Global Surgical Power Tools Market Size, Share, Trends, COVID-19 Impact & Growth Analysis Report – Segmented By Product (Handpiece, Disposable, Accessories), Technology, Devices Type, Application, Distribution, End-User & Region (North America, Europe, APAC, Latin America, Middle East and Africa) – Industry Analysis From 2025 to 2033

Global Surgical Power Tools Market Report Summary

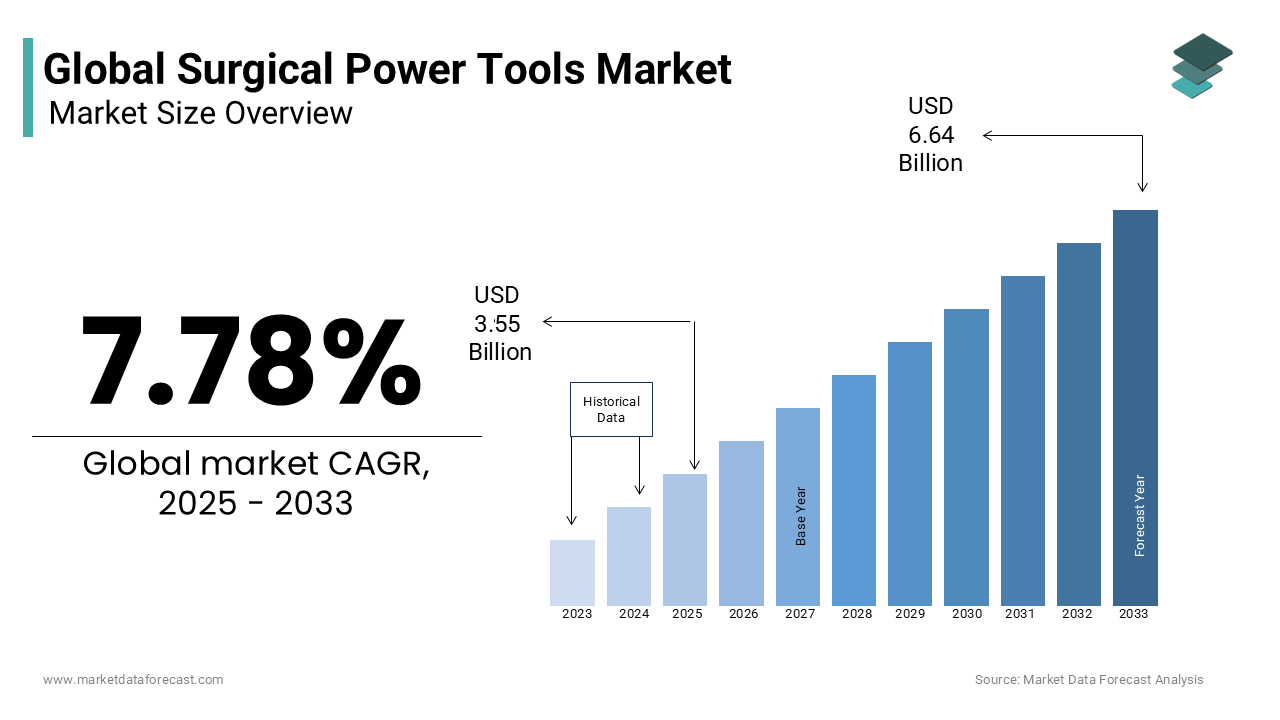

The global surgical power tools market was valued at USD 3.55 billion in 2025 and is projected to reach USD 6.46 billion by 2033, growing at a CAGR of 7.78% during the forecast period from 2025 to 2033. Market growth is driven by rising neurological and orthopedic disorders, increasing geriatric populations, and rapid adoption of electric and battery-powered surgical systems. The shift toward minimally invasive procedures, advancements in high-torque power tools, and continuous integration of robotics and precision-driven surgical devices further contribute to the market’s expansion. Additionally, growing investments in hospital infrastructure and R&D for safer, ergonomic, and more efficient powered instruments continue to strengthen global demand.

Key Market Trends

- Increasing preference for electric and battery-driven tools due to higher torque consistency, reduced vibration, and improved safety.

- Growing adoption of powered instruments in orthopedic, neurosurgical, ENT, and dental procedures driven by rising procedural volumes.

- Expansion of minimally invasive and robot-assisted surgeries requires advanced precision tools.

- Continuous product innovation focused on lightweight ergonomics, improved sterilization features, and enhanced performance.

- Strengthening investments in healthcare infrastructure and R&D, particularly in emerging markets.

Segmental Insights

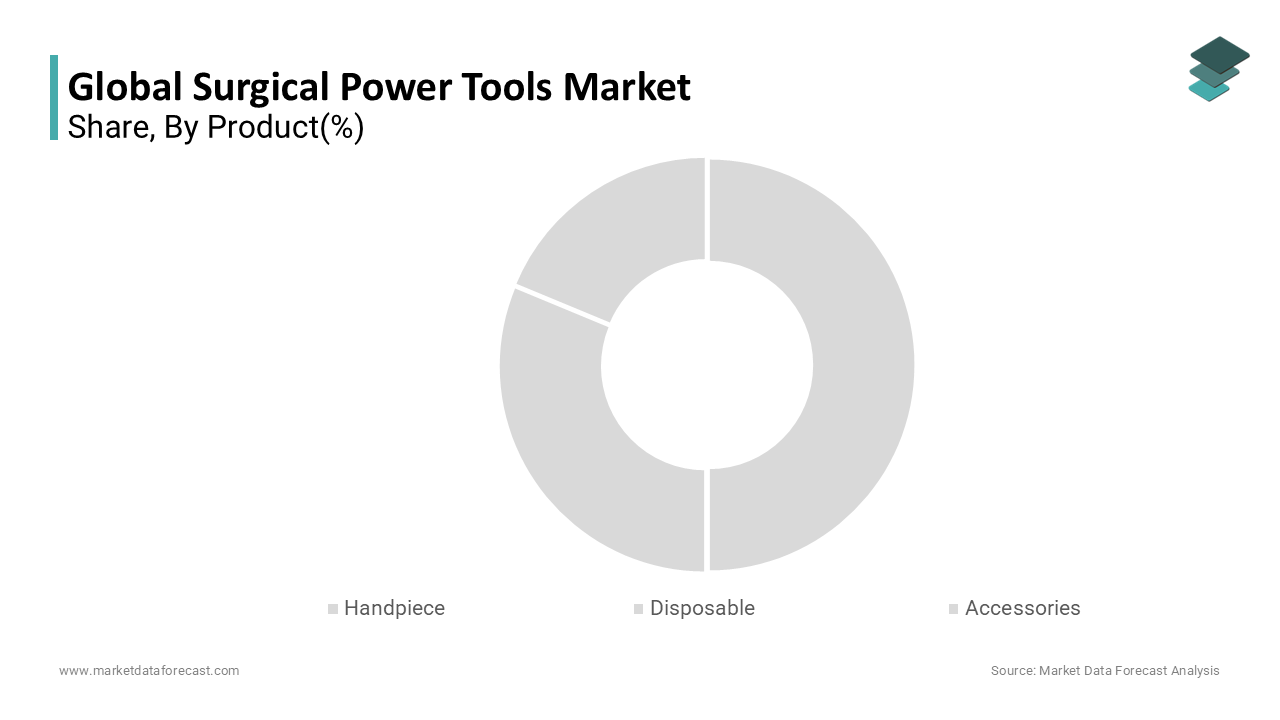

- Based on product, handpieces held the largest share of the global surgical power tools market in 2024, driven by their efficiency, compatibility with multiple attachments, and improved surgical control.

- Based on technology, electric-powered tools dominated the market in 2024 due to their consistent torque delivery, lower maintenance requirements, and widespread replacement of pneumatic systems across surgical specialties.

- Based on device type, large bone power tools contributed significantly to market growth owing to rising orthopedic conditions such as osteoarthritis, hip fractures, and osteoporosis, and increasing demand for hip and knee arthroplasty procedures.

Regional Insights

- North America was the leading region in 2023, supported by advanced healthcare infrastructure, strong reimbursement systems, and high procedural volumes across orthopedic and neurosurgical specialties.

- Europe held the second-largest share, driven by increasing surgical procedures, adoption of modern powered instruments, and strong medical device innovation in countries such as Germany, the UK, France, and Italy.

- Asia-Pacific is expected to witness the fastest growth due to rising healthcare investments, expanding access to advanced surgeries, and growing orthopedic disorder prevalence in China, Japan, and India.

- China accounted for a major share of the APAC market, supported by rapid hospital expansion, technological adoption, and a large aging population requiring orthopedic care.

Competitive Landscape

The global surgical power tools market is dominated by established medical device manufacturers focusing on high-performance power systems, ergonomic design, and continuous product innovation. Companies increasingly invest in electric and battery-driven technologies, strategic partnerships, and expansion into emerging markets to strengthen market presence. Emphasis on durability, safety, sterility, and precision remains central to competitive positioning. Aesculapius Farmaceutici Srl, Anthrax Solution, Aygun Surgical Instrument, B. Braun Melsungen AG, Ceterix Orthopaedics, De Soutter Medical, Medtronic Plc, Stryker Co., and Zimmer Biomet are key market players.

Global Surgical Power Tools Market Size

. The market size for surgical power tools is expected to grow at a CAGR of 7.78% from 2025 to 2033 and will be worth USD 6.46 billion by 2033 from USD 3.55 billion in 2025.

Surgical power tools are powered instruments used in various surgical procedures to cut, fixate, shape, and dissect bone and emulsify, aspirate, and split soft tissue. However, these instruments are generally utilized for various purposes, including surgery on bone or bone fragments. These power tools are also used for screwing, reaming, drilling, and other operations. It includes a handpiece, disposables, and various extras. Sports medicine, reconstructive and extremities surgery, spinal, neurosurgery, and ENT (ear, nose, and throat) operations use surgical power tools. Electric handpieces and air-driven handpieces are the two most common surgical handpieces; however, due to the rapid research and development activities, high-torque electric handpieces have also been developed. Orthopedic surgery, ENT surgery, neurology surgery, dental surgery, and cardiothoracic surgery are a few of the major surgical procedures that can benefit from these technologies. The development of such power instruments has transformed surgical techniques by making the entire procedure more efficient and flawless. Surgical power tools are medical instruments that operate with an additional power source. Surgical power tools let surgeons conduct specific tasks during a surgical procedure, such as changing biological tissue or gaining access to examine an organ.

MARKET DRIVERS

The growing incidence of neurological disorders and the aging population primarily drive the surgical power tools market growth.

The increasing prevalence of neurological disorders is majorly driving the market growth because neurological disorders lead to significant death and disability causes across the globe. Also, due to its beneficial factors, such as improved reliability, high performance, and a longer life cycle, there has been a significant increase in the adoption of surgical power tools over the forecast period. Furthermore, the growing geriatric population across the globe is considered one of the key growth contributors to the market. Because the senior population is more suspectable to various neurological disorders, and in recent years, there has been a significant increase in the number of health disorders such as osteoarthritis, hip fractures, and osteoporosis. As a result of this circumstance, the number of substantial bone procedures such as hip and knee arthroplasty has increased. Therefore, the worldwide surgical power tools market is expected to witness an upward sales curve over the forecast period.

In addition, the advanced technological advancements in the healthcare sectors and the growing adoption of innovative surgical power tools, large bone orthopedic saws, arthroscopic shavers, surgical staplers, powered ENT devices, and surgical robots are accelerating the market growth. Pneumatic surgical drills are frequently replaced with electrically powered neurosurgery drills. This is due to their low cost and self-sufficient power system; electric motors are expected to be in high demand in the following years.

Moreover, increasing investments and funding by the government and private organizations on research and development activities and the advancement of healthcare infrastructure support market growth. Therefore, rising research and development activities are expected to provide lucrative growth opportunities for manufacturers to introduce new products into the market.

MARKET RESTRAINTS

On the other hand, the high cost of surgical devices is the primary concern for market growth. Other constraints limiting market growth include the high cost of power tool repair and replacement parts and changes in raw material costs.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product, Technology, Devices Type, Application, Distribution, End-User & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leader Profiled | Aesculapius Farmaceutici Srl, Anthrax Solution, Aygun Surgical Instrument, B. Braun Melsungen Ag, Ceterix Orthopaedics, De Soutter Medical, Medtronic Plc, Stryker Co, and Zimmer Biomet. |

SEGMENTAL ANALYSIS

By Product Insights

Based on the product, the handpiece segment accounted significant share of the global surgical power tools market in 2024 and it is likely to continue its dominance during the forecast period. The handpiece product segment is driven owing to its beneficial factors such as smooth surgical delivery, automatic power optimization, and high compatibility.

By Technology Insights

Based on technology, the electric-powered power tools segment commanded a substantial market share since this instrument provides continuous torque even under high resistance and load. Furthermore, by introducing electrically operated power tools, enhanced safety precautions associated with accidental accidents have been reduced, accelerating the market expansion.

By Device Type Insights

Based on the device type, the large bone power tools held a significant share in 2023 in the global surgical power tools market and are anticipated to continue the dominating trend during the forecast period owing to the increasing prevalence of osteoarthritis, hip fractures, osteoporosis, and other significant bone injuries. In addition, however, the rising number of knee arthroplasty procedures, among others, is creating a lucrative development opportunity for the market.

By Application Insights

Based on the application, orthopedic surgery is projected to record a considerable share in the market during the forecast period in the global surgical power tools market due to the growing adoption of minimally invasive surgical procedures and the growing number of road accidents and sports.

By Distribution Channel Insights

Based on the distribution channel, the direct tender segment is likely to register a healthy share during the forecast period of low-cost device procurement and large dependence of hospitals among other end users on direct tenders.

By End-User Insights

Based on the end-user, the hospital segment dominated most of the market share in the global market due to the increasing patient population, rising number of surgeries, and high healthcare investments.

REGIONAL ANALYSIS

Geographically, the North American market dominated the global surgical power tools market in 2023 and it is anticipated to continue its dominance throughout the forecast period. The regional market growth is driven by the growing healthcare sector, the presence of advanced healthcare infrastructure, and favorable reimbursement policies. In addition, the presence of significant market players and the global level leading countries such as the United States and Canada are expanding the regional market growth. The United States is the primary growth contributor in the region. Technological advancements, high healthcare expenditure, and leading manufacturing companies are fuelling market growth. On the other hand, Canada is estimated to record a promising share in the market during the forecast period.

Europe was the second-largest market in the global surgical power tools market in 2020, and it is estimated to account for a substantial share during the forecast period. The increasing number of Orthopedic surgeries, growing demand for effective surgical power tools, and the evolving healthcare sector. Further, emerging countries such as Germany, the UK, Italy, France, and Spain are the growth contributors in the region. The UK is anticipated to register a prominent share in the European surgical power tools market. The factors such as increasing investments in research and development activities, the growing need for surgical power tools and the geriatric population and neurological disorders are boosting the market growth.

The Asia Pacific is projected to grow significantly during the forecast. Rising urbanization, healthcare sector improvement, and favorable reimbursement policies propel market growth. There has been a significant increase in health disorders such as osteoarthritis, hip fractures, and osteoporosis across the region in recent years. As a result of this scenario, the number of significant bone procedures such as hip and knee arthroplasty has increased. In addition, countries such as China, Japan, and India significantly contribute to the APAC regional market growth.

China accounted for the largest market share in the APAC surgical power tools market, and it is expected to record a substantial share in this region during the forecast period. The growing geriatric population, increasing prevalence of orthopedic disorders and technological advancements in the sector boost the market growth.

Further, the Indian market is projected to grow at a promising rate in the coming period. Increasing government initiatives through medical awareness programs, improving the healthcare sector, and enhancing industrial manufacturing facilities and infrastructure improvement are contributing to the market growth in the country.

KEY MARKET PARTICIPANTS

Some of the companies that are playing a dominating role in the global surgical power tools market include

- Aesculapius Farmaceutici Srl

- Anthrax Solution

- Aygun Surgical Instrument

- B. Braun Melsungen Ag

- Ceterix Orthopaedics

- De Soutter Medical

- Medtronic Plc

- Stryker Co

- Zimmer Biomet

RECENT HAPPENINGS IN THIS MARKET

- In June 2021, Stryker announced a collaboration with Texas Health Hospital Mansfield. The hospital will use the whole Stryker product line to help it on its quest to eradicate harm in the operating room for both healthcare providers and patients and this aids the company's future sales growth.

- Beijing, China, 25 October 2019 - Johnson & Johnson Medical (Shanghai) Ltd. Made an agreement for a co-marketing and distribution deal and an R&D collaboration with TINAVI, the Chinese orthopedic robots industry leader. This collaborative partnership enables DePuy Synthes1, the orthopedics division of Johnson & Johnson Medical Devices Companies*, to deliver TINAVI's robotic spine and trauma surgery solutions to the highly competitive Chinese orthopedics implant market.

MARKET SEGMENTATION

This research report on the surgical power tools market is segmented and sub-segmented into the following categories.

By Product

- Handpiece

- Disposable

- Accessories

By Technology

- Electric-operated power tools

- Battery-driven power tools

- Pneumatic power tools

- Others

By Device Type

- Large Bone Power Tools

- Small Bone Power Tools

- Medium Bone Power Tools

- Others

By Application

- Dental surgery

- Orthopedic surgery

- ENT surgery

- Cardiothoracic

- Surgery

- Neurology surgery

- Others

By Distribution Channel

- Direct Tenders

- Third-Party Distribution

By End-User

- Hospitals

- Ambulatory Surgical Centers (ASC)

- Clinics

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

Who are the key players in the surgical power tools market?

Stryker Corporation, Medtronic plc, Johnson & Johnson, Conmed Corporation, Zimmer Biomet Holdings, Inc. and B. Braun Melsungen AG are some of the notable companies in the surgical power tools market.

What factors are driving the growth of the surgical power tools market?

The global surgical power tools market is valued at USD 3.29 bn in 2024.

What is the Global Surgical Power Tools Market?

It refers to powered surgical instruments used in orthopedic, neurosurgery, ENT, and other procedures for cutting, drilling, reaming, sawing, and driving implants.

What types of surgical power tools are commonly used?

Drills, saws, reamers, staplers, shavers, battery-powered tools, and pneumatic power tools.

Which segment dominates the surgical power tools market?

Battery-powered surgical tools dominate due to improved portability, safety, efficiency, and reduced risk of infections.

What are the key applications of surgical power tools?

Orthopedics, neurosurgery, cardiothoracic surgery, ENT procedures, dental surgery, and plastic/reconstructive surgeries.

Who are the main end users of these tools?

Hospitals, ambulatory surgical centers, specialty clinics, and orthopedic centers.

What technological advancements are shaping the market?

Introduction of lightweight motors, improved sterilizable batteries, cordless systems, and integration of smart sensors.

What challenges are faced by the surgical power tools industry?

High cost, maintenance requirements, frequent sterilization needs, and risk of cross-contamination if not handled properly.

What is the long-term outlook for the global surgical power tools market?

The market is expected to grow steadily, driven by rising surgical cases, aging populations, and continuous technological innovation.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com