Global SSD Caching Market Size, Share, Trends, & Growth Forecast Report By SSD Interface (SATA, SAS and PCIE), Application (Deal and Client), & Region, Industry Forecast From 2024 to 2033

Global SSD Caching Market Size

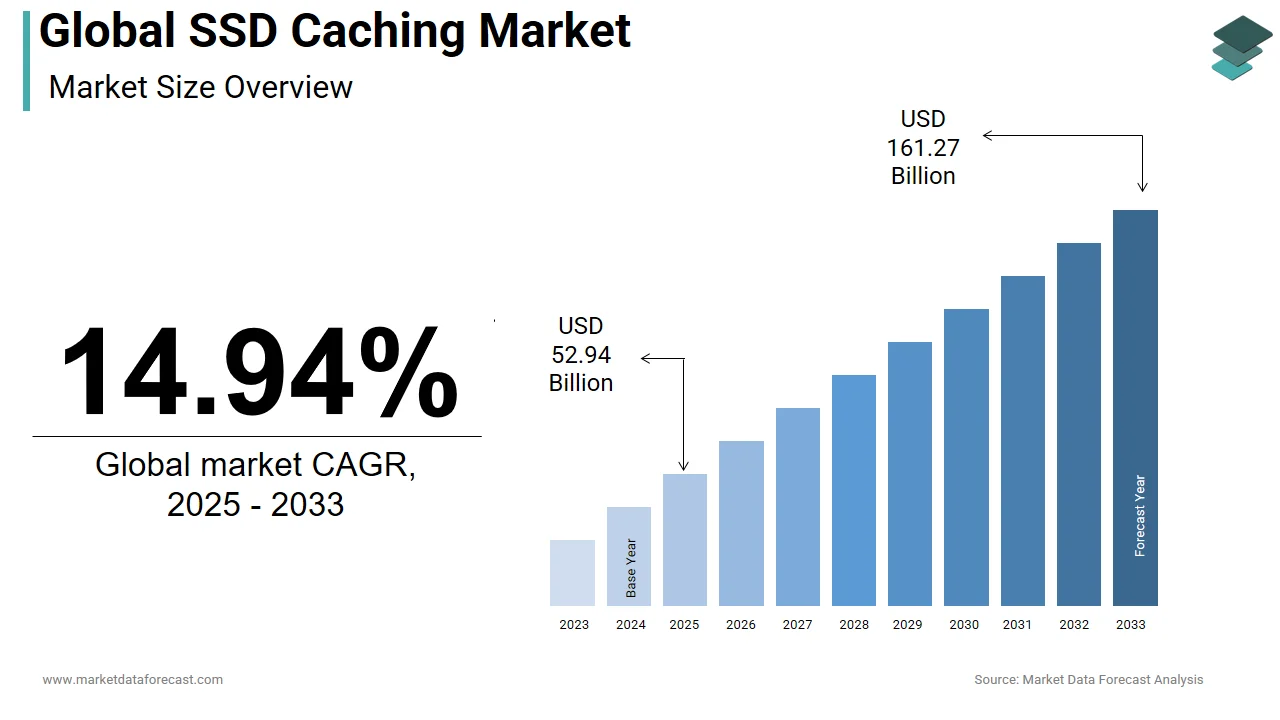

The Global solid-state drives (SSD) market was worth USD 46.06 billion in 2024. The global market is anticipated to reach USD 52.94 billion in 2025 and USD 161.27 billion by 2033, growing at a CAGR of 14.94% during the projection period 2025 to 2033.

SSD stands for Solid State Drive, which Intel launched to improve the performance of computers that use the hard drive. It is a storage device that makes use of interconnected flash memories or IC assemblies as memory to store information without power. The main variance between a hard drive and an SSD is that the former uses rotating metal platters to store data, while the SSD has no moving parts. A solid-state drive (SSD) is a non-volatile storage medium that stores persistent data in solid flash memory. SSD is faster, quieter, and generally preferable compared to hard drives (HDD). With higher capacity, faster speed, and more user-friendly prices, SSDs are expected to replace hard drives shortly. SSDs are like hard drives in that they are non-volatile storage media. In these, data is stored on a series of interconnected microchips in the place of spinning discs. This makes accessing memory much faster, and boot times are drastically reduced on SSDs, increasing the adoption of SSDs in IT.

MARKET DRIVERS

Due to the growing reception of advanced technologies, North America is expected to be a leading market in cloud, IoT, big data, and high-end cloud computing.

The rising need for storage due to the high adoption of these technologies is driving market growth in the region. Improvements in NAND flash technology have enabled enterprise SSD manufacturers to utilize low-resistance NAND flash options such as a multi-level cell (MLC), a three-level cell (TLC), and 3D NAND. Advantages of low resistance NAND flash forms include lower cost and higher capacity, which has increased market growth. Small and medium-sized businesses generally use MLC SSD, which offers longer service life and better performance than TLC SSD and is relatively cheaper than SLC SSD. Due to their higher volume and lower cost, TLC SSD users are general customers in the market.

Enterprise SSDs cache data permanently or temporarily in non-volatile solid-state memory. It is designed for servers, storage systems, and directly attached devices (DAS). These SSDs typically use NAND flash memory, offer advanced performance, and consume less power than spinning hard drives. However, they are generally priced higher. Advantages of enterprise SSDs over customer SSDs include protection of data stored in DRAM in the event of a power failure, higher performance, more robust error correction code (ECC), consistent and persistent quality of service, and more extended warranty. Early enterprise SSDs used single-level cell (SLC) NAND flash recollection, which stores one bit per cell and provides the highest level of endurance and performance, with a typical life cycle of 100,000 writes per cell. Higher access latencies (i.e., lower throughput) and fewer write erase cycles on a specific block (i.e., longer lifespan).

MARKET RESTRAINTS

However, many factors hinder the growth of this industry. Hard drives are available on the market, while SSD drives are hard to come by. Also, SSDs have limited storage capacity. And to increase storage capacity, consumers have to pay a considerable sum. Another disadvantage of SSDs is their shorter lifespan than hard drives. However, due to technological advancements, these downsides slowly reduce the downsides that make customers more inclined to use SSDs. The developers are also striving to increase the privacy and security of this market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 14.94% |

| Segments Covered | By SSD Interface, Application, and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | OCZ Synapse, Intel, Mushkin, Super Talent Technology, Edge Memory, Dataplex, Corsair, MyDigital SSD, Virident Systems, Transcend, Plextor, Micron, HGST, ADATA, Samsung, LSI, AMD, Romex Software, Proximal Data, Cachebox, Adaptec, and others. |

REGIONAL ANALYSIS

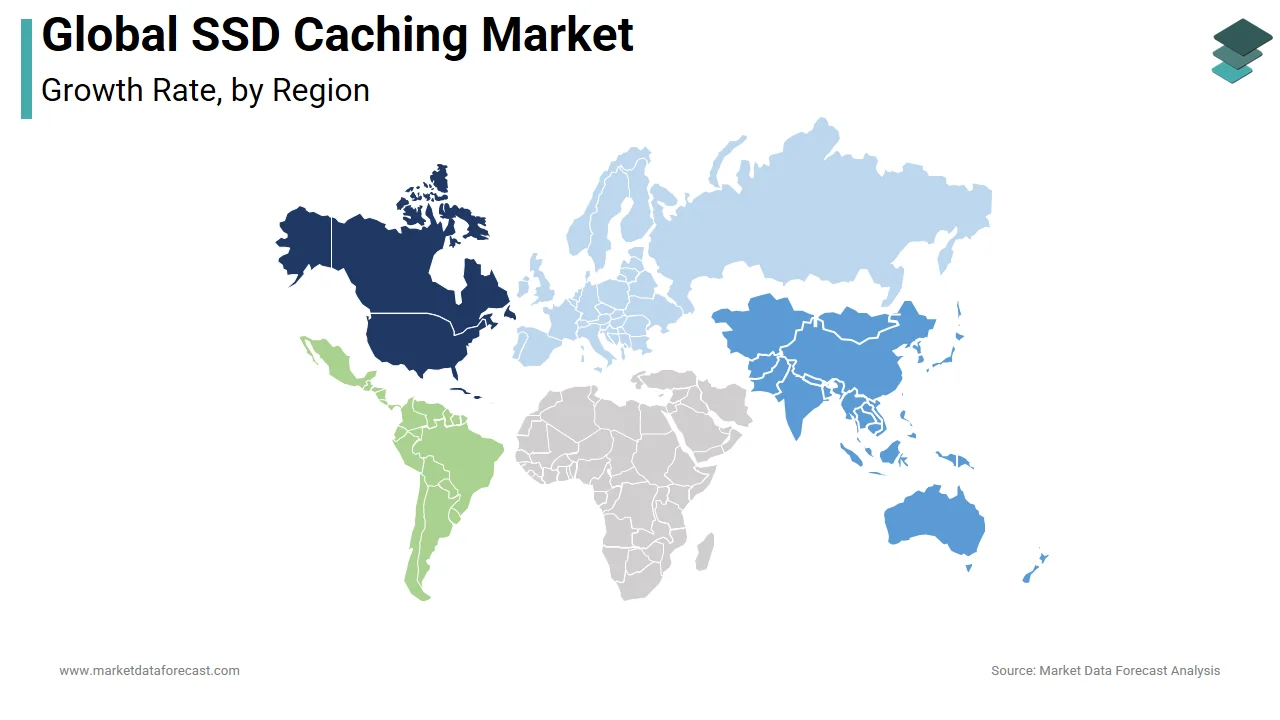

Asia-Pacific dominates the global SSD caching market. Countries like Japan, China, and Taiwan are emerging as leading markets for SSDs. One of the main reasons for this is the growth of technological advances in these countries and the presence of a large market for electronic products.

KEY PARTICIPANTS IN THE MARKET

Companies playing a promising role in the global SSD caching market are Scandisk, OCZ Synapse, Intel, Mushkin, Super Talent Technology, Edge Memory, Dataplex, Corsair, MyDigital SSD, Virident Systems, Transcend, Plextor, Micron, HGST, ADATA, Samsung, LSI, AMD, Romex Software, Proximal Data, Cachebox, Adaptec and others. Companies like Toshiba, Samsung, and others are among the few companies in these countries promoting SSD technology. Even India is growing in terms of SSD manufacturing. Other market players are the United States, Europe, the Middle East, and Africa, experiencing increased flash memory requirements due to the growing smartphone consumer base.

RECENT HAPPENINGS IN THE MARKET

-

In February 2020, Kioxia Corporation, a memory solutions provider, announced that its PCIe 4.0 NVMe enterprise and data center SSDs line has now been delivered to its customers.

-

In December 2019, Intel Corporation launched its AS5000G5-F series of mid-range all-flash storage with a two-port Optane SSD in partnership with Inspur. The AS5000G5-F series offers around 8 million IOPS and 0.1ms latency, making it a highly-performing midrange storage platform in the industry.

-

In April 2019, Micron Technology Inc. announced its new series of SSDs with NVM Express (NVMe) protocol, which brings storage performance at higher capacities to the enterprise and cloud computing markets.

MARKET SEGMENTATION

This research report on the global SSD caching market has been segmented and sub-segmented based on SSD interface, application and region.

By SSD Interface

-

SATA

-

SAS

-

PCIE

By Application

-

Deal

-

Client

By Region

-

North America

-

Europe

-

Asia-Pacific

-

Latin America

-

Middle East and Africa

Frequently Asked Questions

What is the current size of the global SSD caching market?

As of the latest data in 2025, the global SSD caching market is estimated to be valued at USD 52.94 billion.

What are the key drivers contributing to the growth of the global SSD caching market?

Factors such as increasing data-intensive applications, demand for faster data access, and the rise of cloud computing are driving the growth of the SSD caching market globally.

Which regions are witnessing the highest adoption of SSD caching technology?

Currently, North America and Asia-Pacific are experiencing the highest adoption rates of SSD caching technology, attributed to technological advancements and increased IT infrastructure investments.

What are the predominant trends shaping the global SSD caching market in 2024?

Trends such as the integration of machine learning algorithms for intelligent caching, NVMe SSDs, and the growing popularity of hybrid storage solutions are influencing the market dynamics.

How are the advancements in 5G technology influencing the global SSD caching market?

The rollout of 5G technology is expected to increase the demand for faster data storage and retrieval, providing opportunities for SSD caching solutions to thrive in a high-speed data environment.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com