Europe Veterinary Healthcare Market Research Report – Segmented By Animal Type (Livestock Animals, Companion Animals), Product , End-User and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis From 2025 to 2033

Europe Veterinary Healthcare Market Size

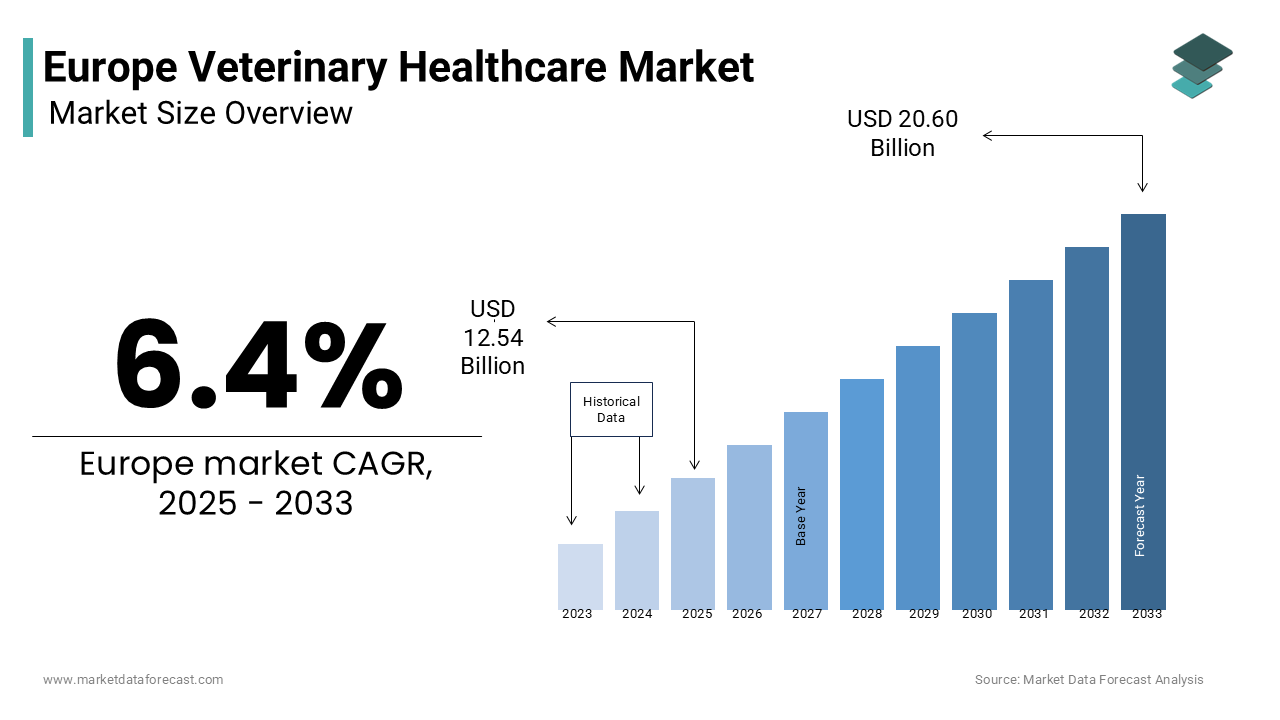

The europe veterinary healthcare market size was valued at USD 11.79 billion in 2024. The size of the market is expected to be worth USD 12.54 billion in 2025 and USD 20.60 billion by 2033, growing at a CAGR of 6.4% from 2025 to 2033.

The Europe animal healthcare market has a broad array of products and services aimed at diagnosing, treating, and preventing diseases in livestock, companion animals, and aquaculture. It includes pharmaceuticals such as vaccines, parasiticides, antibiotics, and biologics, along with veterinary diagnostics, digital health solutions, and nutritional supplements. The market is shaped by stringent regulatory frameworks, rising pet ownership, growing awareness about zoonotic diseases, and increasing investment in agricultural productivity.

This surge in pet adoption has directly fueled demand for premium veterinary care and preventive treatments. In the livestock sector, the European Food Safety Authority (EFSA) notes a steady increase in disease monitoring programs across major meat-producing nations such as Spain, Poland, and the Netherlands. With outbreaks of African swine fever and avian influenza posing persistent threats, there is heightened emphasis on biosecurity and prophylactic interventions.

Moreover, the rise in veterinary telemedicine and digital monitoring tools endorsed by organizations such as the Federation of Veterinarians of Europe (FVE) is transforming how animal health is managed.

MARKET DRIVERS

Rising Pet Ownership and Humanization of Pets

One of the most significant drivers of the Europe animal healthcare market is the growing trend of pet humanization, where pets are increasingly viewed as family members rather than just animals. This shift in perception has led to increased spending on pet wellness, preventive care, and premium veterinary services. According to the European Pet Food Industry Federation (FEDIAF), over 80 million households in Europe owned at least one pet in 2023, with dog and cat ownership experiencing the highest growth. This behavioral change has spurred demand for high-quality pet food, advanced diagnostic services, and specialized medications. The UK’s Companion Animal Health Report 2023 highlighted that pet owners spent an average of €1,200 per year on veterinary care alone, up from €900 in 2020. Furthermore, the availability of pet insurance has facilitated access to premium healthcare options.

Increasing Incidence of Zoonotic and Livestock Diseases

Another key driver influencing the Europe animal healthcare market is the rising incidence of zoonotic and livestock diseases, necessitating stronger veterinary interventions and preventive measures. Outbreaks of diseases such as avian influenza, foot-and-mouth disease, and African swine fever have become more frequent in recent years, prompting governments and farmers to invest heavily in animal health management strategies. As reported by the European Centre for Disease Prevention and Control (ECDC) in 2023, Europe experienced one of its largest avian flu outbreaks, affecting over 25 countries and resulting in the culling of millions of poultry birds. This led to a surge in vaccine procurement and biosecurity investments, particularly in France, the Netherlands, and Hungary. Similarly, the European Food Safety Authority (EFSA) documented a significant increase in reported cases of bovine tuberculosis between 2020 and 2023, primarily in Ireland and the UK. To mitigate these risks, national agricultural departments have intensified surveillance programs and vaccination campaigns. For instance, the German Federal Ministry of Food and Agriculture allocated additional funding in 2023 to strengthen early warning systems and support rapid response mechanisms for livestock disease control.

MARKET RESTRAINTS

Regulatory Stringency and Antibiotic Use Restrictions

A significant restraint affecting the Europe animal healthcare market is the stringent regulatory environment governing the use of antibiotics and other pharmaceutical agents in veterinary medicine. The European Medicines Agency (EMA) has implemented strict guidelines to curb antimicrobial resistance (AMR), limiting the availability and application of certain drugs in both livestock and companion animal treatment. As part of the EU One Health Action Plan against Antimicrobial Resistance, several member states have imposed mandatory reductions in veterinary antibiotic usage. While this initiative supports public health goals, it also restricts treatment options available to veterinarians, particularly in managing bacterial infections in farm animals. Moreover, compliance with EMA regulations requires extensive documentation, clinical trials, and approval processes, delaying the introduction of new veterinary medicines.

High Cost of Advanced Veterinary Treatments

The escalating cost of advanced veterinary treatments is another critical factor restraining the growth of the Europe animal healthcare market. As medical technologies evolve, so does the price of diagnostics, surgical procedures, and specialty pharmaceuticals, making them less accessible to small-scale farmers and budget-conscious pet owners. Similarly, in the livestock sector, the adoption of precision animal health monitoring systems and automated vaccination equipment remains limited among small and medium-sized farms due to high initial investment costs. These financial barriers hinder widespread adoption of cutting-edge veterinary solutions, particularly in economically constrained regions.

MARKET OPPORTUNITIES

Expansion of Digital and Telemedicine Solutions in Veterinary Care

A promising opportunity emerging in the Europe animal healthcare market is the rapid expansion of digital and telemedicine solutions designed to improve access, efficiency, and monitoring of veterinary services. Driven by advancements in artificial intelligence, remote diagnostics, and mobile connectivity, these technologies are reshaping how animal health is managed across both urban and rural settings. According to the Federation of Veterinarians of Europe (FVE), a large share of veterinary clinics in Germany and the Netherlands have adopted teleconsultation platforms since 2021, allowing pet owners to seek professional advice without in-person visits. In the UK, the Royal College of Veterinary Surgeons (RCVS) reported a key increase in virtual consultations between 2022 and 2023, indicating a structural shift in service delivery. Additionally, wearable devices and IoT-enabled monitoring tools are gaining traction in livestock management. The European Innovation Partnership for Agricultural Productivity and Sustainability (EIP-AGRI) highlights that smart collars and activity trackers are now deployed on over 20% of dairy farms in France and Denmark to detect early signs of illness and optimize breeding cycles.

Growth in Alternative Protein Sources and Associated Animal Health Needs

The emergence and expansion of alternative protein sources—including insect-based feed, plant proteins, and cultured meat—are creating new opportunities within the Europe animal healthcare market. As the livestock industry seeks sustainable feeding solutions, the health implications of novel feedstocks on farmed animals are becoming a focal point for research and product development. According to the European Feed Manufacturers’ Federation (FEFANA), insect meal and algae-based feeds have gained regulatory approval in several EU countries, with production capacity expected to triple by 2026. However, the transition to unconventional diets has introduced unique digestive and immune challenges in poultry and swine, necessitating tailored nutritional supplements and probiotics to maintain optimal health. Moreover, the rise of cellular agriculture has prompted interest in biopharmaceuticals that support cell culture viability and disease resistance in lab-grown meat production.

MARKET CHALLENGES

Fragmented Regulatory Landscape Across EU Member States

A major challenge confronting the Europe animal healthcare market is the fragmented regulatory landscape across EU member states, which complicates market entry, product approvals, and pricing strategies for manufacturers. Although the European Medicines Agency (EMA) provides overarching guidelines, individual countries maintain distinct authorization processes, reimbursement policies, and labeling requirements. According to the European Animal Health Association (EPRUMA), differences in national veterinary drug registration timelines can delay product launches several months in some markets. Such discrepancies create inefficiencies and increase operational complexity for multinational companies. Additionally, disparities in pricing and reimbursement mechanisms further exacerbate market fragmentation. These inconsistencies hinder standardization efforts and slow down the adoption of innovative therapies across the region. Addressing this challenge requires greater harmonization of regulatory frameworks under EU coordination, enabling smoother cross-border commercialization and ensuring equitable access to essential animal healthcare products throughout Europe.

Growing Consumer Skepticism Toward Chemical-Based Veterinary Products

An emerging challenge in the Europe animal healthcare market is the increasing skepticism among consumers regarding chemical-based veterinary products, including antibiotics, dewormers, and synthetic growth promoters. Heightened awareness of environmental impact, food safety, and ethical farming practices has led to a shift toward natural and organic alternatives, pressuring pharmaceutical companies to reformulate or justify existing product lines. This sentiment is particularly strong in Nordic countries, where organic farming standards are more rigorous, and consumer trust in chemical interventions is lower. In response, several retailers have imposed restrictions on sourcing from farms using specific veterinary drugs. While this trend promotes sustainable practices, it also creates commercial pressure on traditional pharmaceutical firms to innovate rapidly or risk losing market share. Companies must balance efficacy with consumer expectations, all while maintaining regulatory compliance and ensuring animal welfare remains uncompromised.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Animal Type, Product, End-User, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, and the Czech Republic, |

| Market Leader Profiled | Merck & Co., Inc., Bayer AG, Boehringer Ingelheim GmbH, Cargill, Inc., Ceva Santé Animale, Novasep, Eli Lilly and Company, Koninklijke DSM N.V., Novartis AG, Nutreco N.V., Sanofi S.A., SeQuent Scientific Ltd., Virbac S.A., Vétoquinol S.A., and Zoetis Inc. |

SEGMENTAL ANALYSIS

By Product Insights

Pharmaceuticals represented the biggest segment in the Europe animal healthcare market by accounting for 45% of the total market share in 2024. This dominance is primarily driven by the widespread use of antibiotics, antiparasitics, and anti-inflammatory drugs in both livestock and companion animals. Although regulatory efforts are curbing excessive antibiotic use, demand remains strong for alternative pharmaceutical interventions such as probiotics and immune modulators. Additionally, chronic conditions in pets such as diabetes, arthritis, and kidney disease are on the rise, fueling the need for long-term medication. The pharmaceutical segment also benefits from a robust pipeline of new drug approvals. The European Medicines Agency (EMA) reported that in 2023 alone, it approved over 30 new veterinary pharmaceutical products, reflecting ongoing innovation and investment by major players such as Boehringer Ingelheim and Elanco.

Veterinary services have emerged as the fastest-growing segment within the Europe animal healthcare market, registering a CAGR of 6.7%. This progress is fueled by rising pet ownership, increased consumer spending on premium veterinary care, and the expansion of digital consultation platforms. As pet owners become more health-conscious, there has been a surge in demand for preventive check-ups, dental care, and specialized treatments. Moreover, telemedicine adoption has transformed service delivery models. According to the Federation of Veterinarians of Europe (FVE), more than 60% of veterinary clinics in the Netherlands and Germany integrated remote consultation tools into their practice by 2023, improving access to expert advice and enhancing client engagement. Insurance coverage has further supported this trend, particularly in Sweden, where pet insurance penetration.

By Animal Type Insights

The livestock animals dominated the Europe animal healthcare market by capturing 52.6% of the total market share in 2024. This leading position is attributed to the continent’s significant agricultural output, stringent food safety regulations, and the critical role of livestock in economic stability and food security. The European Commission reported that in 2023, the EU produced over 45 million metric tons of meat annually, requiring extensive veterinary oversight to prevent disease outbreaks and ensure productivity. Countries such as Spain, Germany, and France lead in pig and cattle farming, driving high demand for vaccines, parasiticides, and feed additives. Disease prevention remains a top priority, particularly in light of recurring threats such as African swine fever and avian influenza. Furthermore, advancements in precision livestock farming, including automated health monitoring systems and wearable sensors, have expanded the scope of veterinary interventions. The European Innovation Partnership for Agricultural Productivity and Sustainability (EIP-AGRI) estimates that over 30% of large-scale farms in Northern Europe now employ digital diagnostics, enhancing early disease detection and treatment efficiency.

Companion animals represent the quickly expanding segment in the Europe animal healthcare market, recording a CAGR of 6.9% from 2025 to 2033. This accelerated growth is primarily driven by rising pet ownership, increasing disposable incomes, and shifting attitudes toward pet wellness. According to the study, pet ownership rates in Western Europe have surpassed 25%, with urban populations showing a strong preference for dogs and cats. This trend has directly influenced spending patterns, with pet owners increasingly investing in premium nutrition, preventive treatments, and advanced diagnostics. Pet insurance penetration has also played a crucial role in sustaining demand. In Sweden, as per the Swedish Insurance Association, financial barriers to expensive treatments are significantly reduced. Also, the expansion of veterinary teleconsultation services has improved accessibility, especially in rural areas, further propelling market growth in the companion animal sector.

By End-Use Insights

The hospitals and clinics constitute the largest end-use segment in the Europe animal healthcare market by commanding 58.5% of total market share in 2024. This is associated with the increasing availability of specialized veterinary facilities, higher adoption of diagnostic imaging and surgical procedures, and growing pet owner willingness to invest in advanced treatments. The European College of Veterinary Surgeons (ECVS) reports that in 2023, over 2,500 certified veterinary specialists were practicing across the continent, with concentrations in Germany, France, and the United Kingdom. Moreover, government support for veterinary infrastructure development has been instrumental in expanding hospital networks. This investment has enhanced diagnostic capabilities and improved patient outcomes. Also, partnerships between academic institutions and private veterinary chains have facilitated knowledge exchange and technological integration. The University of Edinburgh's Royal (Dick) School of Veterinary Studies reported a key increase in collaborative research initiatives with clinical partners in 2023, underscoring the sector’s dynamic evolution and sustained leadership in the animal healthcare landscape.

Point-of-care and in-house testing is the fastest-growing end-use segment in the Europe animal healthcare market, exhibiting a CAGR of 7.4%. This progress is driven by the increasing need for rapid diagnostics, rising adoption of portable testing devices, and the convenience they offer in clinical and field settings. The European Society of Veterinary Clinical Pathology (ESVCP) highlights that a large portion of small animal clinics in Germany and the Netherlands utilize in-house analyzers for blood chemistry, urinalysis, and infectious disease screening. This shift reduces reliance on external laboratories and accelerates decision-making in critical cases. In livestock management, mobile diagnostic kits have gained traction for on-farm disease detection. The European Food Safety Authority (EFSA) observed a key rise in the use of lateral flow assays for detecting pathogens such as Salmonella and E. coli among dairy and poultry farms in Poland and Hungary between 2021 and 2023. Moreover, the integration of digital platforms with point-of-care devices has enabled real-time data tracking and remote monitoring. Also, cloud-connected diagnostic tools are being adopted by an increasing number of veterinary practices to improve record-keeping and facilitate teleconsultations, further boosting the segment’s momentum.

REGIONAL ANALYSIS

Germany had the leading position in the Europe animal healthcare market by contributing 18.5% of the total market share in 2024. The country’s robust veterinary pharmaceutical industry, strong pet ownership base, and advanced agricultural sector collectively drive demand for animal healthcare solutions. This high pet density supports a thriving market for premium veterinary medicines, diagnostics, and services. Also, Germany’s pharmaceutical companies, including Bayer Animal Health and Boehringer Ingelheim, play a central role in shaping product innovation and distribution. In the livestock sector, the Federal Ministry of Food and Agriculture (BMEL) reported that in 2023, over 26 million pigs and 14 million cattle were housed across the country, necessitating continuous investments in disease prevention and herd health management. The prevalence of zoonotic diseases and biosecurity concerns has further reinforced the need for vaccinations and antimicrobial alternatives. Moreover, Germany leads in veterinary education and research, with institutions such as the University of Berlin and Ludwig Maximilian University offering specialized training and fostering collaboration between academia and industry.

France remained a key player in the European animal healthcare market in 2024. The country benefits from a well-developed veterinary pharmaceutical sector, a strong presence of multinational manufacturers, and a growing emphasis on pet wellness and livestock health. This shift has led to increased demand for feline-specific medications and diagnostics, prompting pharmaceutical firms to tailor their offerings accordingly. On the agricultural front, the French Ministry of Agriculture (MAA) reported that the country maintained its status as one of Europe’s top producers of beef, pork, and dairy products. It is also a hub for veterinary biotech innovation, with companies like Ceva Santé Animale investing heavily in R&D for next-generation vaccines and digital health solutions. The French National Institute for Agricultural Research (INRA) collaborates closely with industry stakeholders to advance sustainable animal health practices, reinforcing France’s competitive edge in the regional market.

The United Kingdom maintains a prominent role in the Europe animal healthcare market, holding 13% of the total market share in 2023. Despite Brexit-related trade adjustments, the UK continues to be a key player due to its high pet ownership rates, advanced veterinary infrastructure, and progressive regulatory environment. Pet insurance coverage is high, facilitating greater access to premium diagnostics and specialist treatments. In livestock, the UK in 2023 managed over 9 million cattle and 4.5 million sheep, necessitating consistent veterinary oversight to manage disease risks such as bovine tuberculosis and footrot in sheep. Apart from these, the UK leads in veterinary telemedicine adoption, with platforms like Vets Now and Medivet integrating AI-powered diagnostics into daily operations. The Royal College of Veterinary Surgeons (RCVS) supports innovation through regulatory reforms, ensuring the UK remains a forward-looking market despite post-Brexit uncertainties.

The Netherlands contributed majorly to the Europe animal healthcare market, driven by its intensive livestock production, strong export-oriented agriculture, and high adoption of digital veterinary technologies. This concentration necessitates rigorous disease control measures, particularly against pathogens like Porcine Reproductive and Respiratory Syndrome (PRRS) and mastitis in dairy herds. Moreover, the Netherlands leads in smart animal health solutions, with companies like MSD Animal Health and Nutreco investing in IoT-enabled monitoring systems.

Spain accounted for a key share of the Europe animal healthcare market, supported by a substantial livestock population, growing pet ownership, and increasing government focus on animal welfare standards. Disease outbreaks, particularly African swine fever and avian flu, have prompted increased vaccination and biosecurity expenditures. Spain has also embraced digital transformation in animal health, with startups like VetPlus developing cloud-based clinic management tools. Additionally, the Spanish Agency for Medicines and Health Products (AEMPS) has streamlined veterinary drug approval processes, encouraging market entry of innovative therapies and supporting overall market growth.

COMPETITIVE LANDSCAPE

The competition in the Europe animal healthcare market is highly dynamic, shaped by the presence of global pharmaceutical giants, specialized biotech firms, and a growing number of digital health innovators. Established multinational companies dominate due to their extensive R&D capabilities, robust distribution networks, and strong brand recognition. However, smaller niche players are gaining traction by focusing on targeted therapies, alternative medicines, and digital veterinary tools that cater to evolving consumer demands.

Market participants face continuous pressure to innovate amid rising concerns over antimicrobial resistance, stricter regulatory frameworks, and increasing demand for ethical and sustainable practices. Companies must also navigate varying national policies, reimbursement structures, and pricing mechanisms across EU member states, which can hinder uniform market expansion. Additionally, the convergence of human and animal health, known as One Health, is influencing product development strategies, pushing firms to align with broader public health goals. As the market evolves, differentiation through technology, customization, and sustainability will be crucial in maintaining competitive advantage.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the europe veterinary healthcare market include

- Merck & Co., Inc.

- Bayer AG

- Boehringer Ingelheim GmbH

- Cargill, Inc.

- Ceva Santé Animale

- Novasep

- Eli Lilly and Company

- Koninklijke DSM N.V.

- Novartis AG

- Nutreco N.V.

- Sanofi S.A.

- SeQuent Scientific Ltd.

- Virbac S.A.

- Vétoquinol S.A.

- Zoetis Inc.

Top Players in the Europe Veterinary Healthcare Market

Boehringer Ingelheim Animal Health

Boehringer Ingelheim is a global leader in animal healthcare, with a strong presence across Europe. The company offers a comprehensive portfolio of products, including vaccines, parasiticides, and diagnostics for both livestock and companion animals. In Europe, Boehringer Ingelheim plays a pivotal role in disease prevention and control, particularly through its innovative vaccine development programs. Its commitment to research and sustainable farming solutions has made it a trusted partner for veterinarians, farmers, and pet owners alike.

Ceva Santé Animale

Ceva Santé Animale is a major European-based player that has significantly influenced the regional animal healthcare landscape. Known for its focus on innovation and alternative health solutions, Ceva develops advanced vaccines, biologics, and digital tools tailored to meet evolving animal health needs. The company actively collaborates with academic institutions and industry stakeholders to drive forward-thinking approaches in disease management and animal welfare, strengthening its footprint across Europe’s diverse veterinary markets.

Elanco Animal Health

Elanco is a key contributor to the Europe animal healthcare market, offering a broad range of pharmaceuticals, nutritional supplements, and digital health solutions. With deep-rooted partnerships across the agricultural and companion animal sectors, Elanco supports farmers and veterinary professionals in enhancing productivity and animal well-being. The company emphasizes sustainability and responsible medicine use, aligning with European regulatory expectations while advancing therapeutic innovation for both food-producing and companion animals.

Top Strategies Used by Key Players

One of the primary strategies employed by leading players in the Europe animal healthcare market is product innovation and pipeline expansion. Companies are investing heavily in R&D to develop next-generation vaccines, biologics, and digital diagnostics that address emerging diseases and evolving consumer preferences for safer, more sustainable treatments.

Another key approach is strategic collaborations and partnerships, particularly with research institutions, biotech firms, and digital health startups. These alliances enable faster commercialization of novel therapies and support the integration of precision medicine into veterinary care, enhancing treatment efficacy and operational efficiency.

Lastly, market localization and tailored product offerings have become increasingly important. Firms are adapting their portfolios to meet specific regional needs, whether in livestock disease prevention or companion animal wellness, ensuring compliance with local regulations and aligning with cultural and economic conditions across different European markets.

RECENT MARKET DEVELOPMENTS

- In March 2024, Boehringer Ingelheim launched a new line of digital health monitoring tools designed specifically for dairy farms, aiming to enhance early disease detection and improve herd management efficiency across Western Europe.

- In July 2024, Ceva Santé Animale partnered with a French biotech startup specializing in mRNA vaccine platforms to accelerate the development of next-generation veterinary immunizations, strengthening its position in innovative disease prevention.

- In October 2024, Elanco Animal Health introduced a new range of plant-based pet supplements targeting digestive and joint health, aligning with the growing consumer preference for natural and clean-label ingredients in pet nutrition.

- In December 2024, Zoetis expanded its veterinary telehealth services by acquiring a German digital diagnostics platform, enabling real-time remote consultations and diagnostic support for small animal practitioners across Central Europe.

- In February 2025, MSD Animal Health announced a strategic collaboration with a Dutch agritech firm to integrate AI-driven analytics into livestock health monitoring systems, enhancing predictive disease management and supporting sustainable farming practices.

MARKET SEGMENTATION

This research report on the europe veterinary healthcare market has been segmented and sub-segmented into the following categories.

By Animal Type

- Livestock Animals

- Companion Animals

By Product

- Pharmaceuticals

- Feed Additives

By End-User

- Hospitals & Clinics

- Point-of-Care/In-House Testing

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

Which countries in Eastern Europe show the highest growth potential in the veterinary healthcare sector?

Poland and Hungary are emerging as key markets in Eastern Europe.

What factors contribute to the growth of veterinary diagnostics in Northern Europe?

The increasing adoption of advanced diagnostic technologies and rising awareness about pet health are major drivers in Northern Europe.

What factors are hindering the veterinary healthcare market in Switzerland?

High treatment costs and limited insurance coverage pose challenges to market growth in Switzerland.

What is the Europe Veterinary Healthcare Market?

The Europe Veterinary Healthcare Market covers products, services, and technologies used for diagnosing, treating, and preventing diseases in animals, including both companion (pet) and livestock animals.

. What factors are driving the growth of the Europe Veterinary Healthcare Market?

Growth is driven by rising pet ownership, increasing livestock production, technological advancements in diagnostics and vaccines, and government initiatives supporting animal health and food safety.

What are the main product segments in the veterinary healthcare market?

Key product segments include vaccines, pharmaceuticals, feed additives, diagnostics, and medical devices designed for animal health management.

Which countries lead the Europe Veterinary Healthcare Market?

Major contributors include Germany, the United Kingdom, France, Italy, Spain, and the Netherlands, with Germany holding the largest share due to its strong veterinary infrastructure and livestock industry.

What are the key challenges faced by the Europe veterinary healthcare industry?

Challenges include stringent regulatory approvals, rising cost of veterinary treatments, antimicrobial resistance, and economic pressures on livestock producers.

What opportunities exist for new entrants in this market?

Opportunities include developing biologics and natural feed additives, AI-based diagnostics, digital pet wellness platforms, and collaborations with research institutions for vaccine development.

What is the long-term outlook for the Europe Veterinary Healthcare Market?

The market is expected to grow steadily due to increasing animal health awareness, technological advancements, and sustainable government policies, positioning Europe as a global leader in veterinary innovation.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com