- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$9.56 BnMarket Estimate, 2026

$11.57 BnMarket Forecast, 2034

$53.15 BnCAGR, 2026–2034

21%Europe Supply Chain Analytics Market Report Summary

The Europe supply chain analytics market was valued at USD 9.56 billion in 2025, is estimated to reach USD 11.57 billion in 2026, and is projected to reach USD 53.15 billion by 2034, growing at a CAGR of 21% from 2026 to 2034. Market growth is driven by the increasing need for real-time supply chain visibility, rising complexity of global supply networks, and growing adoption of data-driven decision-making across industries. Supply chain analytics solutions help organizations optimize logistics, reduce operational costs, and improve demand forecasting. The rapid expansion of e-commerce, integration of AI and machine learning technologies, and increasing focus on supply chain resilience and sustainability are further accelerating market growth across Europe.

Key Market Trends

- Increasing adoption of data-driven and predictive supply chain solutions.

- Rising demand for real-time visibility and transparency in logistics operations.

- Growing integration of AI, machine learning, and advanced analytics.

- Expansion of cloud-based supply chain analytics platforms.

- Increasing focus on sustainability and resilient supply chain strategies.

Segmental Insights

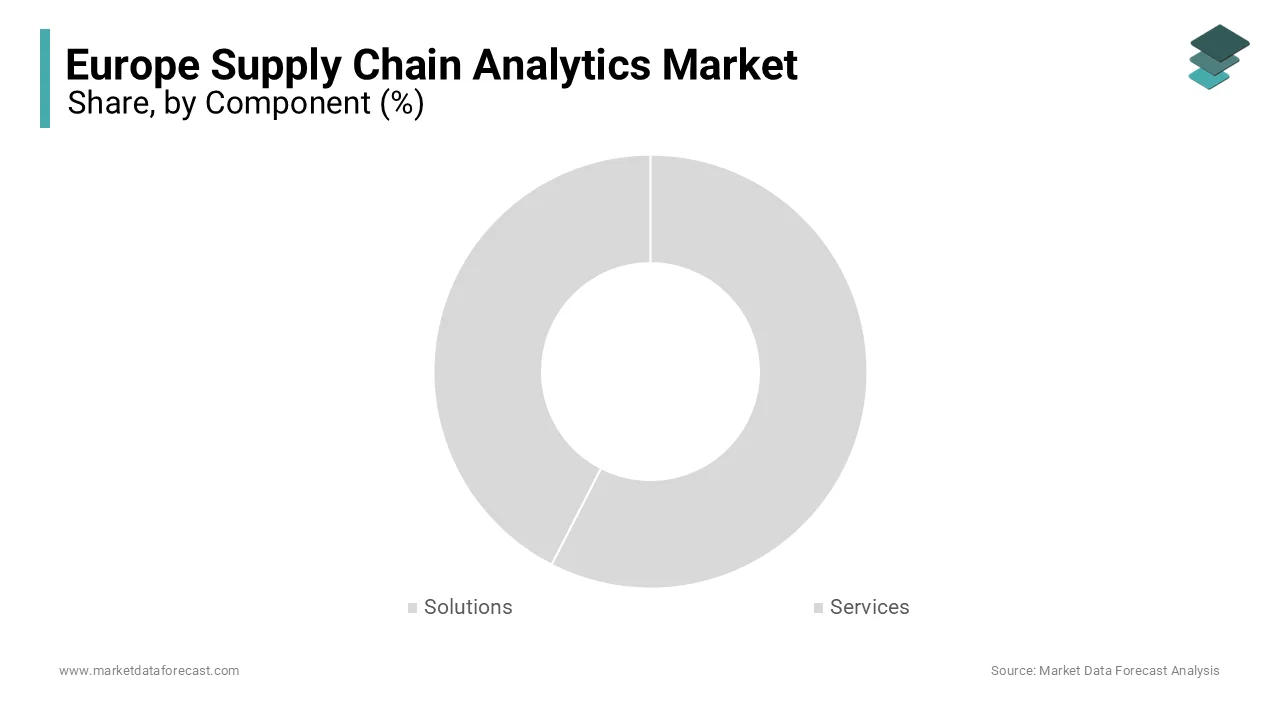

- Based on component, the solutions segment dominated the Europe supply chain analytics market by capturing 65.8% share in 2025, driven by demand for advanced analytics platforms and tools.

- Based on end use, the retail & consumer goods segment led the market with 28.7% share in 2025, supported by high demand for inventory optimization and demand forecasting.

- Based on organization size, the large enterprises segment held the majority share of 65.1% in 2025, driven by higher investment capacity and complex supply chain operations.

- Based on deployment, the cloud segment was the largest with 65.6% share in 2025, supported by scalability, flexibility, and cost efficiency.

Regional Insights

The Europe supply chain analytics market is witnessing rapid growth across major countries due to digital transformation and increasing adoption of advanced analytics solutions.

- Germany led the regional market in 2025 with 28.8% share, supported by its strong industrial base and advanced logistics infrastructure.

- The United Kingdom followed with 22.4% share in 2025, driven by a mature retail sector and strong adoption of digital technologies.

- France holds a significant position due to its strong focus on sustainability and alignment with EU Green Deal initiatives, driving demand for environmentally responsible supply chain solutions.

Competitive Landscape

The Europe supply chain analytics market is highly competitive, with the presence of global technology providers and consulting firms. Market players are focusing on enhancing analytics capabilities, integrating AI-driven insights, and expanding cloud-based offerings. Strategic partnerships, innovation, and investments in digital transformation are shaping competitive dynamics across the region.

Prominent companies operating in the Europe supply chain analytics market include SAP SE, Oracle Corporation, IBM Corporation, SAS Institute Inc., Manhattan Associates, Inc., MicroStrategy, Inc., Lockheed Martin Corporation, Accenture PLC, Genpact Limited, and A.P. Moller - Maersk A/S.

Europe Supply Chain Analytics Market Size

The size of the Europe supply chain analytics market was worth USD 9.56 billion in 2025. The regional market is anticipated to grow at a CAGR of 21% from 2026 to 2034 and be worth USD 53.15 billion by 2034 from USD 11.57 billion in 2026.

Supply chain analytics refers to the use of advanced data-driven tools, technologies, and methodologies to analyze, optimize, and enhance supply chain operations. It encompasses predictive analytics, prescriptive analytics, descriptive analytics, and cognitive computing to provide actionable insights into demand forecasting, inventory management, logistics optimization, and supplier performance. In Europe, the supply chain analytics market has emerged as a critical enabler for businesses seeking to navigate the complexities of global trade, fluctuating consumer demands, and evolving regulatory landscapes.

The growing emphasis on digital transformation has been a key driver of this market. For instance, according to the State of the Digital Decade 2025, the European Commission targets 75% adoption of advanced technologies by 2030; currently, 55.03% of large enterprises have adopted AI technologies, while 69.24% utilize Business Intelligence software to optimize operations. Industries such as retail, manufacturing, healthcare, and automotive are leveraging these solutions to improve efficiency and reduce costs. Research, including DHL's Logistics Trend Radar, indicates that the integration of predictive analytics and AI in logistics can improve delivery efficiency and resource optimization by up to 20%.

The rise of e-commerce, coupled with disruptions caused by events like the COVID-19 pandemic, has further underscored the importance of supply chain visibility and resilience. For example, data from Eurostat reveals that 80% of EU enterprises faced global value chain constraints between 2021 and 2023, leading 32% of firms to prioritize increased digitalization as a core strategy for building future resilience. As sustainability becomes a priority, supply chain analytics is also aiding organizations in achieving their environmental goals by optimizing resource utilization and reducing carbon footprints. This dynamic landscape positions Europe as a hub for innovation and growth in the global supply chain analytics arena.

MARKET DRIVERS

Increasing Adoption of Digital Transformation Initiatives

The rapid adoption of digital transformation across the region’s industries is a significant driver of the Europe supply chain analytics market. The European Commission’s Digital Economy and Society Index indicates that a substantial majority of large enterprises across Europe have integrated data analytics into their operations, with supply chain management serving as a key area for these technological applications. This shift is fueled by the need to enhance operational efficiency, reduce costs, and improve decision-making capabilities. For instance, regional industrial assessments demonstrate that manufacturers leveraging advanced analytics have achieved significant gains in the precision of their inventory records and notable reductions in their overall logistics expenditures. The push toward Industry 4.0, supported by government initiatives like Germany’s Industrie 4.0 strategy, further accelerates this trend. The demand for real-time insights and predictive capabilities is growing, as businesses strive to remain competitive in a rapidly evolving market.

Growing Emphasis on Supply Chain Resilience and Sustainability

The increasing focus on supply chain resilience and sustainability is also contributing to the expansion of the European supply chain analytics market. The European Environment Agency indicates that leading companies across the region are increasingly aligning their operations with environmental and social governance standards, utilizing digital tools to track carbon footprints and enhance the efficiency of their resource use. Additionally, disruptions caused by events like the COVID-19 pandemic have highlighted the importance of building resilient supply chains. Various studies confirm that a vast majority of enterprises experienced substantial operational disturbances during the recent global health crisis, which has accelerated the adoption of predictive technologies to identify and manage future supply chain vulnerabilities. Governments are also encouraging this shift through regulations like the EU Green Deal, which mandates sustainable practices. Organizations can achieve greater transparency, optimize transportation routes, and reduce waste by leveraging analytics. This approach directly aligns with regulatory requirements and consumer expectations for environmentally responsible operations.

MARKET RESTRAINTS

High Implementation Costs and Budget Constraints

The high cost of implementing supply chain analytics solutions continues to hamper the growth of the Europe supply chain analytics market. According to research from the European Investment Bank, a significant portion of small and medium-sized enterprises find that financial constraints and limited capital serve as a major obstacle to the implementation of sophisticated data technologies. The initial investment required for software, hardware, and skilled personnel can be prohibitive, particularly for smaller organizations with limited financial resources. Additionally, findings from European digital tracking initiatives show that only a small fraction of smaller enterprises have achieved a high level of technological integration, with many citing the high costs associated with deployment as a reason for their gradual adoption. While larger enterprises may have the capacity to invest, the financial burden often outweighs the perceived benefits for smaller players. This economic disparity creates a fragmented landscape, hindering the widespread adoption of supply chain analytics across all business scales.

Data Privacy and Security Concerns

Data privacy and security concerns further limit the expansion of the European supply chain analytics market. The General Data Protection Regulation (GDPR), enforced by the European Data Protection Board, imposes strict rules on data collection, storage, and processing, which can complicate analytics implementation. The European Union Agency for Cybersecurity indicates that a substantial number of organizations view the complexities of data protection regulations as a major consideration when implementing new data-driven solutions. Furthermore, the European Union Agency for Cybersecurity has observed a sharp rise in the frequency of digital threats directed at supply chain infrastructures, highlighting a growing risk to the integrity of shared organizational data. These risks deter organizations from fully leveraging analytics tools, as breaches could lead to reputational damage and hefty fines. Balancing innovation with regulatory compliance remains a persistent challenge, limiting the seamless integration of analytics into supply chain operations.

MARKET OPPORTUNITIES

Expansion of AI and Machine Learning Integration

Artificial intelligence (AI) and machine learning (ML) are being integrated into supply chain analytics. This integration creates many possibilities for the expansion of the European supply chain analytics market. The European Commission’s Digital Economy and Society Index reflects that a growing proportion of enterprises across the region are investigating artificial intelligence to refine their decision-making processes and boost overall operational productivity. AI and ML enable predictive analytics, demand forecasting, and real-time supply chain visibility, which can reduce costs and improve agility. For instance, regional industrial assessments demonstrate that manufacturers adopting artificial intelligence for their analytics have achieved significant improvements in maintaining optimal stock levels and enhancing the reliability of their delivery schedules. Furthermore, the EU’s Horizon Europe program has committed substantial financial resources toward research and innovation in artificial intelligence, aiming to accelerate the development and adoption of these technologies across the continent. As businesses increasingly prioritize data-driven strategies, the incorporation of AI and ML is expected to unlock unprecedented growth potential in the supply chain analytics sector.

Rising Demand for Sustainable Supply Chain Solutions

The growing emphasis on sustainability offers a major opportunity for the European supply chain analytics market. The European Environment Agency indicates that an increasing number of companies are restructuring their operations to meet the climate targets established by regional environmental policies, which require significant reductions in carbon emissions by the end of the decade. Supply chain analytics plays a pivotal role in achieving these goals by optimizing transportation routes, reducing energy consumption, and minimizing waste. Research within the logistics sector highlights that many organizations utilizing advanced data tools have successfully enhanced their environmental impact, achieving measurable reductions in their overall carbon footprints through better route and resource management. Additionally, consumer demand for sustainable practices is driving businesses to adopt transparent and eco-friendly supply chains. Governments are also incentivizing green initiatives through funding programs like the EU LIFE program, further propelling the adoption of analytics to meet sustainability targets while enhancing competitiveness.

MARKET CHALLENGES

Limited Availability of Skilled Workforce

The shortage of skilled professionals proficient in this field poses a significant challenge to the European supply chain analytics market. According to the European Centre for the Development of Vocational Training, a significant portion of organizations across the region struggle to recruit professionals with the specialized data skills necessary for managing modern supply chain technologies. The complexity of integrating technologies like AI, machine learning, and big data requires specialized expertise, which is currently in short supply. The European Commission’s digital strategy documents highlight that a limited segment of the current workforce possesses high-level technical competencies, creating a significant hurdle for the broader adoption of advanced digital tools. This skills gap not only delays adoption but also increases reliance on external consultants, raising operational costs. Addressing this challenge necessitates investments in training programs and educational initiatives to equip the workforce with the competencies needed to drive innovation in supply chain analytics.

Fragmented Regulatory Landscape Across Member States

The fragmented regulatory environment across European countries impedes the expansion of the Europe supply chain analytics market. The European Data Protection Board notes that while the General Data Protection Regulation (GDPR) provides a unified framework, individual member states interpret and enforce these rules differently, creating inconsistencies. Research into regional trade logistics reveals that a majority of international supply chain movements encounter setbacks caused by the complex and differing regulatory requirements across various jurisdictions. Additionally, the complexity of adhering to multiple national regulations increases administrative burdens and operational costs for businesses operating across borders. This lack of harmonization hinders the seamless flow of data and goods, limiting the potential of analytics to optimize pan-European supply chains. Streamlining regulations could significantly enhance efficiency and foster greater collaboration within the single market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Component, End Use, Organization Size, Deployment, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Saint-Gobain Group, Ravenwindow, Ppg Industries, Inc., Kinestral Technologies, Inc., Gentex Corporation, Merck Kgaa, Pleotint, Llc, E-Chromic Technologies, Inc., Chromogenic Ab, AGC, Inc., Hitachi Chemical Co., Ltd, Nippon Sheet Glass Co., Ltd, Innovative Glass Corporation, Glasnovations Ltd., Heliotrope Technologies, Sage Electrochromics, Inc., Scienstry, Stellaris, View Inc., And Vista Window Company. |

SEGMENTAL ANALYSIS

By Component Insights

The Solutions segment led the European supply chain analytics market and captured a 65.8% share in 2025. This dominance of the segment is driven by the critical role of tools like logistics analytics in optimizing operations and reducing costs. Research indicates that a majority of service providers are increasingly adopting data-driven solutions for managing their transit routes and stock levels to keep pace with the expansion of online commerce. Solutions such as manufacturing and sales analytics enable real-time monitoring and predictive maintenance, improving efficiency. Their ability to provide actionable insights into complex supply chains makes them indispensable for industries seeking operational excellence and competitive advantage.

The Services segment is predicted to witness the highest CAGR of 15.8% from 2026 to 2034. Professional services dominate this growth. Research from the European Investment Bank suggests that a significant portion of small and medium-sized enterprises seek external specialized support to facilitate their digital transition and technological integration projects. Support and maintenance services ensure compliance with regulations like GDPR and address technical challenges, fostering trust in analytics adoption. The growing complexity of analytics solutions increases dependency on specialized services, making this segment vital for seamless implementation and scalability. Its rapid growth underscores its importance in bridging the skills gap and driving widespread adoption across Europe.

By End Use Insights

The Retail & Consumer Goods segment dominated the European supply chain analytics market and accounted for a 28.7% share in 2025. This leading position of the segment is attributed to the rapid expansion of e-commerce, with online sales growing at a substantial rate. Multiple studies emphasize that a substantial number of retail organizations are utilizing advanced analytics to refine their inventory management, effectively minimizing the risks of both supply shortages and excess stock. Retailers leverage analytics to enhance customer experiences through personalized marketing and efficient last-mile delivery. This segment plays a pivotal role in driving innovation and ensuring operational efficiency amid rising consumer expectations for speed and convenience. Therefore, it has become indispensable for modern retail ecosystems.

The Healthcare segment is estimated to register the fastest CAGR of 16.2% during the forecast period due to the increasing demand for resilient supply chains to manage medical supplies and pharmaceuticals. Healthcare logistics assessments indicate that the implementation of data analytics has notably improved the availability of critical supplies, leading to better operational flow and enhanced care for patients. The COVID-19 pandemic highlighted vulnerabilities in healthcare supply chains, prompting investments in predictive analytics for demand forecasting. This segment is critical for ensuring timely access to essential resources, maintaining cost-effectiveness, and ensuring regulatory compliance as Europe’s aging population drives healthcare spending. This crucial role positions it as a key growth driver.

By Organization Size Insights

The Large Enterprises segment held the majority share of 65.1% of the European supply chain analytics market in 2025. This supremacy of the segment is credited to its ability to invest in advanced analytics tools, enabling end-to-end supply chain visibility and operational efficiency. Large-scale organizations across Europe have reported that the integration of sophisticated analytics allows for a meaningful decrease in their day-to-day operational costs and a measurable rise in their logistics performance. Their complex, global operations necessitate robust solutions for real-time monitoring and predictive insights. Large enterprises are pioneers in digital transformation, driving innovation. Through this, they set benchmarks for smaller organizations and shape the future of supply chain analytics.

The SMEs segment is anticipated to witness the fastest CAGR of 18.3% from 2026 to 2034. This rapid expansion is propelled by affordable cloud-based analytics solutions and government initiatives supporting SME digitalization. Findings from European digital monitoring initiatives show that while adoption is growing, only a fraction of smaller enterprises currently utilize data tools to enhance their delivery schedules and refine their inventory control. Rising competition and consumer demands for faster services push SMEs to adopt analytics, enhancing their competitiveness. Small and medium-sized enterprises (SMEs) form the backbone of the European economy. Their growing adoption of analytics underscores a democratization that fosters broader economic resilience and innovation.

By Deployment Insights

The Cloud segment was the largest segment in the European supply chain analytics market and occupied a 65.6% share in 2025. This prominence of the segment is supported by the scalability, flexibility, and cost-efficiency of cloud-based solutions. Research from European financial institutions indicates that businesses moving their operations to cloud-based environments tend to see a reduction in traditional infrastructure costs while gaining greater flexibility in their operations. Cloud deployment supports real-time data access and seamless integration with emerging technologies like AI and IoT, making it ideal for industries such as retail and logistics. Demand for remote operations and predictive analytics is rising. This ensures the cloud's position as the leading deployment model due to its ability to enhance supply chain visibility.

The Cloud segment is also the fastest-growing, with a projected CAGR of 19.2% over the forecast period, due to the increasing adoption of SaaS platforms, which offer affordable and scalable solutions. European digital tracking reports show that cloud-based platforms are the preferred choice for organizations newly adopting analytics, as these systems offer lower initial investment requirements and a faster setup process. Industries like e-commerce and manufacturing leverage cloud analytics to optimize supply chains and improve decision-making. The cloud’s ability to deliver real-time insights and support dynamic operations is driving digital transformation, innovation, and efficiency in Europe. Consequently, it has become a critical tool for businesses prioritizing this shift.

COUNTRY LEVEL ANALYSIS

Germany Supply Chain Analytics Market Analysis

Germany was the top performer in the European supply chain analytics market and accounted for a 28.8% share in 2025. The growth trajectory of supply chain analytics in Germany is driven by a robust industrial base, particularly in automotive and manufacturing, where analytics optimizes complex supply chains. The Federal Ministry for Economic Affairs and Climate Action indicates that national strategic initiatives have significantly accelerated the digital transformation of the industrial sector, with a growing majority of enterprises either implementing or actively planning the integration of advanced data tools. The presence of global logistics hubs like Hamburg further enhances its capabilities in supply chain innovation. This focus on efficiency and technological advancement solidifies Germany’s position as a market leader.

United Kingdom Supply Chain Analytics Market Analysis

The United Kingdom follows closely behind in the Europe supply chain analytics market and captured a 22.4% share in 2025. This position of the UK market is propelled by its highly digitalized retail sector, which accounts for a notable share of Europe’s e-commerce transactions. The National Health Service (NHS) also leverages analytics to streamline healthcare supply chains, addressing inefficiencies like stockouts. Post-Brexit, government-backed digital transformation programs have encouraged SMEs to adopt analytics solutions. The UK has a tech-savvy population and has made strategic investments in innovation. Consequently, it remains a key contributor to the growth of supply chain analytics in Europe.

France Supply Chain Analytics Market Analysis

France holds a noteworthy share of the European market due to its commitment to sustainability, aligning with the EU Green Deal. Regional environmental assessments reflect that a substantial proportion of French organizations are prioritizing sustainable operational strategies, increasingly utilizing data-driven insights to refine their transit networks and lower their overall environmental impact. Government support for AI and digital innovation accelerates adoption across industries like luxury goods and pharmaceuticals. France plays a pivotal role in advancing sustainable and efficient supply chain solutions across Europe. It achieves this by focusing on predictive analytics and green logistics.

KEY MARKET PLAYERS

The major players in the Europe supply chain analytics market include

- SAP SE

- Oracle Corporation

- IBM Corporation

- SAS Institute Inc.

- Manhattan Associates, Inc.

- MicroStrategy, Inc.

- Lockheed Martin Corporation

- Accenture PLC

- Genpact Limited

- A.P. Moller - Maersk A/S

MARKET SEGMENTATION

This research report on the Europe supply chain analytics market is segmented and sub-segmented into the following categories.

By Component

- Solutions

- Sales & Operations Analytics

- Logistics Analytics

- Manufacturing Analytics

- Planning & Procurement

- Visualization & Reporting

- Services

- Professional Service

- Support & Maintenance

By End Use

- Manufacturing

- High Technology Products

- Retail & Consumer Goods

- Healthcare

- Transportation

- Aerospace & Defense

- Other End Use

By Organization Size

- Large Enterprises

- SMEs

By Deployment

- Cloud

- On-Premise

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe