North America Vision Care Market Size, Share, Trends & Growth Forecast Report By Product Type (Glass Lenses, Contact Lenses, Intraocular Lenses, Contact Solutions, Lasik Equipment, Artificial Tears), Distribution Channel (Retail Stores, Online Stores, Clinics, Hospitals), and Country (United States, Canada, Mexico, Rest of North America) – Industry Analysis From 2025 to 2033.

North America Vision Care Market Size

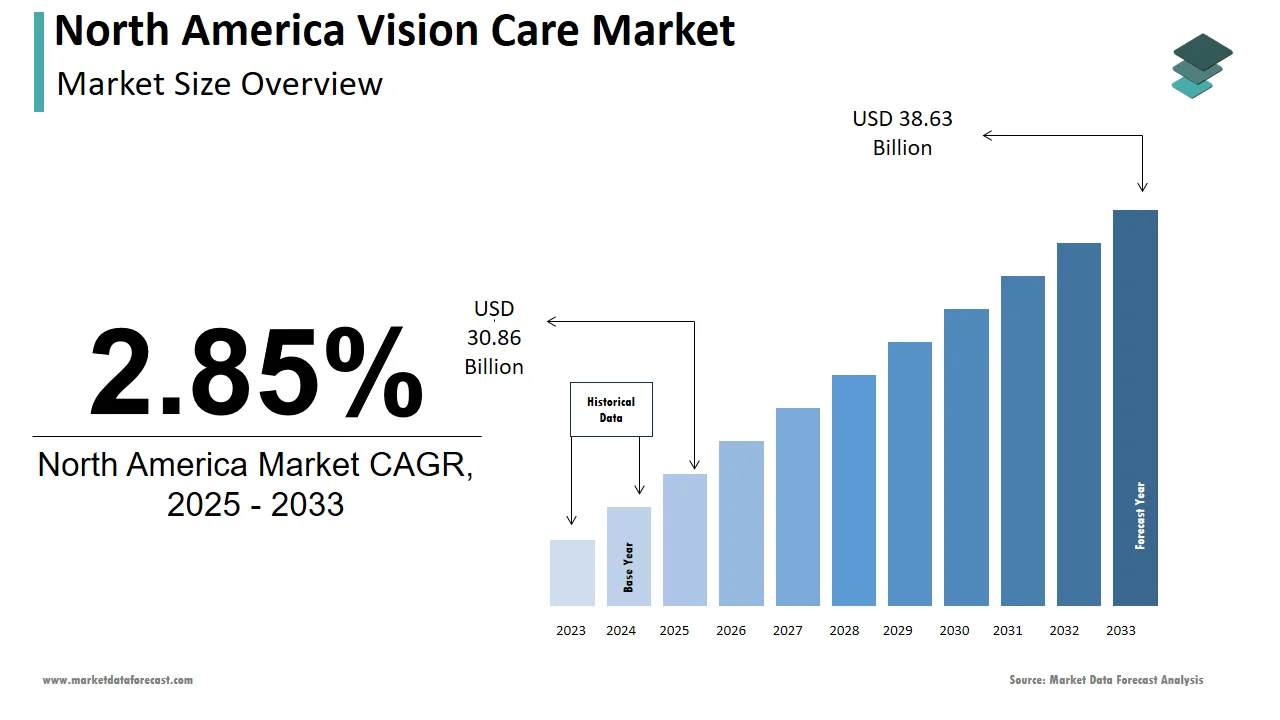

The size of the vision care market in North America was valued at USD 30 billion in 2024. This market is expected to grow at a CAGR of 2.85% from 2025 to 2033 and be worth USD 38.63 billion by 2033 from USD 30.86 billion in 2025.

The North America vision care market has established a dominant presence in the global landscape is driven by rising awareness of eye health and increasing prevalence of vision-related disorders. The United States alone accounts for over 85% of the regional revenue, as per data from the National Eye Institute (NEI). Canada follows closely supported by its robust healthcare infrastructure and growing adoption of corrective lenses. According to the Centers for Disease Control and Prevention (CDC), approximately 11 million Americans aged 12 years and older require some form of vision correction, underscoring the critical demand for vision care products. Aging demographics further amplify this need, with the NEI projecting that the number of individuals with age-related macular degeneration will double by 2050. Innovations in lens technology, such as blue-light-blocking glasses and multifocal contact lenses have also fueled market growth. Despite these positive indicators, accessibility issues persist in rural areas, limiting widespread adoption of advanced vision care solutions.

MARKET DRIVERS

Rising Prevalence of Myopia and Digital Eye Strain

The escalating incidence of myopia and digital eye strain has become a pivotal driver for the vision care market. As per the American Academy of Ophthalmology, myopia affects nearly 42% of the U.S. population, with projections indicating a rise to 50% by 2030. This surge is attributed to lifestyle changes, including prolonged screen time and limited outdoor activities particularly among younger generations. Digital eye strain is caused by excessive use of smartphones and computers and has further amplified demand for corrective lenses and artificial tears. Also, advancements in lens coatings and materials, such as anti-reflective and high-index lenses have enhanced user comfort, making these products indispensable for modern consumers.

Technological Advancements in Vision Correction Solutions

Technological innovations in vision correction have significantly propelled market growth. For instance, LASIK surgery has become increasingly accessible and affordable, with over 95% patient satisfaction rates, as noted by the American Society of Cataract and Refractive Surgery. The development of femtosecond lasers has improved surgical precision, reducing recovery times and enhancing outcomes. Similarly, advancements in intraocular lenses (IOLs) have revolutionized cataract treatment, offering multifocal and toric options for patients. According to the National Institutes of Health, IOL implantation success rates exceed 98%, boosting consumer confidence in these procedures. Furthermore, the integration of AI-driven diagnostic tools in clinics has streamlined pre-operative assessments ensuring personalized treatment plans. These technological breakthroughs not only enhance patient outcomes but also expand the scope of vision care services across North America.

MARKET RESTRAINTS

High Costs of Advanced Vision Correction Procedures

Among the primary barriers to the widespread adoption of advanced vision care solutions is their prohibitive cost. Similarly, premium intraocular lenses used in cataract surgeries often incur additional costs, which are not always covered by insurance plans. These financial burdens deter many patients particularly those in low-income households from seeking necessary treatments. As per the Kaiser Family Foundation, over 27 million Americans lack health insurance further exacerbating affordability concerns. Even corrective lenses, such as specialized contact lenses or blue-light-blocking glasses, can be costly, limiting accessibility for certain demographics. This cost barrier not only hinders market penetration but also widens disparities in eye care access across different socioeconomic groups.

Limited Accessibility in Rural and Underserved Areas

Another significant challenge facing the vision care market is the limited availability of services in rural and underserved regions. As indicated by the Health Resources and Services Administration (HRSA), over 80% of counties in the United States are classified as medically underserved areas, with a shortage of ophthalmologists and optometrists. This gap in healthcare infrastructure restricts access to essential vision care services including comprehensive eye exams and advanced treatments like LASIK or cataract surgery. Beyond this, the absence of retail stores and clinics in these areas further compounds the issue, forcing residents to travel long distances for care. A study by the National Rural Health Association revealed that rural populations are 2.5 times more likely to experience vision impairment compared to urban residents. These accessibility challenges hinder the market's ability to address unmet needs, particularly among vulnerable populations.

MARKET OPPORTUNITIES

Growing Adoption of Online Retail Channels

The shift toward online retail channels presents a transformative opportunity for the vision care market. With e-commerce platforms gaining traction, consumers now have convenient access to a wide range of products, from contact lenses to artificial tears. Companies like Warby Parker and 1-800 Contacts have capitalized on this trend by offering subscription-based models and virtual try-on tools, enhancing customer engagement. To add to this, the proliferation of telemedicine has enabled remote consultations, allowing patients to receive prescriptions without visiting physical clinics. This digital transformation not only expands market reach but also fosters innovation, positioning online retail as a key growth driver for the vision care industry.

Expansion into Preventive Eye Care Solutions

Preventive eye care represents a burgeoning opportunity within the vision care market, driven by increasing awareness of proactive health measures. As per the Centers for Disease Control and Prevention (CDC), regular eye exams can detect conditions like glaucoma and diabetic retinopathy early preventing irreversible damage. This emphasis on prevention has spurred demand for routine screenings and diagnostic tools such as retinal imaging devices. Companies are investing in educational campaigns to promote the importance of annual eye exams, particularly among aging populations. For instance, the American Optometric Association launched initiatives targeting seniors, showcasing the link between eye health and overall well-being. By focusing on preventive solutions, the market can address unmet needs while fostering long-term patient loyalty and trust.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product Type, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States, Canada, Mexico and Rest of North America. |

| Market Leaders Profiled | Johnson & Johnson Vision Care Inc., The Cooper Companies Inc. (CooperVision), EssilorLuxottica, Alcon, Bausch & Lomb, ZEISS International, SynergEyes Inc., and others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The contact lenses segment dominated the North America vision care market by capturing 35.3% of the total revenue in 2024. This influence is stimulated by their convenience, aesthetic appeal, and versatility in addressing various vision correction needs. According to the Contact Lens Institute, over 45 million Americans wear contact lenses, with daily disposable lenses witnessing a surge in demand due to their hygiene benefits. Technological advancements, such as silicone hydrogel materials have enhanced comfort and oxygen permeability making them suitable for extended wear. Additionally, the growing popularity of cosmetic lenses for altering eye color has expanded the segment’s consumer base. Retailers like Johnson & Johnson Vision have introduced innovative designs tailored to diverse lifestyles, reinforcing the segment’s dominance in the market.

The artificial tears segment represented the fastest-growing product segment, with a projected CAGR of 8.2% from 2025 to 2033. This growth is fueled by the rising prevalence of dry eye syndrome, particularly among individuals exposed to prolonged screen time. As per the National Eye Institute, over 16 million Americans suffer from chronic dry eye is creating a substantial demand for lubricating eye drops. The development of preservative-free formulations has further accelerated adoption, as they minimize irritation and are safe for frequent use. Moreover, the integration of hyaluronic acid and other advanced ingredients has enhanced product efficacy appealing to tech-savvy consumers. Partnerships between manufacturers and digital health platforms have also facilitated awareness campaigns driving segment expansion.

By Distribution Channel Insights

The retail stores held the largest share of the North America vision care market i.e. 45% of the total revenue in 2024. This control over the market is due to the widespread availability of vision care products including corrective lenses and contact solutions in brick-and-mortar outlets. Chains like Walmart Vision Center and LensCrafters offer one-stop solutions for eye exams, lens fittings, and product purchases, enhancing customer convenience. In line with the Vision Council, over 60% of consumers prefer in-store purchases for personalized service and immediate product availability. The segment’s influence is further reinforced by strategic collaborations with healthcare providers enabling seamless integration of clinical services. These factors collectively ensure the sustained prominence of retail stores in the market.

The online stores are the fastest-growing distribution channel, with a CAGR of 9.5% during the forecast period. This growth is driven by the increasing popularity of e-commerce platforms, which offer competitive pricing and doorstep delivery. Companies like Warby Parker and Zenni Optical have pioneered direct-to-consumer models is leveraging virtual try-on tools and AI-driven recommendations to enhance user experience. Also, the integration of telemedicine has enabled remote prescription renewals, addressing accessibility challenges. These trends underscore the segment’s rapid expansion and its potential to reshape traditional retail dynamics.

COUNTRY LEVEL ANALYSIS

The U.S. remains the undisputed leader in both value and volume by contributing 74.2% of the regional revenue in 2024. This leading poistion is driven by the country’s robust healthcare infrastructure, high prevalence of vision disorders, and strong consumer awareness. According to the CDC, over 11 million Americans require vision correction fueling demand for corrective lenses and advanced treatments. The U.S. government’s initiatives, such as the Healthy People 2030 program, emphasize preventive eye care, further amplifying market growth. Additionally, the presence of leading manufacturers and retailers ensures a steady supply of innovative products, solidifying the U.S.’s dominance in the market.

Canada is the fastest-growing market, with a CAGR of 7.8% from 2025 to 2033. This upward trajectory is fueled by increasing investments in healthcare and rising adoption of online retail channels. As per the Canadian Association of Optometrists, over 75% of Canadians prioritize regular eye exams driving demand for vision care products. Government initiatives promoting universal healthcare coverage have also expanded accessibility, particularly in rural areas. These factors position Canada as a high-potential market within the region.

Mexico represents an emerging market with significant untapped potential. Economic growth and rising awareness of eye health are expected to drive demand for affordable vision care solutions. Public-private partnerships have begun addressing accessibility challenges, paving the way for future growth.

KEY MARKET PLAYERS

A few of the notable companies operating in the North America vision care market profiled in this report are Johnson & Johnson Vision Care Inc., The Cooper Companies Inc. (CooperVision), EssilorLuxottica, Alcon, Bausch & Lomb, ZEISS International, SynergEyes Inc., and others.

TOP LEADING PLAYERS IN THE MARKET

Johnson & Johnson Vision Care Inc.

Johnson & Johnson Vision is a global leader in vision care, renowned for its innovative product portfolio. The company specializes in contact lenses, intraocular lenses, and surgical equipment, catering to diverse consumer needs. Its strengths include a strong R&D pipeline and strategic collaborations with healthcare providers, ensuring cutting-edge solutions.

Alcon Laboratories

Alcon Laboratories is a pioneer in eye care, offering a comprehensive range of products, from surgical equipment to artificial tears. The company’s focus on sustainability and patient-centric innovation has solidified its market position, making it a trusted name in the industry.

Bausch + Lomb

Bausch + Lomb is a prominent player known for its expertise in corrective lenses and eye health solutions. The company leverages advanced technologies to develop products that enhance user comfort and safety, reinforcing its leadership in the market.

COMPETITION OVERVIEW

The North America vascular stents market is highly competitive, with key players striving to differentiate themselves through innovation and strategic initiatives. Companies like Abbott Laboratories and Boston Scientific dominate the market, leveraging their extensive R&D capabilities to introduce next-generation stents, such as bioresorbable and drug-eluting variants. Regional players also compete by offering cost-effective solutions tailored to local demands. Regulatory approvals and technological advancements play a crucial role in shaping the competitive landscape. Collaborations with healthcare providers and academic institutions further enhance market dynamics, ensuring continuous evolution and growth.

TOP 5 MAJOR ACTIONS TAKEN BY COMPANIES

- In April 2024, Johnson & Johnson Vision launched Acuvue Oasys Max, a new line of contact lenses designed for extended wear, enhancing user comfort.

- In June 2024, Alcon Laboratories partnered with the American Optometric Association to launch a campaign promoting preventive eye care.

- In August 2024, Bausch + Lomb introduced PreserVision AREDS 2 Formula, a dietary supplement aimed at reducing age-related macular degeneration risks.

- In October 2024, CooperVision acquired a startup specializing in smart contact lenses, expanding its product portfolio.

- In December 2024, EssilorLuxottica collaborated with telemedicine platforms to offer virtual eye exams, addressing accessibility challenges.

MARKET SEGMENTATION

This research report on the North America vision care market is segmented and sub-segmented into the following categories.

By Product Type

- Glass Lenses

- Contact Lenses

- Intraocular Lenses

- Contact Solutions

- Lasik Equipment

- Artificial Tears

By Distribution Channel

- Retail Stores

- Online Stores

- Clinics

- Hospitals

By Country

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

1, What is the projected growth of the North America vision care market from 2025 to 2033?

The North America vision care market is expected to grow at a compound annual growth rate (CAGR) of 2.85%, reaching a market value of USD 38.63 billion by 2033 from USD 30.86 billion in 2025

2. What are the key factors driving the growth of the North America vision care market?

Growth is driven by rising awareness of eye health, increasing prevalence of vision-related disorders, advancements in lens technology (e.g., blue-light-blocking glasses and multifocal lenses), and technological innovations such as LASIK surgery and AI-driven diagnostic tools.

3. Which product and distribution channel segments are leading in the North America vision care market?

The contact lenses segment dominated the market in 2024, accounting for 35.3% of total revenue, while artificial tears are the fastest-growing segment with a projected CAGR of 8.2% from 2025 to 2033

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com