Global Wearable Medical Devices Market Size, Share, Trends & Growth Forecast Report - Segmented By Diagnostic Wearable Devices (Wearable Electro-Cardiographs, Wearable Sleep Monitoring Devices, Heart Rate Monitors, Blood Pressure Monitors, Activity Monitors and Electro Encephalogram), Therapeutic Wearable Devices, Application & Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) - Industry Analysis From 2026 to 2034

Market Size, 2025

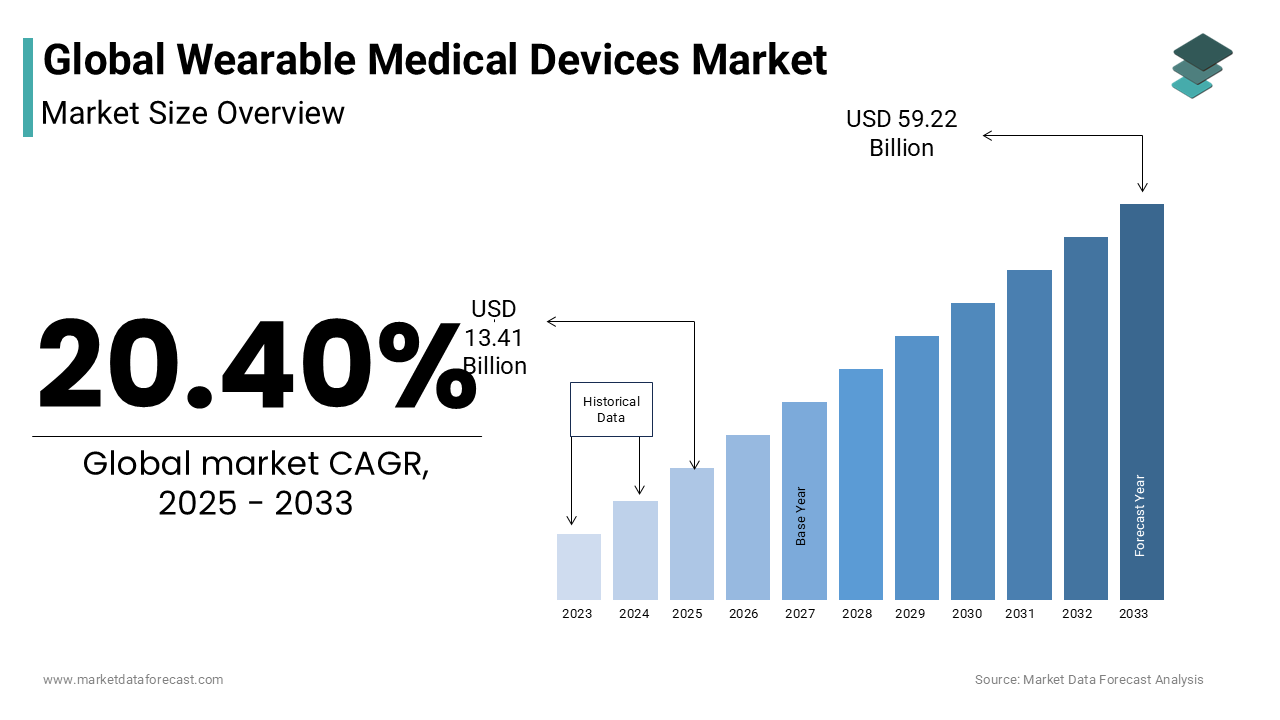

$13.41 BnMarket Estimate, 2026

$16.15 BnMarket Forecast, 2034

$71.32 BnCAGR, 2026–2034

20.40%Global Wearable Medical Devices Market Size

The global wearable medical devices market size was valued at USD 13.41 billion in 2025 and is anticipated to reach USD 16.15 billion in 2026 from USD 71.32 billion by 2034, growing at a CAGR of 20.40%. during the forecast period from 2026 to 2034.

The wearable medical devices are a class of non-invasive, body-worn technologies engineered to continuously monitor, record, and transmit physiological data for diagnostic, therapeutic, or preventive healthcare purposes. These devices include continuous glucose monitors (CGMs), wearable ECG patches, smart hearing aids, respiratory sensors, and implantable loop recorders, often integrated with cloud-based platforms for remote patient monitoring. Their role has expanded beyond chronic disease management to pre-symptomatic detection and post-operative care coordination. According to the World Health Organization, over 460 million people globally live with diabetes, a condition increasingly managed through real-time glucose tracking via devices like Dexcom G7 and Abbott’s FreeStyle Libre.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases Requiring Continuous Physiological Monitoring

The global surge in chronic conditions such as diabetes, cardiovascular diseases, and respiratory disorders is a primary catalyst for the adoption of wearable medical devices, as these ailments necessitate real-time, long-term physiological tracking to prevent complications. According to the World Health Organization, non-communicable diseases account for 74% of all global deaths, with cardiovascular diseases alone causing 17.9 million fatalities annually. The U.S. Centers for Disease Control and Prevention reports that 37 million Americans have diabetes, with another 96 million classified as prediabetic, creating a vast pool of potential users for preventive wearables.

Integration of Wearables into Remote Patient Monitoring and Telehealth Platforms

The institutionalization of telehealth and remote patient monitoring (RPM) has fundamentally elevated the clinical utility of wearable medical devices, which is majorly driving the growth of the wearable medical devices market. Chronic care management programs now routinely deploy wearable ECG patches, blood pressure cuffs, and weight scales to monitor heart failure patients at home. Similarly, India’s National Digital Health Mission has partnered with startups like HealthCube to distribute wearable ECG and SpO2 devices in rural clinics by enabling remote diagnostics for 5 million patients.

MARKET RESTRAINTS

Regulatory Hurdles and Lengthy Approval Processes for Medical-Grade Devices

The path to commercialization for wearable medical devices is restraining the growth of the wearable medical devices market. As per the U.S. Food and Drug Administration, Class II medical devices such as wearable ECG monitors and continuous glucose sensors require an average of 178 days for 510(k) clearance, with some submissions undergoing multiple review cycles. These delays hinder innovation, particularly for startups lacking the resources to navigate compliance frameworks. Additionally, the classification of borderline devices such as smartwatches with ECG functionality remains ambiguous. These regulatory inefficiencies not only slow patient access but also discourage investment in next-generation technologies in regions where reimbursement lags behind approval.

Data Privacy and Security Vulnerabilities in Connected Wearables

The transmission of sensitive biometric data through wearable medical devices exposes users to significant cybersecurity risks with trust and adoption, despite clinical benefits. As per the U.S. Department of Health and Human Services, over 560 healthcare data breaches were reported in 2023, many involving unsecured transmission from wearable devices to cloud platforms. The European Data Protection Board has issued warnings about the risks of re-identification from anonymized physiological datasets, when combined with other digital footprints. Additionally, third-party app integrations often bypass medical device safeguards Apple’s App Store hosts over 1,200 health apps that access wearable data without HIPAA compliance.

MARKET OPPORTUNITIES

Expansion of Preventive Healthcare and Wellness Programs in Corporate and Public Sectors

The growing emphasis on preventive medicine is creating a fertile environment for wearable medical devices to transition from reactive monitoring to proactive health optimization within employer-sponsored wellness initiatives and national public health strategies. According to the World Economic Forum, 68% of Fortune 500 companies now offer wearable-based wellness programs to reduce employee healthcare costs and improve productivity. In the UAE, the Dubai Health Authority mandates wearable integration in corporate wellness plans for firms with over 500 employees. The OECD confirms that every $1 invested in preventive health yields $6 in long-term savings, driving institutional adoption.

Advancements in Sensor Technology and Miniaturization Enabling Medical-Grade Accuracy in Consumer Form Factors

The breakthroughs in micro-sensing, flexible electronics, and low-power biocompatible materials are creating new opportunities for the growth of the wearable medical devices. As per the Massachusetts Institute of Technology’s Microsystems Technology Laboratories, new photoplethysmography (PPG) sensors can now detect blood glucose levels non-invasively with 92% accuracy compared to traditional finger-prick tests, a development poised to revolutionize diabetes management. Similarly, imec, a Belgian nanotechnology research hub, has developed ultra-thin epidermal patches that monitor EEG, ECG, and EMG signals simultaneously, suitable for long-term neurological monitoring. These innovations are supported by advancements in energy efficiency that created biofuel cells to generate power from sweat by eliminating the need for frequent charging

MARKET CHALLENGES

Limited Reimbursement Policies for Wearable Medical Devices in Public and Private Insurance Schemes

The widespread adoption of wearable medical devices is hindered by inconsistent and restrictive reimbursement frameworks in public healthcare systems and emerging markets are impeding the growth of wearable medical devices. As per the World Health Organization, only 18 out of 194 member states have established national reimbursement policies for continuous glucose monitors, leaving millions of diabetic patients to bear out-of-pocket costs. The Centers for Medicare & Medicaid Services, 30% of approved wearable ECG patches are reimbursed under standard RPM codes, creating financial disincentives for providers. The lack of standardized health economic data further complicates decision-making. The Institute for Clinical and Economic Review states that fewer than 20% of wearable device manufacturers submit cost-effectiveness studies to payers.

Variability in Clinical Validation and Accuracy Across Device Categories

The credibility of wearable medical devices is undermined by inconsistent performance across different models and use cases, raising concerns among clinicians and regulators about diagnostic reliability. Similarly, the U.S. Food and Drug Administration issued a safety communication in 2022 warning that certain smartwatch ECG apps may miss atrial fibrillation in patients with low heart rate variability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 20.40% |

| Segments Covered | By Diagnostic Wearable Devices, Therapeutic Wearable Devices, Applications, Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Key Market Players | Fitbit (United States), Philips (Netherlands), LifeWatch (Switzerland), Garmin (Switzerland), Omron (Japan), Drägerwerk (Germany), Nokia Technologies (United States), Jawbone (United States), Polar (Finland), Wor(l)d Global Network (United States), Active insights (United Kingdom), VitalConnect (United States), Xiaomi (China), Misfit (United States) and Monica Healthcare (United Kingdom) |

SEGMENTAL ANALYSIS

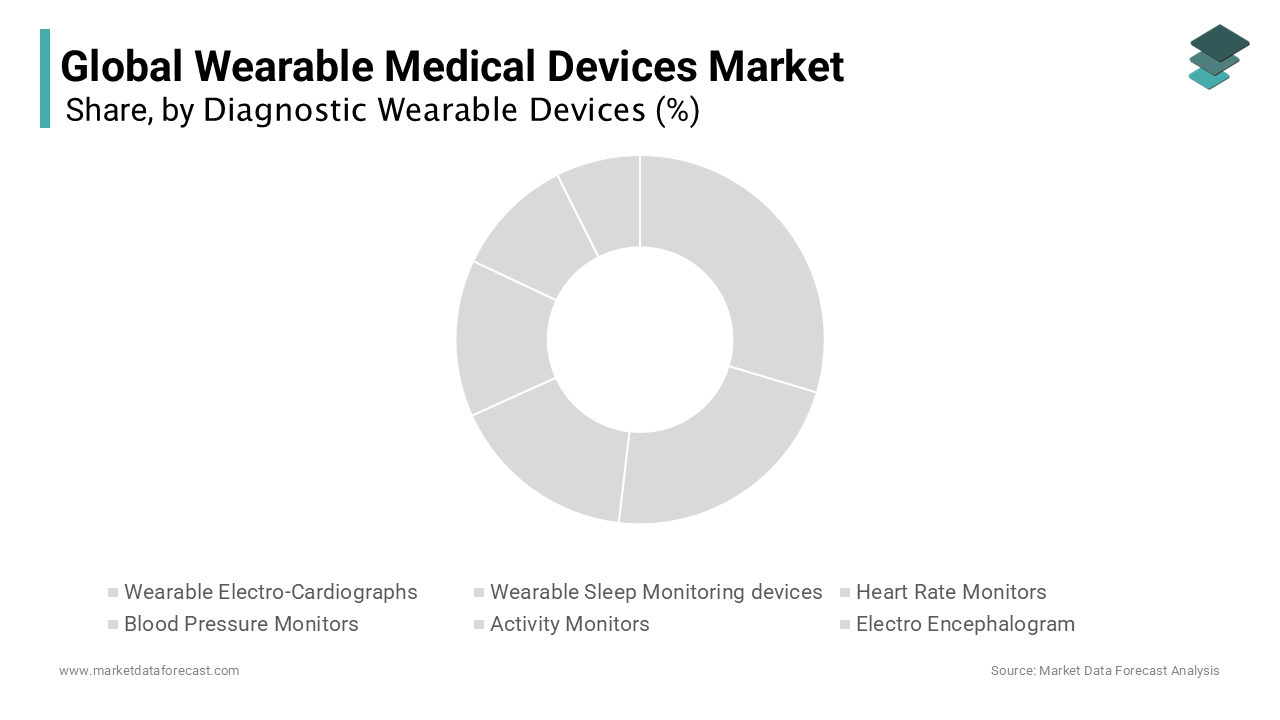

By Diagnostic Wearable Devices Insights

The wearable electrocardiographs (ECG) segment was accounted in holding 31.2% of the wearable devices market share in 2025 with the escalating global burden of cardiovascular diseases and the clinical necessity for prolonged cardiac monitoring to detect arrhythmias, particularly atrial fibrillation. According to the World Health Organization, cardiovascular diseases remain the leading cause of death worldwide, responsible for 17.9 million fatalities annually, with a significant proportion stemming from undiagnosed rhythm disorders. Devices such as the Apple Watch Series 8, Withings ScanWatch, and BioTelemetry’s Zio Patch have demonstrated clinical efficacy; a 2023 study by the Mayo Clinic found that single-lead ECG wearables detected previously unknown AFib in 0.8% of users over 65, prompting timely anticoagulant therapy.

The wearable sleep monitoring devices segment is projected to grow at a CAGR of 18.6% from 2026 to 2034 with the increasing recognition of sleep disorders as contributors to chronic disease and reduced quality of life. The American Academy of Sleep Medicine states that untreated OSA increases the risk of stroke by 3–4 times and heart failure by 140%, prompting healthcare providers to adopt home-based screening tools. Wearable sleep trackers such as the Oura Ring, Dreem headband, and Philips NightBalance offer clinical-grade metrics including oxygen saturation, respiratory rate, and sleep staging, validated against polysomnography. A 2023 trial at Stanford Sleep Medicine Center demonstrated that wrist-based actigraphy wearables achieved 89% accuracy in identifying sleep apnea events when combined with AI algorithms. The U.S. Food and Drug Administration has cleared over 15 wearable sleep devices for diagnostic use since 2020, facilitating insurance reimbursement and clinical integration.

By Therapeutic Wearable Devices Insights

The glucose/insulin monitoring devices segment was the largest by occupying 44.3% of the wearable devices market share in 2025 owing to the global diabetes epidemic and the need for real-time glycemic control to prevent complications such as neuropathy, retinopathy, and cardiovascular disease. In pediatric populations, the Juvenile Diabetes Research Foundation reports that CGM use reduces hypoglycemic events by 40%, which improves safety and quality of life.

The pain management devices segment is swiftly emerging at a CAGR of 19.3% in the coming years with the global opioid crisis and the urgent need for non-pharmacological alternatives to chronic pain treatment. As per the U.S. Department of Health and Human Services, over 10 million Americans misused prescription opioids in 2022, prompting regulatory and clinical shifts toward drug-free interventions. Wearable neuromodulation devices, such as Quell, Nevro’s Senza, and Bioness’s L300 Go, use transcutaneous electrical nerve stimulation (TENS) and targeted nerve modulation to disrupt pain signals.

By Application Insights

The home healthcare segment for wearable medical devices is believed to have the highest share. It is expected to grow to produce profits during the analysis period. The increasing significance of home healthcare services is propelling the market growth.

The fitness and sports segment is anticipated to thrive in the upcoming years. Sports-related wearable devices like waistbands or skin patches use Bluetooth and GPS technology and provide real-time data. The growing tendency for sports and exercise activities also propels the market's growth rate. In addition, increasing awareness of maintaining a healthy lifestyle is likely to fuel the market's demand.

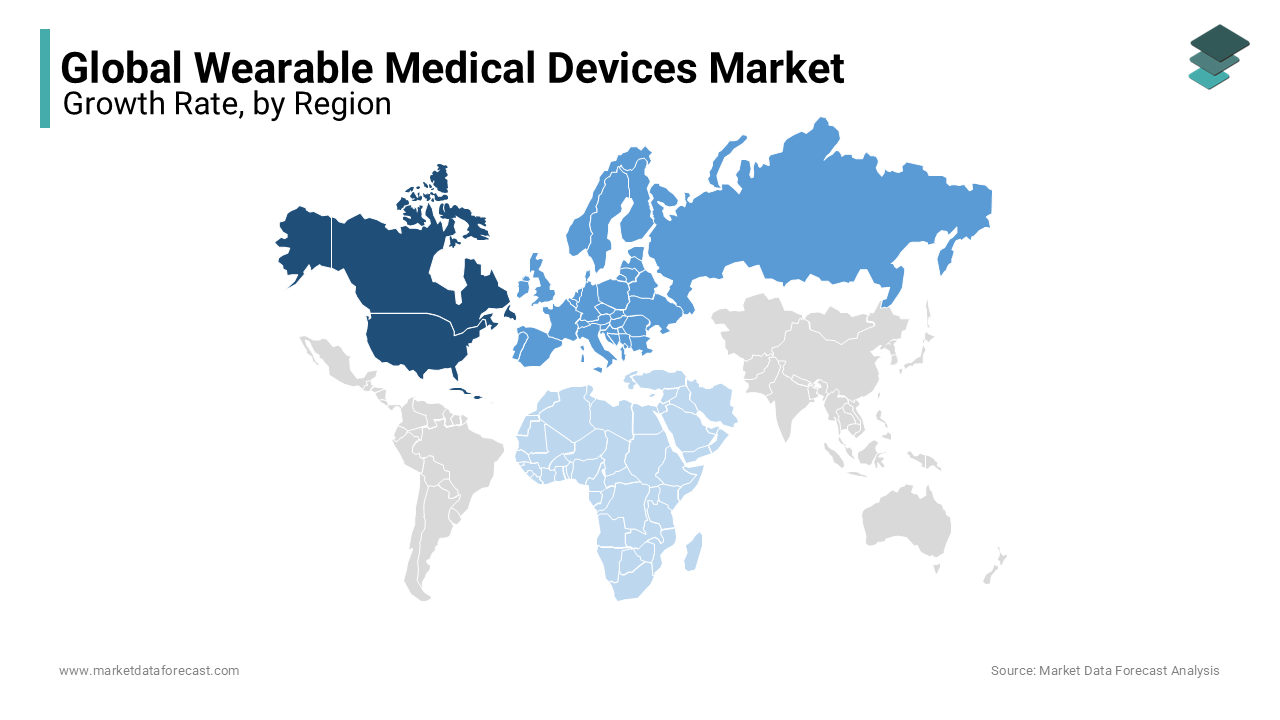

REGIONAL ANALYSIS

North America was the top performer of the global wearable medical devices market with 42.8% in 2025 with the advanced healthcare infrastructure, strong reimbursement frameworks, and high consumer adoption of digital health technologies. Chronic disease prevalence is a key driver 37 million Americans have diabetes, and 122 million suffer from cardiovascular conditions, which is creating sustained demand for continuous monitoring solutions.

Europe was the largest and held 27.5% of the wearable medical devices market share in 2025. The European Union’s Medical Device Regulation (MDR), implemented in 2021, has elevated clinical validation requirements, ensuring that only high-performing wearables gain market access. Germany, France, and the UK are leading adopters, with national health systems increasingly incorporating wearables into chronic disease management.

The Asia-Pacific wearable medical devices market growth is fueled by rapid growth fueled by rising healthcare privatization, digital penetration, and government-led health modernization. China, India, and Japan are key markets, each adopting distinct models of integration. India’s National Digital Health Mission has partnered with startups to distribute wearable ECG and SpO2 devices in rural clinics, reaching 4 million patients.

Latin America wearable medical devices market growth is lucratively growing in the next coming years. Mexico’s proximity to the U.S. drives demand for advanced devices in border cities like Monterrey, where medical tourists access wearable-based diabetes and cardiac programs. However, regulatory fragmentation hinders scalability. Argentina bans direct-to-consumer medical device advertising, while Colombia lacks a unified reimbursement framework.

The Middle East and Africa wearable medical devices market is likely to grow in the coming years. According to the Dubai Health Authority, private hospitals increased wearable procurement by 30% in 2023 to support remote monitoring for cardiac and diabetic patients. In the UAE, over 60% of corporate wellness programs now include wearable fitness trackers, as per the Ministry of Health.

KEY MARKET PLAYERS

Some of the most promising companies operating in the global wearable medical devices market include

- Fitbit (United States)

- Philips (Netherlands)

- LifeWatch (Switzerland)

- Garmin (Switzerland)

- Omron (Japan)

- Drägerwerk (Germany)

- Nokia Technologies (United States)

- Jawbone (United States)

- Polar (Finland)

- Wor(l)d Global Network (United States)

- Active Insights (United Kingdom)

- VitalConnect (United States)

- Xiaomi (China)

- Misfit (United States)

- Monica Healthcare (United Kingdom)

Top Players in the Wearable Medical Devices Market

Abbott Laboratories

Abbott Laboratories has established a formidable presence in the Asia Pacific wearable medical devices market through its pioneering continuous glucose monitoring (CGM) systems, particularly the FreeStyle Libre platform. It launched the FreeStyle Libre 3 in Japan with regulatory approval from the Pharmaceuticals and Medical Devices Agency, achieving full reimbursement under national health insurance. Abbott also initiated clinical collaborations with hospitals in South Korea and Australia to validate the device’s efficacy in pediatric and geriatric populations. The company has invested in localized digital platforms, offering multilingual mobile apps that integrate with regional electronic health records.

Medtronic

Medtronic plays a pivotal role in advancing therapeutic wearable technologies across Asia Pacific, with a strong focus on integrated diabetes management and cardiac monitoring solutions. The company’s MiniMed 780G insulin pump, paired with its Guardian 4 sensor, represents one of the most advanced hybrid closed-loop systems available in the region. In 2023, Medtronic secured reimbursement approval for its CGM-integrated systems in Australia’s Therapeutic Goods Administration and expanded its presence in private hospitals in Thailand and Singapore. It launched a remote monitoring program in collaboration with Apollo Hospitals in India, enabling real-time data sharing between patients and endocrinologists. Medtronic also established a regional innovation hub in Singapore to accelerate the development of AI-driven algorithms for predictive glycemic control. The company has engaged with regulatory bodies in China and Malaysia to streamline approvals for next-generation wearables. Additionally, Medtronic supports physician training initiatives to promote proper device utilization and improve patient outcomes. Its emphasis on clinical integration, regulatory navigation, and long-term patient support has solidified its reputation as a trusted partner in chronic disease management.

Samsung Electronics

Samsung Electronics has emerged as a key innovator in the Asia Pacific wearable medical devices market by bridging consumer technology with clinical-grade health monitoring. While initially positioned as a fitness brand, Samsung’s Galaxy Watch series has evolved into a medically validated platform, with ECG and blood pressure monitoring features approved by South Korea’s Ministry of Food and Drug Safety and India’s CDSCO. In 2023, Samsung partnered with Seoul National University Hospital to conduct large-scale trials on atrial fibrillation detection using its wearable PPG sensors, achieving 91% sensitivity in preliminary results. The company also collaborated with Singapore’s Health Promotion Board to integrate its wearables into national wellness programs, which promote preventive health tracking. Samsung’s Bio-Processor technology, designed for multi-parameter sensing, is being adapted for use in remote patient monitoring pilots in Japan and Malaysia.

Top Strategies Used by the Key Market Participants

Key players in the wearable medical devices market are deploying a range of strategic initiatives to strengthen their competitive positioning and accelerate clinical adoption. Regulatory alignment is a primary focus, with companies investing in local clinical trials and engaging with national health authorities to secure approvals and reimbursement. Strategic partnerships with hospitals, telehealth platforms, and insurance providers are being leveraged to integrate devices into care pathways and improve patient access. Product differentiation is achieved through technological innovation, including AI-driven analytics, sensor miniaturization, and multi-parameter monitoring capabilities. Localization of software interfaces, language support, and data storage infrastructure ensures compliance with regional privacy laws and enhances user engagement. Companies are also expanding direct-to-consumer and B2B sales channels, particularly through e-pharmacies and corporate wellness programs. Investment in post-market surveillance and real-world evidence generation is increasing to demonstrate clinical and economic value to payers. Additionally, firms are enhancing patient support ecosystems with mobile apps, cloud dashboards, and remote care coordination tools. These strategies reflect a shift from standalone devices to integrated, outcome-driven health solutions.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Abbott launched the FreeStyle Libre 3 in Japan with full reimbursement under national health insurance, enabling widespread access to continuous glucose monitoring for diabetic patients and strengthening its presence in the Asia Pacific therapeutic wearables market.

- In May 2023, Medtronic partnered with Apollo Hospitals in India to deploy its MiniMed 780G hybrid closed-loop system in a remote monitoring program, which integrates real-time glucose data into clinical decision-making for diabetes management.

- In August 2023, Samsung collaborated with Seoul National University Hospital to conduct a large-scale clinical trial validating the atrial fibrillation detection accuracy of its Galaxy Watch ECG feature by enhancing its credibility as a medical device in South Korea.

- In February 2024, Dexcom expanded its distribution network in Southeast Asia by partnering with Halodoc and Doctor Anywhere to integrate CGM data into telehealth consultations by improving patient engagement in Indonesia and Malaysia.

- In April 2024, Philips introduced its wearable biosensor patch in Australia for remote monitoring of post-surgical patients, which was supported by a collaboration with private hospital chains to reduce readmission rates and enhance care continuity.

MARKET SEGMENTATION

This research report on the global wearable medical devices market has been segmented and sub-segmented based on diagnostic wearable devices, therapeutic wearable devices, applications, and regions.

By Diagnostic Wearable Devices

- Wearable Electro-Cardiographs

- Wearable Sleep Monitoring Devices

- Heart Rate Monitors

- Blood Pressure Monitors

- Activity Monitors

- Electro Encephalogram

By Therapeutic Wearable Devices

- Pain Management Devices

- Glucose/Insulin Monitoring Devices

- Respiratory Therapy Devices

By Application

- Sports and Fitness

- Home Healthcare

- Patient Monitoring

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

How much is the global wearable medical devices market going to be worth by 2033?

As per our research report, the global market size for wearable medical devices is estimated to be worth USD 59.22 Billion by 2033.

Does this report include the impact of COVID-19 on the wearable medical devices market?

Yes, in this report, the COVID-19 impact on the global wearable medical devices market is included.

Which region had the highest share of the wearable medical devices market in 2024?

Based on the region, the North American regional market led the wearable medical devices market in 2024.

Which are the significant players operating in the wearable medical devices market?

Fitbit (United States), Philips (Netherlands), LifeWatch (Switzerland), Garmin (Switzerland), Omron (Japan), Drägerwerk (Germany), Nokia Technologies (United States), Jawbone (United States), Polar (Finland), Wor(l)d Global Network (United States), Activeinsights (United Kingdom), VitalConnect (United States), Xiaomi (China), Misfit (United States) and Monica Healthcare (United Kingdom) are some of the notable companies operating in the wearable medical devices market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com