Global Medical Device Contract Manufacturing Market Size, Share, Trends, COVID-19 Impact & Growth Analysis Report – Segmented By Device Type (Cardiovascular Devices, Drug Delivery Devices, IVD Devices, Diagnostic Imaging Devices, Orthopedic Devices, Dental Devices, Endoscopy Devices), Service, Class of Device & Region (North America, Europe, APAC, Latin America, Middle East and Africa) – Industry Analysis From 2024 to 2033

Global Medical Device Contract Manufacturing Market Summary

The global medical device contract manufacturing market was valued at USD 86.15 billion in 2024 and is projected to reach USD 188.98 billion by 2033, growing at a CAGR of 9.12%.

This market includes the outsourcing of design, development, and production of medical devices by OEMs to third-party CMOs. Key services include prototyping, regulatory support, machining, assembly, packaging, and sterilization across segments like cardiology, diagnostics, and drug delivery.

Key Market Trends & Insights

- Cardiovascular Devices held the largest share in 2024 (25.5%) due to global demand for stents, pacemakers, and implantable devices.

- Device Development & Manufacturing Services led the service segment with 65.4% market share.

- Class II Devices dominated the market with 45.8% share due to high usage volume.

- Drug Delivery Devices expected to grow at the fastest CAGR of 12.4% through 2033.

- North America led the regional market with 40.1% share in 2024; APAC is the fastest-growing region.

Market Size & Forecast

- 2024 Market Size: USD 86.15 Billion

- 2033 Projected Market Size: USD 188.98 Billion

- CAGR (2024–2033): 9.12%

- Leading Segment: Cardiovascular Devices

Global Medical Device Contract Manufacturing Market Size

The global medical device contract manufacturing market is anticipated to rise from USD 86.15 billion in 2024 to USD 188.98 billion in 2033, growing at a CAGR of 9.12%.

The medical device contract manufacturing market refers to the outsourcing of medical device design, development, and production by original equipment manufacturers (OEMs) to specialized third-party service providers. These contract manufacturing organizations (CMOs) offer a broad range of services, including prototyping, regulatory compliance support, precision machining, assembly, packaging, and sterilization across various therapeutic areas such as cardiology, orthopedics, diagnostics, and minimally invasive surgery.

This market has gained prominence due to the increasing complexity of medical devices, rising R&D costs, and the need for faster time-to-market. According to the Advanced Medical Technology Association (AdvaMed), over 70% of medical device companies in the U.S. are small or mid-sized enterprises that lack in-house manufacturing capabilities, making them highly dependent on contract manufacturers.

Besides, the global shift toward personalized and wearable medical devices further intensifies the need for agile manufacturing partners capable of handling low-volume, high-mix production.

In Europe, the implementation of the Medical Device Regulation (MDR) has significantly increased the burden of compliance, prompting many OEMs to outsource to CMOs with established quality systems and regulatory expertise. This evolving landscape positions contract manufacturing as a strategic enabler for innovation and operational efficiency in the global medical device industry.

MARKET DRIVERS

Rising Demand for Minimally Invasive and Personalized Medical Devices

Among the most influential drivers fueling the growth of the medical device contract manufacturing market is the increasing demand for minimally invasive and personalized medical devices. These advanced devices often require highly specialized manufacturing techniques, including micro-machining, laser welding, and biocompatible material processing—capabilities that many original equipment manufacturers (OEMs) do not possess in-house.

According to the World Health Organization (WHO), chronic diseases such as diabetes, cardiovascular disorders, and respiratory conditions collectively account for over 70% of global deaths annually. As a result, there is a growing preference for implantable and wearable medical devices that offer continuous monitoring and targeted treatment.

Given the intricate nature of these products, OEMs increasingly rely on experienced contract manufacturers to manage production while they focus on innovation and commercialization strategies.

MARKET RESTRAINTS

Cost-Effective Outsourcing Due to High Capital Expenditure in In-House Production

One more key driver boosting the medical device contract manufacturing market is the economic advantage of outsourcing versus investing in expensive in-house production infrastructure. This includes expenditures on cleanroom construction, automation equipment, quality assurance labs, and skilled workforce training.

Given these high entry barriers, especially for startups and small to mid-sized medical device companies, outsourcing to contract manufacturing organizations (CMOs) offers a more viable alternative.

Furthermore, leading CMOs already maintain certified facilities aligned with ISO 13485 standards and FDA Good Manufacturing Practices (GMP). This eliminates the need for OEMs to navigate complex regulatory landscapes independently. As per a 2023 survey by MedTech Dive, over 75% of new medical device entrants prefer to partner with contract manufacturers to accelerate product launches without compromising on quality or compliance.

Stringent Regulatory Requirements and Compliance Burdens

A major restraint affecting the medical device contract manufacturing market is the stringent regulatory environment governing medical device production. As per the U.S. Food and Drug Administration (FDA), all medical device manufacturers must comply with Quality System Regulation (QSR 820), which outlines detailed requirements for design controls, documentation, and process validation. Non-compliance can lead to costly delays, product recalls, or even legal action.

Apart from these, the European Union’s Medical Device Regulation (MDR), implemented in 2021, has significantly increased the burden on both OEMs and their contract manufacturing partners. According to the European Commission, a significant portion of medical device applications submitted under MDR faced rejection or required extensive revisions in the first two years following its enforcement. This has led to longer approval timelines and increased pressure on CMOs to maintain robust quality systems.

These escalating demands make it difficult for smaller CMOs to compete, limiting market expansion and forcing some players to exit the industry altogether.

Intellectual Property and Data Security Concerns

Intellectual property (IP) protection and data security concerns pose another significant challenge to the growth of the medical device contract manufacturing market. As OEMs share proprietary designs, formulations, and technical specifications with contract manufacturers, the risk of IP theft or unauthorized replication increases.

Like, according to the International Trade Administration (ITA), trade secrets and confidential information breaches have been among the top three concerns for U.S. medical device exporters when outsourcing manufacturing overseas.

Apart from these, as medical devices become increasingly digitized and connected, cybersecurity threats have intensified. A breach in manufacturing systems could compromise sensitive patient data or alter device functionality, posing serious safety risks. As per the U.S. Department of Homeland Security (DHS), over 30 medical device-related cybersecurity incidents were reported between 2020 and 2023, underscoring vulnerabilities in outsourced production environments.

To mitigate these risks, OEMs must conduct rigorous due diligence before selecting CMOs, including background checks, audits, and contractual safeguards. However, these additional steps increase transaction costs and slow down decision-making, discouraging some companies from outsourcing critical components or next-generation technologies.

MARKET OPPORTUNITES

Expansion of Wearable and Connected Medical Devices

A promising opportunity driving the medical device contract manufacturing market is the rapid growth of wearable and connected medical devices.

As per the Centers for Disease Control and Prevention (CDC), chronic disease prevalence in the U.S. alone has surged, with over 60% of adults suffering from at least one long-term health condition. This has spurred demand for remote monitoring wearables such as glucose monitors, ECG patches, and smart inhalers.

Contract manufacturers are well-positioned to capitalize on this trend by offering flexible, high-mix, low-volume production capabilities tailored to rapidly evolving wearable technology.

Moreover, CMOs with experience in fast-turn prototyping, embedded software integration, and regulatory-ready manufacturing are gaining a competitive edge in supporting OEMs through accelerated product lifecycles.

Increasing Adoption of AI and Digital Twins in Manufacturing Processes

The integration of artificial intelligence (AI) and digital twin technologies into medical device manufacturing presents a transformative opportunity for the medical device contract manufacturing market. Digital twins—virtual replicas of physical manufacturing processes—enable real-time monitoring, predictive maintenance, and process optimization, improving both efficiency and compliance.

Also, digital twin adoption in regulated industries like healthcare has grown since 2020. CMOs leveraging these technologies can provide OEMs with enhanced traceability, reduced downtime, and better control over production variability.

In addition, AI-driven analytics are being deployed to improve quality assurance. This enhances yield rates and reduces the likelihood of field failures, aligning with stricter regulatory expectations. As more OEMs seek partners capable of delivering smart, data-driven manufacturing, CMOs investing in AI and digital transformation are likely to capture a larger share of the evolving medical device outsourcing landscape.

MARKET CHALLENGES

Supply Chain Disruptions and Component Shortages

A serious challenge impacting the Medical Device Contract Manufacturing Market is the ongoing volatility in global supply chains, particularly regarding semiconductor and electronic component shortages.

Also, according to the U.S. Department of Commerce, the global semiconductor shortage has affected over 169 industries, including medical device manufacturing, where microchips are essential for diagnostics, imaging, and monitoring devices.

In addition, the pandemic-induced disruptions, geopolitical tensions, and logistical bottlenecks have led to extended lead times and fluctuating raw material prices. Like, component delivery delays in 2022 averaged between 20 to 50 weeks, causing production slowdowns and missed product launch deadlines for numerous OEMs relying on contract manufacturers.

Furthermore. These constraints force CMOs to either stockpile inventory at higher costs or redesign products to accommodate available components, both of which impact profitability and customer satisfaction.

Talent Shortage and Workforce Retention Issues

An additional pressing challenge facing the medical device contract manufacturing market is the scarcity of skilled labour and difficulties in workforce retention. Precision manufacturing of medical devices requires expertise in CNC machining, cleanroom protocols, metrology, and regulatory compliance—all of which are in short supply globally.

Moreover, according to the U.S. Bureau of Labor Statistics (BLS), employment in the medical device manufacturing sector grew by 8% in 2023, yet job vacancy rates remained above 10%, indicating a mismatch between available talent and industry needs.

In addition, as noted by the Society of Manufacturing Engineers (SME), nearly 60% of manufacturing firms struggle to find candidates with adequate technical skills for roles in automated production lines.

This talent gap is exacerbated by aging workforces in traditional manufacturing hubs and a lack of interest among younger generations in pursuing careers in industrial settings. So, CMOs are investing in apprenticeship programs, automation to reduce manual dependency, and partnerships with vocational institutions. However, the pace of workforce development remains a bottleneck to sustained growth in the contract manufacturing space.

REGIONAL ANALYSIS

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2023 |

| Forecast Period | 2024 to 2033 |

| Segments Covered | By Type, Service, Class of device, End-User & Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, and Analyst Overview of Investment Opportunities. |

| Market Leaders Profiled | Integer Holdings Corporation, Flex Ltd., Jabil Inc., West Pharmaceutical Inc., Benchmark Electronics Inc., Tecomet Inc., Nortech Systems Inc., TE Connectivity, and Nordson Corporation. |

SEGMENTAL ANALYSIS

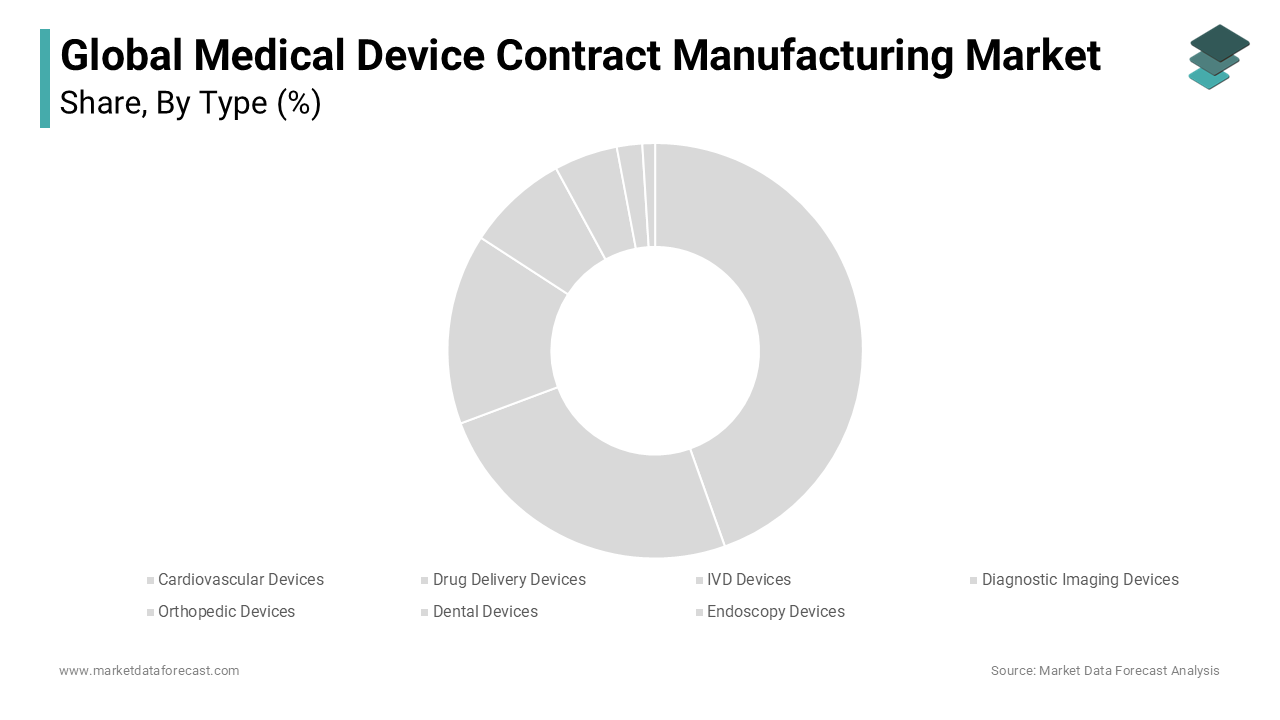

By Type Insights

The cardiovascular devices segment secured the largest share of the medical device contract manufacturing market, accounting for 25.5% of total market revenue in 2024. This control over the segment is primarily driven by the rising prevalence of cardiovascular diseases and the increasing demand for implantable and interventional devices such as pacemakers, stents, and heart valves.

Also, cardiovascular diseases remain the leading cause of death globally, responsible for an estimated 17.9 million deaths annually, according to the World Health Organization (WHO). This has led to a surge in the production of life-saving cardiac devices that require high-precision manufacturing under stringent regulatory conditions—factors that favor outsourcing to contract manufacturers.

Apart from these, over 6 million Americans suffer from heart failure, necessitating long-term medical device support. Therefore, the complexity of these devices, combined with evolving regulatory requirements, makes contract manufacturing a strategic choice for OEMs seeking scalable and compliant production solutions without significant capital investment.

The drug delivery devices segment is projected to grow at the highest CAGR of 12.4% in the forecast period. This rapid development is fueled by the increasing adoption of wearable injectors, auto-injectors, and smart inhalers, especially for chronic disease management and biologic drug administration.

A key driver is the expansion of the biopharmaceutical industry, which relies heavily on advanced delivery systems for therapeutics like monoclonal antibodies and gene therapies. Like, global spending on biologics surpassed $400 billion in 2023, much of which requires specialized delivery mechanisms, as per the IQVIA Institute for Human Data Science.

Moreover, patient preference for self-administration and home-based treatments has surged post-pandemic, further boosting demand for user-friendly and connected drug delivery platforms. So, these trends are compelling original equipment manufacturers (OEMs) to engage contract manufacturers capable of handling precision engineering, electronics integration, and compliance with FDA guidelines for combination products.

By Service Insights

The device development and manufacturing services commanded the medical device contract manufacturing market, capturing 65.4% of the total market share in 2024. This segment encompasses end-to-end services including design, prototyping, clinical trial production, and full-scale commercial manufacturing.

One major factor behind this dominance is the growing number of small and mid-sized medical device firms that lack internal R&D and production capabilities. According to AdvaMed, more than 70% of U.S.-based medical device companies have fewer than 50 employees, making them highly reliant on external partners for product development and scale-up.

Furthermore, contract manufacturers offering integrated design-to-manufacturing solutions are thus positioned as critical enablers in accelerating time-to-market while ensuring regulatory compliance.

The quality management services segment is anticipated to grow at the fastest CAGR of 10.8% during the forecast period. This rise is attributed to the tightening of global regulatory standards and the increasing need for compliance assurance across all stages of medical device production.

With the implementation of the European Union’s Medical Device Regulation (MDR) and the U.S. FDA’s updated Quality System Regulation (QSR 820), OEMs face heightened scrutiny regarding documentation, process validation, and audit readiness. According to the European Commission, nearly 60% of MDR submissions were delayed or rejected due to inadequate quality system documentation in the initial review cycles.

To mitigate risks and ensure continuous compliance, many companies are outsourcing quality assurance, calibration, testing, and audit preparation to experienced contract providers who maintain up-to-date expertise and certified facilities.

By Class of Device Insights

The class II medical devices segment held the biggest share, contributing 45.8% of the total Medical Device Contract Manufacturing Market in 2024. This category includes moderate-risk devices such as infusion pumps, surgical instruments, diagnostic test kits, and powered mobility aids.

A primary driver of this segment's dominance is the sheer volume of Class II devices in circulation and their widespread use in both hospital and outpatient settings. With growing healthcare access and an aging population, demand for these devices continues to rise, encouraging OEMs to outsource production to contract manufacturers with established quality systems and regulatory experience.

The class III medical devices segment is expected to expand at the highest CAGR of 11.6%. Class III devices include high-risk implants such as pacemakers, heart valves, and implantable defibrillators, which require rigorous premarket approval and extensive clinical validation.

This growth is primarily driven by the increasing incidence of chronic diseases and the rising adoption of implantable and life-sustaining devices.

Additionally, as per the National Institutes of Health (NIH), advancements in regenerative medicine and bioengineered implants are fueling innovation in high-risk device categories. Given the complex manufacturing, sterilization, and traceability requirements associated with Class III devices, OEMs increasingly rely on contract manufacturers with specialized cleanroom facilities, validated processes, and deep regulatory expertise to ensure successful commercialization.

REGIONAL ANALYSIS

North America Medical Device Contract Manufacturing Market Insights

North America secured the top position in the medical device contract manufacturing market, accounting for 40.1% of the total market share in 2024. The region's position is underpinned by its robust healthcare infrastructure, presence of leading OEMs and contract manufacturers, and favorable regulatory frameworks.

One key factor driving growth is the high concentration of medical device startups and SMEs that lack in-house production capabilities. Also, the U.S. Food and Drug Administration’s (FDA) proactive engagement with industry stakeholders ensures a conducive environment for innovation and outsourcing.

Moreover, the increasing burden of chronic diseases and the aging population has spurred demand for advanced therapeutic devices, further reinforcing the need for scalable manufacturing solutions. With ongoing investments in digital health, AI-driven diagnostics, and personalized medical devices, North America remains at the forefront of contract manufacturing activity globally.

Europe Medical Device Contract Manufacturing Market Insights

Europe is a significant regional player in the market. The region benefits from a mature medtech ecosystem, a well-established network of contract manufacturers, and alignment with international quality standards such as ISO 13485.

A major driver of growth is the implementation of the Medical Device Regulation (MDR) in 2021, which has prompted many original equipment manufacturers (OEMs) to seek experienced contract partners capable of navigating complex compliance landscapes. With increasing pressure to reduce costs and improve time-to-market, European OEMs continue to leverage contract manufacturing to maintain competitiveness while adhering to evolving regulatory expectations.

Asia-Pacific (APAC) Medical Device Contract Manufacturing Market Insights

The Asia-Pacific (APAC) region is emerging as the fastest-growing market. Countries such as China, India, Japan, and South Korea are witnessing rapid healthcare modernization, increasing disposable incomes, and government initiatives aimed at strengthening local medical device production.

China alone accounts for a significant portion of APAC’s growth. Also, as per the World Bank, healthcare expenditure in China has grown by over 10% annually in recent years, supporting demand for both imported and locally produced medical technologies.

India is also gaining traction as a hub for cost-effective contract manufacturing, particularly for diagnostics and consumables. The Indian government’s "Make in India" initiative has encouraged foreign investment in medical device production, further propelling the role of CMOs in the country’s healthcare supply chain. As APAC economies continue to invest in medtech innovation, the region’s contract manufacturing sector is poised for sustained expansion.

Latin America Medical Device Contract Manufacturing Market Insights

Latin America is an emerging player in medical device contract manufacturing market. While still an emerging market, the region is experiencing gradual growth due to improving healthcare access, regulatory reforms, and increasing local manufacturing capacity.

Brazil leads the regional market, benefiting from a large patient pool and government programs aimed at reducing reliance on imported medical devices. Also, Mexico is another key player, leveraging its proximity to the U.S. and participation in trade agreements to attract foreign investment in medical manufacturing. Despite economic volatility and infrastructure challenges, Latin America presents promising opportunities for CMOs targeting cost-sensitive yet growing markets.

Middle East and Africa Medical Device Contract Manufacturing Market Insights

The Middle East and Africa (MEA) region is gaining attention due to rising healthcare investments, particularly in the Gulf Cooperation Council (GCC) countries.

Saudi Arabia and the United Arab Emirates are leading the charge, with Vision 2030 and UAE Centennial 2071 strategies promoting healthcare modernization and local medical technology production. South Africa also plays a pivotal role in sub-Saharan Africa, serving as a regional hub for medical device distribution and limited contract manufacturing. However, challenges such as inconsistent regulatory frameworks, limited skilled labor, and supply chain disruptions persist. Despite these hurdles, growing awareness of advanced healthcare solutions and increasing private sector participation suggest long-term potential for contract manufacturing expansion in the MEA region.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Integer Holdings Corporation, Flex Ltd., Jabil Inc., West Pharmaceutical Inc., Benchmark Electronics Inc., Tecomet Inc., Nortech Systems Inc., TE Connectivity, and Nordson Corporation are a few of the promising companies operating in the global medical device manufacturing market profiled in this report.

The competitive environment in the Medical Device Contract Manufacturing Market is highly dynamic, shaped by rapid technological advancements, evolving regulatory landscapes, and increasing demand for precision-manufactured devices. Market participants range from large global contract manufacturers with diversified capabilities to niche players specializing in specific therapeutic areas or device classes. This diversity fosters intense competition, where differentiation is achieved through technical expertise, regulatory readiness, and the ability to deliver scalable, cost-effective solutions.

Innovation remains a key battleground, with companies investing heavily in automation, digital quality systems, and cleanroom manufacturing to meet the growing complexity of next-generation medical devices. Strategic acquisitions and partnerships are common, allowing firms to expand service offerings and enter new geographic or product segments. Additionally, customer-centric approaches—such as collaborative R&D engagements and turnkey solutions—are becoming essential for securing long-term contracts with major OEMs.

As healthcare providers and regulators demand higher levels of quality assurance and traceability, contract manufacturers must continuously enhance their compliance frameworks and operational efficiencies. This ongoing evolution ensures that only those firms capable of delivering both technical excellence and agile service delivery will maintain a strong foothold in this expanding and increasingly sophisticated market.

Top Players in the Medical Device Contract Manufacturing Market

One of the leading players is Jabil, a global manufacturing solutions provider with a strong presence in medical device contract manufacturing. Jabil offers end-to-end services, including design, prototyping, and full-scale production for complex medical devices. The company supports major OEMs in developing diagnostics, surgical tools, and wearable health technologies, leveraging its global footprint and deep regulatory expertise.

Another key player is Flex, a multinational electronics manufacturing services company that has expanded significantly into the medical technology sector. Flex specializes in high-mix, low-volume manufacturing tailored to advanced medical devices, supporting clients from concept development through to commercialization with integrated supply chain and quality assurance services.

Medtronic also plays a critical role, though primarily as an original equipment manufacturer, it collaborates extensively with contract manufacturing partners and also provides third-party manufacturing services through its Precision Surgery division. Medtronic’s expertise in surgical and interventional devices makes it a strategic participant in shaping contract manufacturing standards and innovation pathways across the industry.

Top Strategies Used by Key Market Participants

A primary strategy among leading players is expanding service portfolios to offer full lifecycle support, from design and prototyping to post-market surveillance. By integrating engineering, manufacturing, and compliance services, companies enhance their value proposition and reduce client dependency on multiple vendors.

Another major approach is investing in digital transformation and smart manufacturing technologies, such as AI-driven quality control systems, real-time data analytics, and digital twin simulations. These innovations improve production efficiency, traceability, and adherence to evolving regulatory requirements.

Lastly, geographic diversification and localized production capabilities are being pursued to mitigate supply chain risks and cater to regional market demands. Companies are establishing facilities in emerging markets while strengthening partnerships in established regions to ensure agility and responsiveness in a rapidly evolving medtech landscape.

RECENT MARKET DEVELOPMENTS

- In March 2024, Jabil announced the expansion of its medical device manufacturing facility in Malaysia, aiming to increase capacity for high-precision diagnostic and surgical instruments to serve the growing demand in the Asia-Pacific region.

- In July 2023, Flex launched a dedicated digital quality assurance platform designed specifically for medical device manufacturing, enhancing traceability, reducing compliance risks, and improving overall production efficiency for its clients.

- In November 2023, a leading U.S.-based contract manufacturer entered into a strategic collaboration with a European biotech firm to co-develop manufacturing processes for next-generation implantable drug delivery devices, aligning with rising demand for combination products.

- In February 2024, a prominent medical contract manufacturing firm acquired a specialized cleanroom assembly business in Germany, strengthening its capabilities in sterile production environments and expanding its footprint in the European market.

- In May 2024, a top-tier CMO partnered with a leading university research center to develop AI-powered inspection systems for micro-component validation in cardiac and neurological devices, reinforcing its position in high-complexity manufacturing.

MARKET SEGMENTATION

This research report on the global medical device contract manufacturing market has been segmented based on the device type, service, class of device, and region.

By Type

- Cardiovascular Devices

- Drug Delivery Devices

- IVD Devices

- Diagnostic Imaging Devices

- Orthopedic Devices

- Dental Devices

- Endoscopy Devices

By Service

- Device Development and Manufacturing Services

- Device Manufacturing Services

- Process Development Services

- Device Engineering Services

- Quality Management Services

- Packaging Validation Services

- Inspection and Testing Services

- Sterilization Services

By Class of Device

- Class II Medical Devices

- Class III Medical Devices

- Class I Medical Devices

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

How much was the global medical device contract manufacturing market worth in 2024?

The global medical device contract manufacturing market size was valued at USD 86.15 bn in 2024.

Does this report include the impact of COVID-19 on the medical device contract manufacturing market?

Yes, we have studied and included the COVID-19 impact on the global medical device contract manufacturing market in this report.

Which segment by type held the significant share in the medical device contract manufacturing market?

Based on type, the IVD devices segment was the most lucrative among all and accounted for the largest share of the market in 2024.

What are the companies playing a major role in the medical device contract manufacturing market?

Companies playing a significant role in the medical device contract manufacturing market are Integer Holdings Corporation, Flex Ltd., Jabil Inc., West Pharmaceutical Inc., Benchmark Electronics Inc., Tecomet Inc., Nortech Systems Inc., TE Connectivity, and Nordson Corporation.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com