Global Digital Diabetes Management Market Size, Share, Trends & Growth Forecast Report By Type, Product & Service, End-User and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Market Size, 2025

$13 BnMarket Estimate, 2026

$16.03 BnMarket Forecast, 2034

$85.75 BnCAGR, 2026–2034

23.32%Global Digital Diabetes Management Market Report Summary

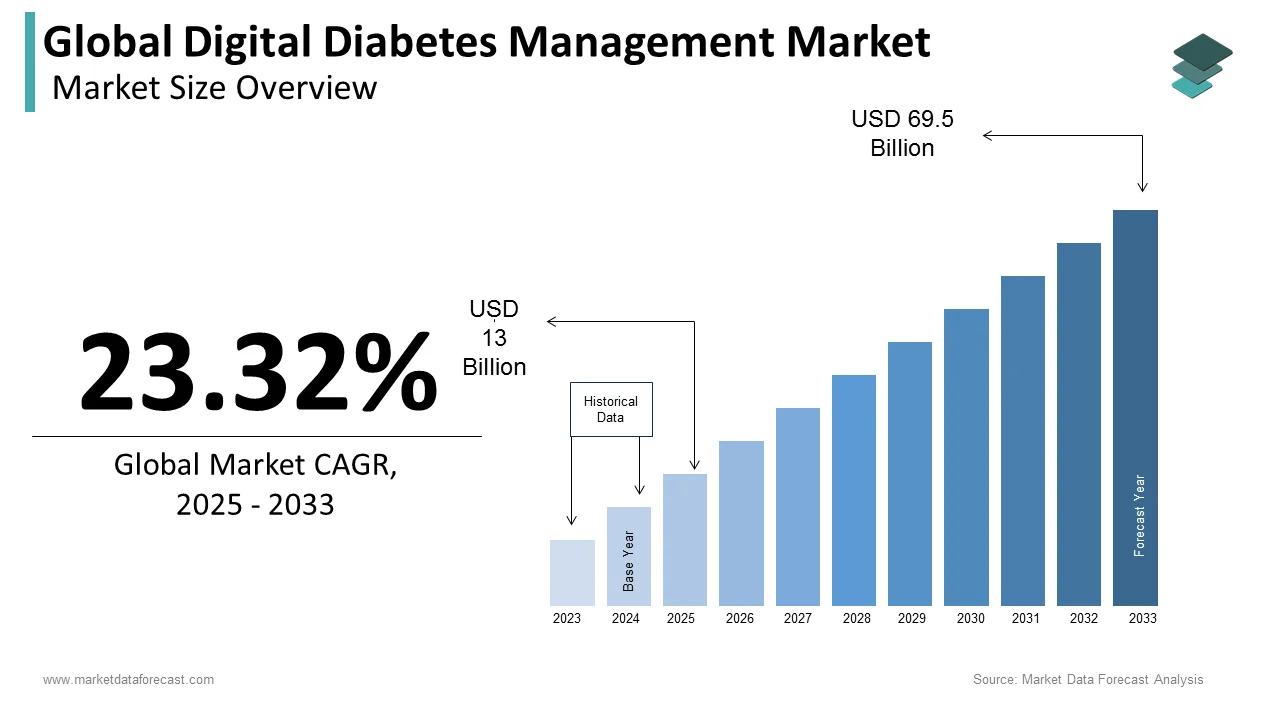

The global digital diabetes management market was valued at USD 13 billion in 2025, is estimated to reach USD 16.03 billion in 2026, and is projected to reach USD 85.75 billion by 2034, growing at a CAGR of 23.32% from 2026 to 2034. Market growth is driven by the rising global prevalence of diabetes, increasing adoption of digital health technologies, and growing demand for continuous monitoring and personalized disease management. Digital diabetes solutions, including wearable devices, mobile apps, and cloud-based platforms, are enabling real-time tracking, improved patient engagement, and better clinical outcomes. Additionally, advancements in connected devices and integration with telehealth services are further accelerating market expansion.

Key Market Trends

- Increasing adoption of wearable and continuous glucose monitoring (CGM) devices.

- Growing demand for remote monitoring and telehealth solutions.

- Rising focus on personalized and data-driven diabetes management.

- Integration of AI and cloud-based analytics in diabetes care.

- Expansion of home healthcare and self-management solutions.

Segmental Insights

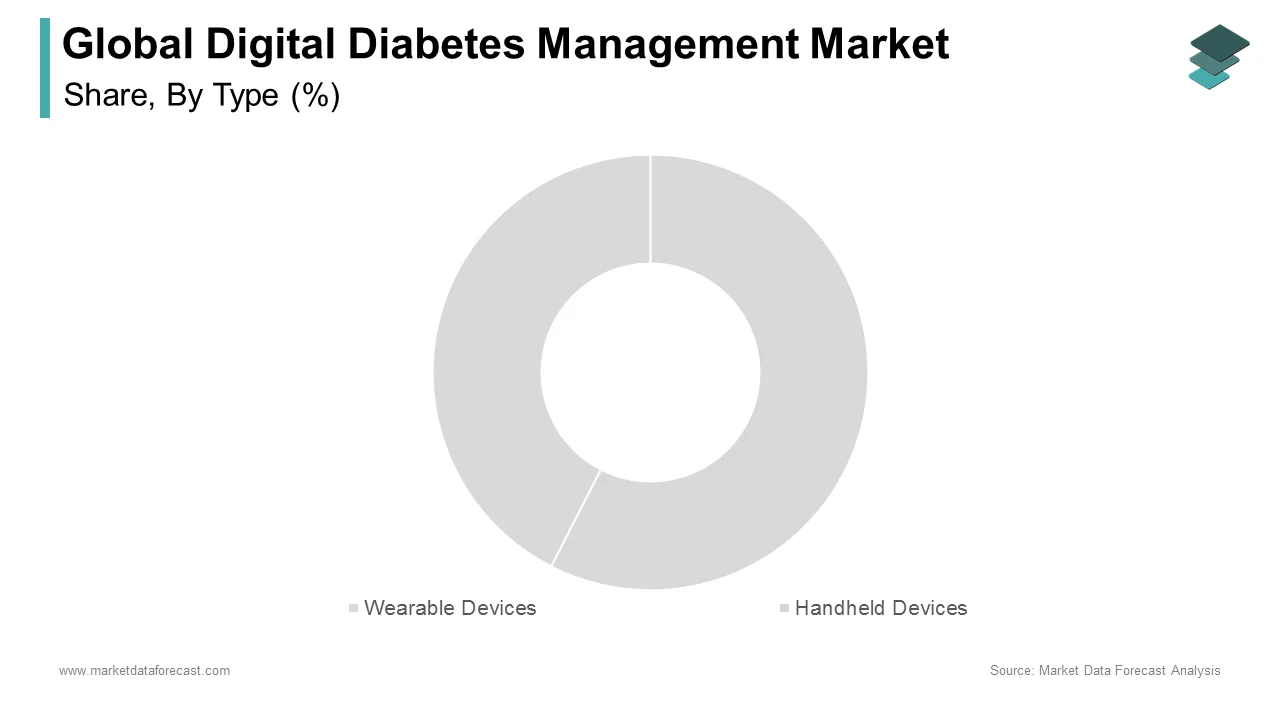

- Based on type, the wearable devices segment dominated the global digital diabetes management market by capturing 61.6% share in 2025, driven by real-time monitoring capabilities and ease of use.

- Based on end user, the individual and home healthcare segment led the market with 70.2% share in 2025, supported by increasing preference for self-management and remote care.

Regional Insights

The global digital diabetes management market is witnessing rapid growth across major regions due to rising disease prevalence and digital health adoption.

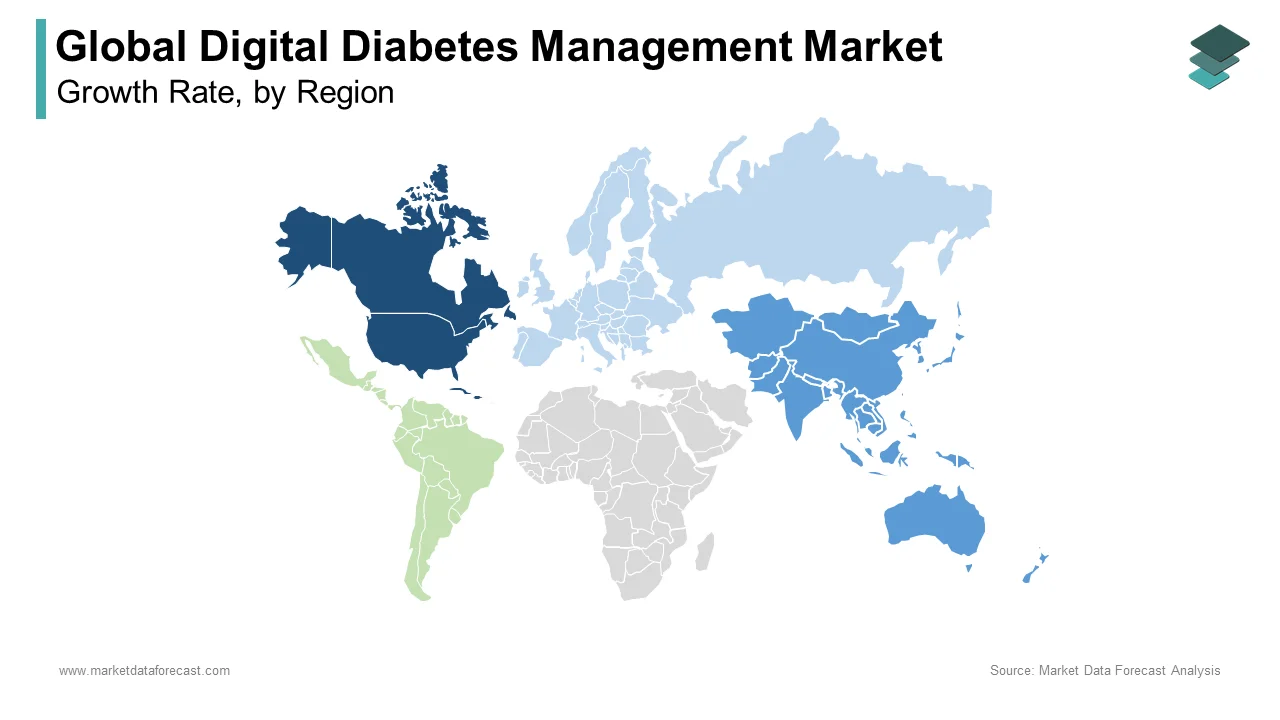

- North America led the market in 2025 with 41.2% share, supported by advanced healthcare infrastructure and high adoption of digital solutions.

- Europe holds a significant share, driven by increasing healthcare digitization and government support.

- Asia-Pacific is emerging as the fastest-growing region due to large diabetic population, improving healthcare access, and increasing adoption of digital health technologies.

Competitive Landscape

The global digital diabetes management market is highly competitive, with major medical device companies and digital health firms focusing on innovation, connectivity, and user-friendly solutions. Companies are investing in advanced wearable technologies, mobile platforms, and data analytics to enhance patient outcomes and expand their market presence.

Prominent companies operating in the global digital diabetes management market include Medtronic, B. Braun, Dexcom, Abbott Laboratories, Roche Diagnostics, Insulet Corporation, Tandem Diabetes Care, Ascensia Diabetes Care, LifeScan, Tidepool, AgaMatrix, Glooko Inc., and DarioHealth.

Global Digital Diabetes Management Market Size

The size of the global digital diabetes management market was valued at USD 13 billion in 2025. The global market is anticipated to grow at a CAGR of 23.32% from 2026 to 2034 and be worth USD 85.75 billion by 2034 from USD 16.03 billion in 2026.

Digital diabetes management encompasses a sophisticated ecosystem of connected devices, mobile applications, cloud-based platforms, and artificial intelligence algorithms designed to monitor, analyze, and optimize glycemic control for individuals living with diabetes. This sector transcends traditional glucometry by integrating Continuous Glucose Monitoring (CGM) sensors with insulin delivery systems and decision support software to create closed-loop or hybrid closed-loop therapeutic environments. As of 2026, the urgency for integrated solutions is driven by the global prevalence of diabetes. According to the International Diabetes Federation, hundreds of millions of adults worldwide are affected, with projections indicating a continued rise in the coming years. According to the World Health Organization, diabetes has been directly responsible for a significant number of deaths, underscoring the critical need for proactive management tools that prevent acute complications. Furthermore, as per the Centers for Disease Control and Prevention, a large majority of people with pre-diabetes remain unaware of their condition, creating a massive latent demand for digital screening and lifestyle intervention platforms. These technologies facilitate real-time data sharing between patients and healthcare providers, which is enabling timely adjustments to therapy and reducing the burden of chronic disease management. The shift from reactive treatment to predictive care defines the current landscape, where digital therapeutics play a pivotal role in mitigating the long-term economic and health impacts of this global epidemic.

MARKET DRIVERS

Escalating Global Prevalence of Diabetes and Need for Continuous Monitoring

The unprecedented rise in diabetes cases globally, which needs a shift from intermittent finger-prick testing to continuous and real-time glucose monitoring, is primarily fuelling the growth of the digital diabetes management market. The sheer volume of patients overwhelms traditional healthcare models, making scalable digital solutions essential for effective disease management. According to the International Diabetes Federation, a significant proportion of adults currently live with diabetes, and this ratio is expected to worsen as urbanization and sedentary lifestyles spread across developing nations. Continuous Glucose Monitoring systems, a cornerstone of digital management, provide detailed insights into glycemic trends that single-point measurements cannot capture. This density of data is crucial for preventing hypoglycemic events, which the American Diabetes Association notes occur frequently in patients on intensive insulin therapy. The ability of digital platforms to aggregate this data and present it in actionable formats empowers patients to make immediate lifestyle and dosing decisions. Furthermore, the aging population in developed countries contributes to higher incidence rates of Type 2 diabetes, driving demand for user-friendly apps that assist elderly patients with medication adherence. As the patient pool expands exponentially, the capacity of manual management diminishes, forcing healthcare systems to adopt digital tools that can handle large-scale monitoring without proportional increases in clinical staff, thereby securing the market's robust growth trajectory.

Technological Advancements in Closed-Loop Systems and Artificial Intelligence

Rapid technological innovations in automated insulin delivery systems and artificial intelligence-driven analytics are further contributing to the global digital diabetes management market expansion. The evolution from simple monitoring to hybrid closed-loop systems, often called artificial pancreases, represents a paradigm shift where algorithms automatically adjust insulin delivery based on real-time sensor data. As per the Juvenile Diabetes Research Foundation, users of advanced hybrid closed-loop systems experience improved time-in-range compared to standard pump therapy, significantly reducing the risk of long-term complications. Machine learning algorithms now analyze historical glucose data, carbohydrate intake, and physical activity to predict future glucose levels with high accuracy, allowing for pre-emptive interventions. These smart systems reduce the cognitive burden on patients, who no longer need to perform complex calculations for every meal or activity. The integration of these devices with smartphone ecosystems enables seamless data synchronization and remote monitoring by caregivers. Additionally, advancements in sensor technology have extended the wear time of CGM devices, which is improving user compliance. The convergence of hardware miniaturization, sophisticated software, and connectivity creates a compelling value proposition that drives adoption among both Type 1 and insulin-dependent Type 2 diabetes populations, which is further fuelling market momentum.

MARKET RESTRAINTS

High Cost of Advanced Devices and Limited Reimbursement Coverage

The prohibitive cost of advanced devices such as Continuous Glucose Monitors and automated insulin pumps, coupled with inconsistent reimbursement policies across different regions, is a significant impediment to the digital diabetes management market growth. The upfront expense for these devices often places them out of reach for many patients without adequate insurance coverage. According to the American Diabetes Association, a considerable portion of people with diabetes in the United States ration their insulin or skip monitoring due to cost, which is a situation that is far more severe in low and middle-income countries where out-of-pocket expenses dominate. In many European and Asian markets, public health systems have been slow to update reimbursement lists to include the latest digital therapeutics and connected devices, creating a disparity in access. The complexity of navigating insurance claims further discourages potential users, particularly those with Type-2 diabetes who are often deemed lower priority for expensive technology despite benefiting from tight glycemic control. Manufacturers face pressure to lower prices, but high research and development costs for regulatory approval limit their ability to do so. Until payers recognize the long-term cost savings of preventing complications through digital management and expand coverage universally, financial constraints will remain a formidable restraint on market penetration.

Data Privacy Concerns and Cybersecurity Vulnerabilities in Connected Devices

Growing concerns regarding data privacy and the cybersecurity risks associated with connected medical devices pose a critical restraint on the digital diabetes management market. These devices collect vast amounts of sensitive personal health information, including real-time location, dietary habits, and detailed physiological data, making them attractive targets for cyberattacks. As noted by the Food and Drug Administration, there has been a noticeable increase in cybersecurity vulnerabilities identified in connected insulin pumps and glucose monitors, with some devices susceptible to unauthorized access. High-profile data breaches in the healthcare sector have eroded patient trust, leading to hesitation in adopting fully connected ecosystems. The General Data Protection Regulation in Europe and similar laws globally impose strict requirements on data handling, increasing the compliance burden for manufacturers and potentially slowing product launches. Patients worry about their data being sold to third parties such as insurers or employers, which could lead to discrimination. The lack of standardized security protocols across different device manufacturers complicates the integration of diverse tools into a unified platform. Until robust, universally accepted cybersecurity frameworks are established and transparent data governance policies are enforced, fear of privacy violations and potential hacking will continue to dampen consumer confidence and slow market uptake.

MARKET OPPORTUNITIES

Expansion into Pre-diabetes and Lifestyle Intervention Markets

A promising opportunity for the digital diabetes management market is in expanding its focus beyond diagnosed patients to the vast population suffering from pre-diabetes and those seeking preventive lifestyle interventions. According to the World Health Organization, hundreds of millions of people globally are affected by prediabetes, representing a massive untapped market for digital platforms that offer coaching, nutrition tracking, and activity monitors to prevent disease progression. Unlike traditional medical devices, which are prescribed after diagnosis, digital health apps can be deployed at scale to at-risk individuals through corporate wellness programs and insurance incentives. As per The Lancet Digital Health, digital lifestyle intervention programs have demonstrated significant reductions in the risk of developing Type 2 diabetes, comparable to pharmaceutical interventions. This preventative approach appeals to payers who seek to avoid the high costs of chronic disease management. Companies can leverage gamification and behavioral psychology within apps to engage users who may not yet identify as patients. The integration of wearable fitness trackers with glucose monitoring capabilities allows for holistic health insights, appealing to the broader wellness consumer. By positioning digital tools as essential for metabolic health rather than just disease management, manufacturers can access a much larger customer base and create recurring revenue streams through subscription models, driving significant market growth.

Integration of Remote Patient Monitoring into Value-Based Care Models

The global shift towards value-based care models presents a lucrative opportunity for the digital diabetes management market. Healthcare systems are increasingly moving away from fee-for-service structures to models where providers are reimbursed based on patient outcomes, which is creating a strong financial incentive to adopt tools that improve glycemic control and reduce hospitalizations. According to the Centers for Medicare and Medicaid Services, new reimbursement codes for remote monitoring services allow physicians to bill for the time spent reviewing patient data and adjusting treatment plans remotely. Digital diabetes management platforms facilitate this by automatically transmitting glucose data to electronic health records and are enabling clinicians to intervene before conditions deteriorate. This capability is particularly valuable for managing patients in rural or underserved areas where access to endocrinologists is limited. The ability to monitor large patient panels efficiently allows clinics to expand their reach without increasing overhead. Furthermore, data generated by these platforms provides real-world evidence that can be used to refine treatment guidelines and demonstrate the efficacy of specific therapies. As healthcare providers strive to meet quality metrics and reduce readmission penalties, the adoption of RPM-enabled digital diabetes tools will accelerate, opening new channels for market expansion.

MARKET CHALLENGES

Interoperability Issues and Fragmentation of Digital Health Ecosystems

The lack of interoperability between diverse devices, software platforms, and electronic health record systems is challenging the digital diabetes management market expansion. Patients often use sensors from one manufacturer, pumps from another, and apps from a third, resulting in disjointed data streams that are difficult to synthesize into a coherent clinical picture. As per the Office of the National Coordinator for Health Information Technology, the absence of universal data standards hinders the seamless exchange of information, forcing clinicians to manually collate data from multiple portals or rely on incomplete datasets. This fragmentation reduces the effectiveness of decision support algorithms that require comprehensive inputs to generate accurate recommendations. Manufacturers frequently employ proprietary communication protocols to lock users into their specific ecosystems, resisting integration with competitor products. This lack of cohesion complicates the workflow for healthcare providers who must navigate multiple interfaces to monitor a single patient. The industry struggles to agree on common APIs and data formats, slowing the development of truly integrated solutions. Until regulatory bodies enforce stricter interoperability mandates and industry consortia establish unified standards, the inefficiency caused by fragmented ecosystems will remain a significant hurdle to optimizing patient care and scaling digital solutions.

User Adherence Fatigue and Complexity of Long-Term Engagement

Maintaining long-term user adherence and engagement remains a significant challenge for the digital diabetes management market, as the chronic nature of the disease often leads to technology fatigue and burnout. While initial adoption rates for new devices and apps are high, research indicates that a significant portion of users discontinue regular use within months due to the daily burden of wearing sensors, calibrating devices, and interacting with complex software interfaces. According to Diabetes Care, alarm fatigue from frequent hyperglycemic or hypoglycemic alerts causes many patients to mute or ignore their devices, reducing the safety benefits of continuous monitoring. The psychological toll of constant surveillance can also lead to anxiety and disengagement, particularly among adolescents and young adults. Furthermore, the complexity of interpreting data trends without adequate support can overwhelm users, leading to frustration and abandonment of the technology. Digital solutions often fail to account for the behavioural and emotional aspects of living with diabetes, focusing too heavily on data metrics rather than user experience. Developing intuitive, low-burden interfaces and incorporating adaptive AI that minimizes unnecessary alerts is critical but technically challenging. Without solving the adherence equation, the full potential of digital management tools to improve long-term health outcomes will remain unrealized, posing a continuing challenge for market sustainability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | By Type, Products & Services, End-User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Medtronic (Ireland), B. Braun (Germany), Dexcom (United States), Abbott Laboratories (United States), Roche Diagnostics (Switzerland), Insulet Corporation (United States), Tandem Diabetes Care (United States), Ascensia Diabetes Care (Switzerland), LifeScan (United States), Tidepool (United States), AgaMatrix (United States), Glooko Inc. (United States), and DarioHealth (Israel). |

SEGMENTAL ANALYSIS

By Type Insights

The wearable devices segment led the market by holding 61.6% of the global market share in 2025. The dominance of the wearable devices segment in the global market is primarily attributed to the paradigm shift from reactive finger-prick testing to proactive continuous monitoring, which offers patients unprecedented visibility into their glycemic trends without disrupting daily life. The ability of wearable devices to provide continuous glucose data that significantly improves clinical outcomes compared to intermittent monitoring methods is further contributing to the dominance of the wearable devices segment in this regional market. Unlike handheld devices that offer a single snapshot in time, wearables such as Continuous Glucose Monitoring sensors capture multiple readings daily, revealing patterns of hyperglycemia and hypoglycemia that would otherwise go undetected. According to the Juvenile Diabetes Research Foundation, users of wearable CGM systems demonstrate improved time-in-range, a critical metric associated with reduced risks of long-term complications. The American Diabetes Association emphasizes that this density of data allows clinicians to make more precise insulin dosing adjustments, which leads to better overall glycemic control. Furthermore, the real-time alert features of these devices warn patients of impending low blood sugar events, preventing severe emergencies. As per the Centers for Disease Control and Prevention, effective use of continuous monitoring can reduce emergency department visits related to severe hypoglycemia. This proven track record of improving patient safety and health metrics has made wearable devices the standard of care for Type 1 diabetes and increasingly for insulin-dependent Type 2 diabetes, which is securing their market leadership.

However, the handheld devices segment is another promising segment and is projected to register the highest CAGR of 10.6% over the forecast period. While currently smaller than the wearable sector, this segment is experiencing rapid expansion due to technological innovations that transform traditional glucometers into smart, connected hubs for data management. The rapid integration of Bluetooth and Wi-Fi connectivity into traditional blood glucose meters, which is bridging the gap between legacy hardware and modern digital ecosystems, is further supporting the expansion of the handheld devices segment in this global market. Manufacturers are upgrading standard glucometers to automatically transmit readings to mobile applications, eliminating manual logging errors and enabling comprehensive data analysis. According to the International Diabetes Federation, hundreds of millions of people with diabetes globally still rely on finger-prick testing due to cost or availability constraints, representing a massive installed base ready for digital upgrades. As per the World Health Organization, handheld meters remain the most accessible tool for diabetes management in low and middle-income countries, and digitizing these devices is the most viable strategy for scaling remote monitoring initiatives. These smart handhelds often include features like voice guidance for the visually impaired and color-coded results, enhancing accessibility. The ability to aggregate data from these ubiquitous devices into cloud platforms allows healthcare providers to monitor large populations effectively. As connectivity becomes a standard feature rather than a premium add-on, the volume of smart handheld device sales is surging, which is driving double-digit growth in this segment.

By End User Insights

The individual and home healthcare segment accounted for the dominating share of 70.2% of the global market in 2025 due to the chronic nature of diabetes, which requires 24/7 management primarily occurring outside of clinical settings. The global healthcare shift towards decentralized care models that empower patients to manage their condition independently within their own homes is further boosting the dominance of the individual and home healthcare segment in the global market. Diabetes management is inherently a daily and hourly endeavour that cannot be confined to periodic hospital visits, necessitating tools that function effectively in domestic environments. According to the Centers for Disease Control and Prevention, people with diabetes spend the vast majority of their time outside clinical settings, meaning most self-care decisions happen at home, work, or school. Digital tools such as mobile apps, connected meters, and wearable sensors are specifically designed to support this autonomy, which provides real-time feedback and decision support exactly when and where it is needed. The rise of telehealth has further reinforced this trend, allowing physicians to review home-generated data remotely and adjust treatment plans without requiring physical appointments. This decentralization reduces the strain on overcrowded hospitals and lowers healthcare costs. Patients increasingly prefer the comfort and privacy of managing their health at home, avoiding the stigma and inconvenience of frequent clinic visits. The proliferation of user-friendly consumer electronics that integrate seamlessly into daily routines has made home management not only feasible but preferable. This fundamental structural reality of chronic disease care ensures that the individual and home sector remains the largest revenue generator.

On the other hand, the hospitals and specialty diabetes clinics segment is projected to experience the fastest CAGR of 15.1% over the forecast period, owing to the integration of advanced digital platforms into institutional workflows to manage complex cases and optimize inpatient care. The increasing integration of sophisticated digital diabetes management platforms into inpatient glycemic control protocols to improve patient safety and outcomes is further contributing to the expansion of the hospitals and specialty diabetes clinics segment in the global market. Hyperglycemia is a common issue in hospitalized patients, even those without a prior diabetes diagnosis, and is associated with higher mortality rates and longer lengths of stay. According to the Society of Hospital Medicine, implementing centralized digital monitoring systems that aggregate glucose data from multiple bedside devices allows nursing staff to respond to abnormalities instantly, reducing the incidence of adverse events. Hospitals are investing in enterprise-level software that integrates with Electronic Health Records to provide a unified view of patient data, facilitating coordinated care among endocrinologists, surgeons, and primary care teams. The ability to remotely monitor patients across different wards from a central nursing station improves efficiency and allows for rapid titration of insulin infusions. Regulatory bodies are also imposing stricter standards for inpatient glycemic control, compelling hospitals to adopt advanced digital solutions to maintain accreditation. The transition from paper charts to fully digital, automated documentation systems streamlines workflows and reduces medical errors. As the clinical evidence supporting tight inpatient control mounts, hospitals are rapidly upgrading their infrastructure, driving significant growth in this institutional segment.

REGIONAL ANALYSIS

North America Digital Diabetes Management Market Analysis

North America held the leading position in the global digital diabetes management market with 41.2% of the global market share in 2025. The lead of North American is majorly driven by the United States, which boasts the highest penetration of advanced diabetes technologies, robust reimbursement frameworks, and a concentrated presence of key industry innovators. Favorable reimbursement policies for Continuous Glucose Monitoring and remote therapeutic monitoring have removed financial barriers for millions of beneficiaries. According to the American Diabetes Association, a significant proportion of individuals with Type 1 diabetes in the US now use CGM technology, a rate higher than any other region. The presence of major corporations such as Dexcom, Abbott, and Medtronic fosters a competitive environment that drives rapid product iteration and availability. Furthermore, the high prevalence of obesity and Type 2 diabetes creates a massive addressable market for digital solutions. The mature healthcare infrastructure supports seamless integration of digital tools into electronic health records, facilitating data-driven care. High disposable income levels and strong patient advocacy groups also contribute to aggressive adoption of cutting-edge technologies. These converging factors ensure that North America remains the primary revenue generator and innovation hub for the global digital diabetes ecosystem.

Europe Digital Diabetes Management Market Analysis

Europe accounted for a promising share of the digital diabetes management market in 2025. The strong government-led healthcare initiatives and a growing emphasis on standardized digital health regulations across the European Union are driving the European market expansion. Europe benefits from universal healthcare systems that increasingly recognize the cost-effectiveness of digital diabetes management in preventing long-term complications. Germany, France, and the United Kingdom are the primary contributors, having updated reimbursement guidelines to include a wider range of CGM systems and digital health applications. As per the European Commission, the Digital Europe Programme is funding projects to create cross-border digital health infrastructures, facilitating the sharing of best practices and data. The implementation of the Medical Device Regulation has raised quality standards, ensuring that only safe and effective digital tools reach the market. Rising awareness of the economic burden of diabetes is prompting national health services to invest in preventive digital solutions. The region's strong focus on data privacy under GDPR has also spurred the development of secure, compliant platforms that build patient trust. Despite some fragmentation in national policies, the overall trend towards harmonization and value-based care is driving steady adoption of digital diabetes technologies across the continent.

Asia Pacific Digital Diabetes Management Market Analysis

The Asia Pacific region is emerging as a dynamic growth engine in the digital diabetes management market and currently holds a notable share of the worldwide market, and exhibits the highest potential for future expansion. This rise is driven by the exploding prevalence of diabetes in populous nations like China and India, coupled with the rapid digitalization of healthcare infrastructure and increasing government support. China has identified diabetes prevention and control as a national priority in its Healthy China 2030 initiative, leading to significant investments in local manufacturing of digital health devices. According to the International Diabetes Federation, the Western Pacific region accounts for the largest number of adults living with diabetes globally, creating urgent demand for scalable management solutions. The widespread adoption of smartphones and mobile internet enables the rapid deployment of app-based management tools, bypassing the need for expensive legacy infrastructure. Japan remains a hub for technological innovation, with its aging population driving demand for automated and user-friendly devices. The proliferation of telemedicine services and partnerships between global players and local distributors is making advanced technologies more accessible. Rising middle-class incomes and increasing health awareness are further which is fuelling the transition from traditional to digital management methods, positioning Asia Pacific as a critical frontier for market growth.

Latin America Digital Diabetes Management Market Analysis

Latin America occupies a modest but growing position in the global digital diabetes management market. The improvement in healthcare access and government initiatives to combat the rising tide of diabetes in countries like Brazil and Mexico are driving the market expansion in Latin America. The region faces challenges due to economic disparities, yet there is a concerted effort to integrate digital tools into public health systems to manage the high burden of disease more efficiently. In Brazil, the Ministry of Health has launched programs to distribute free glucose monitors and is exploring the inclusion of digital monitoring apps in the public healthcare portfolio. According to the Pan American Health Organization, diabetes is a leading cause of death in the region, prompting governments to seek cost-effective digital solutions to reduce hospitalizations. The growing penetration of mobile phones even in remote areas offers a unique opportunity to leapfrog traditional care models with mobile-first diabetes management strategies. Private insurance sectors in countries like Chile and Colombia are beginning to cover digital health services, encouraging adoption among the affluent population. Local startups are developing culturally relevant and affordable apps tailored to regional needs. While infrastructure gaps persist, the combination of urgent medical need and mobile connectivity is fostering a conducive environment for gradual but steady market expansion.

Middle East and Africa Digital Diabetes Management Market Analysis

The market in the Middle East and Africa region holds the smallest share of the global market, yet it displays promising signs of development driven by extremely high diabetes prevalence rates in the Gulf Cooperation Council countries and strategic health diversification plans. Countries like Saudi Arabia and the United Arab Emirates have some of the highest diabetes rates in the world, prompting aggressive government investment in advanced healthcare technologies as part of their Vision 2030 agendas. According to the International Diabetes Federation, the Middle East and North Africa region has the highest comparative prevalence of diabetes globally, creating a critical imperative for effective management tools. Governments in the Gulf are building world-class medical cities and integrating digital health records to improve care coordination. In Africa, while challenges related to infrastructure and affordability remain significant, mobile health initiatives are gaining traction, leveraging the continent's high mobile phone usage to deliver basic diabetes education and monitoring support. International aid organizations and NGOs are partnering with tech firms to pilot low-cost digital solutions in sub-Saharan Africa. The recognition of diabetes as a major threat to economic productivity is driving policy changes that favor digital adoption. Although the market is currently nascent, the sheer magnitude of the disease burden and the commitment of wealthy nations in the region to innovate suggest a positive long-term trajectory for digital diabetes management.

COMPETITIVE LANDSCAPE

The competition in the digital diabetes management market is intense and characterized by rapid technological innovation among established medical device giants and agile digital health startups striving for ecosystem dominance. Major corporations leverage their extensive manufacturing capabilities and regulatory expertise to launch integrated closed-loop systems, while newer entrants differentiate themselves through superior software user interfaces and artificial intelligence-driven analytics. The landscape is dynamic with frequent strategic alliances as hardware manufacturers seek to integrate their devices with leading software platforms to offer end-to-end solutions. Competitive pressure drives continuous improvements in sensor accuracy, wear time, and ease of use to reduce patient burden and enhance adherence. Companies are increasingly competing on the ability to provide predictive insights and automated dosing adjustments that minimize human intervention. Regulatory approval speed and the ability to secure broad insurance reimbursement serve as critical battlegrounds for market share. The shift towards interoperable systems that allow mixing and matching of components from different vendors further intensifies rivalry as firms race to establish their platforms as the industry standard for connected diabetes care globally.

KEY MARKET PARTICIPANTS

Leading companies operating in the global digital diabetes management market are

- Medtronic (Ireland)

- B. Braun (Germany)

- Dexcom (United States)

- Abbott Laboratories (United States)

- Roche Diagnostics (Switzerland)

- Insulet Corporation (United States)

- Tandem Diabetes Care (United States)

- Ascensia Diabetes Care (Switzerland)

- LifeScan (United States)

- Tidepool (United States)

- AgaMatrix (United States)

- Glooko Inc. (United States)

- DarioHealth (Israel)

TOP PLAYERS IN THE MARKET

- Abbott Laboratories stands as a global pioneer in the digital diabetes management sector through its revolutionary FreeStyle Libre family of continuous glucose monitoring systems. The company has democratized access to real-time glucose data by introducing factory-calibrated sensors that eliminate the need for routine finger pricks, thereby transforming patient behavior worldwide. Their recent strategic actions focus on expanding sensor wear duration to 14 days and enhancing connectivity with smart insulin pumps and mobile health applications. Abbott actively collaborates with technology giants to integrate glucose data into broader digital health ecosystems, enabling seamless data sharing between patients and providers. They continue to invest heavily in manufacturing scalability to meet surging global demand while driving down costs to improve accessibility in emerging markets. By consistently launching next-generation sensors with smaller profiles and improved accuracy, Abbott reinforces its leadership in empowering individuals to manage their condition with greater confidence and precision.

- Dexcom Inc maintains a dominant presence in the market by specializing exclusively in continuous glucose monitoring technology designed for high accuracy and real-time data transmission. The company is renowned for its G7 and G8 sensor platforms, which offer rapid warm-up times and direct-to-smartphone connectivity without the need for separate receivers. Dexcom recently intensified its efforts to integrate its devices with automated insulin delivery systems from major pump manufacturers, creating robust closed-loop ecosystems that mimic pancreatic function. Their strategy involves expanding indications for use to include patients with Type 2 diabetes not on intensive insulin therapy, significantly broadening their addressable market. Dexcom also focuses on developing advanced analytics software that provides actionable insights and predictive alerts to prevent hypoglycemic events. Through strategic partnerships with telehealth providers and digital health platforms, they ensure their data reaches caregivers instantly. These continuous innovations in sensor miniaturization and algorithmic intelligence solidify their role as a critical enabler of modern automated diabetes care.

- Medtronic plc contributes substantially to the global market by offering comprehensive hybrid closed-loop systems that combine continuous glucose monitoring with automated insulin delivery capabilities. The company distinguishes itself through its MiniMed portfolio, which integrates sensors, pumps, and algorithms into a unified therapeutic solution that automatically adjusts basal insulin rates. Medtronic has recently launched advanced algorithms capable of predicting glucose trends hours in advance to proactively suspend or increase insulin delivery. They are actively expanding their digital infrastructure by launching cloud-based data platforms that allow clinicians to monitor patient trends remotely and intervene promptly. Their strategy includes securing regulatory approvals for wider age groups and integrating their systems with popular third-party diabetes management apps. Medtronic also invests in global training programs to educate healthcare providers on optimizing closed-loop therapy settings. By focusing on full system integration and remote care capabilities, Medtronic continues to drive the transition towards fully automated artificial pancreas technologies for diverse patient populations.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the digital diabetes management market primarily employ strategic partnerships and ecosystem integrations to create seamless closed-loop solutions that connect sensors, pumps, and software platforms. Companies frequently collaborate with technology firms and pharmaceutical giants to enhance data interoperability and expand the functionality of their devices within broader health networks. Another major strategy involves heavy investment in research and development to miniaturize sensors, extend wear durations, and improve algorithmic accuracy for predictive glucose control. Manufacturers are increasingly focusing on expanding clinical indications to include Type 2 diabetes populations and younger children to capture untapped market segments. Expanding global distribution networks and securing favorable reimbursement policies in key regions help firms increase accessibility and adoption rates. Additionally, companies are developing comprehensive cloud-based data analytics platforms that provide actionable insights for both patients and clinicians to foster long-term engagement. These collaborative and innovation-driven approaches enable market participants to build robust ecosystems that improve patient outcomes while securing competitive advantages.

MARKET SEGMENTATION

This research report on the global digital diabetes management market has been segmented and sub-segmented based on type, products & services, end-user, and region.

By Type

- Wearable Devices

- Handheld Devices

By Product and Service

- Devices

- Smart Glucose Meters

- Continuous Glucose Monitoring Systems

- Smart Insulin Pens

- Smart Insulin Pumps/Closed-Loop Systems and Smart Insulin Patches

- Applications

- Digital Diabetes Management Apps

- Diabetes and Blood Glucose Tracking Apps

- Weight and Diet Management Apps

- Data Management Software and Platforms

- Services

By End-User

- Individual/Home Healthcare

- Hospitals and Specialty Diabetes Clinics

- Academic and Research Institutes

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. Which technologies dominate the global digital diabetes management market?

Continuous glucose monitoring systems and smart insulin pens are key technologies driving growth in the global digital diabetes management market

2. How do wearable devices impact the global digital diabetes management market?

Wearable glucose monitors enable real-time tracking and data sharing, enhancing patient adherence in the global digital diabetes management market

3. What regional trends exist in the global digital diabetes management market?

North America leads with a large market share, while Asia Pacific is the fastest-growing region in the global digital diabetes management market

4. How does telemedicine influence the global digital diabetes management market?

Telemedicine platforms enable remote monitoring and consultations, expanding access and growth in the global digital diabetes management market

5. What role do AI and machine learning play in the global digital diabetes management market?

AI enhances predictive analytics and personalized insulin dosing, advancing innovation in the global digital diabetes management market

6. Which end users are key in the global digital diabetes management market?

Hospitals, clinics, and individual consumers are major end users adopting digital diabetes management solutions worldwide

7. How do government initiatives affect the global digital diabetes management market?

Programs promoting diabetes awareness and digital health adoption support market expansion in the global digital diabetes management market

8. What challenges does the global digital diabetes management market face?

Challenges include device costs, data privacy concerns, and integration with healthcare systems in the global digital diabetes management market

9. What advantages do smart insulin pens offer in the global digital diabetes management market?

Smart pens offer accurate dosing, data tracking, and easier management, fueling adoption in the global digital diabetes management market

10. How is real-time glucose monitoring improving outcomes in the global digital diabetes management market?

Real-time monitoring aids timely interventions and better glycemic control, reducing complications in the global digital diabetes management market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com