. Increased awareness of food waste issues encourages stakeholders to adopt efficient treatment protocols for vegetables, which traditionally had shorter shelf lives compared to fruits. This convergence of health trends, retail innovation, and sustainability goals propels the vegetables segment toward rapid expansion in the coming years.

COUNTRY LEVEL ANALYSIS

Germany Post-Harvest Treatment Market Analysis

Germany led the European post-harvest treatment market and captured a significant share in 2025. This leading position of the German market was attributed to its status as the largest economy and a major hub for food processing and distribution. The country’s advanced agricultural infrastructure and strict adherence to food safety regulations drive significant demand for high-quality preservation technologies. According to the Centre for the Promotion of Imports (CBI), Germany stands as a demanding European market for imported fresh produce, where compliance with strict commercial certification standards drives supplier adoption of precise quality-handling procedures. The presence of leading retail chains such as Aldi and Lidl imposes stringent quality standards on suppliers, encouraging the adoption of innovative preservation methods. German consumers are increasingly aware of food waste issues, supporting initiatives that utilize advanced storage and treatment solutions to extend product viability. The country’s strong focus on sustainability also promotes the use of eco-friendly treatments, aligning with national environmental policies. Investment in research and development for new preservation technologies is high, with numerous institutions collaborating with industry players to innovate. The well-developed cold chain logistics network in Germany ensures that treated produce reaches consumers in optimal condition, reinforcing the market’s growth. This combination of regulatory rigor, consumer awareness, and technological advancement establishes Germany as a key driver of the regional post-harvest treatment market.

France Post-Harvest Treatment Market Analysis

France was positioned second in the Europe post harvest treatment market due to its status as a leading agricultural producer and exporter of high-value fresh produce. The country’s diverse climate supports the cultivation of a wide variety of fruits and vegetables, many of which require specialised post-harvest care to maintain export quality. As per INRAE, the optimization of supply chains and the deployment of information and communication technologies within the fruit and vegetable sector are vital components for tracking and mitigating product losses from the farm gate to the end consumer. French consumers place a high premium on freshness and origin, driving retailers to adopt advanced treatment methods that ensure product integrity. The government’s support for sustainable agriculture through policies like the Ecophyto plan encourages the use of reduced-risk pesticides and biological controls. The presence of major wholesale markets such as Rungis facilitates the distribution of treated produce across Europe, necessitating efficient preservation protocols. Innovation in edible coatings and natural antimicrobials is gaining traction among French producers seeking to differentiate their products in competitive markets. The strong cultural emphasis on gastronomy and quality food further reinforces the demand for effective post-harvest treatments. This alignment of agricultural strength, consumer expectations, and policy support sustains France’s influential role in the regional market.

Spain Post-Harvest Treatment Market Analysis

Spain is a key contributor to the Europe post harvest treatment market. It is one of the continent’s largest producers and exporters of fresh fruits and vegetables. The country’s favorable climate allows for year-round production, but the high temperatures and humidity levels increase the risk of spoilage, making post-harvest treatments essential. According to the Spanish Ministry of Agriculture, Fisheries and Food, Spain acts as a primary European production and export hub for global fruit, wine, and olive oil channels, anchoring the country's macro-agricultural trade value. The concentration of production in regions like Andalusia and Murcia drives demand for scalable treatment solutions such as fungicides and controlled atmosphere storage. Spanish exporters face intense competition in European markets, compelling them to invest in advanced preservation methods to maintain quality during transit. The adoption of integrated pest management strategies includes post-harvest treatments that reduce reliance on synthetic chemicals while ensuring efficacy. Retail partnerships with northern European countries require strict compliance with quality and safety norms, further boosting treatment adoption. The ongoing modernization of packing houses and cold storage facilities enhances the efficiency of post-harvest operations. This strategic focus on maintaining export competitiveness through superior preservation techniques solidifies Spain’s key position in the market.

Italy Post-Harvest Treatment Market Analysis

Italy maintains a strong position in the Europe post harvest treatment market owing to its renowned production of high-quality fruits, vegetables, and specialty crops. The country’s agricultural sector is characterized by small- to medium-sized farms that produce premium goods for both domestic consumption and export. As per sources, the Italian fruit and vegetable trade is highly susceptible to logistics-phase product loss, highlighting a structural need for targeted transport management to conserve embedded resources. The prevalence of perishable items such as tomatoes, citrus fruits, and leafy greens drives demand for targeted preservation solutions. Italian consumers are highly discerning regarding food quality, influencing retailers to prioritize freshness and appearance through advanced treatment methods. The government’s support for organic farming and sustainable practices encourages the adoption of natural preservatives and eco-friendly packaging. Collaboration between research institutions and industry players fosters innovation in bio-based treatments that align with traditional agricultural values. The tourism sector also contributes to demand for high-quality fresh produce, further emphasizing the importance of post-harvest care. This blend of culinary heritage, export orientation, and sustainability focus ensures Italy’s continued relevance in the regional post-harvest treatment landscape.

United Kingdom Post-Harvest Treatment Market Analysis

The United Kingdom plays a significant role in the Europe post harvest treatment market despite its departure from the European Union, maintaining strong trade links and regulatory alignment in food safety. Moreover, the country relies heavily on imports for fresh produce, particularly during winter months, making post-harvest treatments crucial for maintaining quality during long supply chains. According to the Waste & Resources Action Programme (WRAP), collaborative reduction goals across the food industry focus on altering storage behaviors and product packaging to prevent retail and household spoilage. British retailers exert considerable influence over supply chain standards, requiring suppliers to implement rigorous preservation protocols. Consumer awareness of sustainability and ethical sourcing encourages the use of environmentally friendly treatment options. The UK’s advanced logistics infrastructure supports the efficient distribution of treated produce across the country. Investment in smart storage solutions and digital monitoring systems is increasing among major distributors to enhance efficiency. The focus on reducing the carbon footprint in the food supply chain also promotes innovations in low-energy preservation methods. This combination of import dependency, retail power, and sustainability goals sustains the UK’s active participation in the post-harvest treatment market.

COMPETITIVE LANDSCAPE

The competition in the Europe post harvest treatment market is characterized by the presence of several multinational corporations and specialized regional players who strive for technological superiority. Major companies compete through continuous innovation in chemical formulations and biological preservation methods to address the stringent regulatory requirements of the European Union. The market exhibits a moderate level of consolidation as larger entities acquire smaller firms to expand their product offerings and geographic reach. Competitive dynamics are influenced by the increasing demand for sustainable and eco-friendly solutions that align with consumer preferences for organic produce. Companies differentiate themselves by providing integrated services that combine treatment products with technical support and digital monitoring tools. Price competition remains relevant but is often secondary to product efficacy and compliance with safety standards. The entry of new startups focusing on niche biological treatments adds further complexity to the competitive landscape. Established players leverage their extensive distribution networks and brand reputation to maintain dominance while adapting to evolving market trends. This dynamic environment fosters constant improvement in preservation technologies and service delivery models.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Post-Harvest Treatment Products Market include

- Bayer AG

- BASF SE

- Syngenta AG

- UPL Limited

- Corteva Agriscience

- Nufarm Limited

- Eastman Chemical Company

- JBT Corporation

- Pace International LLC

- Decco Worldwide Post-Harvest Holdings B.V.

- Xeda International S.A.

- Agrofresh Solutions, Inc.

TOP LEADING PLAYERS IN THE MARKET

- BASF SE stands as a prominent entity in the Europe post harvest treatment market by offering advanced chemical solutions that preserve produce quality. The company focuses on developing innovative fungicides and coatings that extend shelf life while ensuring food safety compliance. BASF actively collaborates with agricultural stakeholders to introduce sustainable preservation technologies that align with European environmental regulations. Recent initiatives include the launch of bio-based preservatives that reduce chemical residues on fruits and vegetables. The company invests heavily in research and development to create effective treatments for high-value crops. By integrating digital tools for monitoring treatment efficacy, BASF enhances its service offerings. Their commitment to sustainability drives the adoption of eco-friendly products across the supply chain. This strategic focus strengthens their reputation as a reliable partner for farmers and distributors seeking efficient post-harvest solutions.

- Corteva Inc plays a significant role in the Europe post harvest treatment sector through its portfolio of crop protection and seed technologies. The company provides specialized fungicides and ethylene management solutions that help maintain the freshness of harvested produce. Corteva emphasizes innovation by developing biological control agents that offer safer alternatives to traditional chemicals. Their recent actions involve expanding production capabilities for natural preservatives to meet growing organic demand. The company partners with local distributors to ensure widespread availability of its treatment products across European markets. Corteva also engages in educational programs to inform farmers about best practices in post-harvest handling. By focusing on integrated pest management strategies, they provide holistic solutions that address multiple preservation challenges. This approach enhances their market presence and supports sustainable agricultural practices throughout the region.

- Syngenta Group contributes extensively to the Europe post harvest treatment market by delivering comprehensive solutions for preserving fruit and vegetable quality. The company offers a range of fungicides and storage technologies that mitigate spoilage risks during transport and retail display. Syngenta prioritizes sustainability by investing in research for low-impact preservation methods that comply with strict European standards. Recent developments include the introduction of smart packaging solutions that monitor produce condition in real time. The company collaborates with retailers to implement effective post-harvest protocols that reduce waste. Syngenta also supports farmers through technical assistance programs that optimize treatment application. Their focus on innovation ensures that clients have access to cutting-edge technologies for maintaining product integrity. This dedication to quality and sustainability reinforces their position as a key player in the regional market landscape.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe post harvest treatment market primarily focus on product innovation and strategic partnerships to maintain a competitive advantage. Companies invest heavily in research and development to create sustainable and effective preservation solutions that meet regulatory standards. Developing bio-based and natural treatments allows firms to cater to the growing demand for organic produce. Strategic collaborations with retailers and distributors help integrate these technologies into existing supply chains efficiently. Expansion into emerging markets within Eastern Europe provides new growth opportunities for established entities. Mergers and acquisitions enable companies to broaden their product portfolios and access new technologies. Emphasizing digital integration through smart monitoring systems enhances service offerings and customer engagement. These strategies collectively drive market growth and ensure long-term viability in a highly regulated environment.

MARKET SEGMENTATION

This research report on the European post-harvest treatment products market is segmented and sub-segmented into the following categories.

By Type

- Fungicides

- Coatings and Wax

By Application

- Fruits

- Vegetables

By Country

- Germany

- France

- Spain

- Italy

- United Kingdom

- Rest of EuropeA

Frequently Asked Questions

1. What is driving growth in Europe?

Growth is driven by demand for longer shelf life, higher export quality standards, retailer requirements for visual quality, and regulatory and consumer pressure to reduce food loss and chemical residues.

2. Which product types are most important?

Key types include fungicides, coatings and waxes, ethylene inhibitors, sanitizers, and sprout inhibitors, each targeting specific spoilage pathways in different crops.

3. Which crops are the main users?

Fruits and vegetables are the largest application segment, while cereals, grains, nuts, and seeds also use post-harvest treatments for storage protection and quality retention.

4. Which countries lead the market?

Germany, the UK, France, Spain, and Italy are key markets due to large horticultural sectors, advanced cold chains, and strong export activity.

5. Who are the major players?

Major players include BASF, Syngenta, AgroFresh, Fomesa Fruitech (Decco), United Phosphorus Ltd, Nufarm, Sumitomo Chemical, Apeel Sciences, and other agrochemical and post-harvest technology firms.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com