Global Fetal And Neonatal Care Equipment Market Size, Share, Trends & Growth Analysis Report By Product Type, End Users & Region - Industry Forecast (2026 to 2034)

Global Fetal and Neonatal Care Equipment Market Size

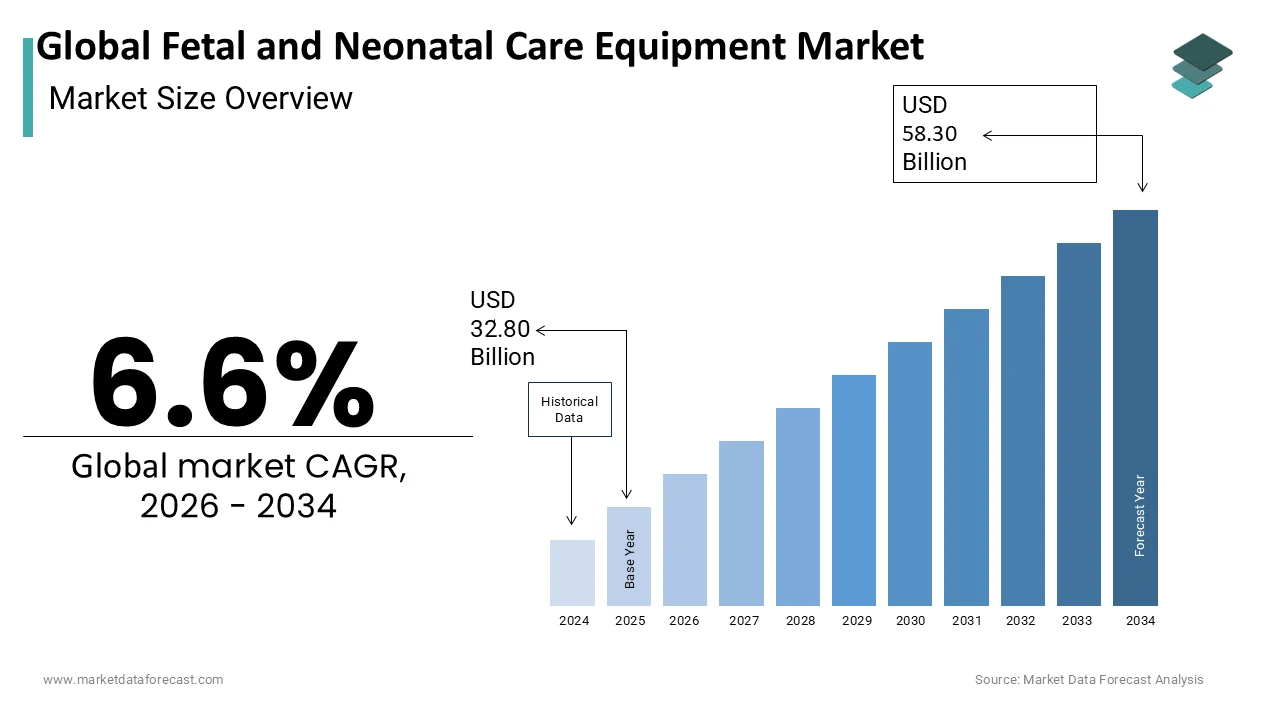

The global fetal and neonatal care equipment market size was valued at USD 32.80 billion in 2025, and it is expected to reach USD 58.30 billion by 2034 from USD 34.97 billion in 2026, growing at a CAGR of 6.6%. From 2026 to 2034.

Fetal and neonatal care equipment is a specialized array of medical devices designed to monitor, support, and treat fetuses during pregnancy and newborns, particularly those born prematurely or with critical health conditions. This sector includes vital technologies such as fetal monitors, neonatal ventilators, incubators, phototherapy units, and pulse oximeters, which are indispensable in modern obstetrics and neonatal intensive care units. The significance of this market is underscored by the global imperative to reduce infant mortality and improve long-term health outcomes for vulnerable infants. According to the World Health Organization, approximately 2.3 million children died in their first month of life in 2022, with preterm birth complications remaining the leading cause of death among children under 5 years. In Europe, according to the European Perinatal Health Report, the rate of very preterm births (less than 32 weeks) varies significantly across countries but averages around 1.5% of all live births. These statistics highlight the persistent need for advanced clinical interventions. As per Eurostat, the average life expectancy in the European Union has risen to 81 years, yet ensuring healthy starts remains a priority for healthcare systems. The integration of digital health solutions and minimally invasive technologies is transforming patient care standards. Regulatory frameworks, such as the European Medical Device Regulation, ensure high safety and performance standards for these critical devices. Consequently, the market is driven by the continuous evolution of clinical practices aimed at enhancing survival rates and reducing morbidity in the most fragile patient populations.

MARKET DRIVERS

Rising Prevalence of Preterm Births and High-Risk Pregnancies

The increasing incidence of preterm births and high-risk pregnancies is driving the growth of the global fetal and neonatal care equipment market. Preterm infants often require immediate and prolonged medical intervention, including respiratory support, thermal regulation, and continuous physiological monitoring, to survive and thrive. According to the World Health Organization, an estimated 13.4 million babies were born preterm globally in recent years, representing more than 1 in 10 live births. This substantial volume creates a consistent and growing demand for specialized equipment, such as neonatal ventilators and incubators, in hospitals worldwide. In Europe, according to the European Foundation for the Care of Newborn Infants, countries with higher rates of assisted reproductive technologies also experience elevated numbers of multiple births, which are frequently associated with prematurity. For instance, the rate of twin births in some European nations exceeds 3% of all deliveries. These complex pregnancies necessitate advanced fetal monitoring systems to detect distress early and ensure timely interventions. As per the Centers for Disease Control and Prevention, the preterm birth rate in the United States was 10.4% in 2022, reflecting a persistent public health challenge. The correlation between maternal age, lifestyle factors, and pregnancy complications further exacerbates this trend. Consequently, healthcare facilities are compelled to invest in state-of-the-art neonatal care infrastructure to manage the rising caseload of vulnerable infants, thereby driving market growth.

Technological Advancements in Non-Invasive Monitoring Solutions

Technological advancements in non-invasive monitoring solutions are another significant driver propelling the fetal and neonatal care equipment market forward. Modern healthcare providers increasingly prefer devices that minimize physical trauma and infection risks for delicate newborns while providing accurate, real-time data. Innovations such as wireless fetal heart rate monitors, wearable pulse oximeters, and transcutaneous carbon dioxide sensors have revolutionized patient care by allowing continuous assessment without restrictive cables or invasive procedures. According to the Journal of Perinatology, the adoption of non-invasive ventilation techniques has reduced the incidence of bronchopulmonary dysplasia in preterm infants by up to 20% in leading neonatal intensive care units. This clinical benefit encourages hospitals to upgrade their equipment portfolios with the latest technology. Furthermore, the integration of artificial intelligence into monitoring systems enables predictive analytics that can alert clinicians to potential deterioration before it becomes critical. As per the European Society for Paediatric Research, there is a growing emphasis on family-centered care, which is facilitated by portable and user-friendly monitoring devices that allow parents to remain close to their infants. The miniaturization of sensors also supports the development of smaller and more efficient equipment suitable for low-birth-weight infants. These technological strides not only improve clinical outcomes but also enhance operational efficiency in healthcare settings. Consequently, the shift towards sophisticated non-invasive technologies drives sustained investment in the fetal and neonatal care equipment sector.

MARKET RESTRAINTS

High Costs of Advanced Neonatal Care Infrastructure

The substantial financial burden associated with acquiring and maintaining advanced neonatal care infrastructure is primarily hampering the fetal and neonatal care equipment market expansion, particularly in low- and middle-income regions. State-of-the-art equipment, such as high-frequency oscillatory ventilators, magnetic resonance imaging systems for neonates, and integrated monitoring stations, requires significant capital investment. According to the World Bank, many developing nations spend less than 5% of their gross domestic product on healthcare, limiting their ability to purchase expensive medical devices. In Europe, despite robust healthcare systems, budget constraints within public hospitals can delay the procurement of new technologies. As per the Organisation for Economic Co-operation and Development, health expenditure per capita varies widely across member countries, es with some nations allocating significantly fewer resources to specialized pediatric care. The ongoing costs of maintenance, calibration, and staff training further strain hospital budgets. For instance, a single neonatal intensive care bed can cost over 100,000 euros to equip fully with necessary monitoring and support systems. Additionally, the rapid pace of technological obsolescence means that equipment may need replacement within a few years, adding to the financial pressure. These economic barriers prevent widespread adoption of the latest care solutions, leading to disparities in patient outcomes. Consequently, the high cost of entry and upkeep acts as a significant brake on market expansion, especially in resource-constrained environments where the need for such equipment is often greatest.

Stringent Regulatory Compliance and Approval Processes

Stringent regulatory compliance and complex approval processes are further hindering the expansion of the global market growth. Medical devices intended for vulnerable populations, such as fetuses and newborns, are subject to rigorous safety and efficacy evaluations to prevent adverse events. In Europe, the implementation of the Medical Device Regulation has increased the documentation and clinical evidence requirements for manufacturers seeking certification. According to the European Commission, the transition to this new regulatory framework has extended the time required for product approval by an average of 6 to 12 months. This delay postpones market entry and increases development costs for companies. Furthermore, the need for extensive clinical trials involving pregnant women and neonates poses ethical and logistical challenges that can stall innovation. As per the US Food and Drug Administration, the number of premarket approvals for pediatric devices remains lower compared to adult devices due to these heightened scrutiny levels. Manufacturers must also navigate varying regulatory landscapes in different countries, which complicates global distribution strategies. The requirement for post-market surveillance and periodic safety updates adds to the operational burden. These regulatory hurdles discourage smaller enterprises from entering the market and limit the diversity of available products. Consequently, the stringent regulatory environment acts as a restraint by slowing down the pace of innovation and increasing the barriers to commercialization for new fetal and neonatal care technologies.

MARKET OPPORTUNITIES

Integration of Telemedicine and Remote Patient Monitoring

The integration of telemedicine and remote patient monitoring is a notable opportunity for growth in the fetal and neonatal care equipment market. The ability to monitor high-risk pregnancies and discharged preterm infants from home reduces hospital readmissions and alleviates pressure on neonatal intensive care units. Wearable devices that track fetal heart rate, uterine contractions, and neonatal vital signs can transmit data securely to healthcare providers for real-time analysis. According to the American Telemedicine Association, the use of remote patient monitoring in obstetrics has increased by 30% since 2020, driven by the need for continuous care outside clinical settings. This trend is supported by improvements in broadband connectivity and smartphone penetration, which facilitate seamless data transmission. In Europe, the European Health Data Space initiative aims to enhance the sharing of health data, which can support the scalability of telehealth solutions. As per the Journal of Medical Internet Studies, remote monitoring of preterm infants after discharge has been shown to reduce parental anxiety and improve early detection of health issues. Healthcare systems are increasingly reimbursing for these services, recognizing their cost-effectiveness and clinical benefits. Manufacturers who develop user-friendly connected devices stand to gain a competitive advantage by addressing the growing demand for home-based care. Consequently, the expansion of telemedicine infrastructure creates a lucrative avenue for equipment providers to innovate and capture new market segments.

Expansion of Neonatal Intensive Care Units in Emerging Economies

The expansion of neonatal intensive care units in emerging economies presents a promising opportunity for the fetal and neonatal care equipment market. Governments in regions such as the Asia-Pacific and Latin America are investing heavily in healthcare infrastructure to reduce infant mortality rates and meet sustainable development goals. According to the United Nations Children's Fund, the neonatal mortality rate in South Asia has declined by 50% since 1990 but remains higher than in developed regions, prompting increased investment in specialized care facilities. Countries like India and China are building new hospitals and upgrading existing ones with modern neonatal care capabilities. As per the Indian Ministry of Health and Family Welfare, the government aims to establish dedicated neonatal intensive care units in all district hospitals by 2025. This initiative creates a substantial demand for essential equipment, such as incubators, radiant warmers, and respiratory support devices. International organizations and non-governmental entities are also providing funding and technical assistance to support these efforts. The growing middle class in these regions is also demanding higher-quality healthcare services, which drives private sector investment in advanced neonatal care. Manufacturers can capitalize on this trend by offering cost-effective and durable equipment tailored to the needs of emerging markets. Consequently, the strategic focus on improving neonatal care infrastructure in developing nations opens up significant growth opportunities for market participants.

MARKET CHALLENGES

Shortage of Skilled Healthcare Professionals

The shortage of skilled healthcare professionals is majorly challenging the fetal and neonatal care equipment market worldwide. Advanced devices require specialized training for operation, interpretation of data, and maintenance, which is not always available in sufficient quantities. According to the World Health Organization, there is a global shortfall of 15 million health workers by 2030, with neonatal specialists being particularly scarce in low-resource settings. In Europe, according to the European Centre for Disease Prevention and Control, workforce retention issues in critical care specialties are exacerbating staffing gaps. Without adequately trained personnel, even the most sophisticated equipment cannot deliver optimal patient outcomes. The complexity of modern neonatal intensive care units demands multidisciplinary teams, including neonatologists, nurses, respiratory therapists, and biomedical engineers. As per the National Association of Neonatal Nurses, the ratio of qualified nurses to critically ill infants in many facilities falls below recommended standards, leading to burnout and potential errors. Training programs are time-consuming and expensive, further limiting the speed at which healthcare systems can scale up their workforce. This human resource constraint limits the adoption of new technologies, as hospitals may hesitate to invest in equipment they cannot staff effectively. Consequently, the lack of skilled professionals acts as a barrier to maximizing the potential of fetal and neonatal care equipment and improving patient care standards.

Risk of Hospital-Acquired Infections and Equipment Sterilization

The risk of hospital-acquired infections and the complexities of equipment sterilization are further challenging the global market expansion. Newborns, particularly those born preterm, have immature immune systems, making them highly susceptible to infections from contaminated medical devices. According to the Centers for Disease Control and Prevention, neonatal sepsis remains a leading cause of morbidity and mortality in intensive care units, with many cases linked to invasive devices such as catheters and ventilators. Ensuring the strict sterilization of reusable equipment is logistically challenging and resource-intensive. As per the Journal of Hospital Infection, outbreaks of multidrug-resistant organisms in neonatal units are often traced back to inadequately cleaned respiratory equipment or monitoring probes. The design of some devices makes thorough cleaning difficult, creating niches where pathogens can persist. Healthcare facilities must adhere to rigorous hygiene protocols, which increase operational costs and workload for staff. Additionally, the shift towards single-use disposable items to mitigate infection risks generates significant medical waste and environmental concerns. Manufacturers face pressure to design equipment that is both easy to sterilize and environmentally sustainable. Failure to address these hygiene challenges can lead to severe clinical consequences and legal liabilities. Consequently, the ongoing battle against hospital-acquired infections requires continuous innovation in device design and sterilization processes, posing a persistent challenge to the market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, End-User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | GE Healthcare, Dickinson and Company, Philips Healthcare, Medtronic, Drägerwerk AG & Co, KGaA, Medtronic plc, and Masimo Corporation. |

SEGMENTAL ANALYSIS

By Product Type Insights

The neonatal care equipment segment dominated the market by capturing the highest share of the global market in 2025. The dominance of the neonatal care equipment segment in the global market can be credited to the absolute physiological necessity for thermoregulation and respiratory support in preterm and low-birth-weight infants. Premature babies lack the subcutaneous fat and mature skin barrier required to maintain body temperature, making incubators and infant warmers indispensable for survival. According to the World Health Organization, approximately 15 million babies are born preterm each year globally, with many requiring immediate admission to neonatal intensive care units for thermal management. These devices create a controlled microenvironment that prevents hypothermia, a condition associated with increased mortality and morbidity. As per the American Academy of Pediatrics, maintaining normothermia is a critical quality indicator in neonatal care, driving hospitals to invest in advanced servo-controlled incubators. Furthermore, respiratory distress syndrome affects nearly 10% of all preterm births, necessitating the use of ventilators and continuous positive airway pressure systems. According to the European Society for Paediatric Research, early respiratory support significantly improves lung development and long-term outcomes. Consequently, the high volume of preterm births combined with the life-saving nature of these devices ensures that neonatal care equipment remains the dominant product category. Hospitals prioritize these investments as they form the backbone of neonatal intensive care infrastructure, ensuring that the most vulnerable patients receive essential life support during their critical first days and weeks of life.

However, the fetal care equipment segment is projected to register the highest CAGR of 7.8% during the forecast period, owing to the increasing adoption of advanced prenatal diagnostic technologies. Expectant parents and healthcare providers are increasingly relying on sophisticated imaging and monitoring tools to detect congenital anomalies and assess fetal well-being early in pregnancy. High-resolution ultrasound devices and fetal MRI systems allow for detailed anatomical assessments that were previously impossible. According to the American College of Obstetricians and Gynecologists, the utilization of detailed anomaly scans has increased by 20% over the past decade due to improved insurance coverage and clinical guidelines. This trend is further supported by the rising maternal age in many developed countries, which correlates with a higher risk of chromosomal abnormalities and pregnancy complications. As per the European Society of Human Reproduction and Embryology, the number of pregnancies in women over 35 has risen significantly, necessitating more frequent and detailed monitoring. Furthermore, the integration of three-dimensional and four-dimensional ultrasound technologies provides enhanced visualization, encouraging wider adoption in clinical practice. Manufacturers are also introducing portable and handheld ultrasound devices that expand access to prenatal care in remote areas. Consequently, the technological evolution of fetal diagnostics, combined with changing demographic patterns, fuels the rapid growth of this segment as stakeholders prioritize early detection and intervention to ensure healthy pregnancy outcomes.

By End-User Insights

The hospitals segment led the market by capturing the largest share of the global market in 2025 due to its role as the central hub for managing high-risk pregnancies and providing intensive neonatal care. Most complicated deliveries and premature births occur in hospital settings where multidisciplinary teams of obstetricians, neonatologists, and nurses are available around the clock. According to the Organisation for Economic Co-operation and Development, over 98% of births in member countries take place in hospitals, ensuring that these institutions are the primary purchasers of specialized equipment. Hospitals are equipped with neonatal intensive care units that require a comprehensive array of devices, including ventilators, incubators, and advanced monitoring systems. As per the American Hospital Association, the average large hospital in the United States has a dedicated neonatal intensive care unit with an average of 15 to 20 beds, each requiring significant equipment investment. The concentration of resources and expertise in hospitals allows for the efficient utilization of expensive and complex technologies. Furthermore, hospitals benefit from economies of scale when procuring equipment, enabling them to negotiate better prices and service contracts. The regulatory requirement for hospitals to maintain certain standards of care also mandates the presence of up-to-date equipment. Consequently, the structural centrality of hospitals in the healthcare delivery system ensures their continued dominance as the primary end-users of fetal and neonatal care equipment.

However, the clinics segment is anticipated to exhibit the highest CAGR of 7.4% during the forecast period, due to the expansion of outpatient prenatal care services. There is a growing trend towards shifting routine prenatal check-ups and minor diagnostic procedures from hospitals to specialized clinics to reduce healthcare costs and improve patient convenience. According to the Ambulatory Care Alliance, the number of standalone obstetrics and gynecology clinics has increased by 15% in the last five years, as patients prefer personalized and accessible care settings. These clinics are increasingly investing in portable ultrasound devices and fetal dopplers to offer comprehensive diagnostic services on-site. The decentralization of healthcare services allows for earlier and more frequent monitoring of fetal health, which can prevent complications and reduce hospital admissions. As per the Journal of Obstetrics and Gynaecology, early detection of fetal anomalies in outpatient settings has improved referral efficiency to tertiary care centers. Furthermore, the rise of private healthcare providers in emerging markets is fueling the establishment of specialized maternal and child health clinics. These facilities are eager to differentiate themselves by offering state-of-the-art diagnostic equipment. Consequently, the shift towards outpatient care models and the proliferation of specialized clinics drive the rapid growth of this segment in the fetal and neonatal care equipment market.

COUNTRY LEVEL ANALYSIS

North America Fetal and Neonatal Care Equipment Market Analysis

North America held the major share of the global market in 2025 due to the advanced healthcare infrastructure and high expenditure on medical technologies. The United States dominates the regional market due to its robust network of specialized hospitals and high prevalence of preterm births. According to the Centers for Disease Control and Prevention, the preterm birth rate in the United States was 10.4% in 2022, creating a sustained demand for neonatal intensive care equipment. The region benefits from favorable reimbursement policies and strong government funding for maternal and child health programs. As per the American Hospital Association, nearly all major hospitals in the US are equipped with level III or IV neonatal intensive care units, which require sophisticated monitoring and support systems. The presence of leading medical device manufacturers in the region also facilitates the rapid adoption of innovative technologies, such as artificial intelligence-enabled monitoring and minimally invasive surgical tools. Additionally, the high awareness among expectant parents regarding prenatal care drives the demand for advanced fetal diagnostic services in outpatient clinics. The regulatory environment governed by the Food and Drug Administration ensures high safety standards, which fosters trust in medical devices. Consequently, the combination of high clinical need, financial support, and technological leadership sustains North America's dominant position in the global market.

Europe Fetal and Neonatal Care Equipment Market Analysis

Europe maintains a significant position in the fetal and neonatal care equipment market, driven by universal healthcare coverage and stringent regulatory standards. Germany, France, and the United Kingdom are the key contributors to the regional market due to their well-established healthcare systems and focus on reducing infant mortality. According to Eurostat, the infant mortality rate in the European Union has declined to below 3 deaths per 1,000 live births, reflecting the effectiveness of neonatal care interventions. The implementation of the Medical Device Regulation has standardized safety and performance requirements across member states, encouraging the adoption of high-quality equipment. According to the European Perinatal Health Report, there is a strong emphasis on regionalized perinatal care, which involves transferring high-risk pregnancies to specialized centers equipped with advanced technology. This centralization drives concentrated purchasing of high-end fetal and neonatal devices. Furthermore, the aging population and delayed childbirth trends in Europe have increased the incidence of high-risk pregnancies, necessitating more frequent monitoring and intervention. Government initiatives, such as the EU4Health program, provide funding for healthcare infrastructure improvements, including neonatal units. Consequently, the focus on quality standardization and centralized care models defines the European market landscape and supports its substantial share in the global industry.

Asia-Pacific Fetal and Neonatal Care Equipment Market Analysis

The Asia-Pacific region is emerging as the fastest-growing market for fetal and neonatal care equipment, fueled by improving healthcare infrastructure and rising awareness of maternal health. China, India, and Japan are the primary drivers of growth in this region due to their large populations and increasing investment in healthcare facilities. According to the World Bank, health expenditure per capita in East Asia and the Pacific has increased by 8% annually over the past decade, enabling greater access to medical technologies. The governments of China and India have launched national programs to reduce infant mortality, which include provisions for equipping district hospitals with neonatal care units. According to the Ministry of Health in India, the Surakshit Matritva Aashwasan initiative aims to ensure quality care during delivery and the postnatal period, driving equipment procurement. Additionally, the rising middle class in the region is demanding higher-quality healthcare services, leading to the expansion of private hospitals and clinics. The increasing prevalence of cesarean sections and assisted reproductive technologies also contributes to the demand for specialized fetal monitoring and neonatal support devices. Manufacturers are responding by introducing cost-effective and durable equipment tailored to the needs of emerging markets. Consequently, the combination of government support, economic growth, and expanding healthcare access positions the Asia-Pacific as a high-potential market in the global landscape.

Latin America Fetal and Neonatal Care Equipment Market Analysis

Latin America represents a developing market for fetal and neonatal care equipment, characterized by disparities in healthcare access but growing investment in public health. Brazil and Mexico are the key markets in the region due to their large populations and ongoing efforts to improve maternal and child health outcomes. According to the Pan American Health Organization, the neonatal mortality rate in Latin America has decreased by 30% since 2000 but remains higher than in developed regions, prompting continued investment in care infrastructure. Governments in the region are implementing policies to expand coverage of prenatal and neonatal services, particularly in underserved areas. According to the Brazilian Ministry of Health, the Rede Cegonha strategy aims to organize care for pregnant women and newborns, ensuring access to appropriate technologies and facilities. This initiative has led to the establishment of new neonatal intensive care units and the upgrading of existing ones. Additionally, the growth of the private healthcare sector in urban areas is driving demand for advanced diagnostic and monitoring equipment. International organizations, such as the Inter-American Development Bank, provide funding for health projects that include the procurement of medical devices. Consequently, the focus on reducing inequality and improving healthcare access drives the gradual expansion of the fetal and neonatal care equipment market in Latin America.

Middle East and Africa Fetal and Neonatal Care Equipment Market Analysis

The Middle East and Africa region presents a mixed market landscape, with high growth potential in the Gulf Cooperation Council countries and significant challenges in sub-Saharan Africa. The United Arab Emirates and Saudi Arabia are leading the market in the Middle East due to their wealthy economies and investment in world-class healthcare facilities. According to the World Health Organization, these countries have achieved infant mortality rates comparable to those of developed nations through extensive use of advanced medical technologies. In contrast, sub-Saharan Africa faces significant barriers due to limited resources and infrastructure. According to the African Union, the continent accounts for a disproportionate share of global neonatal deaths, highlighting the urgent need for basic care equipment. Initiatives, such as the Every Newborn Action Plan, aim to address these gaps by promoting the availability of essential newborn care technologies. Non-governmental organizations and international donors play a crucial role in supplying equipment to public hospitals in low-income countries. The growing medical tourism sector in the Middle East also drives demand for premium fetal and neonatal care services. Consequently, the region is characterized by a dichotomy between high-tech adoption in wealthy nations and fundamental needs in developing areas, shaping a diverse market dynamic.

COMPETITIVE LANDSCAPE

The competition in the fetal and neonatal care equipment market is intense and characterized by the presence of several established global players alongside emerging regional manufacturers. Leading companies compete based on technological innovation, product quality, and after-sales service to secure contracts with hospitals and healthcare facilities. The market is driven by continuous advancements in medical technology, which require substantial investment in research and development. Companies strive to differentiate their products through features such as portability, connectivity,y anuser-friendlyly interfaces that enhance clinical workflow. Price competitiveness is also a significant factor, particularly in emerging markets,s where cost sensitivity is high. However, our premium segments prioritize performance and reliability over cost, allowing established brands to maintain strong positions. Regulatory compliance serves as a barrier to entry for new competitors, ensuring that only qualified players can operate in this critical sector. Collaborations and strategic alliances are common as firms seek to expand their reach and offer comprehensive solutions. The dynamic nature of healthcare needs and technological progress ensures that competition remains vigorous,s fostering an environment of constant improvement and innovation across the global landscape.

KEY MARKET PLAYERS

Some of the noteworthy companies in the global fetal and neonatal care equipment market profiled in the report are

- GE Healthcare

- Dickinson, and Company

- Philips Healthcare

- Medtronic

- Drägerwerk AG & Co., KGaA

- Medtronic plc

- Masimo Corporation.

TOP LEADING PLAYERS IN THE MARKET

- GE HealthCare Technologies Inc maintains a strong presence in the fetal and neonatal care sector through its comprehensive portfolio of imaging and monitoring solutions. The company is renowned for its advanced ultrasound systems that provide high-resolution images for prenatal diagnosis and fetal assessment. Recently, GE HealthCare has focused on integrating artificial intelligence into its devices to enhance diagnostic accuracy and workflow efficiency. The launch of portable ultrasound units has expanded access to critical care in remote and resource-limited settings. The company also emphasizes sustainability by designing energy-efficient equipment and reducing waste in manufacturing processes. Strategic partnerships with healthcare providers enable the development of customized solutions that address specific clinical needs. By leveraging its global distribution network, GE Healthcare ensures the timely delivery of essential medical devices to hospitals worldwide. These initiatives reinforce its reputation as a leader in innovation and reliability within the maternal and child health segment.

- Koninklijke Philips NV is a key contributor to the fetal and neonatal care market,t offering integrated solutions for connected care and patient monitoring. The company specializes in non-invasive ventilation technologies and advanced patient monitors that support the delicate needs of preterm infants. Philips has recently strengthened its position by expanding its telehealth capabilities, allowing for remote monitoring of high-risk pregnancies and discharged neonates. The introduction of wearable sensors enables continuous data collection without restricting infant movement or parental bonding. Philips also invests heavily in research to develop smarter algorithms that predict adverse events early, improving clinical outcomes. The company collaborates with hospitals to create smart neonatal intensive care units that streamline operations and enhance patient safety. By focusing on a holistic care ecosystem,s Philips delivers value beyond individual devices, es fostering long-term relationships with healthcare institutions and improving the standard of care globally.

- Drägerwerk AG & Co KGaA is a prominent player in the fetal and neonatal care equipment market,k et known for high-quality respiratory and monitoring devices. The company provides a wide range of neonatal ventilators, incubators,s and phototherapy systems that are trusted for their precision and durability. Dräger has recently focused on enhancing the user experience of its equipment through intuitive interfaces and ergonomic designs that reduce staff fatigue. The integration of digital tools allows for seamless data exchange between devices and hospital information systems, supporting better decision-making. Dräger also prioritizes training and education programs for healthcare professionals, ensuring optimal use of its technologies. The company actively participates in global health initiatives to improve neonatal care standards in developing regions. By combining engineering excellence with a commitment to patient safety,y Dräger continues to innovate and deliver reliable solutions that support the survival and well-being of vulnerable newborns worldwide.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the fetal and neonatal care equipment market primarily focus on product innovation and strategic collaborations to maintain their competitive edge. Companies invest significantly in research and development to create advanced devices that offer greater precision, safety,y and ease of use. Integration of digital health technologies such as artificial intelligence and remote monitoring capabilities is a common strategy to enhance clinical outcomes and operational efficiency. Manufacturers also pursue mergers and acquisitions to expand their product portfolios and enter new geographical markets. Partnerships with healthcare providers and research institutions facilitate the development of solutions tailored to specific clinical needs. Additionally, companies emphasize regulatory compliance and quality assurance to build trust among customers and ensure patient safety. Sustainability initiatives are increasingly adopted to reduce environmental impact and appeal to socially conscious stakeholders. These strategies enable market participants to differentiate their offerings and respond effectively to evolving healthcare demands while driving long-term growth and stability in the industry.

MARKET SEGMENTATION

This market research report on the global fetal and neonatal care equipment market has been segmented and sub-segmented into the following categories.

By Product Type

-

Fetal Care Equipment

-

Fetal Dopplers

- Ultrasound Devices

- Fetal Monitors

- Fetal MRI Systems

- Fetal Pulse Oximeters

-

- Neonatal Care Equipment

- Incubators

- Infant Warmers

- Respiratory Devices

- Phototherapy Equipment

- Neonatal Monitoring Device

By End User

- Hospitals

- Clinics

By Region

- North America

- Europe

- Asia-pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

How much is the global fetal and neonatal care equipment going to be worth by 2033?

GE Healthcare, Dickinson, and Company, Philips Healthcare, Medtronic, Drägerwerk AG & Co, KGaA, Medtronic plc, and Masimo Corporation are a few of the noteworthy companies operating in the global fetal and neonatal care equipment market.

Which region led the fetal and neonatal care equipment market in 2025?

Geographically, the North American regional market dominated the fetal and neonatal care equipment market in 2025.

Which are the significant players operating in the fetal and neonatal care equipment market?

Yes, we have studied and included the COVID-19 impact on the global fetal and neonatal care equipment market in this report.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com