Global Smartwatch Market Size, Share, Trends & Growth Forecast Report By Product Type (Extension, Standalone, Classic), Therapeutic Application (Sports and Fitness, Personal Assistance, Sports, Medical, Others), and Region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa) – Industry Analysis, 2025 to 2033

Global Smartwatch Market Summary

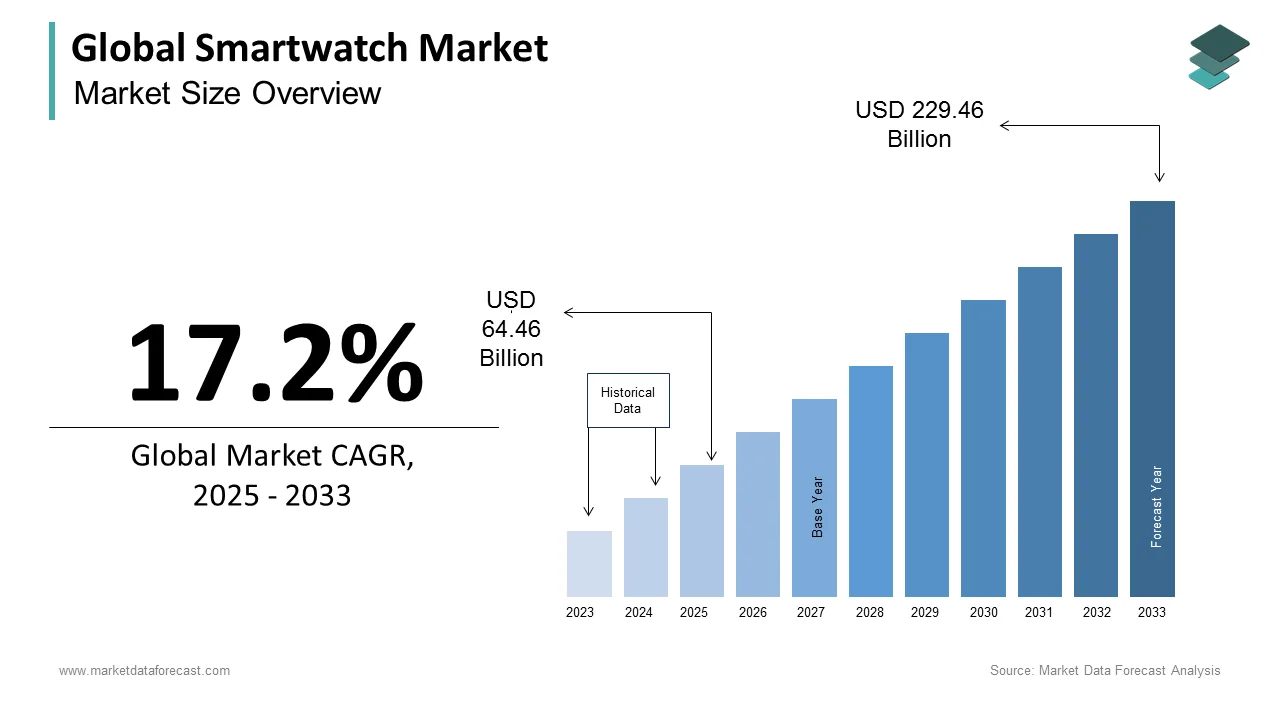

The global smartwatch market was valued at USD 55 billion in 2024 and is projected to reach USD 64.46 billion in 2025 and USD 229.46 billion by 2033, growing at a strong CAGR of 17.2% from 2025 to 2033. The growth of the global smartwatch market is driven by rising adoption of wearable technology, increasing health and fitness awareness, integration of AI and IoT in smart devices, and consumer demand for multifunctional gadgets. In addition, advancements in wireless connectivity, expanding e-commerce penetration, and the premiumization of smart devices are further propelling market expansion.

Key Market Trends

- Growing use of smartwatches for health tracking (heart rate, blood pressure, sleep, and ECG monitoring).

- Strong demand for sports and fitness applications among millennials and Gen Z.

- Standalone smartwatches with LTE/5G connectivity becoming increasingly popular.

- Expanding integration with AI, voice assistants, and smart home ecosystems.

- Rapid growth of e-commerce and online retail channels fueling global accessibility.

Segmental Insights

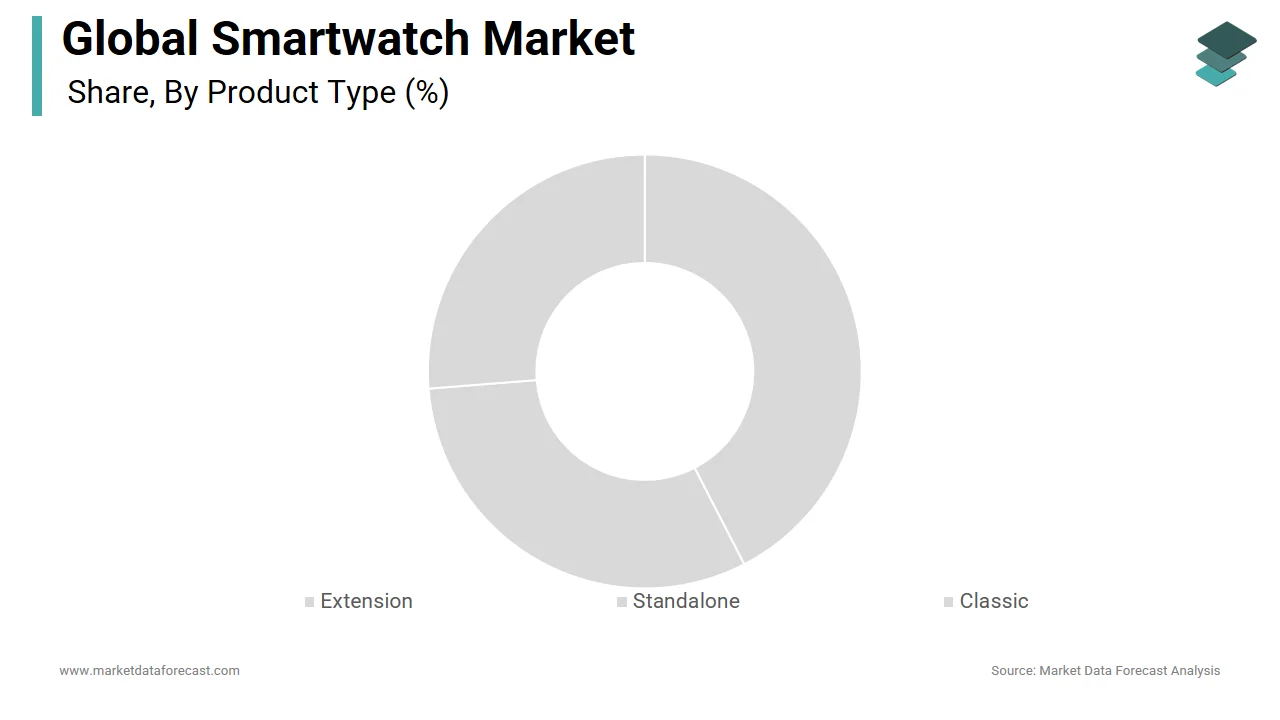

- Based on product type, the standalone segment dominated the global smartwatch market in 2024, supported by consumer preference for independent connectivity features without smartphone dependency.

- Based on application, the sports and fitness segment held the largest share with 42.3% of global smartwatch market revenue in 2024, owing to increased adoption of fitness tracking, performance analytics, and health monitoring tools.

Regional Insights

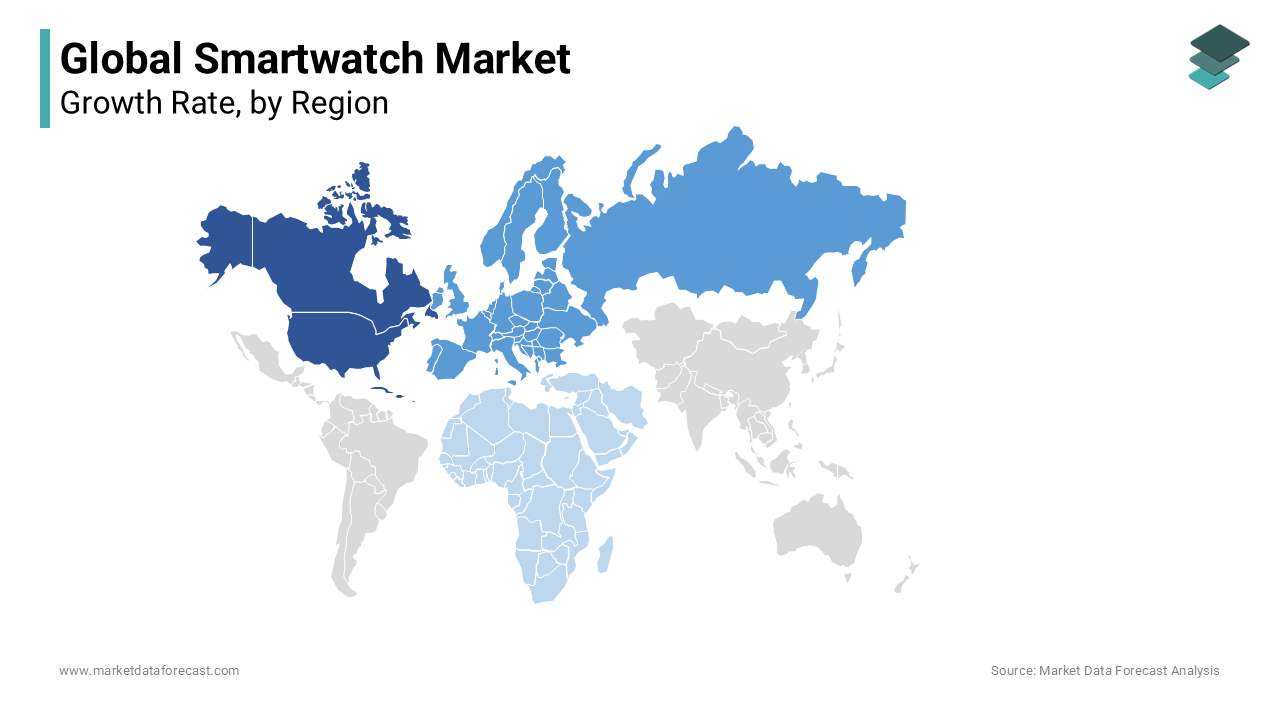

- North America was the leading region in the global smartwatch market in 2024 with a 34.3% share, driven by high consumer purchasing power, technological adoption, and strong presence of leading smartwatch manufacturers.

- Asia-Pacific is anticipated to record the fastest growth during the forecast period, led by rising middle-class consumers, fitness trends, and expanding smartphone ecosystems in countries like China and India.

- Europe maintains steady growth, supported by widespread health-tech adoption and strong brand presence.

Competitive Landscape

The global smartwatch market is competitive and driven by constant innovation, health-tech integration, and brand dominance. Leading companies include Apple Inc., Google Inc., Garmin, Fitbit, Motorola, Sony Corporation, Samsung Electronics, LG Electronics, and Huawei Technologies Co., Ltd.

Global Smartwatch Market Size

The size of the global smartwatch market was worth USD 55 billion in 2024. The global market is anticipated to grow at a CAGR of 17.2% from 2025 to 2033 and be worth USD 229.46 billion by 2033 from USD 64.46 billion in 2025.

The smartwatch is a wearable computing devices that integrate timekeeping with advanced digital functionalities such as health monitoring, connectivity, notifications, and application support. These devices have evolved from simple notification hubs into sophisticated health and fitness companions, incorporating sensors for electrocardiograms (ECG), blood oxygen saturation (SpO2), heart rate variability, and sleep tracking. The integration of artificial intelligence for predictive health analytics and voice-assisted interfaces has further promoted their role in personal digital ecosystems. Regulatory bodies such as the U.S. Food and Drug Administration have cleared certain smartwatch features for medical-grade monitoring with their transition from lifestyle accessories to validated health tools.

MARKET DRIVERS

Rising Global Prevalence of Chronic Diseases and Preventive Healthcare Adoption

The escalating burden of chronic diseases is a pivotal force accelerating smartwatch adoption across both developed and emerging economies. Cardiovascular diseases, diabetes, and respiratory conditions are leading causes of mortality worldwide, which are increasingly being managed through early detection and continuous monitoring, a niche that smartwatches are uniquely positioned to address. According to the World Health Organization, an estimated 17.9 million people die annually from cardiovascular diseases, representing 32% of all global deaths. Devices such as the Apple Watch and Fitbit Sense offer FDA-cleared electrocardiogram (ECG) functionality by enabling users to detect atrial fibrillation, a condition affecting approximately 33.5 million individuals globally, as per a study published in The Lancet. In 2023, over 60 million smartwatches shipped with medical-grade health sensors, as reported by IDC. The American Heart Association emphasizes that early detection of irregular heart rhythms can reduce stroke risk by up to 60%, reinforcing the clinical value of wearable monitoring. Furthermore, insurance providers in markets like the U.S. and Germany are incentivizing wearable use to promote preventive care, thereby reducing long-term healthcare costs.

Advancements in Sensor Technology and Energy Efficiency

The rapid innovation in micro-sensing and power management systems has significantly enhanced the functionality and usability of smartwatches is enhancing the growth of the smartwatch market. Modern smartwatches now incorporate photoplethysmography (PPG) sensors, accelerometers, gyroscopes, and temperature monitors, enabling precise measurement of physiological parameters. For instance, the latest generation of PPG sensors can detect blood pressure trends with 90% correlation to clinical sphygmomanometers, as validated by research from the University of California, San Francisco. Concurrently, advancements in low-power Bluetooth protocols and system-on-chip (SoC) designs, such as the Apple S9 and Qualcomm W5+, have extended battery life to over 36 hours under continuous use, addressing a longstanding consumer concern. Samsung’s Galaxy Watch6, for example, features a 4-in-1 bioelectrical impedance sensor that measures body composition, a capability previously limited to clinical devices. Moreover, the integration of ambient light sensors and adaptive refresh rates such as the 1–48Hz dynamic display in the Apple Watch Ultra reduces energy consumption without compromising user experience.

MARKET RESTRAINTS

High Device Costs and Limited Affordability in Emerging Economies

The premium pricing of advanced smartwatches is limiting the growth of the Smartwatch Market. High-end models from Apple, Samsung, and Garmin often retail between $300 and $800, placing them beyond the discretionary spending capacity of a large portion of the global population. As per the World Bank, over 70% of the world’s population lives in countries where the average annual income is below $10,000, rendering such devices financially inaccessible. Even mid-tier models with essential health features start at $150, a substantial expense in economies where monthly smartphone expenditures average $100 or less. Additionally, recurring costs such as subscription-based health services like Apple’s Advanced Sleep Tracking or ECG history sync further deter long-term ownership. The United Nations Conference on Trade and Development reported in 2023 that digital inequality persists, with only 47% of households in developing nations owning a single computing device. This economic disparity limits the scalability of smartwatch ecosystems, particularly in regions where basic healthcare infrastructure remains underdeveloped. While manufacturers have introduced budget models, these often lack medical-grade sensors or software updates, undermining their utility.

Data Privacy Concerns and Regulatory Fragmentation

The proliferation of health-sensitive data collected by smartwatches has intensified scrutiny over data security and regulatory compliance, which is creating an impediment to consumer trust and market growth. The European Union’s General Data Protection Regulation (GDPR) imposes strict requirements on biometric data processing, yet enforcement varies across member states, complicating global deployment strategies for manufacturers. Furthermore, the absence of a unified global framework for health data interoperability, such as between the U.S. HIPAA and EU GDPR, creates compliance burdens for cross-border health platforms. A report by the Brookings Institution emphasized that inconsistent data governance reduces consumer confidence, with only 38% of respondents trusting tech firms to protect their health information.

MARKET OPPORTUNITIES

Integration with Telemedicine and Remote Patient Monitoring Platforms

The integration of smartwatches with telehealth ecosystems presents a transformative opportunity to revolutionize chronic disease management and post-operative care. According to the World Health Organization, over 500 million people globally suffer from diabetes, a condition requiring constant glucose and activity monitoring functions increasingly supported by next-generation smartwatches. In 2023, the U.S. Centers for Medicare & Medicaid Services expanded reimbursement for remote patient monitoring (RPM) by allowing physicians to bill for data collected via FDA-cleared wearables, thereby incentivizing adoption. Additionally, the UK’s National Health Service launched a digital-first initiative in 2022, partnering with wearable vendors to deploy smartwatches for elderly care, targeting a 25% improvement in early deterioration detection.

Expansion of AI-Powered Personalized Health Analytics

The integration of artificial intelligence into smartwatch platforms is unlocking unprecedented capabilities in predictive health modeling and behavioral intervention, which is hampering the growth of the smartwatch market. Modern AI algorithms can analyze longitudinal biometric datasets to forecast health risks such as hypertension, sleep apnea, and mental fatigue before symptoms manifest. As per a 2023 study published in Nature Medicine, AI models trained on smartwatch-derived heart rate and activity data achieved 85% accuracy in predicting the onset of type 2 diabetes up to six months in advance. Google’s acquisition of Fitbit and subsequent development of its Health Studies API has enabled large-scale research collaborations, including a cardiovascular risk prediction model involving over 10,000 participants. The Stanford University Digital Medicine Group found that AI-enhanced wearables improved medication adherence by 52% in hypertensive patients through personalized nudges and stress alerts. Furthermore, companies like Withings and Huawei are deploying machine learning to detect early signs of respiratory infections by analyzing subtle changes in resting heart rate and breathing patterns. Consumer demand for hyper-personalized insights is rising; a 2023 Deloitte survey revealed that 67% of wearable users prefer devices that offer tailored wellness recommendations.

MARKET CHALLENGES

Interoperability and Fragmentation of Health Data Ecosystems

The lack of seamless integration between wearable devices and existing healthcare IT infrastructures is escalating the growth of the smartwatch market. As per the Office of the National Coordinator for Health Information Technology (ONC), only 35% of U.S. hospitals can automatically ingest wearable-generated data into patient records, limiting its utility in decision-making. Apple’s HealthKit and Google’s Fit platform attempt to bridge this gap, yet cross-platform synchronization remains inconsistent. A 2023 study by the Mayo Clinic revealed that 60% of physicians do not routinely review patient-submitted wearable data due to concerns over data accuracy and integration complexity. The World Health Organization emphasizes that interoperability is essential for achieving universal health coverage, yet fewer than 20 countries have established national standards for wearable data exchange. Additionally, variations in data sampling rates, calibration methods, and timestamp synchronization reduce the reliability of multi-device datasets.

Limited Clinical Validation and Regulatory Hurdles for Advanced Features

The absence of rigorous clinical validation for many features undermines their credibility, and adoption in professional healthcare settings is also hindering the growth of the smartwatch market. Although devices like the Apple Watch have received FDA clearance for ECG and fall detection, most health algorithms, such as stress monitoring, hydration estimation, or blood glucose prediction, lack peer-reviewed clinical trials or regulatory approval. As per the U.S. Food and Drug Administration, only 12 wearable health algorithms had received De Novo classification as of 2023, despite hundreds of claims in the market. A 2022 investigation by JAMA Internal Medicine found that seven popular smartwatches exhibited heart rate measurement errors exceeding 20% during high-intensity exercise, raising concerns about reliability. In emerging markets, regulatory frameworks are often underdeveloped; India’s Central Drugs Standard Control Organization has yet to issue specific guidelines for wearable health claims, leading to unverified marketing.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Apple Inc., Google Inc., Garmin, Fitbit, Motorola, Sony Corporation, Samsung Electronics, LG Electronics, and Huawei Technologies Co., Ltd. |

SEGMENTAL ANALYSIS

By Product Type Insights

The standalone segment was the largest by accounting for a dominant share of the smartwatch market in 2024. As of 2023, standalone models accounted for approximately 48% of total smartwatch shipments worldwide, according to data published by IDC. This dominance stems from their enhanced utility in communication, navigation, and health monitoring without requiring a paired device. The integration of eSIM technology has been a pivotal enabler, allowing users to make calls, stream music, and access emergency services directly from the wrist. As per the GSMA Intelligence report released in 2023, over 120 mobile network operators across 60 countries now support eSIM-enabled wearables, facilitating seamless deployment. The U.S. Federal Communications Commission mandates that personal emergency response systems be accessible and reliable, a requirement increasingly met by standalone models. Moreover, urban professionals and first responders are gravitating toward these devices for hands-free operation in high-intensity environments.

The extension smartwatch segment is projected to expand at a CAGR of 14.7% from 2025 to 2033, with its affordability, broad compatibility, and alignment with the ecosystem strategies of major tech companies. According to the International Telecommunication Union, global smartphone penetration reached 68% in 2023, creating a ready-made user pool for tethered wearables. Android Wear OS devices, such as the Samsung Galaxy Watch and Fossil Gen 6, dominate this segment due to deep integration with mobile operating systems. A 2023 analysis by Counterpoint Research revealed that over 70% of extension smartwatch buyers already own flagship smartphones, which indicates a preference for seamless cross-device synchronization. Additionally, manufacturers are reducing feature gaps; for example, Google’s Wear OS 4 enables offline music playback and GPS tracking even in extension mode. The energy efficiency of non-cellular models also results in longer battery life, averaging 48 to 72 hours by enhancing user satisfaction. As per Deloitte’s Global Mobile Consumer Survey, 58% of users consider battery longevity more important than standalone connectivity, reinforcing the appeal of extension devices.

By Therapeutic Application Insights

The sports and fitness application segment was the largest by capturing 42.3% of the smartwatch market share in 2024, with the global surge in health-conscious consumer behavior and the integration of advanced biometric tracking tailored for athletic performance. Modern smartwatches now offer precise metrics such as VO2 max, training load, recovery time, and running dynamics, appealing to both amateur and professional athletes. According to the World Health Organization, only 27% of adults meet the recommended levels of physical activity, prompting public and private initiatives to promote fitness tracking as a behavioral intervention. Garmin, a leader in performance wearables, saw a 34% year-on-year increase in Forerunner series sales, attributed to triathletes and endurance trainers relying on GPS accuracy and multi-sport modes. A study conducted by the American College of Sports Medicine found that individuals using wearables for fitness tracking maintained 37% higher workout consistency over six months compared to non-users. Additionally, corporate wellness programs in countries like the U.S. and Germany are incentivizing employees to use fitness-enabled smartwatches, with over 60% of Fortune 500 companies offering wearable-based health challenges.

The medical application segment is swiftly emerging with a CAGR of 18.3% from 2025 to 2033, owing to the increasing recognition of smartwatches as tools for remote diagnostics and chronic disease management. As per the American Heart Association, 2.7 million Americans are diagnosed with atrial fibrillation annually, and early detection through wearables can reduce stroke risk by up to 60%. The Apple Heart Study, conducted in collaboration with Stanford Medicine and involving over 400,000 participants, demonstrated that smartwatch alerts led to timely medical consultations in 0.5% of users, confirming arrhythmias. In 2023, the U.S. Centers for Medicare & Medicaid Services expanded reimbursement codes for remote cardiac monitoring, enabling physicians to bill for data collected from consumer wearables. Similarly, the UK’s National Health Service piloted a program in 2022 where 5,000 patients with hypertension used smartwatches to transmit blood pressure trends, resulting in a 25% reduction in clinic visits. The European Commission’s Horizon Europe initiative has allocated €120 million to validate AI-powered wearable diagnostics for early-stage diabetes and sleep apnea.

REGIONAL ANALYSIS

North America Smartwatch Market Analysis

North America was the top performer of the global smartwatch market with 34.3% of share in 2024, with the high disposable income, advanced healthcare infrastructure, and strong digital ecosystem integration. The United States alone accounts for over 90% of regional shipments, driven by early adoption of health-focused wearables and robust partnerships between tech firms and medical institutions. Apple, headquartered in California, dominates with over 50% market share, leveraging its ecosystem synergy and FDA-cleared health features. As per the U.S. Bureau of Labor Statistics, average annual spending on wearable electronics reached $287 per household in 2023, reflecting embedded consumer acceptance. Additionally, 5G network coverage exceeding 85% across major metropolitan areas enables real-time data transmission, enhancing device utility.

Asia-Pacific Smartwatch Market Analysis

Asia-Pacific was ranked second by holding 31.2% of the smartwatch market share in 2024. China alone contributed 45% of regional shipments in 2023, with Huawei and Xiaomi capturing over 50% of the domestic market through affordable, feature-rich models. As per the China Internet Network Information Center, wearable device users surpassed 230 million in 2023, fueled by rising urbanization and digital health awareness. India’s smartwatch market grew by 55% year-on-year, driven by entry-level models priced under $50, catering to a young, tech-savvy population. The Ministry of Health and Family Welfare launched the “Digital Health ID” initiative by encouraging the integration of wearables with personal health records. South Korea, with one of the world’s highest smartphone penetration rates at 94%, as noted by the Korea Communications Commission, has seen widespread adoption of Samsung’s Galaxy Watch series.

Europe Smartwatch Market Analysis

Europe smartwatch market is likely to grow with an expected CAGR during the forecast period. Germany, the UK, and France lead regional demand, with per capita wearable ownership exceeding 35% in Nordic countries. As per the European Health Data Space regulation introduced in 2023, biometric data from wearables can now be shared with clinicians only under strict consent protocols, affecting deployment speed. However, clinical validation initiatives are gaining ground; the Netherlands’ Radboud University Medical Center conducted a trial using smartwatches to monitor Parkinson’s disease progression, achieving 88% accuracy in motor symptom tracking. According to the UK’s National Health Service Digital, 1.2 million patients used wearables for diabetes management in 2023.

Latin America Smartwatch Market Analysis

Latin America smartwatch market growth is likely to be propelled by the rising adoption amid economic volatility and infrastructure limitations. Brazil leads the region with 48% of shipments, driven by urban middle-class demand and localized financing options. As per Brazil’s IBGE, smartphone ownership reached 82% in 2023, creating a foundation for wearable expansion. However, high import tariffs up to 35% on electronic devices keep premium models out of reach for most consumers. The average selling price of smartwatches in the region remains below $120, favoring mid-tier brands like Amazfit and Motorola.

Middle East and Africa Smartwatch Market Analysis

The Middle East and Africa smartwatch market is expected to expand quietly in the coming years. The UAE and Saudi Arabia dominate regional demand, where smartwatch penetration exceeds 28% among smartphone users, as per expected to expand quietly in the coming years. Dubai’s Smart City initiative integrates wearable data into emergency response systems, including automatic crash detection and hospital alerts. In contrast, sub-Saharan Africa faces challenges due to low disposable income and limited digital infrastructure; only 22% of households own a smartphone, as reported by the Alliance for Affordable Internet. However, pilot programs are emerging: Kenya’s Ministry of Health collaborated with a wearable startup in 2023 to monitor maternal health in rural areas using low-cost smartbands. The African Union’s Digital Transformation Strategy aims to increase wearable adoption for disease surveillance by 2030.

COMPETITIVE LANDSCAPE

The competitive landscape of the smartwatch market is marked by a dynamic interplay between technological innovation, brand positioning, and ecosystem strength. Established consumer electronics giants leverage their global reach and R&D capabilities to maintain dominance, while niche players differentiate through specialized functionalities and vertical expertise. The market is characterized by rapid product cycles, with companies striving to outpace rivals through advancements in health monitoring, battery efficiency, and user interface design. Strategic alliances with healthcare providers and software developers are increasingly shaping competitive advantage, as wearables transition from lifestyle accessories to health devices. Brand loyalty plays a significant role, with ecosystem lock-in influencing consumer choice more than standalone features. At the same time, emerging manufacturers from Asia are challenging incumbents with cost-effective models, intensifying competition in mid-tier segments. The convergence of fashion, fitness, and medicine has created a multidimensional battleground where differentiation hinges not only on hardware but also on data intelligence, privacy assurance, and clinical validation.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global smartwatch market include

- Apple Inc.

- Google Inc.

- Garmin

- Fitbit

- Motorola

- Sony Corporation

- Samsung Electronics

- LG Electronics

- Huawei Technologies Co., Ltd.

TOP LEADING PLAYERS IN THE MARKET

- Apple stands as a dominant player in the smartwatch market by having redefined the category with the introduction of the Apple Watch. The company’s success stems from its seamless integration of hardware, software, and ecosystem services, offering users a cohesive experience across devices. Apple emphasizes health innovation, incorporating advanced sensors and FDA-cleared features that position the watch as both a lifestyle accessory and a wellness tool.

- Samsung has established itself as a key innovator in the smartwatch space through its Galaxy Watch series, which combines sleek design with robust performance and cross-platform compatibility. The company leverages its expertise in semiconductors, displays, and mobile technology to deliver feature-rich wearables that appeal to a broad consumer base.

- Garmin has carved a niche as a specialist in performance-oriented smartwatches, particularly in fitness, outdoor adventure, and aviation-grade precision. Unlike generalist competitors, Garmin focuses on delivering highly accurate biometric tracking, extended battery life, and rugged durability for athletes and professionals. The company’s deep expertise in GPS technology and data analytics allows it to serve dedicated user segments, including runners, pilots, and military personnel. Garmin’s commitment to purpose-built devices, minimal reliance on smartphone dependency, and emphasis on long-term software support have earned it a loyal customer base and a respected reputation in the premium wearable segment.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by leading players is deep ecosystem integration, where smartwatches are designed to function as seamless extensions of a broader digital environment. Companies align their wearable devices with smartphones, cloud services, health platforms, and proprietary applications to enhance user retention and encourage brand loyalty. This interconnected experience discourages switching and increases customer lifetime value.

Another prevalent approach is strategic partnerships with healthcare institutions, insurers, and regulatory bodies to validate the medical utility of smartwatches. By collaborating with hospitals, research centers, and government health programs, manufacturers enhance credibility, facilitate clinical adoption, and position their devices as tools for preventive care rather than mere consumer gadgets.

Another key strategy involves continuous innovation in sensor technology and software intelligence. Firms invest heavily in R&D to introduce advanced biometric monitoring, AI-driven insights, and energy-efficient architectures. This focus on technological differentiation allows companies to maintain a competitive edge, justify premium pricing, and respond to evolving consumer expectations for accuracy, reliability, and proactive health management.

GLOBAL SMARTWATCH MARKET NEWS

- In March 2023, Apple launched a new health initiative integrating its smartwatch with major U.S. hospital systems that enable users to share ECG and heart rate data directly with cardiologists. This move is expected to deepen clinical adoption and reinforce the device’s role in preventive healthcare.

- In August 2023, Samsung partnered with Google to accelerate the development of Wear OS, which is enhancing app performance and health tracking capabilities on its Galaxy Watch series. This collaboration aims to strengthen software reliability and user engagement across Android wearables.

- In January 2024, Garmin introduced a new line of rugged smartwatches with multi-band GPS and advanced training metrics by targeting professional athletes and outdoor enthusiasts.

- In June 2023, Fitbit, under Google’s ownership, rolled out an AI-powered sleep coaching program accessible through its premium smartwatches. This enhancement is designed to improve user wellness outcomes and increase subscription-based service engagement.

- In November 2023, Huawei expanded its wearable health research initiative by collaborating with European medical universities to validate blood oxygen and stress monitoring algorithms. This effort is intended to boost regulatory acceptance and international credibility for its smartwatch health features.

MARKET SEGMENTATION

This research report on the global smartwatch market has been segmented based on product type, application, and region.

By Product Type

- Extension

- Standalone

- Classic

By Therapeutic Application

- Sports and Fitness

- Personal Assistance

- Sports

- Medical

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the Smartwatch Market?

The Smartwatch Market encompasses wearable computing devices worn on the wrist, capable of multiple functions such as health monitoring, fitness tracking, smartphone integration, communication, and augmented reality applications

2. Which regions dominate the Smartwatch Market?

North America leads with a market share of over 38% in 2024, followed closely by Europe and a rapidly expanding Asia-Pacific region fueled by rising disposable incomes and mobile technology use

3. What are the main product types in the Smartwatch Market?

Product types include standalone smartwatches, extension smartwatches (paired with smartphones), and classic hybrid smartwatches combining analog and digital features

4. How do health and fitness applications drive the Smartwatch Market?

Increasing health awareness, obesity prevalence, and chronic disease management encourage adoption of smartwatches specialized in heart rate monitoring, sleep tracking, ECG, SpO2 measurement, and exercise assistance

5. Who are the key players in the global Smartwatch Market?

Major players include Apple, Samsung, Garmin, Fitbit (Google), Huawei, Fossil Group, Amazfit, Xiaomi, and Polar Electro

6. What role does IoT play in the Smartwatch Market?

IoT integration allows smartwatches to connect seamlessly to other smart devices for home automation, health data exchange, communication, and entertainment

7. How is AI enhancing the Smartwatch Market?

AI enables predictive health analytics, personalized fitness coaching, voice commands, enhanced sleep data interpretation, and smart notifications, driving user engagement

8. What challenges exist in the Smartwatch Market?

Battery life limitations, privacy concerns, high product costs, design for diverse demographics, and competition from non-display fitness bands constrain market penetration

9. How important is smartwatch app development for market growth?

The availability and innovation in smartwatch apps increase device utility, encourage user retention, and expand functionality from fitness to productivity to telehealth

10. What are the trends in smartwatch displays and hardware?

Trends include AMOLED and OLED screens, extended battery life, improved waterproofing, lightweight design, and integration of sensors such as accelerometers and gyroscopes

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com