Global Patch Management Market Size, Share, Trends & Growth Analysis Report By Vertical (BFSI, Healthcare & Life sciences, Telecommunications and ITES, Government and defense, Education), Application (P.C. Terminal and Mobile terminal), Deployment, End-User & Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) – Industry Forecast (2026 to 2034).

Market Size, 2025

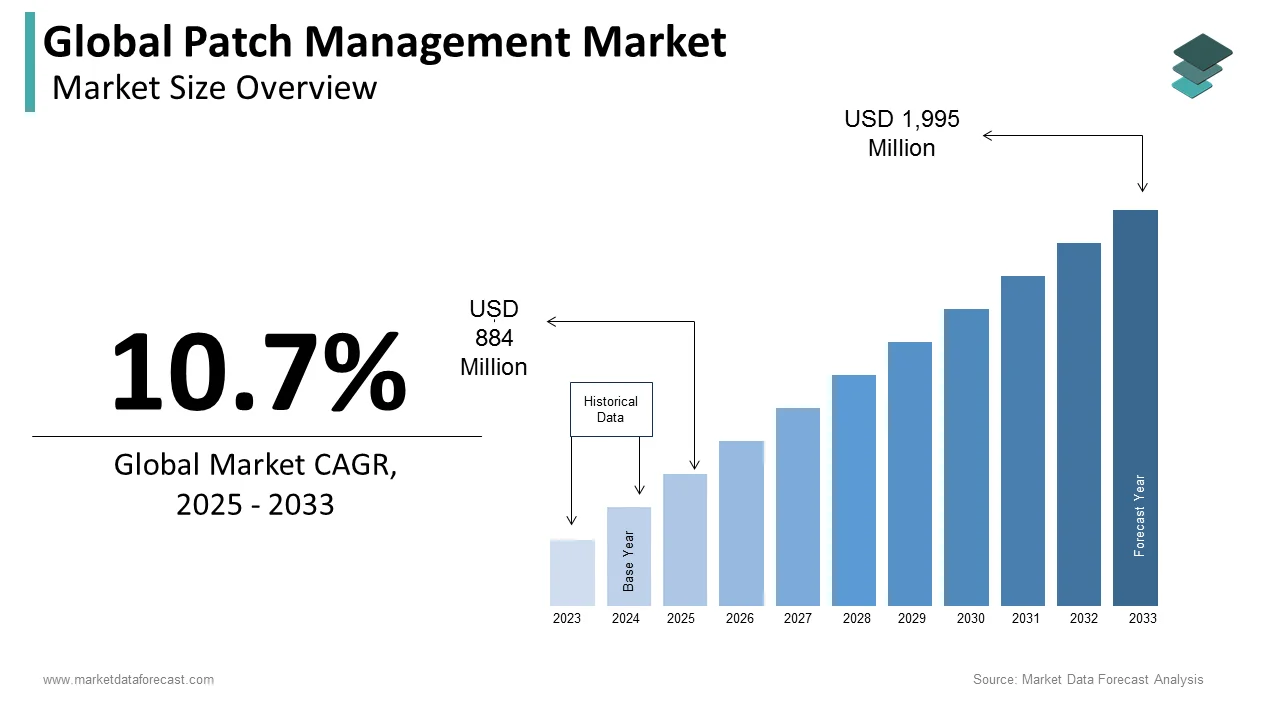

$884 MnMarket Estimate, 2026

$978.5 MnMarket Forecast, 2034

$2207 MnCAGR, 2026–2034

10.7%Global Patch Management Market Report Summary

The global patch management market was valued at USD 884 million in 2025, is estimated to reach USD 978.59 million in 2026, and is projected to reach USD 2,207 million by 2034, growing at a CAGR of 10.7% from 2026 to 2034. Market growth is driven by the increasing frequency of cyber threats, rising need for system security and vulnerability management, and growing adoption of IT infrastructure across enterprises. Patch management solutions help organizations identify, deploy, and manage software updates efficiently, ensuring system security and compliance. The expansion of cloud computing, remote work environments, and regulatory requirements for data protection are further accelerating market growth globally.

Key Market Trends

- Increasing focus on cybersecurity and vulnerability management.

- Rising adoption of automated patch management solutions.

- Growth of cloud computing and remote IT environments.

- Increasing demand for compliance with data protection regulations.

- Expansion of endpoint security and IT asset management solutions.

Segmental Insights

- Based on vertical, the banking, financial services, and insurance (BFSI) segment dominated the global patch management market by capturing 28.9% share in 2025, driven by high security requirements and regulatory compliance.

- Based on application, the PC terminal segment held a dominant share in 2025, supported by widespread use of personal computers across enterprises.

- Based on deployment, the on-premises segment led the market with 55.4% share in 2025, driven by concerns over data security and control.

- Based on end user, the finance segment held the largest share of 26.3% in 2025, due to the critical need for secure IT infrastructure.

Regional Insights

The global patch management market is witnessing steady growth across major regions due to increasing cybersecurity concerns and digital transformation.

- North America led the market in 2025 with 38.4% share, supported by advanced IT infrastructure and high cybersecurity awareness.

- Europe followed with 27.3% share in 2025, driven by strong regulatory frameworks and enterprise adoption.

- Asia-Pacific is expected to witness steady growth due to rapid digital transformation and increasing IT investments.

Competitive Landscape

The global patch management market is highly competitive, with the presence of major software providers and cybersecurity solution companies. Market players are focusing on automation, cloud-based solutions, and integration with broader IT management platforms. Strategic partnerships, product innovation, and expansion of cybersecurity capabilities are shaping competitive dynamics across the market.

Prominent companies operating in the global patch management market include Automox, Autonomic Software, Cisco WebEx, Ecora Software, GFI Software, IBM Software, Ivanti, Kaseya Limited, ManageEngine, NetSPI, Oracle, SolarWinds, Microsoft Corporation, Swipx, Symantec, SysAid Technologies Ltd, and Verismic Software, Inc.

Global Patch Management Market Size

The size of the global patch management market was worth USD 884 million in 2025. The global market is anticipated to grow at a CAGR of 10.7% from 2026 to 2034 and be worth USD 2,207 million by 2034 from USD 978.59 million in 2026.

Patch management is the specialized software solutions and strategic processes designed to identify, acquire, test, and install code changes known as patches into existing computer systems. These updates are critical for correcting security vulnerabilities, fixing bugs, and enhancing functionality across operating systems and applications within an enterprise infrastructure. The urgency for robust patch management has intensified due to the exponential rise in cyber threats that exploit unpatched software flaws. According to the Cybersecurity and Infrastructure Security Agency, a significant majority of successful cyberattacks leverage known vulnerabilities for which patches were already available but not applied. The volume of disclosed vulnerabilities continues to climb, with the National Institute of Standards and Technology recording over 29,000 new common vulnerabilities and exposures in 2023 alone. This deluge of security flaws overwhelms manual IT teams, necessitating automated solutions to maintain compliance and security posture. Furthermore, regulatory frameworks such as the General Data Protection Regulation in Europe and various sector-specific mandates in the United States require organizations to demonstrate timely remediation of security gaps.

MARKET DRIVERS

Escalating Frequency of Zero-Day Exploits and Ransomware Attacks

The alarming increase in zero-day exploits and ransomware campaigns that specifically target unpatched software vulnerabilities is solely fuelling the growth of the patch management market. Cybercriminals have shortened the time between the disclosure of a vulnerability and the deployment of an exploit, often attacking within hours of a patch release or even before one exists. According to the Federal Bureau of Investigation, ransomware attacks caused billions of dollars in losses globally in 2023, with many incidents stemming from failure to apply critical security updates promptly. The sophistication of these attacks means that legacy manual updating processes are insufficient to protect enterprise networks against automated scanning tools used by attackers. The Cybersecurity and Infrastructure Security Agency consistently lists unpatched software as one of the top initial access vectors for malicious actors. Organizations face immense pressure to reduce their window of exposure, driving the adoption of automated patch management solutions that can deploy fixes across thousands of endpoints simultaneously. The financial and reputational devastation resulting from a successful breach forces Chief Information Security Officers to prioritize rapid vulnerability remediation.

Stringent Regulatory Compliance Mandates and Industry Standards

The tightening of global regulatory frameworks and industry standards that mandate rigorous vulnerability management and timely patching protocols is also leveraging the growth of the patch management market. Governments and regulatory bodies worldwide are enforcing stricter data protection laws that hold organizations accountable for security lapses resulting from neglected software updates. The General Data Protection Regulation in the European Union imposes severe fines for data breaches, many of which are attributed to known unpatched vulnerabilities. Similarly, the Payment Card Industry Data Security Standard requires merchants to install vendor-supplied security patches within one month of release to maintain certification. According to the Securities and Exchange Commission, publicly traded companies in the United States must now disclose material cybersecurity incidents and their risk management strategies, including patching procedures, to investors. Non-compliance with these regulations can result in legal penalties, loss of operating licenses, and exclusion from government contracts. The Health Insurance Portability and Accountability Act in the healthcare sector also mandates regular updates to protect patient data. As auditors increasingly scrutinize patch levels during compliance assessments, organizations are compelled to invest in advanced patch management tools that provide detailed reporting and audit trails.

MARKET RESTRAINTS

Operational Disruptions and Compatibility Issues with Legacy Systems

The widespread and effective adoption of patch management solutions is the fear of operational disruptions caused by faulty patches or compatibility conflicts with legacy applications. This factor is majorly hampering the growth of the patch management market. History is replete with instances where a vendor released an update that inadvertently crashed critical business systems or rendered essential software unusable. Many enterprises rely on outdated proprietary software or custom-built applications that are no longer supported by original vendors, making them highly susceptible to breaking when underlying operating systems are updated. The complexity of testing patches across diverse heterogeneous environments containing thousands of different application versions creates a massive bottleneck. The National Institute of Standards and Technology highlights that inadequate testing before deployment is a leading cause of IT outages. Consequently, organizations often adopt a cautious approach, extending the testing cycle and leaving systems vulnerable for longer periods.

Resource Constraints and Shortage of Skilled Cybersecurity Personnel

The acute global shortage of skilled cybersecurity professionals capable of managing complex vulnerability remediation programs effectively is another factor limiting the growth of the patch management market. Implementing and maintaining a robust patch management strategy requires specialized knowledge to prioritize risks, configure policies, and troubleshoot deployment failures. As per data from the International Information System Security Certification Consortium, the global workforce gap in cybersecurity reached 4 million professionals in 2023, leaving many organizations understaffed. Small and medium-sized enterprises often lack the internal expertise to evaluate the vast number of daily vulnerability alerts and determine which patches are critical for their specific environment. The SANS Institute notes that without adequate staffing, even the most sophisticated automated tools cannot be configured optimally, leading to incomplete coverage and persistent security gaps. Furthermore, the high cost of hiring and retaining qualified personnel strains IT budgets, forcing some organizations to rely on basic free tools rather than enterprise-grade solutions.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Predictive Vulnerability Prioritization

The emergence of artificial intelligence and machine learning with various platforms to shift from reactive updating to predictive risk mitigation is expected to substantially elevate new opportunities for the growth of the patch management market. Traditional methods rely on static severity scores like the Common Vulnerability Scoring System, which often fail to reflect the actual context and exploitability of a flaw in a specific environment. AI-driven solutions can analyze vast datasets, including threat intelligence feeds, asset criticality, and active exploitation trends, to predict which vulnerabilities are most likely to be attacked next. These intelligent systems can automatically recommend or even deploy patches for high-risk items without human intervention, freeing up scarce IT resources for strategic tasks. The ability to correlate internal network telemetry with external threat data allows for dynamic policy adjustments that adapt to the evolving threat landscape in real time. Vendors who successfully embed these cognitive capabilities into their offerings will differentiate themselves by delivering measurable risk reduction rather than just compliance metrics. This technological leap addresses the core challenge of alert fatigue and enables businesses to stay ahead of adversaries, opening a lucrative avenue for market expansion and premium pricing models.

Expansion of Unified Endpoint Management for Hybrid Workforces

The permanent shift toward hybrid work models and the proliferation of Internet of Things devices for the evolution of patch management into unified endpoint management solutions is greatly influencing the growth of the patch management market. The traditional perimeter has dissolved, with employees accessing corporate resources from personal devices, home networks, and public Wi Fi, vastly expanding the attack surface. According to the International Data Corporation, the number of connected IoT devices is projected to exceed 29 billion by 2030, many of which run on diverse operating systems requiring distinct patching protocols. Modern patch management platforms that offer cloud native architecture and agentless capabilities can secure devices regardless of their location or network connection status. The ability to manage and patch mobile devices, laptops, servers, and IoT sensors from a single console is becoming a critical requirement for enterprises. The National Security Agency emphasizes that securing remote endpoints is paramount to preventing lateral movement by attackers who compromise less protected devices. Solutions that seamlessly integrate patching with device configuration, inventory management, and threat detection will capture significant market share as organizations seek to simplify their security stacks.

MARKET CHALLENGES

Complexity of Managing Heterogeneous IT Environments and Third-Party Applications

The overwhelming complexity of managing updates across increasingly heterogeneous IT landscapes that include a myriad of third-party applications is one of the key challenges for the growth of the patch management market. While operating system vendors like Microsoft and Linux distributions provide standardized update mechanisms, the ecosystem of third-party software, such as browsers, media players, and productivity tools, lacks a unified patching standard. According to Secunia research, historically and current vulnerability databases, third-party applications now account for a large exploited vulnerabilities than operating systems themselves, yet they often require individual manual updates or proprietary agents. Each application may have its own versioning scheme, installation path, and restart requirements, making automation difficult and error-prone. The sheer number of software titles used in a typical enterprise can exceed several thousand by creating a logistical nightmare for patch managers. The Center for Internet Security notes that failure to patch non OS software is a leading cause of security breaches. Vendors struggle to maintain comprehensive coverage and timely support for this fragmented landscape, often lagging behind vendor releases.

Balancing Speed of Deployment with Rigorous Testing Requirements

The urgent need for rapid patch deployment against the necessity of rigorous testing to prevent system instability is also impeding the growth of the patch management market. The window between vulnerability disclosure and active exploitation has shrunk to days or even hours, demanding immediate action. However, rushing patches into production without adequate testing can lead to catastrophic system failures, data corruption, or application incompatibilities that halt business operations. Organizations must navigate a delicate trade-off where delaying a patch increases security risk while accelerating it increases operational risk. The lack of standardized pre-deployment testing environments that accurately mirror complex production setups exacerbates this dilemma. The National Institute of Standards and Technology advises a structured testing protocol, which inherently consumes time and resources. This tension creates a paradox where security teams push for immediate deployment while operations teams demand extensive validation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Analysed | By Vertical, Application, Deployment, End User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Analysed | North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa |

| Companies Analysed | Automox, Autonomic Software, Cisco WebEx, Ecora Software, GFI Software, IBM Software, Ivanti, Kaseya Limited, ManageEngine, NetSPI, Oracle, SolarWinds, Swipx, Symantec, SysAid Technologies ltd, Verismic Software, Inc |

SEGMENTAL ANALYSIS

By Vertical Insights

The Banking, Financial Services, and Insurance segment was the largest by holding 28.9% in the global patch management market share in 2025, owing to the rigorous regulatory landscape that mandates immediate remediation of security vulnerabilities to protect sensitive customer financial data. Institutions must adhere to strict standards such as the Payment Card Industry Data Security Standard, which requires vendors to install security patches within one month of release. According to the Federal Financial Institutions Examination Council, financial entities face severe sanctions and reputational damage for failing to maintain robust cybersecurity hygiene, including timely patching. The Society for Worldwide Interbank Financial Telecommunication emphasizes that member banks must demonstrate continuous vulnerability management to maintain network access. These compliance requirements force financial institutions to invest heavily in automated patch management solutions that provide auditable trails and guaranteed deployment windows.

The healthcare and life sciences segment is projected to witness the fastest CAGR of 14.2% during the forecast period, with the rapid expansion of the healthcare segment is the explosive growth of Internet of Things devices in clinical settings, ranging from infusion pumps to MRI machines, which often run on outdated operating systems requiring specialized patching. These devices are highly vulnerable to exploitation and can be hijacked to launch attacks or disrupt patient care. According to the Food and Drug Administration, the number of cybersecurity incidents involving medical devices has increased significantly in recent years, prompting stricter guidance on post market security management. The Health Information and Management Systems Society reports that nearly 60% of hospital networks now include thousands of connected medical devices that require regular security updates to prevent compromise. The unique complexity of managing firmware and software updates across diverse medical equipment drives the demand for specialized patch management platforms tailored to healthcare environments.

By Application Insights

The P.C. terminal segment was the largest by holding aa dominant share of the global patch management market in 2025, owing to the overwhelming prevalence of personal computers as the standard work device for employees across all industries globally. Despite the rise of mobile devices, the majority of business applications, data processing, and communication still occur on Windows, macOS, and Linux-based desktops and laptops. Hundreds of millions of PC units are shipped annually for commercial use, creating a massive installed base that requires consistent security updates. The National Institute of Standards and Technology identifies unpatched workstation operating systems as the most frequent vector for malware infiltration and lateral movement within corporate networks. The complexity of managing diverse operating system versions and third-party applications installed on these terminals necessitates sophisticated automated patching tools.

The mobile terminal segment is likely to register the fastest CAGR of 16.5% during the forecast period, with the permanent shift toward hybrid work models where employees rely heavily on personal mobile devices to access sensitive corporate resources. The traditional network perimeter has dissolved, leaving mobile endpoints often outside the protection of corporate firewalls and requiring direct security intervention. The National Security Agency emphasizes that mobile devices are increasingly targeted by state-sponsored actors due to their constant connectivity and rich data stores. Managing patches across thousands of diverse mobile models and operating system versions presents a unique challenge that traditional PC tools cannot address. The need for mobile-specific patch management capabilities that can operate over cellular networks and enforce compliance without user intervention is driving urgent adoption.

By Deployment Insights

The on-premises deployment segment was the largest by holding 55.4% of the global patch management market share in 2025, with the mandatory requirement for many highly regulated industries to keep security data and patch management logs within their own physical boundaries to comply with data sovereignty laws. Sectors such as government, defense, and banking often face regulations that prohibit sensitive vulnerability data from residing on public cloud servers managed by third parties. The federal agencies and contractors must adhere to strict guidelines regarding the storage and processing of security information, which often necessitates on-premises solutions. The General Data Protection Regulation in Europe also imposes constraints on cross-border data transfers, encouraging organizations to maintain local control over their security operations. The ability to audit every aspect of the patching process internally without relying on external vendors provides the assurance needed for compliance officers.

The cloud deployment segment is expected to witness the fastest CAGR of 18.3% in the coming years, with the need to secure employees and devices located outside the traditional corporate network, a scenario where on-premises tools struggle to maintain visibility and connectivity. According to the International Data Corporation, the number of remote workers globally has stabilized at historically high levels, creating a persistent demand for cloud native security solutions. Cloud platforms allow IT administrators to push patches to any device anywhere in the world instantly without complex VPN configurations or firewall adjustments. The Federal Bureau of Investigation warns that remote workers are prime targets for attacks, necessitating real-time protection that only cloud-delivered updates can provide. The ability to scale resources dynamically based on the number of active devices without purchasing additional hardware makes cloud deployment highly attractive.

By End User Insights

The finance end-user segment was the largest by occupying 26.3% of the global patch management market share in 2025, with the unparalleled motivation for cybercriminals to target financial institutions due to the potential for direct financial theft and lucrative ransom payments. According to the Association of Certified Fraud Examiners, the financial services industry suffers the highest median loss per fraud case of any sector, which often reaches millions of dollars per incident. The Cybersecurity and Infrastructure Security Agency identifies the financial sector as a priority target for state-sponsored groups and organized crime syndicates who actively scan for unpatched vulnerabilities to gain entry. The existential threat posed by these attacks forces financial entities to maintain the most aggressive and well-funded patch management programs in the market. The inability to tolerate downtime or data loss means that finance organizations invest disproportionately in advanced automated patching solutions to minimize their window of exposure.

The healthcare end user segment is likely to grow at the fastest CAGR of 15.8% during the forecast period, with the rapid expansion of the Healthcare segment is the massive influx of connected medical devices and the complete digitization of patient records, which have vastly expanded the attack surface for cyber threats. Modern hospitals rely on thousands of IoT devices such as pacemakers, insulin pumps, and imaging systems that often run on legacy operating systems and are difficult to patch using traditional methods. According to the Food and Drug Administration, the number of cybersecurity recalls and safety communications related to medical devices has risen sharply, highlighting the urgent need for specialized patching strategies. The transition to fully electronic health records means that a single breach can expose the sensitive data of millions of patients. The complexity of patching these diverse and critical devices without disrupting patient care drives the demand for advanced healthcare-specific patch management solutions.

REGIONAL ANALYSIS

North America Patch Management Market Analysis

North America was the largest contributor in the global patch management market by capturing 38.4% of the market share in 2025, with the highest concentration of Fortune 500 companies, advanced technological infrastructure, and the most stringent cybersecurity regulations globally. The rigorous enforcement of sector-specific regulations, such as the Health Insurance Portability and Accountability Act in healthcare and the Gramm-Leach-Bliley Act in finance, mandates robust vulnerability management. According to the Cybersecurity and Infrastructure Security Agency, the volume of cyber incidents reported by US entities continues to rise, prompting organizations to prioritize automated patching.

Europe Patch Management Market Analysis

Europe patch management market held second position by holding 27.3% of the share in 2025, with a diverse mix of highly regulated industries in Western Europe and rapidly modernizing IT infrastructures in Eastern Europe, all contributing to steady demand. The increasing frequency of state-sponsored cyberattacks targeting infrastructure and government agencies is boosting the growth of the market. The number of significant cyber incidents reported across member states has grown substantially, driving investments in defensive technologies. Furthermore, the rising adoption of remote work models across countries like Germany, France, and the UK has expanded the attack surface, necessitating cloud-based patch management solutions.

Asia-Pacific Patch Management Market Analysis

The Asia-Pacific patch management market is anticipated to have steady growth opportunities in the coming years, with the rapid digital transformation, the explosion of mobile internet usage, and increasing government focus on cybersecurity sovereignty. As per reports from the Asian Pacific Computer Emergency Response Team, the region experiences a disproportionate share of global malware and phishing attacks, driving urgent demand for security solutions. Governments are increasingly enacting local data protection laws by forcing organizations to adopt formal patch management processes. The widespread adoption of Bring Your Own Device policies in the region's vibrant startup ecosystem creates a complex endpoint environment that requires advanced mobile patching capabilities.

Latin America Patch Management Market Analysis

Latin America patch management market growth is propelled by a growing awareness of cybersecurity risks and a gradual shift from reactive to proactive security postures. The exponential increase in ransomware attacks targeting businesses in Brazil, Mexico, and Colombia has highlighted the importance of timely vulnerability remediation. Cybercrime costs the Latin American economy billions of dollars annually, prompting governments and private sectors to invest more heavily in defense mechanisms. The implementation of new data protection laws, such as the Lei Geral de Protecao de Dados in Brazil, is forcing organizations to formalize their security practices, including patch management, to avoid heavy fines. The expanding banking sector and the rapid adoption of fintech solutions have increased the attack surface, necessitating robust security controls. Furthermore, international corporations operating in the region are extending their global security policies to local branches, driving the uptake of enterprise-grade patching solutions.

Middle East and Africa Patch Management Market Analysis

The Middle East and Africa patch management market growth is driven by the strategic national vision of countries like Saudi Arabia and the United Arab Emirates to become global digital hubs, which includes massive investments in cybersecurity infrastructure and talent development. As per data from the International Telecommunication Union, these nations are implementing rigorous national cybersecurity frameworks that mandate regular patching for sectors, including energy and finance. The region faces sophisticated cyber threats from state actors and criminal groups targeting oil and gas infrastructure, driving demand for high-end patch management solutions. In Africa, the rapid growth of mobile money services and digital banking has created a new frontier for cybercrime, prompting regulators to introduce stricter security guidelines. Initiatives by the African Union to harmonize cybersecurity laws across the continent are beginning to drive awareness and adoption of basic patch management practices.

COMPETITIVE LANDSCAPE

The competition within the patch management market is characterized by intense rivalry between established legacy vendors and agile cloud native startups striving to redefine how organizations handle vulnerability remediation. Major competitors differentiate themselves through the breadth of their third-party application coverage, the speed of their update deployment, and the sophistication of their risk prioritization algorithms. The landscape features a constant race to integrate artificial intelligence and machine learning capabilities that can predict which vulnerabilities are most likely to be exploited and automate the fixing process. Companies frequently engage in strategic acquisitions to expand their endpoint management portfolios and offer unified solutions that combine patching with configuration management and asset discovery. Pricing pressure from open source alternatives and built-in operating system tools compels commercial vendors to demonstrate clear value through superior reporting and compliance features.

KEY MARKET PLAYERS

Companies that are playing a dominating role in the global patch management market, as analyzed in this report, are

- Automox

- Autonomic Software

- Cisco WebEx

- Ecora Software

- GFI Software

- IBM Software

- Ivanti

- Kaseya Limited

- ManageEngine

- NetSPI

- Oracle

- SolarWinds

- Microsoft Corporation

- Swipx

- Symantec

- SysAid Technologies Ltd

- Verismic Software, Inc.

TOP PLAYERS IN THE MARKET

- Microsoft Corporation stands as a foundational pillar in the global patch management landscape due to its ownership of the Windows operating system, which powers the vast majority of enterprise endpoints worldwide. The company provides native tools like Windows Server Update Services and integrates advanced patching capabilities directly into its Microsoft Endpoint Configuration Manager and Intune platforms. Microsoft recently strengthened its market position by enhancing its cloud-based security suite to include automated vulnerability assessment and remediation features driven by artificial intelligence. The firm actively collaborates with the global security community to identify zero-day threats and rapidly deploy out-of-band updates to protect users. These strategic initiatives allow the company to define industry standards for update delivery and secure its role as an indispensable partner for enterprises managing complex IT environments globally.

- Ivanti Inc maintains a robust presence in the patch management sector by offering comprehensive solutions that extend beyond operating systems to cover thousands of third-party applications and mobile devices. The company is deeply involved in helping organizations automate the entire lifecycle of vulnerability management from discovery to verification across hybrid infrastructures. Recent actions include the integration of advanced risk-based prioritization engines that leverage real-time threat intelligence to help customers focus on the most critical vulnerabilities first. Ivanti has also expanded its unified endpoint management capabilities to support remote workforces by enabling secure patching over the internet without requiring virtual private network connections. The organization prioritizes strategic acquisitions to broaden its portfolio and enhance its analytics dashboard for better compliance reporting.

- Automox Inc operates as a major contributor to the patch management market via its cloud native platform designed specifically for modern enterprises seeking agility and simplicity in their security operations. The company offers a software-as-a-service solution that enables IT teams to patch operating systems and third-party applications across Windows, Mac, and Linux environments from a single console. Recent efforts by Automox have centered on expanding its policy-based automation features that allow organizations to enforce security standards without heavy administrative overhead. The firm has launched new integrations with popular IT service management tools to streamline workflow and improve visibility into patch compliance status. Additionally, Automox actively engages in community-driven initiatives to share best practices for cloud security and rapid response to emerging threats.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the patch management market primarily employ strategies focused on cloud migration and artificial intelligence integration to enhance automation and reduce manual effort. Companies heavily invest in developing cloud native platforms that allow for seamless management of remote and distributed endpoints without complex infrastructure. Mergers and acquisitions are frequent as larger entities seek to absorb specialized technologies for third-party application support or mobile device management. Another prevalent strategy involves leveraging real-time threat intelligence feeds to prioritize vulnerabilities based on active exploitation rather than static severity scores. Manufacturers also focus on forming strategic partnerships with IT service management vendors to create unified workflows that simplify compliance reporting. Enhancing user experience through intuitive dashboards and one-click remediation options is a critical priority to address the shortage of skilled security personnel. Furthermore, companies are increasingly adopting subscription-based pricing models to make enterprise-grade security accessible to smaller organizations.

MARKET SEGMENTATION

This research report on the global patch management market has been segmented and sub-segmented based on vertical, application, deployment, end user, and region.

By Vertical

- BFSI

- Healthcare & Life sciences

- Telecommunications and ITES

- Government and defense

- Education

By Application

- P.C. Terminal

- Mobile terminal

By Deployment

- On-Premises

- Cloud

By End User

- Healthcare

- Government

- Education

- Finance

- Legal

- Manufacturing

- Transportation

By Region

- North America

- The U.S.

- Canada

- Rest of North America

- Europe

- UK

- France

- Spain

- Germany

- Italy

- Rest of EU

- Asia Pacific

- India

- China

- Japan

- South Korea

- Australia & New Zealand

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Argentina

- Chile

- Rest of LATAM

- Middle East

- Africa

Frequently Asked Questions

1. Which segments lead the patch management market?

Software solutions hold the largest revenue share in the patch management market, with services registering the fastest growth due to managed patching demands

2. How does cloud adoption affect the patch management market?

Growing cloud infrastructure adoption drives the patch management market to focus on cloud-based patching for better scalability and security

3. What are key industries driving the patch management market?

IT, BFSI, healthcare, manufacturing, and government sectors drive demand in the patch management market, emphasizing regulatory compliance

4. Which countries dominate the patch management market?

France leads with the highest projected CAGR, while the UK and Germany also hold strong positions in the patch management market

5. How important is automated patching in the patch management market?

Automated patching is critical, improving efficiency and threat response times, thus expanding the patch management market significantly

6. What role does regulatory compliance play in the patch management market?

Compliance with GDPR, ENISA, and ISO standards drives adoption in the europe patch management market to meet cybersecurity mandates

7. How do services contribute to the patch management market?

Managed patch services are growing fastest in the patch management market, relieving enterprises of patch deployment burdens

8. What challenges does the patch management market face?

Challenges include complex IT environments and cost sensitivity but are mitigated by cloud and automated patching solutions in the patch management market

9. How does threat landscape influence the patch management market?

Increasing cyber threats prompt organizations to prioritize patching, boosting growth of the patch management market

10. How do hybrid environments affect the patch management market?

Hybrid IT environments increase patch complexity, driving demand for sophisticated patch management in the patch management market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com