Europe Threat Intelligence Market Size, Share, Trends & Growth Forecast Report By Organization Size, Deployment Type, Type, and By Country (United Kingdom, Germany, France, Netherlands, Sweden) – Industry Analysis and Forecast, 2026 to 2034

Europe Threat Intelligence Market Summary

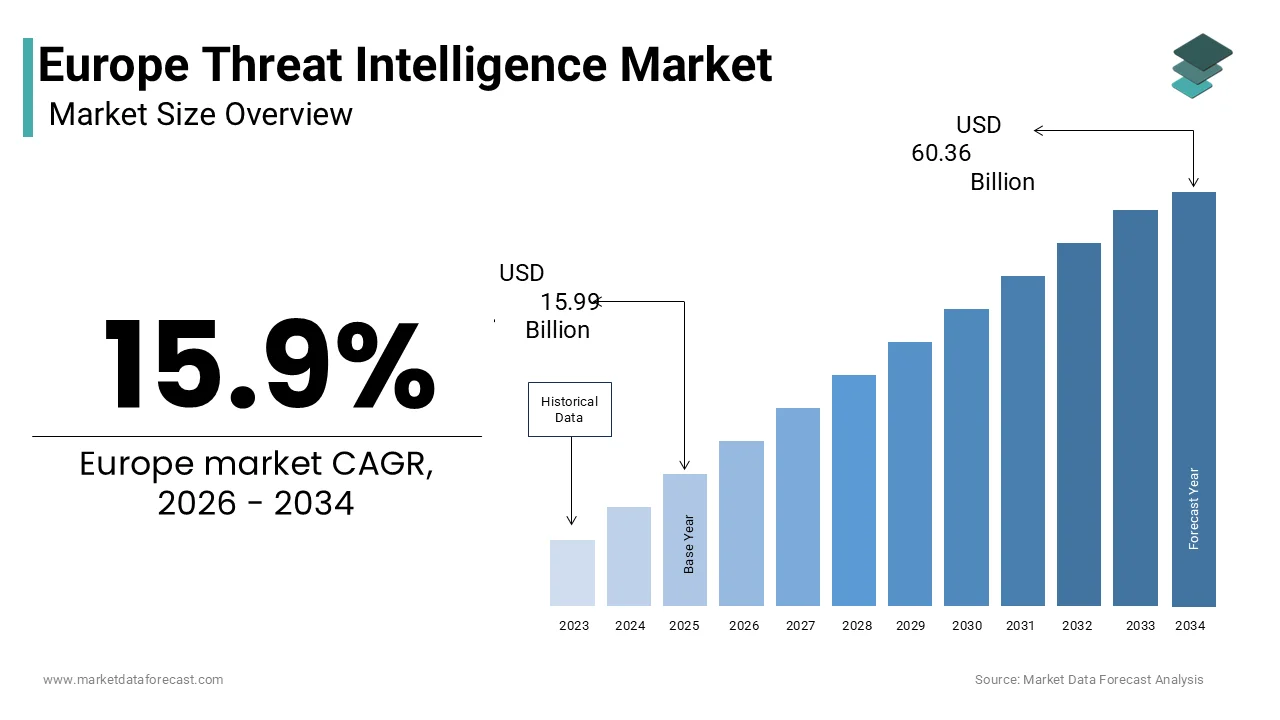

Europe’s threat intelligence market, valued at USD 15.99 billion in 2025, is projected to reach USD 60.36 billion by 2034 at a CAGR of 15.9%, driven by NIS2 and DORA compliance mandates, escalating ransomware activity, and AI-powered predictive cyber defense adoption.

Key Market Insights

- 2025 Market Size: USD 15.99 billion

- 2026 Market Size: USD 18.54 billion

- 2034 Forecast: USD 60.36 billion

- CAGR (2026–2034): 15.9%

- Base Year: 2025

- Forecast Period: 2026–2034

Quick Growth Drivers

- Mandatory adoption under NIS2 and DORA regulations

- Sharp rise in ransomware and state-sponsored cyberattacks

- Expansion of critical infrastructure digitization

- Growing reliance on predictive, intelligence-led security models

- Increasing integration of AI and machine learning in cyber defense

Principal Restraints

- Fragmented data-sharing and privacy interpretations under GDPR

- Legal ambiguity around sharing indicators of compromise across borders

- Limited interoperability across national threat-sharing platforms

- Heavy dependence on generic, low-context commercial intelligence feeds

High-Value Opportunities

- AI-driven predictive threat analytics and automated enrichment

- Expansion of EU-wide intelligence sharing under the Cyber Solidarity Act

- Growth of managed threat intelligence services for SMEs

- Sector-specific intelligence tailored for finance, energy, healthcare, and defense

Key Market Challenges

- Severe shortage of skilled cyber threat intelligence analysts

- Alert fatigue due to high-volume, low-relevance data feeds

- Lack of standardized metrics to measure intelligence effectiveness

- Difficulty proving ROI of threat intelligence investments

Fastest-Growing Segments

- Small & Medium Enterprises (CAGR 25.5%) – driven by MDR adoption

- Cloud-Based Deployment (CAGR 23.4%) – aligned with EU cloud-first policies

- Threat Intelligence Services (CAGR 25.5%) – strategic advisory and managed intelligence demand

Regional Leadership & Dynamics

- United Kingdom (19.4%) – mature cybersecurity ecosystem and financial sector adoption

- Germany – industrial IP protection and IT Security Act 2.0 enforcement

- France – sovereign intelligence focus and SecNumCloud-certified platforms

- Netherlands – leader in public–private intelligence sharing frameworks

- Sweden – hybrid threat defense and AI-driven national CERT initiatives

What Wins Commercially

- Compliance-ready intelligence aligned with NIS2, DORA, and GDPR

- Sector-specific and context-rich intelligence, not raw indicators

- AI-enabled predictive analytics and early campaign detection

- Seamless integration with SIEM, SOAR, and MDR platforms

- Sovereign, EU-based data processing and transparency

Top Strategic Ask for Executives

Shift from indicator-heavy feeds to AI-enabled, sector-specific, and regulation-aligned threat intelligence that delivers measurable risk reduction and operational impact.

Leading Players

Some of the companies that are playing a dominating role in the Europe Threat Intelligence Market include:

- Recorded Future

- CrowdStrike Holdings, Inc.

- IBM Corporation

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Microsoft Corporation

- Check Point Software Technologies Ltd.

- Splunk Inc.

- Darktrace plc

- Sophos Group plc

Europe Threat Intelligence Market Size

The Europe threat intelligence market was valued at USD 15.99 billion in 2025 and increased to USD 18.54 billion in 2026. The market is projected to reach USD 60.36 billion by 2034, growing at a CAGR of 15.9% from 2026 to 2034.

Threat intelligence includes technologies, services,s and analytical frameworks that enable public and private organizations to proactively identify, anticipate and mitigate cyber threats through the collection, interpretation and dissemination of actionable intelligence on adversarial tactics, infrastructure, and indicators of compromise. Unlike reactive cybersecurity tools, threat intelligence operates on a predictive and contextual basis,s integrating data from open sources, dark web monitoring, proprietary telemetry, and strategic geopolitical analysis. The urgency of this market has intensified as Europe confronts a surge istate-sponsoreded attacks, ransomware campaigns,,s and supply chain compromises. In 2023, the European Union faced a substantial number of cybersecurity incidents reported to national authorities as per the European Union Agency for Cybersecurity. The average cost of a data breach in the region reached 4.1 million euros as per IBM’s Cost of a Data Breach Report 2023, underscoring the financial stakes of inadequate preparedness. Regulatory mandates such as the revised Network and Information Security Directive and the Digital Operational Resilience Act now compel critical infrastructure operators to integrate threat intelligence into their risk management frameworks, which is making it a compliance imperative rather than an optional security enhancement.

MARKET DRIVERS

Mandatory Regulatory Compliance Under NIS2 and DORA

The enforcement of the revised Network and Information Security Directive and the Digital Operational Resilience Act has fundamentally reshaped demand for threat intelligence across Europe by transforming it from a best practice into a legal obligation, which is majorly propelling the growth of the European threat intelligence market. NIS2, which applies to a large number of entities in energy, transport, health, and digital infrastructure sectors, mandates continuous threat monitoring and information sharing with national cybersecurity authorities as per the European Commission. Similarly, DORA requires financial institutions to implement advanced threat detection systems and conduct regular threat-led penetration testing. These regulations explicitly reference the use of threat intelligence feeds to identify emerging attack patterns and adversary infrastructure. In Germany, for instance, the Federal Office for Information Security now requires operators of essential services to demonstrate real-time intelligence integration as part of their certification process. According to a 2025 survey by the European Banking Federation, 78% of major banks increased threat intelligence budgets specifically to meet DORA requirements. This regulatory convergence eliminates discretionary adoption and embeds threat intelligence into the core governance of Europe’s most critical sectors, ensuring sustained institutional demand regardless of short-term threat fluctuations.

Escalation of Ransomware and State-Sponsored Cyber Operations

Europe has become a primary theater for sophisticated cyber aggression, with ransomware groups and nation-state actors increasingly targeting critical infrastructure and public services, which is further boosting the European threat intelligence market expansion. In 2023, ransomware attacks in the European Union increased significantly year on year, according to the European Union Agency for Cybersecurity, with healthcare and education sectors suffering the most disruptive incidents. Simultaneously, state-sponsored groups linked to Russia, China, and Iran executed numerous campaigns against European government networks and defense contractors as documented in ENISA’s Threat Landscape 2023. The intrusion into the European Parliament’s email system in early 2025 and the coordinated attacks on Ukrainian refugee databases in Poland and Germany exemplify the strategic nature of these operations. Such incidents have compelled organizations to move beyond signature-based detection toward intelligence-led defense that anticipates attacker behavior. Threat intelligence enables defenders to correlate indicators across sectors, identify campaign infrastructure before exploitation, and preemptively block command-and-control channels. As hybrid warfare increasingly incorporates cyber elements, European entities view threat intelligence not merely as a technical tool but as a component of national and economic resilience.

MARKET RESTRAINTS

Fragmented Data Privacy and Intelligence-Sharing Legal Frameworks

Despite shared security objectives, the European threat intelligence market is constrained by divergent national interpretations of data protection and liability laws that inhibit cross-border intelligence collaboration. The General Data Protection Regulation, while harmonizing privacy standards, creates ambiguity regarding the lawful processing of IP addresses, malware samples, and attacker identifiers, which may be classified as personal data. In France, for example, the data protection authority CNIL has issued guidance requiring explicit anonymization of threat data before sharing, whereas Sweden permits broader operational exchange under national security exemptions. This legal fragmentation discourages private firms from participating in public-private information exchanges for fear of regulatory penalties. A 2025 study by the Centre for European Policy Studies found that only 29% of European cybersecurity teams regularly contribute to national threat-sharing platforms due to liability concerns. Additionally, the lack of standardized sharing protocols,s such as consistent use of STIX, TAXII, or MISP across member states, es reduces interoperability. Until the EU establishes a unified legal safe harbor for cybersecurity data exchange, threat intelligence will remain siloed, which is undermining collective defense and market scalability.

Shortage of Skilled Analysts to Interpret and Operationalize Intelligence

The effectiveness of threat intelligence is heavily dependent on human expertise, yet Europe faces a severe deficit in professionals capable of contextualizing raw data into actionable security decisions, which is further hampering the expansion of the European threat intelligence market. The European Union currently has a significant number of unfilled cybersecurity positions, according to the European Commission’s Cybersecurity Skills Gap Study 2025, with threat analysis among the most specialized and undersupplied roles. Academic programs in cyber threat intelligence remain limited, with fewer than 15 universities across the EU offering dedicated curricula as per the European Higher Education Area database. Consequently, many organizations deploy threat intelligence platforms without adequate staffing, leading to alert fatigue and underutilization. As per a survey by the SANS Institute in 2023, 64% of European security operations centers receive more than 10,000 threat indicators weekly but act on less than 5% due to resource constraints. This capability gap forces reliance on managed security service providers, increasing costs and reducing strategic autonomy. Without significant investment in workforce development and automated intelligence enrichment, the full potential of threat intelligence will remain unrealized across the European market.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Predictive Threat Analytics

The incorporation of artificial intelligence and machine learning into threat intelligence platforms offers a transformative opportunity for the European threat intelligence market. European vendors such as Recorded Future and ThreatQuotient are deploying natural language processing models to analyze multilingual dark web forums and malware code repositories in real time. According to the European Innovation Council, 45 AI-driven projects were funded under the 2025 Pathfinder program with a total budget of €138 million, which is supporting innovations across cybersecurity, health, and computing. These models can reduce indicator validation time from hours to seconds and identify zero-day exploitation patterns before public disclosure. For example, an AI system piloted by the Dutch National Cyber Security Centre in 2023 was reported to have successfully anticipated ransomware activity targeting logistics firms by monitoring Russian-language hacker chatter and cryptocurrency wallet movements. As the volume of threat data grows exponentially, AI-enabled intelligence becomes not just an efficiency tool but a strategic necessity, ty enabling proactive defense in an era of hyper-accelerated cyber conflict.

Expansion of Threat Intelligence Sharing through the EU Cyber Solidarity Act

The proposed Cyber Solidarity Act introduces a groundbreaking opportunity to institutionalize threat intelligence sharing across Europe through the creation of a Union-wide Cybersecurity Emergency Mechanism and distributed Security Operations Centers, which is another promising opportunity in the European threat intelligence market. Scheduled for adoption in 2025, the legislation mandates the establishment of national and cross-border Security Operations Centers that will pool threat data from critical sectors and deploy rapid response teams during major incidents. According to the European Commission, these centers will operate on a trusted partner model with standardized protocols for anonymized data exchange and joint analysis. The Act also allocates €1.1 billion, with about two-thirds from the EU budget, to fund infrastructure and training. Pilot programs in the Baltic states have already demonstrated that shared intelligence significantly reduced incident response times during coordinated phishing campaigns against energy grids. By creating a legal, technical, and financial ecosystem for collective defense, the Cyber Solidarity Act has the potential to transform Europe from a collection of national silos into a unified cyber resilience bloc, thereby expanding the addressable market for interoperable threat intelligence solutions.

MARKET CHALLENGES

Over-Reliance on Generic Commercial Feeds with Low Operational Value

Many European organizations procure threat intelligence from commercial vendors that deliver high-volume but low-relevance data streams lacking sector-specific context or actionable playbooks, which is majorly challenging the growth of the European threat intelligence market. According to a 2025 report by Germany’s Federal Office for Information Security, a significant share of commercial feeds used by enterprises contained indicators already blocked by standard firewalls or outdated within short timeframes. This generic intelligence fails to address the unique threat landscape of individual industries such as maritime logistics or pharmaceutical research, where attacker motives and tactics differ significantly. Consequently, security teams experience alert fatigue and deprioritize intelligence integration despite regulatory mandates. The problem is exacerbated by vendors marketing aggregated open-source data as premium intelligence without human validation or strategic analysis. Without industry-tailored intelligence that maps to specific attack surfaces and adversary playbooks, organizations cannot translate data into defensive actions. This misalignment between supply and operational need risks creating a false sense of security and undermining the credibility of the threat intelligence market as a whole.

Lack of Standardized Metrics to Evaluate Intelligence Effectiveness

The European threat intelligence market suffers from an absence of universally accepted performance indicators, which is making it difficult for organizations to assess return on investment or compare vendor offerings. Unlike firewall throughput or encryption strength, threat intelligence efficacy is inherently contextual and time-delayed. A feed may prevent an attack that never materializes, rendering its value invisible. As per a 2025 study by the European Organisation for Security, only 18% of European enterprises use structured evaluation frameworks such as the Threat Intelligence Platform Evaluation Model developed by MITRE. Most rely on subjective measures like dashboard aesthetics or feed volume rather than metrics such as mean time to enrichment, predictive accuracy, or incident prevention rate. This measurement gap enables low-quality providers to persist in the market and discourages strategic procurement. Furthermore, regulators have not mandated specific intelligence quality standards under NIS2, leaving implementation to organizational discretion. Until Europe adopts common evaluation criteria aligned with operational outcomes, the market will struggle to mature beyond commoditized data delivery toward true intelligence as a service.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Organization Size, Deployment Type, Type, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Recorded Future, FireEye, Inc. (Trellix), CrowdStrike Holdings, Inc., IBM Corporation, Cisco Systems, Inc., Palo Alto Networks, Inc., Microsoft Corporation, Secureworks, Inc., Check Point Software Technologies Ltd., Splunk Inc., Trend Micro Incorporated, Intel Security (McAfee), ZeroFox, Inc., Flashpoint (Ablative Ltd.), Anomali, Inc., Darktrace plc, RiskIQ (Microsoft), Digital Shadows (Seekurity Ltd.), Kaspersky Lab, Sophos Group plc. |

SEGMENTAL ANALYSIS

By Organization Size Insights

The large enterprises segment dominated the European threat intelligence market in 2025 by accounting for a 65.6% of the regional market share in 2025. The dominance of the large enterprises segment in this regional market can be attributed to their complex digital footprints, regulatory exposure, and mature security operations centers capable of absorbing and operationalizing intelligence. Industries such as finance, energy, and telecommunications are mandated under NIS2 and DORA to implement proactive threat monitoring, which is making intelligence integration non-discretionary. Large enterprises in Europe are disproportionately affected by stringent cybersecurity regulations that explicitly require threat intelligence integration. The revised Network and Information Security Directive applies to a large number of organizations across critical sectors, mandating real-time threat monitoring and cross-entity information sharing as per the European Commission. Similarly, the Digital Operational Resilience Act compels major financial institutions to conduct threat-led penetration testing using up-to-date adversary intelligence. In Germany, for example, the Federal Financial Supervisory Authority requires banks with assets over €50 billion to maintain dedicated threat intelligence units. According to a 2025 survey by the European Banking Federation, 89% of Tier 1 banks had integrated commercial and open-source intelligence feeds into their security orchestration platforms.

The small and medium enterprises segment is the fastest growing in the European threat intelligence market and is estimated to register a CAGR of 25.5% over the forecast period, owing to the convergence of managed security services, regulatory trickle-down, and cloud-native intelligence platforms tailored for resource-constrained environments. Small and medium enterprises are increasingly accessing threat intelligence indirectly through managed detection and response providers that bundle intelligence into subscription-based security operations. In 2023, a majority of European SMEs relied on external managed security service providers for threat monitoring,g according to Eurostat’s survey on business digitalization. Firms like Nucleus Security in the Netherlands and Cybertrap in Germany embed curated threat feeds into their MDR offerings, which is enabling SMEs to benefit from intelligence without in-house expertise. The European Cyber Resilience Act further incentivizes this model by requiring software vendors to support third-party monitoring, which facilitates MDR integration. A pilot program by France’s ANSSI in 2025 found that SMEs using MDR with integrated threat intelligence reduced breach impact compared to those using basic antivirus solutions.

By Deployment Type Insights

The cloud-based deployment segment led the market by holding 58.7% of the regional market share in 2025. The leading position of the cloud segment in the regional market is driven by its broader shift toward agile, scalable, and cost-efficient security architectures that align with digital transformation strategies across public and private sectors.

European organizations are prioritizing cloud migration as part of national and corporate digital agendas, making cloud-native threat intelligence the default deployment model. The European Commission’s Cloud Rulebook for Europe aims to accelerate public sector cloud adoption, with a large share of new government IT projects required to be cloud-eligible by 2025. Simultaneously, private enterprises are retiring legacy on-premise systems, with many European CIOs reporting that over half their workloads now run in cloud environments as per a 2023 IDC Europe survey.

The cloud segment is also the fastest growing in the European threat intelligence market and is likely to grow at a CAGR of 23.4% over the forecast period, owing to the converging trends in regulatory enablement, vendor innovation, and operational necessity. European regulators are actively promoting cloud-based threat intelligence through standardized security certifications and interoperability mandates. The European Union’s Cybersecurity Act empowers ENISA to certify cloud security services, with threat intelligence platforms now eligible under the European Cybersecurity Certification Scheme for Cloud Services. In 2025, France’s ANSSI granted its first “SecNumCloud” certification to a threat intelligence SaaS provider,r enabling use by defense and energy ministries. Similarly, the German Federal Office for Information Security includes cloud intelligence feeds in its recommended security controls for critical operators.

By Type Insights

The solutions segment held the major share of 56.9% of the regional market in 2025. The growth of the solutions segment in the European threat intelligence market is attributed to its strong demand for automated platforms that deliver structured intelligence through dashboards, APIs, and integration modules. Organizations prioritize solutions that reduce manual analysis and accelerate response through orchestration and enrichment capabilities. European security teams face overwhelming alert volumes and limited analyst capacity, which is making automated threat intelligence solutions essential for operational efficiency. According to a 2023 study by the SANS Institute, European security operations centers receive thousands of alerts per day but investigate only a small fraction due to resource constraints. Intelligence platforms like ThreatConnect and Anomali address this by automatically enriching alerts with contextual data, enabling tier-one analysts to triage accurately. In the Netherlands, a pilot by the National Cyber Security Centre showed that automated intelligence enrichment reduced false positives and accelerated incident classification.

The services segment is promising and is anticipated to witness a CAGR of 25.5% over the forecast period. Factors such as the rising need for contextual interpretation, strategic advisory, and managed intelligence operations that platforms alone cannot provide are contributing to the growth of the services segment in the European threat intelligence market. While automated solutions handle tactical indicators, European decision makers increasingly require human-curated strategic intelligence on geopolitical cyber risks, threat actor motivations, and campaign forecasting. In 2025, a survey by the European Confederation of Directors’ Associations found that 64% of board-level risk committees commissioned bespoke threat intelligence services to assess exposure to state-sponsored attacks and supply chain compromises.

COUNTRY LEVEL ANALYSIS

United Kingdom Threat Intelligence Market Analysis

The United Kingdom captured the leading position in the European threat intelligence market in 2025 by holding 19.4% of the regional market share. The dominance of the UK in the European market is driven by its mature cybersecurity ecosystem, strong regulatory framework, and high concentration of financial and technology firms. According to the UK’s National Cyber Security Centre, a majority of FTSE 350 companies had implemented formal threat intelligence programs by 2023. The country pioneered public-private threat sharing through initiatives like the Cyber Security Information Sharing Partnership, which connects thousands of organizations with real-time intelligence feeds. The UK’s departure from the EU has not diminished its cybersecurity ambition, with the 2022 National Cyber Strategy committing £2.6 billion to enhance threat detection and response capabilities. The Financial Conduct Authority mandates intelligence-led testing for major banks under its Operational Resilience Framework, accelerating adoption in the finance sector. Additionally, London hosts a dense cluster of threat intelligence vendors, including Digital Shadows and Surevine, fostering innovation and talent development.

Germany Threat Intelligence Market Analysis

Germany commanded a significant share of the European threat intelligence market in 2025 owing to its industrial base, stringent data protection laws, and proactive national cybersecurity strategy. According to the Federal Office for Information Security, a large majority of critical infrastructure operators in energy, transport, and health sectors integrated threat intelligence into their security operations by 2023 to comply with the IT Security Act 2.0. The country’s Mittelstand manufacturing firms are increasingly adopting intelligence services to protect intellectual property from industrial espionage, with many reporting targeted cyber reconnaissance in 2023 as per a DIHK survey. Germany also leads in threat intelligence standardization, hosting the development of the Open Security Information Exchange framework and promoting STIX/TAXII adoption across EU institutions. The Federal Ministry of the Interior has allocated €1.2 billion under the Cyber Innovation Fund to support AI-driven intelligence analytics and cross-sector information-sharing platforms.

France Threat Intelligence Market Analysis

France holds a notable share of the European threat intelligence market due to its centralized cybersecurity governance and strategic focus on sovereignty. According to the French National Cybersecurity Agency, a majority of operators of essential services implemented certified threat intelligence platforms by 2023 under the transposition of NIS2 into national law. The country operates the Cyber Threats Operational Centre, which fuses intelligence from military, private, and international sources to produce national alerts distributed via the secure CyCLONe platform. France’s defense procurement agency has mandated that all major contractors integrate sovereign threat intelligence feeds to protect classified programs, with vendors like Thales and Airbus offering tailored services. The 2023 French Cybersecurity Strategy allocated €1.4 billion to develop domestic intelligence capabilities, reducing reliance on non-EU providers. Additionally, France pioneered the SecNumCloud certification, ensuring that cloud-based intelligence services meet strict data residency and encryption standards.

Netherlands Threat Intelligence Market Analysis

The Netherlands is anticipated to grow at a healthy CAGR in the European threat intelligence market over the forecast period, owing to its advanced digital infrastructure, neutral geopolitical stance, and leadership in public-private cyber collaboration. According to the Dutch National Cyber Security Centre, a large majority of top enterprises participate in the National Threat Sharing Framework, which provides anonymized intelligence on ransomware, phishing, and supply chain attacks. The country hosts critical internet infrastructure,e including the Amsterdam Internet Exchange, making it a prime target and thus a pioneer in defensive intelligence. In 2023, the Dutch Ministry of Justice launched the Cyber Intelligence Fusion Cell to correlate signals from law enforcement, intelligence agencies, and the private sector to preempt critical incidents. Dutch financial institutions are required under the DORA transposition to conduct threat-led stress tests using up-to-date intelligence feeds. Furthermore, the Netherlands serves as a European base for global vendors like CrowdStrike and Palo Alto Networks, enabling rapid product localization and customer support.

Sweden Threat Intelligence Market Analysis

Sweden is expected to occupy a notable share of the European threat intelligence market during the forecast period due to its digital society model, robust public sector cybersecurity, and proactive stance against hybrid threats. According to the Swedish Civil Contingencies Agency, a majority of central government agencies implemented automated threat intelligence feeds by 2023 following high-profile intrusions into parliamentary and defense networks. The country’s Digitaliseringsstrategi mandates that all public digital services integrate real-time threat monitoring with intelligence shared via the national CERT-SE platform. Sweden’s strong presence in telecommunications with Ericsson and in gaming with companies like King necessitates advanced protection against intellectual property theft and disinformation campaigns. In 2025, the Swedish Defence Research Agency launched an AI-powered intelligence fusion project to detect coordinated inauthentic behavior targeting democratic processes. Additionally, Sweden champions GDPR-compliant intelligence sharing within the Nordic region through joint exercises and standardized protocols.

COMPETITIVE LANDSCAPE

Competition in the European threat intelligence market is characterized by a dynamic interplay between global vendors with scale and European specialists emphasizing data sovereignty and regulatory alignment. The market is not driven by price but by trust, accuracy,y and contextual relevance,ce with differentiation hinging on sector expertise,ise integration depth,epth and compliance readiness. Global firms leverage broad data setsAI-poweredwered analytics, while European companies emphasize privacy by design and collaboration with national cybersecurity authorities. Regulatory mandates under NIS2 and DORA have raised the bar for intelligence quality,y compelling vendors to move beyond raw indicators toward predictive and strategic insights. The rise of managed services is also reshaping competition as smaller organizations outsource intelligence operations. Meanwhi, the interoperability through STIX TAXII and participation in national sharing communities have become table stakes. This environment rewards vendors that balance global threat visibility with local legal and operational realities,ies fostering a competitive landscape that is both technically sophisticated and policy sensitive.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Threat Intelligence Market include

- Recorded Future

- FireEye, Inc. (Trellix)

- CrowdStrike Holdings, Inc.

- IBM Corporation

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Microsoft Corporation

- Secureworks, Inc.

- Check Point Software Technologies Ltd.

- Splunk Inc.

- Trend Micro Incorporated

- Intel Security (McAfee)

- ZeroFox, Inc.

- Flashpoint (Ablative Ltd.)

- Anomali, Inc.

- Darktrace plc

- RiskIQ (Microsoft)

- Digital Shadows (Seekurity Ltd.)

- Kaspersky Lab

- Sophos Group plc

TOP LEADING PLAYERS IN THE MARKET

- Recorded Future is a leading global provider of threat intelligence with a strong footprint across Europe serving government agencies,ncies financial institutions, and critical infrastructure operators. The company leverages machine learning and natural language processing to analyze vast volumes of open source dark web and technical data in real time. In Europe, it supports national cybersecurity centers and major enterprises with predictive intelligence on ransomware campaigns, nation-state activity, and emerging vulnerabilities. In 2025, Recorded Future expanded its London office and launched a multilingual intelligence module tailored for EU regulatory compliance, including GDPR aligned data handling and NIS2-ready reporting templates. These enhancements reinforce its position as a trusted strategic intelligence partner for European decision makers navigating complex cyber threat landscapes.

- Mandiant plays a pivotal role in the European threat intelligence market through its deep expertise in incident response and adversary tracking. As part of Google Cloud, the company integrates its intelligence directly into Chronicle and other security platforms used widely across European enterprises. Mandiant’s analysts have attributed numerous state-sponsored campaigns targeting European energy finance and defense sectors, providing actionable context that goes beyond indicators. In early 2025, Mandiant opened a dedicated European Threat Intelligence Fusion Center in Dublin to support localized analysis and faster response for EU clients. It also introduced a DORA-compliant intelligence feed for financial institutions, enabling threat-led testing aligned with regulatory mandates. These actions solidify its relevance in Europe’s evolving compliance-driven security ecosystem.

- EclecticIQ is a European-born threat intelligence company headquartered in the Netherlands that specializes in open source and community-driven intelligence platforms for governments and large enterprises. The company’s core offering enables organizations to collect, process,s and operationalize intelligence from diverse sources while maintaining data sovereignty—a critical concern under EU regulations. EclecticIQ collaborates closely with national CSIRTs and NATO on joint threat analysis initiatives and contributes to EU standardization efforts for STIX TAXII interoperability. In 2025, the company launched its Federated Threat Intelligence Platform, designed for cross-border public sector collaboration with built in GDPR compliant anonymization and audit trails. It also secured accreditation under the UK’s Certified Cyber Security Service Provider scheme. These developments underscore its commitment to building a sovereign, resilient intelligence infrastructure for Europe.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European threat intelligence market are focusing on regulatory alignment by embedding NIS2 DORA and GDPR requirements directly into their intelligence workflows and reporting structures. They are investing in localized data processing through regional threat fusion centers to ensure data sovereignty and reduce latency. Strategic partnerships with cloud providers and security orchestration platforms enable seamless integration into existing enterprise ecosystems. Companies are also enhancing multilingual and sector-specific intelligence feeds to improve relevance for European industries such as energy, finance, and healthcare. Additionally, they are offering managed intelligence services to address the acute shortage of skilled analysts,s particularly among small and medium enterprises and public sector bodies across the continent.

MARKET SEGMENTATION

This research report on the europe threat intelligence market is segmented and sub-segmented into the following categories.

By Organization Size

- Large Enterprises

- Small and Medium Enterprises

By Deployment Type

- Cloud-Based

- On-Premise

By Type

- Solutions

- Services

By Country

- United Kingdom

- Germany

- France

- Netherlands

- Sweden

Frequently Asked Questions

1. Who are the top players in the Europe Threat Intelligence Market?

Leading companies in the Europe Threat Intelligence Market include IBM Security, CrowdStrike, Recorded Future, Darktrace, and Anomali. These firms provide AI-driven platforms for threat detection and SOC integration.

2. What drives growth in the Europe Threat Intelligence Market?

Rising cyberattacks, GDPR/NIS2 regulations, and AI/IoT vulnerabilities propel the Europe Threat Intelligence Market. Organizations seek predictive intel to counter ransomware and espionage targeting critical infrastructure.

3. What are the main segments in the Europe Threat Intelligence Market?

The Europe Threat Intelligence Market segments by organization size (large enterprises, SMEs), deployment (cloud, on-premise), type (solutions, services), and verticals like BFSI, healthcare, and government.

4. How does AI impact the Europe Threat Intelligence Market?

AI transforms the Europe Threat Intelligence Market by enabling real-time threat prediction, multilingual analysis, and automated detection of malware or disinformation. It reduces response times by up to 50% in SOCs

5. What is the role of cloud in the Europe Threat Intelligence Market?

Cloud deployment dominates the Europe Threat Intelligence Market, offering scalable intel for distributed IT environments amid rising hybrid threats. It supports real-time sharing across EU borders.

6. What regulations affect the Europe Threat Intelligence Market?

GDPR, NIS2, and DORA shape the Europe Threat Intelligence Market, mandating proactive threat monitoring and data protection compliance for enterprises facing insider and external risks.

7. What are key threats in the Europe Threat Intelligence Market context?

The Europe Threat Intelligence Market addresses ransomware, DDoS from hacktivists like NoName057(16), and state-sponsored espionage exploiting regulatory gaps across member states.

8. How does threat intelligence benefit European enterprises?

In the Europe Threat Intelligence Market, enterprises gain proactive defense, faster breach detection, and compliance via integrated SOCs and SIEM platforms tailored to regional threats.

9. What verticals dominate the Europe Threat Intelligence Market?

BFSI, telecom/IT, energy/utilities, healthcare, and government lead the Europe Threat Intelligence Market, facing high-stakes attacks on critical infrastructure.

10. What future trends shape the Europe Threat Intelligence Market?

Trends in the Europe Threat Intelligence Market include deepfake defenses, dark web monitoring, and federated SOC/CTI alliances for EU-wide threat modeling using ML.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com