Global IoT Microcontroller Market Size, Share, Trends, & Growth Forecast Report By Product (8 Bit, 16 Bit, and 32 Bit), Application (Industrial Automation, Smart Homes, Consumer Electronics, and Smart Wearables), and Region (North America, Europe, APAC, Latin America, Middle East and Africa) – Industry Analysis from 2026 to 2034

Global IoT Microcontroller Market Size

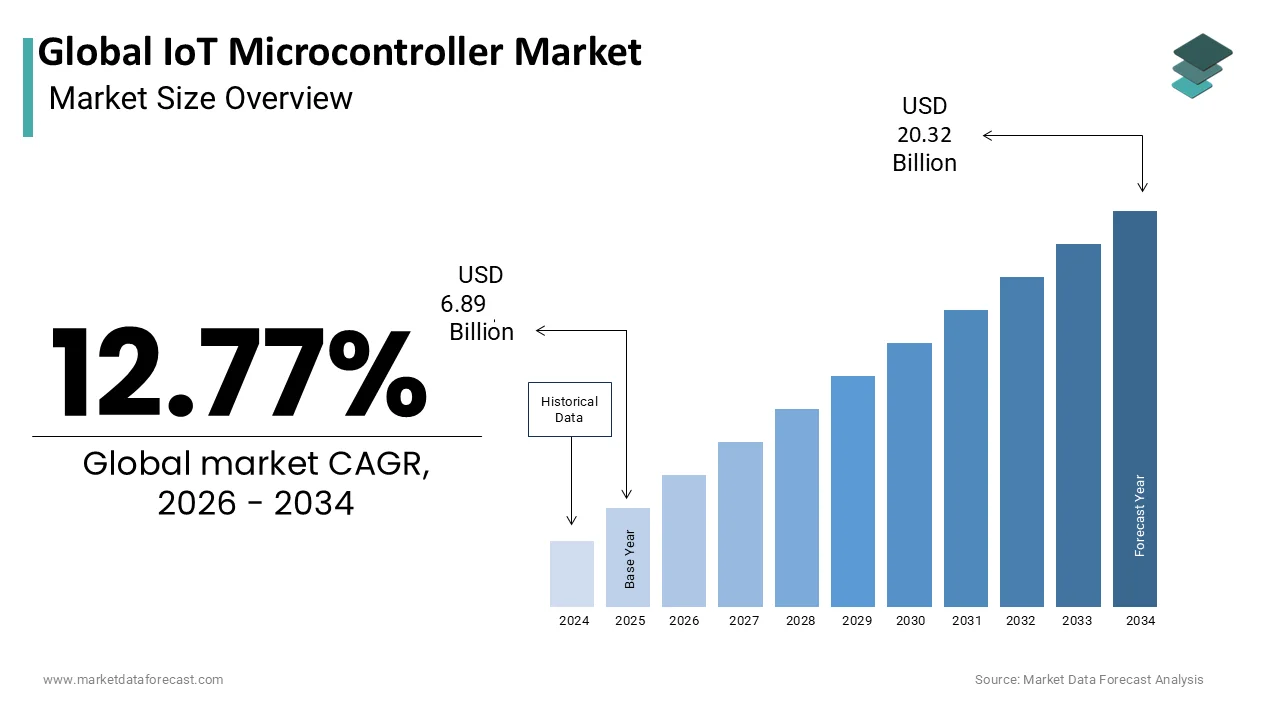

The global IoT microcontroller market size is expected to be worth USD 6.89 billion in 2025. It is expected to grow at a CAGR of 12.77% during the forecast period and reach a value of USD 20.32 billion by 2034 from USD 7.77 billion in 2026.

The IoT microcontroller, often embedded with integrated memory, input/output peripherals, and connectivity modules, enables smart, real-time data processing at the edge of connected networks. They are widely used across consumer electronics, industrial automation, healthcare wearables, automotive systems, and smart infrastructure. According to the International Telecommunication Union (ITU), global IoT device connections are expected to surpass 50 billion by 2030, which reflects the growing integration of microcontroller-driven solutions in everyday life. The demand for energy-efficient, secure, and compact computing units has surged as industries shift toward decentralized intelligence and low-latency decision-making capabilities.

MARKET DRIVERS

Surge in Smart Device Adoption Across Consumer and Industrial Sectors

One of the primary drivers of the IoT microcontroller market is the rapid proliferation of smart devices across both consumer and industrial sectors. As per the International Data Corporation (IDC), global shipments of smart home devices alone surpassed 1 billion units in 2023, which is driven by increasing demand for connected lighting, security systems, and voice-controlled appliances.

This trend is further amplified by the expansion of Industry 4.0, where manufacturing, logistics, and energy management systems rely heavily on IoT-enabled sensors and controllers. According to the World Economic Forum, over 70% of large-scale manufacturers have deployed or are piloting IoT-based monitoring and automation systems by requiring high-performance yet energy-efficient microcontrollers.

Advancements in Edge Computing and Real-Time Data Processing

Another major driver fueling the IoT microcontroller market is the growing emphasis on edge computing and real-time data processing. Traditional cloud-centric models are being supplemented with localized data analysis to reduce latency, improve efficiency, and enhance system responsiveness. According to the Institute of Electrical and Electronics Engineers (IEEE), nearly 60% of enterprise IoT deployments now incorporate some form of edge processing architecture. Microcontrollers with onboard AI accelerators and neural processing units are increasingly being used in applications such as predictive maintenance, autonomous robotics, and environmental sensing. These chips enable local decision-making without relying on continuous cloud connectivity, making them ideal for mission-critical operations. Furthermore, advancements in ultra-low-power microcontroller designs have enabled long-term deployment in remote or battery-operated environments. As noted by the European Processor Initiative, the push for sovereign semiconductor development in Europe includes significant investments in next-generation microcontrollers tailored for edge-IoT applications.

MARKET RESTRAINTS

Supply Chain Disruptions and Semiconductor Shortages

A significant restraint affecting the IoT microcontroller market is the ongoing volatility in the global semiconductor supply chain. Despite efforts to diversify production, geopolitical tensions, logistical bottlenecks, and raw material shortages continue to impact manufacturing timelines and availability. Additionally, lead times for microcontroller units (MCUs) remain extended, with many components experiencing delays exceeding 50 weeks, as reported by Susquehanna International Group in their semiconductor lead time analysis. These disruptions hinder product development cycles for OEMs and delay the rollout of new IoT products in fast-moving consumer electronics and industrial automation sectors.

Rising Complexity in Firmware and Software Integration

Another critical constraint in the IoT microcontroller market is the increasing complexity of firmware and software integration required to manage diverse applications and ensure interoperability. Modern microcontrollers must support multiple communication protocols, real-time operating systems, and security frameworks, which significantly increase development costs and time-to-market. According to the Institute of Electrical and Electronics Engineers (IEEE), over 40% of IoT project delays are attributed to software compatibility issues and firmware bugs. Additionally, as reported by the European Cybersecurity Organisation (ECSO), ensuring end-to-end security across heterogeneous IoT ecosystems remains a formidable challenge for developers using different microcontroller platforms. Furthermore, the shortage of skilled embedded systems engineers capable of managing complex codebases limits scalability.

MARKET OPPORTUNITIES

Expansion of Green and Energy-Efficient IoT Applications

Governments and private enterprises are increasingly investing in smart grids, precision farming, and climate tracking systems that rely on ultra-low-power microcontrollers to operate autonomously for extended periods. According to the International Energy Agency (IEA), smart grid investments exceeded $300 billion globally in 2023, with Europe leading in renewable energy integration and digital metering. Moreover, initiatives like the European Green Deal emphasize the need for resource-efficient digital technologies, encouraging the adoption of sustainable hardware. As reported by the Fraunhofer Institute for Integrated Circuits, several European startups are developing self-powered microcontroller units that harvest ambient energy from light or vibration sources.

Integration with Artificial Intelligence at the Edge

A major opportunity shaping the IoT microcontroller market is the increasing integration of artificial intelligence (AI) directly at the edge of IoT networks. Unlike traditional models that rely on centralized cloud processing, AI-enhanced microcontrollers enable real-time decision-making through on-chip inference, which reduces latency and bandwidth dependency. Additionally, the European Processor Initiative (EPI) is funding research into AI-optimized microcontroller architectures tailored for industrial and automotive applications.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Connected Devices

A notable challenge facing the IoT microcontroller market is the rising concern over cybersecurity vulnerabilities in connected devices. According to the European Union Agency for Cybersecurity (ENISA), over 60% of IoT-related breaches in 2023 stemmed from weak authentication mechanisms, unpatched firmware, or insufficient encryption within embedded microcontrollers. Furthermore, as reported by the European Cybersecurity Organisation (ECSO), the lack of standardized security protocols across different microcontroller platforms complicates device certification and regulatory compliance.

Rapid Technological Obsolescence and Compatibility Issues

Another significant challenge for the IoT microcontroller market is the rapid pace of technological obsolescence and the resulting compatibility challenges. According to the Semiconductor Engineering journal, the average lifecycle of an IoT microcontroller before a newer variant is released is less than three years. This rapid evolution poses difficulties for original equipment manufacturers (OEMs) designing long-term solutions in industrial and medical applications where longevity and stability are crucial. Additionally, as reported by the Institute of Electrical and Electronics Engineers (IEEE), interoperability issues between microcontroller platforms from different vendors complicate system integration and upgrades. Companies developing IoT ecosystems must navigate fragmented toolchains, inconsistent software libraries, and varying pinouts, increasing development overhead.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2026 to 2034 |

| Base Year | 2026 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | NXP Semiconductors, Renesas Electronics Corporation, Texas Instruments Incorporated, Silicon Laboratories, Infineon Technologies, Holtek |

SEGMENTAL ANALYSIS

By Product Insights

The 32-bit microcontroller segment dominated the IoT microcontroller market by accounting for 45.3% of the market share in 2025. A key driver behind this segment’s dominance is the growing adoption of 32-bit MCUs in industrial automation and automotive electronics, where precision and reliability are critical. Additionally, advancements in ultra-low-power 32-bit cores from the ARM Cortex-M series have enabled widespread deployment in battery-operated devices. According to Arm Holdings, more than 25 billion Cortex-M-based chips were shipped globally in 2023, with a significant portion dedicated to IoT applications.

The 8-bit microcontroller segment is swiftly emerging with a CAGR of 9.1% throughout the forecast period. One significant factor fueling this expansion is the increasing use of 8-bit MCUs in consumer appliances, smart meters, and home automation accessories, particularly in emerging markets where affordability is a priority. According to the International Telecommunication Union (ITU), over 300 million low-cost IoT devices were deployed across Asia-Pacific and Latin America in 2023, many utilizing 8-bit controllers for basic sensor interfacing and control functions. Moreover, companies like Microchip Technology and Renesas Electronics have introduced enhanced 8-bit MCUs featuring improved analog integration and lower power consumption, extending their applicability in edge sensing and monitoring tasks.

By Application Insights

The industrial automation segment wccounted in holding 35.4% of the IoT microcontroller market share in 2025. A primary growth driver is the accelerated adoption of Industry 4.0 technologies, including predictive maintenance, asset tracking, and real-time process optimization. Another contributing element is the integration of artificial intelligence and machine learning algorithms into factory floor equipment, which requires efficient yet compact microcontroller units. As per the European Processor Initiative (EPI), European industrial firms are investing heavily in AI-driven microcontroller modules tailored for smart manufacturing environments.

The smart wearables application segment is swiftly emerging with a CAGR of 10.3% in the coming years. One key contributing factor is the growing emphasis on personal health monitoring and remote patient care, especially post-pandemic. According to the U.S. Centers for Disease Control and Prevention (CDC), wearable health device usage increased by over 50% between 2020 and 2023, driven by chronic disease management and wellness-focused lifestyles. Additionally, the introduction of ultra-low-power microcontroller units with integrated biometric sensors has enabled longer battery life and enhanced functionality in compact form factors. Companies like STMicroelectronics and Nordic Semiconductor have launched specialized 32-bit MCUs designed for wearable applications, supporting features such as heart rate monitoring, ECG measurement, and motion detection.

REGIONAL ANALYSIS

North America was the top performer in the global IoT microcontroller market by holding 30.1% of the share in 2025. A major growth driver is the expansion of smart cities and industrial IoT deployments, particularly in the United States. According to the U.S. Department of Commerce, over 100 cities have initiated smart grid and intelligent transportation projects leveraging IoT microcontroller-based sensors and gateways. In addition, North America benefits from strong R&D investments in AI-integrated microcontrollers, supported by federal initiatives such as the CHIPS and Science Act. As per the National Institute of Standards and Technology (NIST), U.S.-based semiconductor firms accounted for over 70% of global patents filed in edge computing microcontrollers in 2023.

Europe held 22.1% of the IoT microcontroller market share in 2025. A key growth factor is the supportive regulatory environment under the European Green Deal and Digital Compass Strategy, which encourages the deployment of smart grids, energy-efficient buildings, and secure microcontroller-based infrastructure. Another contributing element is the push for indigenous semiconductor development, exemplified by the European Processor Initiative and funding programs for secure microcontroller design.

APAC IoT microcontroller market is likely to gain huge traction with a prominent CAGR in the coming years. One key growth enabler is the massive scale of consumer electronics manufacturing, particularly in smartphones, wearables, and home automation devices. Additionally, government-led initiatives such as India’s Smart Cities Mission and Indonesia’s digital transformation roadmap are accelerating the deployment of IoT infrastructure. As per the Asia IoT Business Council, A PAC is expected to maintain the highest CAGR in the global IoT microcontroller market due to expanding industrial automation and rural digitization efforts.

Latin America IoT microcontroller market is likely to have significant growth opportunities in the coming years. A major growth driver is the expansion of smart agriculture technologies, where microcontroller-powered soil sensors and irrigation systems are improving yield efficiency. Additionally, the adoption of prepaid electricity and water meters in urban centers like Mexico City and Bogotá has boosted demand for low-cost microcontrollers.

The Middle East and Africa IoT microcontroller market is substantially to grow with strategic investments in smart infrastructure and security-focused IoT applications.

A notable growth enabler is the expansion of smart city initiatives in the Gulf Cooperation Council (GCC) countries, particularly in Saudi Arabia and the UAE. According to the Dubai Smart City Authority, over $20 billion has been allocated for IoT-enabled urban infrastructure by 2030, including traffic management, surveillance, and building automation—each requiring microcontroller-based control systems.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the global IoT microcontroller market include NXP Semiconductors, Renesas Electronics Corporation, Texas Instruments Incorporated, Silicon Laboratories, Infineon Technologies, Holtek Semiconductor Inc., Nuvoton Technology Corporation, STMicroelectronics, Broadcom, Microchip Technology Inc., a nd Espressif Systems (Shanghai) Co., Ltd.,d Others.

The competition in the IoT microcontroller market is highly dynamic, driven by rapid technological evolution, increasing demand for secure and intelligent edge devices, and the need for power-efficient embedded solutions. A mix of established semiconductor giants, specialized chipmakers, and emerging startups is vying for dominance across various IoT verticals. While large players benefit from strong R&D capabilities, mature product portfolios, and extensive distribution networks, smaller firms are leveraging agility and niche innovations to carve out market space.

Differentiation strategies include performance optimization, enhanced security features, and integration of wireless communication modules. Companies are also focusing on ecosystem development, partnering with cloud service providers and software developers to offer end-to-end IoT solutions. As industries continue to adopt smart technologies, competition is intensifying not only in product design but also in scalability, interoperability, and sustainability claims. Additionally, geopolitical shifts and supply chain constraints are influencing regional manufacturing strategies, prompting firms to diversify production bases and invest in domestic foundry partnerships to ensure long-term resilience.

Top Players in the Market

STMicroelectronics

STMicroelectronics is a global leader in semiconductor solutions and plays a pivotal role in shaping the IoT microcontroller landscape. The company offers a broad portfolio of ultra-low-power MCUs tailored for smart wearables, industrial automation, and connected home devices. The company actively collaborates with cloud service providers and AI startups to enhance edge computing capabilities. Its commitment to sustainability and open innovation has strengthened its presence across diverse IoT applications, which is making it a key influencer in the global market.

NXP Semiconductors

NXP Semiconductors is a major contributor to the IoT microcontroller domain, known for its secure and scalable embedded solutions. The company’s Kinetis and LPC series of microcontrollers are widely used in automotive, industrial IoT, and smart city applications.

NXP emphasizes integration of hardware-based security and wireless connectivity into its MCU offerings, addressing growing concerns around device authentication and data integrity. NXP continues to drive advancements in secure, intelligent, and connected microcontroller systems worldwide by aligning with industry consortia and investing in R&D for next-generation architectures.

Microchip Technology

Microchip Technology is a leading provider of microcontroller solutions, particularly for cost-sensitive and low-power IoT applications. Its extensive product line includes 8-bit, 16-bit, and 32-bit MCUs designed for consumer electronics, medical devices, and smart sensors.

Microchip focuses on ease of use, offering development tools and comprehensive software ecosystems that enable rapid prototyping and deployment. Through strategic acquisitions and partnerships, the company continues to expand its footprint in both traditional and emerging IoT markets, reinforcing its position as a trusted player in the global microcontroller ecosystem.s

Top Strategies Used by Key Market Participants

Integration of Edge AI and Machine Learning Capabilities

Leading players are embedding artificial intelligence and machine learning directly into microcontroller units to enable real-time decision-making at the device level. This shift allows for local data processing without relying heavily on cloud infrastructure, improving latency, efficiency, and privacy in IoT applications.

Expansion of Secure-by-Design Microcontroller Architectures

With rising cybersecurity threats, companies are prioritizing built-in security features such as secure boot, trusted execution environments, and cryptographic accelerators. These enhancements ensure robust protection against tampering and unauthorized access, especially in mission-critical and industrial IoT deployments.

Strategic Collaborations with Cloud and Software Ecosystem Providers

To streamline development and deployment, key players are forming alliances with cloud platforms, operating system vendors, and AI startups. These partnerships help create unified toolchains and support frameworks that simplify application development, enhance interoperability, and accelerate time-to-market for IoT product developers.

RECENT HAPPENINGS IN THE MARKET

- In February 2025, STMicroelectronics launched the new STM32WBA Series, its first wireless-enabled 32-bit microcontroller family based on the Arm Cortex-M55 core, which aimed at accelerating AI-driven IoT applications while maintaining ultra-low power consumption.

- In June 2025, NXP Semiconductors announced a partnership with Google Cloud IoT, integrating its EdgeVerse platform with Google’s Vertex AI to provide developers with streamlined tools for deploying machine learning models directly on NXP-based microcontrollers.

- In September 2025, Microchip Technology introduced the PIC32CX-BZ2, a secure, Bluetooth Low Energy-enabled microcontroller designed specifically for connected home appliances and industrial sensor nodes by enhancing its footprint in entry-level IoT segments.

- In January 2025, Infineon Technologies unveiled the PSoC 64 Secure AWS Certified Microcontroller, featuring pre-integrated cloud connectivity and hardware-based security to simplify IoT device certification and deployment for enterprise customers.

- In April 2025, Renesas Electronics expanded its RA Family of 32-bit microcontrollers with new variants supporting multi-protocol connectivity and real-time processing, which area targeting smart factory and healthcare monitoring applications across North America and Europe.

MARKET SEGMENTATION

This research report on the global IoT microcontroller market has been segmented and sub-segmented based on product, application, and region.

By Product

- 8 Bit

- 32 Bit

By Application

- Industrial Automation

- Smart wearables application

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

Which region dominates the global IoT microcontroller market?

APAC had a significant share of the global IoT microcontroller market share in 2024.

What are the drivers of the global IoT microcontroller market?

Increasing demand for IoT microcontrollers in various applications is one of the key factors boosting the market growth.

What is the global IoT microcontroller market growth?

IoT microcontroller market size is estimated to be worth USD 18.02 billion by 2033, growing at a CAGR of 12.77% from 2024 to 2033.

What is the global IoT microcontroller market segmentation by component?

The global IoT microcontroller market is segmented by component into industrial automation, smart homes, consumer electronics, smartphones, wearables, smart utility, smart transportation& logistics, smart retail, and others.

Who are the key global IoT microcontroller market players?

Broadcom, Microchip Technology Inc., Espressif Systems (Shanghai) Co., Ltd, Infineon Technologies, Holtek Semiconductor Inc., Nuvoton Technology Corporation, STMicroelectronics, NXP Semiconductors, Renesas Electronics Corporation, Texas Instruments Incorporated, and Silicon Laboratories are some of the key players in the global IoT microcontroller market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com