Europe Smart Water Management Market Size, Share, Trends, and Growth Analysis Report, Segmented by Component, End User, and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

$5.84 BnMarket Estimate, 2026

$6.40 BnMarket Forecast, 2034

$13.27 BnCAGR, 2026–2034

9.55%Europe Smart Water Management Market Report Summary

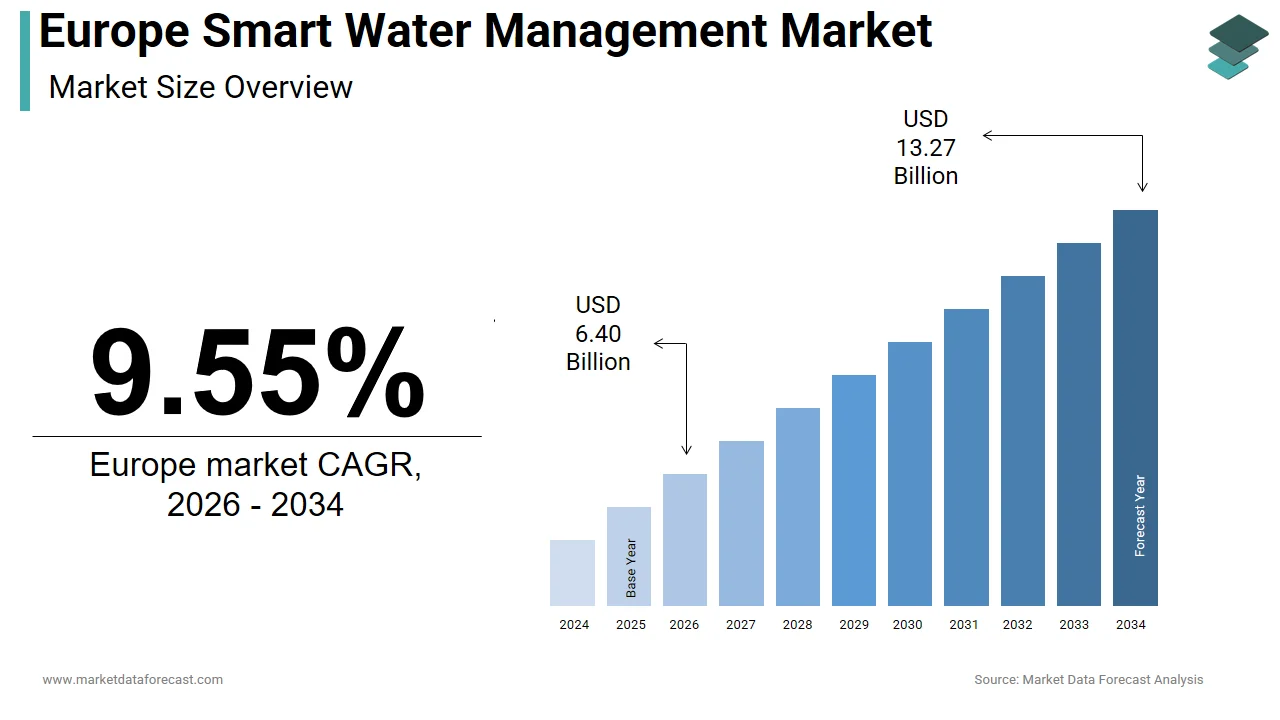

The Europe smart water management market was valued at USD 5.84 billion in 2025, is estimated to reach USD 6.40 billion in 2026, and is projected to reach USD 13.27 billion by 2034, growing at a CAGR of 9.55% from 2026 to 2034. Market growth is driven by increasing water scarcity concerns, aging water infrastructure, and the need for efficient water resource management. The adoption of digital technologies such as IoT, AI, and advanced analytics is enabling utilities to optimize water distribution, reduce leakage, and improve operational efficiency. Additionally, stringent environmental regulations and government initiatives focused on sustainability are accelerating the deployment of smart water solutions across Europe.

Key Market Trends

- Rising adoption of IoT and AI in water management systems.

- Increasing focus on reducing water loss and leakage.

- Growing investments in smart infrastructure and digital utilities.

- Stringent environmental regulations and sustainability goals.

- Expansion of data-driven water management solutions.

Segmental Insights

- Based on component, the solutions segment dominated the Europe smart water management market by capturing 45.1% share in 2025, driven by demand for advanced analytics and monitoring platforms.

- Based on end user, the commercial and industrial segment led the market with 55.2% share in 2025, supported by high water usage and efficiency requirements.

Regional Insights

The Europe smart water management market is witnessing strong growth across major economies.

- Germany led the market in 2025 with 18.3% share, driven by advanced infrastructure and strong industrial demand.

- France followed with 14.4% share, supported by government initiatives and sustainability programs.

- The United Kingdom maintains a significant presence due to ongoing investments in smart utilities and infrastructure modernization.

Competitive Landscape

The Europe smart water management market is highly competitive, with companies focusing on digital innovation, strategic partnerships, and expanding service offerings. Integration of smart sensors, cloud platforms, and analytics tools is a key strategy among market players.

Prominent companies operating in the Europe smart water management market include IBM Corporation, Oracle Corporation, Schneider Electric SE, Veolia Environnement, Xylem, Inc. (Sensus), Siemens AG, Suez Group, ABB Group, Itron, Inc., Landis+Gyr Group AG, Honeywell International, Inc., and Badger Meter, Inc.

Europe Smart Water Management Market Size

The Europe smart water management market was valued at USD 5.84 billion in 2025, is estimated to reach USD 6.40 billion in 2026, and is projected to reach USD 13.27 billion by 2034, growing at a CAGR of 9.55% from 2026 to 2034.

Smart Water Management (SWM) is the use of digital technologies, such as the Internet of Things (IoT), sensors, and data analytics, to monitor, control, and optimize water resources in real-time. This technological paradigm shift is critical for modernizing aging utility networks across the continent. The urgency for such solutions is underscored by significant environmental pressures. As per the European Environment Agency (EEA), approximately 25% of all abstracted water in the European Union is lost through leaks in distribution networks, a figure that the revised Urban Waste Water Treatment Directive (UWWTD) aims to reduce through mandatory monitoring and infrastructure upgrades. This substantial loss highlights the inefficiency of traditional monitoring systems. Furthermore, climate change exacerbates water scarcity issues, with southern European countries facing severe drought conditions. According to the Joint Research Centre of the European Commission, river flow in some Mediterranean regions could decrease by up to 40 percent by the end of the century under high emission scenarios. These ecological realities necessitate a transition from reactive maintenance to predictive management. Smart water systems enable real-time data collection, allowing utilities to detect anomalies instantly. The regulatory landscape also supports this transition with the European Union pushing for stricter water quality standards and resource efficiency targets. Consequently, the adoption of smart meters and leak detection systems is becoming a strategic imperative for municipalities and private water operators aiming to ensure sustainable water security and operational resilience in the face of growing demographic and climatic challenges.

MARKET DRIVERS

Escalating Water Scarcity and Climate-Induced Stress Drive Technological Adoption

The intensifying frequency and severity of droughts across the region accelerate the growth of the Europe smart water management market. Climate models indicate a significant shift in precipitation patterns, leading to prolonged dry spells, particularly in Southern and Central Europe. As per the European Environment Agency (EEA), approximately 20% of the European territory and 30% of its population are affected by water scarcity on average each year, illustrating an intensifying trend. This statistic underscores the urgent need for efficient water utilization strategies. Traditional water management practices are increasingly inadequate to handle these volatile conditions. Smart water technologies offer precise monitoring capabilities that allow utilities to track consumption patterns and identify inefficiencies immediately. For instance, smart meters provide granular data that helps in detecting unauthorized usage and minor leaks before they escalate into major losses. The European Commission has emphasized that improving water efficiency could save up to 40 percent of the water currently used in certain sectors. This potential for conservation drives investment in digital infrastructure. Moreover, the agricultural sector, which accounts for up to 80% of total water abstraction in Southern Europe, is increasingly adopting smart irrigation and precision farming to mitigate water stress. These systems utilize soil moisture sensors and weather forecasts to deliver water only when necessary. The convergence of regulatory pressure and environmental necessity compels stakeholders to integrate intelligent systems that ensure water security amidst changing climatic realities.

Stringent Regulatory Frameworks and Infrastructure Modernization Mandates Accelerate Market Growth

The European Union’s robust regulatory environment plays a pivotal role in propelling the Europe smart water management market forward. Legislation such as the revised Urban Wastewater Treatment Directive and the Drinking Water Directive imposes strict requirements on water quality monitoring and leakage reduction. As per the European Commission, member states are required to reduce water losses in distribution networks significantly to comply with new efficiency standards. These mandates compel water utilities to upgrade their existing infrastructure with smart technologies capable of real-time monitoring and reporting. Aging pipeline networks in many European cities suffer from high Non-Revenue Water (NRW) rates, which reach an EU average of 25% and exceed 45% in certain Eastern and Mediterranean municipalities. Smart sensors and acoustic loggers enable proactive leak detection, thereby helping utilities meet regulatory compliance while reducing operational costs. Additionally, the European Green Deal aims to make Europe the first climate-neutral continent by 2050, which includes ambitious targets for resource efficiency. Water is identified as a key resource in this transition. According to the European Court of Auditors (ECA), public water supply networks in the EU face a significant investment gap, requiring an estimated €25 billion annually in infrastructure upgrades to meet long-term environmental and quality standards. The availability of funding through mechanisms like the Recovery and Resilience Facility further supports these modernization efforts. Utilities are thus incentivized to adopt digital solutions that not only ensure compliance but also enhance operational transparency and accountability in water resource management.

MARKET RESTRAINTS

High Initial Capital Expenditure and Complex Integration Processes Restrain Market Expansion

The high initial capital expenditure associated with deploying smart water management systems acts as a significant restraint for many utilities, particularly smaller municipalities, as well as for the European smart water management market. This is despite clear benefits. The cost of installing smart meter sensors, communication networks, and data analytics platforms is substantial. Sources report that the water infrastructure sector requires a massive increase in annual funding to upgrade existing networks and comply with new regional environmental mandates. For many local water authorities with limited budgets, allocating funds for digital transformation competes with other critical infrastructure repairs. The return on investment for smart water technologies, although positive in the long term, often takes several years to materialize. This delayed financial benefit discourages immediate adoption, especially in regions with tight fiscal constraints. Furthermore, integrating new digital systems with legacy infrastructure presents technical challenges. Many existing water networks rely on outdated equipment that is not compatible with modern Internet of Things devices. Retrofitting these systems requires specialized engineering expertise and custom solutions, which further inflate costs. According to a study by the International Water Association, the complexity of integrating heterogeneous data sources from various vendors can lead to interoperability issues. These technical hurdles, combined with financial barriers, create a cautious approach among decision makers. Consequently, the pace of market penetration is slower than anticipated as organizations struggle to justify the upfront costs against uncertain immediate gains.

Data Privacy Concerns and Cybersecurity Vulnerabilities Impede Trust and Adoption

The increasing reliance on digital connectivity in water management introduces serious cybersecurity risks and data privacy concerns that hinder the growth of the Europe smart water management market. Smart water systems generate vast amounts of data regarding consumption patterns, infrastructure status, and user behavior. This data, if compromised, can reveal sensitive information about household activities or critical infrastructure vulnerabilities. Regional cybersecurity authorities note that essential utility services are facing a growing volume of digital threats, leading to a heightened focus on protecting critical water infrastructure. Such threats pose a risk to public health and safety as malicious actors could potentially manipulate water quality parameters or disrupt supply. The General Data Protection Regulation in Europe imposes strict rules on data handling, requiring utilities to implement robust security measures. Compliance with these regulations adds another layer of complexity and cost to smart water projects. Many utilities lack the internal expertise to manage sophisticated cybersecurity protocols effectively. According to the European Federation of National Associations of Water Services, ensuring end-to-end security from sensor to cloud remains a major challenge. The fear of data breaches and potential liability issues makes some stakeholders hesitant to fully embrace connected technologies. Until comprehensive security frameworks are standardized and trusted, the perceived risk associated with digital water management will continue to act as a brake on widespread adoption across the continent.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Predictive Maintenance Presents Significant Opportunities

The application of artificial intelligence and machine learning algorithms in SWM creates a pathway for enhancing operational efficiency, which is likely to fuel the expansion of the Europe smart water management market. These technologies enable predictive maintenance by analyzing historical and real-time data to forecast equipment failures before they occur. Research indicates that predictive maintenance can reduce maintenance costs by 10 to 40 percent and extend the lifespan of assets by 20 to 40 percent, driving significant operational efficiency. For European water utilities facing aging infrastructure, this capability is invaluable. AI-driven systems can process data from thousands of sensors simultaneously, identifying subtle patterns that indicate impending leaks or pump failures. This proactive approach minimizes downtime and prevents costly emergency repairs. Furthermore, artificial intelligence optimizes energy consumption in water treatment and distribution processes. Pumping stations, which are major energy consumers, can be operated more efficiently by adjusting speeds based on predicted demand. According to the International Energy Agency, the water sector accounts for approximately 4 percent of global electricity use, highlighting the potential for energy savings through smart optimization. The ability to reduce both water and energy losses aligns with sustainability goals and regulatory requirements. As computational power increases and algorithms become more sophisticated, the accuracy of predictions improves. This technological advancement encourages utilities to invest in AI-enabled platforms that offer tangible economic and environmental benefits, thereby driving market expansion.

Expansion of Smart City Initiatives and Urban Digitalization Creates New Avenues for Growth

The broader trend of smart city development across the region provides a fertile ground for the growth of the European smart water management market. Municipalities are increasingly adopting holistic digital strategies to improve urban living standards and resource efficiency. Water management is a core component of these initiatives as it intersects with energy waste and public health. European statistical authorities show that a vast majority of the population resides in cities, towns, and suburbs, highlighting the essential need for sophisticated resource management in these densely populated regions. Smart city frameworks facilitate the integration of water data with other urban systems such as traffic and energy grids. This interconnectedness allows for more coordinated responses to emergencies and better overall resource allocation. For example, during heavy rainfall events, smart water systems can communicate with stormwater management infrastructure to prevent flooding. The European Innovation Partnership on Smart Cities and Communities supports such integrated approaches by fostering collaboration between technology providers and city planners. Funding programs under the Horizon Europe framework further encourage pilot projects that demonstrate the value of integrated smart water solutions. These initiatives lower the barrier to entry for new technologies by providing testbeds and financial support. As more cities commit to digital transformation, the demand for scalable and interoperable smart water solutions will rise. This urban digitalization trend thus creates a sustained pipeline of opportunities for market players to innovate and deploy advanced water management technologies.

MARKET CHALLENGES

Interoperability Issues Among Heterogeneous Technology Providers Pose Implementation Challenges

The lack of standardization and interoperability among diverse technology providers is a major limiting factor for the expansion of the Europe smart water management market. The market comprises numerous vendors offering proprietary sensors, communication protocols, and software platforms. As per the Open Geospatial Consortium, the absence of universal standards leads to siloed data systems that cannot easily exchange information. This fragmentation complicates the creation of unified dashboards for comprehensive water network monitoring. Utilities often find themselves locked into specific vendor ecosystems, which limit flexibility and increase long-term costs. Integrating devices from different manufacturers requires custom middleware and extensive testing, which delays project timelines. According to the International Organization for Standardization, efforts to establish common data models for smart water are ongoing, but adoption remains uneven. The rapid pace of technological innovation further exacerbates this issue as new devices enter the market with incompatible features. This lack of harmony hinders the scalability of smart water solutions. Large-scale deployments require seamless integration of thousands of devices, yet current technical barriers prevent smooth operation. Utilities hesitate to invest in solutions that may become obsolete or incompatible with future upgrades. Until industry-wide standards are widely adopted and enforced, the challenge of interoperability will persist. This technical fragmentation undermines the potential benefits of smart water management by creating inefficiencies and increasing the complexity of system architecture.

Shortage of Skilled Workforce and Technical Expertise Hinders Effective Deployment

The successful implementation and operation of SWM systems require a workforce with specialized skills in data science, cybersecurity, and Internet of Things technologies, which holds back the growth of the European Smart Water Management market. However, there is a significant shortage of such professionals within the traditional water utility sector. Studies found that the industry's need for advanced technical expertise is growing faster than the current workforce can be trained or recruited. Many existing employees lack the training needed to manage complex digital infrastructures, analyze big data, or respond to cyber threats. This skills gap leads to suboptimal utilization of smart technologies and increased reliance on external consultants, which raises operational costs. Training programs are often insufficient to bridge this divide quickly enough to meet market demands. According to the European Water Association, the transition to digital water management requires a cultural shift within organizations that is difficult to achieve without adequate human capital. Utilities struggle to attract tech talent due to competition from the broader technology sector, which offers higher salaries and more dynamic work environments. This recruitment challenge slows down the adoption rate of advanced solutions. Without a competent workforce to interpret data and maintain systems, the promised efficiencies of smart water management remain unrealized. Addressing this human resource deficit is crucial for the market to reach its full potential. Until educational institutions and industry bodies collaborate to develop targeted training initiatives, the shortage of skilled professionals will remain a persistent obstacle.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Component, End User, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | IBM Corporation, Oracle Corporation, Schneider Electric SE, Veolia Environnement, Xylem, Inc. (Sensus), Siemens AG, Suez Group, ABB Group, Itron, Inc., Landis+Gyr Group AG, Honeywell International, Inc., Badger Meter, Inc., and Others. |

SEGMENTAL ANALYSIS

By Component Insights

The solutions segment dominated the Europe smart water management market and accounted for a 45.1% share in 2025. This dominance of the segment is driven by the critical need for advanced software platforms that can process vast amounts of data generated by sensors and meters. The main accelerator for the solutions segment is the increasing deployment of sophisticated analytics platforms that enable real-time monitoring and decision-making. Water utilities are transitioning from manual data collection to automated systems that provide instant insights into network performance. These software solutions integrate data from various sources, including supervisory control and data acquisition systems and geographic information systems, to create a comprehensive view of the water network. The ability to predict demand patterns and optimize distribution schedules significantly enhances operational efficiency. This financial benefit, coupled with regulatory pressures to improve service quality, drives the adoption of solution-based technologies. Furthermore, the complexity of modern water networks requires robust software capable of handling large datasets and providing actionable insights. The shift towards cloud-based platforms also facilitates easier access and scalability for utilities of all sizes. Consequently, the demand for integrated software solutions continues to outpace hardware components as organizations prioritize data-driven management strategies to ensure sustainable water resource utilization. Stringent regulatory frameworks across Europe mandate detailed reporting on water quality consumption and leakage rates, which significantly boosts the demand for management solutions. The European Union Drinking Water Directive requires member states to monitor and report various parameters regularly, necessitating efficient data management systems. Manual processes are prone to errors and cannot meet the frequency and accuracy standards imposed by regulators. Smart water management solutions offer automated compliance features that reduce the administrative burden on utilities. These systems ensure transparency and accountability, which are key requirements under current legislation. Additionally, the Urban Wastewater Treatment Directive imposes strict limits on pollutant discharge, requiring continuous monitoring of treatment plant outputs. Software solutions enable real-time tracking of these parameters, allowing operators to take corrective actions immediately. The ability to demonstrate compliance through auditable digital records is a significant advantage for utilities facing potential fines for non-compliance. Thus, regulatory pressure acts as a powerful catalyst for the adoption of comprehensive software solutions in the smart water management sector.

The services segment is predicted to witness the highest CAGR of 12.5% over the forecast period. This quick surge of the segment is supported by the increasing complexity of smart water systems, which require specialized expertise for installation, maintenance, and optimization. The complexity of integrating smart water technologies with legacy infrastructure drives the demand for professional installation and integration services. Many European water utilities operate aging networks that are not inherently compatible with modern Internet of Things devices. Professional service providers offer the technical expertise needed to configure sensor communication gateways and central management platforms. Therefore, utilities are increasingly outsourcing these tasks to experienced vendors who can guarantee proper setup and functionality. The rise of heterogeneous technology ecosystems further complicates integration efforts, requiring customized solutions for each project. Service providers play a crucial role in bridging the gap between different vendors and ensuring interoperability. Additionally, the need for regular calibration and maintenance of sensors to maintain accuracy contributes to the growth of the services segment. As the number of deployed devices increases, the volume of required maintenance services also rises. This trend is expected to continue as utilities expand their smart water initiatives and seek reliable partners to manage the technical aspects of their digital transformation journeys. The rising threat of cyberattacks and the need for continuous system monitoring are fueling the growth of managed services in the smart water market. Water utilities often lack the internal resources to manage cybersecurity risks and perform round-the-clock monitoring of their digital infrastructure. Managed service providers offer comprehensive solutions, including threat detection, incident response, and regular security audits. These services also include remote monitoring of network performance, enabling proactive identification and resolution of issues. The shift towards cloud-based platforms further increases the reliance on managed services for data storage and processing. Utilities benefit from the scalability and flexibility offered by these services, which allow them to adjust resources based on demand. Moreover, managed services provide regular software updates and patches, ensuring that systems remain secure and efficient. As the sophistication of cyber threats evolves, the demand for professional managed services will continue to grow, driving the expansion of this segment in the Europe smart water management market.

By End User Insights

The commercial and industrial segment led the Europe smart water management market and captured a 55.2% share in 2025. This leading position of the segment is attributed to the high water consumption levels in these sectors and the strong economic incentive to reduce operational costs through efficiency improvements. Industrial facilities such as manufacturing plants, power generation stations, and food processing units are major consumers of water, making efficiency a top priority. High water usage translates into high operational costs, which motivates companies to invest in smart water management technologies. Smart meters and leak detection systems enable industries to monitor consumption in real time and identify areas for improvement. According to sources, improving water efficiency in industrial processes can reduce energy consumption since water and energy use are closely linked. This dual benefit of saving both water and energy provides a compelling business case for adoption. Furthermore, many industries face strict environmental regulations regarding wastewater discharge and resource usage. Smart water systems help companies comply with these regulations by providing accurate data on water usage and quality. The return on investment for smart water technologies in the industrial sector is often faster than in other segments due to the large volumes of water involved. Consequently, industries are leading the adoption of advanced water management solutions to enhance sustainability and competitiveness. The growing emphasis on corporate sustainability and environmental, social, and governance reporting is a key driver for smart water adoption in the commercial and industrial sector. Companies are under increasing pressure from investors, customers, and regulators to demonstrate their commitment to environmental stewardship. As per research, water management is a critical component of sustainability reports for many industries. Smart water management systems provide the accurate and verifiable data needed for these reports. The transparency helps businesses build trust with stakeholders and enhance their brand reputation. Moreover, achieving sustainability targets often requires significant reductions in water footprint, which can only be achieved through precise monitoring and control. Smart technologies enable companies to set baseline metrics, track progress, and identify opportunities for conservation. The alignment of smart water initiatives with broader corporate sustainability goals drives investment in these technologies. Additionally, green building certifications such as LEED and BREEAM encourage the use of smart water systems in commercial buildings. These factors collectively contribute to the dominance of the commercial and industrial segment in the smart water management market.

The residential segment is anticipated to witness the fastest CAGR of 11.8% from 2026 to 2034. This accelerated growth of the segment is fueled by rising consumer awareness about water conservation and the widespread rollout of smart metering infrastructure by utilities. Increasing awareness among homeowners about water conservation and the benefits of smart home technology is driving the adoption of smart water devices in the residential sector. Consumers are becoming more conscious of their environmental footprint and are seeking ways to reduce water waste. Smart water meters and leak detectors allow residents to monitor their usage in real time via mobile applications, empowering them to make informed decisions. This potential for savings appeals to cost-conscious consumers, especially in regions with high water tariffs. Furthermore, the integration of smart water devices with broader smart home ecosystems enhances their appeal. Users can control irrigation systems and detect leaks remotely, adding convenience and security to their homes. The availability of user-friendly interfaces and affordable devices has lowered the barrier to entry for residential users. As smart home adoption continues to rise, the demand for connected water management solutions in households will increase significantly. This trend is supported by government initiatives promoting smart metering and water efficiency at the consumer level. Government mandates and utility-led initiatives to install smart meters in residential areas are a major catalyst for growth in this segment. Several European countries have implemented policies requiring the replacement of traditional water meters with smart counterparts to improve billing accuracy and reduce non-revenue water. As per studies, millions of smart water meters are being installed across Europe each year. For instance, Italy has one of the highest penetration rates of smart water meters globally, driven by regulatory requirements. These initiatives are often funded by utilities or government subsidies, making the technology accessible to residents. Smart meters enable dynamic pricing models, which incentivize consumers to shift usage to off-peak hours. This flexibility helps balance demand and reduces strain on the water network. Additionally, the data collected from residential smart meters provides valuable insights for utilities to plan infrastructure upgrades and detect leaks in the distribution network. The combination of regulatory support and technological advancement ensures steady growth in the residential segment of the smart water management market.

COUNTRY LEVEL ANALYSIS

Germany Smart Water Management Market Analysis

Germany outperformed other countries in the Europe smart water management market and secured a 18.3% share in 2025. Its strong industrial base and stringent environmental regulations drive the adoption of advanced water management technologies. Germany is known for its engineering excellence and commitment to sustainability, which fosters innovation in the water sector. The German government has implemented strict laws regarding water quality and resource efficiency, prompting industries and municipalities to invest in smart solutions. As per the Federal Environment Agency of Germany, water scarcity is becoming a growing concern in certain regions due to climate change. This has led to increased investment in leak detection and monitoring systems. The country’s robust infrastructure supports the deployment of Internet of Things devices and data analytics platforms. According to the German Water Partnership, the digitalization of the water sector is a key priority for future development. Major cities like Berlin and Munich are implementing smart water projects to improve efficiency and reduce losses. The presence of leading technology providers and research institutions further strengthens Germany’s market position. Collaborative efforts between the public and private sectors accelerate the adoption of innovative solutions. Germany’s focus on Industry 4.0 principles extends to the water sector, promoting the integration of digital technologies. This comprehensive approach ensures that Germany remains at the forefront of the European smart water management landscape.

France Smart Water Management Market Analysis

France was the second-largest player in the Europe smart water management market and occupied a share of 14.4% in 2025. Factors such as its extensive water infrastructure and proactive government policies support the growth of smart water technologies. France faces challenges related to aging pipelines and water scarcity in southern regions, which necessitate modernization efforts. The French government has launched initiatives to improve water efficiency and reduce leaks in distribution networks. As per the French Ministry of Ecological Transition, non-revenue water rates in some areas exceed 20 percent, prompting investments in smart metering and leak detection. Major utilities such as Veolia and Suez are leading the adoption of digital solutions to optimize operations. According to the French Water Partnership, the integration of digital technologies is essential for achieving sustainable water management goals. Smart water projects are being implemented in major cities like Paris and Lyon to enhance service quality. The country’s strong regulatory framework encourages innovation and investment in the water sector. France is also a hub for research and development in water technologies, fostering collaboration between academia and industry. The emphasis on circular economy principles drives the adoption of solutions that promote water reuse and efficiency. These factors contribute to France’s significant share in the regional market.

United Kingdom Smart Water Management Market Analysis

The United Kingdom maintains a noteworthy presence in the Europe smart water management market. The country’s aging water infrastructure and regulatory pressure from Ofwat propel the adoption of smart technologies. Water companies in the UK are required to reduce leakage rates significantly as part of their business plans. As per Ofwat, the water regulator for England and Wales, companies must reduce leakage. This target has accelerated the deployment of smart meters and acoustic leak detection systems. The UK government supports these initiatives through funding and policy incentives. Smart water technologies help companies meet regulatory requirements while improving customer service. The country’s advanced telecommunications infrastructure facilitates the connectivity of smart devices. Major water companies such as Thames Water and Severn Trent are investing heavily in digital transformation. The focus on resilience and sustainability drives the adoption of predictive maintenance and data analytics. The UK’s commitment to net zero emissions also influences water management strategies, promoting energy-efficient solutions. These dynamics ensure the UK remains a key player in the European smart water management market.

Italy Smart Water Management Market Analysis

Italy witnessed a consistent growth in the Europe smart water management market. It has one of the highest penetration rates of smart water meters in Europe, driven by regulatory mandates and high leakage rates. Italy faces significant challenges with water infrastructure, resulting in substantial non-revenue water losses. As per the Italian National Institute of Statistics, leakage rates in some regions exceed 40 percent, highlighting the urgent need for intervention. The Italian Regulatory Authority for Energy Networks and Environment has mandated the installation of smart meters to improve billing accuracy and reduce losses. According to Utilitalia, the association of public utility services' smart metering is a key strategy for modernizing the water sector. Major cities like Milan and Rome are implementing advanced water management systems to enhance efficiency. The country’s focus on digital innovation supports the adoption of the Internet of Things and data analytics. Italian companies are developing innovative solutions for leak detection and network monitoring. The government provides incentives for utilities to invest in smart technologies. These efforts contribute to Italy’s strong presence in the regional market. The combination of regulatory pressure and technological advancement drives continuous growth in the sector.

Spain Smart Water Management Market Analysis

Spain is predicted to expand significantly in the Europe smart water management market between 2026 and 2034. Its frequent droughts and water scarcity issues fuel the adoption of SWM solutions. Spain is one of the most water-stressed countries in Europe, making efficiency a national priority. As per the Spanish Ministry for Ecological Transition, climate change is expected to exacerbate water scarcity, affecting agriculture and urban supply. Smart irrigation systems and leak detection technologies are widely used to conserve water. According to the Spanish Association of Water Supply and Sanitation, the deployment of smart meters is increasing rapidly in major cities. Barcelona and Madrid are leading examples of smart water implementation with advanced monitoring systems. The government supports these initiatives through funding and policy frameworks. Spanish companies are innovating in the field of water technology, exporting solutions globally. The focus on sustainable agriculture drives the adoption of precision irrigation systems. These factors ensure Spain’s significant role in the European smart water management market. The urgency of water conservation continues to propel investment in digital solutions.

COMPETITIVE LANDSCAPE

The competition in the Europe smart water management market is characterized by a dynamic mix of established multinational corporations and agile specialized technology providers. Leading players compete intensely based on technological innovation, service quality, and strategic partnerships. The market exhibits a moderate level of consolidation as major companies acquire smaller firms to enhance their digital offerings and expand their geographic presence. Differentiation is achieved through the development of proprietary software platforms that offer advanced analytics and predictive maintenance capabilities. Price competition remains relevant but is often secondary to the value provided by integrated solutions that ensure regulatory compliance and operational efficiency. New entrants face significant barriers due to the high capital requirements and technical complexity of deploying smart water infrastructure. However, niche players continue to emerge with focused solutions for specific challenges, such as leak detection or water quality monitoring. Collaborative ecosystems are becoming increasingly important as stakeholders recognize the benefits of interoperable systems. This competitive landscape drives continuous improvement and innovation, ensuring that utilities have access to cutting-edge technologies for sustainable water management.

KEY MARKET PLAYERS

The leading companies operating in the Europe smart water management market include:

- IBM Corporation

- Oracle Corporation

- Schneider Electric SE

- Veolia Environnement

- Xylem, Inc. (Sensus)

- Siemens AG

- Suez Group

- ABB Group

- Itron, Inc.

- Landis+Gyr Group AG

- Honeywell International, Inc.

- Badger Meter, Inc.

TOP PLAYERS IN THE MARKET

- Xylem Inc stands as a pivotal force in the Europe smart water management sector by leveraging its extensive portfolio of digital solutions and hardware. The company actively contributes to the global market through its innovative Xylem Vue platform, which integrates data analytics with operational technology. Recent actions include the expansion of its smart metering capabilities across major European cities to enhance leak detection accuracy. Xylem focuses on strategic partnerships with local utilities to deploy advanced sensor networks that optimize water distribution efficiency. Their commitment to sustainability drives continuous investment in research and development for energy-efficient pumping systems. By integrating artificial intelligence into its monitoring tools, Xylem enables predictive maintenance that reduces non-revenue water significantly. This approach strengthens their position as a leader in providing holistic water infrastructure solutions that address both environmental and economic challenges faced by modern municipalities throughout the continent.

- Suez Group plays a critical role in the Europe smart water management landscape by offering comprehensive digital services tailored to urban and industrial needs. The company enhances its global footprint through the deployment of its Aquadvanced suite, which utilizes real-time data to optimize network performance. Recent initiatives involve the implementation of smart leakage control systems in several French and Spanish municipalities to combat high water loss rates. Suez prioritizes the integration of Internet of Things devices with cloud-based analytics to provide actionable insights for utility operators. Their strategy emphasizes collaborative innovation with technology partners to develop scalable solutions for complex water challenges. By focusing on circular economy principles, Suez supports clients in achieving sustainability goals while improving operational resilience. This dedicated approach ensures their continued influence in shaping the future of intelligent water management practices across European regions.

- Veolia Environnement significantly impacts the Europe smart water management market through its robust digital transformation strategies and extensive service network. The company contributes globally by deploying its Smart Water Management solutions, which combine advanced metering infrastructure with data analytics platforms. Recent efforts include the rollout of intelligent monitoring systems in key German and Italian cities to enhance resource efficiency. Veolia focuses on leveraging big data to predict consumption patterns and identify infrastructure vulnerabilities proactively. Their involvement extends to developing customized software solutions that integrate seamlessly with existing utility operations. By prioritizing customer-centric innovations, Veolia helps municipalities reduce operational costs and improve service reliability. The company’s commitment to digital excellence is evident in its continuous upgrades to telemetry and remote control systems. These actions reinforce their status as a premier provider of sustainable water management technologies that address the evolving needs of European communities.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe smart water management market primarily employ strategic partnerships and collaborations to expand their technological capabilities and market reach. Companies frequently engage in joint ventures with technology firms to integrate artificial intelligence and Internet of Things solutions into their existing portfolios. Another major strategy involves mergers and acquisitions, in which established entities purchase innovative startups to gain specialized digital tools and expertise. Product innovation remains central as firms invest heavily in research and development to create advanced sensors and analytics platforms that offer superior performance. Additionally, market participants are focusing on geographic expansion by targeting emerging markets in Eastern Europe, where infrastructure modernization is gaining momentum. Service diversification is also common with companies offering comprehensive managed services, including cybersecurity and maintenance support. These strategies collectively enable key players to strengthen their competitive position and meet the evolving demands of utilities and municipalities across the region effectively.

MARKET SEGMENTATION

This research report on the Europe smart water management market has been segmented and sub-segmented into the following categories.

By Component

- Solution

- Enterprise Asset Management

- Smart Irrigation Management

- Advanced Pressure Management

- Customer Information System & Billing

- Network Management

- Analytics & Data Management

- Leak Detection

- Others

- Water Meters

- Automatic Meter Reading

- Advanced Metering Infrastructure

- Services

- Professional Services

- Managed Services

By End User

- Commercial & Industrial

- Residential

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe smart water management market?

The Europe smart water management market covers connected tools that monitor, measure, and optimize water use. It includes smart meters, sensors, software, and analytics for utilities and cities.

How does the Europe smart water management market function?

The Europe smart water management market functions through sensors, meters, cloud platforms, and analytics that collect water data, detect leaks, and support faster utility decisions.

What drives growth in the Europe smart water management market?

The Europe smart water management market grows because of water scarcity, infrastructure upgrades, sustainability targets, and rising adoption of digital utility systems.

Which countries lead the Europe smart water management market?

The Europe smart water management market is led by Germany, the UK, France, and Spain, where utilities are investing in smart meters, monitoring systems, and water efficiency tools.

What components define the Europe smart water management market?

The Europe smart water management market includes solutions, smart meters, services, software, sensors, and analytics platforms used for water management and utility optimization.

What technologies shape the Europe smart water management market?

The Europe smart water management market is shaped by IoT, AI, SCADA, advanced metering, cloud systems, and real-time monitoring that improve water control and planning.

How does smart metering impact the Europe smart water management market?

The Europe smart water management market benefits from smart metering because utilities can track use more accurately, improve billing, and reduce water loss.

What trends influence the Europe smart water management market?

The Europe smart water management market is influenced by digital water transformation, remote monitoring, automation, predictive analytics, and smart city projects.

What challenges face the Europe smart water management market?

The Europe smart water management market faces high deployment costs, legacy infrastructure, integration complexity, and the need for stronger data interoperability.

How does leak detection fit the Europe smart water management market?

The Europe smart water management market relies on leak detection tools to find water losses quickly, reduce waste, and support more efficient utility operations.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com