Europe Target Drone Market Size, Share, Trends & Growth Forecast Report By Type, By Use, and By Country (Germany, United Kingdom, France, Italy, Spain, Netherlands, Poland & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Target Drone Market Report Summary

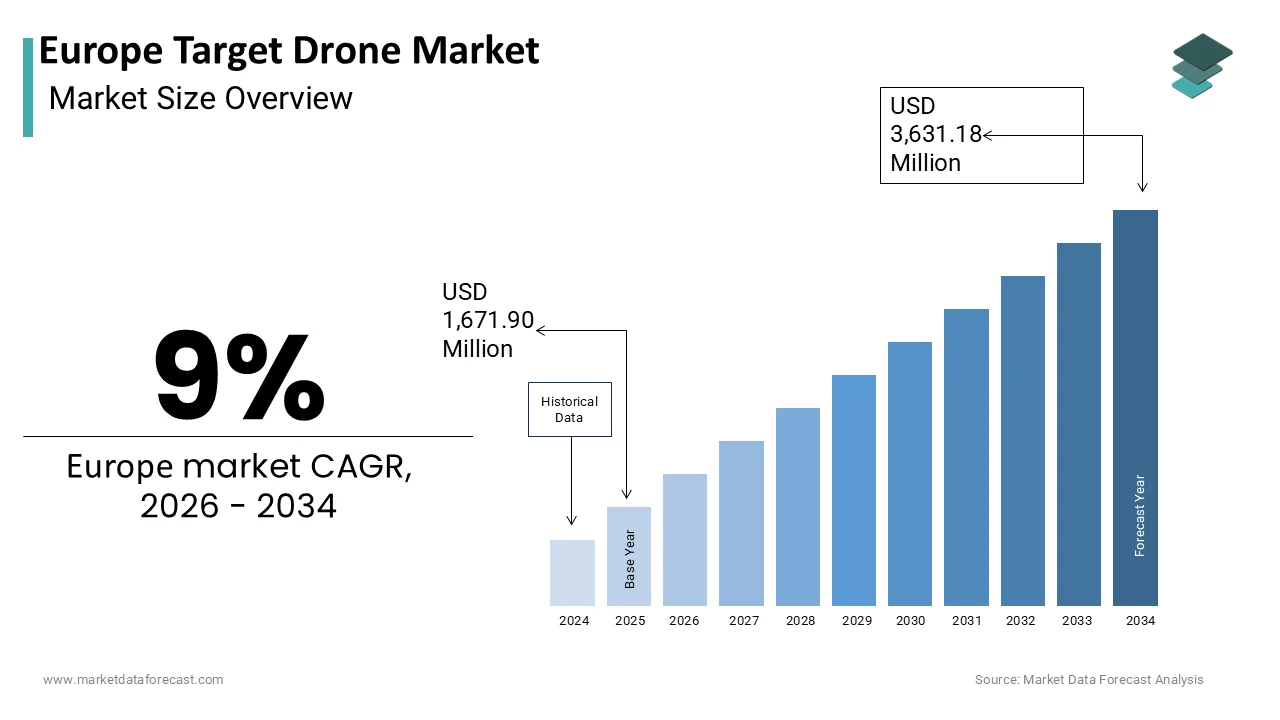

The Europe Target Drone Market was valued at USD 1,671.90 million in 2025 and is projected to reach USD 3,631.18 million by 2034, growing from USD 1,822.37 million in 2026 at a CAGR of 9.00% during the forecast period. Growth is driven by escalating geopolitical tensions demanding realistic combat training, technological advancements in AI-enabled threat simulation, and expansion of multinational training collaborations. Airspace regulatory constraints and high procurement costs are shaping market dynamics.

Key Market Trends

- Rising integration of AI-enabled autonomous swarm target drone operations

- Growing demand for supersonic fixed-wing drones simulating fifth-generation fighters

- Increasing procurement of marine target drones for littoral warfare training

- Expansion of pooled multinational target drone fleets under EU defense cooperation

- Rising cybersecurity investment to protect networked drone command and control links

Segmental Insights

- Based on type, fixed-wing dominated the market in 2025, driven by superior speed and aerodynamic fidelity in replicating modern fighter threats.

- Based on use, aerial target drones led the market in 2025, driven by essential validation needs for integrated air defense and missile interception systems.

- Rotary wing is the fastest-growing type segment, driven by rising demand for urban and counter-drone close-quarters training scenarios.

Regional Insights

- Germany, France, and the United Kingdom lead regional procurement, leveraging domestic industrial capabilities for indigenous target drone development.

- Poland and Romania are increasing target drone acquisitions to support expanded air policing missions along alliance borders.

- Marine target drones are the fastest-growing use segment, driven by naval modernization and littoral warfare training initiatives.

Competitive Landscape

The market is highly competitive, with manufacturers focusing on AI integration, modular payload systems, and cost-effective additive manufacturing. Companies are pursuing strategic partnerships and collaborative research to accelerate innovation and share development costs among allied nations.

Prominent players in the market include QinetiQ Group plc, Airbus SE, Leonardo S.p.A., Saab AB, Kratos Defense & Security Solutions Inc., Northrop Grumman Corporation, BAE Systems plc, Thales Group, Denel Dynamics, AeroTargets International LLC, Griffon Aerospace, and SCR (Sierra Nevada Corporation).

Europe Target Drone Market Size

The Europe Target Drone Market is projected to grow from USD 1,671.90 million in 2025 to USD 1,822.37 million in 2026 and reach USD 3,631.18 million by 2034, registering a CAGR of 9% during the forecast period from 2026 to 2034.

Target drones represent specialized unmanned aerial vehicles engineered specifically for military training and weapons testing applications. These systems simulate enemy aircraft or missile threats to allow armed forces to practice interception, tracking,g and engagement protocols without risking pilot lives or expensive operational assets. The European defense landscape has witnessed intensified focus on air combat readiness as geopolitical tensions reshape security priorities across the continent. According to the European Defence Agency, total defense expenditure by EU Member States reached approximately 279 billion euros in 2023, which signals robust investment in modernization programs, ms including realistic training infrastructure. As per NATO reports, the Alliance has significantly strengthened its deterrence and defence posture, with high-readiness forces growing to 500,000 troops, demonstrating sustained demand for credible threat simulation platforms. The technological evolution of target drones now incorporates advanced radar cross-section manipulation, electronic warfare capabilities, and autonomous flight patterns that closely mimic contemporary adversary tactics. Military academies and training centers across Germany, France, and the United Kingdom have integrated these systems into their curricula to prepare personnel for complex multi-domain battlefields. The shift from traditional towed targets to intelligent unmanned platforms reflects a broader transformation in how European armed forces approach preparedness, ensuring that training environments replicate the sophistication of modern aerial threats while maintaining cost efficiency and operational safety standards throughout extended deployment cycles.

MARKET DRIVERS

Escalating Geopolitical Tensions Driving Realistic Combat Training Requirements

The deterioration of security architectures across Eastern Europe has compelled nations to prioritize authentic combat simulation capabilities, which is one of the major factors driving the expansion of the European target drones market. According to the Stockholm International Peace Research Institute, total military spending in Europe rose by 17% in 2024 to 693 billion dollars, reflecting heightened geopolitical tensions. This fiscal commitment directly translates into the procurement of advanced training assets, including target drones that replicate fifth-generation fighter characteristics. Modern air defense systems require validation against high-speed maneuvering targets that emulate stealth profiles and electronic countermeasures. As per data from the European Defence Fund, approximately 1.065 billion euros were allocated in 2025 specifically for collaborative research and development projects, including those focused on air combat and training technologies. The need to validate interceptor missiles, radar systems, and command-control networks against realistic threats has made target drones indispensable. Nations such as Poland, Romania, and the Baltic states have initiated programs to acquire high-performance target drones to support their expanded air defense networks. The complexity of modern warfare demands that pilots and ground operators train against adversaries possessing similar technological advantages, which conventional methods cannot provide. Consequently, defense ministries are prioritizing contracts with manufacturers capable of delivering scalable, customizable target drone fleets that can operate in contested electromagnetic environments while providing detailed post-mission analytics for performance assessment and tactical refinement.

Technological Advancements Enabling High-Fidelity Threat Simulation

Recent breakthroughs in artificial intelligence, miniaturized sensors, and composite materials have transformed target drone capabilities significantly, which is further contributing to the European target drones market growth. For instance, the integration of machine learning algorithms allows target drones to execute adaptive flight paths that respond dynamically to interceptor actions, creating more challenging training scenarios. Modern systems now achieve speeds exceeding Mach 2 while maintaining radar signatures comparable to advanced fighter aircraft, which was previously unattainable for unmanned platforms. As per technical specifications released by major defense contractors, newer target drones incorporate modular payload bays, enabling rapid configuration changes between electronic warfare simulation, decoy deployment, and kinetic threat emulation. The adoption of additive manufacturing techniques has reduced production costs significantly while improving structural durability, allowing for multiple recovery and reuse cycles. Advanced telemetry systems transmit real-time performance data to training commanders, facilitating immediate feedback and scenario adjustment during live-fire exercises. Research initiatives like Horizon Europe continue to fund projects focused on autonomous swarm technologies for target drones, enabling coordinated multi-vehicle attacks that test saturation defenses. These technological enhancements ensure that training environments remain relevant against evolving adversary tactics while extending operational lifespan and reducing lifecycle costs for military operators seeking maximum return on investment from their training infrastructure expenditures.

MARKET RESTRAINTS

Stringent Regulatory Frameworks Limiting Operational Flexibility

European airspace regulations impose significant constraints on target drone deployment, particularly in densely populated regions where military training ranges overlap with civilian aviation corridors, which is a significant impediment to the regional market growth. According to the European Union Aviation Safety Agency, navigating the complex authorization processes for specific and certified category operations remains a primary challenge, requiring coordination between national civil aviation authorities and defense ministries. The implementation of the U-space regulatory framework mandates rigorous risk assessments, geo-fencing capabilities, and detect-and-avoid systems, which increase development costs and extend certification timelines. As per reports from Eurocontrol, the integration of unmanned systems into non-segregated airspace requires ongoing coordination to avoid disruptions to civil traffic, creating bureaucratic hurdles that can limit training frequency and scope. Noise pollution restrictions further constrain operations, with several member states enforcing strict decibel limits that prohibit high-speed, low-altitude flights near residential areas. The fragmented nature of national regulations across member states creates additional compliance burdens for manufacturers who must navigate differing certification requirements, export controls, and operational permits. This regulatory complexity discourages smaller innovators from entering the market and forces established defense contractors to allocate substantial resources toward legal compliance rather than technological advancement. The resulting operational limitations reduce the realism of training exercises as forces cannot always replicate certain threat scenarios within approved parameters, ultimately compromising preparedness levels despite increased defense budgets.

High Development and Procurement Costs Constraining Market Accessibility

The sophisticated nature of modern target drones results in substantial financial barriers that limit procurement volumes, especially for smaller European nations with constrained defense budgets, which is further impeding the expansion of the European target drones market. According to defense procurement data, the unit cost for a high-performance target drone capable of supersonic flight and electronic warfare simulation can range from 2 million to 5 million euros, excluding maintenance and operational expenses. As per budgetary reports from the European Defence Agency, member states have significantly increased their procurement budgets to address capability gaps, though high costs remain a factor. The total cost of ownership extends beyond the initial acquisition, with annual maintenance representing a significant percentage of the purchase price due to specialized components and skilled technician requirements. Recovery failures during training exercises result in asset loss, further inflating effective costs. Budget pressures force difficult trade-offs between quantity and capability, with many nations opting for fewer high-end systems rather than larger fleets of moderate-performance alternatives. This financial constraint limits training intensity and reduces the diversity of threat scenarios that units can practice against. The concentration of manufacturing among a few specialized suppliers also reduces competitive pricing pressure, perpetuating high costs and limiting market expansion, particularly for emerging economies within Europe seeking to modernize their air defense training infrastructure amid competing fiscal priorities.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Autonomous Swarm Operations

The emergence of artificial intelligence-driven swarm technologies presents promising opportunities for target drone applications, which is enabling coordinated multi-vehicle operations that challenge next-generation defense systems. For instance, AI-enabled swarms can execute complex collaborative behaviors, including distributed sensing, adaptive formation flying, and synchronized electronic attacks that overwhelm traditional interception protocols. Major defense contractors are investing heavily in this domain, with initiatives like the European Defence Fund consistently supporting autonomous systems development. As per technical demonstrations conducted by leading aerospace firms, groups of small target drones successfully simulated saturation attacks against integrated air defense networks, revealing vulnerabilities in current detection and engagement algorithms. The scalability of swarm operations allows militaries to generate realistic mass raid scenarios at a fraction of the cost associated with deploying manned aircraft or large individual drones. Machine learning algorithms enable these swarms to learn from previous engagements, continuously improving tactical effectiveness while reducing human operator workload. The modularity of swarm systems permits mixed configurations combining different drone types with varying payloads, creating heterogeneous threat profiles that better reflect contemporary adversary capabilities. This technological trajectory aligns with NATO strategic directives, positioning AI-powered target drone swarms as critical enablers for future readiness validation across European armed forces seeking to maintain qualitative advantages in increasingly contested operational environments.

Expansion of Multinational Training Collaborations and Shared Infrastructure

Growing emphasis on interoperability among European allied forces is driving demand for standardized target drone platforms that support joint training exercises and collective capability development, which is another notable opportunity for the European target drones market. According to NATO records, multinational exercises have become a cornerstone of the Alliance’s defensive posture, with participating nations seeking common training assets to ensure seamless coordination during combined operations. The Permanent Structured Cooperation framework under the European Union has facilitated numerous collaborative projects focused on shared training infrastructure, including pooled target drone fleets that reduce individual national procurement burdens while enhancing operational compatibility. As per data from the European Defence Industrial Development Programme, member states are increasingly committing funds to develop interoperable training systems, including compatible target drones with standardized data links and communication protocols. This collaborative approach enables smaller nations to access high-fidelity training capabilities that would otherwise be financially prohibitive, while fostering deeper tactical integration among allied forces. Shared maintenance facilities and joint operator training programs further optimize resource utilization, creating sustainable ecosystems for target drone operations. The standardization of interfaces and performance specifications allows for the seamless integration of target drones from different manufacturers into unified training networks, promoting competition and innovation. This trend toward collective procurement and shared infrastructure represents a structural shift in how European nations approach defense modernization, leveraging economies of scale and collaborative expertise to maximize training effectiveness.

MARKET CHALLENGES

Cybersecurity Vulnerabilities Threatening Operational Integrity

The increasing connectivity and software dependence of modern target drones expose them to sophisticated cyber threats that could compromise training exercises or enable adversarial exploitation of sensitive military data. According to reports from the European Union Agency for Cybersecurity, incidents of attempted unauthorized access to military systems remain a top priority, with networked platforms like drones representing attractive targets due to their valuable telemetry data. As per analysis from defense cybersecurity firms, platforms lacking adequate encryption protocols for command and control links are susceptible to signal interception, spoofing, or hijacking during training missions. The integration of commercial off-the-shelf components further exacerbates vulnerabilities, as these elements often contain undocumented backdoors or unpatched software flaws. Successful cyber intrusions could allow adversaries to manipulate flight parameters, corrupt performance data, or even seize control of drones, turning them into hazards during live-fire exercises. The complexity of securing distributed networks connecting multiple drones, ground stations, and analysis systems creates numerous attack surfaces that require continuous monitoring and updating. Many European defense contractors struggle to implement comprehensive cybersecurity measures due to limited expertise and competing development priorities, leaving critical gaps in system protection. Addressing these vulnerabilities requires substantial investment in secure coding practices, hardware-based encryption, and regular penetration testing, which increases development costs and extends deployment timelines while remaining essential for maintaining operational trust.

Supply Chain Disruptions Impacting Production Timelines and Component Availability

The target drone manufacturing sector faces persistent supply chain vulnerabilities stemming from geopolitical tensions, trade restrictions, and concentrated sourcing of critical components, particularly semiconductors and advanced composite materials, which is another noteworthy challenge to the European target drones market. According to the European Commission, a significant portion of defense electronics suppliers have reported delays in receiving specialized microprocessors essential for flight control systems and sensor integration. As per data from aerospace and defense industry associations, reliance on non-European sources for rare earth elements and high-performance batteries creates strategic dependencies that expose manufacturers to export controls and political leverage from supplier nations. The consolidation of semiconductor manufacturing in certain regions means that any disruption, whether from natural disasters, diplomatic conflicts, or logistical bottlenecks, immediately impacts European production schedules, forcing costly redesigns or temporary production halts. Trade policy uncertainties further complicate procurement planning, with changing tariff structures and export license requirements adding administrative burdens and cost volatility. The specialized nature of target drone components limits alternative sourcing options, as few suppliers meet stringent military-grade quality standards, creating single points of failure within supply networks. These disruptions force manufacturers to maintain larger inventory buffers, tying up capital and increasing storage costs while still failing to guarantee timely delivery to defense customers. The resulting production delays cascade through the entire acquisition process, postponing training schedules and compromising readiness timelines for armed forces.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Use, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | Germany, United Kingdom, France, Italy, Spain, Netherlands, Poland, Rest of Europe |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Type Insights

The fixed-wing segment dominated the market with the highest share of the European market in 2025, primarily because they offer superior aerodynamic efficiency and higher speed capabilities that closely mimic modern fighter aircraft and missile threats. For instance, fixed-wing platforms account for a significant majority of all target drone procurements due to their ability to sustain supersonic speeds and execute complex high-altitude maneuvers. These systems provide realistic radar cross-section profiles that are essential for validating advanced air defense radars and interceptor missiles, which require targets with specific kinematic properties. As per technical reports, fixed-wing drones typically achieve longer flight durations compared to rotary counterparts, enabling extended training sessions without frequent recovery operations. The structural design allows for the integration of sophisticated electronic warfare payloads and decoy dispensers that simulate contemporary adversary tactics effectively. Military forces prioritize these platforms because they can replicate the flight envelopes of fifth-generation fighters, including steep climbs, rapid descents, and high-G turns that rotary systems cannot physically achieve. The cost-effectiveness of fixed-wing designs also contributes to dominance, as manufacturing processes benefit from established aerospace supply chains and mature production techniques. This segment leadership remains secure as air combat training increasingly emphasizes beyond-visual-range engagements where speed and altitude performance are critical determinants of training realism and operational readiness validation.

On the other side, the rotary wing segment is the fastest-growing segment and is predicted to witness a promising CAGR in the European market during the forecast period owing to the increasing demand for low-altitude urban combat simulation and close-quarters battle training scenarios. For instance, the versatility of vertical takeoff and landing capabilities allows these systems to operate from confined spaces such as ship decks, forward operating bases, and urban environments where runway infrastructure is unavailable. As per defense reports, rotary-wing target drone acquisitions have increased to support counter-unmanned aerial system training, which requires slow-moving, hovering targets that emulate commercial drones used by adversarial forces. The ability to maintain stationary positions or execute precise low-speed maneuvers makes rotary platforms indispensable for testing short-range air defense systems, point-defense weapons, and electronic jamming equipment. Modern rotary target drones incorporate advanced stabilization systems and modular payload bays that enable rapid reconfiguration between visual, infrared, and radar threat simulations. According to industry reports, the miniaturization of electric propulsion systems has reduced operational costs while extending mission endurance through hybrid power configurations. A growing emphasis on asymmetric warfare training, particularly in counter-terrorism and irregular conflict scenarios, has elevated demand for rotary platforms that can replicate the tactical behaviors of small unmanned aerial vehicles. Military academies across Europe and North America have integrated rotary target drones into curricula focusing on urban warfare preparedness, ensuring that personnel develop proficiency against emerging low-altitude threats that conventional fixed-wing systems cannot adequately simulate.

By Use Insights

The aerial target drones segment led the market with the highest share of the regional market in 2025 because they provide essential validation for integrated air defense systems, surface-to-air missiles, and airborne interception protocols. According to global defense expenditure data, a significant portion of budgets is allocated to testing and certification activities, which require realistic aerial threat simulation. As per operational requirements published by NATO, aerial targets must replicate the kinetic and electronic signatures of manned fighters, cruise missiles, and unmanned combat aerial vehicles to ensure defense systems perform reliably under combat conditions. The complexity of modern air warfare demands multi-dimensional threat emulation, including high-speed approaches, low-observable profiles, and electronic countermeasure deployment, which only specialized aerial target drones can provide consistently. Military forces conduct thousands of live-fire exercises annually, requiring reliable, recoverable, or expendable targets that withstand extreme stress while transmitting detailed telemetry data for post-mission analysis. According to procurement statistics from the European Defence Agency, member states continue to purchase aerial target systems to support expanded air policing missions and collective defense commitments. The strategic imperative to maintain air superiority drives continuous investment in aerial targets that evolve alongside adversary capabilities, ensuring that defense networks remain effective against emerging threats. This segment dominance reflects the fundamental role of air power in contemporary military doctrine, where validated interception capabilities determine national security posture and alliance credibility.

On the other end, the marine target drones segment represents the fastest-growing use segment and is predicted to showcase a promising CAGR in the European market during the forecast period owing to the extensive naval modernization initiatives and an increasing focus on littoral warfare capabilities across major maritime powers. For instance, significant portions of budgets are being directed toward anti-ship missile testing, coastal defense validation, and mine countermeasure training. As per naval reports, marine target drones are essential for simulating fast-attack craft, unmanned surface vessels, and sea-skimming missiles that pose asymmetric threats to high-value naval assets. The growing prevalence of swarm tactics in naval warfare necessitates realistic multi-vessel target scenarios that test coordinated defense responses and distributed lethality concepts. Modern marine targets incorporate waterproof housings, salt-resistant materials, and autonomous navigation systems capable of executing complex sea-state maneuvers that challenge radar tracking and weapon guidance algorithms. According to procurement records from various European navies, marine target drone acquisitions have increased to support expanded fleet exercises in contested waters. The strategic shift toward distributed maritime operations requires validation of networked sensor systems and cooperative engagement capabilities against realistic surface threats. Rising tensions in various maritime regions have further accelerated the demand for marine targets that replicate adversary patrol boats and missile boats, enabling navies to refine tactics, techniques, and procedures for high-intensity maritime conflicts. This growth trajectory reflects a broader transformation in naval doctrine, emphasizing agility, resilience, and layered defense against diverse surface threats.

COUNTRY LEVEL ANALYSIS

Europe Target Drone Market Analysis

Europe will likely accelerate the development of standardized, interoperable training ecosystems to support the Alliance’s unified air defense strategies over the coming years. Europe occupies the second-largest market position in the global market due to the rapid modernization efforts driven by heightened security concerns and collaborative defense initiatives. According to data from the European Defence Agency, member states have significantly increased their collective defense spending, with substantial allocations directed toward air defense capabilities and realistic training infrastructure. As per reports from NATO Allied Air Command, European nations conduct hundreds of joint exercises annually, requiring standardized target drone platforms that ensure seamless interoperability among multinational forces. The Permanent Structured Cooperation framework has facilitated numerous collaborative projects focused on shared training assets, including pooled target drone fleets that reduce individual national procurement burdens. Germany, France, and the United Kingdom lead regional procurement activities, leveraging industrial capabilities to develop indigenous target drone solutions. According to analysis from the Stockholm International Peace Research Institute, Eastern European nations,s including Poland and Romania, are significantly increasing target drone acquisitions to support expanded air policing missions along alliance borders. Research initiatives funded by the European Union continue to drive innovation in AI-enabled target swarms. Regulatory harmonization efforts through the European Union Aviation Safety Agency aim to streamline approval processes, although fragmented national regulations continue to pose operational challenges. Regional growth reflects a strategic prioritization of collective defense readiness and technological sovereignty amid evolving security architectures.

COMPETITIVE LANDSCAPE

The competitive landscape of the target drones market features intense rivalry among established aerospace giants and specialized unmanned system developers striving to deliver superior performance and cost efficiency. Major corporations leverage extensive resources to integrate artificial intelligence and autonomous capabilities,s creating sophisticated platforms that mimic evolving adversary tactics. Smaller innovative firms challenge incumbents by offering niche solutions focused on specific threat profiles such as low observable signatures or swarm coordination. Price competition remains significant as defense budgets face pressure, forcing manufacturers to balance advanced features with affordability through scalable production methods. Intellectual property disputes occasionally arise regarding proprietary algorithms and sensor technologies,ies highlighting the value placed on technological advantages. Geographic diversification strategies enable companies to mitigate risks associated with regional political instability while accessing varied procurement cycles. Collaboration with government research institutions fosters breakthrough innovations in materials science and propulsion systems,tems maintaining continuous improvement in flight endurance and maneuverability. The market demands constant adaptation to regulatory changes and cybersecurity threats, requiring agile operational frameworks and robust risk management protocols.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Target Drone Market include

- QinetiQ Group plc

- Airbus SE

- Leonardo S.p.A.

- Saab AB

- Kratos Defense & Security Solutions, Inc.

- Northrop Grumman Corporation

- BAE Systems plc

- Thales Group

- Denel Dynamics

- AeroTargets International LLC

- Griffon Aerospace

- SCR (Sierra Nevada Corporation)

TOP LEADING PLAYERS IN THE MARKET

- Kratos Defense and Security Solutions stands as a pivotal innovator specializing in high-performance expendable and recoverable target drones that simulate advanced adversary threats for military training. The company has consistently delivered cutting-edge platforms such as the XQ 58A Valkyrie, which integrates artificial intelligence capabilities to execute autonomous missions. Recent strategic initiatives include expanding production facilities in Oklahoma to meet surging demand fromthe United States armed forces and international allies. Kratos focuses on modular designs, allowing rapid configuration changes between electronic warfare simulation and kinetic threat emulation. Their commitment tocost-effectivee manufacturing through additive techniques ensures competitive pricing while maintaining superior flight characteristics. The firm actively collaborates with government agencies to develop next-generation swarm technologies, enhancing its technological leadership position.

- Boeing remains a dominant force, leveraging its extensive aerospace expertise to produce sophisticated target drone systems that replicate fifth-generation fighter capabilities for comprehensive air defense validation. The company recently secured multiple contracts to supply MQ 28 Ghost Bat variants adapted for target roles, demonstrating versatility in unmanned platform development. Boeing invests heavily in research and development,t focusing on stealth characteristics and advanced sensor integration to challenge modern radar systems. Their global supply chain enables efficient delivery of complex systems to NATO partners and Indo-Pacific allies. The corporation emphasizes interoperability, ensuring seamless integration with existing command and control networks. Recent partnerships with software firms enhance autonomous decision-making algorithms, strengthening operational effectiveness during live fire exercises.

- Leonardo S.p.A serves as a leading European manufacturer providing advanced target drone solutions tailored to meet stringent NATO standards and regional security requirements. The company recently launched new variants of its Falco Evo platform incorporating enhanced electronic warfare payloads and improved endurance capabilities for extended training scenarios. Leonardo prioritizes indigenous development,t reducing dependency onon-Europeanan suppliers while fostering technological sovereignty among member states. Their recent collaborations with other European defense contractors focus on shared infrastructure projects promoting interoperability across allied forces. The firm invests in sustainable manufacturing practices utilizing composite materials that reduce environmental impact while improving structural durability. Leonardo actively participates in European Defence Fund initiatives driving innovation in autonomous swarm technologies and artificial intelligence integration for future combat training environments.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the target drones market primarily employ strategic partnerships and collaborative research initiatives to accelerate technological innovation and share development costs among allied nations. Companies frequently engage in mergers and acquisitions to absorb specialized startups possessing niche expertise in artificial intelligence or advanced materials science. Product differentiation through modular payload systems allows manufacturers to offer customizable solutions addressing diverse training requirements across air, land,d and maritime domains. Investment in additive manufacturing techniques significantly reduces production timelines and material waste, te enabling rapid prototyping and cost-competitive pricing structures. Expansion into emerging markets, particularly inthe Asia Pacific and Middle East regions, provides access to growing defense budgets and modernization programs. Focusing on cybersecurity enhancements ensures protection against sophisticated digital threats compromising operational integrity during sensitive training exercises. Regulatory compliance strategies help navigate complex airspace restrictions, facilitating broader operational flexibility for military customers seeking realistic simulation environments.

EUROPE TARGET DRONES MARKET NEWS

- In March 2024, Kratos Defense announced the expansion of its Oklahoma facility to increase production capacity for XQ-58A Valkyrie target drones supporting United States Air Force training requirements and strengthening the Target drones market presence.

- In June 2024, Boeing secured a contract to supply modified MQ 28 Ghost Bat platforms to the Australian Defense Force for advanced air combat training exercises and to strengthen the Target drones market presence.

- In September 2024, Leonardo S.p.A launched new Falco Evo variants with enhanced electronic warfare payloads for NATO-allied nations, strengthening the Target drones market presence

- In January 2025, Kratos Defense partnered with Microsoft to integratecloud-basedd artificial intelligence algorithms into target drone swarm operations, strengthening the Target drones market presence.

- On May 20,25 Boeing collaborated with European aerospace firms to develop interoperable target drone systems for joint multinational training exercises and to strengthen the target drone market presence.

MARKET SEGMENTATION

This research report on the europe target drone market is segmented and sub-segmented into the following categories.

By Type

- Fixed Wing

- Rotary Wing

By Use

- Aerial Target Drones

- Marine Target Drones

- Ground Target Drones

By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Poland

- Rest of Europe

Frequently Asked Questions

1. What is driving growth in Europe?

Growth is driven by rising defense budgets, modernization of military training, increased use of advanced missiles and air‑defense systems, and efforts to improve training realism and safety.

2. Which segment leads the market?

Aerial target drones lead the market and are also the fastest‑growing segment.

3. Which applications are most important?

Main applications include military live‑fire training, missile and radar testing, and air‑defense system evaluation.

5. Who are the major players?

Key global and European players include Airbus, BAE Systems, Leonardo, QinetiQ, Safran, Lockheed Martin, Northrop Grumman, Boeing, and Kratos.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com