Global Diabetes Devices Market Size, Share, Trends & Growth Forecast Report – Segmented By Product Type (Glucose Monitoring Devices, Insulin Delivery Systems & Control Solutions) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis From 2025 to 2033

Global Diabetes Devices Market Size

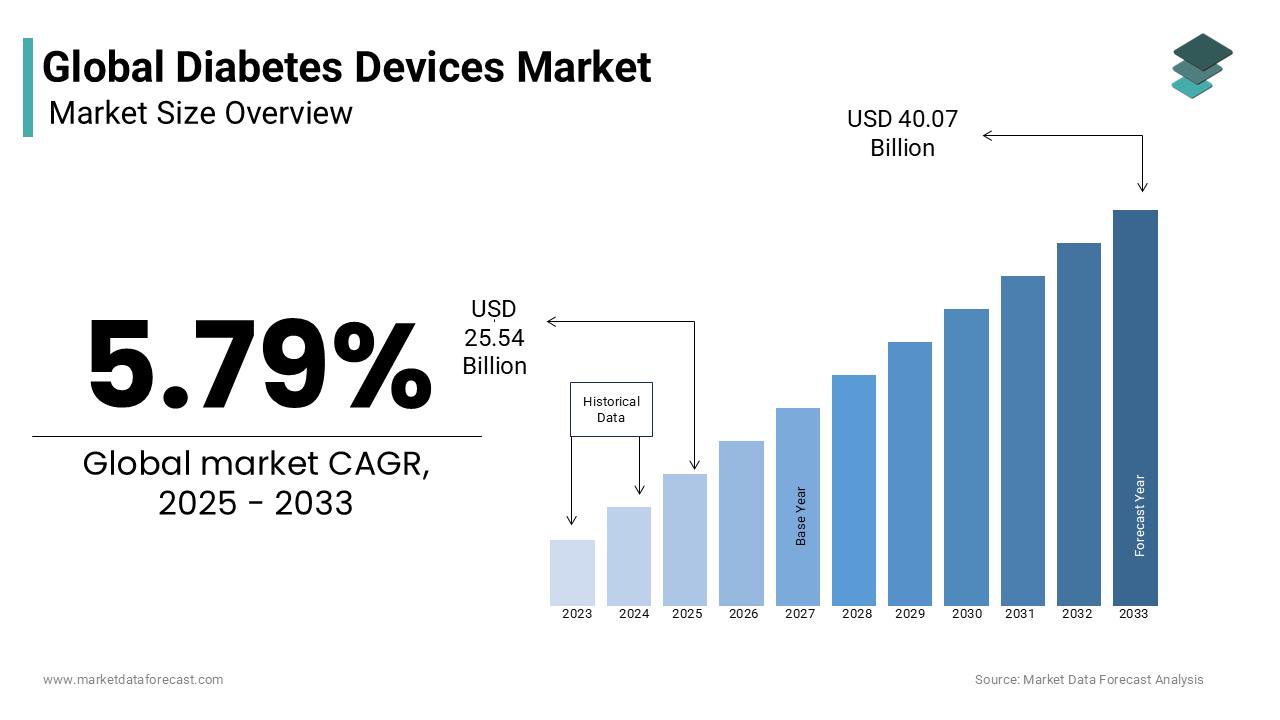

The global diabetes devices market size was valued at USD 24.14 billion in 2024 and is anticipated to reach USD 25.54 billion in 2025 from USD 40.07 billion by 2033, growing at a CAGR of 5.79% during the forecast period from 2025 to 2033.

Diabetes devices are medical technologies designed for glucose monitoring, insulin delivery, and disease management, including continuous glucose monitors (CGMs), insulin pumps, blood glucose meters, and smart pens. These devices play a critical role in enabling real-time glycemic control and reducing long-term complications associated with diabetes. As of 2023, over 537 million adults worldwide were living with diabetes, a figure projected to rise to 643 million by 2030, according to the International Diabetes Federation. The integration of digital health tools has transformed patient engagement, with increasing number of insulin-dependent individuals in high-income countries using CGMs regularly. Additionally, advancements in sensor accuracy, algorithm-driven insulin dosing, and interoperability with mobile platforms have elevated the standard of care. The growing prevalence of type 2 diabetes among younger populations and rising awareness of hypoglycemia prevention are further reinforcing the clinical necessity of advanced diabetes technologies.

MARKET DRIVERS

Rising Global Prevalence of Diabetes and Increasing Diagnosis Rates

The escalating burden of diabetes is a primary catalyst for the expansion of diabetes device adoption. Type 2 diabetes accounts for approximately 90% of cases, with increasing incidence among individuals under 40 due to sedentary lifestyles and obesity. Also, in India, over 77 million individuals are affected, as documented by the Indian Council of Medical Research, creating massive demand for affordable and scalable monitoring solutions. This surge in prevalence has prompted public health systems to expand screening programs, increasing early detection and subsequent prescription of glucose-lowering devices, particularly in urban and semi-urban healthcare settings.

Technological Advancements in Closed-Loop and Interoperable Systems

The evolution of hybrid closed-loop insulin delivery systems, often referred to as artificial pancreas systems, has significantly enhanced patient adherence and glycemic outcomes. These systems integrate CGMs with insulin pumps to automatically adjust basal insulin based on real-time glucose readings. As per clinical data published in The New England Journal of Medicine, users of the Medtronic 780G system achieved 71% time-in-range (70–180 mg/dL), a 13% improvement over sensor-augmented pumps. The FDA has approved multiple interoperable systems since 2020, including the Tidepool Loop, which allows third-party integration of Dexcom G6 and Omnipod 5, increasing patient choice. These advancements not only reduce the cognitive burden of diabetes management but also demonstrate superior clinical outcomes, driving both physician recommendations and patient demand.

MARKET RESTRAINTS

High Out-of-Pocket Costs and Inadequate Reimbursement Frameworks

Despite clinical benefits, access to advanced diabetes devices remains limited due to financial barriers. In the United States, a single CGM sensor can cost between $100 and $140 per month, with insulin pumps ranging from $5,000 to $8,000, according to the Health Care Cost Institute. Medicare and many private insurers cover CGMs for insulin-dependent patients, coverage for hybrid closed-loop systems is inconsistent. In low- and middle-income countries, out-of-pocket expenses constitute more than 80% of device costs, rendering them unaffordable for the majority. As per a 2023 study by the Lancet Global Health Commission, fewer than 5% of people with type 1 diabetes in sub-Saharan Africa have access to CGMs, highlighting a stark disparity in technological equity and limiting global market penetration.

Regulatory Heterogeneity and Delayed Market Approvals in Emerging Regions

Divergent regulatory pathways across countries create significant delays in the commercialization of diabetes devices, particularly in fast-growing markets. Countries like Indonesia and Nigeria lack specialized review divisions for digital health technologies, resulting in prolonged evaluation periods. According to the World Health Organization, only 34 of 194 member states have established medical device regulations equivalent to ISO 13485 standards. This regulatory fragmentation forces manufacturers to tailor submissions for each jurisdiction, increasing compliance costs and slowing product launches. Additionally, post-market surveillance requirements vary widely, complicating long-term device performance tracking and discouraging investment in regions with high disease burden but uncertain regulatory stability.

MARKET OPPORTUNITIES

Expansion of Digital Therapeutics and AI-Driven Personalized Management Platforms

The convergence of diabetes devices with artificial intelligence and digital therapeutics presents a transformative opportunity for personalized care. AI-powered platforms can analyze glucose trends, meal inputs, physical activity, and insulin usage to generate actionable insights and predictive alerts. Companies like DarioHealth and Livongo (now part of Teladoc) have demonstrated that behavioral nudges and real-time coaching improve HbA1c levels by an average of 0.8% over six months. Furthermore, the FDA’s Digital Health Pre-Cert Program has streamlined approval for software-as-a-medical-device (SaMD) applications, accelerating innovation. Hence, the scalability of mobile-based interventions offers a cost-effective pathway to expand access beyond traditional device users.

Integration of Non-Invasive and Minimally Invasive Glucose Monitoring Technologies

Emerging non-invasive glucose monitoring solutions are poised to overcome adherence barriers associated with finger-prick testing and subcutaneous sensors. Technologies utilizing optical spectroscopy, transdermal microneedles, and interstitial fluid analysis are advancing rapidly. In 2023, Abbott launched its Libre Sense Glucose Sport Biosensor in Europe, a minimally invasive wearable that measures glucose in athletes via a skin patch, as per the European Association for the Study of Diabetes. Similarly, the GlucoTrack device, which uses ultrasound, electromagnetic, and thermal technologies, received CE marking and is undergoing U.S. clinical trials. These innovations could dramatically improve user comfort and compliance, particularly among pediatric and elderly populations, opening new consumer segments and reducing long-term complications through continuous, pain-free monitoring.

MARKET CHALLENGES

Data Security and Privacy Risks in Connected Diabetes Devices

The increasing connectivity of diabetes devices exposes users to cybersecurity vulnerabilities and data privacy breaches. Insulin pumps and CGMs that transmit data via Bluetooth or cloud platforms are susceptible to hacking, potentially leading to unauthorized insulin dosing or data theft. In 2022, the U.S. Food and Drug Administration issued a safety communication regarding cybersecurity flaws in certain Medtronic insulin pumps, urging patients to update firmware, as documented in the FDA Medical Device Safety Network. The sensitive nature of continuous glucose data, often linked to mobile identities, raises concerns about misuse by insurers or employers. Ensuring end-to-end encryption, secure firmware updates, and regulatory compliance with HIPAA and GDPR remains a complex challenge, particularly for smaller device manufacturers lacking dedicated cybersecurity infrastructure.

Limited Long-Term Clinical Validation of Emerging Device Efficacy in Diverse Populations

While diabetes devices demonstrate strong performance in controlled trials, real-world effectiveness varies significantly across demographic and socioeconomic groups. CGM accuracy declined in individuals with darker skin pigmentation due to optical interference in sensor technology. Similarly, hybrid closed-loop systems have been predominantly tested in high-literacy, tech-savvy populations, with limited data on elderly, rural, or low-income users. Bridging these gaps requires inclusive clinical trials, culturally adapted interfaces, and robust patient support ecosystems to ensure equitable outcomes

SEGMENTAL ANALYSIS

By Type Insights

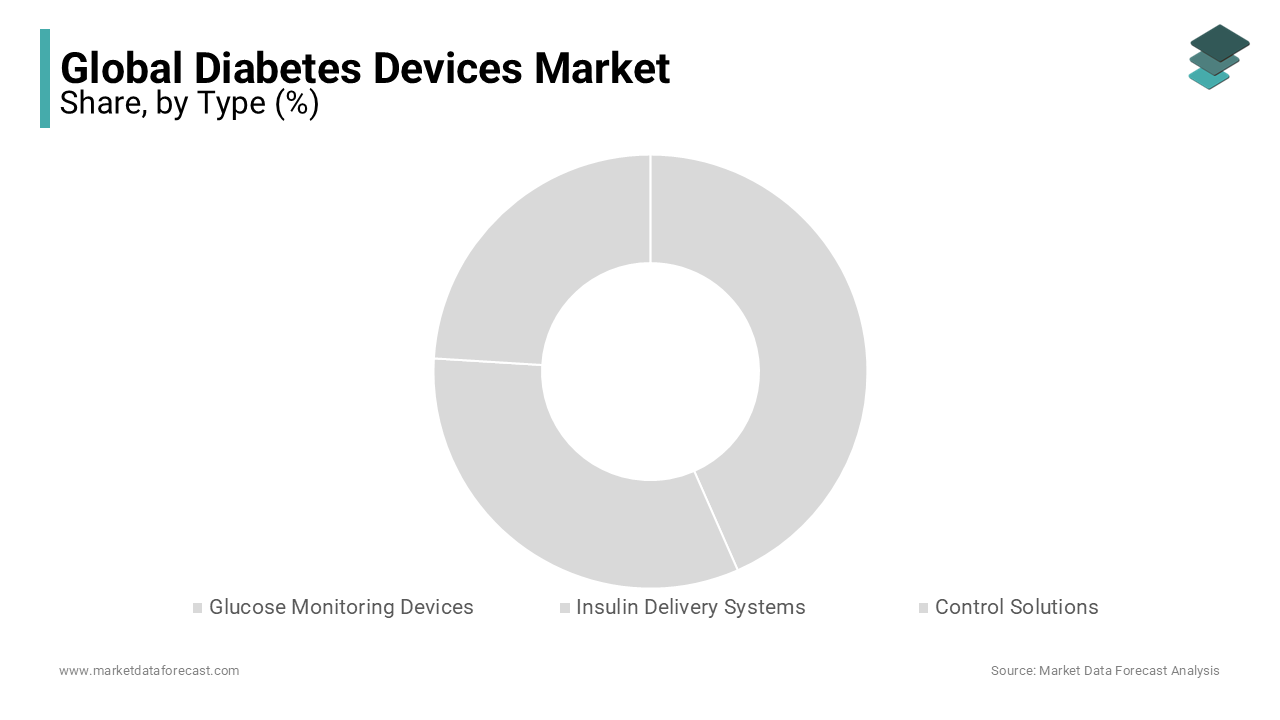

The glucose monitoring devices segment was the largest product type in the diabetes devices market by capturing a 56.6% of global revenue in 2024. This dominance is primarily driven by the widespread adoption of continuous glucose monitors (CGMs) and the critical need for real-time glycemic tracking. According to the American Diabetes Association, individuals with type 1 diabetes experience hypoglycemia for an average of 72 minutes per day, making constant monitoring essential for preventing acute complications. The shift from traditional blood glucose meters to CGMs has accelerated, with over 45% of insulin-treated patients in the U.S. now using CGM systems, as per the Centers for Disease Control and Prevention. Additionally, clinical evidence from the DIAMOND study demonstrated that CGM users achieve an average HbA1c reduction of 0.6% compared to self-monitoring, reinforcing physician confidence. The integration of CGMs with smartphone applications and telehealth platforms has further enhanced patient engagement, solidifying this segment’s central role in modern diabetes management.

The insulin delivery systems & control solutions is the fastest-growing segment and is projected to expand at a CAGR of 14.8% from 2025 to 2033. This surge is fueled by the rising adoption of hybrid closed-loop systems, commonly known as artificial pancreas systems, that automate insulin delivery based on real-time glucose data. As per clinical data from the International Journal of Clinical Endocrinology and Metabolism, patients using automated insulin delivery systems spend 72% of their day within the target glucose range (70–180 mg/dL), a 15% improvement over manual methods. The FDA has approved multiple interoperable insulin pump systems since 2020, enabling patient customization and increasing accessibility. Furthermore, the growing prevalence of type 1 diabetes in pediatric populations, over 1.2 million children globally, as reported by the International Diabetes Federation, has intensified demand for safe, automated solutions that reduce caregiver burden. Technological advancements, combined with increasing insurance coverage, are accelerating clinical integration and consumer uptake.

REGIONAL ANALYSIS

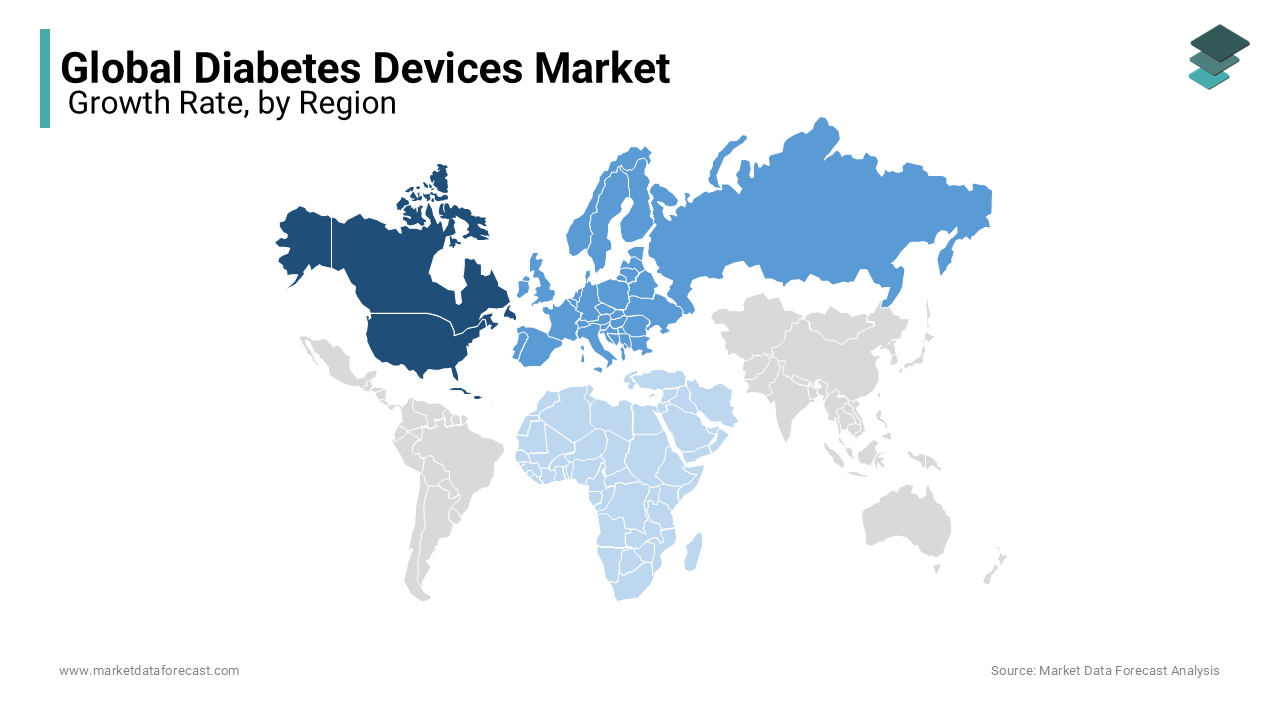

North America held the largest share of the global diabetes devices market at 41.6%, with the United States serving as the dominant force in innovation and adoption. The U.S. has the highest per capita utilization of advanced diabetes technologies, driven by a well-established network of endocrinologists and strong reimbursement support from Medicare and private insurers. As of 2023, Medicare covered CGMs for over 1.8 million beneficiaries with insulin-dependent diabetes, according to the Centers for Medicare & Medicaid Services. The country is home to leading device manufacturers such as Dexcom, Medtronic, and Tandem Diabetes Care. Additionally, the integration of diabetes devices into digital health platforms like Apple Health and Google Fit has enhanced data interoperability. With over 38 million Americans living with diabetes, as per the CDC, the domestic demand for precision management tools continues to drive technological advancement and market expansion.

Europe holds a significant market share, with Germany, the United Kingdom, and France leading in clinical adoption and regulatory standardization. The European Union’s Medical Device Regulation (EU MDR) has strengthened post-market surveillance and performance requirements, increasing trust in device reliability. Germany has implemented nationwide reimbursement for CGMs and insulin pumps under statutory health insurance, resulting in an increase in device prescriptions between 2020 and 2023. The UK’s National Health Service launched the Diabetes Technology Adoption Programme in 2022, prioritizing access to automated insulin delivery for high-risk patients. As per Diabetes UK, over 150,000 individuals now use CGMs through public healthcare channels. Additionally, the presence of research hubs like the University of Cambridge’s Wellcome-MRC Institute enhances clinical validation and innovation, positioning Europe as a leader in evidence-based technology integration.

The Asia Pacific region accounts for a notable share of the global market, with China and India emerging as high-growth centers due to rising diabetes prevalence and expanding healthcare infrastructure. China has over 141 million adults with diabetes, the highest national burden globally, as reported by the Chinese Center for Disease Control and Prevention. The government’s Healthy China 2030 initiative includes digital health integration, facilitating regulatory approval for CGMs and smart insulin pens. India, with millions of affected individuals, is witnessing increased private-sector investment in affordable glucose monitoring solutions. However, cost barriers and limited specialist access in rural areas constrain broader penetration, though telemedicine and subsidized programs are gradually improving access.

Latin America is also a key player in the market, with Brazil and Mexico representing the most advanced ecosystems for diabetes device adoption. Brazil has the highest diabetes prevalence in the region, affecting 18.7% of adults over 20, as documented by the Brazilian Ministry of Health. The country’s public health system, SUS, provides limited coverage for glucose meters but has initiated pilot programs for CGM access in type 1 diabetes patients. Private insurance plans increasingly cover insulin pumps. Mexico has seen growth in private clinics offering integrated diabetes care, supported by partnerships with U.S.-based device companies. However, import tariffs and regulatory delays hinder widespread availability. As per the Pan American Health Organization, only 8% of insulin-dependent patients in the region use CGMs, highlighting significant unmet need. Nonetheless, rising awareness and digital health adoption are creating pathways for future expansion.

The Middle East and Africa collectively represent small share of the global diabetes devices market, yet face disproportionate disease burdens. Saudi Arabia has one of the highest diabetes rates globally, with 18.3% of adults affected, as per the Saudi Ministry of Health. The country has invested in smart health initiatives, including the integration of CGMs into national diabetes registries. The UAE has established specialized diabetes centers in Dubai and Abu Dhabi, offering advanced insulin pumps and CGMs through private healthcare providers. In South Africa, the prevalence of type 2 diabetes has doubled since 2000, reaching 13.1% of adults, according to the South African Medical Research Council. However, access to devices remains limited, with fewer than 3% of type 1 patients using insulin pumps. As per the International Diabetes Federation, over 24 million people in the African region live with diabetes, but less than 5% have access to CGMs. Public-private partnerships and localized pricing models are emerging as critical enablers for future market development.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global diabetes devices market include

- Roche Diagnostics

- Johnson & Johnson

- LifeScan, Inc

- Animas Inc.

- Becton-Dickinson

- Novo Nordisk

- Bayer AG

- Abbott Laboratories

- Ypsomed AG

- Medtronic ple

- Insult Inc.

- Terumo Corporation

- Tandem Diabetes Care, Inc

- Dexcom, Inc. (U.S.).

Competition in the diabetes devices market is defined by a race for technological superiority, regulatory agility, and patient engagement across diverse healthcare ecosystems. Established leaders like Abbott, Dexcom, and Medtronic are locked in a dynamic contest to dominate both glucose monitoring and insulin delivery segments through continuous innovation and ecosystem integration. The rise of interoperable platforms and artificial intelligence has shifted the competitive axis from hardware alone to data-driven care management. Emerging regional players are challenging incumbents with lower-cost alternatives, particularly in high-prevalence, cost-sensitive markets. Differentiation is increasingly achieved through user experience, algorithm accuracy, and seamless connectivity rather than device specifications alone. Moreover, reimbursement policies, cybersecurity standards, and cultural adaptability are becoming decisive factors in market access. This evolving landscape demands not only clinical efficacy but also scalability, affordability, and deep integration into both clinical and digital health infrastructures to sustain long-term leadership.

Top Players in the Diabetes Devices Market

Abbott has significantly expanded its footprint in the Asia Pacific diabetes devices market through the widespread adoption of its FreeStyle Libre continuous glucose monitoring (CGM) system. The company has secured reimbursement in Japan, Australia, South Korea, and Thailand, enabling broader patient access across public and private healthcare systems. The company also partnered with local telehealth platforms in Indonesia and the Philippines to integrate CGM data into remote diabetes management programs. Additionally, Abbott established a regional training network for healthcare providers, conducting over 500 educational workshops in 2023 alone. These initiatives have strengthened clinical trust and accelerated device adoption, particularly among type 2 diabetes patients who previously relied on finger-prick testing.

Dexcom has intensified its strategic presence in the Asia Pacific region by advancing regulatory approvals and forging partnerships with digital health providers. In 2022, the company received approval for its Dexcom G7 CGM in Japan, a milestone that opened access to one of the most technologically advanced diabetes care markets in the region. Dexcom collaborated with the Australian Digital Health Agency to ensure interoperability of its devices with national e-health records, enhancing data continuity for clinicians. Dexcom also engaged with public hospitals in New Zealand to pilot integration of G6 into pediatric diabetes programs. These efforts reflect a focused strategy on digital integration, regulatory alignment, and user-centric service models that position Dexcom as a leader in next-generation glucose monitoring across high-income Asia Pacific markets.

Medtronic has reinforced its role in insulin delivery innovation across the Asia Pacific by expanding access to its advanced hybrid closed-loop systems. The company’s MiniMed 780G system received regulatory clearance in Australia, Singapore, and South Korea by 2023, offering automated insulin dosing with predictive low-glucose suspend technology. Medtronic partnered with Thailand’s Ministry of Public Health to conduct real-world effectiveness studies in diverse patient populations, supporting evidence-based adoption. In India, the company launched a subsidized patient assistance program for the MiniMed 770G, targeting urban centers with high concentrations of type 1 diabetes cases. Additionally, Medtronic established a regional innovation hub in Bangalore to adapt user interfaces for local languages and cultural preferences. By combining clinical validation, affordability initiatives, and localized design, Medtronic is driving the transition from manual insulin therapy to automated control solutions in a region historically reliant on basic diabetes management tools.

Top Strategies Used by Key Market Participants

Key players in the diabetes devices market are leveraging technological integration, regulatory acceleration, and patient-centric service models to strengthen their competitive positioning. Companies are prioritizing interoperability by designing devices that sync seamlessly with smartphones, electronic health records, and third-party applications to enhance data utility. Strategic partnerships with telehealth providers and national health systems are being utilized to embed devices into broader care pathways. Firms are investing in AI-driven analytics to generate personalized insights and predictive alerts, improving clinical outcomes. Regulatory harmonization is a critical focus, with manufacturers aligning submissions to meet both FDA and CE standards for faster global rollout. Additionally, direct-to-consumer distribution, subscription-based pricing, and patient support platforms are being deployed to improve adherence and long-term engagement, transforming diabetes devices from episodic tools into continuous care ecosystems.

RECENT MARKET HAPPENINGS

- In January 2023, Abbott launched the FreeStyle Libre 3 in India, featuring real-time smartphone alerts and reduced sensor size, enhancing patient comfort and adherence to strengthen its market presence.

- In September 2022, Dexcom received regulatory approval for the Dexcom G7 in Japan, enabling market entry into one of Asia’s most advanced healthcare systems and expanding its regional footprint.

- In March 2024, Medtronic initiated a real-world evidence study in collaboration with Thailand’s Ministry of Public Health to validate the MiniMed 780G system in diverse patient populations.

- In June 2023, Abbott partnered with Indonesia’s Halodoc telehealth platform to integrate FreeStyle Libre data into remote diabetes consultations, improving care continuity in underserved regions.

- In November 2023, Dexcom launched a direct-to-consumer subscription model in Singapore, offering device delivery and cloud analytics to enhance user retention and digital engagement.

REPORT COVERAGE

| Metric | Value |

|---|---|

| Base Year | 2024 |

| Market Size Available | 2024 to 2033 |

| Forecast Period | 2025 to 2033 |

| Quantitative Units | Market Size in USD Billion and CAGR from 2025 to 2033 |

| Various Analyses Included | Global, Regional & Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE; Porter's Five Forces; Competitive Landscape; Investment Opportunities |

| Segments Covered | Type and Region |

| Key Market Players | Roche Diagnostics, Johnson & Johnson, LifeScan, Inc. and Animas Inc., Becton- Dickinson, Novo Nordisk, Bayer AG, Abbott Laboratories, Ypsomed AG, Medtronic ple, insult Inc., Terumo Corporation, Tandem Diabetes Care, Inc. and Dexcom, Inc. (U.S.). |

| Regions Analyzed | North America, Europe, APAC, Latin America, Middle East & Africa |

| Countries Covered | U.S, Canada, Mexico, UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Brazil, Argentina, Chile, KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan and Other Countries |

| Report Format | PDF, Excel, PPT, BI |

| Customization | Report customization as per your requirements with respect to countries, region and segmentation. |

MARKET SEGMENTATION

This research report on the global diabetes devices market has been segmented and sub-segmented based on the type and region.

By Product Type

- Glucose Monitoring Devices

- Self-Blood Glucose Monitoring Devices

- Glucose Meters

- Test Strips

- Lancets

- Hemoglobin A1C Testing Kits

- Continuous Glucose Monitoring Devices

- Self-Blood Glucose Monitoring Devices

- Insulin Delivery Systems

- Insulin Syringes

- Insulin Pens

- Insulin Pumps

- Jet Injectors

- Control Solutions

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the Europe Diabetes Devices Market?

The Europe Diabetes Devices Market refers to medical technologies designed to monitor and manage diabetes, including glucose monitoring systems, insulin delivery devices, and continuous glucose monitoring (CGM) systems.

What are the main drivers of the Europe Diabetes Devices Market?

Key drivers include rising diabetes prevalence, technological advancements in glucose monitoring, increased healthcare spending, and growing patient awareness regarding diabetes management.

What are the major restraints in the Europe Diabetes Devices Market?

High device costs, limited reimbursement in some countries, and data security concerns associated with smart diabetes devices remain key challenges.

Which segment holds the largest share in the Europe Diabetes Devices Market?

The blood glucose monitoring devices segment holds the largest share due to their widespread adoption and affordability among diabetic patients.

Which countries dominate the Europe Diabetes Devices Market?

Germany, the United Kingdom, France, Italy, and Spain are the leading markets, supported by advanced healthcare infrastructure and high adoption of smart diabetes technologies.

What are the latest trends shaping the Europe Diabetes Devices Market?

Trends include wearable glucose sensors, non-invasive monitoring devices, AI-driven insulin delivery systems, and smartphone-based diabetes management platforms.

What are the opportunities for new entrants in the diabetes devices market?

Opportunities lie in developing affordable CGMs, introducing AI-based predictive analytics, and expanding digital insulin management ecosystems.

What regulatory standards govern diabetes devices in Europe?

Diabetes devices are regulated under the European Medical Device Regulation (MDR) and ISO 15197 standards for accuracy, safety, and performance compliance.

How does Europe compare globally in the diabetes devices market?

Europe ranks second globally, after North America, due to strong healthcare systems, high awareness levels, and adoption of advanced glucose monitoring solutions.

What is the future outlook for the Europe Diabetes Devices Market?

The market is expected to grow rapidly with increasing adoption of smart glucose sensors, digital insulin delivery, and AI-based diabetes management platforms, supporting personalized patient care across the region.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com