Global Smart Contact Lenses Market Size, Share, Trends, & Growth Analysis Report By Type, Application, End-User & Region (North America, Europe, APAC, Latin America, Middle East and Africa), Industry Analysis from 2026 to 2034

Market Size, 2025

$13.45 BnMarket Estimate, 2026

$16.44 BnMarket Forecast, 2034

$81.91 BnCAGR, 2026–2034

22.23%Global Smart Contact Lenses Market Size

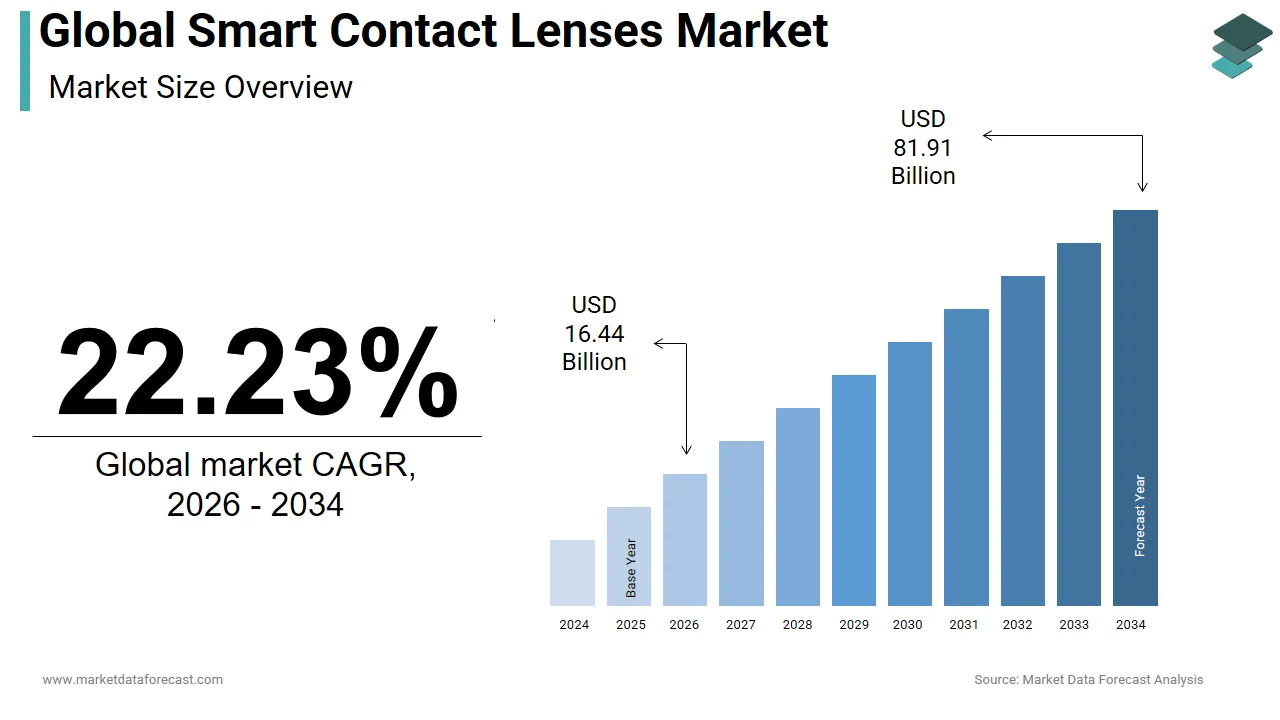

The global smart contact lenses market was valued at USD 13.45 billion in 2025. The global market is anticipated to grow at a CAGR of 22.23% from 2026 to 2034, reaching USD 81.91 billion by 2034, up from USD 16.44 billion in 2026.

The smart contact lenses are a cutting-edge segment of wearable technology that integrates microelectronics, sensors, and wireless communication systems into contact lenses for health monitoring, augmented vision, and other advanced applications. These lenses are designed to function beyond traditional vision correction, offering capabilities such as real-time glucose monitoring through tear analysis, intraocular pressure tracking for glaucoma patients, and heads-up display features for augmented reality experiences. As per the International Diabetes Federation (IDF), approximately 537 million adults were living with diabetes in 2021, a number expected to rise significantly by 2030. This growing patient base has prompted extensive research into biosensing contact lenses that can continuously monitor biomarkers in tears, potentially transforming chronic disease management.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases Requiring Continuous Monitoring

The increasing prevalence of chronic diseases such as diabetes and glaucoma, which require continuous physiological monitoring, is promoting the growth of the Smart Contact Lenses Market. These conditions necessitate frequent data collection to manage symptoms effectively and prevent complications by making wearable biosensors like smart contact lenses an attractive solution.

According to the Centers for Disease Control and Prevention (CDC), more than 10% of the U.S. population suffers from diabetes, with similar or higher rates emerging in developed regions across Europe and Asia. Smart contact lenses equipped with embedded biosensors can measure glucose levels from tear fluid, eliminating the need for painful blood tests. These medical applications have attracted significant investment from both healthcare and technology sectors.

Advancements in Wearable Technology and Augmented Reality Integration

The rapid evolution of wearable technology and the integration of augmented reality (AR) into everyday life is fuelling the growth of the Smart Contact Lenses Market. Smart contact lenses offer a natural extension of this trend by providing hands-free, immersive visual enhancements without the bulkiness of conventional devices. Companies like Mojo Vision and Innovega have demonstrated prototypes capable of overlaying real-time data onto a user’s field of view, including navigation prompts, translation services, and fitness metrics. These innovations align with the broader push toward ambient computing, where information is delivered intuitively within a user’s line of sight.

MARKET RESTRAINTS

High Development and Regulatory Compliance Costs

The high cost associated with product development and regulatory compliance is declining the growth of the Smart Contact Lenses Market. The integration of microelectronics, biosensors, and wireless communication systems into a thin, flexible lens requires advanced engineering, rigorous safety testing, and adherence to stringent medical device regulations. According to the U.S. Food and Drug Administration (FDA), the approval process for bioelectronic wearables involves multiple phases of clinical trials, material safety assessments, and long-term biocompatibility studies. These requirements significantly increase time-to-market and financial investment, discouraging smaller firms from entering the space. Additionally, manufacturing smart lenses at scale presents technical challenges, particularly in ensuring consistent performance, durability, and sterility across batches.

Consumer Skepticism and Privacy Concerns

The consumer skepticism and privacy concerns pose a significant barrier to the widespread adoption of smart contact lenses. Unlike traditional wearables such as smartwatches or fitness trackers, smart lenses operate directly on the eye, raising apprehensions about safety, data security, and surveillance risks. According to the Pew Research Center, nearly 60% of respondents expressed discomfort with body-integrated devices that collect personal health or behavioral data. Concerns include unauthorized access to biometric information, potential misuse of visual data captured through AR lenses, and the psychological impact of constant digital immersion. In addition, media coverage surrounding invasive technologies and data breaches has heightened public caution. For instance, Google Glass faced backlash due to fears of covert recording, and similar reservations apply to smart lenses with integrated cameras or environmental sensing capabilities. Addressing these concerns requires transparent communication, robust encryption protocols, and clear data governance policies.

MARKET OPPORTUNITIES

Integration with Telemedicine and Remote Patient Monitoring Systems

The integration of advanced technology with telemedicine and remote patient monitoring platforms is elevating the growth of the Smart Contact Lenses Market. According to the World Health Organization (WHO), telemedicine usage surged during the pandemic and continues to play a role in managing chronic diseases, especially in rural and underserved populations. Smart lenses that monitor glucose levels, intraocular pressure, or hydration status offer valuable insights that can be transmitted directly to healthcare providers via secure cloud networks. Pharmaceutical and tech firms are already exploring ways to link smart lenses with mobile apps and electronic health records, enabling continuous monitoring and timely interventions. For example, diabetic patients could receive automated alerts if abnormal glucose trends are detected by allowing them to take preventive measures before complications arise.

Expansion into Augmented Reality Applications Across Industries

Their application in augmented reality (AR) across various industries such as aviation, defense, logistics, and retail is also to showcase new opportunities for the growth of the Smart Contact Lenses Market. These lenses provide a discreet, hands-free interface for real-time data visualization, enhancing productivity and decision-making in professional environments. According to Deloitte Insights, the adoption of AR in enterprise operations is accelerating, with applications ranging from maintenance assistance and remote collaboration to training simulations and customer engagement. Smart contact lenses can serve as lightweight, wearable displays that overlay schematics, instructions, or contextual information directly into a worker’s field of view. In defense, AR-enabled lenses could provide soldiers with battlefield intelligence, target identification, and night vision capabilities without obstructing peripheral vision. Retailers are also exploring the use of AR lenses for immersive shopping experiences, allowing customers to visualize products in real time without needing external devices.

MARKET CHALLENGES

Technical Limitations in Power Management and Miniaturization

The technical complexity involved in power management and component miniaturization is ascribed to restricting the growth of the Smart Contact Lenses Market. According to IEEE Spectrum, current prototypes often rely on ultra-low-power chips and energy-harvesting techniques to extend battery life, but achieving sufficient power density for continuous operation remains elusive. Some designs explore near-field communication (NFC) or radio-frequency energy transfer, but these approaches are still in experimental stages. Furthermore, heat dissipation is a concern, as even minor temperature increases near the cornea can cause discomfort or tissue damage. Ensuring that electronic components do not interfere with oxygen permeability and tear flow is another crucial design constraint.

Ethical and Regulatory Uncertainty Surrounding Data Handling

The ethical and regulatory uncertainty regarding data handling presents a significant challenge for the Smart Contact Lenses Market. According to the European Data Protection Board (EDPB), wearable devices that capture continuous sensory data raise complex issues related to consent, transparency, and data ownership. Regulatory bodies in different jurisdictions have yet to establish clear guidelines specific to smart lenses, which is leading to inconsistencies in compliance requirements. In some countries, strict data localization laws may restrict cross-border transmission of sensitive health information, complicating global deployments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, End-User & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Google LLC, Sensimed AG, Novartis International AG, Samsung Electronics Company Ltd, Rockwell Automation Inc., Sony Corporation, Hitachi Ltd, Alcon Laboratories, Inc., Atmel Corporation, and Mojo Vision, Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The daily wear soft lenses segment held 43.2% of the Smart Contact Lenses Market share in 2024. According to the American Optometric Association (AOA), over 70% of contact lens wearers in the U.S. prefer soft lenses, indicating a strong preference trend that extends into smart lens adoption. Moreover, daily disposables align well with hygiene-conscious consumers who seek reduced risk of eye infections and lower maintenance requirements. Smart lens developers are leveraging this preference by designing biocompatible, flexible electronics embedded within soft hydrogel or silicone hydrogel materials.

The planned replacement lenses segment is projected to grow with a CAGR of 14.6% during the forecast. In regions with high rates of refractive errors, such as North America and Europe, planned replacement lenses are increasingly preferred for their economic viability and convenience. Additionally, manufacturers are introducing smart versions of these lenses that incorporate biosensors for glucose monitoring or intraocular pressure tracking, extending their utility beyond traditional vision correction. These features appeal to chronic disease patients who require regular health data without the burden of frequent device changes. Furthermore, healthcare professionals recommend planned replacement schedules to reduce complications related to microbial keratitis and protein buildup, encouraging wider adoption across clinical and home-use settings.

By Application Insights

The Continuous glucose monitoring (CGM) segment held 51.2% of the Smart Contact Lenses Market share in 2024. According to the International Diabetes Federation (IDF), over 537 million adults were living with diabetes in 2021, with projections exceeding 643 million by 2030. This growing patient base has intensified research into alternative monitoring methods that eliminate the discomfort of finger-prick tests. Smart contact lenses equipped with tear-based biosensors offer a promising solution by continuously measuring glucose levels through ocular fluids. Major players such as Google Health and Novartis have explored prototypes capable of transmitting real-time glucose data to smartphones or cloud platforms, enabling proactive diabetes management.

The Intraocular pressure (IOP) monitoring segment is anticipated to register a CAGR of 15.8% in the coming years. As per the World Health Organization (WHO), glaucoma affects nearly 80 million people worldwide, with early detection being key to preventing vision loss. The Sensimed Triggerfish lens, one of the first FDA-approved smart contact lenses, has already demonstrated the feasibility of real-time IOP tracking for glaucoma patients.

By End-User Insights

The hospitals and clinics segment was the largest and held a significant share of the Smart Contact Lenses Market in 2024. Smart lenses used in hospitals are primarily employed for diagnostic purposes, including continuous glucose monitoring and intraocular pressure assessment. According to the American Academy of Ophthalmology (AAO), many ophthalmology departments are piloting smart lens trials to improve glaucoma management and diabetic retinopathy screening. These settings provide structured calibration, data validation, and integration with electronic health records (EHRs), ensuring compliance with medical device regulations. Additionally, hospitals often serve as testing grounds for new technologies before they reach consumer markets. Government-funded research programs and partnerships between academic institutions and tech firms are accelerating clinical deployment. As per the National Institutes of Health (NIH), over 30 clinical trials involving smart contact lenses were underway in 2023, focusing on disease monitoring and treatment efficacy.

The home care settings segment is expected to register a CAGR of 16.4% with the shift toward decentralized healthcare delivery and increasing demand for self-monitoring tools. Patients managing chronic conditions such as diabetes and glaucoma are increasingly adopting portable, user-friendly diagnostic wearables. According to the Centers for Disease Control and Prevention (CDC), nearly 90% of older Americans suffer from at least one chronic illness, prompting a surge in home-based health monitoring solutions. Smart contact lenses offer a discreet, non-invasive method for collecting real-time physiological data without requiring frequent hospital visits. Technological advancements in wireless connectivity, mobile app integration, and cloud-based analytics are making it easier for consumers to interpret and act upon health insights derived from smart lenses. Moreover, the rise of telehealth services allows physicians to remotely review patient data captured via smart lenses, enhancing continuity of care.

REGIONAL ANALYSIS

North America Smart Contact Lenses Market Analysis

North America was the largest contributor of the global Smart Contact Lenses Market by accounting for 38.3% of the share in 2024. The United States leads in clinical trials and product development initiatives, supported by major players such as Google, Johnson & Johnson Vision, and Bausch + Lomb. According to the National Eye Institute (NEI), over 45 million Americans use contact lenses, providing a substantial consumer base for next-generation smart lenses.

Federal support for wearable medical devices, coupled with high smartphone penetration and digital health literacy, has accelerated the adoption of smart lens technology. Regulatory bodies like the FDA are actively reviewing new submissions, facilitating faster commercialization pathways.

Europe Smart Contact Lenses Market Analysis

Europe Smart Contact Lenses Market held 24.3% of the share in 2024 due to its strong emphasis on healthcare innovation and regulatory harmonization. Positioned as a leader in medical device approvals, the region fosters a conducive environment for smart lens development and clinical trials. Countries like Germany, Switzerland, and the United Kingdom host world-class research institutions and ophthalmic centers that collaborate with tech startups and multinational corporations. The Medical Device Regulation (MDR) framework ensures rigorous safety and performance standards while supporting digital health integration. Public-private partnerships, such as Horizon Europe grants, further encourage cross-border collaboration in wearable diagnostics. Additionally, the aging population and rising prevalence of diabetes and glaucoma in Western Europe create a growing demand for continuous monitoring solutions, reinforcing the region’s strategic importance in the smart lens landscape.

Asia-Pacific Smart Contact Lenses Market Analysis

Asia-Pacific Smart Contact Lenses Market growth is lucratively growing with the growing diabetic population, increasing investment in digital health, and expanding ophthalmic infrastructure. Japan and South Korea lead in technological development, with companies like Sony, Samsung, and LG investing in AR-integrated smart lenses and biosensor research. According to the International Diabetes Federation (IDF), China alone accounts for over 140 million diabetes cases, which is creating a vast pool of prospective users for glucose-monitoring lenses. India and Southeast Asian nations are witnessing a surge in telemedicine adoption, driving interest in remote diagnostic tools.

Latin America Smart Contact Lenses Market Analysis

Latin America Smart Contact Lenses Market is swiftly growing with an emerging role in regional healthcare innovation. Positioned as a growing market for digital health solutions, the region is experiencing increased demand for non-invasive monitoring tools due to rising chronic disease prevalence and improved healthcare access. Brazil led the market with academic institutions and startups exploring smart lens applications for diabetes and glaucoma management. Mexico and Argentina are also witnessing interest in smart health wearables, supported by expanding telemedicine networks and government-backed health tech initiatives.

Middle East and Africa Smart Contact Lenses Market Analysis

The Middle East and Africa Smart Contact Lenses Market growth is an evolving sector within the region’s broader digital health transformation. Positioned as a market with high unmet medical needs, MEA is witnessing growing investment in wearable diagnostics and telemedicine. The Gulf Cooperation Council (GCC) countries, particularly the UAE and Saudi Arabia, are leading the charge with national health digitization strategies under frameworks like Saudi Vision 2030 and UAE Centennial 2071. According to the Dubai Health Authority (DHA), there has been a surge in interest in AI-driven diagnostics and remote patient monitoring solutions. Africa faces infrastructural and financial barriers but shows promise in select areas such as teleophthalmology and mobile health applications. Countries like South Africa and Egypt are piloting smart lens research collaborations with international partners, aiming to address high rates of undiagnosed diabetes and glaucoma.

COMPETITIVE LANDSCAPE

The Smart Contact Lenses Market is highly competitive, characterized by a blend of tech giants, established medical device firms, and innovative startups striving to redefine wearable diagnostics and augmented vision. While Google and Johnson & Johnson bring brand recognition and extensive resources, niche players like Sensimed and Mojo Vision are making significant strides in specific therapeutic applications.

Competition is intensifying not only in technological innovation but also in regulatory navigation, clinical validation, and consumer acceptance. Firms are racing to overcome engineering challenges related to power efficiency, sensor accuracy, and long-term ocular safety while ensuring seamless integration with digital health ecosystems.

Differentiation is increasingly driven by application focus, whether in continuous glucose monitoring, intraocular pressure tracking, or augmented reality interfaces. Strategic alliances, intellectual property acquisition, and pilot programs with hospitals are shaping the pace of market entry.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global smart contact lenses market include

Google LLC, Sensimed AG, Novartis International AG, Samsung Electronics Company Ltd, Rockwell Automation Inc., Sony Corporation, Hitachi Ltd, Alcon Laboratories, Inc., Atmel Corporation, and Mojo Vision, Inc. are some of the noteworthy companies operating in the global smart contact lenses market profiled in this report.

TOP LEADING PLAYERS IN THE MARKET

- Verily, a subsidiary of Alphabet Inc. has been a pioneer in developing smart contact lenses for health monitoring applications. The company’s early collaboration with Novartis to develop a glucose-monitoring lens laid the foundation for future innovations in this space. Although the initial diabetes-focused project was discontinued, Verily continues to explore applications in ophthalmic diagnostics and chronic disease management. Its integration of microelectronics, data analytics, and biocompatible materials has significantly influenced the direction of smart lens research globally.

- Johnson & Johnson Vision, a division of Johnson & Johnson, is a leading player in traditional contact lens manufacturing and has extended its expertise into the smart lens domain. The company has invested heavily in partnerships and internal R&D to integrate biosensors into soft contact lenses for continuous eye health monitoring. Johnson & Johnson is positioning itself as a bridge between conventional vision correction and next-generation wearable diagnostics.

- Sensimed is a trailblazer in intraocular pressure monitoring through its FDA-approved smart contact lens, the Triggerfish. The lens continuously tracks pressure fluctuations over 24 hours by offering valuable insights for personalized treatment planning. Sensimed’s success in clinical validation and regulatory approval has set a benchmark for other companies entering the market. Its focus on medical-grade wearables has contributed significantly to the legitimacy and credibility of smart contact lenses in healthcare.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by key players in the Smart Contact Lenses Market is strategic collaborations and joint ventures between technology firms and established ophthalmic or pharmaceutical companies. These partnerships enable access to specialized expertise in sensor development, biocompatibility, and regulatory pathways, which is accelerating time-to-market for complex bioelectronic devices.

Another strategy is investment in advanced R&D focused on miniaturization and flexible electronics by allowing manufacturers to embed biosensors and wireless communication modules into ultra-thin, wearable lenses without compromising comfort or functionality. Companies are also exploring energy-efficient designs and novel power sources such as near-field communication (NFC) and energy harvesting.

The targeted regulatory engagement and pilot testing in clinical environments have become essential strategies. Companies ensure compliance, build physician trust, and refine product performance before broader commercial deployment.

GLOBAL SMART CONTACT LENSES MARKET NEWS

- In February 2024, Johnson & Johnson Vision announced a strategic partnership with a Swiss biomedical research institute to advance biosensor-integrated contact lenses for diabetic monitoring by aiming to enhance diagnostic accuracy and expand clinical applications beyond current limitations.

- In May 2024, Google Health resumed its exploratory work on smart lenses by collaborating with a South Korean semiconductor manufacturer to develop ultra-thin, flexible microchips tailored for integration into future generations of bioelectronic contact lenses.

- In August 2024, Sensimed launched a new version of its Triggerfish smart contact lens with improved telemetry capabilities, designed for longer wear duration and better patient comfort with its dominant position in glaucoma diagnostics.

- In October 2024, Mojo Vision unveiled an updated prototype of its AR-enabled smart contact lens featuring enhanced display resolution and integrated voice-command functionality by signaling a shift toward broader consumer applications beyond medical use.

- In December 2024, a Japanese startup specializing in nano-biosensors signed a licensing agreement with a U.S.-based eyewear giant to co-develop a line of affordable, mass-producible smart lenses targeting both healthcare and enterprise markets by marking a pivotal step toward commercial scalability.

MARKET SEGMENTATION

This research report on the global smart contact lenses market has been segmented and sub-segmented based on type, application, end-user, and region.

By Type

- Rapid Gas Permeable (RGP)

- Daily Wear Soft Lenses

- Extended wear

- Planned Replacement

By Application

- Continuous Glucose Monitoring

- Intraocular Pressure Monitoring

By End-User

- Hospital & Clinics

- Home Care Settings

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the global smart contact lenses market?

The global smart contact lenses market develops embedded sensor lenses monitoring glucose, eye pressure, and vital signs non-invasively for health management.

Why grow the global smart contact lenses market?

The global smart contact lenses market expands with diabetes prevalence demanding continuous glucose monitoring without finger pricks.

What drives the global smart contact lenses market?

Glaucoma monitoring needs propel the global smart contact lenses market alongside AR vision enhancement applications.

Which applications lead the global smart contact lenses market?

Diabetes management dominates the global smart contact lenses market through tear glucose analysis technology.

What materials define the global smart contact lenses market?

PHEMA hydrogels enable sensor integration in the global smart contact lenses market for comfort and breathability.

How does power work in the global smart contact lenses market?

Micro-antennas harvest RF energy in the global smart contact lenses market powering embedded electronics wirelessly.

Which conditions benefit from the global smart contact lenses market?

Glaucoma patients gain IOP tracking in the global smart contact lenses market preventing vision loss proactively.

What challenges face the global smart contact lenses market?

Miniaturization limits battery life in the global smart contact lenses market requiring wireless charging innovations.

How does AR fit the global smart contact lenses market?

Augmented reality overlays information in the global smart contact lenses market for navigation and data visualization.

What is glucose sensing in the global smart contact lenses market?

Enzyme-based sensors detect tear glucose in the global smart contact lenses market correlating to blood levels.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com