- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$619.4 BnMarket Estimate, 2026

$688.7 BnMarket Forecast, 2034

$1610.2 BnCAGR, 2026–2034

11.2%Global Personalized Medicine Market Size

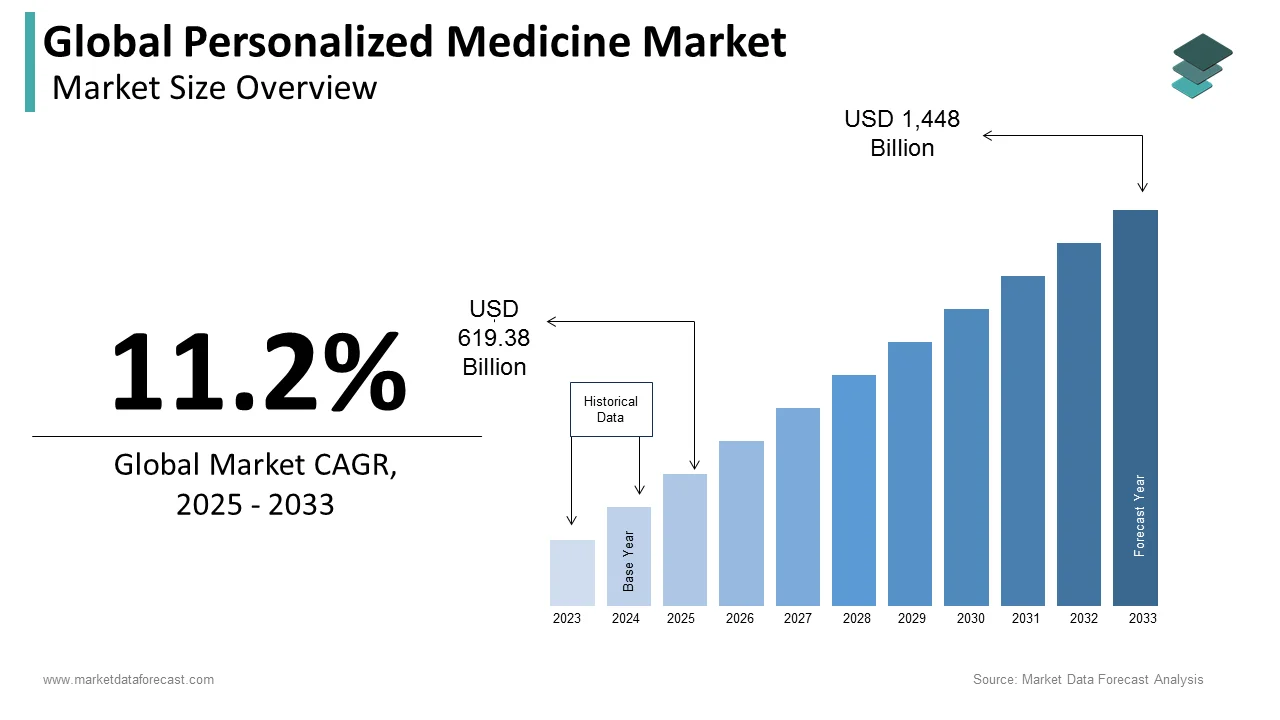

The global personalized medicine market size was worth USD 619.38 billion in 2025 and is forecast to grow at a 11.2% CAGR between 2026 and 2034, reaching USD 1,610.28 billion by 2034, up from USD 688.75 billion in 2026.

Personalized medicine is are therapy dynamically calibrated to an individual’s genomic, proteomic, metabolic, and environmental profile. As per the National Institutes of Health, over 350 FDA-approved drugs now include pharmacogenomic biomarkers in their labeling, guiding dosing or patient selection. According to a study, the percentage of oncology trials using biomarkers has grown significantly over time. The increasing use of biomarkers is a central pillar of personalized medicine, allowing for the targeting of tumor-specific biomarkers with new therapies. In the US, personalized medicines accounted for more than one-third of new drug approvals for the fourth consecutive year in 2023. This is not merely precision, but it is predictive, preventive, and participatory medicine, where molecular diagnostics precede prescription, and therapeutic response is no longer probabilistic but programmable.

MARKET DRIVERS

Clinical Superiority of Biomarker-Guided Therapies in Oncology

The demonstrable clinical superiority of biomarker-guided therapies in oncology, where response rates and survival metrics eclipse conventional regimens, fuels the growth of the personalized medicine market. According to the study, patients receiving genomically matched therapies exhibited a percentage of objective response rate compared to that in unmatched cohorts. As per research, NSCLC patients treated with EGFR mutation-targeted osimertinib achieved a median progression-free survival of several months versus that number of months with chemotherapy. In metastatic melanoma, BRAF/MEK inhibitor combinations increase survival compared to those with dacarbazine. These outcomes compel payers and providers to prioritize molecular profiling.

Declining Cost and Rapid Advancement of Genomic Sequencing

The plummeting cost and accelerating speed of genomic sequencing, which has transitioned from research luxury to clinical utility, are also driving the growth of the personalized medicine market. As per research, the cost of whole-exome sequencing has fallen, down from that in 2011, while turnaround time for clinical-grade panels has now in days. In Japan, a portion of its tertiary hospitals offer in-house NGS panels for solid tumors, which reduces outsourcing delays, as per a study. This cost compression democratizes access.

MARKET RESTRAINTS

Fragmented Genomic Data Infrastructure and Lack of Interoperability

The persistent fragmentation of genomic data infrastructure, which impedes interoperability and longitudinal analysis across institutions and borders, constrains the expansion of the personalized medicine market. According to a study, only a portion of clinical sequencing labs in high-income countries use standardized data formats compatible with international repositories. In Europe, only few member states had operational national genomic data hubs as of 2024. This siloing prevents aggregation of rare variant outcomes, delays therapy matching, and inflates validation costs.

Limited Clinician Genomic Literacy and Interpretation Gaps

The inadequacy of clinician genomic literacy, which creates a translational chasm between molecular data generation and therapeutic decision-making, further slows down the growth rate of the personalized medicine market. Only a portion of practicing oncologists felt confident interpreting NGS reports without genetic counselor support. According to a study, a portion of consultants could not correctly identify when a germline finding required referral. In Germany, a share of primary care physicians never order pharmacogenomic tests due to interpretation anxiety. This knowledge deficit stalls adoption. Personalized medicine’s barrier is no longer technology. It is human capital.

MARKET OPPORTUNITIES

Integration of Real-World Evidence (RWE) with Genomic Data

The integration of real-world evidence with genomic data to dynamically refine treatment algorithms beyond clinical trial constraints is likely to promote new opportunities for the personalized medicine market. Linking EHR-derived outcomes with genomic profiles enabled the identification of CDK4/6 inhibitor resistance markers in breast cancer faster than traditional trials. Also, real-world progression-free survival for NSCLC patients on targeted therapies correlated within a portion of trial data, which validates RWE as a regulatory-grade endpoint.

Pharmacogenomic-Guided Prescribing in Primary Care

Pharmacogenomic-guided prescribing in primary care, where preemptive genotyping can prevent adverse drug reactions and optimize chronic disease management, is expected to give potential opportunities for the personalized medicine market. As per research, implementing CYP2D6/CYP2C19 testing for antidepressants reduced trial-and-error prescribing and cut emergency visits for side effects. Sweden’s nationwide PGx implementation could prevent adverse drug events annually. This shifts personalized medicine from a reactive oncology niche to a proactive and population-scale preventive infrastructure, which makes genomics foundational to safe and effective primary care.

MARKET CHALLENGES

Ethical and Legal Ambiguity in Incidental Germline Findings

The ethical and legal ambiguity surrounding incidental germline findings, which creates clinical paralysis and patient anxiety when somatic testing reveals hereditary risk, is a key limiting factor impacting the expansion of the personalized medicine market. As per the research, a portion of tumor-only sequencing cases uncover pathogenic BRCA, Lynch syndrome, or TP53 variants with implications for relatives. According to a study, a share of clinicians declined to report such findings due to a lack of consent protocols or genetic counseling resources. This gray zone forces institutions to either suppress clinically significant data or risk psychological and legal fallout. The absence of standardized consent frameworks, mandatory counseling pathways and liability protections means the full diagnostic power of sequencing is ethically shackled, turning potential lifesaving insights into medico-legal landmines.

Misalignment Between Reimbursement Models and Diagnostic Costs

The misalignment between value-based reimbursement models and the upfront cost of molecular diagnostics, which disincentivizes payer coverage despite long-term savings, also hampers the growth of the personalized medicine market. While comprehensive genomic profiling in NSCLC saves a notable amount per patient over months by avoiding ineffective therapies, U.S. Medicare reimburses only a portion per test. In Germany, a portion of hospitals absorb NGS costs internally due to delayed or partial insurer reimbursement. Australia rejected coverage for tumor mutational burden testing in 2023, citing insufficient budget impact modeling. This disconnect forces providers into a financial triage that involves testing only the young, the affluent, or the trial-eligible. The inequities personalized medicine was designed to resolve, including stratification by geography, institution, and socioeconomic status, will persist until payers recognize diagnostics as cost-avoidance tools instead of expense line items.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Therapeutic Area, End-User, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | GE Healthcare, Cepheid, Asuragen Incorporated, Illumina Inc., Abbot Incorporated, Dako A/S, Biogen, Genelex Corp, Exagen Diagnostics Inc., Qiagen Inc., DNA Direct, and Agendia N.V. |

SEGMENTAL ANALYSIS

By Therapeutic Area Insights

The oncology segment dominated the personalized medicine market with a significant share in 2025. Cancer is fundamentally a disease of genomic dysregulation, where driver mutations dictate therapeutic vulnerability, and is largely driving the growth of the oncology segment in the global market. In metastatic melanoma, inhibitors achieve response rates in mutation-positive patients versus those in wild-type patients, as per the study. Similarly, according to research, patients receiving genomically matched therapies had a higher progression-free survival than unmatched cohorts. Payers support this. The G-BA is responsible for assessing the clinical benefit of new medical services and products to determine whether they should be reimbursed by the statutory health insurance system.

The psychiatry segment is predicted to witness the highest CAGR of 21.7% from 2025 to 2033. The expansion of the psychiatry segment is propelled by pharmacogenomic-guided prescribing to mitigate trial-and-error toxicity and non-response in mood disorders. In addition, implementing preemptive genotyping for SSRIs reduced emergency department visits for adverse reactions and improved remission rates. Also, PGx-guided prescribing in depression reduced polypharmacy. Oncology uses tumor sequencing, but psychiatry leverages germline DNA, which is stable, accessible via saliva, and predictive across drug classes. This transforms mental health from subjective symptom management to biologically anchored precision prescribing.

By End-User Insights

The hospital segment had the largest share of the worldwide market in 2025 and is expected to continue holding the leading position throughout the forecast period. The growing patient visits to the hospitals and increasing patient population of chronic diseases propel the segmental growth.

On the other hand, the academic Institutes, clinical care, and research laboratories segment is predicted to grow at the highest CAGR during the forecast period owing to the growing investments by the research centers and government bodies in favor of personalized medicine.

By Application Insights

The companion diagnostics segment remained a prominent segment with a 49.4% share of the global personalized medicine market in 2024. Regulatory and commercial symbiosis exists with targeted therapeutics, and no precision drug reaches the market without its diagnostic counterpart, which drives the growth of the companion diagnostics segment in the global market. The U.S. approved new companion diagnostics, a portion of which were linked to oncology agents. Payers enforce this linkage. Germany’s statutory insurers reimburse targeted therapies only when accompanied by validated CDx results. The economic logic is inescapable. CDx reduces drug development failure rates, as per study, and increases net drug revenue through patient stratification. This is not a diagnostic tool but a gatekeeper of therapeutic value, and that is making CDx the non-negotiable infrastructure upon which the entire personalized medicine edifice is constructed.

The health informatics segment is estimated to register a CAGR of 26.3% from 2025 to 2033. The growth of the health informatics segment is fueled by the convergence of multi-omic data, AI-driven phenotyping, and real-world evidence platforms that dynamically refine treatment algorithms beyond static clinical trials. As per research, linking EHR outcomes with genomic profiles enabled the identification of CDK4/6 inhibitor resistance markers months faster than traditional research. Health informatics continuously optimizing adaptive learning healthcare systems where every patient's outcome feeds back into the algorithm, in stark contrast to CDx's binary test-treat model.

REGIONAL ANALYSIS

North America Personalized Medicine Market Analysis

North America led the global personalized medicine market with a 47.3% share in 2024. The domination of North America in the global market is primarily driven by regulatory permissiveness, venture-backed innovation, and payer experimentation. Private insurers cover preemptive PGx testing for millions of members. Simultaneously, academic medical centers, such as Mayo Clinic, Vanderbilt, and UCSF, embed genomics into routine care, which creates de facto national pilots. This ecosystem of regulatory agility, capital density, and clinical integration makes North America not just the largest but the most rapidly iterated personalized medicine laboratory on earth.

Europe Personalized Medicine Market Analysis

Europe held 27.3% of the global personalized medicine market share in 2024. State-mandated genomic infrastructure and cross-border data harmonization under the EHDS Regulation contribute to the growth of Europe in the global market. The U.K.’s Genomes Project expanded and mandates the return of actionable findings to treating clinicians, with a portion of oncology cases receiving genomically guided therapy. France established high-throughput sequencing platforms, which process genomes annually. Europe’s growth is policy-engineered, unlike North America’s market-driven model, which leverages public health systems to scale equitable access while enforcing strict data sovereignty.

Asia Pacific Personalized Medicine Market Analysis

Asia Pacific is likely to see the quickest expansion in the global personalized medicine market. The expansion of the Asia Pacific is fueled by national sequencing initiatives, oncology trial density, and leapfrog adoption of AI-driven diagnostics. Japan launched SCRUM-Japan, which enrolls patients in real-world biomarker-outcome registries. China’s “Healthy China 2030” blueprint includes tumor profiling as a pillar, with BGI and Burning Rock processing a large number of NGS tests annually. The region’s growth is uniquely mobile-integrated and policy-subsidized, which makes it the most dynamically scaled and socially embedded personalized medicine ecosystem outside the West.

Latin America Personalized Medicine Market Analysis

Latin America is moving ahead steadfastly in of the personalized medicine market. The growth of Latin America is driven by public-private oncology alliances and regional biomarker hubs, overcoming infrastructure gaps. Brazil’s National Cancer Institute partnered to offer subsidized NGS panels for advanced cancer patients annually. Testing for EGFR and ALK in Latin America is often done in private labs and frequently relies on sponsorship from pharmaceutical companies. Latin America bypasses legacy systems by embedding CDx into national treatment guidelines and training oncologists via virtual tumor boards.

Middle East and Africa Personalized Medicine Market Analysis

The Middle East and Africa is predicted to grow in the personalized medicine market between 2025 and 2033, owing to the sovereign sequencing programs and diaspora-driven knowledge transfer. Saudi Arabia’s Vision 2030 Genomics Program established the Genome Program, sequencing citizens to map population-specific variants. South Africa partnered to offer subsidized NGS for BRCA and Lynch syndrome across public hospitals. This region’s market is not scaled by volume but by strategic sovereignty by leveraging genomics to build indigenous diagnostic capacity and reduce therapeutic dependency on the Global North.

COMPETITIVE LANDSCAPE

The personalized medicine market is a high-stakes convergence of diagnostics, data, and drug development, where incumbents like Roche and Illumina compete with agile entrants like Guardant Health and Foundation Medicine. Differentiation pivots on three axes: regulatory velocity, analytical breadth, and clinical embedment. Roche leverages therapeutic co-development, Illumina controls sequencing infrastructure, while Thermo Fisher offers workflow modularity. Startups disrupt with liquid biopsy and AI-native interpretation. Competition is no longer about test accuracy alone; it’s about turnaround time, EHR integration, payer coverage, and global scalability. The winner will not be the most comprehensive panel but the most seamlessly operationalized one, which turns molecular insights into real-time, reimbursed, routine clinical decisions across continents.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global personalized medicine market include

- GE Healthcare

- Cepheid

- Asuragen Incorporated

- Illumina Inc.

- Abbot Incorporated

- Dako A/S

- Biogen

- Genelex Corp

- Exagen Diagnostics Inc.

- Qiagen Inc.

- DNA Direct

- Agendia N.V.

Top Players in the Personalized Medicine Market

- Roche Diagnostics anchors personalized medicine through its vertically integrated companion diagnostics, co-developing assays alongside targeted therapies. In addition, it launched the NAVIFY Mutation Profiler, which enables NGS-based tumor profiling in under hour across many genes. It expanded its VENTANA PD-L1 IHC portfolio to cover new immuno-oncology agents globally. Its acquisition of GenMark Diagnostics enhanced multiplex molecular detection for infectious disease stratification. Roche’s strategy embeds diagnostics not as add-ons but as inseparable co-therapeutics, which ensures its assays gatekeep global access to precision oncology.

- Illumina powers personalized medicine by democratizing high-throughput sequencing, enabling clinical labs to run tumor, germline, and liquid biopsy panels at scale. Illumina’s DRAGEN Bio-IT Platform now auto-interprets most clinically relevant variants, reducing bioinformatic barriers. Through its acquisition of Grail, it accelerated multi-cancer early detection adoption. Illumina’s dominance lies not in owning diagnostics but in owning the infrastructure that generates the data upon which all precision decisions are made.

- Thermo Fisher Scientific drives personalized medicine through modular, end-to-end biomarker workflows, from sample prep to NGS to companion diagnostic kits. Thermo Fisher partnered to co-develop liquid biopsy assays for therapy resistance monitoring. Thermo Fisher’s strength is interoperability. Its platforms allow labs to mix, match, and scale workflows without vendor lock-in.

Top Strategies Used by Key Market Participants

Leaders vertically integrate diagnostics with therapeutics to control end-to-end value chains and lock in reimbursement. They embed AI and automation into sequencing and variant interpretation to reduce turnaround time and bioinformatic dependency. Strategic acquisitions target niche biomarker developers and clinical trial service providers to expand test menus and accelerate regulatory pathways. They forge real-world evidence alliances with EHR and registry platforms to validate clinical utility beyond trials.

GLOBAL PERSONALIZED MEDICINE MARKET NEWS

- In February 2023, Ocean Genomics, an AI company that develops advanced computational platforms, received a strategic investment from Accenture to promote AI-driven Drug Discovery and the Development of Personalized Medicines.

- In May 2018, Advanced Diagnostic Laboratory Test (ADLT) received approval for FoundationOne CDx, and Foundation Medicine announced this. These are highly used for solid tumors that integrate with companion diagnostics. The company’s portfolio is expected to expand with this product approval.

- In October 2018, novel RNA-seq library preparation solutions were announced by Qiagen. It is expected that this solution will promote various applications in next-generation sequencing techniques.

- In January 2018, Foundation Medicine and the European Organization for Research and Treatment of Cancer collaborated to promote the Foundation’s comprehensive genomic profiling in personalized medicine.

MARKET SEGMENTATION

This report on the global personalized medicine market has been segmented and sub-segmented based on the therapeutic area, end-user, application, and region.

By Therapeutic Area

- Oncology

- Neurology

- Cardiology

- Antiviral

- Psychiatry

- Others

By End User

- Hospitals

- Molecular Diagnostic Laboratories and Testing Facilities

- Academic Institutes, clinical care, and Research Laboratories

- Contract Research Organizations

- Bio and health informatics companies

- Others (Service providers, partners, venture capitalists, etc.)

By Application

- Companion Diagnostics

- Biomarker identification

- Health Informatics

- Clinical Research

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa