- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

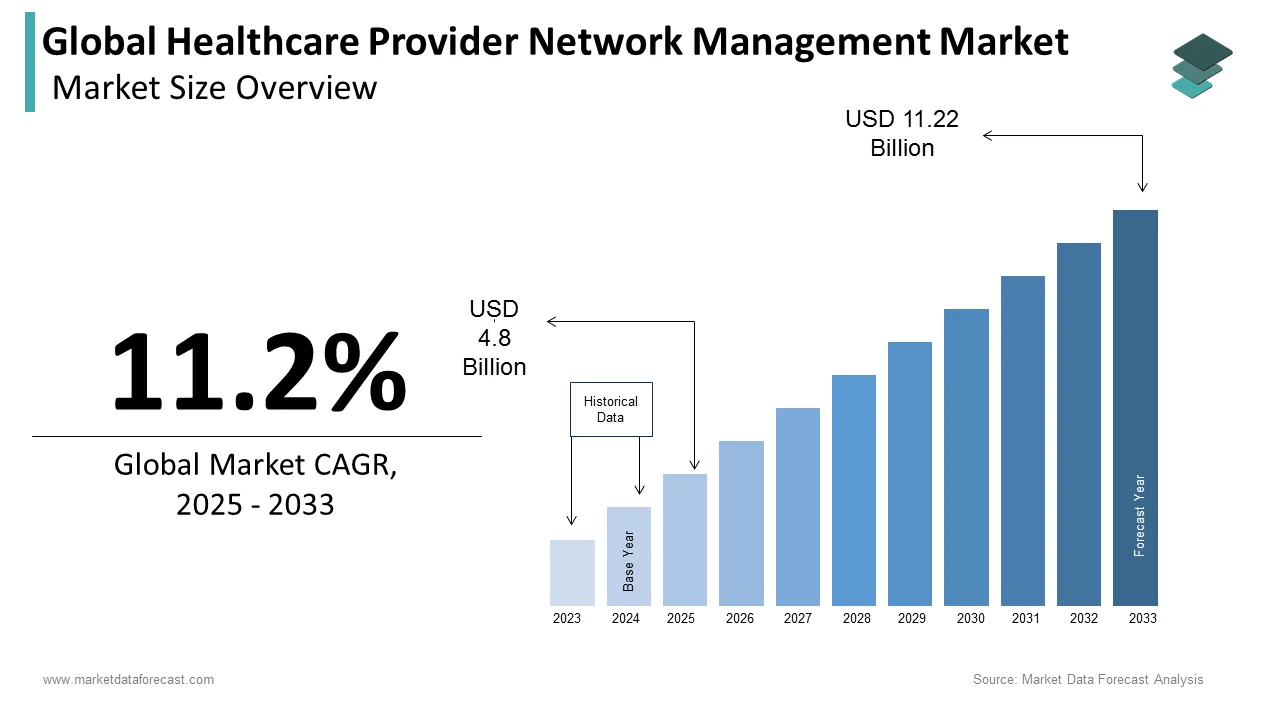

Market Size, 2025

$4.8 BnMarket Estimate, 2026

$5.34 BnMarket Forecast, 2034

$12.48 BnCAGR, 2026–2034

11.2%Global Healthcare Provider Network Management Market Report Summary

The global healthcare provider network management market is witnessing substantial growth due to increasing healthcare digitization, rising demand for efficient provider coordination, and growing emphasis on cost optimization and value-based care models. Healthcare organizations are increasingly adopting provider network management solutions to streamline administrative workflows, improve patient access, enhance claims management, and strengthen payer-provider collaboration. The expansion of cloud-based healthcare platforms, AI-driven analytics, and interoperability solutions is further accelerating market growth globally.

Key Market Trends

- Rising adoption of cloud-based provider network management platforms.

- Increasing focus on value-based care and coordinated healthcare delivery models.

- Growing demand for AI-driven analytics and provider performance monitoring solutions.

- Expansion of outsourced healthcare administrative services to improve operational efficiency.

- Strengthening integration of interoperability and healthcare data exchange systems.

Segmental Insights

- Based on component, the platforms segment dominated the global healthcare provider network management market in 2025 by accounting for 58.5% market share, driven by rising adoption of centralized provider data management and workflow automation systems.

- Based on outsourcing services, the outsourcing services segment is anticipated to witness the fastest growth, registering a CAGR of 16.2% from 2026 to 2034, supported by increasing demand for cost-effective healthcare administration and specialized operational support services.

Regional Insights

The global healthcare provider network management market is witnessing strong expansion across major regions, supported by healthcare modernization initiatives, increasing digital transformation, and growing investments in healthcare IT infrastructure.

- North America remained the leading regional market in 2025 with 43.7% share, driven by advanced healthcare IT adoption, large payer networks, and strong emphasis on value-based care systems.

- Europe held the second-largest position with 28.5% share in 2025, supported by coordinated healthcare systems, strong regulatory frameworks, and increasing digital health investments.

- Asia-Pacific is experiencing significant growth due to rapid healthcare digitization, expanding healthcare infrastructure, and increasing adoption of digital health platforms across emerging economies.

Competitive Landscape

The global healthcare provider network management market is characterized by strong competition among healthcare IT companies, business process outsourcing firms, and analytics solution providers focusing on operational efficiency and network optimization. Market players are emphasizing AI-driven analytics, automation capabilities, and cloud-enabled management platforms to strengthen market positioning. Strategic collaborations, acquisitions, and investments in healthcare interoperability and data management technologies are shaping competitive dynamics across the market.

Prominent companies operating in the global healthcare provider network management market include Infosys BPO, Ltd., McKesson Corporation, Mphasis Limited, Aldera, Inc., Ayasdi, Inc., Genpact Limited, Optum, Inc., Vestica Healthcare, LLC (A Skygen USA Company), Syntel, Inc., and TriZetto Corporation (A Cognizant Company).

Global Healthcare Provider Network Management Market Size

The global healthcare provider network management market was worth US$ 4.8 billion in 2025 and is anticipated to reach a valuation of US$ 12.48 billion by 2034 from US$ 5.34 billion in 2026, and it is predicted to register a CAGR of 11.2% during the forecast period 2026 to 2034.

Healthcare provider network management (PNM) is the strategic orchestration of clinical professionals, facilities, and administrative infrastructures to enable coordinated patient care across complex healthcare ecosystems globally. This discipline has transcended basic directory functions to become essential for health system sustainability, cross-border care delivery, and value-based reimbursement models worldwide. According to the World Health Organization, global health expenditure reached 9.8 trillion United States dollars in 2021, representing approximately 10.3 percent of global gross domestic product, which amplifies the operational imperative for efficient provider network coordination. As per the Organisation for Economic Co-operation and Development, healthcare employs over 10 percent of the workforce in developed economies, creating substantial administrative complexity that network management solutions must address. The International Telecommunication Union reports that 67 percent of the global population now uses the internet, enabling digital health infrastructure, yet significant disparities persist between high-income and low-income regions. Furthermore, the World Bank indicates that physician density varies from 0.2 per 1000 population in low-income countries to 3.5 per 1000 in high-income nations, highlighting the workforce distribution challenges that sophisticated network management platforms must accommodate. These foundational realities underscore the intricate regulatory, technological, and demographic forces shaping provider network management adoption across diverse global healthcare architectures.

MARKET DRIVERS

Escalating Global Patient Mobility: Creating Cross-Border Network Coordination Imperatives

Increasing international patient movement for specialized treatments generates substantial demand for advanced provider network management capabilities that support seamless care continuity across geographical boundaries, which drives the growth of the healthcare provider network management market. According to research, the global medical tourism market is projected to exceed 273 billion United States dollars by 2032, advancing at an annual growth rate of roughly 10% to 12%, reflecting rising patient expectations for specialized care across borders. As per the World Health Organization, cross-border health service delivery requires heightened subregional coordination, as global human mobility has expanded significantly, demanding collaborative frameworks to manage patients seeking specialized treatments outside their home nations. This mobility pattern necessitates robust network verification, credentialing synchronization, and quality monitoring capabilities that can operate across diverse regulatory environments. Provider network management platforms that can reconcile varying national accreditation standards while maintaining real-time data exchange capabilities address critical operational gaps for international care coordination. The demographic reality of aging populations in developed economies, combined with medical expertise concentration in specific regions, further intensifies the need for networks that coordinate care across administrative and geographical boundaries. Healthcare organizations investing in interoperable network infrastructure position themselves to capture value from this expanding patient mobility trend while improving care coordination outcomes and regulatory compliance across multiple jurisdictions globally.

Accelerating Artificial Intelligence Deployment in Global Healthcare Operations

The strategic integration of artificial intelligence technologies into healthcare delivery systems is happening worldwide and is propelling the expansion of the healthcare provider network management market. This shift creates a powerful demand for intelligent provider network management solutions. According to the World Health Organization, artificial intelligence can alleviate healthcare workforce shortages by automating administrative tasks, optimizing resource allocation, and supporting clinical decision-making, particularly in resource-constrained settings. Machine learning algorithms enable predictive analytics for network adequacy assessment, automated credential verification, and intelligent referral routing based on historical utilization patterns, quality metrics, and patient outcomes across diverse healthcare environments. Global health initiatives emphasizing secondary use of health data for research and innovation provide additional impetus for intelligent network management solutions that can anonymize aggregate data while preserving analytical utility. Healthcare systems facing budget constraints and workforce challenges increasingly value AI capabilities that enhance operational efficiency without proportional increases in administrative staffing. Organizations that develop explainable artificial intelligence features compliant with international regulatory expectations for algorithmic transparency will capture first-mover advantages in emerging markets. The convergence of policy support, technological capability, and operational necessity creates sustained demand for AI-enhanced network management platforms that deliver measurable improvements in care coordination efficiency and patient access across diverse global healthcare environments.

MARKET RESTRAINTS

Persistent Global Interoperability Fragmentation Across Diverse Health Infrastructures

The absence of uniform technical standards and semantic harmonization across international healthcare systems significantly constrains the growth of the global healthcare provider network management market. According to the World Health Organization, while more than 70% of countries have implemented national digital health strategies, many of these frameworks lack financial commitments and standardized data exchange protocols, creating substantial integration challenges for network management platforms. This technological heterogeneity forces solutions to maintain multiple integration pathways, increasing implementation complexity and operational costs across different regions. As per global health infrastructure metrics, wide disparities in foundational utilities persist, with primary health facilities in low-income settings lacking reliable electricity or stable local networks, illustrating the severely fragmented landscape that international network management vendors must accommodate. Divergent national priorities regarding health terminology, data architecture, and digital infrastructure create conceptual differences that translate into practical implementation barriers for global network management solutions. Furthermore, regulatory fragmentation regarding data sovereignty, cross-border data transfer restrictions, and varying security frameworks complicates interoperability efforts across jurisdictions. Until global health systems achieve greater technical and semantic alignment, provider network management solutions will face elevated customization requirements, prolonged deployment timelines, and uncertain return on investment calculations. These barriers particularly impact healthcare organizations in emerging markets, with limited technological resources dampening adoption momentum across the global landscape.

Stringent and Divergent Global Data Privacy Regulations Creating Implementation Complexity

Different jurisdictions have established rigorous and varied data protection requirements, which hamper the expansion of the global healthcare provider network management market. These regulations introduce substantial compliance burdens that restrain the deployment of global provider network management solutions. According to the United Nations Conference on Trade and Development, 137 countries have enacted data protection legislation, yet significant variations exist in scope and healthcare-specific provisions, creating compliance complexity for international network management operations. Healthcare provider networks inherently process sensitive personal health information, requiring meticulous consent management, access controls, and audit capabilities that increase solution complexity across different regulatory environments. As per the International Telecommunication Union, organizations operating across multiple jurisdictions must navigate overlapping obligations, including regional data protection frameworks, national health data laws, and sector-specific directives, which complicates network management architecture design globally. The requirement for patient-centric transparency with varying consent mechanisms further challenges traditional network management workflows that historically relied on institutional data sharing agreements in certain regions. These regulatory complexities elevate implementation costs, extend validation cycles, and introduce ongoing compliance monitoring requirements that particularly burden small and medium-sized healthcare providers in emerging markets. The administrative overhead associated with compliant network management will continue to restrain market penetration, especially in regions with limited legal and technical expertise. This barrier will persist until global regulatory frameworks achieve greater harmonization or provide clearer implementation guidance for cross-border health data exchange.

MARKET OPPORTUNITIES

Expansion of Cloud Native Architectures Enabling Scalable Global Network Solutions

The migration toward cloud-based delivery models offers substantial growth opportunities for PNM platforms across global healthcare systems, a shift likely to promote the growth of the healthcare provider network management market. According to sources, global cloud infrastructure investment in healthcare exceeded 28 billion United States dollars in 2023, with high annual growth rates in emerging markets, driving scalable global network deployment. Cloud native architectures enable rapid deployment, seamless integration across diverse healthcare environments, and scalable performance that accommodates growing provider networks without proportional infrastructure investments globally. As per the World Health Organization, healthcare organizations particularly value cloud platforms that support multi-tenant architectures, enabling shared services across integrated care systems while maintaining data sovereignty requirements across different jurisdictions. This budget reallocation creates favorable conditions for cloud-based network management solutions that offer reduced total cost of ownership, enhanced disaster recovery capabilities, and simplified regulatory compliance management across diverse regulatory environments. The global emphasis on federated architecture principles to preserve privacy while enabling distributed access aligns with cloud delivery models that can reconcile these objectives across different national frameworks. Organizations developing cloud-native network management solutions with built-in interoperability standards will capture significant market share. These platforms offer automated compliance monitoring and elastic scaling capabilities to meet the flexible, scalable, and cost-effective demands of worldwide digital health transformations.

Growth of Value-Based Care Models Requiring Sophisticated Global Network Analytics

The transition from fee-for-service reimbursement to value-based payment arrangements across healthcare systems worldwide creates compelling prospects for advanced PNM solutions equipped with robust analytics capabilities, which is expected to boost the expansion of the global healthcare provider network management market. According to global health system reviews, value-based care initiatives are primarily in early adoption stages within high-income nations, requiring advanced provider tracking and performance analytics to gradually transition from volume to value. Network management platforms that can aggregate clinical, financial, and patient experience data to generate actionable insights enable healthcare organizations to optimize network composition, negotiate favorable contracts, and demonstrate value to payers and regulators globally. As per the Organisation for Economic Co-operation and Development, artificial intelligence can improve care quality by supporting personalised medicine, enabling earlier detection of diseases, and facilitating real-time patient monitoring across different healthcare environments. Solutions that support risk stratification, performance benchmarking, and shared savings calculations are essential for successful value-based contracting in emerging and developed markets alike. Regions with higher digital readiness provide ideal early adoption environments for value-based network analytics, while emerging markets represent significant growth potential as digital infrastructure matures globally. Furthermore, global health initiatives facilitating secondary data use for health system improvement create opportunities for network management platforms to contribute anonymized aggregate insights that inform policy development and quality improvement initiatives worldwide.

MARKET CHALLENGES

Reconciling Diverse Global Regulatory Requirements Within Unified Platforms

The multiplicity of healthcare regulations, data protection laws, and reimbursement frameworks across nations worldwide is a formidable challenge for PNM solution providers operating within the global healthcare provider network management market. According to the World Health Organization, stakeholders warn that overlapping frameworks, including regional data protection regulations, medical device directives, and artificial intelligence governance, create compliance uncertainty and inconsistent national interpretations across different jurisdictions. Each country maintains distinct requirements for provider credentialing, patient consent documentation, data retention periods, and breach notification protocols, which network management platforms must accommodate without compromising system integrity globally. As per the International Telecommunication Union, solution providers face the dual challenge of maintaining regulatory compliance across jurisdictions while delivering consistent user experiences and interoperable functionality across diverse technological environments. The requirement to support multiple languages, clinical terminologies, and coding systems further increases development complexity and maintenance overhead for global platforms. Organizations serving international healthcare systems must invest substantially in legal expertise, regulatory monitoring, and configurable architecture to navigate this fragmented global landscape. Smaller solution providers may struggle to achieve the scale necessary for multi-country compliance, potentially limiting innovation and competition in emerging markets. The regulatory reconciliation challenge will continue to elevate implementation risks and constrain market expansion, particularly for organizations targeting cross-border healthcare delivery models. This will persist until global health policy achieves greater harmonization or provides clearer safe harbor provisions for compliant network management.

Addressing Global Workforce Digital Competency Gaps Across Healthcare Systems

The uneven distribution of digital skills among healthcare professionals throughout the world creates significant adoption barriers for sophisticated PNM solutions across different regions within the healthcare provider network management market. According to the World Health Organization, developing and retaining digital health talent in the healthcare sector requires scaling global education and training programmes, talent attraction schemes, and reskilling initiatives to strengthen joint health and technology competences worldwide. This competency gap manifests in resistance to new workflows, difficulties in utilizing advanced analytics features, and challenges in maintaining data quality within network management platforms across diverse cultural and educational contexts. As per the International Telecommunication Union, the proportion of individuals with basic or above basic digital skills ranges significantly across global regions, highlighting the training burden that solution providers must address in different markets. Network management platforms that assume high levels of digital literacy may experience low utilization rates or configuration errors that compromise data integrity and operational effectiveness in emerging markets. Furthermore, the migration of healthcare professionals across borders for employment purposes introduces additional complexity as practitioners trained in one national system encounter different network management interfaces and workflows in another region. Solution providers must invest in intuitive user interfaces, comprehensive training programmes, and multilingual support resources to overcome these competency barriers globally. The absence of standardized digital competency frameworks for healthcare professionals across different regions further complicates adoption strategies worldwide.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 11.2% |

| Segments Covered | By Component and Region. |

|

Various Analyses Covered | Global, Regional, and country-level analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Infosys BPO, Ltd. (India), McKesson Corporation (U.S.), Mphasis Limited (India), Aldera, Inc. (U.S.), Ayasdi, Inc. (U.S.), Genpact Limited (U.S.), Optum, Inc. (U.S.), Vestica Healthcare, LLC (A Skygen USA Company) (U.S.), Syntel, Inc. (U.S.) and TriZetto Corporation (A cognizant company) (U.S.)., and Others. |

SEGMENTAL ANALYSIS

By Component Insights

The Platforms component segment maintained dominance in the global market by accounting for a 58.5% share in 2025. This segment’s dominance was driven by healthcare organizations prioritizing automated credentialing verification, contract management, and provider data synchronization to address escalating administrative complexity. As per the World Health Organization, global health expenditure reached 9.8 trillion United States dollars in 2021, creating operational imperatives for efficient provider coordination that manual processes cannot satisfy. The platforms segment benefits from regulatory mandates demanding real-time data accuracy, interoperability, and compliance reporting, which legacy systems struggle to deliver. Healthcare payers and integrated delivery networks, particularly in North America and Europe, invest substantially in these platforms to ensure adherence to evolving standards while reducing operational burden. The integration of artificial intelligence and machine learning within network management platforms further enhances predictive analytics capabilities, enabling proactive network optimization and risk mitigation across diverse care settings. Organizations leveraging advanced platforms achieve measurable improvements in provider onboarding timelines, data integrity scores, and operational efficiency metrics. The sustained investment in digital infrastructure, coupled with the imperative for scalable solutions that accommodate growing provider networks, ensures the platforms segment maintains its market leadership position throughout the forecast period as healthcare systems worldwide pursue value-based care models requiring sophisticated network oversight capabilities.

By Outsourcing Services Insights

On the other hand, the outsourcing services segment is predicted to witness the highest CAGR of 16.2% from 2026 to 2034 due to increasing healthcare organization preference to delegate non-core network management functions to specialized vendors to enhance operational efficiency and access expert capabilities without expanding internal staffing. According to ITU Global Telecommunication & ICT Infrastructure Focus, commercial healthcare information technology spending exceeded 380 billion United States dollars in 2023, with outsourcing services capturing an increasing allocation as organizations navigate complex regulatory environments. The outsourcing segment encompasses critical activities, including provider credentialing verification, contract administration, data migration, and ongoing technical support, which are essential for maximizing return on technology investments while controlling operational costs. Growing regulatory requirements around data security, interoperability, and reporting further amplify demand for compliance-focused managed services that provide continuous monitoring and optimization. Organizations operating across multiple jurisdictions particularly value outsourced services that deliver specialized expertise in regional regulatory frameworks without requiring extensive internal legal and technical resources. The services segment also benefits from rising adoption of cloud-based delivery models, which require specialized migration, integration, and maintenance expertise that external vendors can provide more cost-effectively. Healthcare systems worldwide are aggressively pursuing digital transformation initiatives. In this environment, strategic partnerships between platform vendors and service providers create synergistic value propositions that accelerate market penetration and customer retention across diverse geographical and operational contexts.

REGIONAL ANALYSIS

North America Healthcare Provider Network Management Market Analysis

North America remained in the lead by capturing a 43.7% share of the global Healthcare Provider Network Management Market in 2025. This leading position was attributed to mature private insurance infrastructure, a complex regulatory environment, and substantial healthcare expenditure that necessitates sophisticated network management capabilities across diverse provider types. As per the Centers for Medicare and Medicaid Services, the United States national health expenditure reached 4.3 trillion United States dollars in 2021, creating operational imperatives for efficient provider coordination and cost containment that drive platform adoption. The North American market benefits from early adoption of value-based care models, which require granular provider performance tracking, network adequacy assessment, and quality metric reporting across integrated delivery networks. Federal initiatives, including the 21st Century Cures Act and information blocking rules, further compel healthcare organizations to invest in interoperable network management platforms that support real-time data exchange. The concentration of major health insurers and technology vendors within the region generates sustained demand for enterprise-grade solutions that scale across diverse geographical and operational contexts. Organizations operating within this market prioritize solutions that support automated credentialing, compliance monitoring, and predictive analytics to navigate the intricate regulatory landscape while improving care coordination outcomes. The continued evolution of payment models, coupled with technological innovation, ensures North America remains the primary growth engine for the global Healthcare Provider Network Management Market throughout the forecast horizon.

Europe Healthcare Provider Network Management Market Analysis

Europe occupied the second position within the global Healthcare Provider Network Management Market and held a 28.5% share in 2025. This growth of the European market was supported by comprehensive digital health policies and substantial public healthcare investment across member states. According to the European Commission, the European Health Data Space framework establishes common standards for electronic health data exchange, enabling seamless integration of network management platforms across diverse care settings throughout the region. As per the Organisation for Economic Co-operation and Development, healthcare expenditure represented 10.4 percent of European Union gross domestic product in 2022, creating operational pressures that sophisticated network management solutions can address through improved coordination efficiency. The European market benefits from national digital health strategies in countries like Germany, France, and the Nordic nations that mandate interoperable provider directories and standardized credentialing processes. Organizations operating within Europe prioritize solutions that support multi-stakeholder coordination, including public health insurers, private providers, and integrated care systems, while maintaining strict compliance with General Data Protection Regulation requirements. The region's emphasis on cross-border care coordination and population health management further amplifies demand for analytics-enabled network tools that facilitate coordinated care delivery across geographical boundaries. Europe's regulatory framework, encouraging innovation while ensuring data protection, creates a balanced environment for network management solution adoption across diverse healthcare organizational models and national contexts.

Asia Pacific Healthcare Provider Network Management Market Analysis

Asia Pacific experiences significant growth within the global Healthcare Provider Network Management Market due to rapid digital health adoption and expanding healthcare infrastructure across emerging economies. According to the World Health Organization, the Asia Pacific region accounts for over 60 percent of the global population, creating substantial demand for scalable provider network management solutions that can accommodate diverse healthcare delivery models. As per the International Telecommunication Union, internet penetration in the Asia-Pacific region reached 66% in 2023, establishing the digital health infrastructure development required to expand advanced network coordination capabilities across urban and rural settings. The Asia Pacific market benefits from government initiatives in countries like India, China, and Singapore that allocate significant resources toward interoperable health information systems and standardized provider data management protocols. Organizations operating within this region prioritize solutions that accommodate varying levels of technological maturity while supporting national interoperability standards and regulatory requirements. The focus on expanding healthcare access and reducing disparities further amplifies demand for network analytics that optimize provider distribution and care pathway efficiency across diverse geographical contexts. Asia Pacific's ongoing healthcare system transformation, coupled with increasing private sector investment, creates sustained opportunities for innovative network management solutions that enhance care coordination and system resilience across emerging and developed markets within the region.

Latin America Healthcare Provider Network Management Market Analysis

Latin America is an emerging player within the global Healthcare Provider Network Management Market, owing to healthcare system modernization initiatives and increasing digital health adoption across the region. According to the Pan American Health Organization, several Latin American countries have initiated national digital health strategies that allocate funding toward interoperable provider directories and standardized credentialing processes to improve care coordination efficiency. As per the World Bank and OECD joint indicators, healthcare expenditure in Latin America and the Caribbean averaged roughly 6.8% of gross domestic product, creating operational imperatives for efficient provider network management that can optimize resource allocation across public and private systems. The Latin American market benefits from growing private insurance penetration and expanding integrated delivery networks that require sophisticated platform capabilities for provider onboarding, contract management, and performance monitoring. Organizations operating within this region prioritize solutions that accommodate diverse regulatory environments while supporting multilingual interfaces and varying levels of technological infrastructure. The focus on improving healthcare access in rural and underserved communities further amplifies demand for cloud-based network management tools that enable remote provider coordination and telehealth integration. Latin America's ongoing healthcare reforms, coupled with increasing technology investment, create growth opportunities for innovative network management solutions that enhance care coordination and system efficiency across diverse national contexts within the region.

Middle East and Africa Healthcare Provider Network Management Market Analysis

The Middle East and Africa region is predicted to expand notably in the global Healthcare Provider Network Management Market from 2026 to 2034 due to strategic healthcare investments and digital transformation initiatives across select markets. According to the World Health Organization, several countries in the Middle East, including the United Arab Emirates, Saudi Arabia, and Qatar, have launched comprehensive national health strategies that prioritize digital health infrastructure and interoperable provider network capabilities. As per the International Telecommunication Union, active mobile broadband penetration expanded to roughly 44% across the African region alongside stronger adoption in Arab States, creating a developing digital health infrastructure baseline that helps vendors scale network management options. The Middle East and Africa market benefits from government-led healthcare modernization programs that allocate substantial resources toward electronic health record systems and standardized provider data exchange protocols. Organizations operating within this region prioritize solutions that accommodate varying levels of technological maturity while supporting multilingual interfaces and diverse regulatory frameworks across national boundaries. The focus on medical tourism development and regional healthcare hub creation further amplifies demand for sophisticated network management tools that enable cross-border provider coordination and quality assurance. The Middle East and Africa's strategic healthcare investments, coupled with increasing private sector participation, create emerging opportunities for innovative network management solutions that enhance care coordination and system resilience across diverse national contexts within the region.

COMPETITIVE LANDSCAPE

The Healthcare Provider Network Management Market exhibits moderate consolidation with several established technology firms and healthcare services organizations competing for global market share across diverse regions. Competition centers on solution comprehensiveness, interoperability capabilities, regulatory compliance support, and customer success outcomes rather than price alone in international contexts. Differentiation emerges through artificial intelligence integration, cloud deployment flexibility, and specialized expertise in value-based care network optimization across varying healthcare system architectures. Market participants increasingly pursue strategic partnerships to expand geographical coverage and enhance solution portfolios through complementary technology acquisitions targeting emerging markets. The competitive environment rewards organizations that demonstrate measurable improvements in provider onboarding timelines, data accuracy scores, and operational efficiency metrics across diverse cultural and regulatory environments. Customer retention depends on continuous innovation, responsive support, and adaptability to evolving regulatory requirements across multiple international healthcare systems. Emerging vendors focus on niche capabilities such as specialty network management or regional regulatory expertise to establish footholds within specific market segments across global contexts. The overall competitive dynamic encourages technological advancement and customer-centric solution design that enhances care coordination and system efficiency across the worldwide healthcare ecosystem while addressing diverse stakeholder needs.

KEY MARKET PLAYERS

Some of the key players in the healthcare provider network management market are

- Infosys BPO, Ltd. (India)

- McKesson Corporation (U.S.)

- Mphasis Limited (India)

- Aldera, Inc. (U.S.)

- Ayasdi, Inc. (U.S.)

- Genpact Limited (U.S.)

- Optum, Inc. (U.S.)

- Vestica Healthcare, LLC (A Skygen USA Company) (U.S.)

- Syntel, Inc. (U.S.)

- TriZetto Corporation (A Cognizant Company) (U.S.)

TOP PLAYERS IN THE MARKET

- Optum Inc maintains a prominent position within the Healthcare Provider Network Management Market through its comprehensive portfolio of data analytics, provider engagement, and network optimization solutions. The organization leverages its extensive health services ecosystem to deliver integrated platforms that support credentialing verification, contract management, and performance monitoring across diverse payer and provider environments globally. The company's commitment to interoperability standards and regulatory compliance enables healthcare organizations to navigate complex operational requirements while improving care coordination outcomes across multiple jurisdictions. Optum's collaborative approach with health plans, hospital systems, and physician groups facilitates scalable network management solutions that adapt to evolving market dynamics and stakeholder needs worldwide.

- Infosys Limited contributes significantly to the Healthcare Provider Network Management Market through its specialized healthcare consulting services and technology implementation expertise, serving global clients. The organization partners with international health systems to design, deploy, and optimize network management platforms that enhance operational efficiency and regulatory compliance across diverse geographical contexts. The company's focus on cloud native architectures and agile development methodologies enables rapid deployment of network management solutions that scale across diverse organizational and cultural contexts. Infosys emphasizes client-centric innovation through dedicated healthcare practice teams that deliver tailored solutions addressing specific network optimization challenges and strategic objectives for international healthcare organizations.

- McKesson Corporation plays a vital role in the Healthcare Provider Network Management Market through its integrated technology platforms and supply chain expertise that support provider network coordination globally. The organization delivers comprehensive solutions for provider enrollment, credentialing, and performance analytics that enable health plans and delivery systems to optimize network composition and care delivery outcomes across multiple regions. The company's commitment to regulatory compliance and quality improvement facilitates trusted network management solutions that support value-based care initiatives and population health management objectives worldwide. McKesson leverages its extensive healthcare ecosystem to deliver scalable platforms that adapt to evolving market requirements and stakeholder expectations across diverse care settings and geographical boundaries.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Leading participants in the Healthcare Provider Network Management Market prioritize strategic partnerships to expand solution capabilities and geographical reach across diverse healthcare environments. Organizations frequently pursue acquisitions of specialized technology firms to enhance artificial intelligence analytics and interoperability features within their platforms for global deployment. Cloud native architecture adoption represents a common strategic focus, enabling scalable deployment and seamless integration across diverse healthcare environments worldwide. Investment in regulatory compliance capabilities ensures solutions adapt to evolving data protection and interoperability requirements across multiple international jurisdictions. Customer-centric innovation through dedicated healthcare practice teams facilitates tailored solutions addressing specific network optimization challenges in different regional contexts. Emphasis on outcome-based pricing models aligns vendor incentives with client success metrics, enhancing long-term partnership value across global markets. Continuous research and development investments drive technological differentiation through predictive analytics, automated workflows, and real-time performance monitoring capabilities that address diverse healthcare system needs.

MARKET SEGMENTATION

This research report on the global healthcare provider network management market has been segmented and sub-segmented based on the component, and region.

By Component

- Services

- Internal Services

- Outsourcing Services

- Platforms/Services

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa