Global Protein Chip Market Size, Share, Trends & Growth Forecast Report By Technology (Analytical Microarrays, Functional Protein Microarrays and Reverse Phase Protein Microarray), Application (Diagnostics, Proteomics, Protein Functional Analysis and Antibody Characterization) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Market Size, 2025

$3.92 BnMarket Estimate, 2026

$4.63 BnMarket Forecast, 2034

$17.67 BnCAGR, 2026–2034

18.21%Global Protein Chip Market Report Summary

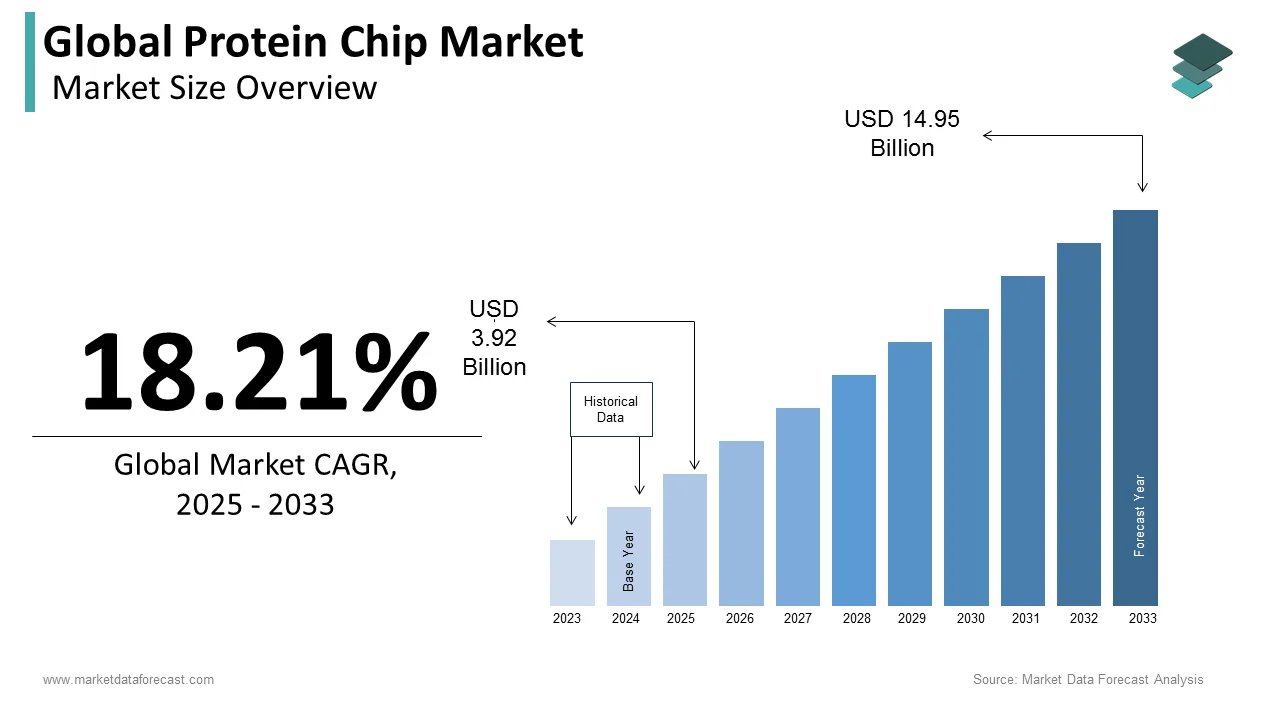

The global protein chip market was valued at USD 3.92 billion in 2025, is estimated to reach USD 4.63 billion in 2026, and is projected to reach USD 17.67 billion by 2034, growing at a CAGR of 18.21% from 2026 to 2034. Market growth is driven by increasing demand for high-throughput proteomics, rising focus on personalized medicine, and advancements in biomarker discovery. Protein chips enable rapid analysis of protein interactions, expression levels, and disease markers, making them essential tools in diagnostics and drug development. The expansion of precision medicine, growing research in genomics and proteomics, and increasing investments in biotechnology are further accelerating market growth globally.

Key Market Trends

- Increasing adoption of proteomics and biomarker discovery technologies.

- Rising demand for high-throughput and miniaturized diagnostic tools.

- Growing focus on personalized and precision medicine.

- Expansion of drug discovery and development activities.

- Advancements in microarray and lab-on-a-chip technologies.

Segmental Insights

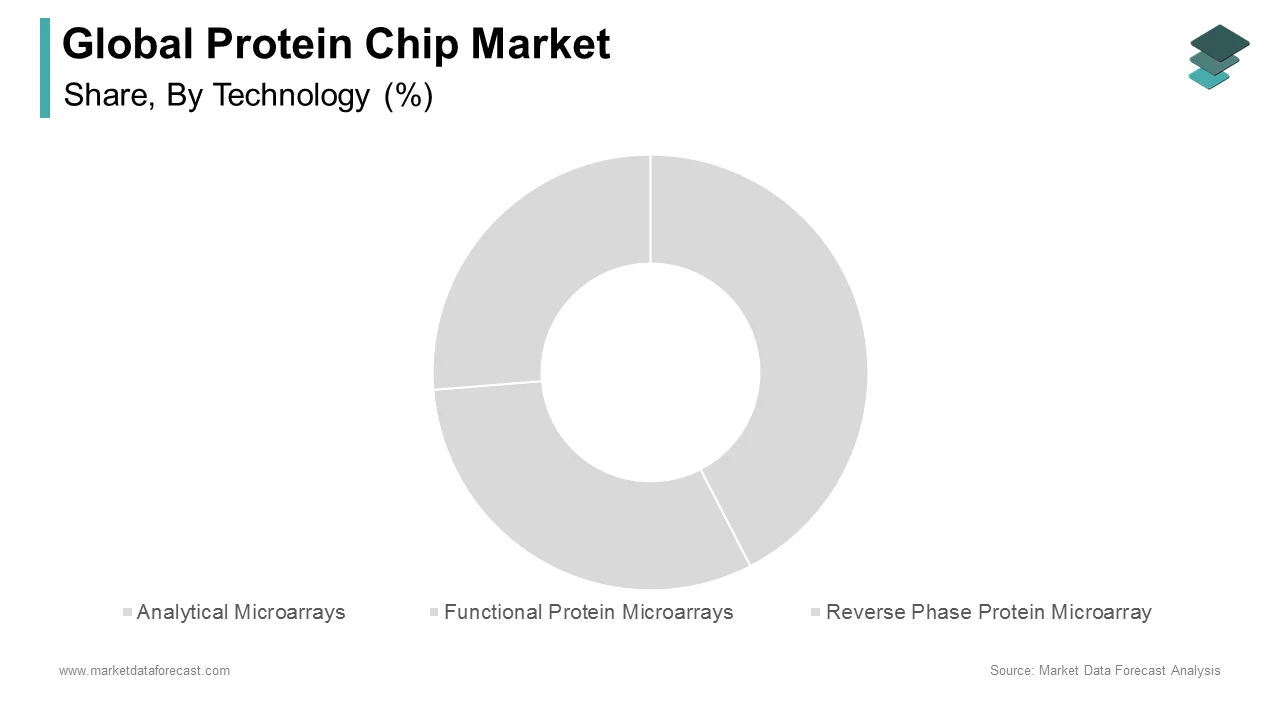

- Based on technology, the analytical microarrays segment dominated the global protein chip market by capturing 40.9% share in 2025, driven by its widespread application in protein analysis and diagnostics.

- Based on application, the diagnostics segment led the market with 36.6% share in 2025, supported by increasing use in disease detection and clinical testing.

Regional Insights

The global protein chip market is witnessing strong growth across major regions due to increasing research activities and technological advancements.

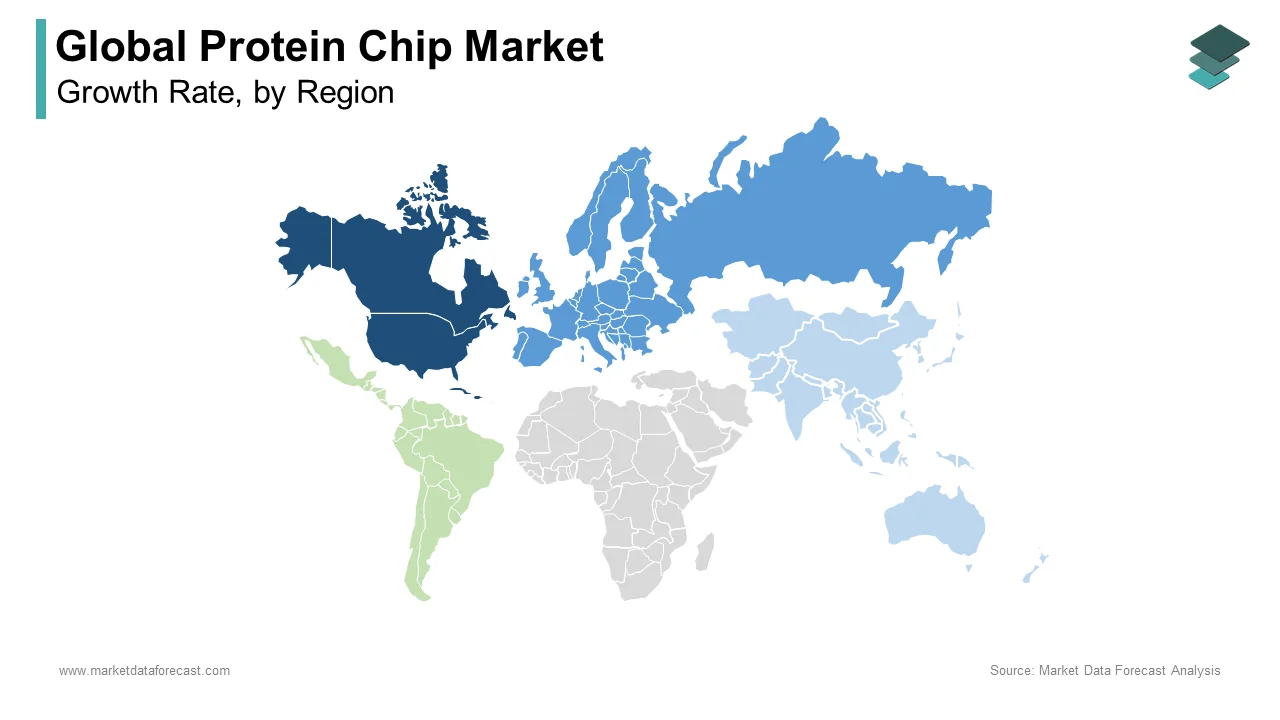

- North America led the market in 2025 with 35.5% share, supported by strong biotechnology research and advanced healthcare infrastructure.

- Europe holds a significant share, driven by increasing investments in life sciences and research initiatives.

- Asia-Pacific is expected to register the fastest CAGR due to growing biotechnology sector, increasing healthcare investments, and expanding research capabilities.

Competitive Landscape

The global protein chip market is highly competitive, with the presence of major biotechnology and life sciences companies. Market players are focusing on innovation, expanding product portfolios, and enhancing research capabilities. Strategic collaborations, acquisitions, and investments in advanced technologies are shaping competitive dynamics across the market.

Prominent companies operating in the global protein chip market include SEQUENOM, Inc., Sigma Aldrich Corporation, Affymetrix, Inc., Merck KGaA, Thermo Fisher Scientific, EMD Millipore, Illumina, Inc., Life Technologies Corporation, and Agilent Technologies.

Global Protein Chip Market Size

The size of the global protein chip market was worth USD 3.92 billion in 2025. The global market is anticipated to grow at a CAGR of 18.21% from 2026 to 2034 and be worth USD 17.67 billion by 2034 from USD 4.63 billion in 2026.

Protein chip represents a specialized sector within the broader proteomics landscape, which focuses on high-throughput platforms that enable the simultaneous analysis of thousands of proteins. These biochips function by immobilizing specific proteins or antibodies on a solid substrate to detect interactions, expression levels, and functional activities within biological samples. As of 2026, this technology serves as a critical enabler for biomarker discovery, drug development, and clinical diagnostics, offering superior multiplexing capabilities compared to traditional enzyme-linked immunosorbent assays. Unlike genomic tools that analyze static DNA sequences, protein chips provide dynamic insights into cellular states since protein levels fluctuate in response to disease progression and therapeutic intervention. As per the UK Biobank, large-scale initiatives are underway to analyze proteins in hundreds of thousands of participants, illustrating the massive scale of current proteomic efforts. This surge in studies underscores the transition from research-grade applications to clinical utility, where protein chips facilitate the identification of novel therapeutic targets for complex conditions such as cancer and neurodegenerative disorders. The technology continues to evolve with improvements in surface chemistry and detection sensitivity, positioning it as an indispensable tool for modern biomedical research and personalized healthcare strategies.

MARKET DRIVERS

Escalating Global Burden of Chronic Diseases Demands Advanced Diagnostic Solutions

The rising prevalence of chronic diseases globally is primarily driving the growth of the global protein chip market. According to the World Health Organization, chronic conditions such as cardiovascular diseases, cancer, and diabetes account for the majority of deaths worldwide, which is creating an urgent need for early and accurate diagnostic tools. Protein chips address this demand by enabling the simultaneous detection of multiple biomarkers associated with these pathologies in a single assay, significantly reducing the time and sample volume required for diagnosis. For instance, the ability to profile hundreds of cytokines and signalling proteins allows clinicians to identify specific disease subtypes and monitor treatment responses with precision. As the global population ages, the incidence of age-related disorders continues to climb, further intensifying the requirement for high-throughput screening methods. As per research findings, early detection of biomarkers through protein microarrays has been shown to improve patient survival in oncology applications. Consequently, healthcare systems are increasingly integrating protein chip-based diagnostics into routine screening protocols to manage the growing patient load efficiently. This shift is supported by substantial investments in healthcare infrastructure, with governments allocating significant funding toward preventive medicine initiatives that rely on advanced proteomic technologies to mitigate the economic impact of chronic disease management.

Substantial Increase in Proteomics Research Funding Accelerates Biomarker Discovery

Significant increments in research and development funding from both public and private sectors are propelling the growth of the protein chip market. The global proteomics market is projected to expand at a compound annual growth rate of 13% from 2025 to 2030, reaching a valuation of 57.2 billion USD. This financial momentum is largely attributed to strategic grants aimed at unraveling the human proteome and identifying novel biomarkers for untreatable diseases. As per the UK Biobank, large-scale studies are underway to measure thousands of proteins across hundreds of thousands of samples, demonstrating the scale of contemporary investment. Similarly, foundations such as the Michael J Fox Foundation have committed substantial funding to accelerate biomarker research in neurodegenerative diseases using advanced proteomic tools. These funds facilitate the development of next-generation protein chips with enhanced sensitivity and specificity, allowing researchers to detect low-abundance proteins that were previously undetectable. Academic institutions and biotechnology firms are leveraging these resources to validate protein signatures for various conditions, thereby shortening the translational gap between laboratory findings and clinical applications. The influx of capital also supports the standardization of assay protocols, which is essential for regulatory approval and widespread commercial adoption. As venture capital continues to flow into proteomics startups, the market witnesses a rapid proliferation of innovative chip designs tailored for specific therapeutic areas.

MARKET RESTRAINTS

High Manufacturing and Development Costs Limit Market Accessibility

The exorbitant cost associated with the development and manufacturing of protein chips remains a significant barrier to their widespread adoption and hampers the global market growth. Producing high-quality protein microarrays requires sophisticated fabrication facilities, expensive reagents, and highly specialized antibodies, which collectively drive up the final price of the product. The high cost of microarray production and validation restricts revenue growth and limits access for smaller research laboratories and developing nations. Unlike DNA chips, which benefit from amplification techniques to reduce material costs, proteins cannot be amplified, necessitating larger quantities of pure sample for each assay. This inherent limitation increases the cost per test, making large-scale screening programs financially prohibitive for many healthcare providers. Furthermore, the need for a custom array design for specific research questions adds to the expense, as each new target requires unique optimization of immobilization chemistry and detection parameters. The financial burden extends to the end user, where the cost of proprietary scanners and analysis software can be very high, creating a high entry threshold for potential adopters. Consequently, many institutions continue to rely on lower-cost, lower-throughput methods such as western blotting or standard ELISA, despite the superior data density offered by protein chips. Until manufacturing processes become more automated and economies of scale are achieved, cost will remain a persistent restraint on market expansion.

Technical Limitations in Sensitivity and Reproducibility Hinder Clinical Validation

Persistent technical challenges regarding sensitivity and reproducibility are also hindering the expansion of the protein chip market. Proteins are inherently unstable molecules that are susceptible to denaturation due to minor changes in pH, temperature, or surface interaction, which can compromise the integrity of the assay. As noted by News Medical, variability in protein folding and the lack of universal amplification methods lead to significant between-run variations and false negative results. The dynamic range of protein concentrations in biological fluids spans several orders of magnitude, yet many current chip platforms struggle to detect low-abundance biomarkers in the presence of high-abundance proteins. This limitation reduces the reliability of the data generated, making it difficult to validate findings for regulatory approval. Additionally, the absence of standardized protocols for sample preparation and data analysis contributes to inconsistent results across different laboratories. As per published studies, reproducibility rates for certain protein array experiments have been shown to fall below acceptable thresholds, raising concerns about their suitability for diagnostic decision making. The complexity of protein interactions further complicates assay design, as non-specific binding can generate high background noise that obscures true signals. Until these technical hurdles are overcome through advancements in surface chemistry and detection algorithms, the transition of protein chips from research tools to approved clinical diagnostics will remain sluggish.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence Enhances Data Analysis and Predictive Capabilities

The convergence of artificial intelligence with protein chip technology is a promising opportunity for the protein chip market. AI algorithms can process the vast datasets generated by high-density protein arrays to identify complex patterns and correlations that are imperceptible to human analysts. According to Biomedicine and Pharmacotherapy, the integration of machine learning models with biochip data enables predictive analytics for personalized medicine, potentially revolutionizing disease diagnosis in the near future. Deep learning techniques are particularly effective in deconvoluting noisy signals and improving the accuracy of biomarker identification, thereby addressing some of the sensitivity issues inherent in traditional methods. This synergy allows for the development of smart diagnostic platforms that can provide real-time risk assessments and therapeutic recommendations based on an individual's proteomic profile. Pharmaceutical companies are increasingly adopting AI-driven protein chip analysis to accelerate drug discovery pipelines, reducing the time required to identify viable drug targets. The ability to model protein structure and interaction networks using AI also opens new avenues for understanding disease mechanisms at a molecular level. As computational power increases and algorithms become more sophisticated, the value proposition of protein chips will shift from mere data generation to actionable clinical intelligence. This technological fusion is expected to attract significant investment and drive the adoption of protein chips in precision oncology and rare disease diagnostics.

Expansion of Point of Care Testing Applications Drives Market Penetration

The miniaturization of protein chip technology offers substantial opportunities for expansion into the point-of-care testing sector. Traditional proteomic analysis requires centralized laboratories and extended turnaround times, but emerging lab-on-a-chip devices enable rapid, on-site diagnostics suitable for clinical settings and remote locations. Advances in microfluidics and sensor technology have allowed for the development of portable protein chips that can deliver results in minutes rather than days. This capability is particularly valuable for managing infectious disease outbreaks and monitoring chronic conditions in resource-limited environments where access to advanced medical infrastructure is scarce. The global push towards decentralized healthcare models supports the deployment of these devices, with demand for rapid diagnostic tools expected to rise significantly. Manufacturers are focusing on creating user-friendly interfaces and disposable chip formats that reduce the need for specialized training and expensive equipment. The potential to integrate these devices with smartphone applications for data transmission and telemedicine further enhances their utility. As regulatory bodies streamline approval pathways for point-of-care diagnostics, protein chip manufacturers are well-positioned to capture a growing share of the immediate testing market. This shift not only broadens the customer base but also creates new revenue streams through recurring sales of consumable chip cartridges.

MARKET CHALLENGES

Lack of Standardization Impedes Regulatory Approval and Commercialization

The absence of universally accepted standards for protein chip fabrication and data interpretation is challenging the global market growth. Unlike genomic sequencing, which has benefited from established consensus protocols, the proteomics field suffers from a fragmentation of methodologies regarding antibody selection, surface immobilization, and signal detection. According to Growth Plus Reports, issues related to standardization and accuracy restrict the revenue growth of the global protein microarray market by hindering the comparison of results across different studies and platforms. This lack of harmonization complicates the regulatory approval process, as agencies require rigorous validation and reproducibility data that is difficult to generate without standardized controls. Variability in reagent quality and lot-to-lot differences further exacerbate the problem, leading to inconsistencies that can invalidate clinical trials. The industry also faces challenges in establishing reference ranges for protein biomarkers, which are essential for diagnostic interpretation. Without a unified framework for quality control, manufacturers struggle to gain the trust of clinicians and payers who demand reliable and consistent performance. Efforts by consortia to develop common standards are ongoing, but progress is slow due to the diverse nature of protein targets and application requirements. Until a robust standardization ecosystem is established, the pathway to widespread clinical adoption will remain obstructed by regulatory uncertainty and skepticism.

Scarcity of High-Quality Specific Antibodies Limits Assay Development

The availability of high-affinity and highly specific antibodies remains a critical bottleneck in the protein chip market. Antibodies serve as the primary capture agents in most protein array formats, yet producing them for thousands of distinct protein targets is a time-consuming and labor-intensive process. As highlighted in Drug Discovery World, the production of antibodies is often the rate-limiting step in biochip content creation, greatly limiting the supply of comprehensive arrays. Many commercially available antibodies suffer from cross-reactivity or low specificity, which leads to false positive results and compromised data integrity. The human proteome consists of tens of thousands of proteins, along with numerous splice variants and post translational modifications, each requiring unique recognition elements that are not always available. The cost of generating and validating new antibodies can be very high, making the creation of whole proteome chips economically challenging. Furthermore, the stability of antibodies on chip surfaces varies, with some losing activity over time or under specific storage conditions. This scarcity forces researchers to limit the scope of their assays to well-characterized proteins, thereby missing potential novel biomarkers. While recombinant antibody technologies and aptamers offer potential solutions, they have not yet fully replaced traditional antibodies in terms of performance and market acceptance. Overcoming this supply chain constraint is essential for unlocking the full potential of protein chip technology.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | SEQUENOM, Inc., Sigma Aldrich Corporation, Affymetrix, Inc., EMD Millipore, Illumina, Inc., Life Technologies Corporation, and Agilent Technologies. |

SEGMENTAL ANALYSIS

By Technology Insights

The analytical microarrays segment dominated the market by accounting for 40.9% of the global market share in 2025. The dominance of the analytical microarrays segment in the global market is driven by the segment's critical role in high-throughput biomarker discovery and its established utility in clinical diagnostics, where quantification of specific protein targets is paramount. The unparalleled ability of analytical microarrays to screen thousands of samples for specific biomarkers with high sensitivity, which is a capability essential for modern precision medicine, is further driving the dominating position of the segment in the global market. According to the National Institutes of Health, a majority of proteomic studies aimed at identifying cancer biomarkers utilize analytical microarray platforms due to their robustness and reproducibility. These arrays allow researchers to measure the expression levels of hundreds of proteins simultaneously from minute sample volumes, significantly accelerating the timeline for drug target validation. As per the World Health Organization, the global burden of cancer is expected to rise substantially, necessitating scalable diagnostic tools. Pharmaceutical companies rely heavily on this technology during the early phases of drug development to stratify patient populations, a process that has been shown to reduce clinical trial failure rates. The maturity of the technology means that protocols are well standardized, reducing the barrier to entry for laboratories compared to newer functional assays. Consequently, the widespread adoption in both academic research institutions and commercial diagnostic labs ensures that analytical microarrays remain the revenue backbone of the technology sector.

On the other hand, the functional protein microarrays segment is projected to register the highest CAGR of 15.1% over the forecast period in the global market, owing to the increasing need to understand protein-protein interactions, enzyme-substrate relationships, and post-translational modifications, which are critical for unraveling complex biological pathways that analytical arrays cannot fully address. The scientific community's shifting focus from mere protein quantification to understanding dynamic protein functions and interaction networks is also favouring the expansion of the functional protein microarray segment in the global market. As per Nature Methods, the number of published studies utilizing functional arrays to map protein interactions has been rising significantly in recent years. These arrays display full-length, correctly folded proteins, enabling the detection of binding events with DNA, RNA, lipids, and other proteins, which is indispensable for systems biology research. The Human Proteome Project has emphasized that understanding these interactions is key to deciphering the mechanisms of diseases like Alzheimer's and diabetes, where pathway dysregulation plays a central role. Pharmaceutical companies are increasingly deploying functional arrays in their target identification pipelines to discover novel drug binding sites, a strategy that has shortened the lead optimization phase. The ability to study post translational modifications such as phosphorylation and glycosylation in a high-throughput manner provides insights that are unattainable with genomic or simple analytical approaches. As the complexity of biological questions increases, the unique capability of functional arrays to provide mechanistic insights ensures their status as the fastest-growing technology segment.

By Application Insights

The diagnostics segment led the market by capturing 36.6% of the global market share in 2025. The leading position of the diagnostics segment in the global market is primarily attributed to the critical role of protein chips in early disease detection, patient stratification, and monitoring therapeutic efficacy across a wide spectrum of medical conditions. The global surge in chronic diseases that demands efficient and accurate early detection methods to improve patient outcomes and reduce healthcare costs is also contributing to the dominance of the diagnostics segment in the global market. According to the Centers for Disease Control and Prevention, chronic diseases affect a large proportion of adults in the United States, creating a massive volume of patients requiring regular monitoring. Protein chips offer a multiplexed approach that can detect multiple disease-specific biomarkers from a single drop of blood, significantly enhancing diagnostic speed and accuracy compared to single-analyte tests. For example, cardiac protein chips can simultaneously measure multiple markers to diagnose myocardial infarction rapidly, a capability that has proven life-saving. As per the World Economic Forum, early diagnosis through advanced proteomics is expected to generate substantial economic savings globally by preventing disease progression. Furthermore, the integration of protein chips into newborn screening programs for metabolic disorders is expanding their reach. The ability to provide comprehensive diagnostic profiles makes protein chips an indispensable asset in modern clinical laboratories, securing their position as the leading application segment.

On the other side, the proteomics research segment is anticipated to grow at the fastest CAGR of 16.1% over the forecast period, owing to the exponential increase in fundamental biological research aimed at decoding the human proteome and understanding the molecular basis of life. The unprecedented level of funding directed towards large-scale proteome mapping initiatives by governments and private organizations globally is also propelling the expansion of the proteomics segment in the global market. As highlighted by the European Commission, the Horizon Europe program has allocated significant funding specifically for proteomics research projects, aiming to create a comprehensive atlas of human proteins. Similarly, the National Human Genome Research Institute in the US has expanded its mandate to include collaborative proteome initiatives, attracting participation from numerous research institutions worldwide. These massive funding pools enable researchers to purchase high-end protein chip systems and consumables in bulk, directly boosting market revenue. The initiative to map the proteomes of various model organisms and disease states requires the high-throughput capabilities that only protein chips can provide. Academic publications in the field of proteomics have surged in recent years, reflecting the intensity of research activity. Private philanthropy is also playing a crucial role, with foundations investing heavily in proteomic research to combat neglected diseases. This concerted financial push ensures a steady demand for protein chip technologies, making proteomics research the most dynamic growth segment in the market.

REGIONAL ANALYSIS

North America Protein Chip Market Analysis

North America dominated the protein chip market in 2025 with 35.5% of the worldwide market share. The leading position of North America in the global market is attributed to its robust healthcare infrastructure, high concentration of top-tier research institutions, and the presence of major market players driving innovation. The United States serves as the epicenter of this activity, hosting the headquarters of key industry leaders such as Thermo Fisher Scientific and Agilent Technologies. According to the National Science Foundation, the US accounts for a significant portion of global spending on life sciences research and development, much of which is directed towards proteomics and protein chip technologies. The favorable regulatory environment facilitated by the FDA, which has streamlined approval processes for innovative diagnostic devices, further accelerates market growth. Additionally, the high prevalence of chronic diseases in the region, as reported by the CDC, creates a persistent demand for advanced diagnostic solutions. Strong collaboration between academia and industry fosters rapid technology transfer and commercialization, while high reimbursement rates for advanced diagnostic tests encourage adoption in clinical settings. These converging factors ensure that North America maintains its premier position in the global landscape.

Europe Protein Chip Market Analysis

Europe was another significant regional segment in the global market and accounted for a promising share of the global market in 2025. The strong government support for scientific research and a well-established pharmaceutical sector are driving the protein chip market expansion in Europe. The region benefits from coordinated efforts such as the Horizon Europe framework, which prioritizes health and digital transformation, providing substantial grants for proteomics projects. Germany and the United Kingdom are primary contributors, hosting world-class research facilities and biotechnology hubs. As per Eurostat, the European Union invested heavily in research and innovation in 2025, with a significant fraction allocated to life sciences and medical technologies. The presence of renowned pharmaceutical companies in Switzerland, Germany, and France drives demand for protein chips in drug discovery and development. Furthermore, the increasing focus on personalized medicine within the EU, supported by initiatives like the 1+ Million Genomes Initiative that now includes proteomic components, is stimulating market expansion. The regulatory landscape, governed by the European Medicines Agency, ensures high standards for diagnostic devices, fostering trust and adoption among healthcare providers. The region’s emphasis on cross-border collaboration and data sharing enhances the utility of protein chip technologies in large-scale epidemiological studies, solidifying its status as a key market player.

Asia Pacific Protein Chip Market Analysis

The Asia Pacific region is predicted to be the fastest-growing region and register the highest CAGR among regions in the global market during the forecast period. This rising prominence is driven by rapid economic development, increasing healthcare expenditure, and a growing focus on indigenous research and development in countries like China, Japan, and India. China has made strategic investments in biotechnology as part of its national development plans, aiming to become a global leader in life sciences. According to the Chinese Ministry of Science and Technology, government funding for biomedical research has been increasing steadily, directly benefiting the proteomics sector. Japan remains a hub for technological innovation, with its aging population driving urgent demand for advanced diagnostics for age-related diseases. The proliferation of contract research organizations in India and China offers cost-effective solutions for global pharmaceutical companies, boosting the consumption of protein chip consumables. Rising awareness about preventive healthcare and the expansion of hospital infrastructure in emerging economies like South Korea and Singapore further contribute to market expansion. The region is also witnessing a surge in local manufacturing of protein chip components, reducing dependency on imports and lowering costs. These dynamic factors position the Asia Pacific as a critical growth engine for the global protein chip market.

Latin America Protein Chip Market Analysis

Latin America occupies a modest but growing position in the global protein chip market due to the improvements in healthcare infrastructure and increasing research activities in Brazil and Mexico. The region is gradually transitioning from basic research to more advanced proteomic applications, supported by government initiatives aimed at modernizing the healthcare sector. In Brazil, the Ministry of Health has launched programs to enhance the capacity of public laboratories, including the acquisition of advanced diagnostic equipment. According to the Pan American Health Organization, healthcare spending in Latin America has been rising steadily, facilitating the adoption of new technologies. The presence of a large population burdened by infectious diseases and rising chronic conditions creates a compelling need for efficient diagnostic tools. Academic institutions are increasingly collaborating with international partners to gain access to cutting-edge protein chip technologies for research purposes. Although economic volatility and limited reimbursement policies pose challenges, growing awareness of the benefits of early diagnosis and the expanding biotechnology sector in countries like Argentina and Chile are fostering a conducive environment for market growth.

Middle East and Africa Protein Chip Market Analysis

The Middle East and Africa hold the smallest share of the global protein chip market, yet it displays promising signs of development driven by strategic diversification efforts and improving healthcare systems. Countries in the Gulf Cooperation Council, particularly Saudi Arabia and the UAE, are leading the charge by investing heavily in healthcare infrastructure and research as part of their vision to reduce oil dependency. According to the Saudi Vision 2030 health sector transformation program, significant funding is being allocated to build world-class medical cities and research centers equipped with advanced technologies like protein chips. The rising prevalence of genetic disorders and diabetes in the region necessitates advanced diagnostic capabilities, spurring demand. South Africa serves as a key hub for biomedical research in the African continent, with institutions focusing on infectious disease proteomics supported by international grants. The World Bank notes that healthcare investment in the region has increased in recent years, although baseline levels remain low compared to other regions. Challenges such as a limited-skilled workforce and infrastructure gaps persist, but initiatives to train local talent and establish regional centers of excellence are addressing these issues. The gradual improvement in regulatory frameworks and the influx of foreign direct investment in the life sciences sector indicate a positive trajectory for market expansion in the coming years.

COMPETITIVE LANDSCAPE

The competition in the protein chip market is characterized by intense rivalry among established life science giants and agile biotechnology startups striving for technological supremacy. Major corporations leverage their extensive distribution networks and broad product portfolios to maintain dominance, while smaller firms differentiate themselves through specialized innovations in surface chemistry and antibody specificity. The landscape is dynamic with frequent mergers and acquisitions as larger entities seek to absorb novel technologies that enhance multiplexing capabilities and data analysis precision. Competitive pressure drives continuous investment in research and development to lower costs and improve sensitivity for clinical applications. Companies are increasingly competing on the ability to provide integrated solutions that combine hardware, reagents, and sophisticated software into seamless workflows. Regulatory compliance and the speed of obtaining approvals for diagnostic kits also serve as critical battlegrounds. The push towards personalized medicine further intensifies competition as firms race to develop proprietary biomarker panels that offer unique clinical insights and secure lucrative contracts with healthcare providers and pharmaceutical partners globally.

KEY MARKET PARTICIPANTS

A few of the notable companies leading the global protein chip market profiled in this report are

- SEQUENOM, Inc.

- Sigma Aldrich Corporation

- Affymetrix, Inc.

- Merck KGaA

- Thermo Fisher Scientific

- EMD Millipore

- Illumina, Inc.

- Life Technologies Corporation

- Agilent Technologies

TOP PLAYERS IN THE MARKET

- Thermo Fisher Scientific stands as a preeminent force in the global protein chip landscape by offering an extensive portfolio of analytical and functional microarray solutions. The company leverages its vast resources to integrate protein chip technologies with advanced mass spectrometry and liquid handling systems, creating comprehensive workflows for proteomics researchers. Their recent strategic actions focus on expanding their catalog of validated antibodies and recombinant proteins to enhance the sensitivity and specificity of their arrays. Thermo Fisher actively invests in developing user-friendly software platforms that simplify complex data analysis for clinical diagnostics. By fostering collaborations with leading academic institutions and biotechnology firms, they accelerate the translation of research findings into commercial applications. Their commitment to innovation ensures they remain at the forefront of biomarker discovery and drug development sectors globally.

- Agilent Technologies maintains a significant presence in the protein chip market through its high-performance microarray platforms and robust detection instruments. The company specializes in providing reliable solutions for protein expression profiling and interaction studies that cater to both academic and pharmaceutical sectors. Agilent recently intensified its efforts to improve surface chemistry technologies, which allow for better protein immobilization and reduced background noise in assays. They have launched new automated scanning systems that increase throughput and reproducibility for large-scale clinical studies. Their strategy involves strengthening their global distribution network to ensure rapid access to consumables and technical support for customers worldwide. Agilent also focuses on integrating artificial intelligence capabilities into its data analysis software to help researchers identify subtle patterns in complex proteomic datasets more efficiently.

- Merck KGaA operates as a critical enabler in the protein chip ecosystem by supplying high-quality reagents, antibodies, and custom array fabrication services. The company distinguishes itself through its deep expertise in life science materials, which are essential for producing reliable and sensitive protein microarrays. Merck has recently expanded its portfolio of recombinant antibodies and aptamers to address the growing demand for specific binding agents in functional assays. They are actively investing in state-of-the-art manufacturing facilities to ensure consistent supply and quality control for global clients. Their strategic partnerships with diagnostic developers help accelerate the commercialization of novel protein chip-based tests for infectious diseases and cancer. Merck also prioritizes sustainability by developing eco-friendly production processes for their biochip components while maintaining high-performance standards for research and clinical applications.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the protein chip market primarily employ strategic acquisitions and partnerships to expand their technological capabilities and product portfolios. Companies frequently acquire innovative startups specializing in novel surface chemistries or antibody engineering to enhance assay sensitivity and specificity. Another major strategy involves heavy investment in research and development to create next-generation platforms that integrate artificial intelligence for advanced data analytics. Manufacturers are increasingly focusing on developing miniaturized and portable devices to capture the growing point-of-care testing sector. Collaborations with academic institutions and pharmaceutical giants help validate new biomarkers and accelerate regulatory approvals for diagnostic applications. Expanding global distribution networks ensures faster delivery of consumables and instruments to emerging markets. Additionally, companies are standardizing protocols and offering comprehensive training programs to reduce the complexity of adoption for end users and foster long-term customer loyalty in this competitive landscape.

MARKET SEGMENTATION

This research report on the global protein chip market has been segmented and sub-segmented based on the technology, application, and region.

By Technology

- Analytical Microarrays

- Functional Protein Microarrays

- Reverse Phase Protein Microarray

By Application

- Diagnostics

- Proteomics

- Protein Functional Analysis

- Antibody Characterization

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. Which technologies dominate the global protein chip market?

Analytical microarrays are the most dominant technology, followed by reverse phase protein microarrays in the global protein chip market

2. What are key applications in the global protein chip market?

Applications include antibody characterization, clinical diagnostics, biomarker discovery, and disease profiling in the global protein chip market

3. How does personalized medicine impact the global protein chip market?

Personalized medicine drives demand for protein chips to analyze individualized protein interactions and biomarkers in the global protein chip market

4. How is research and development influencing the global protein chip market?

R&D investments in proteomics enhance the development of advanced protein chip platforms, fueling growth in the global protein chip market

5. What are the main end users in the global protein chip market?

Academic, research institutions, biotech companies, and pharmaceutical firms are primary end users in the global protein chip market

6. How do cancer diagnostics relate to the global protein chip market?

Protein chips enable high-throughput screening of cancer biomarkers, advancing diagnostics and therapy monitoring in the global protein chip market

7. What are the advantages of protein chips compared to traditional methods?

Protein chips allow simultaneous analysis of thousands of proteins with small sample volumes, increasing precision and throughput in the global protein chip market

8. What challenges does the global protein chip market face?

Challenges include high costs, complex manufacturing, and technical expertise required in the global protein chip market

10. How do digital technologies enhance the global protein chip market?

Integration of AI and bioinformatics improves data analysis and accuracy in the global protein chip market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com