Middle-East And Africa Pest Control Market Size, Share, Growth, Trends, And Forecast Research Report, Segmented By Type, Application, Pest Type, And By Country (KSA, UAE, Israel, South Africa, And Ethiopia, Kenya, Egypt, Sudan, Rest of GCC Countries, and Rest of MEA), Industry Analysis From (2026 to 2034)

Middle East and Africa Pest Control Market Size

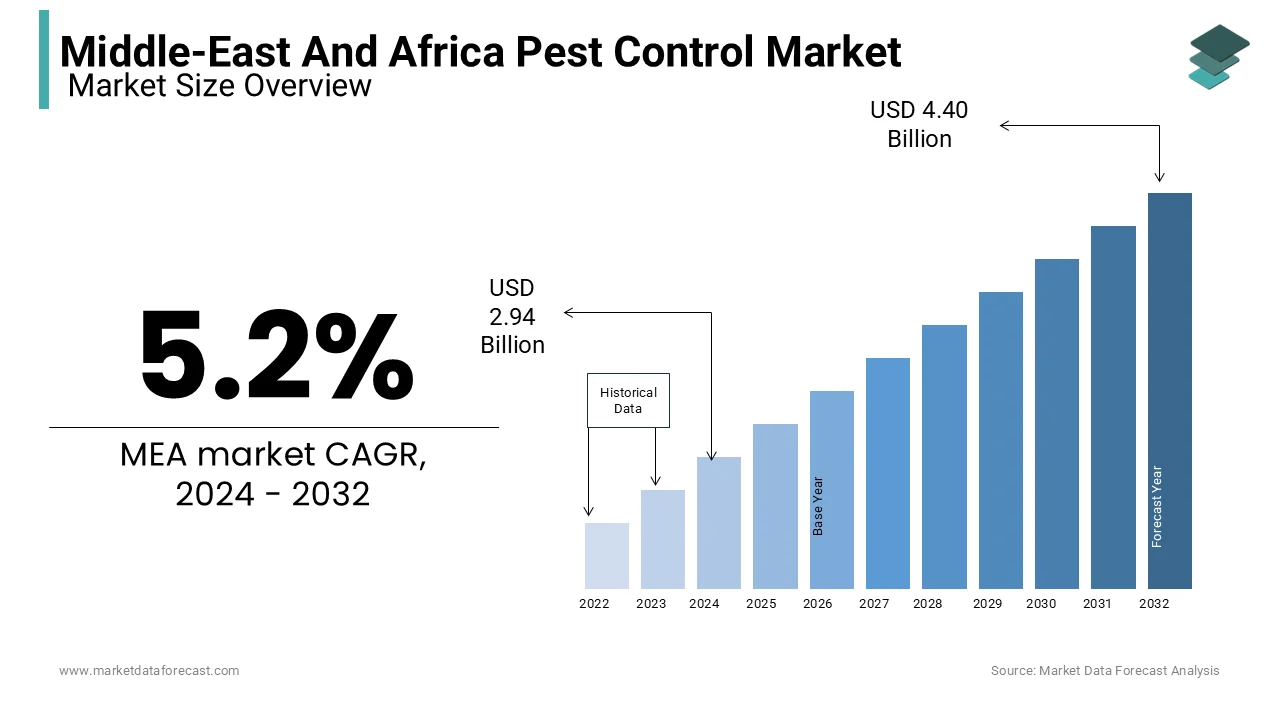

The Middle East and Africa pest control market was valued at USD 3.09 billion in 2025 and is anticipated to reach USD 3.25 billion in 2026 from USD 4.88 billion by 2034, estimated to grow at a CAGR of 5.2% from 2026 to 2034.

Middle-East and Africa Pest Control Market

The pest control market operates within a complex environmental and demographic landscape, where rapid population shifts and climatic variations intensify pest proliferation risks. According to the World Health Organization, vector borne diseases account for more than 17% of all infectious diseases and cause more than 700,000 deaths annually, with a disproportionate impact across tropical and subtropical zones in the region. As per the International Plant Protection Convention, Africa experiences annual agricultural yield losses between 30% and 60% due to pest infestations, which directly compromises food security and rural livelihoods. Urbanization trends further reshape exposure dynamics, as the United Nations projects that more than 60% of Africa's population will reside in urban centers by 2050, creating concentrated habitats conducive to pest transmission. Climate variability amplifies these challenges by extending vector activity seasons and enabling geographic range expansion of invasive species. Regulatory frameworks across Gulf Cooperation Council nations and select African states are increasingly emphasizing integrated pest management protocols and chemical risk assessment, to balance efficacy with environmental stewardship. The convergence of public health imperatives, agricultural productivity demands, and urban infrastructure development defines the operational boundaries of this market, while underscoring its critical role in regional resilience and sustainable development.

MARKET DRIVERS

Accelerating Urbanization and Infrastructure Expansion Fuelling Residential and Commercial Demand

Rapid urban transformation across the Middle East and Africa region generates sustained demand for professional pest control services, as dense population centers create ideal conditions for rodent and insect proliferation, which is primarily driving the growth of the Middle East and Africa pest control market. According to United Nations data, more than 60% of Africa's population is projected to live in urban areas by 2050, representing a tripling of the current urban population base. This demographic shift concentrates waste generation, water storage, and food supply chains within confined spaces, thereby elevating exposure to vectors such as cockroaches, termites, and mosquitoes. In Gulf Cooperation Council nations, urban development indices indicate that residential and commercial construction activity expanded by 8.3% annually between 2020 and 2024, necessitating integrated pest management protocols during and post construction phases. Municipal authorities in cities like Dubai and Nairobi now mandate pest control certifications for new hospitality and healthcare facilities, which institutionalizes service procurement. Furthermore, as per the Food and Agriculture Organization, urban households in sub Saharan Africa allocate approximately 12% of monthly expenditures to home maintenance, including pest mitigation, reflecting growing consumer awareness. The proliferation of high rise apartments, shopping complexes, and logistics hubs intensifies the need for scheduled fumigation, monitoring, and preventive treatments. This structural demand is reinforced by rising middle class expectations for hygienic living environments and regulatory compliance requirements, that transform pest control from discretionary spending to essential infrastructure maintenance.

Escalating Vector Borne Disease Burden Driving Public Health and Institutional Procurement

The growth of the Middle East and Africa pest control market is also driven by the persistent threat of vector transmitted illnesses compels governments and international agencies to prioritize pest control as a core public health intervention across the Middle East and Africa. According to the World Health Organization, more than 700,000 deaths occur annually from diseases such as malaria, dengue, and leishmaniasis, with the Eastern Mediterranean Region bearing a significant morbidity burden. As per the Institute for Health Metrics and Evaluation, Sudan and Yemen recorded the highest Disability Adjusted Life Years lost to vector borne diseases in 2023, underscoring urgent intervention needs. National malaria control programs in countries like Kenya and Ethiopia allocate substantial budgets to indoor residual spraying and larval source management, which directly expands procurement of professional pest control services. The Africa Phytosanitary Programme, supported by the International Plant Protection Convention, enhances surveillance capacity for crop and human health pests, thereby creating institutional demand for geospatial monitoring and targeted intervention technologies. Climate induced shifts in vector habitats further intensify seasonal outbreaks, prompting preemptive public sector contracting. Additionally, as per WHO EMRO data, arboviral diseases, including Rift Valley fever and West Nile virus, are increasingly reported across the region, necessitating integrated vector management strategies. This public health imperative translates into sustained institutional demand that stabilizes market growth independent of consumer discretionary cycles, while fostering innovation in eco-friendly and precision application methodologies.

MARKET RESTRAINTS

Fragmented Regulatory Landscapes Impeding Standardized Service Delivery And Product Registration

Divergent national frameworks governing pesticide registration, application protocols, and operator licensing create substantial operational friction for pest control providers across the Middle East and Africa, which is a key restraint to the regional market growth. According to CropLife Africa Middle East, the region encompasses over 50 distinct regulatory jurisdictions, each with unique documentation requirements, approval timelines, and restricted substance lists, which escalates compliance costs and delays market entry. As per the Food and Agriculture Organization, only 18 of 54 African nations maintain fully functional pesticide registration authorities, capable of evaluating new active ingredients within internationally accepted timeframes. This regulatory fragmentation forces multinational service providers to maintain parallel operational protocols, increasing administrative overhead by an estimated 35% according to industry assessments. In Gulf Cooperation Council states, while harmonization efforts exist, implementation timelines vary significantly, with Saudi Arabia requiring 18 to 24 months for new product approvals compared to 6 to 9 months in the United Arab Emirates. Furthermore, as per REACH24H Consulting, emerging economies in North and Sub Saharan Africa frequently update banned substance lists without transitional grace periods, disrupting existing service contracts. The absence of mutual recognition agreements for operator certifications restricts labor mobility and necessitates country specific training investments. These structural barriers disproportionately affect small and medium enterprises, limiting market consolidation and innovation diffusion, while elevating service costs for end users, particularly in rural and peri urban communities.

Limited Technical Capacity and Skilled Workforce Shortages Constraining Service Quality and Scalability

A critical deficit in trained pest management professionals and technical support infrastructure impedes the regional market expansion. According to the International Plant Protection Convention, fewer than 2,000 certified plant health officers serve the entire African continent, resulting in inadequate surveillance coverage and delayed outbreak response. As per the Africa Phytosanitary Programme training initiative, over 50 specialists from six pilot nations required intensive retraining in geospatial pest monitoring tools, highlighting the foundational skills gap. In commercial pest control segments, industry associations estimate that less than 30% of field technicians in Sub Saharan Africa possess formal certification in integrated pest management principles, leading to inconsistent application practices and suboptimal outcomes. Furthermore, as per CropLife International, the ratio of extension officers to smallholder farmers exceeds 1 to 3,000 in many East African nations, limiting knowledge transfer on safe and effective pest control methods. This capacity constraint is exacerbated by limited access to continuing education, digital tools, and calibrated equipment, particularly in rural jurisdictions. The shortage of entomologists and public health specialists further restricts evidence based strategy development at municipal and national levels. Consequently, service providers face challenges in scaling operations, maintaining quality assurance, and adopting advanced technologies, which ultimately elevates customer acquisition costs and constrains market penetration, especially in underserved regions with high pest pressure.

MARKET OPPORTUNITIES

Digital Transformation and Geospatial Technologies Enabling Precision Pest Surveillance And Management

The integration of digital monitoring platforms and geographic information systems presents a promising opportunity for the Middle East and Africa pest control market growth. According to the International Plant Protection Convention, the Africa Phytosanitary Programme has equipped pilot countries with ArcGIS enabled tablets and advanced survey protocols, allowing real time pest detection and predictive modeling. As per United States Department of Agriculture partnerships, geospatial analytics can reduce survey response times by up to 60%, while improving targeting accuracy for intervention resources. In urban settings, smart sensor networks and internet of things enabled traps generate continuous data streams on pest activity, enabling dynamic scheduling and resource optimization for service providers. Furthermore, as per FAO Kenya, digital platforms facilitate farmer reporting of crop pest outbreaks, creating early warning systems that trigger coordinated public private response mechanisms. The proliferation of mobile connectivity across the region, with over 500 million smartphone users in Sub Saharan Africa as of 2024, provides infrastructure for app based service booking, remote diagnostics, and customer education. Machine learning algorithms, trained on regional pest behavior patterns, can forecast infestation risks, allowing preemptive treatment that reduces chemical usage and environmental impact. This technological convergence not only elevates service quality but also creates new revenue streams through data analytics subscription models and predictive maintenance contracts. Early adopters gain a competitive advantage through demonstrable outcomes, transparency, and regulatory compliance, positioning digital enablement as a critical growth lever.

Expansion of Biopesticides And Eco Friendly Solutions Aligning With Sustainability Mandates And Consumer Preferences

Growing regulatory emphasis on environmental protection and rising consumer preference for non-toxic interventions create a substantial opportunity for the regional market growth. According to CropLife Africa Middle East, the Sustainable Pesticide Management Framework prioritizes reduction of Highly Hazardous Pesticides and accelerates registration pathways for biological alternatives in nine target nations, including Kenya, Morocco, and Egypt. As per the Food and Agriculture Organization, biopesticides derived from microbial, botanical, or mineral sources now represent over 15% of new pesticide registrations in North African markets, reflecting shifting regulatory priorities. In commercial agriculture segments, integrated pest management protocols increasingly incorporate biological control agents, such as parasitoid wasps and entomopathogenic fungi, which reduce chemical dependency while maintaining yield protection. Furthermore, as per WHO guidelines, vector control programs are evaluating insect growth regulators and bacterial larvicides as sustainable alternatives to conventional insecticides for malaria and dengue prevention. Consumer awareness campaigns by municipal authorities in Gulf cities have increased demand for green certified pest control services by an estimated 25% year on year, according to industry surveys. The alignment of biopesticide innovation with circular economy principles and climate resilience objectives attracts impact investment and development finance. Companies that establish local production facilities for region specific biological agents can achieve cost advantages, while supporting agricultural sovereignty and environmental stewardship, positioning this segment for accelerated growth.

MARKET CHALLENGES

Climate Change Induced Shifts In Pest Ecology Complicating Prediction And Intervention Strategies

Accelerating climatic variability fundamentally alters pest distribution patterns, reproductive cycles, and resistance profiles, which is creating significant operational uncertainty for control providers across the Middle East and Africa and challenging the regional market growth. According to the Intergovernmental Panel on Climate Change, rising temperatures and altered precipitation regimes have expanded the geographic range of key vectors, such as Aedes aegypti mosquitoes, into previously unaffected highland areas of East Africa. As per the International Centre of Insect Physiology and Ecology, climate driven shifts enable up to three additional reproductive cycles annually for major crop pests like Fall Armyworm, intensifying infestation pressure and reducing treatment windows. Furthermore, as per FAO assessments, increased frequency of extreme weather events disrupts scheduled pest control operations, damages application equipment, and compromises chemical efficacy through runoff or degradation. In arid regions of the Middle East, prolonged droughts concentrate rodent populations around limited water sources, elevating zoonotic disease transmission risks while complicating bait placement strategies. The unpredictability of pest emergence timelines challenges inventory management and workforce deployment for service providers, leading to either resource underutilization or emergency response cost escalation. Additionally, as per research published in Environmental Research Letters, evolving pest genotypes exhibit accelerated resistance to conventional active ingredients, necessitating continuous formulation innovation and resistance monitoring. These dynamic ecological shifts require substantial investment in adaptive research, real time surveillance infrastructure, and flexible operational models, which strain resources, particularly for small and medium enterprises operating in resource constrained environments.

Economic Volatility And Currency Fluctuations Constraining Investment In Advanced Technologies And Workforce Development

Macroeconomic instability across multiple jurisdictions in the Middle East and Africa impedes long term capital allocation, which is essential for technological modernization and human capital development within the pest control sector and further challenging the Middle East and Africa pest control market growth. According to the International Monetary Fund, currency depreciation exceeding 40% against the US dollar occurred in several Sub Saharan African economies during 2023 to 2024, elevating import costs for specialized equipment, calibration tools, and active ingredients. As per World Bank data, inflation rates above 20% in nations such as Egypt and Nigeria erode household disposable income, reducing discretionary spending on preventive pest management services. Furthermore, as per industry assessments, the high upfront cost of digital monitoring systems, geospatial software, and eco friendly formulations remains prohibitive for small and medium enterprises, which constitute over 70% of service providers in the region. Limited access to affordable financing mechanisms restricts investment in technician training, certification programs, and safety equipment, which compromises service quality and regulatory compliance. In public sector procurement, budget reallocations during fiscal consolidation periods frequently delay or cancel multi year pest control contracts, creating revenue uncertainty for established operators. Additionally, as per CropLife Africa Middle East, volatile foreign exchange rates complicate long term supply agreements for imported biological control agents and precision application hardware. These financial constraints collectively hinder the sector's ability to adopt innovation, scale operations, and meet evolving customer expectations, particularly in high growth urban and agricultural segments where demand for advanced solutions is accelerating.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.2% |

| Segments Covered | By Type, Application, Type of Pest, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | Algeria, Bahrain, Egypt, Kuwait, Qatar, Saudi Arabia, UAE |

| Market Leaders Profiled | Ecolab, Rollins, Rentokil Initial, Service Master Global Holdings, Massey Services, Arrow Exterminations, Sanix Incorporated, Asante, and Dodson Brothers Exterminating Company. |

SEGMENT ANALYSIS

By Type Insights

The chemical segment led the market by holding the highest share of the Middle East and Africa pest control market in 2025 due to its proven effectiveness in rapidly eliminating pest populations across diverse environmental conditions. As per the Food and Agriculture Organization, chemical interventions remain the primary defense against crop destroying pests in regions where food security pressures demand immediate yield protection. The widespread availability of registered chemical formulations across Gulf Cooperation Council nations and Sub Saharan Africa enables scalable deployment for both preventive and reactive pest management scenarios. Furthermore, as per CropLife Africa Middle East, regulatory frameworks in key markets like South Africa and Egypt have streamlined approval processes for low toxicity chemical products, which maintains market accessibility while addressing environmental concerns. The cost efficiency of chemical treatments compared to alternative methods appeals to budget constrained smallholder farmers and municipal authorities managing public health vector control programs. Additionally, the compatibility of chemical solutions with existing application infrastructure, including sprayers, foggers, and baiting systems, reduces adoption barriers for service providers. This segment's dominance is further reinforced by continuous innovation in targeted delivery mechanisms, that minimize non target exposure while maximizing pest mortality rates. The convergence of regulatory support, operational practicality, and demonstrated efficacy ensures chemical pest control maintains its leading position, despite growing interest in sustainable alternatives.

The biological control segment is anticipated to register the highest CAGR of 10.4% during the forecast period in the Middle East and Africa pest control market, as regional policies increasingly favor environmentally sustainable pest management approaches. According to the International Plant Protection Convention, the Africa Phytosanitary Programme has accelerated registration pathways for microbial and botanical biopesticides in nine priority nations, including Kenya, Morocco, and Egypt, which directly stimulates market entry for biological solution providers. As per the Food and Agriculture Organization, biological control agents derived from parasitoids, predators, and entomopathogenic fungi now represent over 15% of new pesticide registrations in North African markets, reflecting shifting regulatory priorities. The growing adoption of integrated pest management protocols in commercial agriculture segments further propels demand for biological alternatives, that preserve beneficial insect populations while suppressing target pests. Furthermore, as per WHO guidelines, vector control programs across the Eastern Mediterranean Region are evaluating bacterial larvicides and insect growth regulators as sustainable substitutes for conventional insecticides in malaria and dengue prevention initiatives. Consumer awareness campaigns by municipal authorities in Gulf cities have increased demand for green certified pest control services by an estimated 25% year on year, according to industry surveys. The alignment of biological control innovation with circular economy principles and climate resilience objectives attracts impact investment and development finance. Companies establishing local production facilities for region specific biological agents achieve cost advantages, while supporting agricultural sovereignty and environmental stewardship, positioning this segment for accelerated expansion.

By Application Insights

The agricultural and residential segment held the dominant market position in 2025 with 57.4% of the regional market share in 2025 due to the critical intersection of food production needs and urban household hygiene requirements. According to the Food and Agriculture Organization, pest induced crop losses in Sub Saharan Africa range between 30% and 60% annually, which compels farmers to prioritize professional pest management services to safeguard yields and livelihoods. As per United Nations data, more than 60% of Africa's population will reside in urban centers by 2050, creating concentrated residential environments where pest proliferation risks intensify and demand for household pest control solutions escalates. The proliferation of smallholder farming systems across the region, which account for over 80% of agricultural production in many East African nations, further amplifies demand for accessible and affordable pest control interventions. Furthermore, as per the World Health Organization, vector borne diseases, including malaria and dengue, disproportionately affect residential communities in tropical and subtropical zones, which drives household investment in preventive pest management measures. Municipal authorities in cities like Nairobi and Lagos now mandate pest control certifications for new residential developments, which institutionalizes service procurement and expands market reach. The convergence of agricultural productivity pressures, urbanization trends, and public health imperatives ensures this application segment maintains its leading position, while creating opportunities for integrated service models that address both farm and home pest challenges.

However, the commercial pest control segment is estimated to register a CAGR of 11.4% during the forecast period in the regional market, as expanding hospitality, food service, and retail sectors prioritize hygiene compliance and brand protection. According to the United Nations World Tourism Organization, international tourist arrivals worldwide reached 1.465 billion in 2024, nearly on par with pre pandemic figures, while the Middle East led regional recoveries by climbing 29% above 2019 benchmarks, stimulating demand for professional pest management services across hotels, resorts, and dining establishments. As per the Food and Agriculture Organization, food safety regulations in Gulf Cooperation Council nations now require mandatory pest control certifications for commercial food handling facilities, which institutionalizes service procurement and expands market accessibility. The rapid proliferation of shopping malls, logistics hubs, and office complexes in urban centers like Dubai, Riyadh, and Johannesburg creates new service opportunities for scheduled monitoring and preventive treatment contracts. Furthermore, as per industry assessments, commercial property managers allocate approximately 8% of annual facility maintenance budgets to pest control services, reflecting growing recognition of pest management as essential infrastructure rather than discretionary expenditure. The rising middle class consumer expectations for hygienic commercial environments further incentivize businesses to invest in comprehensive pest management programs. This segment's accelerated growth is reinforced by technological adoption, including digital monitoring platforms and internet of things enabled traps that enable dynamic scheduling and resource optimization for service providers. The alignment of commercial pest control with regulatory compliance, brand reputation management, and customer satisfaction objectives positions this application segment for sustained expansion.

By Type Of Pest Insights

The insects segment led the market by holding 41.7% of the regional market share in 2025 due to the widespread prevalence of disease transmitting and property damaging insect species across the region. According to the World Health Organization, mosquito borne diseases, including malaria, dengue, and chikungunya, account for more than 700,000 deaths annually, with a disproportionate impact across tropical and subtropical zones in the Middle East and Africa. As per the Food and Agriculture Organization, crop damaging insects, such as Fall Armyworm and desert locusts, cause annual agricultural yield losses exceeding 30% in Sub Saharan Africa, which compels farmers to prioritize insect specific control interventions. The proliferation of urban environments across the region creates ideal breeding conditions for cockroaches, ants, and flies, which elevates demand for residential and commercial insect management services. Furthermore, as per the International Centre of Insect Physiology and Ecology, climate driven shifts enable up to three additional reproductive cycles annually for major insect pests, intensifying infestation pressure and reducing treatment windows. Municipal vector control programs in cities like Cairo and Lagos allocate substantial budgets to insecticide spraying and larval source management, which directly expands procurement of professional insect control services. The versatility of insect control solutions, including chemical sprays, baits, traps, and biological agents, ensures broad applicability across residential, commercial, and agricultural settings. This segment's dominance is further reinforced by continuous innovation in targeted delivery mechanisms, that minimize non target exposure while maximizing insect mortality rates. The convergence of public health imperatives, agricultural productivity demands, and urban infrastructure development ensures insect pest control maintains its leading position.

The termites segment is a promising segment and is predicted to expand at a CAGR of 6.2% during the forecast period in the Middle East and Africa pest control market, as expanding construction activity and property ownership across the region elevates demand for structural pest protection services. According to a global environmental report coordinated with the World Bank, the annual economic cost of structural damage to buildings from termites in urban areas is about $15 to $20 billion worldwide, which increases to over $30 billion per year when agricultural and forestry losses are included, representing a significant impact across warm climate regions, including the Middle East and Africa. As per industry assessments, residential and commercial property owners in Gulf Cooperation Council nations allocate approximately 5% of annual maintenance budgets to termite prevention and treatment, reflecting growing recognition of structural pest management as essential infrastructure. The rapid proliferation of wooden construction elements and landscaping features in urban developments creates new service opportunities for scheduled monitoring and preventive treatment contracts. Furthermore, as per the Food and Agriculture Organization, termite resistant building codes and treatment protocols are increasingly mandated for new construction projects in South Africa and Egypt, which institutionalizes service procurement and expands market accessibility. The rising middle class expectations for property preservation and asset protection further incentivizes homeowners to invest in comprehensive termite management programs. This segment's accelerated growth is reinforced by technological adoption, including remote monitoring sensors and targeted baiting systems, that enable precise intervention with minimal environmental impact. The alignment of termite control with property value preservation, insurance requirements, and regulatory compliance objectives positions this pest type segment for sustained expansion.

COUNTRY ANALYSIS

South Africa Pest Control Market Analysis

South Africa accounted for the leading share of the Middle East and Africa pest control market in 2025 and is likely to experience steady market development driven by its advanced smart infrastructure initiatives, expanding retail nodes, and strict adherence to export agricultural standards. According to the United Nations, over 67% of South Africa's population resides in urban areas, which creates concentrated environments conducive to pest proliferation and elevates demand for professional pest management services. As per the Food and Agriculture Organization, the country's agricultural sector continues to be a cornerstone of economic development, contributing significantly to national gross domestic product and export compliance, which compels commercial farmers to prioritize pest control interventions to safeguard crop yields. The robust hospitality and tourism industry further stimulates demand for pest control services across hotels, restaurants, and entertainment venues, that must maintain stringent hygiene standards. Furthermore, as per industry assessments, South African municipalities allocate substantial budgets to public health vector control programs targeting malaria and dengue prevention, which expands institutional procurement of professional pest management solutions. The country's well developed distribution infrastructure and skilled workforce enable efficient service delivery across urban and rural jurisdictions. Additionally, as per CropLife Africa Middle East, South Africa maintains one of the region's most comprehensive pesticide registration systems, which facilitates market entry for innovative pest control products while ensuring environmental safety. The convergence of regulatory maturity, economic diversification, and public health priorities positions South Africa as the regional market leader with sustained growth potential.

COMPETITIVE LANDSCAPE

The Middle East And Africa Pest Control Market features a competitive landscape characterized by multinational corporations regional specialists and local service providers. Multinational players leverage global expertise technology platforms and brand recognition to serve premium commercial and industrial segments while regional specialists offer localized knowledge and cost competitive solutions for agricultural and residential markets. Competition intensifies around service quality technological adoption and sustainability credentials as clients increasingly demand integrated pest management approaches and eco friendly formulations. Market consolidation accelerates through strategic acquisitions as larger players seek geographic expansion and capability enhancement. Differentiation strategies emphasize digital service platforms predictive analytics and preventive maintenance models to enhance customer retention and operational efficiency. Regulatory compliance expertise and public health partnerships create competitive advantages in institutional procurement segments. The convergence of technological innovation sustainability mandates and service quality expectations shapes competitive dynamics while creating opportunities for agile players who can balance global standards with local market nuances.

KEY PLAYERS MARKET

Some of the major players dominating the market in the region, by their products and services, include

- Rollins

- Rentokil Initial

- Ecolab

- Service Master Global Holdings

- Massey Services

- Arrow Exterminations

- Sanix Incorporated

- Asante

- Dodson Brothers Exterminating Company.

Top Three Players In The Market

- Rentokil Initial maintains a prominent global presence in pest management through its comprehensive service portfolio and technology enabled solutions. The company's strategic acquisitions across Africa including operations in Nigeria Ghana and Kenya have strengthened its regional footprint while elevating service standards to align with global protocols. Rentokil Initial leverages digital monitoring platforms and predictive analytics to deliver proactive pest management for commercial hospitality and industrial clients. The company's commitment to integrated pest management approaches and eco friendly formulations resonates with evolving regulatory expectations and sustainability mandates across the Middle East And Africa region. Recent investments in technician training programs and localized solution development enhance service quality and market responsiveness.

- Ecolab contributes significantly to global pest control through its science based solutions and public health expertise. The company's water hygiene and infection prevention capabilities complement its pest management offerings creating integrated value for healthcare hospitality and food service clients. Ecolab's research driven approach to formulation development ensures efficacy while minimizing environmental impact aligning with regional sustainability priorities. Strategic partnerships with local distributors and service providers enhance market accessibility across diverse Middle East And Africa jurisdictions. Recent expansions in technical support infrastructure and digital service platforms strengthen customer engagement and operational efficiency.

- Rollins Inc strengthens its global pest control position through its consumer focused brands and operational excellence. The company's Orkin and Clark brands deliver standardized service protocols while adapting to local pest ecology and regulatory requirements across the Middle East And Africa region. Rollins invests in technician certification programs and technology adoption to enhance service quality and customer satisfaction. Strategic focus on residential and small commercial segments addresses growing middle class demand for reliable pest management solutions. Recent initiatives in digital customer engagement and preventive service models drive retention and market share expansion.

Top Strategies Used By Key Market Participants

Key players in the Middle East And Africa Pest Control Market prioritize strategic acquisitions to accelerate geographic expansion and service capability enhancement. Companies invest in digital transformation including internet of things enabled monitoring predictive analytics and mobile service platforms to improve operational efficiency and customer experience. Sustainability integration through eco friendly formulations biological control adoption and integrated pest management protocols aligns offerings with regulatory expectations and consumer preferences. Workforce development initiatives including technician certification programs and localized training enhance service quality and market responsiveness. Strategic partnerships with local distributors government agencies and agricultural cooperatives expand market accessibility and institutional procurement opportunities.

MARKET SEGMENTATION

This research report on the Middle East and Africa pest control market is segmented and sub-segmented into the following categories.

By Type

- Chemical

- Mechanical

- Biological Control

By Application

- Commercial

- Industrial

- Agricultural and Residential Control

By Type of Pest

- Termites

- Insects

- Rodents

- Wildlife

By Country

- Algeria

- Bahrain

- Egypt

- Kuwait

- Qatar

- Arabia

- UAE

- Others

Frequently Asked Questions

What is the Middle-East and Africa pest control market?

It is the market for professional services and products used to manage, prevent, and eliminate pests in residential, commercial, agricultural, and public environments.

Why is pest control important in this region?

Pest control is crucial because warm climates, rapid urbanization, and agricultural activity increase pest pressures that can harm health, food security, and property.

What types of pests are commonly controlled in the Middle-East and Africa?

Mosquitoes, cockroaches, rodents, termites, flies, and agricultural insect pests are among the most common pest types.

What kinds of pest control solutions are used?

Chemical sprays, baits, traps, fumigation, biological controls, and integrated pest management practices are widely used.

How does climate affect pest pressure in this market?

High temperatures and seasonal moisture create environments where pests reproduce rapidly and require ongoing control measures.

What drives demand for pest control services?

Population growth, urban expansion, public health concerns, and agricultural protection needs drive market demand.

How do regulations influence the pest control market?

Government rules on pesticide registration, safe use standards, and environmental protection shape what products can be sold and how services are delivered.

Are integrated pest management (IPM) approaches gaining traction?

Yes, IPM approaches that combine biological, cultural, and chemical methods are increasingly preferred for sustainable pest control.

What challenges does the Middle-East and Africa pest control market face?

Resistance to pesticides, environmental concerns, lack of skilled professionals, and inconsistent regulation are key challenges.

How does agricultural demand impact the market?

Agriculture drives significant demand for pest control products to protect crops, reduce losses, and ensure food supply stability.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com