U.S. Biosimilar Market Size, Share, Trends, and Growth Analysis Report, Segmented by Drug Class, Disease Indication, Distribution Channel, and Country – Industry Forecast From 2026 to 2034

U.S. Biosimilar Market Size

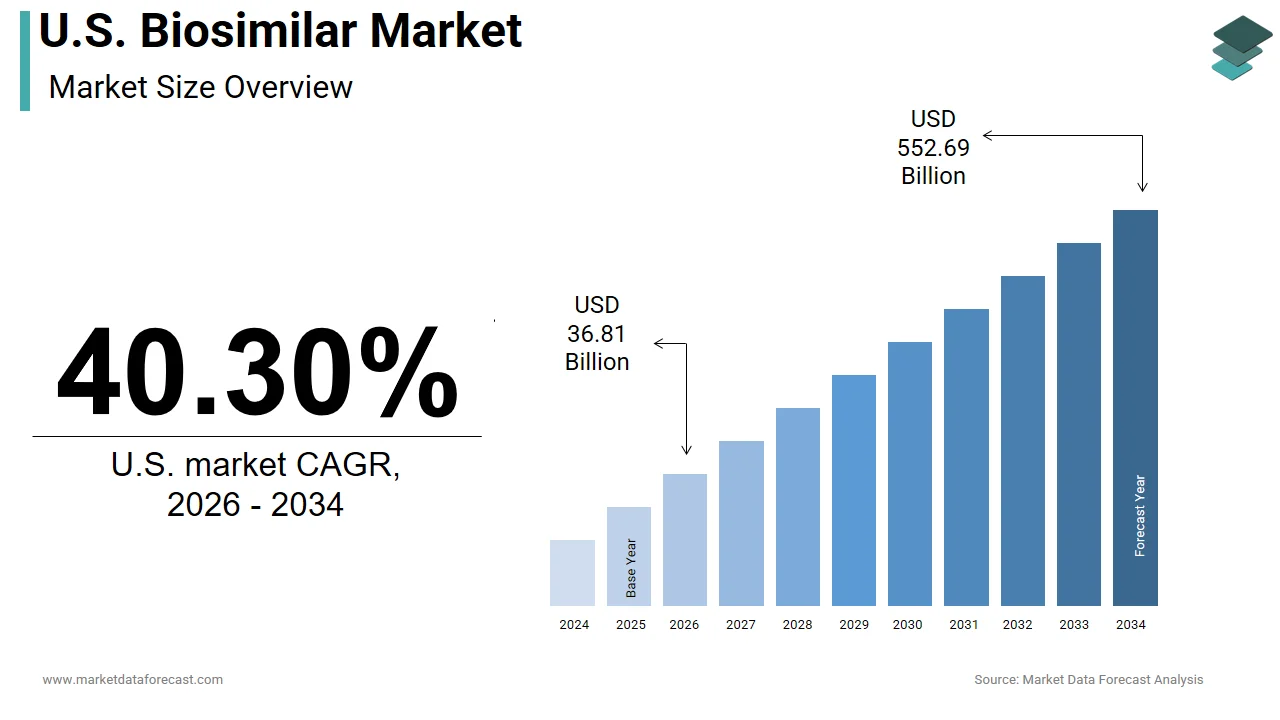

The U.S. biosimilar market was valued at USD 26.24 billion in 2025, is estimated to reach USD 36.81 billion in 2026, and is projected to reach USD 552.69 billion by 2034, growing at a CAGR of 40.30% from 2026 to 2034.

The biosimilar is pharmaceutical industry focused on biological medical products that are highly similar to already approved biological medicines, known as reference products. These agents serve as cost effective alternatives for treating complex chronic conditions, such as cancer autoimmune disorders and diabetes. As per the Food and Drug Administration, over 50 biosimilars have received approval in the United States since the passage of the Biologics Price Competition and Innovation Act in 2010. This regulatory framework was designed to increase competition and reduce healthcare costs while maintaining high standards of safety and efficacy. Cancer remains a leading cause of death with the American Cancer Society estimating nearly 2 million new cancer cases will be diagnosed in 2024. Many of these patients require biologic therapies which are often prohibitively expensive without competitive alternatives. The aging population further amplifies demand as individuals over 65 are more likely to develop conditions requiring biologic intervention. This demographic shift creates sustained pressure on the healthcare system to provide affordable treatment options. Biosimilars offer a viable solution by lowering out of pocket costs for patients and reducing expenditure for payers. The integration of these products into clinical practice reflects a broader effort to enhance accessibility and sustainability in healthcare delivery across the nation.

MARKET DRIVERS

Escalating Healthcare Costs and Payer Pressure for Cost Containment

The rising burden of healthcare expenditures is escalating the growth of the United States biosimilar market. Biological drugs are among the most expensive treatments available often costing tens of thousands of dollars annually per patient. Private payers and pharmacy benefit managers are increasingly implementing formulary strategies that favor biosimilars over reference biologics to manage costs. The Medicare Program which covers millions of seniors faces budgetary constraints that necessitate the use of lower cost alternatives. The widespread adoption of biosimilars could save the federal government billions of dollars over the next decade. Hospital systems also face pressure to reduce supply chain costs under value-based care models. The American Hospital Association notes that drug costs represent a substantial portion of hospital expenses prompting administrators to seek efficient procurement options. The Inflation Reduction Act further incentivizes the use of cost effective therapies by allowing Medicare to negotiate prices for certain high expenditure drugs. This legislative environment encourages the transition from expensive originator biologics to biosimilars.

Increasing Prevalence of Chronic and Autoimmune Diseases

The growing incidence of chronic and autoimmune diseases is fuelling the growth of the United States biosimilar market. Conditions, such as rheumatoid, arthritis Crohn’s disease, and multiple sclerosis require long term management with biologic therapies. As per the Arthritis Foundation more than 58 million adults in the United States have been diagnosed with some form of arthritis many of whom require advanced biological treatments. The complexity of these diseases necessitates consistent access to medication to prevent progression and disability. The Centers for Disease Control and Prevention reports that autoimmune diseases affect approximately 24 million Americans highlighting the vast patient pool requiring therapeutic intervention. Cancer diagnoses also contribute to this demand with breast cancer and colorectal cancer being prevalent conditions treated with biologics. The American Cancer Society estimates that there are over 17 million cancer survivors in the United States many of whom require ongoing maintenance therapy. Biosimilars provide a reliable source of these essential medications ensuring that patients can adhere to treatment regimens without prohibitive costs. The expansion of indications for existing biologics further broadens the addressable patient population. Regulatory approvals for biosimilars in oncology and immunology have increased providing clinicians with more options for personalized care. As the population ages and lifestyle factors contribute to higher disease rates the need for accessible and affordable biologic treatments intensifies.

MARKET RESTRAINTS

Physician Hesitancy and Lack of Clinical Familiarity

The physician hesitancy and a lack of familiarity with biosimilar science is hampering the growth of the United States biosimilar market. Many healthcare providers remain cautious about switching patients from reference biologics to biosimilars due to concerns about efficacy and safety, despite regulatory assurances. As per a survey by the American Medical Association, a substantial number of physicians express uncertainty regarding the interchangeability of biosimilars and their reference products. The concept of extrapolation where a biosimilar is approved for all indications of the reference product without separate clinical trials for each condition can confuse clinicians. The educational gaps persist among prescribing physicians leading to slower adoption rates in clinical practice. Physicians may fear potential immunogenic reactions or reduced therapeutic effectiveness when transitioning patients. This reluctance is particularly pronounced in oncology where treatment outcomes are critical and deviations are perceived as risky. The lack of long term real world data compared to established reference products further exacerbates these concerns. Medical societies have issued guidelines supporting biosimilar use but implementation varies widely across institutions. Continuing medical education programs are attempting to bridge this knowledge gap but progress is gradual.

Patent Litigation and Regulatory Exclusivity Periods

The complex patent litigation and extended regulatory exclusivity periods for reference biologics is another factor restricting the growth of the United States biosimilar market. Originator manufacturers often employ aggressive legal strategies to delay biosimilar competition including filing numerous patents related to manufacturing processes and formulations. As per the Federal Trade Commission, these patent thickets can extend market exclusivity well beyond the initial patent expiration date preventing timely biosimilar launch. This statutory protection creates a substantial barrier to entry for biosimilar developers, who must wait years before filing for approval. According to the Generic Pharmaceutical Association lengthy legal battles can add several years to the development timeline increasing costs and uncertainty for manufacturers. Some reference product sponsors also engage in settlement agreements with biosimilar applicants to delay market entry in exchange for financial compensation. These practices limit consumer choice and maintain high prices for biological medicines. The unpredictability of litigation outcomes discourages investment in biosimilar development particularly for smaller companies with limited resources.

MARKET OPPORTUNITIES

Expansion into Oncology and Immunology Therapeutic Areas

The expansion of biosimilars into oncology and immunology therapeutic areas is creating new opportunities for the growth of the United States biosimilar market. These sectors represent the largest share of biologic spending offering significant potential for cost savings and increased patient access. As per the National Comprehensive Cancer Network, the adoption of biosimilars in cancer care can reduce treatment costs substantially allowing healthcare systems to treat more patients within fixed budgets. New biosimilar approvals for key oncology drugs such as trastuzumab and bevacizumab are opening avenues for broader utilization in breast lung and colorectal cancers. The American Society of Clinical Oncology supports the use of biosimilars to enhance the sustainability of cancer care delivery. In immunology biosimilars for tumor necrosis factor inhibitors are gaining traction for treating rheumatoid arthritis and inflammatory bowel disease. Pharmaceutical companies are investing heavily in developing biosimilars for high revenue generating reference products in these fields. The pipeline includes candidates for interleukin inhibitors and other targeted therapies used in autoimmune disorders. The potential for combination therapies involving biosimilars also offers new treatment paradigms.

Development of Interchangeable and Substitutable Biosimilars

The development of interchangeable and substitutable biosimilars by facilitating automatic substitution at the pharmacy level is additionally to promote new opportunities for the growth of the United States biosimilar market. Interchangeable biosimilars meet additional FDA standards that allow them to be substituted for the reference product without the intervention of the prescriber. As per the Food and Drug Administration achieving interchangeability status enhances the commercial viability of biosimilars by simplifying the switching process for pharmacists and payers. State laws regarding substitution vary but many are being updated to permit pharmacy level substitution for designated interchangeable biosimilars. This regulatory advancement reduces administrative burdens and accelerates market penetration. The ability to substitute biosimilars seamlessly encourages wider adoption in community pharmacies and outpatient settings. This trend is particularly beneficial for chronic disease management, where consistent medication supply isimportant. The expansion of interchangeable designations across various therapeutic classes increases the scope of opportunities for biosimilar manufacturers.

MARKET CHALLENGES

Navigating Complex Reimbursement and Pricing Structures

Navigating complex reimbursement and pricing structures is to pose as a major challenge for the growth of the United States biosimilar market. The fragmented healthcare system involves multiple payers each with distinct formularies rebate requirements and coverage policies. In some cases, the higher rebate margins offered by originator companies make reference products more financially attractive to pharmacy benefit managers than lower priced biosimilars. This perverse incentive structure undermines the economic advantage of biosimilars and slows adoption. According to the American Health Care Association, hospitals may face financial penalties under certain payment models if they switch to lower cost alternatives due to how reimbursement benchmarks are calculated. The lack of uniformity in coding and billing for biosimilars further complicates administrative processes for healthcare providers. Distinct Healthcare Common Procedure Coding System codes for each biosimilar require careful tracking and management. Manufacturers must engage in extensive negotiations with payers to secure favorable formulary placement.

Supply Chain Vulnerabilities and Manufacturing Complexity

The supply chain vulnerabilities and the inherent complexity of manufacturing biological products is additionally to decline the growth of the United States biosimilar market. Unlike small molecule generics, biosimilars are produced in living cells requiring precise control over environmental conditions and raw materials. As per the International Society for Pharmacoeconomics and Outcomes Research, any deviation in the manufacturing process can affect the quality and consistency of the final product. This sensitivity necessitates robust quality control measures and specialized facilities which are capital intensive to build and maintain. The reliance on single source suppliers for critical raw materials such as cell culture media and chromatography resins increases the risk of supply disruptions. The complexity of scaling up production to meet commercial demand while maintaining regulatory compliance is a significant hurdle. Global supply chain disruptions, such as those experienced during the pandemic have highlighted the fragility of these networks. As per the Department of Health and Human Services ensuring a resilient supply chain for critical medicines is a national priority but remains difficult to achieve. Biosimilar manufacturers must invest heavily in redundancy and risk mitigation strategies to ensure consistent product availability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Drug Class, Disease Indication, Distribution Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Drug Class Insights

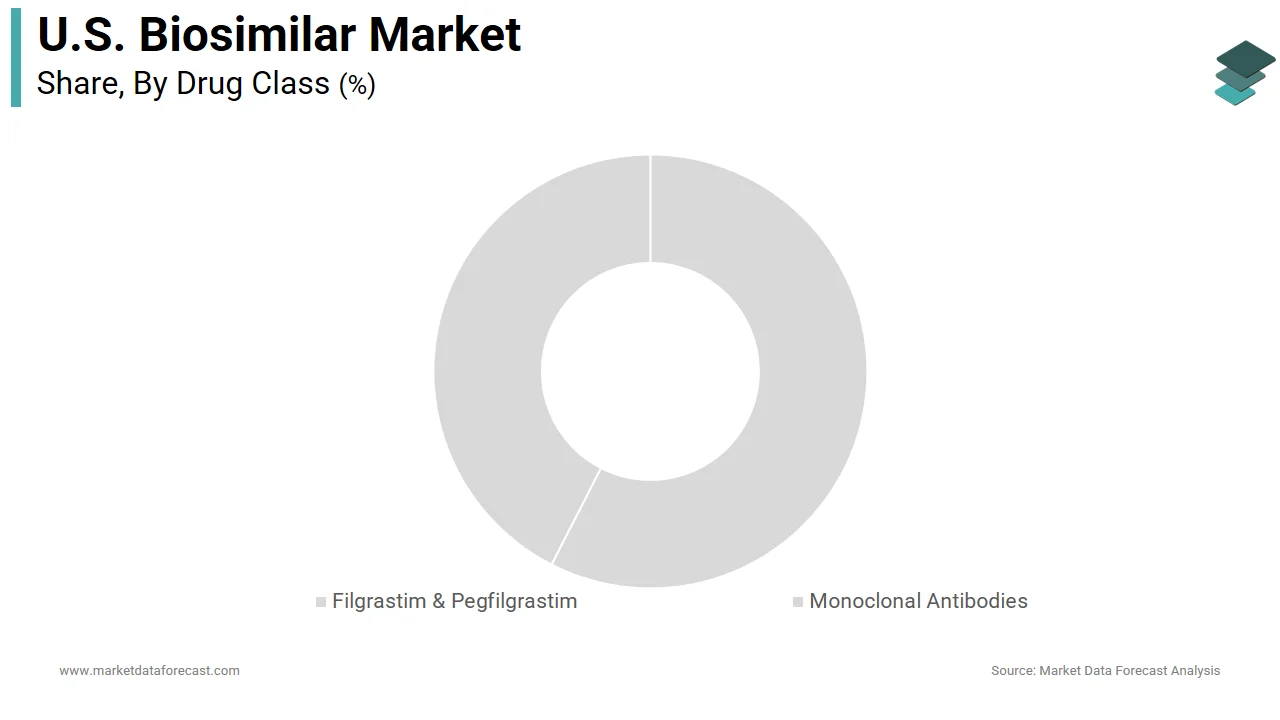

The monoclonal antibodies segment was accounted in holding 44.3% of the United States biosimilar market share in 2025 due to their widespread application in treating high prevalence chronic conditions, such as cancer and autoimmune disorders. These biologics target specific proteins involved in disease progression offering precise therapeutic effects that have become standard of care. As per the American Cancer Society, approximately 1.9 million new cancer cases were diagnosed in 2023 many of which require monoclonal antibody treatments like trastuzumab or rituximab. The sheer volume of patients needing these therapies creates a massive demand for cost effective alternatives. Additionally, the Centers for Disease Control and Prevention reports that over 58 million adults suffer from arthritis a condition frequently managed with tumor necrosis factor inhibitors which are monoclonal antibodies. The clinical efficacy of these drugs has established them as first line treatments ensuring consistent prescription volumes. Healthcare providers rely on these agents for long term disease management making them a staple in hospital and outpatient settings. The extensive patent expirations of blockbuster monoclonal antibodies have opened the door for numerous biosimilar entries further cementing this class's dominance.

The filgrastim and pegfilgrastim segment is esteemed to grow at a fastest CAGR of 12.5% from 2026 to 2034 with their role in supporting chemotherapy regimens by preventing neutropenia a common and serious side effect of cancer treatment. As per the National Comprehensive Cancer Network, guidelines the use of colony stimulating factors is recommended for patients receiving myelosuppressive chemotherapy to reduce the risk of infection and hospitalization. The increasing incidence of cancer diagnoses necessitates higher volumes of these supportive care medications. The American Cancer Society estimates that millions of cancer patients undergo chemotherapy annually creating a steady and growing demand for filgrastim and pegfilgrastim. Biosimilars in this category have achieved high levels of physician acceptance due to their established safety profile and ease of administration. The availability of multiple biosimilar options has fostered competition leading to significant price reductions that encourage broader usage. The simplicity of switching between reference products and biosimilars in this class due to clear clinical equivalence data further accelerates growth. Hospitals and oncology practices are increasingly standardizing the use of these biosimilars to manage costs while maintaining high standards of patient care.

By Disease Indication Insights

The cancer segment was accounted in holding a significant share of the United States biosimilar market in 2025 due to the high burden of the disease and the heavy dependence on biologic therapies for treatment. Malignancies, such as breast, colorectal, and lung cancer, require complex treatment protocols that often include monoclonal antibodies and other biologics. As per the American Cancer Society, nearly 2 million new cancer cases are expected to be diagnosed in the United States in 2024, the vast patient population requiring intervention. Many of these patients receive biologics as part of their standard care regimen creating a substantial base for biosimilar adoption. The high cost of reference biologics used in oncology places a significant financial strain on healthcare systems prompting a shift toward more affordable biosimilar alternatives. According to the National Comprehensive Cancer Network the integration of biosimilars into cancer care pathways is essential for sustaining the financial viability of oncology practices. Hospitals and clinics are actively replacing reference products with biosimilars to reduce procurement costs while maintaining therapeutic efficacy. The clinical equivalence of biosimilars in oncology has been well documented encouraging physician confidence in their use.

The autoimmune diseases segment is likely to register a fastest CAGR of 14.2% from 2026 to 2034 owing to the rising prevalence of conditions such as rheumatoid arthritis psoriasis and inflammatory bowel disease which require long term biological management. More than 58 million adults in the United States have been diagnosed with arthritis many of whom suffer from autoimmune forms that necessitate advanced therapy, as per the study. The chronic nature of these diseases means that patients remain on treatment for years creating a sustained demand for medications. Biosimilars for tumor necrosis factor inhibitors and interleukin inhibitors are becoming increasingly popular due to their ability to provide similar clinical benefits at lower costs. The introduction of biosimilars has helped bridge this gap by making effective treatments more affordable and accessible. Insurance providers are encouraging the use of biosimilars for autoimmune conditions through tiered formularies that lower out of pocket costs for patients.

By Distribution Channel Insights

The hospital pharmacies segment was accounted in holding a significant share of the United States biosimilar market in 2025 with the predominant administration of intravenous biosimilars in clinical settings. Many biosimilars, particularly those used in oncology and severe autoimmune conditions require infusion or injection under medical supervision. As per the American Hospital Association, hospitals serve as the primary site of care for complex treatments ensuring that patients receive medications safely and effectively. The infrastructure of hospital pharmacies allows for the proper storage handling and preparation of biological products which often require strict temperature control. This logistical capability makes hospitals the preferred channel for distributing high value biosimilars. Additionally, hospital formularies are managed by pharmacy and therapeutics committees that evaluate and approve biosimilars based on clinical and economic criteria. According to the Vizient Inc hospital purchasing consortium the adoption of biosimilars in hospital settings has accelerated due to group purchasing organizations negotiating favorable contracts. These agreements facilitate rapid integration of biosimilars into hospital supply chains. The concentration of specialized healthcare providers in hospitals also supports the prescribing and monitoring of biosimilar therapies.

The online pharmacies segment is esteemed to grow at an anticipated CAGR of 16.8% from 2026 to 2034 with the increasing availability of biosimilars that can be self-administered at home, such as subcutaneous injections for autoimmune diseases. Patients prefer the convenience and privacy of receiving medications through mail order services, which eliminate the need for frequent hospital visits. As per the National Association of Boards of Pharmacy, accredited online pharmacies have expanded their offerings to include specialized biologics ensuring safe and compliant delivery. The rise of telehealth has facilitated remote consultations and prescriptions enabling seamless access to biosimilars through digital platforms. The integration of telehealth with online pharmacy services has improved medication adherence and patient satisfaction. Online pharmacies often offer competitive pricing and discount programs that make biosimilars more affordable for uninsured or underinsured patients. The ability to compare prices and read reviews empowers consumers to make informed decisions about their healthcare purchases. The expansion of cold chain logistics ensures that temperature sensitive biosimilars are delivered safely to patients homes.

COMPETITIVE LANDSCAPE

The competition in the United States biosimilar market is intense and characterized by the entry of both established pharmaceutical giants and specialized biosimilar developers. Major players compete on the basis of product portfolio diversity manufacturing capability and pricing strategies. The market sees frequent launches of interchangeable biosimilars which provide a competitive advantage through automatic substitution privileges. Companies differentiate themselves by offering robust clinical data and real world evidence to reassure physicians about safety and efficacy. Patent litigation remains a significant factor with originator companies often employing legal tactics to delay biosimilar entry. However regulatory reforms and judicial decisions are increasingly favoring competition. Payers play a crucial role by shaping formularies and incentivizing the use of lower cost biosimilars through tiered copayment structures. Collaboration with patient advocacy groups helps build awareness and acceptance among consumers.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. biosimilar market include

- Pfizer Inc.

- Amgen Inc.

- Samsung Bioepis

- Sandoz Group AG

- Pfizer Inc

- Novartis AG

- Celltrion Inc.

- Viatris Inc.

- Coherus BioSciences

TOP PLAYERS IN THE MARKET

- Amgen Inc is a pioneering biotechnology company that has established a strong presence in the United States biosimilar market through its strategic portfolio of high quality biological medicines. The company leverages its extensive manufacturing expertise and global supply chain to deliver reliable biosimilar products for oncology and inflammation. Recent actions include the launch of multiple interchangeable biosimilars which facilitate easier substitution by pharmacists and increase market accessibility. Amgen actively engages in educational initiatives to build physician confidence in biosimilar science and safety profiles. The company invests heavily in research and development to expand its pipeline with next generation biosimilars targeting complex diseases.

- Sandoz Group AG is a global leader in generic and biosimilar medicines playing a pivotal role in the United States market by providing affordable alternatives to reference biologics. The company focuses on developing a diverse portfolio of biosimilars for chronic conditions such as autoimmune disorders and cancer. Recent strategies involve significant investments in advanced manufacturing facilities to ensure consistent product quality and supply reliability. Sandoz actively collaborates with healthcare providers to streamline the adoption of biosimilars through evidence based clinical data and support programs. The company pursues strategic partnerships and licensing agreements to expand its product offerings and reach new therapeutic areas.

- Pfizer Inc is a prominent pharmaceutical corporation that contributes significantly to the United States biosimilar market through its robust portfolio of innovative biological treatments. The company utilizes its vast resources and scientific capabilities to develop biosimilars that meet rigorous standards for safety and efficacy. Recent actions include the expansion of its biosimilar pipeline with approvals for key molecules in oncology and immunology. Pfizer engages in proactive market access strategies to secure formulary placement and promote the value of its biosimilars to payers and providers. The company invests in digital health tools to support patient adherence and monitoring during treatment. These efforts demonstrate its commitment to improving healthcare affordability and accessibility while maintaining a strong competitive edge in the dynamic biosimilar industry.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States biosimilar market primarily focus on securing interchangeability designation from regulatory authorities to enable automatic substitution at the pharmacy level. Companies invest heavily in clinical trials to demonstrate equivalence and build trust among healthcare providers and patients. Strategic partnerships with group purchasing organizations help secure favorable formulary placement and drive volume adoption. Manufacturers prioritize expanding their pipelines with biosimilars for high value blockbuster drugs in oncology and immunology. Educational initiatives are implemented to address physician hesitancy and clarify the scientific basis for biosimilar approval. Investment in advanced manufacturing technologies ensures consistent quality and supply chain reliability. Pricing strategies often involve aggressive discounts compared to reference products to attract cost conscious payers. Legal teams actively navigate patent landscapes to mitigate litigation risks and accelerate market entry. These comprehensive approaches enhance market penetration and sustainable growth in the competitive biosimilar landscape.

MARKET SEGMENTATION

This research report on the U.S. biosimilar market has been segmented and sub-segmented into the following categories.

By Drug Class

- Filgrastim & Pegfilgrastim

- Monoclonal Antibodies

- Others

By Disease Indication

- Cancer

- Autoimmune Diseases

- Arthritis

- Psoriasis

- Neutropenia

- Others

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. biosimilar market?

The U.S. biosimilar market develops highly similar biologic medicines to approved reference products, offering cost-effective treatment alternatives.

How does the U.S. biosimilar market function?

The U.S. biosimilar market follows FDA 351(k) pathway requiring analytical, nonclinical, and clinical studies proving similarity to reference biologics.

What drives growth in the U.S. biosimilar market?

The U.S. biosimilar market grows from patent expirations on blockbusters, cost pressures, and expanding FDA approvals for complex molecules.

Which therapeutic areas lead the U.S. biosimilar market?

Oncology and immunology dominate the U.S. biosimilar market with monoclonal antibodies for cancer and autoimmune disease treatments.

What is FDA interchangeability in the U.S. biosimilars market?

FDA interchangeability allows pharmacy-level substitution in the U.S. biosimilar market after additional switching studies prove no clinical differences.

How does regulation shape the U.S. biosimilar market?

FDA's BPCIA provides 12-year reference exclusivity plus litigation periods before U.S. biosimilar market entry is possible.

What role do oncology biosimilars play in the U.S. biosimilar market?

Oncology biosimilars lead the U.S. biosimilar market uptake due to high treatment costs and supportive oncology provider adoption.

Why is manufacturing critical in the U.S. biosimilar market?

Manufacturing similarity through analytical studies forms the foundation of the U.S. biosimilar market approval process.

What challenges face the U.S. biosimilar market?

Patent thickets, naming confusion, and provider hesitancy slow adoption in the U.S. biosimilar market despite regulatory progress.

How do payers influence the U.S. biosimilar market?

Payers drive uptake in the U.S. biosimilar market through preferred formulary placement and reimbursement incentives.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com