North America Contract Research Organization (CRO) Services Market Size, Share, Trends & Growth Forecast Report By Type (Early Phase Development Services, Clinical, Laboratory Services, Others), Application (Oncology, Neurology, Cardiology, Infectious Disease, Metabolic Disorder, Renal/Nephrology, Others), End-User (Pharmaceutical & Biotechnological Companies, Medical Device Companies, Academic & Research Institutes, Others), and Country (United States, Canada, Mexico, Rest of North America) – Industry Analysis, 2024 to 2033

North America Contract Research Organization (CRO) Services Market Size

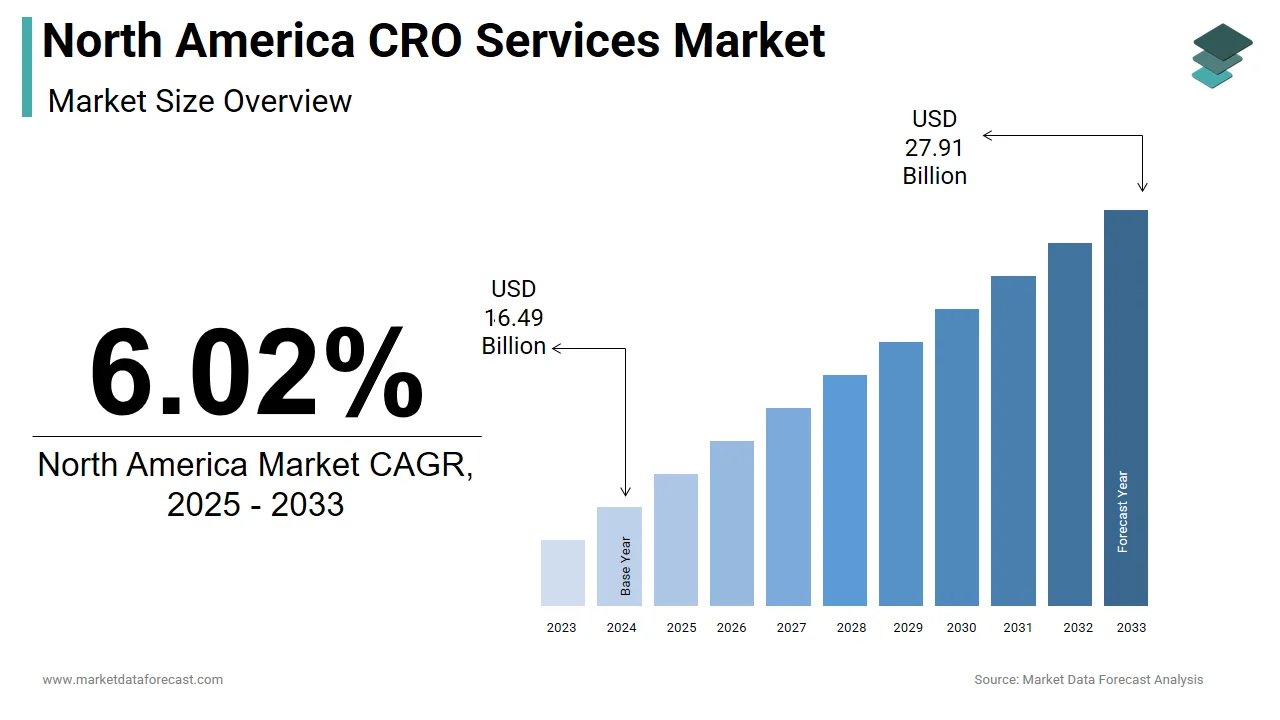

The North America contract research organization (CRO) services market is projected to grow from USD 16.49 billion in 2024 to USD 27.91 billion by 2033, at a CAGR of 6.02%.

Contract Research Organizations (CROs) in North America provide outsourced research and development services to pharmaceutical, biotechnology, and medical device companies. These organizations support various stages of drug discovery, clinical trials, regulatory compliance, and post-market surveillance, enabling innovators to streamline operations and reduce time-to-market. The North American CRO market is particularly robust due to the region’s advanced healthcare infrastructure, strong intellectual property protections, and presence of leading pharmaceutical firms. Additionally, the National Institutes of Health reported a 9% increase in biomedical research grants during this period, further reinforcing the need for contract-based scientific and analytical services. Moreover, evolving regulatory expectations and rising costs associated with internal R&D have prompted companies to outsource critical functions. The shift toward personalized medicine, digital health integration, and decentralized clinical trials has also expanded the scope of CRO activities.

MARKET DRIVERS

Rising Outsourcing of Clinical Trials by Pharmaceutical Companies

One of the primary drivers of the North America CRO services market is the increasing trend among pharmaceutical and biotech firms to outsource clinical trial operations. As drug development becomes more complex and costly, companies are leveraging CROs to manage trial logistics, patient recruitment, data management, and regulatory submissions. In 2023, the U.S. Food and Drug Administration received a record 1,785 Investigational New Drug (IND) applications, many of which were supported by CROs in Phase I to Phase III trial execution. Large pharmaceutical firms such as Pfizer, Merck, and Bristol-Myers Squibb have significantly ramped up their outsourcing ratios, with some delegating over 60% of clinical development work to external partners. Additionally, the adoption of decentralized clinical trials facilitated by digital health tools and remote monitoring is enhancing the scalability and efficiency of outsourced trial models. As per the Biotechnology Innovation Organization, nearly 40% of new clinical studies initiated in North America in 2024 included elements of virtual or hybrid trial designs managed by CROs. This evolution not only reduces operational burdens but also improves patient access and retention by making outsourcing an increasingly attractive proposition for life sciences firms.

Growth of Biopharmaceutical and Specialty Drug Development

The rapid expansion of biopharmaceutical and specialty drug development in North America is another key driver propelling the growth of the contract research organization market. Unlike traditional small-molecule drugs, biologics and specialty therapeutics require highly specialized manufacturing, testing, and regulatory pathways areas where CROs offer deep expertise. According to the Biotechnology Innovation Organization, the U.S. biopharma industry attracted over $140 billion in investment between 2021 and 2024, supporting the development of more than 3,000 novel therapies currently in the pipeline. Biologics, including monoclonal antibodies, gene therapies, and cell-based treatments, often necessitate extensive preclinical and clinical validation before approval. The U.S. Food and Drug Administration approved a record 72 novel therapeutics in 2023, many of which involved outsourced non-clinical and clinical research services provided by CROs. Furthermore, the rise of personalized medicine and companion diagnostics has introduced additional layers of complexity to drug development.

MARKET RESTRAINTS

High Operational and Compliance Costs

A significant restraint in the North America CRO services market is the high operational and compliance costs associated with conducting regulated research. CROs must adhere to stringent quality standards set by the U.S. Food and Drug Administration (FDA), Good Clinical Practice (GCP), and International Council for Harmonisation (ICH) guidelines, all of which require substantial investments in infrastructure, personnel training, and audit readiness. According to the Tufts Center for the Study of Drug Development, compliance-related expenditures account for nearly 20% of total clinical trial costs. These financial pressures are exacerbated by the increasing complexity of clinical trials, especially in areas such as gene therapy and immuno-oncology, which demand specialized facilities and highly trained staff. A 2023 report by Deloitte found that nearly 35% of mid-sized CROs faced challenges scaling operations due to budget constraints related to electronic data capture systems, laboratory information management systems (LIMS), and cybersecurity protocols. Additionally, maintaining FDA registration and ISO certifications involves recurring fees and documentation overhead, further burdening smaller players. Moreover, regulatory inspections have become more frequent and rigorous. In 2024, the FDA conducted over 400 facility inspections globally, with approximately 25% resulting in Form 483 observations requiring corrective actions. \

Talent Shortage and Workforce Retention Challenges

A persistent challenge affecting the North America CRO services market is the shortage of skilled professionals and difficulties in workforce retention. Conducting high-quality clinical and preclinical research requires experts in pharmacology, biostatistics, regulatory affairs, and data science fields where talent availability has not kept pace with industry demand. Educational institutions have struggled to meet the growing demand for trained clinical researchers, with only 18% of universities offering dedicated clinical trial management programs as of 2024, according to the Association of Clinical Research Professionals. This gap has led to longer onboarding periods and increased training costs for CROs, particularly those specializing in complex therapeutic areas such as neurology and rare diseases. Additionally, the competitive nature of the life sciences sector has intensified talent attrition. Major pharmaceutical companies and tech-driven startups often lure experienced CRO employees with higher salaries and broader career opportunities. As per McKinsey & Company, turnover rates among senior-level clinical research associates reached 18% in 2024, impacting project continuity and client satisfaction.

MARKET OPPORTUNITIES

Expansion of Digital Health and Decentralized Clinical Trials

A transformative opportunity shaping the North America CRO services market is the rapid adoption of digital health technologies and the rise of decentralized clinical trials (DCTs). Traditional clinical trial models are being reimagined to include remote patient monitoring, wearable sensors, telemedicine consultations, and electronic consent processes all of which are driving demand for CROs with digital infrastructure capabilities. This shift is driven by both patient convenience and operational efficiency. Remote data collection reduces site visits, enhances patient retention, and broadens recruitment demographics. As per Frost & Sullivan, decentralized trials have demonstrated a 25% faster enrollment rate and 15% lower dropout rate compared to conventional models. CROs such as IQVIA, Medidata, and PPD have responded by expanding their digital health offerings, integrating AI-driven analytics, and developing proprietary eClinical platforms to support sponsors in executing hybrid and fully virtual trials.

Growth of Real-World Evidence and Post-Market Surveillance Services

An emerging opportunity within the North America CRO services market is the growing emphasis on real-world evidence (RWE) and post-market surveillance (PMS) studies. As regulatory bodies and payers increasingly demand proof of long-term efficacy and safety, pharmaceutical companies are turning to CROs for robust observational studies, pragmatic trials, and pharmacovigilance support. According to the U.S. Food and Drug Administration, over 60% of novel drug approvals in 2023 included post-marketing study commitments with the heightened importance of ongoing data collection. Real-world evidence plays a crucial role in regulatory decision-making, payer reimbursement strategies, and comparative effectiveness research. The Centers for Medicare & Medicaid Services reported a 20% increase in utilization of real-world data for coverage determinations between 2021 and 2024. This trend has spurred CROs to develop sophisticated data analytics platforms capable of aggregating electronic health records, claims data, and patient-reported outcomes. Additionally, the rise of value-based healthcare models has incentivized manufacturers to demonstrate tangible patient outcomes, further boosting demand for RWE services. CROs that enhance their capabilities in artificial intelligence, machine learning, and longitudinal data analysis are well-positioned to capture this rapidly evolving segment of the research landscape.

MARKET CHALLENGES

Regulatory Complexity and Evolving Compliance Requirements

A major challenge facing the North America CRO services market is the increasing complexity of regulatory frameworks and evolving compliance requirements. CROs must navigate a dynamic landscape shaped by continuous updates from the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), and other global regulatory bodies. These changes often impact trial design, data submission formats, and reporting obligations, which is necessitating constant adaptation by service providers. For instance, the FDA’s recent push for diversity action plans in clinical trials has mandated CROs to implement inclusive recruitment strategies and demographic subgroup analyses, adding operational layers to trial execution. Additionally, the introduction of the Electronic Submissions Gateway and enhanced data integrity rules under ALCOA+ principles has required CROs to upgrade their IT infrastructures and audit practices. Moreover, cross-border trials introduce additional complexities due to varying regional regulations. A survey by the Association of Clinical Research Professionals found that nearly 40% of CROs operating in North America reported increased administrative burdens when managing multi-jurisdictional studies.

Increasing Competition from Smaller and Niche CROs

The North America CRO services market is witnessing intensified competition from smaller, agile, and niche-focused CROs that offer specialized services tailored to specific therapeutic areas or research methodologies. Unlike large global CROs that provide end-to-end solutions, these boutique firms differentiate themselves through speed, flexibility, and domain expertise, attracting clients seeking customized engagement models. This shift is particularly evident in fields such as gene therapy, rare diseases, and digital biomarkers, where deep technical knowledge is more valuable than scale. Additionally, venture-backed CROs are emerging with innovative business models, leveraging cloud-based platforms and AI-driven analytics to undercut traditional pricing structures. Furthermore, the rise of decentralized clinical trials has enabled smaller CROs to operate remotely without the overhead of large infrastructure, allowing them to compete effectively against established players.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Type, Application, End-user, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered

| United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | Quintiles Transnational Holdings Inc., Laboratory Corporation of America Holdings, Pharmaceutical Product Development, PAREXEL International Corporation, ICON Plc, PRA Health Sciences Inc., InVentiv Health Inc., Charles River Laboratories International Inc., INC Research Holdings Inc., and Wuxi PharmaTech.. |

SEGMENTAL ANALYSIS

By Type Insights

The Chemistry, Manufacturing and Controls (CMC) services segment was accounted in holding 38.4% of the North America CRO services market share in 2024. The U.S. Food and Drug Administration mandates comprehensive CMC documentation for Investigational New Drug (IND) applications, making these services indispensable for biopharmaceutical companies seeking approval. According to the FDA, over 1,785 INDs were submitted in 2023, with each requiring extensive analytical testing, formulation development, and process validation areas where CROs provide specialized expertise. Moreover, the rise in complex modalities such as biologics, cell and gene therapies, and mRNA vaccines has significantly increased demand for advanced CMC capabilities. These therapies require highly controlled manufacturing processes, necessitating outsourced support from CROs experienced in aseptic filling, stability studies, and GMP compliance. Additionally, increasing regulatory scrutiny on supply chain integrity and raw material sourcing has prompted pharmaceutical firms to rely on CROs for end-to-end quality assurance.

The discovery services segment is swiftly growing with an anticipated CAGR of 12.6% throughout the forecast period. Biotech startups and academic research institutions are increasingly outsourcing discovery-phase activities to CROs due to the high costs and technical complexity associated with in-house R&D. Furthermore, the shift toward precision medicine and personalized therapies has expanded the scope of discovery research. Pharmaceutical companies are also leveraging CRO-led discovery platforms to identify novel therapeutic candidates more efficiently.

The clinical trial services segment was accounted in holding 55.4% of the North America CRO services market share in 2024. According to the U.S. Food and Drug Administration, over 1,785 Investigational New Drug (IND) applications were submitted in 2023 alone, reflecting a surge in clinical trial activity. Major pharmaceutical firms such as Pfizer, Merck, and Bristol-Myers Squibb have outsourced a substantial portion of their clinical development work to CROs to manage costs, accelerate timelines, and access specialized expertise. North America’s well-established clinical trial infrastructure, including leading academic medical centers, patient recruitment networks, and regulatory alignment with the FDA, further reinforces its position as a hub for clinical research.

The laboratory services segment is likely to gain huge traction with an estimated CAGR of 11.9% in the next coming years. One key driver is the integration of companion diagnostics in oncology and rare disease therapies, which requires precise laboratory testing for patient stratification and treatment response monitoring. Additionally, the rise of biologics and gene therapies has intensified the need for specialized assays and stability testing, areas where CROs offer scalable solutions. Another contributing factor is the growing use of centralized labs in multi-site clinical trials to ensure consistency and regulatory compliance. The Association of Clinical Research Professionals noted that over 70% of large-scale trials in 2024 utilized centralized lab services provided by CROs.

By Application Insights

The oncology segment held 32.6% of the North America CRO services market share in 2024. According to the American Cancer Society, over 1.9 million new cancer cases were diagnosed in the United States in 2024, reinforcing the urgency for novel treatments. In response, pharmaceutical companies and biotechs have prioritized oncology pipeline expansion, with the Biotechnology Innovation Organization reporting that over 1,200 oncology drugs were in active development nationwide. The U.S. Food and Drug Administration has also played a pivotal role in accelerating oncology approvals, particularly through expedited pathways such as Breakthrough Therapy and Priority Review. Furthermore, the rise of immunotherapy, targeted therapy, and CAR-T cell treatments has introduced new complexities in trial design, patient selection, and biomarker analysis, further increasing reliance on specialized CROs.

The neurology segment is estimated to grow with a CAGR of 13.1% in the next coming years. The National Institute of Neurological Disorders and Stroke reported a 12% increase in federal funding for neuroscience research in 2024, supporting studies on Alzheimer’s, Parkinson’s, multiple sclerosis, and epilepsy. Additionally, the passage of the Accelerating Access to Critical Therapies for ALS Act (ACT for ALS) in 2023 spurred investment in neuromuscular disease research, which is prompting biotech firms to collaborate with CROs for accelerated trial execution. Pharmaceutical companies are also intensifying efforts in CNS drug development following recent breakthroughs in gene therapy and RNA-based treatments. Moreover, the adoption of digital biomarkers and wearable sensors in neurological assessments has enabled more precise outcome measurements, enhancing trial efficiency. As per Deloitte, nearly 50% of neurology-focused CRO engagements in 2024 included digital endpoints, which is signaling a shift toward more data-driven approaches in this historically challenging therapeutic domain.

By End-user Insights

The pharmaceutical and biotechnological companies segment was the largest and held a dominant share of the North America CRO services market in 2024. According to the Biotechnology Innovation Organization, U.S.-based biopharma companies raised over $140 billion in venture capital and public equity financing between 2021 and 2024, fueling a surge in outsourced research partnerships. Large pharmaceutical firms such as Amgen, Eli Lilly, and AbbVie have also increased their reliance on CROs to manage complex clinical trials, regulatory submissions, and post-market surveillance. The U.S. Food and Drug Administration reported a record 1,785 Investigational New Drug (IND) applications in 2023, many of which were supported by CROs in both preclinical and clinical phases. Furthermore, the rise of biologics, gene therapies, and mRNA-based vaccines has created a demand for specialized CRO services in areas such as pharmacokinetics, bioanalytics, and stability testing. Additionally, the shift toward decentralized clinical trials and digital health integration has led pharmaceutical firms to partner with tech-enabled CROs for scalable and efficient trial execution.

The academic and research institutes segment is lucratively growing with an anticipated CAGR of 12.4% in the next coming years. According to the National Institutes of Health, federal research funding reached over $46 billion in 2024, with a significant portion allocated to university-led clinical and translational research projects. Many academic institutions lack the internal infrastructure to conduct large-scale trials independently, prompting them to engage CROs for study coordination, data management, and regulatory support. Furthermore, the rise of precision medicine initiatives and investigator-sponsored trials has heightened the demand for outsourced research services. The Association of Clinical Research Professionals reported that over 30% of academic clinical trials in 2024 involved CRO support, particularly in oncology, neurology, and infectious disease research. In addition, academic medical centers are increasingly partnering with CROs to commercialize early-stage discoveries and bring novel therapies to market faster.

COUNTRY-WISE ANALYSIS

United States CRO Services Market Insights

The United States was the top performer in the North America CRO services market with 83.1% of the share in 2024. The U.S. Food and Drug Administration continues to be a central authority for global drug approvals, attracting multinational sponsors to conduct clinical trials and regulatory submissions within the country. In 2023 alone, over 1,785 Investigational New Drug (IND) applications were filed, many of which were supported by CROs in preclinical, clinical, and analytical services. The Biotechnology Innovation Organization reported that U.S. biopharma firms raised over $140 billion in venture capital and public equity financing between 2021 and 2024, enabling a surge in outsourced research partnerships. Additionally, academic institutions and medical research centers have increasingly collaborated with CROs to execute investigator-initiated trials and translational studies.

Canada CRO Services Market Insights

Canada was the positioned second by occupying 10.3% of the North America CRO services market in 2024. The Canadian government has actively supported life sciences innovation through programs such as the Strategic Innovation Fund and the Quebec Life Sciences Strategy, encouraging both domestic and international firms to establish R&D operations in the country. According to BIOTECanada, the nation’s biopharmaceutical sector saw a 13% increase in R&D spending in 2024, with Montreal, Toronto, and Vancouver emerging as key hubs for clinical research. Canadian universities and teaching hospitals are increasingly engaging CROs to support investigator-led trials, particularly in oncology, neurology, and rare diseases. Additionally, Canada’s streamlined regulatory environment under Health Canada has made it an attractive destination for multinational clinical trials.

KEY MARKET PLAYERS

The North American Contract Research Organization (CRO) Services Market is mainly dominated by companies such as Quintiles Transnational Holdings Inc., Laboratory Corporation of America Holdings, Pharmaceutical Product Development, PAREXEL Interntional Corporation, ICON Plc, PRA Health Sciences Inc., InVentiv Health Inc., Charles River Laboratories International Inc., INC Research Holdings Inc., and Wuxi PharmaTech.

TOP LEADING PLAYERS IN THE MARKET

IQVIA

IQVIA is a global leader in contract research services, offering end-to-end solutions across clinical development, real-world evidence, and commercialization support. In North America, the company plays a pivotal role in advancing drug development through its vast data analytics capabilities and extensive clinical trial network. Its integration of AI-driven insights and digital health technologies has redefined how pharmaceutical companies approach research and patient engagement. IQVIA's strategic focus on innovation and scalability continues to influence industry standards and enhance efficiency across clinical and non-clinical phases of drug development.

LabCorp Drug Development

LabCorp Drug Development, a division of Laboratory Corporation of America, is a major player in the North American CRO space, known for its strong laboratory infrastructure and deep expertise in bioanalytical testing, central lab services, and clinical trial execution. The company supports a wide range of therapeutic areas with a focus on oncology, immunology, and rare diseases. Its ability to integrate diagnostics with clinical trials enhances precision medicine strategies, which is making it a preferred partner for biopharma firms seeking comprehensive, data-rich research outcomes.

PAREXEL International Corporation

PAREXEL is a globally recognized CRO that has significantly contributed to the evolution of clinical research methodologies in North America. The company supports complex drug development programs, particularly in biologics and advanced therapies with a broad service portfolio spanning regulatory consulting, pharmacovigilance, and clinical trial management. PAREXEL’s emphasis on digital transformation, including decentralized trial models and risk-based monitoring, has positioned it as a forward-thinking partner for life sciences companies aiming to accelerate their R&D timelines while maintaining compliance and quality standards.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies adopted by leading players in the North America CRO services market is digital transformation and technology integration. CROs are investing heavily in artificial intelligence, machine learning, and cloud-based platforms to streamline clinical trial operations, enhance data analytics, and improve patient recruitment and retention. These tools enable more predictive modeling, faster decision-making, and better trial oversight.

Another key strategy is strategic acquisitions and partnerships. Major CROs are acquiring niche firms specializing in biomarker analysis, digital health, or specialized therapeutic areas to expand their service offerings and geographical reach. Collaborations with academic institutions and tech companies further enhance their research capabilities and innovation pipelines.

COMPETITION OVERVIEW

The competition in the North America CRO services market is highly dynamic, shaped by a mix of established global CROs, emerging boutique firms, and evolving client expectations. Large-scale organizations dominate with comprehensive service portfolios and extensive global networks, leveraging their experience in regulatory compliance and large clinical trial execution. However, smaller and specialized CROs are gaining traction by offering agility, domain-specific expertise, and cost-effective solutions tailored to niche therapeutic areas and innovative modalities such as gene therapy and personalized medicine.

Technological advancements are reshaping the competitive landscape, with CROs increasingly integrating digital tools like AI-driven analytics, remote monitoring, and decentralized trial platforms to differentiate themselves. Client demand for faster, more efficient, and data-rich research processes is pushing firms to innovate continuously and invest in digital infrastructure. Additionally, the growing emphasis on real-world evidence, post-market surveillance, and regulatory advisory services is expanding the scope of competition beyond traditional clinical trial support.

RECENT MARKET DEVELOPMENTS

- In January 2024, IQVIA launched a new decentralized clinical trial platform designed to enhance patient accessibility and reduce trial timelines by integrating wearable sensors and virtual study visits. This initiative aimed to provide sponsors with a scalable solution for executing hybrid and fully remote clinical studies.

- In March 2024, LabCorp expanded its central laboratory services by opening a new high-throughput biomarker testing facility in North Carolina, which is reinforcing its capacity to support complex oncology and neurology trials with advanced diagnostic capabilities.

- In June 2024, PAREXEL announced a strategic partnership with a leading AI-driven drug discovery firm to integrate real-world data into early-phase research by enabling faster target identification and candidate selection for pharmaceutical clients.

- In September 2024, Covance, now part of LabCorp, introduced a next-generation patient recruitment program leveraging predictive analytics and social media outreach to improve enrollment rates in difficult-to-recruit therapeutic areas such as rare diseases and pediatrics.

- In November 2024, Syneos Health acquired a specialized pharmacovigilance consultancy firm to strengthen its safety monitoring and regulatory compliance offerings in support of post-market surveillance and risk evaluation studies for biopharma clients.

MARKET SEGMENTATION

This research report on the North America contract research organization (CRO) services market is segmented and sub-segmented into the following categories.

By Type

- Early Phase Development Services

- Chemistry, Manufacturing and Controls (CMC)

- Preclinical Service

- Discovery

- Clinical

- Phase 1

- Phase 2

- Phase 3

- Phase 4

- Laboratory Services

- Others

By Application

- Oncology

- Neurology

- Cardiology

- Infectious Disease

- Metabolic Disorder

- Renal/Nephrology

- Others

By End-user

- Pharmaceutical & Biotechnological Companies

- Medical Device Companies

- Academic & Research Institutes

- Others

By Country

- United States

- Canada

- Mexico

- Rest of North America

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com