Europe Procurement Outsourcing Market Size, Share, Trends, and Growth Analysis Report, Segmented by Component, Deployment, Industry Vertical, Organization Size, and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

$2.12 BnMarket Estimate, 2026

$2.33 BnMarket Forecast, 2034

$4.94 BnCAGR, 2026–2034

9.85%Europe Procurement Outsourcing Market Report Summary

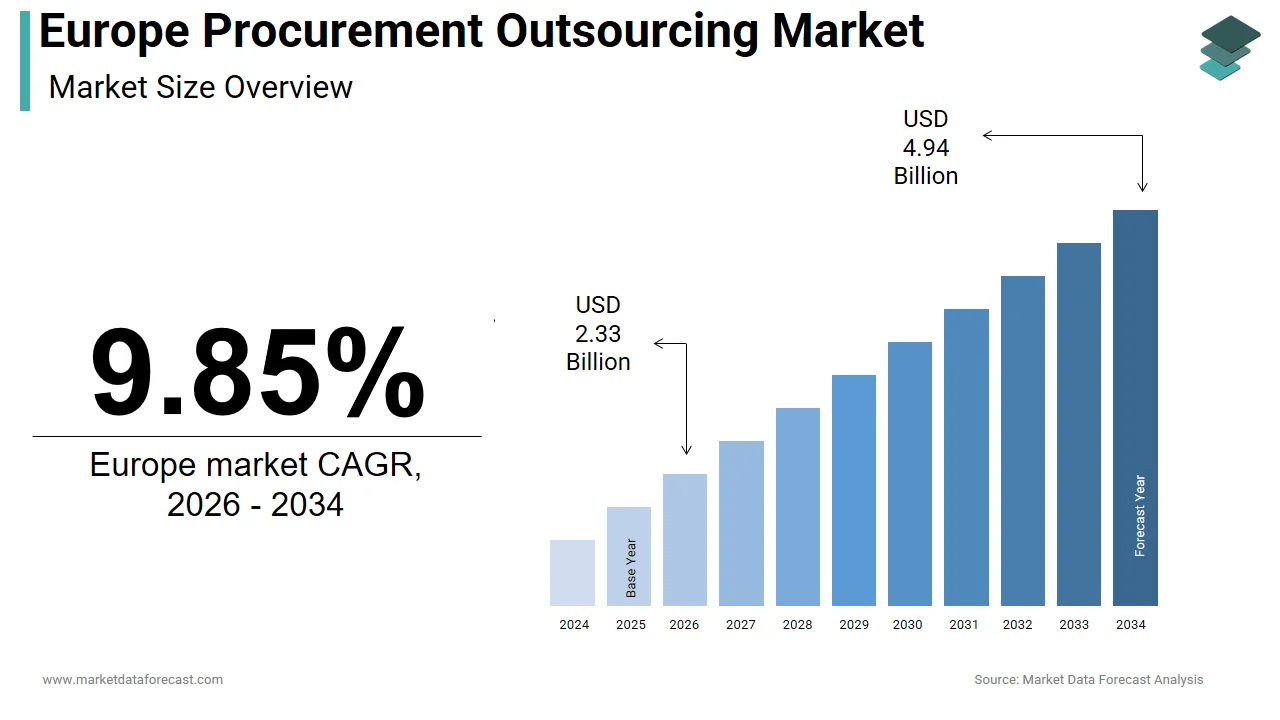

The Europe procurement outsourcing market was valued at USD 2.12 billion in 2025, is estimated to reach USD 2.33 billion in 2026, and is projected to reach USD 4.94 billion by 2034, growing at a CAGR of 9.85% from 2026 to 2034. Market growth is driven by increasing demand for cost optimization, operational efficiency, and strategic sourcing across enterprises. Organizations are increasingly outsourcing procurement functions to focus on core business activities while leveraging advanced technologies such as AI, analytics, and automation. Additionally, the growing adoption of cloud-based procurement solutions and the need for supplier risk management are further accelerating market expansion across Europe.

Key Market Trends

- Rising demand for cost reduction and process efficiency.

- Increasing adoption of cloud-based procurement solutions.

- Growing use of AI, analytics, and automation in sourcing.

- Expansion of strategic sourcing and supplier management services.

- Increasing focus on risk management and compliance.

Segmental Insights

- Based on component, the services segment dominated the Europe procurement outsourcing market in 2025, driven by increasing reliance on third-party expertise.

- Based on deployment, the cloud segment held the largest share in 2025, supported by scalability, flexibility, and cost efficiency.

- Based on industry vertical, the BFSI segment led the market with 32.3% share in 2025, driven by complex procurement needs and regulatory requirements.

Regional Insights

The Europe procurement outsourcing market is witnessing steady growth across major economies.

- Germany led the market in 2025 with 24.1% share, supported by strong industrial and corporate sectors.

- The United Kingdom followed with 20.8% share, driven by a mature outsourcing ecosystem and financial services industry.

- France remains a key market due to strict regulatory frameworks and increasing focus on sustainable procurement practices.

Competitive Landscape

The Europe procurement outsourcing market is highly competitive, with companies focusing on digital transformation, service innovation, and expanding global delivery capabilities. Strategic partnerships and investments in AI-driven procurement platforms are key competitive strategies.

Prominent companies operating in the Europe procurement outsourcing market include Infosys Limited, Tata Consultancy Services Ltd., HCL Technologies Ltd., WNS (Holdings) Ltd., NB Ventures, Inc. (Global eProcure), Wipro Limited, IBM Corporation, Accenture PLC, Genpact Limited, and Capgemini SE.

Europe Procurement Outsourcing Market Size

The Europe procurement outsourcing market was valued at USD 2.12 billion in 2025, is estimated to reach USD 2.33 billion in 2026, and is projected to reach USD 4.94 billion by 2034, growing at a CAGR of 9.85% from 2026 to 2034.

Procurement outsourcing is the practice of hiring an external third-party provider to manage all or part of an organization's purchasing activities, including supplier sourcing, contract negotiation, and transactional purchasing. This business practice allows organizations to leverage external expertise, advanced technologies, and global supplier networks to enhance efficiency and reduce operational costs. In the contemporary European economic landscape, procurement has evolved from a transactional activity to a strategic function focused on value creation, risk mitigation, and sustainability. As per Eurostat, extra-EU imports of goods into the European Union totaled €2.5 trillion in 2025, underscoring the critical importance of efficient procurement mechanisms in managing cross-border trade flows. Furthermore, the European Commission reported that public procurement accounts for approximately 15% of the European Union’s gross domestic product, highlighting the substantial volume of transactions managed through formalized procurement processes. The market is characterized by a shift towards digital transformation, with companies increasingly adopting artificial intelligence and blockchain technologies to streamline supplier selection and contract management. Regulatory frameworks such as the Corporate Sustainability Reporting Directive are also influencing procurement strategies, compelling organizations to prioritize ethical sourcing and environmental compliance. Consequently, outsourcing partners are expected to provide not only cost savings but also robust compliance monitoring and sustainability reporting capabilities. This evolving dynamic positions procurement outsourcing as a vital component of corporate strategy, enabling businesses to navigate complex regulatory environments and volatile supply chains while focusing on core competencies.

MARKET DRIVERS

Escalating Focus on Supply Chain Resilience and Risk Mitigation

Rising global disruptions have forced European organizations to prioritize supply chain resilience, which accelerates the growth of the Europe procurement outsourcing market. Consequently, this shift is driving higher demand for specialized procurement outsourcing services. Recent geopolitical tensions, pandemics, and natural disasters have exposed vulnerabilities in traditional linear supply chains, necessitating more agile and diversified sourcing strategies. As per the European Central Bank (ECB), annual inflation stabilized at 2.1% in late 2025, but continued volatility in international trade prompted firms to outsource procurement to manage unpredictable import price fluctuations. Outsourcing partners offer access to extensive global supplier networks and advanced risk management tools that enable companies to identify alternative sources quickly and mitigate potential disruptions. These providers utilize predictive analytics to monitor supplier health and geopolitical risks, allowing organizations to proactively adjust their sourcing strategies. Additionally, procurement outsourcing firms possess the expertise to navigate complex international trade regulations and customs procedures, reducing the administrative burden on internal teams. The ability to scale procurement operations up or down in response to market fluctuations provides further flexibility, ensuring business continuity during periods of uncertainty. By leveraging the specialized knowledge and resources of outsourcing providers, European companies can build more robust and resilient supply chains that withstand external shocks. This strategic imperative drives sustained investment in procurement outsourcing, as organizations seek to safeguard their operations against future disruptions and maintain competitive advantage in a volatile global market.

Stringent Regulatory Compliance and Sustainability Mandates

The implementation of rigorous environmental, social, and governance regulations across the region serves as a significant driver for the Europe procurement outsourcing market. The European Union’s Green Deal and the Corporate Sustainability Reporting Directive impose strict requirements on companies to disclose and manage the environmental and social impacts of their supply chains. Under the Corporate Sustainability Reporting Directive (CSRD), approximately 50,000 European companies are now mandated to report on sustainability, a fourfold increase that drives the need for specialized outsourcing partners to manage complex value-chain data. Managing these requirements internally requires specialized expertise and resources that many organizations lack. Procurement outsourcing providers offer dedicated sustainability services, including supplier audits, carbon footprint assessments, and ethical sourcing verification, helping clients meet regulatory obligations efficiently. These partners utilize advanced software platforms to track and analyze sustainability data across multiple tiers of the supply chain, ensuring transparency and accountability. Furthermore, outsourcing enables companies to align their procurement practices with circular economy principles, such as waste reduction and material recycling, which are increasingly mandated by law. The complexity of navigating diverse national regulations within the EU further incentivizes organizations to rely on experts who possess comprehensive knowledge of local compliance requirements. Businesses can outsource procurement functions to ensure adherence to evolving legal standards. This approach also enhances corporate reputation while meeting the growing expectations of environmentally conscious consumers and investors.

MARKET RESTRAINTS

Data Security and Privacy Concerns

Data security and privacy concerns are a limiting factor for the growth of the Europe procurement outsourcing market. This is particularly challenging given the region's stringent regulatory environment. Procurement processes involve the exchange of sensitive information, including supplier contracts, pricing details, and proprietary product specifications. According to the 2025 Verizon DBIR, breaches involving third parties now account for 30% of all cybersecurity incidents, doubling from previous years and increasing the perceived risk of outsourcing critical data. The General Data Protection Regulation imposes severe penalties for data breaches, making organizations hesitant to share critical information with third-party providers. Companies fear that outsourcing may expose them to additional security risks, especially if providers lack robust cybersecurity infrastructure or operate in jurisdictions with weaker data protection laws. The complexity of ensuring end-to-end data encryption and access control across multiple stakeholders further complicates the outsourcing arrangement. Additionally, the potential for intellectual property theft or unauthorized data sharing by vendor employees remains a persistent concern. Organizations must conduct thorough due diligence and implement strict contractual safeguards to mitigate these risks, which can be time-consuming and costly. The fear of reputational damage resulting from a data breach often outweighs the potential cost savings of outsourcing, leading some companies to retain procurement functions in-house. This caution slows down the adoption of outsourcing services, particularly among industries handling highly sensitive data, such as pharmaceuticals and defense.

Resistance to Change and Internal Cultural Barriers

Resistance to change and internal cultural barriers within organizations significantly restrain the expansion of the Europe procurement outsourcing market. Many established companies have long-standing internal procurement teams and processes, creating a sense of ownership and reluctance to delegate these functions to external providers. A survey by the Chartered Institute of Procurement and Supply (CIPS) found that only 2% of organizations have fully automated procurement processes, indicating that a lack of digital maturity remains a significant barrier to effective outsourcing integration. Employees often fear job losses or a loss of control over strategic decisions, leading to passive or active opposition to outsourcing projects. This cultural inertia can hinder the smooth transition of responsibilities and disrupt operational efficiency during the initial phases of engagement. Additionally, there is often a lack of trust in external providers’ ability to understand the unique nuances of the organization’s business model and culture. Misalignment between the client’s expectations and the provider’s delivery can result in dissatisfaction and contract termination. Overcoming these barriers requires significant change management efforts, including clear communication, stakeholder engagement, and training programs. However, many organizations underestimate the effort required to manage this cultural shift, leading to failed outsourcing implementations. The difficulty in altering entrenched organizational behaviors and mindsets thus serves as a persistent restraint on the broader acceptance and expansion of procurement outsourcing services across the European market.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Advanced Analytics

The integration of artificial intelligence and advanced analytics into procurement processes unlocks potential for the expansion of the Europe procurement outsourcing market. AI-driven tools can automate routine tasks such as invoice processing, supplier screening, and contract analysis, freeing up human resources for strategic activities. As per a study, AI-centric spending in Europe is projected to reach $133 billion by 2028. Procurement outsourcing providers are leveraging this to offer "Autonomous Sourcing" as a high-margin service. Outsourcing providers are investing heavily in these technologies to offer enhanced value to clients, including predictive demand forecasting and dynamic pricing optimization. Machine learning algorithms can analyze vast amounts of historical data to identify patterns and trends, enabling more informed decision-making. For instance, AI can predict supplier delays based on weather patterns or political events, allowing companies to proactively adjust their inventory levels. Additionally, natural language processing tools can review contracts for compliance risks and unfavorable terms, reducing legal exposure. The ability to provide real-time visibility into spend data and supplier performance empowers organizations to negotiate better terms and identify cost-saving opportunities. By leveraging these advanced technologies, outsourcing partners can deliver superior insights and operational improvements that were previously unattainable. This technological differentiation creates new revenue streams for providers and strengthens their value proposition, driving increased demand for sophisticated procurement outsourcing services in Europe.

Expansion of Strategic Sourcing and Category Management Services

The expansion of strategic sourcing and category management services creates new paths for growth in the Europe procurement outsourcing market. Organizations are increasingly seeking partners who can provide end-to-end strategic support, rather than just transactional processing. According to research, modern procurement leaders are shifting from pure cost-cutting to "Total Value" models, where outsourcing can unlock 15% to 30% reductions in category-specific tail spend through specialized digital platforms. Outsourcing providers are expanding their offerings to include deep category expertise in areas such as raw materials, IT services, and logistics. This specialized knowledge allows them to identify market trends, benchmark prices, and negotiate favorable contracts on behalf of clients. Furthermore, strategic sourcing involves collaborative relationships with key suppliers to drive innovation and continuous improvement. Outsourcing partners facilitate these collaborations by managing supplier performance and fostering long-term partnerships. The shift towards value-based procurement, where focus is placed on total cost of ownership rather than just purchase price, further drives demand for strategic services. Providers who can demonstrate tangible value through improved quality, reduced lead times, and enhanced supplier reliability are well-positioned to capture market share. This evolution from tactical to strategic procurement outsourcing enables clients to achieve broader business objectives, such as innovation acceleration and market expansion, creating a compelling case for deeper engagement with outsourcing partners.

MARKET CHALLENGES

Complexity of Managing Multi-Tier Supply Chains

The complexity of managing multi-tier supply chains remains a serious challenge for the Europe procurement outsourcing market. Modern supply chains often extend beyond direct suppliers to include sub-suppliers and raw material producers, creating an intricate network that is difficult to monitor and control. Per the European Commission's CSDDD guidelines, companies must now monitor operations down to the "Tier-N" level. A lack of data interoperability between outsourcers and sub-suppliers remains the primary hurdle for 70% of EU firms. Outsourcing providers struggle to gather accurate data from these distant nodes in the supply chain, limiting their ability to assess risks and ensure compliance. The sheer volume of suppliers and the diversity of geographical locations add to the logistical and administrative burden. Additionally, differing regulatory standards across countries complicate the standardization of procurement processes and compliance checks. Language barriers and cultural differences further hinder effective communication and collaboration with remote suppliers. The lack of standardized data formats and systems among various suppliers makes integration and data analysis challenging. Providers must invest in advanced tracking technologies and build extensive networks of local partners to gain visibility into multi-tier supply chains. However, these efforts are resource-intensive and often yield incomplete results. The inability to fully map and manage complex supply networks limits the effectiveness of outsourcing services and exposes clients to unforeseen risks, representing a persistent challenge for the industry.

Talent Shortage and Skill Gaps in Specialized Procurement Roles

A shortage of skilled professionals with expertise in strategic procurement and supply chain management further hinders the expansion of the Europe procurement outsourcing market. As procurement functions become more strategic and technology-driven, the demand for individuals with advanced analytical, negotiation, and digital skills has surged. According to Cedefop's 2025 Skills Intelligence, over 70% of European employers report a shortage of workers with the specific "Twin Transition" skills (Green + Digital) required to operate modern, outsourced procurement ecosystems. Outsourcing providers face intense competition for this limited talent pool, driving up recruitment and retention costs. The lack of qualified personnel can hinder the ability of providers to deliver high-quality services and meet client expectations. Additionally, the rapid pace of technological change requires continuous upskilling and reskilling of the workforce, which demands significant investment in training and development. Providers who fail to attract and retain top talent risk losing clients to competitors who can offer more sophisticated and reliable services. The scarcity of experienced category managers and strategic sourcing experts further exacerbates the problem, limiting the capacity of providers to expand their service offerings. This human resource constraint impedes the growth and innovation potential of the procurement outsourcing sector, making talent acquisition and development a critical challenge for industry participants.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Component, Deployment, Industry Vertical, Organization Size, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Component Insights

The services segment led the Europe procurement outsourcing market and captured a substantial share in 2025. This leading position of the segment is attributed to the inherent nature of procurement outsourcing, which primarily involves the delegation of human-intensive tasks such as strategic sourcing, supplier management, and contract negotiation to specialized third-party providers. Key drivers for this segment are the urgent requirement for specialized expertise and the optimization of operational performance, often unmet internally. Information from the Chartered Institute of Procurement and Supply indicates that a high proportion of organizations in Europe are turning to external service providers to secure specialized expertise and enhance the speed of their supply chain operations. Companies rely on service providers to manage complex global supply chains, navigate regulatory landscapes, and implement best practices without the burden of hiring and training extensive internal staff. Additionally, the shift towards strategic procurement requires deep analytical capabilities and market intelligence, which service providers offer through dedicated teams of experts. These teams conduct spend analysis, identify cost-saving opportunities, and negotiate favorable terms with suppliers, delivering tangible financial benefits to clients. The flexibility offered by service-based models allows businesses to scale their procurement operations up or down based on demand fluctuations, ensuring optimal resource utilization. Furthermore, the ongoing management of supplier relationships and performance monitoring requires continuous human intervention, reinforcing the demand for comprehensive service offerings. This reliance on expert manpower and strategic guidance solidifies the Services segment as the cornerstone of the procurement outsourcing market in Europe.

The solutions segment is anticipated to witness the fastest CAGR of 13.5% during the forecast period. This swift expansion of the segment is fueled by the increasing adoption of digital technologies and automation tools that enhance procurement processes. Research emphasizes a strong and consistent growth in software investment as European firms prioritize automated analytics to navigate increasingly complex supply networks. Furthermore, the primary driver is the integration of artificial intelligence and machine learning into procurement platforms, which enables predictive analytics, automated supplier screening, and intelligent contract management. These technologies significantly reduce manual effort, minimize errors, and accelerate decision-making processes. Organizations are investing in cloud-based procurement suites that offer real-time visibility into spend data and supplier performance, allowing for more agile and informed sourcing strategies. Additionally, the rise of blockchain technology for secure and transparent transaction recording is gaining traction, particularly in industries with complex supply chains. The demand for user-friendly interfaces and mobile accessibility further drives the adoption of advanced procurement solutions. Companies seek integrated platforms that seamlessly connect with enterprise resource planning systems, providing a unified view of procurement activities. The ability to leverage data-driven insights for strategic advantage makes these solutions indispensable for modern businesses. Consequently, the rapid technological evolution and the compelling value proposition of efficiency and accuracy drive the robust growth of the Solutions segment.

By Deployment Insights

The cloud deployment segment was the largest in the Europe procurement outsourcing market and occupied a significant share in 2025. This prominence of the segment is credited to the numerous advantages cloud-based platforms offer, including scalability, accessibility, and lower total cost of ownership. Cloud solutions enable organizations to access procurement tools and data from any location, facilitating collaboration among distributed teams and global suppliers. A study reflects nearly universal internet connectivity across the continent, supporting a vast infrastructure of digital services that underpin modern business functions. A key force behind this segment is the ease of implementation and maintenance compared to on-premises systems. Cloud-based procurement platforms require minimal upfront infrastructure investment and offer automatic updates, ensuring that users always have access to the latest features and security patches. This model aligns well with the subscription-based pricing structures preferred by many European enterprises, particularly small and medium-sized businesses. Additionally, cloud solutions provide enhanced disaster recovery capabilities and data redundancy, ensuring business continuity in the event of local hardware failures. The ability to integrate seamlessly with other cloud-based enterprise applications, such as customer relationship management and human resources systems, creates a cohesive digital ecosystem. Furthermore, the flexibility to scale resources up or down based on usage demands allows companies to optimize costs effectively. These benefits make cloud deployment the preferred choice for organizations seeking agility, efficiency, and competitive advantage in their procurement operations.

The on-premises segment is likely to experience the fastest CAGR of 4.2% from 2026 to 2034. It remains relevant for specific sectors that prioritize data sovereignty and strict control over IT infrastructure. Large enterprises and organizations in highly regulated industries, such as defense and government, often prefer on-premises solutions to maintain full authority over their sensitive procurement data. As per the European Union Agency for Cybersecurity, concerns about data privacy and security continue to influence deployment choices, with some entities opting for on-premises systems to mitigate risks associated with third-party cloud storage. The primary driver for this segment is the need for customized security protocols and compliance with stringent local regulations that may restrict data storage outside national borders. On-premises systems allow organizations to implement tailored security measures and avoid dependency on internet connectivity, ensuring uninterrupted operations in areas with poor network coverage. Additionally, businesses with significant existing IT infrastructure investments may find it cost-effective to utilize their current servers rather than migrating to the cloud. However, the high initial capital expenditure and ongoing maintenance requirements limit the appeal of on-premises solutions for most retailers. The lack of flexibility and scalability compared to cloud options further restrains growth. Despite these challenges, the on-premises segment persists in niche markets where control and security are paramount, maintaining a stable but limited presence in the overall market.

By Industry Vertical Insights

The Banking, Financial Services, and Insurance (BFSI) segment dominated the Europe procurement outsourcing market and accounted for a 32.3% share in 2025. This dominance of the segment is driven by the sector's complex supply chain requirements, stringent regulatory compliance needs, and the critical importance of cost efficiency. Financial institutions procure a wide range of services and goods, including IT infrastructure, professional services, and office supplies, requiring sophisticated management strategies. According to the European Banking Authority, financial institutions are facing a massive wave of new regulatory requirements, driving up operational costs and encouraging the outsourcing of non-core functions to specialized providers. A top factor for this segment is the need for transparency and risk mitigation in supplier relationships. BFSI organizations face intense scrutiny regarding anti-money laundering and know your customer regulations, which extend to their supply chains. Outsourcing providers offer specialized expertise in vendor due diligence, contract compliance, and risk assessment, helping banks navigate these complex requirements. Additionally, the competitive nature of the financial sector drives the need for cost optimization, with procurement outsourcing enabling significant savings through strategic sourcing and volume consolidation. The ability to leverage global supplier networks and negotiate better terms further enhances the value proposition for BFSI clients. Furthermore, the digitization of banking services requires efficient procurement of technology solutions, an area where specialized providers excel. These factors collectively establish the BFSI sector as the leading adopter of procurement outsourcing services in Europe.

The Healthcare segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 14.2% during the forecast period, owing to the increasing complexity of medical supply chains, rising healthcare expenditures, and the urgent need for operational efficiency. Hospitals and healthcare providers procure a vast array of products, including pharmaceuticals, medical devices, and equipment, requiring precise inventory management and timely delivery. As per the World Health Organization, healthcare spending in Europe is expected to increase by 4 percent annually, driving demand for optimized procurement processes. The primary driver is the critical need for supply chain resilience and reliability, particularly highlighted by recent global health crises. Healthcare organizations are increasingly outsourcing procurement to ensure uninterrupted access to essential medical supplies and to mitigate risks associated with supplier disruptions. Outsourcing providers offer specialized expertise in managing regulated medical products, ensuring compliance with safety standards and tracking expiration dates. Additionally, the shift towards value-based care encourages hospitals to reduce costs without compromising quality, making strategic sourcing essential. Procurement outsourcing enables healthcare providers to consolidate purchases, negotiate better prices with suppliers, and improve inventory turnover. The integration of digital tools for real-time tracking and automated reordering further enhances efficiency. Furthermore, the growing emphasis on sustainability in healthcare procurement drives the adoption of eco-friendly sourcing practices facilitated by outsourcing partners. These dynamics contribute to the robust growth of the healthcare segment in the procurement outsourcing market.

COUNTRY LEVEL ANALYSIS

Germany Procurement Outsourcing Market Analysis

Germany was the top performer in the Europe procurement outsourcing market and accounted for a 24.1% share in 2025. A key booster of the market in Germany is the complex global supply chains of its multinational corporations, which require sophisticated sourcing strategies and risk management. Moreover, the market position in Germany shows a strong industrial base, particularly in the automotive and manufacturing sectors, which rely heavily on efficient supply chain management. German companies are known for their emphasis on precision, quality, and regulatory compliance, driving the demand for specialized procurement services. Reports from the Federal Statistical Office of Germany confirm that the industrial sector remains a cornerstone of the national economy, with the manufacturing segment serving as a primary driver for sophisticated procurement strategies and supply chain management. Companies seek outsourcing partners to navigate international trade regulations, manage supplier diversity, and ensure sustainability compliance. The stringent environmental laws in Germany, such as the Supply Chain Due Diligence Act, compel businesses to monitor their suppliers closely, a task efficiently handled by outsourcing providers. Additionally, the high labor costs in Germany incentivize companies to outsource non-core procurement activities to reduce operational expenses. The presence of leading global procurement service providers in major cities like Frankfurt and Munich further strengthens the market ecosystem. Furthermore, the digital transformation initiatives in German industry, known as Industry 4.0, drive the adoption of advanced procurement technologies and analytics. These factors collectively sustain Germany’s position as the largest and most mature market for procurement outsourcing in Europe.

United Kingdom Procurement Outsourcing Market Analysis

The United Kingdom was the next prominent country in the Europe procurement outsourcing market and captured a 20.8% share in 2025. The main reason for the market is the post Brexit regulatory environment, which has introduced new complexities in cross-border trade and supply chain management. Besides these, the market in the UK reveals a mature service sector and a strong tradition of outsourcing business processes. British companies are early adopters of strategic procurement practices, driven by the need for cost efficiency and competitive advantage in a globalized economy. Data from the Office for National Statistics emphasizes that the service sector is the overwhelming contributor to the nation's economic output, fueling a sustained and substantial requirement for professional procurement and outsourcing expertise. Organizations are increasingly relying on outsourcing partners to navigate customs procedures, tariff implications, and changing trade agreements. Additionally, the strong presence of financial services and retail industries in the UK drives demand for specialized procurement solutions in these sectors. The focus on sustainability and corporate social responsibility is also a key driver, with companies seeking providers who can help them achieve ethical sourcing goals. The UK’s robust legal framework and established business infrastructure support the growth of procurement outsourcing. Furthermore, the availability of skilled professionals and advanced technology infrastructure enables providers to deliver high-quality services. These dynamics maintain the UK’s status as a pivotal market for procurement outsourcing innovation and adoption.

France Procurement Outsourcing Market Analysis

France remains a noteworthy player in the Europe procurement outsourcing market due to the stringent regulatory framework regarding public procurement and corporate sustainability. The market status in France is influenced by strong government initiatives promoting economic efficiency and a growing emphasis on sustainable procurement practices. French enterprises, particularly in luxury goods, aerospace, and energy sectors, are increasingly adopting outsourcing to enhance their supply chain resilience and compliance. As per the National Institute of Statistics and Economic Studies, the French economy is showing steady growth, with businesses investing in digital transformation and operational optimization. The French Duty of Vigilance Law requires large companies to identify and prevent human rights and environmental risks in their supply chains, driving demand for specialized outsourcing services. Companies seek providers with expertise in supplier auditing, risk assessment, and compliance monitoring to meet these legal obligations. Additionally, the focus on cost reduction and efficiency improvement in a competitive global market encourages French firms to outsource strategic sourcing activities. The presence of major multinational corporations headquartered in Paris further boosts the market. Furthermore, the integration of digital technologies in procurement processes is gaining traction, supported by government incentives for digitalization. These factors contribute to the steady growth and sophistication of the procurement outsourcing market in France.

Italy Procurement Outsourcing Market Analysis

Italy experienced a steady growth in the Europe procurement outsourcing market owing to the need for modernization and efficiency in traditional manufacturing sectors. The market status in Italy is characterized by a diverse industrial base, including fashion, automotive, and machinery, which presents significant opportunities for procurement outsourcing. Italian companies are increasingly recognizing the benefits of external expertise in managing complex supply chains and reducing costs. As per the Italian National Institute of Statistics, the service sector represents 73 percent of Italy’s GDP, indicating a strong potential for business process optimization. Many Italian firms are small and medium-sized enterprises that lack the internal resources for sophisticated procurement management, making outsourcing an attractive option. The focus on export-oriented growth also drives demand for providers who can manage international supplier relationships and logistics. Additionally, the increasing awareness of sustainability and ethical sourcing issues is prompting companies to seek specialized support. The government’s support for digital innovation and infrastructure development further facilitates market growth. Furthermore, the integration of Italy into broader European supply chains necessitates compliant and efficient procurement practices. These factors contribute to the emerging potential of the procurement outsourcing market in Italy, with steady growth expected in the coming years.

Spain Procurement Outsourcing Market Analysis

Spain is predicted to expand significantly in the Europe procurement outsourcing market over the forecast period due to the need for cost reduction and process optimization in key sectors such as tourism, retail, and telecommunications. The market status in Spain is marked by ongoing digital transformation initiatives and increasing adoption of strategic procurement practices. Spanish enterprises are increasingly leveraging outsourcing to improve operational efficiency and compete in the global market. Recent data from the National Statistics Institute of Spain underscores that digital solutions are becoming increasingly integral to the country's economic performance, reflecting a broad-based transformation that enhances the efficiency of national commerce. Companies are seeking outsourcing partners to streamline procurement processes, reduce administrative burdens, and access global supplier networks. The rise of e-commerce and digital services has also increased the complexity of supply chains, driving demand for specialized management solutions. Additionally, the focus on sustainability and corporate responsibility is influencing procurement decisions, with companies seeking providers who can help them achieve green sourcing goals. The improvement in digital infrastructure and internet connectivity supports the adoption of cloud-based procurement tools. Furthermore, the presence of multinational corporations with regional headquarters in Madrid and Barcelona stimulates market activity. These factors collectively drive the expansion of the procurement outsourcing market in Spain, with a positive outlook for future growth.

COMPETITIVE LANDSCAPE

The competition in the Europe procurement outsourcing market is intense and characterized by the presence of global consulting firms, specialized business process providers, and technology-driven startups. Major players compete on the basis of technological innovation, domain expertise, and the ability to deliver measurable cost savings and efficiency improvements. Differentiation is increasingly achieved through the integration of advanced analytics, artificial intelligence, and automation tools that enhance decision-making and process agility. Sustainability and compliance capabilities have become critical differentiators, as European regulations demand greater transparency and ethical standards in supply chains. Providers are forming strategic alliances with technology companies to offer comprehensive digital solutions that address complex procurement challenges. The market sees frequent mergers and acquisitions as firms seek to expand their capabilities and geographic reach. Customer retention relies heavily on the quality of service delivery and the ability to adapt to changing business needs. Price sensitivity remains a factor, particularly among small and medium-sized enterprises, but value-based pricing models are gaining traction. The dynamic nature of global supply chains requires continuous innovation and flexibility, driving competitors to constantly evolve their offerings to maintain a competitive edge in this rapidly changing landscape.

KEY MARKET PLAYERS

The leading companies operating in the Europe procurement outsourcing market include:

- Infosys Limited

- TATA Consultancy Services Ltd.

- HCL Technologies Ltd.

- WNS (Holdings) Ltd.

- NB Ventures, Inc. (Global eProcure)

- Wipro Limited

- IBM Corporation

- Accenture PLC

- Genpact Limited

- Capgemini SE

TOP PLAYERS IN THE MARKET

- Accenture plc is a global professional services company that plays a pivotal role in the Europe procurement outsourcing market by offering end-to-end supply chain and procurement solutions. The company contributes significantly to the global market through its extensive network of delivery centers and advanced digital capabilities. Accenture has recently strengthened its position by integrating artificial intelligence and automation into its procurement services, enabling clients to achieve greater efficiency and cost savings. The firm focuses on sustainable sourcing practices, helping European organizations meet stringent environmental regulations. By leveraging its myNav platform, Accenture provides cloud-based procurement transformations that enhance visibility and agility. Its strategic partnerships with leading technology providers further expand its service offerings. Accenture continues to invest in talent development and innovation, ensuring it remains at the forefront of procurement transformation. This holistic approach allows the company to deliver measurable value to clients across various industries in Europe.

- Genpact Limited is a leading provider of business process management and procurement outsourcing services with a strong presence in Europe. The company contributes to the global market by combining deep industry knowledge with digital technologies to optimize procurement functions. Genpact has recently enhanced its market position by expanding its Lean Digital approach, which integrates process excellence with advanced analytics and machine learning. The firm offers specialized services in strategic sourcing, supplier management, and procure-to-pay processes. Genpact actively collaborates with technology partners to deploy intelligent automation solutions that reduce manual effort and improve accuracy. Its focus on data-driven insights enables clients to make informed sourcing decisions and mitigate supply chain risks. The company also emphasizes sustainability and ethical sourcing, aligning with European regulatory requirements. Genpact continues to innovate its service portfolio and deliver operational excellence. This strategy strengthens its reputation as a trusted partner for procurement transformation in the European market.

- IBM Corporation is a key player in the Europe procurement outsourcing market, leveraging its expertise in technology and consulting to transform procurement operations. The company contributes to the global market through its Watson AI platform and blockchain solutions that enhance transparency and efficiency in supply chains. IBM has recently strengthened its position by focusing on hybrid cloud environments and AI-driven procurement analytics. These technologies enable real-time visibility into spend data and supplier performance, allowing clients to optimize costs and manage risks effectively. IBM’s consulting services help organizations redesign their procurement processes for greater agility and resilience. The company also prioritizes sustainability, offering tools to track and reduce carbon footprints across supply networks. By integrating advanced technologies with strategic consulting, IBM delivers comprehensive procurement solutions that address complex business challenges. Its commitment to innovation and client success solidifies its leadership in the European procurement outsourcing landscape.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe procurement outsourcing market predominantly employ strategies focused on digital transformation and automation to enhance operational efficiency. Companies are increasingly integrating artificial intelligence and machine learning into their service offerings to provide predictive analytics and intelligent sourcing recommendations. Strategic partnerships with technology vendors enable the deployment of advanced cloud-based platforms that offer real-time visibility and collaboration. Providers are also emphasizing sustainability and ethical sourcing to help clients comply with stringent European regulations. Expansion of specialized industry verticals allows firms to offer tailored solutions that address unique sector challenges. Continuous investment in talent development ensures the availability of skilled professionals capable of managing complex procurement processes. Service differentiation through value-added insights and strategic consulting helps retain clients and drive long-term engagements. These strategies collectively aim to deliver superior value, reduce costs, and mitigate risks for organizations navigating the evolving procurement landscape.

MARKET SEGMENTATION

This research report on the Europe procurement outsourcing market has been segmented and sub-segmented into the following categories.

By Component

- Services

- Solutions

By Deployment

- Cloud

- On-Premise

By Industry Vertical

- BFSI

- IT & Telecommunication

- Healthcare

By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe procurement outsourcing market?

The Europe procurement outsourcing market covers services where companies delegate purchasing, supplier selection, and contract management to external experts for cost savings and efficiency.

How does the Europe procurement outsourcing market function?

The Europe procurement outsourcing market works through providers handling sourcing, negotiations, compliance checks, and analytics while clients focus on core business activities.

What drives growth in the Europe procurement outsourcing market?

The Europe procurement outsourcing market grows due to digital transformation, cost pressures, regulatory compliance, and demand for specialized procurement expertise across industries.

Which countries lead the Europe procurement outsourcing market?

The Europe procurement outsourcing market is led by Germany, the UK, France, and Italy, where manufacturing, finance, and public sectors actively outsource procurement functions.

What services define the Europe procurement outsourcing market?

The Europe procurement outsourcing market includes strategic sourcing, supplier management, category expertise, contract negotiation, spend analytics, and compliance support.

What industries shape the Europe procurement outsourcing market?

The Europe procurement outsourcing market serves manufacturing, BFSI, healthcare, IT, telecom, retail, and public sector organizations seeking procurement optimization.

How does regulation influence the Europe procurement outsourcing market?

The Europe procurement outsourcing market is shaped by GDPR, ESG rules, public tender laws, and supply chain transparency requirements that demand compliant outsourcing partners.

What trends affect the Europe procurement outsourcing market?

The Europe procurement outsourcing market sees growth in digital platforms, AI analytics, sustainable sourcing, and end-to-end source-to-pay outsourcing models.

What challenges face the Europe procurement outsourcing market?

The Europe procurement outsourcing market faces data security concerns, cultural alignment issues, complex integrations, and balancing cost savings with strategic value.

How does digital transformation impact the Europe procurement outsourcing market?

The Europe procurement outsourcing market benefits from digital tools like e-procurement platforms, AI spend analysis, and automated workflows that improve efficiency.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com