Global Semiconductor Market Size, Share, Trends & Growth Forecast Report By Semiconductor Type, Technology, Business Model, and By Region (Asia Pacific, North America, Europe, Latin America, Middle East & Africa) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

$668.3 BnMarket Estimate, 2026

$711.6 BnMarket Forecast, 2034

$1175.9 BnCAGR, 2026–2034

6.5%Global Semiconductor Market Summary

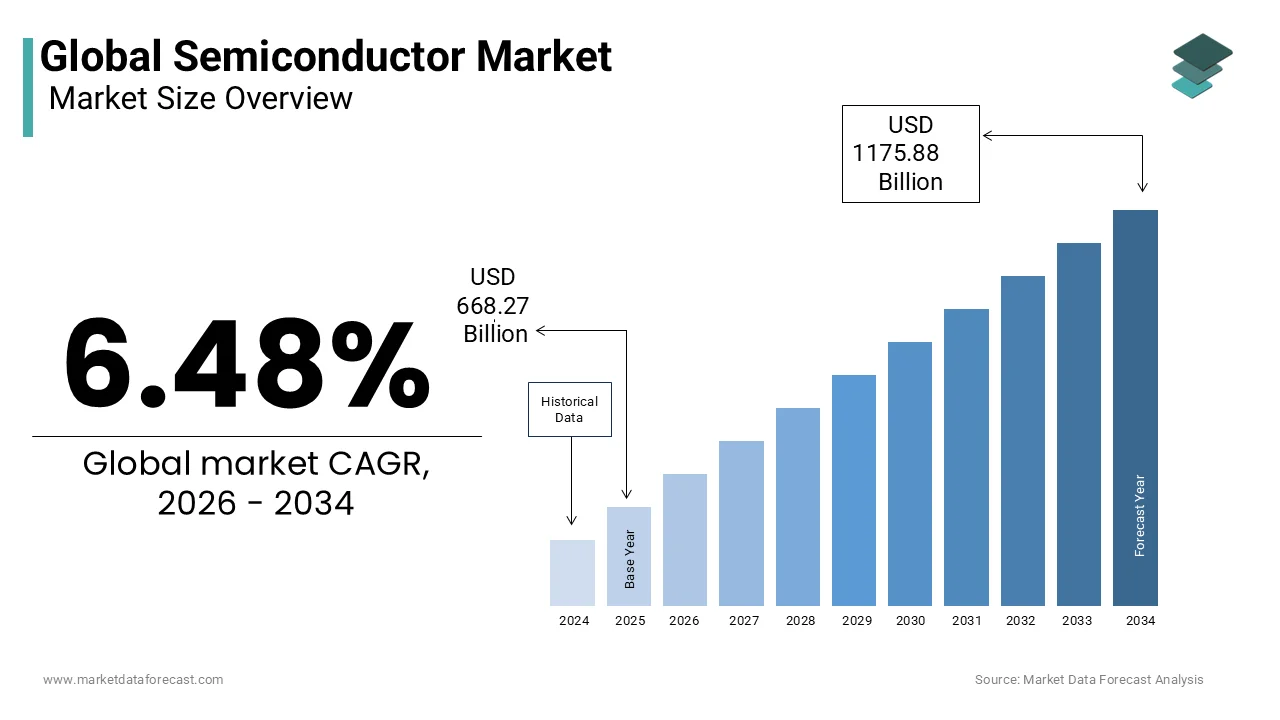

The global semiconductor market was valued at USD 668.27 billion in 2025, is expected to reach USD 711.57 billion in 2026, and is projected to grow to USD 1,175.88 billion by 2034, registering a CAGR of 6.48% from 2026 to 2034. Growth is being fueled by AI-driven chip demand, 5G and beyond-5G infrastructure expansion, EV electrification, advanced packaging innovation, and sovereign semiconductor policies worldwide.

Key Market Highlights

- 2025 Market Size: USD 668.27 Billion

- 2026 Estimate: USD 711.57 Billion

- 2034 Forecast: USD 1,175.88 Billion

- CAGR (2026–2034): 6.48%

- Devices Shipped (2024): 1.4+ Trillion Units

- Dominant Segment: Integrated Circuits (ICs)

- Fastest Technology Growth: Sub-3nm Nodes (34.2% CAGR)

- Largest Region: Asia Pacific (72.1% share in 2025)

Quick Growth Drivers

- AI accelerators and high-performance computing chips

- 5G base stations and emerging 6G R&D

- Electric vehicle power electronics (SiC & GaN adoption)

- Data center hyperscale expansion

- Edge computing and IoT device proliferation

Principal Restraints

- Export controls and geopolitical fragmentation

- EUV equipment supply limitations

- $20B+ cost for advanced 300mm fabs

- Talent shortage in sub-5nm process engineering

- Capital concentration among top foundries

High-Value Opportunities

- Silicon Carbide (SiC) and Gallium Nitride (GaN) power semiconductors

- Chiplet architectures & heterogeneous integration

- 3D stacking (CoWoS, Foveros, HBM integration)

- Automotive ADAS and autonomous systems

- Defense and sovereign semiconductor programs

Key Market Challenges

- Water consumption & fluorinated gas emissions

- Sub-3nm yield management complexity

- Supply chain over-concentration in East Asia

- Skilled workforce deficit (70,000+ projected shortfall in the U.S.)

- Increasing fab construction timelines (4–5 years)

What Wins Commercially (Competitive Edge)

- Advanced node capability (<3nm)

- EUV lithography mastery

- Chiplet + 3D packaging integration

- Wide-bandgap power semiconductor leadership

- Geographic fab diversification

Top Strategic Ask for Executives

- Accelerate chiplet & heterogeneous integration strategies

- Diversify supply chains beyond concentrated hubs

- Invest in SiC/GaN power device scaling

- Build talent pipelines through university-industry partnerships

- Strengthen water recycling & green fab initiatives

Leading Players

Some of the companies that are playing a dominating role in the global semiconductor market include:

- Intel Corporation

- Samsung Electronics Co.

- Qualcomm Incorporated

- Taiwan Semiconductor Manufacturing Company

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Micron Technology, Inc.

- Texas Instruments Incorporated

- ASML Holding N.V.

Global Semiconductor Market Size

The global semiconductor market was valued at USD 668.27 billion in 2025 and is expected to reach USD 711.57 billion in 2026, and is projected to grow to USD 1175.88 billion by 2034, with a CAGR of 6.48% from 2026 to 2034.

The semiconductor is a design, fabrication, and deployment of integrated circuits (ICs) that serve as the foundational components for virtually all modern electronic systems. These microchips, composed of materials like silicon and gallium arsenide, enable functions ranging from data processing and memory storage to power regulation and signal transmission. As per the Semiconductor Industry Association (SIA), over 1.4 trillion semiconductor devices were shipped globally in 2024, embedded in applications from smartphones and medical imaging systems to autonomous vehicles and industrial robotics.

MARKET DRIVERS

Proliferation of AI-Specific Chips in Data Centers and Edge Devices

The surge in artificial intelligence applications for specialized semiconductor architectures optimized for machine learning workloads is driving the growth of the semiconductor market. AI accelerators such as tensor processing units (TPUs) and neural processing units (NPUs) deliver orders-of-magnitude improvements in inference efficiency. Google’s deployment of its fifth-generation TPU in cloud infrastructure has reduced AI training time for models like PaLM by 40%, as documented in its 2024 sustainability report. Additionally, edge AI chips from companies like Qualcomm and Hailo are being integrated into autonomous drones and surveillance systems, where low-latency inference is critical.

Expansion of 5G and Beyond-5G Communication Infrastructure

The global rollout of 5G networks and the development of 6G research platforms are propelling the growth of the semiconductor market. 5G base stations require advanced RF chips, power amplifiers, and millimeter-wave transceivers capable of handling data rates up to 10 Gbps, far exceeding 4G capabilities. In China, Huawei’s 5G infrastructure deployments incorporate over 1,500 custom-designed RFICs and ASICs per macro site, according to the China Academy of Information and Communications Technology. Meanwhile, the U.S. National Science Foundation has allocated $500 million to 6G research hubs focusing on terahertz-frequency semiconductors, with prototypes already demonstrating data transmission at 116 Gbps in lab conditions. This technological evolution demands gallium nitride (GaN) and silicon carbide (SiC) substrates for superior thermal and electrical performance, which is accelerating innovation in compound semiconductor materials.

MARKET RESTRAINTS

Geopolitical Fragmentation and Export Control Restrictions

The increasing geopolitical tensions have led to stringent export controls on advanced semiconductor technologies, which are restraining the growth of the semiconductor market. According to the Semiconductor Industry Association, these restrictions have delayed advanced chip production timelines by 12 to 18 months for several Asian foundries. The Netherlands’ ASML, the sole producer of EUV machines, reported a 30% decline in shipments to China in 2024 due to compliance requirements, as disclosed in its annual financial statement. Japan has also joined export controls on 23 semiconductor manufacturing tools, which further constrain equipment availability.

Escalating Costs of Advanced Node Fabrication Facilities

The financial barrier to constructing and operating cutting-edge semiconductor fabrication plants is the leveraging of the growth of the semiconductor market. Building a state-of-the-art 300mm fab capable of producing 3nm or 2nm logic chips now exceeds $20 billion, according to the U.S. Congressional Research Service. TSMC’s Arizona facility is projected to cost $40 billion for two phases, which reflects inflation in equipment, cleanroom engineering, and talent acquisition. Smaller firms and emerging economies find it nearly impossible to justify such investments without government subsidies. This capital intensity limits competition, concentrates production among a few global players, and increases systemic risk in the event of geopolitical or natural disruptions to key fabrication hubs.

MARKET OPPORTUNITIES

Growth of Silicon Carbide and Gallium Nitride in Power Electronics

The wide-bandgap semiconductors, such as silicon carbide (SiC) and gallium nitride (GaN), offer higher efficiency, thermal resilience, and miniaturization. SiC-based power devices are now integral to electric vehicle inverters, where they reduce energy losses by up to 50% compared to traditional silicon IGBTs. According to the U.S. Department of Energy, the adoption of SiC in Tesla’s Model 3 powertrain improved range by 5–7% without battery enlargement. In renewable energy, solar inverters using GaN transistors achieve conversion efficiencies exceeding 99%, as verified by the National Renewable Energy Laboratory (NREL).

Adoption of Chiplets and Heterogeneous Integration in Advanced Packaging

The shift toward chiplet-based design and 3D heterogeneous integration is revolutionizing semiconductor architecture by enabling modular, cost-effective system scaling beyond traditional monolithic designs, and is accelerating the growth of the semiconductor market. Instead of fabricating an entire system-on-chip (SoC) on a single die, chiplets allow disaggregation of functions, CPU, GPU, and memory into smaller, optimized dies interconnected via advanced packaging like Intel’s Foveros or TSMC’s CoWoS. According to Yole Développement, the chiplet market is projected to grow at a CAGR of 29% through 2028, driven by demand for customizable, high-performance computing. AMD’s EPYC processors, built with chiplet architecture, deliver 64 cores per socket while reducing yield loss by 35%, as reported in its 2024 technical white paper. Apple’s M-series chips utilize TSMC’s 3D stacking to integrate 24 billion transistors with minimal latency.

MARKET CHALLENGES

Persistent Shortage of Skilled Semiconductor Engineers and Technicians

The critical talent deficit in design, fabrication, and process engineering, threatening innovation and production scalability, is challenging the growth ofthe semiconductor market. According to the U.S. Bureau of Labor Statistics, there will be a shortfall of 70,000 semiconductor engineers by 2030, even with current university enrollment trends. South Korea’s Semiconductor Industry Association disclosed that 65% of companies struggle to recruit process engineers capable of managing sub-5nm node production.

Environmental Impact of Semiconductor Manufacturing Processes

The semiconductor fabrication is inherently resource-intensive, raising sustainability concerns related to water consumption, chemical waste, and carbon emissions. In Taiwan, TSMC’s fabs account for 10% of the island’s industrial water usage, which is prompting government scrutiny during drought periods. Additionally, the use of fluorinated gases like sulfur hexafluoride (SF₆), which has a global warming potential 23,500 times greater than CO₂, remains prevalent in etching processes. According to the U.S. Environmental Protection Agency, semiconductor manufacturing contributed 2.8 million metric tons of CO₂-equivalent emissions in 2022 from energy and gas usage.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Semiconductor Type, Technology Node, Business Model, End-Use Sector, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Indorama Ventures Public Company Limited, Loro Piana S.P.A., Xinao Textiles Inc., Marzotto Group, Südwolle Group GmbH, Merinotex, Pendleton Woolen Mills, The Woolmark Company |

SEGMENTAL ANALYSIS

By Semiconductor Insights

The Integrated Circuits (ICs) segment was the largest and held a dominant share of thesemiconductorr market in 2025. ICs consolidate millions of transistors into single chips to perform complex functions such as data processing, memory storage, and signal control. According to the U.S. Department of Commerce, over 900 billion IC units were shipped globally in 2024, driven by demand for microprocessors, DRAM, and NAND flash memory. In smartphones alone, each device contains an average of 25 ICs, including application processors, power management ICs, and RF transceivers, as reported by the Consumer Technology Association.

The optoelectronics segment is likely to grow with an expected CAGR of 13.7% during the forecast period, with the rising demand for photonic components in data transmission, sensing, and renewable energy. According to the International Electrotechnical Commission (IEC), global deployment of 400G and 800G optical transceivers in data centers surged by 65% in 2024. Sony’s image sensor division reported a 42% increase in unit shipments for automotive and industrial cameras, reflecting growing adoption in autonomous vehicles.

By Technology Node Insights

The technology nodes of the 28nm segment held 45.3% of the global semiconductor market share in 2025. These nodes remain the workhorses for automotive electronics, industrial control systems, power management, and legacy communication infrastructure. According to the Semiconductor Industry Association (SIA), over 70% of automotive microcontrollers and 80% of analog chips are manufactured on 40nm and above processes due to their reliability, radiation tolerance, and cost efficiency. In 2024, STMicroelectronics produced over 100 million 130nm automotive MCUs for electric vehicle battery management systems, as disclosed in its annual sustainability report. Similarly, industrial programmable logic controllers (PLCs) from Siemens and Rockwell Automation rely on 180nm and 130nm nodes for long-term stability and temperature resilience.

The sub-3nm technology node is likely to grow with an expected CAGR of 34.2% during the forecast period with the insatiable demand for ultra-high-performance computing in AI, cloud infrastructure, and mobile SoCs. These advanced nodes enable transistor densities exceeding 300 million per square millimeter, allowing chips to deliver unprecedented computational throughput with lower power consumption. According to TechInsights, Apple’s A17 Pro chip, fabricated on TSMC’s 3nm process, integrates 19 billion transistors while reducing power draw by 30% compared to its 5nm predecessor. Samsung’s 2nm Gate-All-Around (GAA) transistors, scheduled for 2025 volume production, are projected to improve performance by 25% and reduce leakage by 50%, as confirmed by the Korea Institute of Science and Technology. In AI accelerators, NVIDIA’s next-generation Blackwell architecture will utilize sub-3nm nodes to achieve exa-scale inference capabilities.

By Business Model Insights

The Integrated Device Manufacturers (IDMs) segment accounted in holding 54.3% of the share in 2025. This vertical integration allows IDMs to optimize performance, ensure supply continuity, and maintain stringent quality standards in high-reliability applications. According to the U.S. Department of Defense, IDMs like Intel, Samsung, and Texas Instruments supply over 80% of chips used in defense electronics, where traceability and domestic production are mandatory. In 2024, Samsung’s semiconductor division operated 12 fabrication lines across South Korea and the U.S., producing memory and logic chips with minimal external dependency, as reported in its corporate transparency statement. Intel’s IDM 2.0 strategy includes reclaiming manufacturing leadership through its Arizona and Ohio fabs, backed by $52 billion in CHIPS Act funding.

The fabless semiconductor model segment is anticipated to grow with an expected CAGR of 16.8% during the forecast period, with the rise of specialized chip designers leveraging third-party foundries for rapid innovation and reduced capital burden. Companies like NVIDIA, AMD, and Qualcomm focus exclusively on architecture and IP development, outsourcing fabrication to TSMC, Samsung Foundry, and GlobalFoundries. The success of RISC-V-based startups like SiFive, which raised $175 million in 2024 for open-architecture chips, highlights the model’s agility.

REGIONAL ANALYSIS

Asia Pacific Semiconductor Market Insights

Asia Pacific was the top performer of the global semiconductor market by capturing 72.1% othemarket share in 2025. China, Taiwan, South Korea, and Japan collectively dominate front-end fabrication, packaging, and materials supply. Taiwan Semiconductor Manufacturing Company (TSMC) alone produces over 90% of the world’s advanced logic chips below 7nm, as reported by the Industrial Technology Research Institute (ITRI). South Korea’s Samsung and SK Hynix control 70% of the global DRAM market, with combined investments exceeding $300 billion in semiconductor expansion by 2030, according to the Korea Semiconductor Industry Association.

North America Semiconductor Market Insights

North AmAmerica'semiconductor market was the largest and held 21.2% of the share in 2025, with the growing prominence in chip design, IP development, and strategic policy direction. The United States is home to leading fabless companies such as NVIDIA, AMD, and Qualcomm, which collectively hold over 75% of the AI accelerator and mobile SoC markets, according to the Semiconductor Industry Association. Intel’s resurgence through its IDM 2.0 strategy includes constructing two new fabs in Ohio, supported by $8.5 billion in direct funding under the CHIPS and Science Act, as confirmed by the U.S. Department of Commerce.

Europe Semiconductor Market Insights

Europe's semiconductor market growth is likely to grow with the highest CAGR in the coming years. The region produces 90% of the world’s automotive microcontrollers, with Infineon, NXP, and STMicroelectronics dominating the supply chain, according to the European Semiconductor Industry Association (ESIA). The EU Chips Act aims to double the region’s market share to 20% by 2030, allocating €43 billion in public and private investment. In 2024, Intel announced a $33 billion fab investment in Magdeburg, Germany, while TSMC opened a 12-inch wafer plant in Dresden for automotive-grade chips.

Latin America Semiconductor Market Insights

Latin American semiconductor market is likely to grow with limited fabrication but growing importance in assembly, testing, and niche applications. Mexico serves as a key back-end hub, hosting packaging and testing facilities for companies like ON Semiconductor and NXP, which employ over 30,000 workers across the country. Brazil’s aerospace and defense sectors utilize domestically designed analog and RF chips, with Embraer integrating locally produced semiconductors in avionics systems.

Middle East & Africa Semiconductor Market Insights

The Middle East and Africa semiconductor market is growing steadily during the forecast period. The UAE leads the region through its Advanced Technology Research Council (ATRC) and investments in semiconductor R&D, including a $1.4 billion partnership with GlobalFoundries to establish a secure chip design center in Abu Dhabi. South Africa’s CSIR (Council for Scientific and Industrial Research) developed a radiation-hardened microcontroller for satellite use, tested in low Earth orbit missions.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

The Key Players of the Semiconductor Market Include

- Intel Corporation

- Samsung Electronics Co.

- Qualcomm Incorporated

- SK hynix Inc. – South Korea

- NVIDIA Corporation

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Broadcom Inc.

- Advanced Micro Devices, Inc.

- Micron Technology, Inc.

- Texas Instruments Incorporated

- Infineon Technologies AG

- NXP Semiconductors N.V.

- MediaTek Inc.

- Analog Devices, Inc.

- ASML Holding N.V.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the semiconductor market are deploying a range of high-impact strategies to maintain technological dominance and supply chain resilience. Leading firms are investing heavily in advanced node development, with TSMC, Samsung, and Intel collectively allocating over $100 billion annually toward sub-3nm process innovation and EUV lithography. Vertical integration is a dominant theme, as seen in Intel’s IDM 2.0 model and Samsung’s end-to-end memory-to-foundry ecosystem. Strategic geographic diversification is accelerating, with companies establishing fabs in allied nations to mitigate geopolitical risks and comply with local content mandates. Additionally, companies are prioritizing advanced packaging technologies such as chiplets and 3D stacking to extend Moore’s Law, while also focusing on sustainable manufacturing through water recycling, carbon-neutral fabs, and green supply chain initiatives.

COMPETITION OVERVIEW

The competition in the semiconductor market is defined by high stakes of technological innovation, geopolitical alignment, and capital intensity. While TSMC dominates advanced logic manufacturing, Samsung and Intel are aggressively contesting the foundry space with next-generation GAA transistor technologies. In memory, SK Hynix and Micron are pushing HBM3E and LPDDR5X adoption to support AI workloads, creating a performance arms race. Fabless giants like NVIDIA and AMD rely on these foundries to deliver AI and data center chips, forming interdependent ecosystems. Geopolitical pressures are reshaping alliances, with nations prioritizing domestic production through subsidies and trade policies. Meanwhile, China’s SMIC and Huawei are advancing 7nm capabilities despite export controls in a fragmented global landscape.

TOP LEADING PLAYERS IN THE MARKET

TSMC (Taiwan Semiconductor Manufacturing Company)

TSMC is the top player in the global semiconductor market, particularly in the Asia Pacific region, where its advanced fabrication capabilities serve as the backbone for cutting-edge chip production. Headquartered in Hsinchu Science Park, Taiwan, the company operates the world’s most advanced 3nm and 2nm node manufacturing lines, supplying logic chips to leading AI and mobile SoC designers. The company also broke ground on a second fab in Arizona, USA, while expanding its R&D center in Taiwan to focus on 2D materials and 3D IC integration.

Samsung Electronics (Device Solutions Division)

Samsung’s semiconductor division has been instrumental in shapingthe Asia Pacific’s memory and foundry landscape, which is combining vertical integration with aggressive node scaling. Additionally, Samsung’s collaboration with Hyundai on automotive MCUs and with SK Telecom on 6G-ready RFICs underscores its strategic pivot toward diversified applications.

Intel Corporation

Intel has reasserted its strategic presence in the Asia Pacific semiconductor market through a dual approach of technological resurgence and regional manufacturing expansion. While historically strong in North America, Intel has intensified its regional footprint by establishing design centers in Bangalore, Shanghai, and Tokyo, focusing on AI accelerators, network processors, and edge computing SoCs. Intel also signed a $33 billion agreement with the German government to build a semiconductor mega-campus in Magdeburg, enhancing EU-Asia supply chain resilience. In Japan, Intel partnered with Rapidus to support the development of 2nm-class chips, which is contributing engineering expertise and tooling knowledge.

GLOBAL SEMICONDUCTOR MARKET NEWS

- In January 2022, TSMC announced the construction of its first semiconductor fab in Kumamoto, Japan, with a $7 billion investment supported by the Japanese government, aiming to produce 12nm and 16nm chips for automotive and industrial clients by 2025 to strengthen regional supply chain resilience.

MARKET SEGMENTATION

Global Semiconductor Market Segmentation

This research report on the Global Semiconductor Market is segmented and sub-segmented into the following categories.

By Semiconductor Type

-

Integrated Circuits (ICs)

-

Optoelectronics

-

Memory Devices

-

Sensors & Discretes

-

Others

By Technology Node

-

28nm

-

14–7nm

-

Sub-3nm

By Business Model

-

Integrated Device Manufacturers (IDMs)

-

Fabless Semiconductor Companies

-

Foundries

-

Outsourced Assembly & Testing

By End-Use Sector

-

Automotive

-

Consumer Electronics

-

Industrial

-

Healthcare & Medical Devices

-

Telecommunications

-

Others

By Region

-

Asia Pacific

-

North America

-

Europe

-

Latin America

-

Middle East & Africa

Frequently Asked Questions

1. What is the Global Semiconductor Market?

The Global Semiconductor Market refers to the worldwide ecosystem of companies involved in designing, manufacturing, and selling semiconductor devices and components that power modern electronic products and systems across diverse industries.

2. What are the main drivers of growth in the Global Semiconductor Market?

The Global Semiconductor Market's growth is mainly driven by consumer electronics demand, expansion of 5G networks, and rapid advances in artificial intelligence, automotive technology,

and IoT integration, resulting in accelerating semiconductor innovation.

3. Which regions lead the Global Semiconductor Market?

Asia Pacific accounts for the largest share of the Global Semiconductor Market, with major manufacturing hubs based in China, South Korea, and Taiwan,

boosted by strong government support and industrial infrastructure.

4. What are the top companies in the Global Semiconductor Market?

Major companies in the Global Semiconductor Market include Intel Corporation, Samsung Electronics, Broadcom Inc., Qualcomm, and TSMC, which collectively drive industry innovation, volume, and market leadership.

5. What are the main components in the Global Semiconductor Market?

The Global Semiconductor Market includes memory chips, logic devices, analog integrated circuits, microcontroller units (MCUs),

and sensors, each supporting different electronics applications and end-user markets

6. How has the Global Semiconductor Market been affected by supply chain disruptions?

The Global Semiconductor Market experienced significant delays, cost escalations, and chip shortages due to global supply chain disruptions, as events like the pandemic and geopolitical issues strained logistics and material flows.

7. What role does artificial intelligence play in the Global Semiconductor Market?

Artificial intelligence drives demand for specialized semiconductor chips such as GPUs and high-performance computing units, making AI one of the fastest-growing applications in the Global Semiconductor Market.

8. What is the forecasted size of the Global Semiconductor Market?

The Global Semiconductor Market is projected to exceed $1 trillion by 2030, with strong annual growth rates supported by adoption in automotive, healthcare, communications, and cloud computing applications

9. How important are electric vehicles in the Global Semiconductor Market?

Electric vehicles are a critical growth segment of the Global Semiconductor Market, requiring advanced chips for power management, ADAS systems, and vehicle-to-everything infrastructure, spurring semiconductor demand and innovation.

10. What are logic devices in the Global Semiconductor Market?

Logic devices in the Global Semiconductor Market are central to computing and processing systems, playing vital roles in AI, data centers, smartphones, and networking technologies worldwide.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com