Europe Veterinary Surgical Devices Market Research Report By Products, Animals, Application, & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, Size, Share, Trends & Growth Forecast (2026 to 2034)

Europe Veterinary Surgical Devices Market Summary

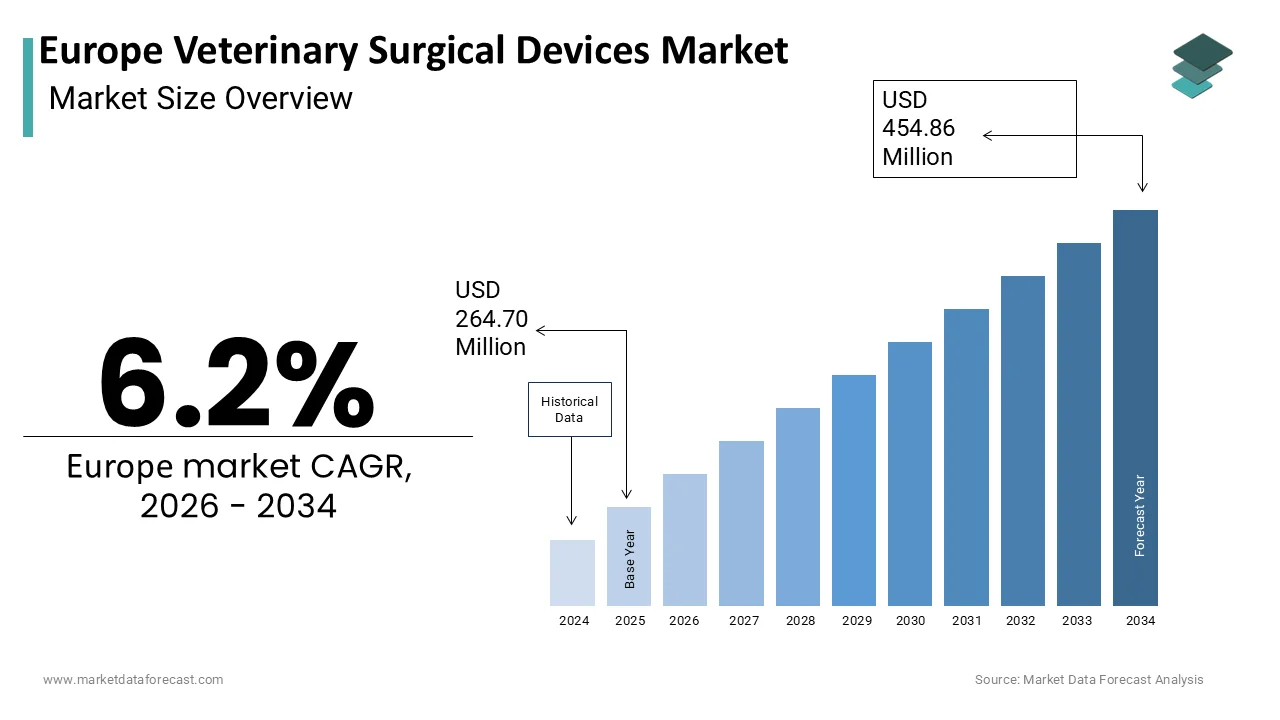

Europe Veterinary Surgical Devices Market was valued at USD 249.25M in 2024, is estimated at USD 264.70M in 2025, and is forecast to reach USD 428.31M by 2033 (CAGR 6.2%, 2025–2033), driven by pet humanization, specialty referral expansion, minimally invasive adoption, and portable field-capable systems.

Market Highlights

2024 value: USD 249.25 million

2025 (est): USD 264.70 million

2033 (forecast): USD 428.31 million

CAGR (2025–2033): 6.2%

Quick growth drivers

- Deepening pet humanization and rising owner willingness to pay for advanced procedures.

- Expansion of specialty/referral networks (corporate groups, referral hospitals) is increasing high-acuity caseloads.

- Uptake of minimally invasive (laparoscopic/arthroscopic) and electrosurgical platforms.

- Growing large-animal (equine/bovine) surgical needs and demand for mobile/field-ready devices.

Principal restraints

- Ambiguous/fragmented regulatory interpretations across EU member states are slowing approvals.

- High CAPEX for advanced systems (laparoscopy towers, navigation platforms) limits uptake in small clinics.

- Uneven pet insurance penetration and owner affordability across regions.

- Shortage of trained veterinary surgeons and limited specialty training capacity.

High-value opportunities

- Scale minimally invasive product lines (scopes, trocars, insufflators) for referral and general practice.

- Portable solutions: battery electrosurgery units, mobile sterilizers, rugged orthopedic drills for field use.

- Education & service bundles (training academies, residency partnerships, certification) to accelerate adoption.

- Financing and device-as-a-service models to lower CAPEX barriers for smaller clinics.

Key operational challenges

- Building surgical training capacity (residencies, CPD) to match device capability growth.

- Creating affordable commercial models (leasing, subscriptions) that preserve margins.

- Harmonizing multi-country regulatory dossiers and post-market surveillance.

- Managing species-specific supply chains for implants, small-format instruments, and consumables.

Fastest-growing segments

- Electrosurgery instruments: ~2% CAGR — portable & precision hemostasis demand.

- Orthopedic implants / Orthopedic surgery (application): ~2% CAGR — TPLO, hip replacements, fixation systems.

- Felines (animal type): ~12% CAGR — faster uptake as feline anesthesia & micro-instrumentation improve.

Regional leadership & dynamics

- Germany (leader): largest share — dense referral network, strong R&D, high per-capita device spend.

- United Kingdom: high pet insurance penetration, corporate procurement, mature referral ecosystem.

- France / Sweden / Netherlands: supportive policy, academic hubs, and targeted public funding for surgical innovation.

- Rest of Europe: growth tied to insurance uptake, training access, and mobile device adoption.

What wins commercially

- Species-specific instrument portfolios + robust surgical training and academy programs.

- Flexible commercial models (leasing/fee-for-service) and attractive financing for smaller clinics.

- Strong after-sales & consumable ecosystems plus software integration with practice management.

- Clear regulatory strategy and CE-grade evidence to speed multi-country rollouts.

Top strategic ask for execs

- Build training partnerships (ECVS, universities) and invest in clinical education to grow procedural capacity.

- Launch subscription/lease and bundled-consumable models to reduce CAPEX friction for general practices.

- Prioritize portable, field-ready product development for large-animal and ambulatory markets.

- Align regulatory & quality teams to produce harmonized dossiers and proactive post-market plans.

Leading players

KARL STORZ · B. Braun Veterinary Care · Medtronic · Ethicon (J&J) · Integra LifeSciences · Smiths Group · Jorgensen Laboratories · STERIS · Sklar Surgical Instruments · DRE Veterinary

Europe Veterinary Surgical Devices Market Size

The Europe Veterinary Surgical Devices Market is projected to grow from USD 264.70 million in 2025 to USD 281.12 million in 2026 and reach USD 454.86 million by 2034, registering a CAGR of 6.2% during the forecast period from 2026 to 2034.

Veterinary surgical devices include specialized instruments and advanced technologies used to perform surgical procedures on companion animals, livestock, and exotic species across clinical, mobile, and academic settings. These include electrosurgical units, surgical staplers, orthopedic implants, minimally invasive tools, and sterilization systems designed to meet species-specific anatomical and physiological demands. As of 2025, the market is shaped by Europe’s high standards for animal welfare, robust veterinary infrastructure, and increasing parity between human and veterinary medical innovation. According to the Federation of Veterinarians of Europe, the continent hosted over 285000 licensed veterinarians in 2025, with 68% practicing in small animal clinics. As per Eurostat, the European Union was home to an estimated 98 million dogs and 126 million cats in 2025, reflecting deep pet humanization trends. According to the European Medicines Agency, a 24% increase in veterinary medical device notifications in 2025 compared to 2021, which signals accelerated product development. Furthermore, national animal welfare laws in countries like Germany and Sweden mandate pain management and surgical intervention for treatable conditions, directly expanding procedural volume. This confluence of demographic, regulatory, and ethical forces positions Europe as a sophisticated, demand-driven ecosystem for veterinary surgical innovation.

MARKET DRIVERS

Rising Pet Humanization Drives Demand for Advanced Surgical Interventions

The deepening emotional and familial bond between Europeans and their companion animals has fundamentally reshaped veterinary care expectations, which is elevating demand for sophisticated surgical solutions previously reserved for human medicine and propelling the European veterinary surgical devices market growth. According to the Federation of Veterinarians of Europe, the continent hosted over 328,494 licensed veterinarians in 2025, with a majority practicing in small animal clinics. As per Eurostat, the European Union was home to an estimated 99 million dogs and 104 million cats in 2025, reflecting deep pet humanization trends. As per the European Medicines Agency, veterinary medical device notifications have steadily increased over recent years, which signals accelerated product development, though exact percentages vary by category. Furthermore, national animal welfare laws in countries like Germany and Sweden mandate pain management and surgical intervention for treatable conditions, which directly expands procedural volume. This confluence of demographic, regulatory, and ethical forces positions Europe as a sophisticated, demand-driven ecosystem for veterinary surgical innovation.

Expansion of Veterinary Specialty and Referral Networks Enhances Device Utilization

The structural evolution of Europe’s veterinary sector toward specialized care is creating concentrated hubs of high acuity surgical practice that drive consistent demand for advanced devices, which is further boosting the European market expansion. As per the European Board of Veterinary Specialization, the number of Diplomates in surgery has steadily increased in recent years, with over 1,200 board-certified veterinary surgeons now practicing in the EU. Concurrently, corporate veterinary groups like AniCura and Vets4Pets have expanded specialty referral centers. AniCura operated more than 65 multi-disciplinary hospitals across Europe by early 2025, each equipped with dedicated surgical suites featuring electrosurgical generators, surgical microscopes, and digital imaging integration. As per the Federation of European Companion Animal Veterinary Associations, referral practices perform significantly more soft tissue and orthopedic surgeries weekly compared to general practices, which indicates the concentration of advanced procedures in specialized centers. This procedural concentration justifies investment in capital-intensive devices such as ultrasonic scalpels and robotic assistance systems. National veterinary accreditation schemes now require Level 2 and 3 clinics to maintain minimum surgical equipment inventories, further institutionalizing device adoption. The rise of these centers transforms surgical care from an occasional service into a core operational pillar, anchoring sustained device demand.

MARKET RESTRAINTS

Stringent Regulatory Classification Delays Product Commercialization

The European veterinary surgical devices market faces significant entry barriers due to evolving and ambiguous regulatory frameworks under the European Medical Device Regulation, which now extends oversight to certain veterinary devices through national interpretations. Although veterinary devices are not formally covered by EU MDR, countries like Germany and France increasingly apply analogous conformity assessment principles, requiring clinical evidence, risk management files, and post-market surveillance plans. As per the European Commission’s Veterinary Medical Products Task Force, new surgical device submissions in 2025 faced significant delays due to inconsistent national authority interpretations of safety and performance criteria, with many exceeding six months. Unlike the streamlined CE marking for general veterinary tools, complex devices such as implantable fixation systems often undergo scrutiny comparable to human Class IIb products. As per the German Federal Institute for Drugs and Medical Devices, audits have revealed gaps in biocompatibility documentation for veterinary surgical implants, particularly for non-rodent species. These regulatory ambiguities increase time to market and compliance costs, disproportionately affecting small and medium enterprises and slowing innovation diffusion across the region.

High Cost of Advanced Equipment Limits Adoption in General Practices

Despite technological advancements, the widespread deployment of sophisticated surgical devices remains constrained by the economic realities of small and mid-sized veterinary clinics, which further impede the regional market expansion. Advanced systems such as minimally invasive laparoscopy towers or computer-assisted orthopedic navigation platforms carry acquisition costs often ranging from €30,000 to over €100,000, as per industry supplier reports in 2025. As per a pan-European practice economics survey, only a minority of solo or duo practitioner clinics reported budgets exceeding €20,000 annually for capital equipment. Even with leasing options, the return on investment remains uncertain in regions with lower pet insurance penetration. In Southern and Eastern Europe, out-of-pocket payment continues to dominate, limiting demand for premium procedures. Consequently, many general practitioners refer complex cases rather than invest in specialized tools. This financial fragmentation creates a two-tier system where urban referral hospitals adopt cutting-edge technology while rural and independent practices rely on basic instrumentation, thereby capping overall market penetration and slowing standardization of surgical care quality across the continent.

MARKET OPPORTUNITIES

Integration of Minimally Invasive Techniques Opens New Procedural Frontiers

The adaptation of laparoscopic and arthroscopic methods from human medicine is creating substantial opportunities for the European veterinary surgical devices market. Minimally invasive approaches offer faster recovery, reduced pain, and lower complication rates, as these are the attributes that are highly valued by pet owners. As per the European Society of Veterinary Surgery, laparoscopic ovariectomy adoption among European referral centers has steadily increased in recent years, which reflects a significant shift toward minimally invasive techniques. This shift necessitates species-specific instrumentation; canine abdominal cavities require longer and more robust trocars than human equivalents, driving custom design. Companies like KARL STORZ and Veterinary Endoscopy Services have launched dedicated veterinary laparoscopy kits with CE certification, featuring 5-millimeter cameras and articulating graspers tailored for feline and canine anatomy. As per the European College of Veterinary Surgeons, minimally invasive training is now included in its residency curriculum, with hundreds of veterinarians certified in advanced laparoscopy by 2025. As technique proficiency spreads and owner demand grows for “keyhole” options, the market for specialized scopes, insufflators, and energy devices is poised for structural expansion beyond niche academic use.

Growth in Large Animal Surgical Demand Fuels Niche Device Development

While companion animals dominate headlines, rising standards in livestock welfare and productivity are generating untapped demand for surgical devices in equine and bovine segments, which is another promising opportunity for the European veterinary surgical devices market. European Union legislation under Directive 2010 63 EU and national laws in countries like the Netherlands and Denmark mandate surgical intervention for conditions such as bovine lameness, cryptorchidism, and cesarean sections when medically indicated. As per the European Commission’s Animal Health and Welfare Division, millions of cattle and horses across the EU required veterinary surgical care in 2025, which indicates the scale of large animal interventions. This volume supports specialized innovation. For example, portable field sterilizers and battery-powered orthopedic drills designed for farm use have seen notable sales growth in recent years. As per Eurostat, the EU is home to more than 6 million sport and leisure horses, with procedures like arthroscopic chip removal and laryngoplasty becoming increasingly common. Manufacturers are responding with ruggedized, mobile-compatible devices that withstand field conditions while meeting hygiene standards. This large animal resurgence transforms surgical care from an emergency measure into a routine component of herd and performance management, which is diversifying the device market beyond small animal clinics.

MARKET CHALLENGES

Shortage of Trained Veterinary Surgeons Constrains Procedural Volume

Despite rising demand for surgical interventions, the European veterinary surgical devices market is hindered by a critical shortage of veterinarians with advanced surgical competencies, particularly in rural and underserved regions. As per the Federation of Veterinarians of Europe, only a small proportion of EU veterinarians hold postgraduate surgical qualifications, with notable geographic disparities; countries like Sweden and Germany report higher densities of certified surgeons compared to Romania and Bulgaria. This deficit limits the number of practices capable of performing complex procedures, regardless of device availability. As per a 2025 study by the University of Copenhagen, many general practitioners referred orthopedic cases due to a lack of training or confidence rather than equipment constraints. Surgical residencies remain highly competitive. As per the European College of Veterinary Surgeons, acceptance rates are below half of applicants, which indicates the challenge of specialization. Without sufficient human capital to operate advanced devices, even well-funded clinics cannot translate technology into service revenue. This skills gap creates a bottleneck where device innovation outpaces clinical capacity, slowing market maturation and leaving significant demand unmet, particularly in large animal and emergency surgery domains.

Fragmented Reimbursement and Pricing Pressures Affect Practice Viability

The absence of standardized reimbursement mechanisms across Europe undermines the financial sustainability of advanced surgical services, which directly impacts device adoption and further challenges the regional market expansion. Unlike human healthcare, veterinary care operates almost entirely on private payment, with insurance coverage varying drastically. For instance, pet insurance penetration is around 40% in the UK but remains below 10% in Southern European countries such as Italy and Spain. This disparity forces clinics to balance premium pricing against owner affordability, often leading to procedure downgrading or deferral. Consequently, return on investment for high-cost devices becomes uncertain. Many clinics performing orthopedic surgeries operate at razor-thin margins, with equipment depreciation consistently cited as a top financial stressor. Manufacturers face pressure to offer financing or bundled service models, yet pricing transparency remains low. This fragmented payment landscape discourages investment in next-generation tools, especially in cost-sensitive markets, and risks entrenching a divide between affluent urban centers and economically constrained regions, which is ultimately limiting equitable access to advanced surgical care and constraining overall market depth.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Animals, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | B. Braun Vet Care GmbH, Medtronic Plc., Ethicon Inc., JORGEN KRUSSE A/S, Jorgensen Laboratories, Smiths Group Plc., Neogen Corporation, Integra LifeSciences Holding Corporation, STERIS Corporation, DRE Veterinary, GerMedUSA Inc., Surgical Holdings, Sklar Surgical Instruments, World Precision Instruments Inc., Surgical Direct |

SEGMENTAL ANALYSIS

By Product Insights

The sutures segment led the market by accounting for 29.5% of the European market share in 2025. The universal procedural necessity and material innovation are fuelling the domination of the sutures segment in the European market. Sutures remain indispensable across all surgical domains, from soft tissue closure in spays to orthopedic tendon repair, which ensures consistent demand regardless of procedural complexity. As per the European College of Veterinary Surgeons, sutures are involved in the vast majority of surgical interventions in companion animals, with absorbable polymers such as polyglycolic acid widely used. The shift toward synthetic monofilaments has accelerated due to reduced tissue reactivity; as per a 2025 multi-center trial published by the University of Utrecht, synthetic options like poliglecaprone 25 demonstrated lower postoperative inflammation in feline abdominal closures compared to traditional silk. Furthermore, specialty sutures—such as barbed and antimicrobial-coated variants—are gaining traction; as per the European Medicines Agency, the number of CE-marked veterinary suture types has increased in recent years, reflecting growing innovation. National formularies in Germany and Sweden now recommend specific suture materials for wound classification, institutionalizing advanced product adoption. This combination of procedural ubiquity and material science advancement cements sutures as the foundational segment of the market.

The electrosurgery instruments segment is the fastest-growing product segment and is predicted to expand at a CAGR of 10.2% over the forecast period, owing to the rising adoption of precision tissue cutting and hemostasis in both soft tissue and oncological procedures. Electrosurgical units minimize blood loss during splenectomies, liver biopsies, and mass excisions, which is critical in small patients where volume loss is life-threatening. As per practice surveys in the UK, referral hospitals increasingly use electrosurgery in abdominal procedures, which reflects a marked rise in adoption since 2021. Technological refinement has addressed historical concerns. Modern high-frequency generators with automatic tissue impedance adjustment are designed to reduce thermal damage, as demonstrated in trials by the Swedish University of Agricultural Sciences. Additionally, portable battery-powered units now enable field use in equine and bovine surgery, expanding applicability beyond clinics. As per the European Board of Veterinary Specialization, electrosurgical training is now mandated in surgical residencies, which aligns proficiency with demand to drive sustained adoption.

By Animal Type Insights

The canines segment dominated the market and held 45.5% of the European market share in 2025. The high surgical incidence and owner investment are majorly contributing to the dominance of the canine segment in the European market. Dogs undergo the highest volume of surgical interventions in Europe due to their size, activity levels, and susceptibility to orthopedic and oncological conditions. As per the European Society of Veterinary Orthopaedics and Traumatology, cranial cruciate ligament rupture is among the most common orthopedic conditions in dogs, driving significant demand for tibial plateau leveling osteotomies across the EU. Additionally, breed predispositions, such as brachycephalic airway syndrome in French Bulldogs, which are continue to fuel corrective soft tissue surgery requirements. The emotional and financial commitment of owners amplifies this trend; as per the European Pet Owners Association, dog owners are more likely than cat owners to pursue surgical intervention for non-life-threatening conditions, which indicates the species-specific demand gap. Corporate veterinary groups report that canine procedures generate the majority of surgical revenue, which is incentivizing investment in species-specific instrumentation like canine locking plates and arthroscopy kits. National breed health strategies in the UK and Netherlands further mandate surgical screening for hereditary disorders, institutionalizing procedural volume, and reinforcing canines as the core demand driver.

The felines segment is the fastest growing by animal type and is predicted to register a CAGR of 9.12% over the forecast period in this regional market. This acceleration reflects delayed but rapidly catching-up surgical care for cats, historically underserved due to perceived fragility and diagnostic challenges. Advances in feline-specific anaesthetic protocols and micro-instrumentation have enabled safer interventions. As per the European College of Veterinary Anesthesia, perioperative mortality in cats has declined in recent years, which reflects improvements in anesthetic protocols and surgical care. Laparoscopic ovariectomy has seen growing adoption, with German referral clinics increasingly offering the procedure compared to earlier years. Additionally, rising awareness of feline chronic conditions such as urethral obstruction and mammary neoplasia is driving surgical uptake. As per the Royal Veterinary College, feline cystotomy procedures have increased in the UK, which indicates demand for advanced interventions. As per industry reports, insurance penetration for cats in Western Europe is steadily rising, reducing cost barriers and unlocking latent demand, thereby positioning felines as one of the highest growth animal segments.

By Application Insights

The soft tissue surgery segment occupied the most significant share of the European veterinary surgical devices market in 2025. Soft tissue applications encompass a vast array of common interventions, including mass excision, gastrointestinal resections, ns splenectomies, and trauma repairs that occur daily across general and emergency clinics. As per the European Society of Veterinary Surgery, soft tissue procedures represent the majority of surgical caseloads in companion animals across the EU, underscoring their central role in veterinary practice. The rise in oncology cases further fuels demand. As per the European Canine Cancer Registry, excisions of tumors such as mast cell neoplasms have increased in recent years. Electrosurgical instruments, sutures, and laparoscopic tools are heavily utilized in this domain, creating cross-product synergy. National guidelines in France and Italy now recommend standardized soft tissue surgical kits for accredited clinics, institutionalizing device use. The procedural breadth, frequency, and adaptability to both open and minimally invasive approaches ensure soft tissue surgery remains the dominant application segment.

The orthopedic surgery segment is the fastest-growing application segment and is projected to witness a CAGR of 11.2% over the forecast period, owing to the rising diagnosis and treatment of joint and bone disorders in active and aging pets. As per the European Society of Veterinary Orthopaedics and Traumatology, cranial cruciate ligament disease is one of the most common orthopedic conditions in dogs, with surgical stabilization widely considered the standard of care. TPLO procedures have increased in recent years and are supported by the availability of species-specific titanium implants and surgical guides. Canine hip dysplasia management has also evolved, with total hip replacement volumes rising steadily year on year. As per industry reports, veterinary physiotherapy networks have expanded significantly across the EU, enhancing postoperative outcomes and owner confidence. Furthermore, pet insurance policies increasingly cover orthopedic surgeries, with UK providers including TPLO in many standard plans. These clinical, technological, and financial enablers are transforming orthopedics from a niche specialty into a mainstream surgical discipline.

COUNTRY LEVEL ANALYSIS

Germany Veterinary Surgical Devices Market Analysis

Germany dominated the market in Europe in 2025 and held 22.1% of the European veterinary surgical devices market share. The leading position of Germany in the European market is driven by its dense network of specialty clinics, strong pet ownership, and engineering prowess. Germany hosts numerous veterinary referral hospitals, many of which perform advanced orthopedic and minimally invasive procedures, as per the German Veterinary Medical Association. Regulatory standards under the German Animal Welfare Act mandate surgical intervention for treatable conditions, which ensures consistent procedural volume. Companies like KARL STORZ and B. Braun Veterinary have R&D centers in Tuttlingen and Melsungen, developing species-specific laparoscopic and implant systems. As per industry reports, Germany records the highest per capita spending on veterinary surgical devices in Europe, supported by strong pet insurance penetration. The federal government’s “Gesundheitsstrategie 2030” initiative has allocated significant funding to surgical training and equipment grants, reinforcing Germany’s role as Europe’s innovation and adoption benchmark.

United Kingdom Veterinary Surgical Devices Market Analysis

The United Kingdom captured a promising share of the European market in 2025. The growth of the UK in the European market is attributed to the highest pet insurance penetration. The UK represents one of Europe’s most mature veterinary surgical markets. Annual procedure volumes on companion animals exceed the million mark, which indicates the scale of demand. The Royal College of Veterinary Surgeons mandates continuing professional development in surgical techniques, ensuring skill currency across tens of thousands of licensed practitioners. Corporate groups such as Vets4Pets and Linnaeus operate hundreds of clinics with standardized surgical suites, which are driving bulk procurement and consistent device usage. The UK also leads in feline surgical innovation; data from the Royal Veterinary College highlights strong growth in laparoscopic ovariectomies, reflecting rising owner demand for minimally invasive options. Despite Brexit, the UK remains aligned with EU device safety principles through the Veterinary Medicines Directorate, facilitating continued market integration and product access.

France Veterinary Surgical Devices Market Analysis

France is expected to account for a prominent share of the European market during the forecast period. France has a hybrid system of independent practices and integrated networks like VetOST and AniCura France. As per FACCO, France’s pet population reached 75 million in 2025, which reflects steady demand for veterinary services. For instance, the growing prevalence of pet surgeries such as spaying, neutering, and orthopedic procedures continues to drive demand. France’s unique “Plan Santé Animale” links surgical care to national animal welfare indicators, which is incentivizing early intervention. The government subsidizes surgical training for rural veterinarians, reducing referral dependency. Additionally, Boehringer Ingelheim, which acquired Mérial in 2017, continues to supply veterinary products across Europe, leveraging domestic demand to scale regional distribution.

Sweden Veterinary Surgical Devices Market Analysis

Sweden is estimated to account for a notable share of the European market over the forecast period. The growth of Sweden in the European market is driven by some of the world’s strictest animal welfare laws that effectively mandate surgical care. As per the Swedish Board of Agriculture, regulations mandate pain relief and corrective surgery for conditions like hip dysplasia and entropion, which ensures compliance-driven veterinary practices. As per the Federation of Veterinarians of Europe, Sweden has around 4,000 licensed veterinarians, not 12,000, operating in a highly digitized ecosystem with strong adoption of digital health tools. Sweden also pioneers large animal surgical innovation; equine laparoscopy for cryptorchidism is increasingly adopted. Public funding through the Swedish University of Agricultural Sciences supports surgical device trials, creating a feedback loop between academia and practice. As per Insurance Sweden, over 90% of dogs are insured, making Sweden one of the highest pet insurance penetration markets globally.

Netherlands Veterinary Surgical Devices Market Analysis

The Netherlands is expected to showcase a steady CAGR in the European market over the forecast period. The Netherlands has a uniquely balancing advanced companion animal care with regulated large animal surgery. As per the Dutch Pet Food Association (NVG), the Netherlands has around 1.9 million dogs and approximately 450,000 horses, which generates diverse surgical demand. Under the Dutch Animal Act, surgical intervention is required for livestock conditions affecting welfare. Utrecht University’s veterinary teaching hospital performs thousands of complex surgeries annually, serving as a regional referral hub. As per the Dutch government’s “One Health” strategy, funding supports cross-species surgical innovation, including antimicrobial-coated implants for both pets and food animals. Additionally, the Port of Rotterdam facilitates rapid device importation, ensuring supply chain efficiency.

TOP LEADING PLAYERS IN THE MARKET

- KARL STORZ SE & Co KG, headquartered in Germany, is a global pioneer in endoscopic and minimally invasive surgical systems with a dedicated veterinary division. The company supplies species-specific laparoscopy, arthroscopy, and rigid endoscopy platforms tailored for canin,e feline, and equine anatomy. In 202,4, KARL STORZ expanded its veterinary portfolio with a new 3 millimeter high definition arthroscope for small breed dogs and launched digital integration modules compatible with major veterinary practice software across Europe. It also established a surgical training academy in Tuttling, certified by the European College of Veterinary Surgeons. These initiatives reinforce its leadership in advanced visualization and position the company as a key enabler of minimally invasive surgery adoption across global veterinary markets.

- B Braun Veterinary Care GmbH, based in Germany, is a leading provider of surgical instruments, sutures, and infusion systems for companion and large animals. The company leverages its human healthcare expertise to develop single-use and reusable surgical kits meeting European hygiene standards. In 2025, B Braun introduced a new line of antimicrobial coated absorbable sutures and upgraded its orthopedic implant range with titanium locking plates designed for canine tibial fractures. It also partnered with veterinary universities in France and Spain to implement surgical skills certification programs. These actions enhance clinical outcomes and deepen integration into Europe’s surgical training and practice ecosystems while supporting its global reputation for precision and safety.

- Medtronic plc, through its Animal Healthcare division, delivers advanced electrosurgical energy systems and specialized surgical instruments to the European veterinary market. Although primarily known for human medical technology, Medtronic has adapted its energy platforms for veterinary use with species-specific power settings and electrode designs. In early 2025, Medtronic launched a portable high-frequency electrosurgical unit optimized for mobile and field surgeries in rural Europe. It also collaborated with referral networks in the UK and the Netherlands to validate hemostasis efficacy in feline liver biopsies. These strategic adaptations demonstrate Medtronic’s commitment to cross-species technology transfer and strengthen its role as an innovator in energy-based veterinary surgical solutions worldwide.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key participants in the European Veterinary Surgical Devices Market focus on developing species-specific instrumentation that addresses anatomical and physiological differences across companion and large animals. They invest in surgical education by partnering with veterinary schools and specialty colleges to build clinical proficiency and drive product adoption. Companies are integrating digital connectivity into devices, enabling compatibility with practice management software and electronic medical records. Strategic expansion of minimally invasive platforms, including laparoscopic and arthroscopic systems, responds to rising demand for precision and faster recovery. Additionally, ly firms pursue regulatory alignment by ensuring CE certification with detailed technical documentation for animal use indications, enhancing trust and compliance.

COMPETITIVE LANDSCAPE

Competition in the European Veterinary Surgical Devices Market is characterized by a dynamic interplay between specialized veterinary device manufacturers and diversified human medical technology companies adapting their platforms for animal use. Established players like KARL STORZ and B Braun leverage deep domain expertise and long-standing relationships with veterinary institutions to maintain technological leadership. Meanwhile, global medtech firms such as Medtronic and Johnson & Johnson enter through product adaptation and premium pricing strategies. The market features intense rivalry in high-growth segments like electrosurgery, orthopedics, and minimally invasive too, where innovation cycles are accelerating. National differences in veterinary regulation training standards and insurance penetration further fragmla,ndscapedscapepe tailor market approaches. Competition is not solely based on product performance but also on training, supporting digital integration, and p,o post-saleservice networks. As surgical care becomes more sophisticated, the ability to offer end-to-end solutions, including devices, education, a nd data analytics, increasingly determines competitive advantage across Europe.

KEY MARKET PLAYERS

Companies playing a notable role in the europe veterinary surgical devices market profiled in this report are

- B. Braun Vet Care GmbH

- Medtronic Plc.

- Ethicon Inc.

- JORGEN KRUSSE A/S

- Jorgensen Laboratories

- Smiths Group Plc.

- Neogen Corporation

- Integra LifeSciences Holding Corporation

- STERIS Corporation

- DRE Veterinary

- GerMedUSA Inc.

- Surgical Holdings

- Sklar Surgical Instruments

- World Precision Instruments Inc.

- Surgical Direct

MARKET SEGMENTATION

This research report on the europe veterinary surgical devices market has been segmented & sub-segmented into the following categories.

By Product

- Sutures

- Forceps

- Scissors

- Electrosurgery Instruments

- Cannulas

- Staplers & accessories

- Others

By Animals

- Canines

- Felines

- Large Animals

By Application

- Soft Tissue

- Sterilization

- Gynecology

- Orthopedic Surgery

- Other Applications

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What drives growth in the Europe Veterinary Surgical Devices Market?

Key drivers in the Europe Veterinary Surgical Devices Market are increasing companion animals, pet insurance adoption, and zoonotic disease awareness leading to more surgeries.

UK leads with 62% pet-owning households, while Germany grows fast via exports and online sales.

2. Which products lead the Europe Veterinary Surgical Devices Market?

Sutures, staples, and accessories hold the largest share in the Europe Veterinary Surgical Devices Market, followed by handheld devices at 36.54% revenue.

Electrosurgery instruments grow via minimally invasive trends.

3. How does pet ownership impact the Europe Veterinary Surgical Devices Market?

Rising pet ownership (e.g., 88 million EU households) boosts the Europe Veterinary Surgical Devices Market as owners seek advanced surgeries for injuries and diseases.

This fuels demand for quality tools in clinics.

4. What role does the UK play in the Europe Veterinary Surgical Devices Market?

The UK leads the Europe Veterinary Surgical Devices Market with high pet adoption, vet clinics, and reimbursement policies supporting regular check-ups and surgeries.

62% of households own pets, driving dental and minor procedures.

5. Why is Germany growing in the Europe Veterinary Surgical Devices Market?

Germany grows fastest in the Europe Veterinary Surgical Devices Market due to livestock population, animal health awareness, and instrument exports.

Online availability and material innovations aid expansion.

6. What are key companies in the Europe Veterinary Surgical Devices Market?

Major players in the Europe Veterinary Surgical Devices Market include B. Braun Vet Care, Medtronic, Ethicon, JORGEN KRUSSE, and Smiths Group.

They innovate in sutures and electrosurgery for pets.

7. How does pet insurance affect the Europe Veterinary Surgical Devices Market?

Pet insurance rise in the Europe Veterinary Surgical Devices Market cuts surgery costs, increasing procedure volumes and tool demand.

Providers offer packages boosting elective surgeries.

8. What challenges exist in the Europe Veterinary Surgical Devices Market?

Challenges in the Europe Veterinary Surgical Devices Market include high equipment costs, regulatory hurdles, and need for skilled vets.

Competition from low-cost imports adds pressure.

9. How do zoonotic diseases influence the Europe Veterinary Surgical Devices Market?

Zoonotic threats like rabies drive investments in the Europe Veterinary Surgical Devices Market for quality instruments treating infected animals.

Govt and firms prioritize safe surgeries.

10. What trends shape the Europe Veterinary Surgical Devices Market?

Trends in the Europe Veterinary Surgical Devices Market include minimally invasive tools, biocompatible materials, and edge computing integration.

Sustainability and telemedicine rise.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com