Global Prosthetics Market Size, Share, Trends & Growth Forecast Report By Product Type, Technology, End-User and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Global Prosthetics Market Report Summary

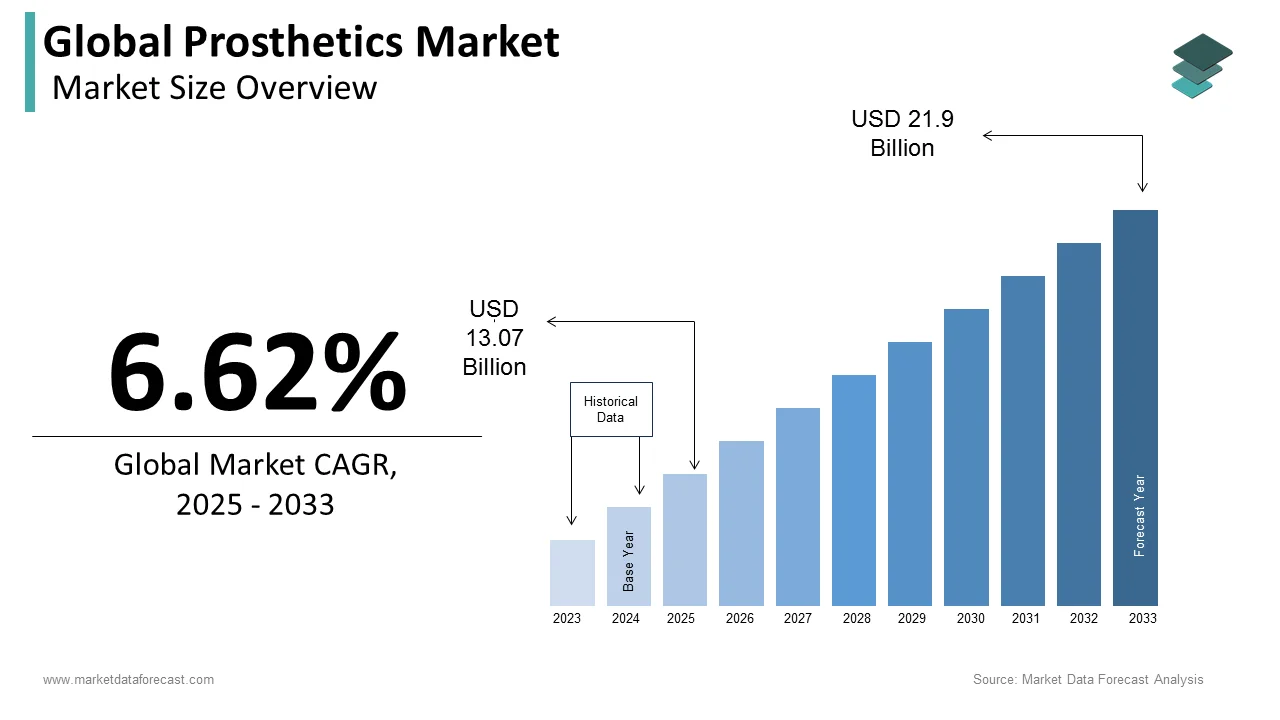

The global prosthetics market was valued at USD 13.07 billion in 2025, is estimated to reach USD 13.94 billion in 2026, and is projected to reach USD 23.27 billion by 2034, growing at a CAGR of 6.62% from 2026 to 2034. Market growth is driven by the increasing prevalence of limb loss due to trauma, diabetes, and vascular diseases, along with rising demand for advanced prosthetic solutions. Technological advancements in materials, robotics, and sensor integration are significantly improving the functionality and comfort of prosthetic devices. Additionally, growing awareness, improved rehabilitation services, and expanding healthcare access are further supporting market growth globally.

Key Market Trends

- Rising prevalence of diabetes and vascular diseases leading to limb loss.

- Increasing adoption of advanced and bionic prosthetic devices.

- Advancements in robotics, sensors, and lightweight materials.

- Growing focus on patient mobility, comfort, and customization.

- Expansion of rehabilitation services and prosthetic care centers.

Segmental Insights

- Based on product type, the lower extremity prosthetics segment dominated the global prosthetics market by capturing 66.5% share in 2025, driven by the high incidence of lower limb amputations.

- Based on technology, the body-powered prosthetics segment held the largest share of 46.4% in 2025, supported by affordability, durability, and ease of use.

- Based on end user, the prosthetic clinics segment led the market with 54.4% share in 2025, driven by specialized care and customization services.

Regional Insights

The global prosthetics market is witnessing steady growth across regions due to increasing healthcare awareness and technological advancements.

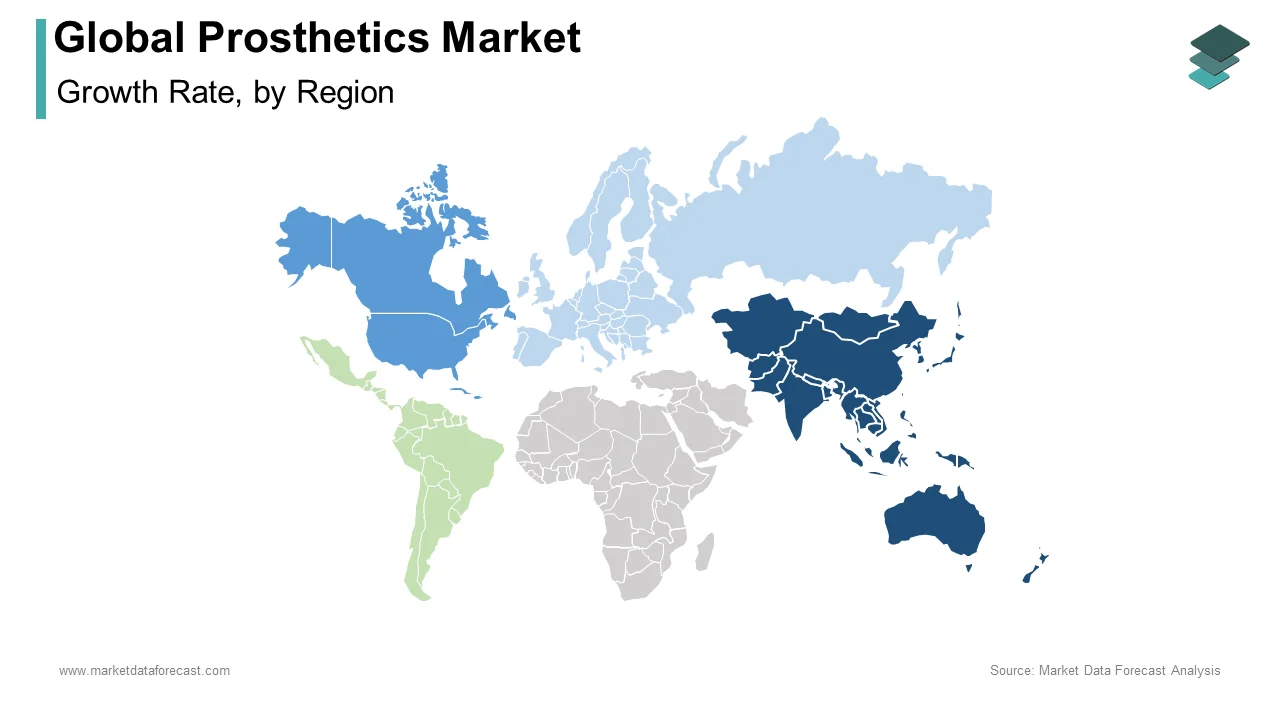

- North America led the market in 2025 with 41.4% share, supported by advanced healthcare infrastructure and high adoption of innovative prosthetic technologies.

- Europe followed with 26.2% share in 2025, driven by strong public healthcare systems and technological innovation.

- Asia-Pacific is the fastest-growing region due to increasing healthcare investments and rising awareness.

- Latin America holds a notable share, supported by improving healthcare access and rehabilitation services.

Competitive Landscape

The global prosthetics market is competitive, with the presence of established manufacturers and emerging innovators focusing on advanced prosthetic technologies. Companies are investing in R&D, developing bionic and AI-integrated prosthetics, and expanding their global reach. Strategic collaborations and product innovation are shaping competitive dynamics across the market.

Prominent companies operating in the global prosthetics market include CBPE Capital LLP (Blatchford Limited), Coapt LLC, Colfax Corporation (DJO, LLC), Ossur (College Park Industries), Mobius Bionics LLC, Motorica LLC, Ottobock SE & Co. KGaA, Naked Prosthetics, Blatchford Products Ltd, Protunix, and Steeper Group.

Global Prosthetics Market Size

The size of the global prosthetics market was worth USD 13.07 billion in 2025. The global market is anticipated to grow at a CAGR of 6.62% from 2026 to 2034 and be worth USD 23.27 billion by 2034 from USD 13.94 billion in 2026.

Prosthetics are artificial devices intended to replace missing body parts resulting from trauma, disease, or congenital conditions. These devices range from simple cosmetic covers to advanced bionic limbs equipped with microprocessors and sensory feedback systems that mimic natural human movement. The primary objective extends beyond physical restoration to include the psychological rehabilitation and social reintegration of amputees. Globally, the need for such interventions is substantial, with the World Health Organization estimating that approximately 30 million people require prosthetic or orthotic devices yet lack access to them. According to the Centers for Disease Control and Prevention, amputations remain a major public health issue in the United States, with vascular disease and diabetes contributing significantly to these cases. As per the International Committee of the Red Cross, conflict zones add heavily to the burden, with landmines and explosive remnants of war continuing to cause new limb losses every year. Technological evolution has shifted the paradigm from passive replacement to active restoration, with myoelectric sensors now allowing users to control grip strength and wrist rotation through muscle signals. According to the Global Partnership for Assistive Technology, access to appropriate prosthetic care remains extremely limited in low-income regions, where only a small fraction of those in need receive support. This landscape defines a critical intersection of medical necessity, engineering innovation, and humanitarian obligation.

MARKET DRIVERS

Rising Prevalence of Diabetes and Vascular Diseases Leading to Amputations

The escalating global incidence of diabetes mellitus and peripheral vascular diseases is driving the expansion of the global prosthetics market. Chronic hyperglycemia often leads to diabetic neuropathy and poor circulation, resulting in non-healing ulcers that frequently necessitate amputation to prevent life-threatening infections. According to the International Diabetes Federation, the number of adults living with diabetes continues to rise globally, creating a vast and expanding pool of potential amputees. As per the American Diabetes Association, diabetes is responsible for a large share of non-traumatic lower-limb amputations in the United States. The aging population exacerbates this trend, as older adults are more susceptible to vascular complications and slower wound healing processes. Furthermore, the rising rates of obesity globally act as a compounding factor, increasing the strain on the cardiovascular system and accelerating the onset of peripheral artery disease. As healthcare systems improve survival rates for patients with severe chronic conditions, the subsequent need for rehabilitative devices, including prosthetics, grows proportionally. This demographic shift ensures a sustained and increasing volume of patients requiring sophisticated lower extremity solutions to regain mobility and independence.

Technological Advancements in Bionic and Myoelectric Prosthetics

Breakthroughs in robotics, artificial intelligence, and neural interfacing have fundamentally transformed the functionality and appeal of modern prosthetic devices, which is further driving market expansion through enhanced user adoption. Contemporary bionic limbs utilize myoelectric sensors to detect electrical signals from residual muscles, allowing users to perform complex movements such as individual finger articulation and variable grip strength with intuitive control. According to the Journal of NeuroEngineering and Rehabilitation, advanced microprocessor-controlled knees improve safety and confidence for transfemoral amputees compared to mechanical alternatives. As per the European Society of Physical and Rehabilitation Medicine, osseointegration technology has shown high success rates, eliminating socket discomfort and improving force transmission. Additionally, the development of sensory feedback systems allows users to perceive texture and temperature, bridging the gap between biological and artificial limbs. These technological leaps not only improve functional outcomes but also reduce the psychological burden of limb loss, encouraging earlier adoption and upgrades. As manufacturing costs decrease through 3D printing and modular designs, these high-tech solutions become increasingly accessible and fuel demand across diverse economic segments.

MARKET RESTRAINTS

Prohibitive Costs and Inadequate Insurance Reimbursement Policies

The exorbitant cost of advanced prosthetic devices, coupled with restrictive insurance coverage, is significantly hampering the prosthetics market growth worldwide. According to the Amputee Coalition, many applicants seeking bionic devices face denial of claims due to insurers categorizing advanced components as luxury items rather than medically necessary. Policies often impose strict caps on reimbursement amounts or limit replacements to long intervals, ignoring the rapid wear and tear experienced by active users or growing children. In developing nations, the situation is even more dire, with the World Bank noting that only a small fraction of amputees in low-income countries can afford even basic prosthetic care due to a lack of government funding and insurance infrastructure. The high maintenance costs and need for specialized fitting further exacerbate the financial burden, forcing many patients to rely on outdated or ill-fitting devices that hinder mobility and cause secondary health issues. Until reimbursement frameworks evolve to recognize the long-term socioeconomic benefits of advanced prosthetics, cost will remain a primary constraint on market growth.

Shortage of Certified Prosthetists and Orthotists Globally

A critical scarcity of trained professionals capable of designing, fitting, and maintaining prosthetic devices is further limiting the prosthetics market expansion worldwide. The complexity of modern prosthetics requires highly skilled practitioners who can integrate clinical assessment with technical engineering, yet the global workforce is insufficient to meet rising demand. According to the National Commission on Orthotic and Prosthetic Education, the number of certified prosthetists and orthotists in the United States is relatively low compared to the population in need. As per the World Health Organization, some regions in low- and middle-income countries have extremely limited access to prosthetists, with ratios far below adequate levels. This shortage leads to prolonged waiting times for initial fittings, which delays rehabilitation and increases the risk of muscle atrophy and joint contractures. Furthermore, the lack of experts restricts the deployment of advanced technologies, as sophisticated bionic limbs require precise calibration and ongoing adjustments that general medical staff cannot provide. Educational programs face capacity constraints and high tuition costs, limiting the pipeline of new graduates. Without a significant expansion in training infrastructure and recruitment initiatives, the human resource gap will continue to stifle the effective delivery of prosthetic services worldwide.

MARKET OPPORTUNITIES

Integration of 3D Printing and Additive Manufacturing Technologies

The adoption of 3D printing and additive manufacturing offers a promising opportunity for the prosthetics market. Traditional manufacturing methods involve labor-intensive molding and machining processes that can take weeks and cost thousands of dollars, whereas 3D printing allows for the rapid fabrication of custom sockets and structural components within days at a fraction of the price. According to e-NABLE, 3D printed prosthetic hands can be produced at very low material costs, making them viable for children who outgrow devices quickly and require frequent replacements. The technology enables unprecedented customization, allowing scanners to capture precise residual limb geometries and generate perfectly fitted sockets that enhance comfort and suspension. As per the Journal of Prosthetics and Orthotics, 3D printed sockets have been shown to reduce fit issues compared to conventional casted models. Furthermore, decentralized production models allow local clinics in remote areas to print devices on-site, eliminating logistical barriers and shipping costs associated with centralized factories. As material science advances to produce stronger, lighter, and more durable polymers and metals, the scope of 3D printed prosthetics will expand from temporary devices to permanent high-performance solutions, opening vast new markets in underserved regions.

Development of Neural Interfaces and Sensory Feedback Systems

The emerging field of neural interfaces and sensory feedback offers a lucrative opportunity to revolutionize prosthetic functionality by restoring the bidirectional communication loop between the brain and the artificial limb. Current prosthetics primarily rely on motor commands, but next-generation systems aim to provide tactile sensation, allowing users to feel pressure, texture, and temperature, which is crucial for fine motor tasks and embodiment. According to research from the University of Chicago, clinical trials involving targeted muscle reinnervation and implanted electrodes have shown promising results, with participants able to identify objects by touch alone. This capability significantly reduces the cognitive load required to operate a prosthetic and mitigates the phenomenon of phantom limb pain, which affects a large share of amputees. The commercialization of these neuro-technological advancements could create a premium market segment for high-end restorative devices, attracting investment from both medical device giants and technology companies. As regulatory pathways for implantable devices become clearer and long-term safety data accumulates, the integration of sensory feedback will likely become a standard feature in upper limb prosthetics, driving substantial revenue growth and improving the quality of life for millions of users globally.

MARKET CHALLENGES

Psychological Barriers and Device Abandonment Rates

Despite technological strides, psychological factors and poor device fit contribute to high abandonment rates, which pose a significant challenge to the prosthetics market growth. According to the studies, many upper limb amputees eventually stop using their prosthetic devices, often citing discomfort, excessive weight, or the inability to perform daily tasks efficiently as primary reasons. The psychological adjustment to limb loss is profound, and if the initial prosthetic experience is frustrating or painful, users may retreat from rehabilitation entirely. According to the Archives of Physical Medicine and Rehabilitation, lack of intuitive control and insufficient sensory feedback are major contributors to dissatisfaction, leading users to prefer simpler devices or no device at all. Furthermore, the aesthetic appearance of prosthetics can impact self-esteem, with many users feeling self-conscious about mechanical looks that draw unwanted attention. The disconnect between clinical expectations and real-world usability often results in devices being stored away rather than integrated into daily life. Addressing this challenge requires a holistic approach that combines improved ergonomic design with robust psychological support and extensive training programs.

Regulatory Hurdles and Lengthy Approval Processes for Innovative Devices

The stringent and often protracted regulatory approval processes for novel prosthetic technologies create significant delays in market entry and increase development costs for manufacturers, which further challenge the growth of the global prosthetics market. Agencies such as the Food and Drug Administration in the United States and the European Medicines Agency classify advanced bionic and implantable prosthetics as high-risk devices, requiring extensive clinical trials and rigorous documentation to prove safety and efficacy. According to the Advanced Medical Technology Association, the average time to market for new neuro-prosthetic devices has increased in recent years due to evolving compliance requirements. These delays deny patients access to cutting-edge solutions that could dramatically improve their quality of life. Additionally, the uncertainty surrounding reimbursement eligibility during the approval phase creates financial risks for manufacturers. Streamlining regulatory pathways while maintaining safety standards is essential to foster innovation and ensure that technological advancements reach patients promptly.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Technology, End-User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | CBPE Capital LLP (Blatchford Limited), Coapt LLC., Colfax Corporation (DJO, LLC), Ossur (College Park Industries), Mobius Bionics LLC., Motorica LLC., Naked Prosthetics, Ottobock SE & Co. KGaA, Protunix, and Steeper Group. |

SEGMENTAL ANALYSIS

By Product Type Insights

The lower extremity prosthetics segment led the market by holding 66.5% of the global market share in 2025. This dominance is directly correlated with the higher incidence of lower limb amputations compared to upper limb losses, driven primarily by vascular diseases and diabetes. The biomechanical complexity of walking and bearing body weight necessitates robust and often expensive devices ranging from basic feet to microprocessor-controlled knees. According to the Centers for Disease Control and Prevention, lower limb amputations occur in large numbers annually in the United States, vastly outnumbering upper limb procedures. The aging global population further exacerbates this trend, as older adults are more susceptible to peripheral artery disease and diabetic complications that lead to leg loss. As per the World Health Organization, lower limb mobility is critical for independence, driving consistent demand for replacements and upgrades throughout a patient's life. Furthermore, trauma from road accidents and conflicts frequently results in lower limb injuries, sustaining a steady flow of new patients requiring these essential devices across both developed and developing nations.

Within the product type category, the knee prosthetics segment is projected to be the fastest-growing sub-segment and expand at a CAGR of 9.4% over the forecast period, owing to the transition from mechanical hinges to intelligent microprocessor-controlled knees that offer unprecedented stability and adaptability. Transfemoral amputees face significant challenges with balance and fall risk, driving strong demand for advanced solutions that mimic natural knee function. The aging population, which is more prone to falls and fractures, represents a key demographic seeking these safer technologies. According to the National Institute on Aging, falls are a leading cause of injury-related death among older adults, prompting clinicians and patients to prioritize stability features found in high-tech knee units. Furthermore, insurance coverage expansions in major markets are increasingly recognizing the cost-effectiveness of preventing fall-related hospitalizations through better prosthetic technology. The integration of sensors and artificial intelligence allows these knees to adjust resistance in real time based on walking speed and terrain, appealing to a broader range of activity levels. As manufacturing costs decrease and accessibility improves, the adoption of advanced knee prosthetics is accelerating faster than any other component type.

By Technology Insights

The body-powered prosthetics segment retained the largest share of the global market by capturing 46.4% of the global market in 2025. The growth of the body-powered prosthetics segment in the global market is attributed to their mechanical simplicity, exceptional durability, and lower cost compared to electrically powered alternatives. These devices operate through a harness and cable system that translates body movements into hand or hook closure, providing direct proprioceptive feedback to the user. In developing regions and for patients with limited access to electricity or specialized maintenance, body-powered limbs remain the standard of care. The Veterans Health Administration in the United States continues to prescribe body-powered devices for a significant portion of upper limb amputees due to their reliability in rugged environments. According to the International Society for Prosthetics and Orthotics, body-powered devices demonstrate lower failure rates compared to myoelectric counterparts, making them ideal for manual laborers and children who subject their limbs to heavy use. The lack of batteries and complex electronics eliminates charging concerns and reduces downtime, ensuring continuous usability. While technology advances, the practical advantages of mechanical systems ensure they remain the most widely used solution globally.

On the other hand, the electrically powered prosthetics segment is the fastest-growing technology segment and is expected to exhibit a CAGR of 10.4% over the forecast period, owing to the rapid advancements in sensor technology, battery efficiency, and artificial intelligence that have dramatically improved the functionality and intuitiveness of these limbs. Modern myoelectric hands offer multiple grip patterns and individual finger movement, closely mimicking natural human dexterity. The decreasing cost of components and increasing insurance coverage in developed markets are removing historical barriers to adoption. According to the Journal of NeuroEngineering and Rehabilitation, user satisfaction scores for myoelectric devices have risen significantly in recent years due to improved control algorithms and lighter materials. The growing veteran population in North America and Europe, who often have access to comprehensive healthcare benefits, is a key demographic driving this growth. Additionally, the aesthetic appeal of lifelike silicone covers and the psychological benefit of controlling a device through muscle signals are attracting more users. As technology matures and becomes more affordable, the electrically powered segment is poised to capture an increasing share of the global market.

By End-User Insights

The prosthetic clinics segment dominated the market by accounting for 54.4% of the global market share in 2025. These specialized facilities serve as the primary point of contact for amputees, offering comprehensive services ranging from initial assessment and casting to fitting, alignment, and long-term maintenance. The concentrated expertise of certified prosthetists and orthotists within these clinics ensures high-quality customization that general hospitals often cannot match. Patients prefer clinics for their personalized care models and the ability to build long-term relationships with their providers. According to the National Association of Prosthetists and Orthotists, a majority of routine prosthetic adjustments and repairs are performed in outpatient clinic settings. The decentralized nature of clinics allows them to serve local communities effectively, reducing travel burdens for patients requiring frequent follow-ups. Furthermore, many clinics operate as independent businesses or part of larger networks, allowing for flexible scheduling and dedicated attention to patient rehabilitation goals. The holistic approach of combining device provision with gait training and counseling solidifies their position as the central hub for prosthetic care delivery globally.

On the other end, the rehabilitation centers segment is emerging as the fastest-growing end-user segment for prosthetics and is estimated to witness a CAGR of 9.2% over the forecast period, owing to the increasing recognition of the critical role intensive rehabilitation plays in successful prosthetic adoption and the shifting of post-acute care to specialized facilities. Hospitals are increasingly discharging amputees earlier to reduce costs, transferring the burden of recovery to dedicated rehab centers equipped with advanced gait labs and simulation technologies. The rise in traumatic injuries from accidents and conflicts has also boosted admissions to these centers, where multidisciplinary teams focus on maximizing functional independence. According to the Commission on Accreditation of Rehabilitation Facilities, the number of accredited rehabilitation programs specializing in amputee care has increased in recent years. These centers are investing heavily in robotic gait training systems and virtual reality tools to accelerate the learning curve for new prosthetic users. The trend towards value-based care, which rewards functional outcomes rather than volume of services, further drives referrals to specialized rehabilitation facilities capable of delivering measurable improvements in patient mobility and quality of life.

REGIONAL ANALYSIS

North America Prosthetics Market Analysis

North America held 41.4% of the global market share in 2025. The supremacy of North America in the global prosthetics market is driven by favorable reimbursement policies, high disposable income, and a mature ecosystem of care. Medicare and private insurers in the US cover a wide range of prosthetic components, including advanced microprocessor knees and myoelectric hands, reducing financial barriers for patients. According to the National Institutes of Health, the US invests heavily in biomedical research, spurring the development of next-generation neural interfaces and osseointegration techniques. As per the Amputee Coalition, millions of people in the US live with limb loss, creating a vast addressable market. The concentration of top-tier rehabilitation centers and certified prosthetists ensures high-quality service delivery and patient education. Furthermore, the legal framework protecting the rights of individuals with disabilities mandates reasonable accommodations, encouraging workforce participation, and the need for functional prosthetics. These structural and demographic factors create a self-reinforcing cycle of demand and innovation that keeps North America at the forefront.

Europe Prosthetics Market Analysis

Europe captured the second-largest position in the global prosthetics market in 2025 with 26.2% of the global market share due to a diverse landscape of well-funded public healthcare systems and advanced technological adoption. The growth of the prosthetics market in Europe is propelled by robust public funding, an aging demographic, and a strong focus on research and development. National health services in countries like the UK and Germany provide comprehensive coverage for prosthetic devices, minimizing out-of-pocket costs for patients and ensuring high uptake rates. According to Eurostat, the proportion of people over 65 is increasing rapidly, correlating with higher demand for mobility aids. As per the European Commission, numerous collaborative research projects are funded to improve prosthetic functionality and reduce costs, fostering innovation across the continent. The region's strong tradition of engineering excellence supports the production of high-precision mechanical and electronic components. Furthermore, the emphasis on social inclusion and disability rights drives policies that support employment and active lifestyles for amputees, necessitating reliable and advanced prosthetic solutions. The harmonization of regulations under the EU Medical Device Regulation also streamlines market entry for new technologies, encouraging competition and variety.

Asia Pacific Prosthetics Market Analysis

Asia Pacific is the fastest-growing region in the global prosthetics market. The rapid ascent of the Asia Pacific prosthetics market is fueled by economic development, government health initiatives, and a large burden of disease. Rapid urbanization and industrialization have led to an increase in workplace and road traffic accidents, generating a steady stream of traumatic amputations requiring immediate intervention. Governments in China and India are implementing national disability acts and health insurance schemes that expand coverage for prosthetic devices. According to the Asian Development Bank, rising disposable incomes are allowing more families to seek private care and advanced prosthetic options. As per the International Osteoporosis Foundation, Asia is expected to account for a majority of global hip fractures by 2050, further driving demand. The region is also becoming a manufacturing hub, with local companies producing cost-effective devices that cater to price-sensitive markets. The growing awareness of disability rights and the influence of international NGOs are helping to destigmatize limb loss and encourage rehabilitation. As healthcare infrastructure improves and accessibility increases, the latent demand in this populous region is expected to drive sustained double-digit growth.

Latin America Prosthetics Market Analysis

Latin America accounts for a notable share of the global prosthetics market. Brazil and Mexico are the regional leaders, driven by expanding private healthcare sectors and government efforts to improve public health infrastructure. The development of the prosthetics market in Latin America is driven by the dual burden of chronic diseases and traumatic injuries, alongside efforts to strengthen social safety nets. According to the Pan American Health Organization, musculoskeletal disorders are among the top causes of disability in the region, creating a pressing need for affordable management solutions. As per the Latin American Society of Physical Medicine and Rehabilitation, a growing network of trained professionals is working to improve care standards. The presence of local manufacturers helps reduce costs and tailor devices to the specific needs and climates of the region. Economic growth in certain sectors is increasing the affordability of private healthcare, allowing more individuals to access advanced prosthetic technologies. International collaborations and donations from global organizations also play a vital role in supplying devices to public hospitals. Despite economic challenges, the fundamental need for mobility and the push for social inclusion are driving steady progress in the market.

Middle East and Africa Prosthetics Market Analysis

The Middle East and Africa region holds the smallest share of the global prosthetics market but presents distinct opportunities for humanitarian and commercial growth. The Gulf Cooperation Council countries, particularly the UAE and Saudi Arabia, are leading the way with high investments in world-class healthcare facilities and prosthetic centers. In contrast, many African nations face significant challenges related to conflict, landmines, and limited healthcare infrastructure, resulting in a high unmet need for basic prosthetic devices. The emerging growth of the prosthetics market in the Middle East and Africa is driven by post-conflict reconstruction efforts, government vision plans, and increasing awareness of disability rights. As per Saudi Vision 2030, national goals include developing advanced healthcare ecosystems, leading to the importation of state-of-the-art prosthetic technologies and the training of local specialists. According to the Global Fund, substantial investments in health systems indirectly benefit prosthetic services through improved infrastructure. In Africa, the fight against the legacy of landmines and the rising incidence of diabetes are key drivers, supported by funding from global health organizations and NGOs. The establishment of regional centers of excellence marks a significant step towards building local capacity. The growing population and urbanization are also contributing to increased healthcare utilization. While challenges remain, the commitment to improving health security and the influx of resources are laying the groundwork for sustainable market growth in the coming decades.

COMPETITIVE LANDSCAPE

The competition in the prosthetics market is intense and characterized by a mix of established multinational corporations and agile niche innovators striving for technological superiority. Large players leverage their extensive distribution networks and brand reputation to dominate developed markets, while smaller firms compete through specialized products or lower-cost solutions for emerging economies. Differentiation increasingly relies on integrating smart technologies such as sensors and machine learning algorithms rather than purely mechanical advantages. Regulatory compliance and clinical evidence serve as significant barriers to entry, favoring companies with robust quality management systems and resources for extensive trials. The shift towards value-based care forces competitors to demonstrate superior functional outcomes and cost effectiveness to secure reimbursement from payers and government programs. Price pressure remains a challenge, particularly in public healthcare systems, driving manufacturers to optimize production efficiency without compromising quality. Mergers and acquisitions activity is high as companies seek to fill technology gaps or enter new geographic regions quickly. This dynamic environment fosters continuous innovation in material science and digital health integration to maintain competitive advantage and meet evolving patient expectations globally.

KEY MARKET PLAYERS

Companies playing a promising role in the global prosthetics market profiled in this report are

- CBPE Capital LLP (Blatchford Limited)

- Coapt LLC

- Colfax Corporation (DJO, LLC)

- Ossur (College Park Industries)

- Mobius Bionics LLC

- Motorica LLC

- Ottobock SE & Co KGaA

- Naked Prosthetics

- Blatchford Products Ltd

- Ottobock SE & Co. KGaA

- Protunix

- Steeper Group

TOP PLAYERS IN THE MARKET

- Össur hf stands as a global leader in non-invasive orthopedics, specializing in prosthetic limbs and bracing solutions. The company delivers advanced bionic knees and myoelectric hands that utilize sensor technology to mimic natural human movement. Össur recently strengthened its market position by launching next-generation microprocessor-controlled legs that offer enhanced stability for active users. Their strategic focus includes expanding direct patient care clinics worldwide to improve access and service quality. The firm invests heavily in research and development to integrate artificial intelligence into device algorithms for better gait adaptation. By acquiring smaller innovative startups and forming partnerships with rehabilitation centers, Össur ensures continuous technological leadership. These initiatives demonstrate their commitment to restoring mobility and independence for amputees through cutting-edge engineering and comprehensive care models globally.

- Ottobock SE & Co KGaA operates as a premier German manufacturer renowned for high-quality prosthetic components and digital health solutions. The company provides a vast portfolio ranging from mechanical joints to sophisticated bionic hands with intuitive grip patterns. Ottobock has recently expanded its global footprint by opening new production facilities and innovation hubs to accelerate product development. They actively collaborate with sports organizations to develop high-performance limbs for Paralympic athletes, which drives brand visibility and credibility. The firm leverages digital platforms to offer remote tuning and monitoring services for prosthetic users, enhancing long term satisfaction. Their commitment to sustainability involves using recyclable materials in manufacturing processes to reduce environmental impact. Through strategic acquisitions and continuous investment in neural interface technologies, Ottobock maintains its reputation as a pioneer in restoring human mobility and setting industry standards worldwide.

- Blatchford Products Ltd functions as a leading British engineering company dedicated to designing life-changing prosthetic limbs and orthotic devices. The organization distinguishes itself through proprietary hydraulic ankle systems that allow users to walk confidently on uneven terrain and slopes. Blatchford recently invested in advanced manufacturing technologies, including 3D printing, to customize sockets and reduce delivery times significantly. Their strategy focuses on expanding clinical services in emerging markets to reach underserved populations with high-quality care. The company partners with military veteran groups to provide specialized trauma care and rehabilitation support for injured service members. They prioritize user feedback to drive iterative design improvements that enhance comfort and functionality daily. By combining engineering excellence with compassionate patient care, Blatchford continues to empower amputees to lead active and fulfilling lives while solidifying its presence in the global prosthetics sector.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the prosthetics market primarily employ strategic acquisitions of innovative startups to rapidly integrate advanced technologies like artificial intelligence and neural interfaces into their product portfolios. Companies invest heavily in research and development to create lighter, more durable materials and intuitive control systems that mimic natural limb movement effectively. Expanding direct-to-patient clinical networks allows firms to control the entire care journey from fitting to long term maintenance and build strong brand loyalty. Major participants form strategic partnerships with hospitals and rehabilitation centers to secure referral streams and offer comprehensive training programs for clinicians and users. Developing customized solutions through 3D scanning and printing technologies enables providers to offer personalized fits that improve comfort and reduce rejection rates significantly. Providers also focus on digital health integration by offering apps for remote device tuning and performance tracking to enhance user experience. These collective strategies aim to drive technological leadership, expand market reach, and improve patient outcomes in the evolving global prosthetics landscape.

MARKET SEGMENTATION

This research report on the global prosthetics market has been segmented and sub-segmented based on the product type, technology, end-user, and region.

By Product Type

- Upper Extremity Prosthetics

- Hand Prosthetics

- Elbow Prosthetics

- Shoulder Prosthetics

- Lower Extremity Prosthetics

- Foot & Ankle Prosthetics

- Knee Prosthetics

- Hip Prosthetics

- Liners

- Sockets

By Technology

- Body Powered

- Electrically Powered

- Hybrid Prosthetics

By End-User

- Prosthetic Clinics

- Hospitals

- Rehabilitation Centers

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. Which regions lead the global prosthetics market?

North America dominates the global prosthetics market, driven by advanced healthcare infrastructure, technology adoption, and government initiatives for amputee care

2. What are the key segments in the global prosthetics market?

Segments include powered prosthetics, upper and lower limb prosthetics, robotic prosthetics, and clinics or hospitals as end users in the global prosthetics market

3. How do technological advancements impact the global prosthetics market?

AI, robotics, and sensor integration improve prosthetic functionality and user experience, accelerating growth in the global prosthetics market

4. How does diabetes prevalence affect the global prosthetics market?

Rising diabetes-related amputations increase demand for prosthetic devices, significantly driving growth in the global prosthetics market

5. What role do hospitals play in the global prosthetics market?

Hospitals hold a major market share due to post-surgical prosthetic fittings and integration of prosthetics into rehabilitation in the global prosthetics market

6. How are rehabilitation centers influencing the global prosthetics market?

Rehabilitation centers are the fastest-growing end users, offering customized therapy and prosthetic adjustments in the global prosthetics market

7. What is the importance of myoelectric prosthetics in the global prosthetics market?

Myoelectric prosthetics provide advanced motor control and improved dexterity, fueling adoption in the global prosthetics market

8. How does 3D printing technology influence the global prosthetics market?

3D printing enables personalized, cost-effective prosthetics, expanding potential applications in the global prosthetics market

9. What challenges does the global prosthetics market face?

High costs, regulatory approval delays, and lack of awareness in emerging markets challenge growth in the global prosthetics market

10. How does aging population impact the global prosthetics market?

An aging population with mobility impairments increases demand for prosthetics in the global prosthetics market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com