UK White Goods Market Size, Share, Trends, and Growth Analysis Report, Segmented by End-User, Type and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

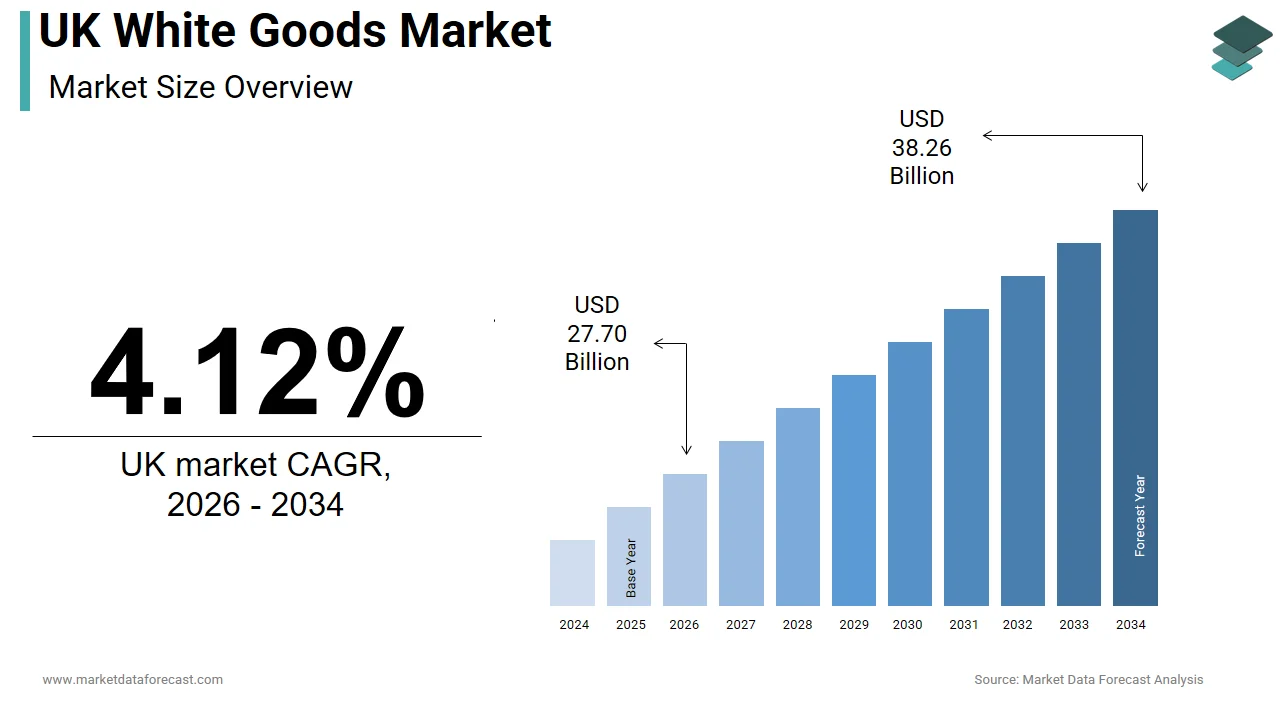

$26.60 BnMarket Estimate, 2026

$27.70 BnMarket Forecast, 2034

$38.26 BnCAGR, 2026–2034

4.12%UK White Goods Market Report Summary

The UK white goods market was valued at USD 26.60 billion in 2025, is estimated to reach USD 27.70 billion in 2026, and is projected to reach USD 38.26 billion by 2034, growing at a CAGR of 4.12% from 2026 to 2034. Market growth is driven by rising demand for energy-efficient household appliances, increasing adoption of smart home technologies, and growing consumer spending on home improvement products. White goods such as refrigerators, washing machines, dishwashers, ovens, and cleaning equipment remain essential household appliances, supporting consistent market demand. The growing focus on sustainability, energy conservation, and connected appliance ecosystems is further contributing to market expansion across the United Kingdom.

Key Market Trends

- Rising demand for energy-efficient and environmentally friendly appliances.

- Increasing adoption of smart and connected home appliances.

- Growing consumer preference for premium and multifunctional household equipment.

- Expansion of replacement demand driven by appliance upgrades and modernization.

- Increasing focus on sustainable manufacturing and energy-saving technologies.

Segmental Insights

- Based on end user, the household segment dominated the UK white goods market in 2025, driven by strong demand for essential home appliances and increasing investments in home modernization and convenience-oriented products.

- Based on type, the cleaning equipment segment led the market by accounting for 38.7% share in 2025, supported by the essential role of laundry and hygiene maintenance in daily household activities and growing demand for advanced washing and cleaning solutions.

Country Analysis

- The United Kingdom held a significant position in the European white goods market by accounting for 21.4% share in 2025, supported by high household appliance penetration, rising consumer demand for smart home technologies, and growing replacement purchases of aging appliances. Increasing awareness regarding energy-efficient products and government initiatives promoting sustainability are further supporting long-term market growth.

Competitive Landscape

The UK white goods market is characterized by strong competition among global appliance manufacturers focusing on product innovation, energy efficiency, and smart connectivity features. Market participants are emphasizing the development of connected appliances, sustainable technologies, and premium product portfolios to strengthen market positioning. Strategic partnerships, product launches, and investments in advanced manufacturing and digital technologies are shaping competitive dynamics across the market.

Prominent companies operating in the UK white goods market include BSH Hausgeräte, Whirlpool Corporation, Electrolux Group, Samsung Electronics, LG Electronics, Haier Group, Beko UK Ltd, Miele, Hisense, and Smeg.

UK White Goods Market Size

The UK white goods market was valued at USD 26.60 billion in 2025, is estimated to reach USD 27.70 billion in 2026, and is projected to reach USD 38.26 billion by 2034, growing at a CAGR of 4.12% from 2026 to 2034.

White goods refer to major household appliances used for routine domestic tasks like cooking, cleaning, and food preservation. This market has a mature consumer base where replacement demand significantly outweighs new housing installations due to the established nature of the property market. The industry operates within a highly regulated environment focused on energy efficiency and environmental sustainability, driven by both national legislation and consumer preference. According to data from the Office for National Statistics, there are approximately 28 million households in the United Kingdom, establishing a substantial consumer base for the domestic appliance market. The average lifespan of major appliances has extended due to technological improvements, yet consumer desire for smart connectivity and enhanced functionality drives earlier replacement cycles. According to reporting from the Department for Energy Security and Net Zero, the residential sector accounts for approximately 30% of total UK energy consumption, with domestic white goods contributing significantly to a home's specific electricity usage. This statistic underscores the critical role of energy-efficient models in meeting national carbon reduction targets. The market is also influenced by the rise of online retail channels, which now account for a significant share of appliance sales, offering consumers greater choice and price transparency. Manufacturers are increasingly integrating Internet of Things capabilities into their products, allowing for remote monitoring and predictive maintenance. These technological advancements, coupled with strict eco design regulations, shape the competitive landscape, requiring continuous innovation in product design and operational efficiency to meet the evolving needs of British consumers.

MARKET DRIVERS

Stringent Energy Efficiency Regulations and Consumer Cost Savings

The implementation of stringent energy efficiency regulations and the consequent consumer desire for cost savings are the main reasons behind the growth of the UK white goods market. This trend compels the adoption of newer, more efficient appliances. The reintroduction of the A to G energy label scale by the UK government has simplified consumer understanding of energy performance, making high-efficiency models more attractive. According to data often cited by the Energy Saving Trust, upgrading an old, inefficient refrigerator to a modern energy-efficient model can save a household significantly on electricity bills, with estimates often ranging between £40 and £60 annually, depending on the specific model size and efficiency gap. This financial incentive is particularly potent during periods of high energy prices, which have been a significant concern for British families in recent years. The Ecodesign for Energy Related Products Regulations mandate minimum efficiency standards for new appliances, ensuring that inefficient models are phased out of the market. According to research, consumers are increasingly willing to pay a premium for appliances with higher energy ratings due to the long-term savings they offer. This shift in purchasing behavior drives manufacturers to innovate and produce advanced compressor and motor technologies that reduce power consumption. The regulatory framework not only protects the environment but also provides a clear value proposition for consumers looking to reduce their household expenditure. This alignment of regulatory pressure and economic benefit creates a robust demand for upgraded white goods that deliver superior performance and lower operating costs.

Integration of Smart Home Technology and Connectivity

The rapid integration of smart home technology and connectivity features further contributes to the growth of the UK white goods market. This enhances user convenience and enables advanced functionality. Modern consumers increasingly seek appliances that can be controlled remotely via smartphones and integrated into broader home automation ecosystems. As per various surveys, nearly 40-50% of UK households now own at least one smart home device, indicating a rapidly growing comfort level with connected technology. Smart washing machines and dishwashers allow users to start cycles, remotely monitor progress, and receive maintenance alerts, which appeals to busy lifestyles. The ability to optimize energy usage through smart scheduling further enhances the appeal of these appliances. According to a study, the demand for Wi-Fi-enabled appliances has grown significantly, with younger demographics leading the adoption curve. Manufacturers are responding by embedding sensors and artificial intelligence into their products to provide personalized usage insights and predictive diagnostics. This technological evolution transforms white goods from static utilities into interactive components of the digital home. The convenience of automated reordering for detergents and remote troubleshooting reduces the burden of household management. As broadband penetration remains high across the United Kingdom, the infrastructure supports the seamless operation of connected appliances. This trend drives replacement demand as consumers upgrade older non-connected units to participate in the smart home ecosystem, thereby sustaining market growth.

MARKET RESTRAINTS

Economic Volatility and Reduced Disposable Income

Economic volatility and reduced disposable income are hampering the expansion of the UK white goods market. This delays replacement cycles and shifts consumer preference toward budget options. High inflation rates and rising living costs have squeezed household budgets, forcing many consumers to postpone non-essential purchases, including appliance upgrades. According to data from the Office for National Statistics, pressures on real household disposable income have reduced purchasing power, aligning with separate industry consumer confidence indexes (like GfK) that show a marked decline in consumer willingness to make major purchases. When existing appliances break down, consumers are increasingly opting for repairs or purchasing second-hand units rather than investing in new premium models. This behavior extends the lifespan of older, less efficient appliances, which contradicts sustainability goals and reduces sales volume for manufacturers. According to studies, there has been a noticeable shift in market share from premium brands to value-oriented retailers as shoppers prioritize affordability over advanced features. The uncertainty surrounding future economic conditions makes consumers hesitant to commit to high upfront costs, even if long-term savings are promised. This financial caution impacts the entire supply chain from manufacturers to retailers, who must adjust inventory levels and promotional strategies to match reduced spending power. The prolonged replacement cycle also means that innovation adoption slows down as fewer new units enter the market. This economic restraint creates a challenging environment for growth, requiring companies to focus on value propositions and flexible financing options to maintain sales momentum.

Supply Chain Disruptions and Raw Material Scarcity

Supply chain disruptions and raw material scarcity also hinder the UK white goods market. This increases production costs and causes delivery delays. The global shortage of semiconductors and other critical components has impacted the manufacturing of smart appliances and electronic control boards essential for modern white goods. According to manufacturing and logistics data, component shortages and global transit bottlenecks have caused lead times for certain domestic appliances to extend, matching broader operational constraints highlighted in the Confederation of British Industry (CBI) industrial trends surveys. The reliance on imported materials such as steel, aluminum, and copper exposes manufacturers to volatile commodity prices, which erode profit margins. These increased costs are often passed on to consumers, resulting in higher retail prices that further dampen demand. According to sources, the complexity of global supply chains makes them vulnerable to geopolitical tensions and trade barriers, which can disrupt the flow of goods. The post Brexit regulatory environment has added layers of administrative complexity and customs checks that slow down imports into the United Kingdom. Retailers face challenges in maintaining adequate stock levels, leading to lost sales opportunities when popular models are unavailable. The unpredictability of supply forces companies to hold larger inventories, which ties up capital and increases storage costs. These operational challenges hinder the ability of manufacturers to respond quickly to market demands and introduce new products efficiently. The market will continue to face constraints until supply chain stability is restored. These constraints will limit growth and increase operational risks for all participants.

MARKET OPPORTUNITIES

Expansion of Circular Economy and Refurbishment Services

The expansion of circular economy practices and refurbishment services offers a strong opening for the UK white goods market. This growth effectively addresses sustainability concerns while simultaneously catering to budget-conscious consumers. There is growing interest in extending the lifecycle of appliances through professional repair, remanufacturing, and resale, which aligns with environmental goals and waste reduction targets. According to data from the climate action NGO WRAP and electrical recycling bodies, the UK generates substantial amounts of electrical and electronic waste annually, emphasizing the critical need for robust circular economy and end-of-life management frameworks. Companies that establish robust take back schemes and certified refurbishment programs can capture value from used appliances while building brand loyalty. The right to repair legislation encourages manufacturers to design products that are easier to fix and provide spare parts for longer periods. According to consumer surveys, a significant portion of shoppers are open to buying refurbished appliances if they come with warranties and quality guarantees. This segment allows retailers to offer lower price points without compromising on reliability, appealing to students and first-time buyers. Partnerships with independent repair networks can enhance service coverage and customer satisfaction. The development of digital platforms for trading in old appliances simplifies the process for consumers and ensures proper recycling of materials. By embracing circular business models, companies can differentiate themselves in a crowded market and contribute to national sustainability objectives. This approach not only opens new revenue streams but also strengthens corporate social responsibility profiles which are increasingly important to modern consumers.

Growth in Built-In and Integrated Appliance Segments

The growth in built-in and integrated appliance segments offers a transformative opportunity for the UK white goods market. This is driven by trends in home renovation and interior design. Consumers are increasingly prioritizing aesthetic coherence in their kitchens and utility rooms, leading to higher demand for appliances that blend seamlessly with cabinetry. According to insights from the Kitchen Bathroom Bedroom Specialists Association (KBSA), kitchen renovations remain a highly popular home improvement priority, with homeowners consistently investing in premium, integrated design solutions. Built-in refrigerators, dishwashers, and ovens offer a streamlined look that appeals to those seeking a minimalist and modern aesthetic. This trend is particularly strong in urban areas where space optimization is crucial and every square inch of storage matters. According to studies, the premium segment of the market is driving this growth as consumers view integrated appliances as a mark of luxury and sophistication. Manufacturers are responding by developing slimline and customizable units that fit standard cabinet dimensions while offering advanced features. The collaboration between appliance makers and kitchen designers facilitates smoother installation and better customer experiences. The higher margin potential of built-in products compared to freestanding units provides financial incentives for retailers to promote these options. As housing stock ages and homeowners choose to improve rather than move, the demand for integrated solutions is expected to rise. This segment allows companies to tap into the lucrative home improvement market and build long-term relationships with customers through design-led offerings.

MARKET CHALLENGES

Complexity of Regulatory Compliance and Eco Design Standards

The complexity of regulatory compliance and evolving eco-design standards is a major limitation to the UK white goods market. This increases development costs and time to market. Manufacturers must navigate an intricate web of regulations concerning energy efficiency, material sourcing, recyclability, and chemical usage, which vary across different jurisdictions. Under enforcement frameworks monitored by the Office for Product Safety and Standards (OPSS), compliance with UK Ecodesign Regulations demands rigorous product testing and extensive technical documentation to ensure market access. The frequent updates to these standards force companies to continuously redesign products and update manufacturing processes to remain compliant. According to studies, the cost of certification and testing has risen significantly, placing a burden on smaller manufacturers who lack dedicated regulatory teams. The divergence between UK and EU regulations post Brexit adds another layer of complexity, requiring separate compliance strategies for different markets. Failure to meet these standards can result in hefty fines, product recalls, and reputational damage. The need to balance regulatory requirements with consumer expectations for performance and price creates a delicate engineering challenge. Additionally, the push for greater recyclability requires changes in material composition, which may affect durability or aesthetics. Keeping pace with these regulatory changes demands significant investment in research and legal expertise. This ongoing compliance burden slows down innovation and increases operational overheads, making it difficult for companies to maintain agility in a fast-moving market.

Shortage of Skilled Installation and Repair Technicians

The shortage of skilled installation and repair technicians significantly impedes the expansion of the UK white goods market. This labor gap directly impacts overall customer satisfaction and the quality of after-sales service. As appliances become more technologically advanced, the need for specialized knowledge to install and fix them has increased. However, the industry faces a declining pool of qualified engineers due to an aging workforce and insufficient training pipelines. Reports from the Electrical Contractors Association (ECA) highlight a critical skills gap within the UK electrotechnical sector, which mirrors broader labor shortages and extended service wait times across the domestic appliance repair market. Delayed installations and repairs can result in negative reviews and loss of brand loyalty as consumers expect immediate service for essential household items. The complexity of smart appliances requires technicians to be proficient in both mechanical and digital systems, which raises the bar for entry into the profession. According to recruitment data, finding staff with the right combination of technical and customer service skills is increasingly difficult and expensive. This labor shortage increases operational costs for service providers who must offer higher wages to attract talent. It also limits the capacity of companies to expand their service networks into rural areas. The inability to provide timely support undermines the value proposition of premium appliances and can deter consumers from upgrading. Addressing this challenge requires industry-wide investment in vocational training and apprenticeship programs to ensure a sustainable supply of skilled workers for the future.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By End-User, Type, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United Kingdom |

| Market Leaders Profiled | BSH Hausgeräte, Whirlpool Corporation, Electrolux Group, Samsung Electronics, LG Electronics, Haier Group, Beko UK Ltd., Miele, Hisense, Smeg, and Others. |

SEGMENTAL ANALYSIS

By End User Insights

The household segment accounted for a substantial enough share to become the largest in the UK white goods market in 2025. High rates of home ownership and the consistent need to replace aging appliances within residential properties have supported the prominence of this segment. According to data from the Office for National Statistics, approximately 65% of UK households are owner-occupied, representing a large consumer segment that traditionally seeks long-term property maintenance and efficiency solutions. The average age of housing stock in the UK means that many homes require regular upgrades to kitchen and laundry facilities to meet modern expectations. According to appliance industry lifecycle standards, the typical lifespan of a major domestic washing machine or refrigerator averages between 10 and 15 years, naturally establishing a predictable market cycle for replacement units. This natural turnover ensures a baseline demand that is less susceptible to economic fluctuations compared to commercial sectors. Homeowners are increasingly viewing white goods as long-term investments, leading to higher spending on premium models with advanced features. The stability of the residential sector provides manufacturers with a reliable revenue stream, allowing them to plan production and inventory more effectively. Furthermore, the emotional connection consumers have with their homes drives frequent renovations and updates, which often include new appliance purchases. This deep-rooted demand structure cements the household segment as the primary driver of volume and value in the UK white goods market.

Consumer preference for energy efficiency and smart home integration further strengthens the dominance of this segment by aligning product offerings with modern lifestyle values and cost-saving goals. British homeowners are increasingly aware of the environmental impact and running costs of their appliances, prompting a shift toward high-efficiency models. Sources highlight that a large majority of UK consumers actively use energy efficiency ratings as a core deciding factor when purchasing new white goods. The desire to reduce household bills has accelerated the adoption of A-rated refrigerators and heat pump tumble dryers, which offer significant long-term savings. Additionally, the rise of smart home technology has made connected appliances highly desirable for tech-savvy households who value remote control and automation. According to research, sales of Wi Fi enabled washing machines and ovens have grown substantially as users seek convenience and enhanced functionality. Manufacturers respond to this demand by integrating artificial intelligence and IoT capabilities into residential products, creating a competitive landscape focused on innovation. The ability to monitor energy usage and receive maintenance alerts via smartphone apps adds tangible value for homeowners. This convergence of sustainability and technology ensures that the household segment remains at the forefront of market growth, driving continuous product development and consumer engagement.

The hospitality segment is anticipated to witness the fastest CAGR of 4.8% over the forecast period, owing to the robust post-pandemic recovery and surge in tourism. Hotels, restaurants, and catering establishments are investing heavily in upgrading their commercial kitchens and laundry facilities to meet increased guest expectations and operational demands. According to VisitBritain's inbound tourism forecasts, international visitor numbers are projected to rebound strongly, surpassing 2019 records by 2025, which serves to bolster occupancy rates and food service volumes across the UK. This resurgence necessitates the replacement of worn-out equipment and the installation of high-capacity commercial-grade appliances such as industrial dishwashers, large refrigeration units, and professional cooking ranges. The competitive nature of the hospitality sector forces businesses to maintain high standards of hygiene and efficiency, which drives demand for reliable and advanced white goods. According to the trade body UKHospitality, many establishments are undergoing strategic renovations to modernize their facilities, driving secondary demand for updated commercial appliances. The need for faster turnover and greater throughput in commercial kitchens requires equipment that can handle intensive use without compromising performance. This operational pressure creates a steady stream of demand for durable and high-performance white goods. The expansion of the boutique hotel and fine dining sectors also contributes to this growth, as these segments often prioritize premium and specialized equipment to enhance their service offerings.

The adoption of commercial-grade energy-efficient solutions accelerates the growth of the hospitality segment by helping businesses manage rising operational costs and meet sustainability targets. Hospitality operators face significant pressure to reduce energy consumption due to high utility bills and corporate social responsibility commitments. As per guidelines from the Carbon Trust, commercial kitchens are among the most energy-intensive areas in any building, making efficiency upgrades a priority. Modern commercial refrigeration and cooking equipment offer substantial energy savings compared to older models through improved insulation and smarter control systems. The introduction of strict environmental regulations for commercial buildings further incentivizes the adoption of green technologies. Manufacturers are developing specialized commercial lines that combine high performance with low energy usage, appealing to cost-conscious hoteliers and restaurateurs. The ability to demonstrate sustainable practices also enhances brand reputation among environmentally conscious travelers. This dual benefit of cost reduction and ethical alignment drives rapid procurement of new equipment in the hospitality sector. As the industry continues to professionalize and standardize its operations, the demand for advanced commercial white goods will remain strong, sustaining high growth rates.

By Type Insights

In 2025, the cleaning equipment segment held the majority share of 38.7% of the UK white goods market because of the essential nature of laundry and hygiene maintenance in daily life. Unlike other appliances that may be used intermittently, cleaning equipment is required frequently by almost every household and business, ensuring consistent demand. The frequent use shortens the effective lifespan of machines, prompting earlier replacements compared to less-utilized appliances. Also, the cultural emphasis on cleanliness and presentation in the UK further drives the need for reliable and effective cleaning solutions. The introduction of hybrid washer dryer units has also boosted sales by offering space-saving solutions for urban apartments where separate units are not feasible. The reliability of cleaning equipment is paramount for consumers, leading to strong brand loyalty and willingness to invest in quality products. This fundamental necessity ensures that the cleaning equipment segment remains the largest contributor to market volume and revenue.

Technological advancements in fabric care significantly drive the top position of this segment by offering superior performance and convenience that appeal to modern consumers. Innovations such as steam cleaning, allergen removal programs, and automatic detergent dispensing have transformed washing machines from basic utilities into sophisticated care systems. The integration of smart sensors that adjust water and energy usage based on load size enhances efficiency and reduces environmental impact. Heat pump technology in tumble dryers has also gained traction due to its energy efficiency and gentle drying capabilities. These technological improvements justify higher price points and encourage consumers to upgrade from older models. The continuous innovation in cleaning technologies keeps the segment dynamic and attractive to buyers seeking the latest features. This focus on enhanced performance and user experience sustains the leadership of cleaning equipment in the UK white goods market.

The heating and cooling equipment segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 6.2% between 2026 and 2034 due to the national transition away from gas boilers toward electrified heating solutions. The government’s commitment to net zero emissions has led to policies that discourage the installation of new gas boilers and promote alternative technologies such as air source heat pumps. Air source heat pumps, which function similarly to reverse cycle air conditioners, are classified under white goods in many contexts due to their indoor unit components and installation requirements. The phasing out of fossil fuel heating creates a massive replacement market for millions of homes across the United Kingdom. According to sources, the demand for electric heating solutions is expected to multiply in the coming decade as regulatory deadlines approach. This structural shift in home heating infrastructure drives significant growth for manufacturers of heating and cooling appliances. The need for efficient climate control in both winter and summer further supports this trend as weather patterns become more extreme. This regulatory and environmental push positions heating and cooling equipment as the most rapidly expanding category in the market.

The increasing demand for climate control comfort accelerates the growth of the heating and cooling segment as consumers seek to improve indoor living conditions amidst changing weather patterns. Rising summer temperatures in the UK have led to a surge in demand for air conditioning and cooling systems, which were previously considered luxury items. Moreover, the need for efficient heating during colder months remains critical, driving sales of advanced radiators and electric heaters. The integration of smart thermostats and zoned heating controls allows users to optimize comfort while managing energy costs. This dual demand for heating and cooling creates a year-round market for climate control appliances. Manufacturers are responding with versatile units that offer both functions, enhancing their appeal. The growing awareness of indoor air quality also drives interest in systems with filtration capabilities. This combination of comfort-seeking behavior and technological availability fuels the rapid expansion of the heating and cooling equipment segment.

COUNTRY ANALYSIS

UK White Goods Market Analysis

The United Kingdom was positioned second in the European white goods market and captured a 21.4% share in 2025. This growth of the country’s market was propelled by a high penetration of owned appliances and a steady replacement cycle driven by an aging housing stock. The market in the UK shows a strong focus on energy efficiency and sustainability. As one of the largest consumer markets in Europe, the UK serves as a key indicator for trends in appliance innovation and environmental compliance. According to historical consumer trend data tracked via the Office for National Statistics, the vast majority of UK households own standard domestic white goods, which form the foundation of baseline market demand. One of the primary driving factors is the government’s aggressive climate change agenda, which mandates strict energy efficiency standards for all new appliances. Data originally published by the former Department for Business, Energy and Industrial Strategy (BEIS), and continued by its successor departments, indicates that UK households are heavily motivated to adopt efficiency measures by the potential for long-term cost savings on their energy bills. Also, a major point helping this market stay ahead is the widespread adoption of smart home technology, which encourages consumers to upgrade to connected devices that offer greater control and convenience. The robust retail infrastructure, including strong online channels, ensures wide accessibility and competitive pricing. Consumer awareness of environmental issues also influences purchasing decisions, with many shoppers preferring brands that demonstrate sustainable practices. The UK’s departure from the EU has led to distinct regulatory frameworks that require manufacturers to adapt their products specifically for the British market. This unique regulatory environment, combined with high consumer expectations, drives continuous innovation and maintains the UK’s status as a leading market for advanced and eco-friendly white goods.

COMPETITIVE LANDSCAPE

The competition in the UK white goods market is intense and characterized by a mix of global multinational corporations and established regional brands vying for consumer attention. Major players compete based on technological innovation, energy efficiency, and design aesthetics rather than price alone due to the commoditization of basic functions. The market is segmented between premium brands that offer advanced smart features and value-oriented brands that focus on affordability and durability. Retailers hold significant bargaining power, influencing which products gain shelf space and promotional support. The shift toward online sales has increased price transparency, forcing manufacturers to differentiate through unique selling propositions such as customization and superior customer service. Regulatory pressures regarding energy labels and recyclability create a level playing field but also raise entry barriers for new competitors. Brand loyalty remains important but is increasingly challenged by the availability of high-quality alternatives. Companies must continuously innovate to stay relevant as consumer expectations evolve toward smarter and more sustainable home solutions. The ability to provide reliable after-sales support and spare parts availability is also a critical competitive factor. Success depends on balancing innovation, cost efficiency, and environmental responsibility in a highly regulated and discerning market.

KEY MARKET PLAYERS

The major players in the UK white goods market include

- BSH Hausgeräte

- Whirlpool Corporation

- Electrolux Group

- Samsung Electronics

- LG Electronics

- Haier Group

- Beko UK Ltd

- Miele

- Hisense

- Smeg

TOP PLAYERS IN THE MARKET

- Beko UK Ltd maintains a strong presence in the United Kingdom by offering affordable and energy-efficient home appliances that cater to a wide range of consumers. The company is deeply committed to sustainability and has recently launched initiatives to promote the circular economy through repair and recycling programs. Beko has strengthened its market position by introducing smart appliances that integrate seamlessly with modern home automation systems. Their focus on innovative technologies such as heat pump tumble dryers aligns with national energy efficiency goals. By investing in local customer service and extended warranty options, Beko builds trust and loyalty among British households. These strategic actions enhance brand reputation and ensure continued relevance in a competitive retail environment focused on value and environmental responsibility.

- Whirlpool Corporation UK serves the market with a diverse portfolio of premium brands, including KitchenAid and Hotpoint, known for their quality and reliability. The company focuses on delivering superior user experiences through advanced design and durable engineering. Recently, Whirlpool has accelerated its digital transformation by enhancing connectivity features in its appliance lines, allowing users to control devices remotely. The firm has also invested in sustainable manufacturing practices to reduce its carbon footprint and meet strict regulatory standards. By expanding its service network and offering personalized support, Whirlpool strengthens customer relationships. Their commitment to innovation in cooking and cleaning technologies ensures they remain a preferred choice for consumers seeking high-performance and long-lasting household solutions in the UK.

- Samsung Electronics UK is a leading innovator in the white goods sector, renowned for its cutting-edge technology and sleek designs. The company drives market growth by integrating artificial intelligence and Internet of Things capabilities into its refrigerators, washing machines, and ovens. Recently, Samsung has expanded its Bespoke line, which allows customers to customize the appearance of their appliances to match interior decor. This personalization strategy appeals to style-conscious consumers and differentiates their products from competitors. Samsung also prioritizes energy efficiency and smart home integration, ensuring their appliances meet modern lifestyle needs. Samsung leverages strong retail partnerships to expand its reach. Through robust after-sales support, it solidifies its position as a top-tier provider of connected and stylish home appliances in the United Kingdom.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the UK white goods market primarily focus on product innovation to develop energy-efficient and smart connected appliances that meet stringent environmental regulations. Companies invest heavily in research and development to create features such as remote monitoring and automated maintenance alerts. Strategic partnerships with retailers and online platforms ensure wide distribution and visibility for new product launches. Manufacturers emphasize sustainability by using recycled materials and offering take-back schemes for old units to support circular economy goals. Enhancing after-sales service through extended warranties and rapid repair networks helps build consumer trust and brand loyalty. Digital marketing campaigns target specific demographics, highlighting cost savings and convenience benefits. These strategies enable participants to adapt to changing consumer preferences, maintain compliance with eco design standards, and drive growth in a mature and competitive market landscape.

MARKET SEGMENTATION

This research report on the UK white goods market has been segmented and sub-segmented based on the following categories.

By End-User

- Hospitals and Clinics

- Hospitality Industry

- Drycleaners and Cleaning Agencies

- Household

By Type

- Sewing Machine

- Preservation and Cooking Equipment

- Cleaning Equipment

- Heating and Cooling Equipment

Frequently Asked Questions

What is the UK white goods market?

The UK white goods market includes major household appliances such as refrigerators, washing machines, tumble dryers, dishwashers, and ovens used in homes across the United Kingdom for daily living.

Why is the UK white goods market growing?

The UK white goods market is growing due to housing development, renovation activities, replacement demand, energy-efficient appliance upgrades, and consumer preference for smart home appliances.

Who buys products from the UK white goods market?

Homeowners, renters, property developers, landlords, kitchen renovators, and new home buyers purchase from the UK white goods market for residential and rental property needs.

What products are included in the UK white goods market?

The UK white goods market includes refrigerators, freezers, washing machines, tumble dryers, dishwashers, ovens, hobs, cookers, and integrated kitchen appliances for home use.

How does energy efficiency impact the UK white goods market?

Energy efficiency drives the UK white goods market through demand for low-energy appliances, cost savings, environmental consciousness, government incentives, and compliance with energy regulations.

What challenges face the UK white goods market?

Challenges in the UK white goods market include supply chain disruptions, raw material costs, Brexit impacts, high energy prices, and competition from budget imports and online retailers.

Which demographic uses the UK white goods market most?

Homeowners, families, new tenants, and property renovators represent the largest demographics in the UK white goods market for appliance purchases and replacements.

How does smart technology affect the UK white goods market?

Smart technology shapes the UK white goods market through demand for connected appliances, remote control features, energy monitoring, app integration, and IoT-enabled home automation.

What role does replacement demand play in the UK white goods market?

Replacement demand is central to the UK white goods market, as older appliances reach end-of-life, requiring upgrades with newer, more efficient, and feature-rich models.

Is the UK white goods market competitive?

Yes, the UK white goods market is highly competitive with major appliance brands, budget manufacturers, private label products, online retailers, and continuous innovation in features.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com