U.S Carbonated Soft Drinks Market Size, Share, Trends & Growth Forecast Report Segmented By Product Type (Soft Drinks, Carbonated Water, Sports and Energy Drinks, Soda, Others), Flavor, Distribution Channel, And Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 To 2034

U.S Carbonated Soft Drinks Market Size

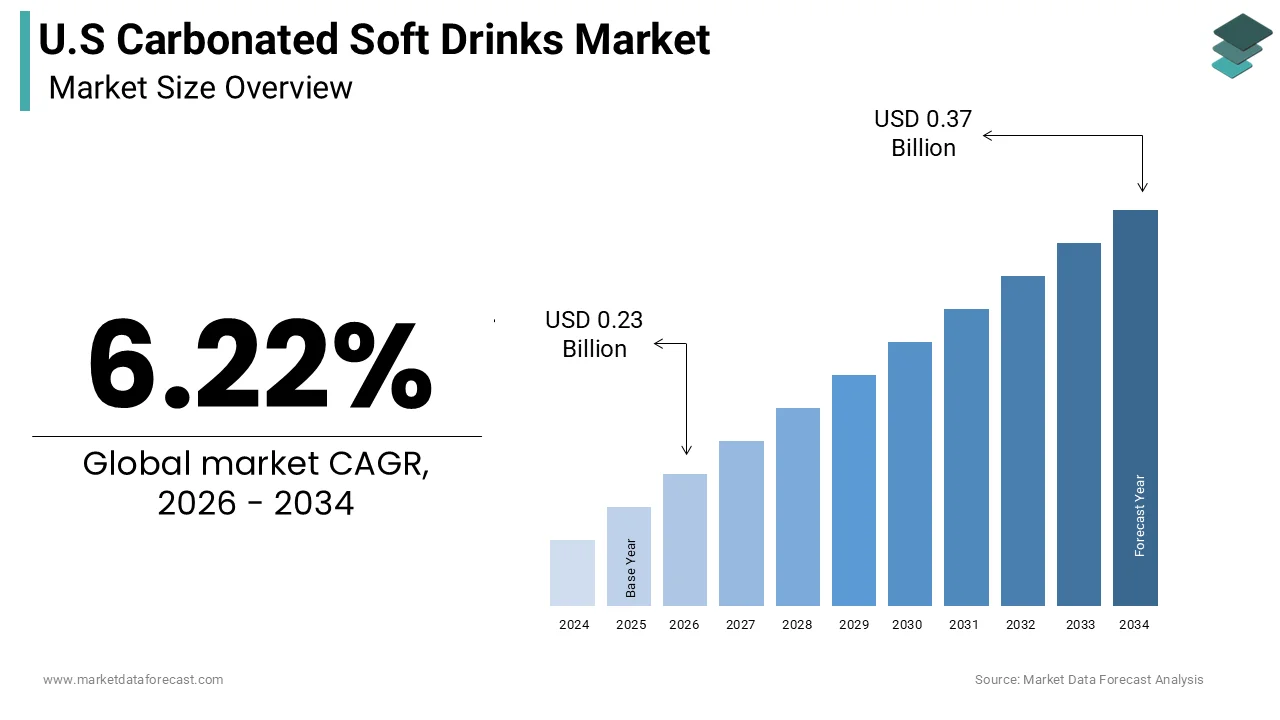

The U.S carbonated soft drinks market size was calculated to be USD 0.22 billion in 2025 and is anticipated to be worth USD 0.37 billion by 2034, from USD 0.23 billion in 2026, growing at a CAGR of 6.22% during the forecast period.

The carbonated soft drinks are beverages characterized by the infusion of carbon dioxide under pressure, ranging from traditional colas and lemon limes to sparkling waters and functional sodas. As per the Centers for Disease Control and Prevention, approximately 42.4% of US adults are obese, a statistic that has significantly influenced dietary choices and reduced the consumption of full-sugar beverages. Concurrently, the plastic waste from single-use bottles remains an environmental concern, prompting industry shifts toward sustainable packaging solutions. Consumers are increasingly scrutinizing labels for artificial additives, driving manufacturers to reformulate products with natural sweeteners such as stevia and monk fruit. The integration of functional ingredients like probiotics and adaptogens further blurs the line between soft drinks and health supplements.

MARKET DRIVERS

Innovation in Zero-Calorie and Natural Sweetener Formulations

The development of advanced zero-calorie and natural sweetener formulations, addressing the growing consumer demand for guilt-free indulgence, is fuelling the growth of the United States carbonated soft drinks market. Modern shoppers are actively seeking beverages that provide the sensory experience of soda without the associated health risks of excessive sugar intake. As per the International Food Information Council, 73% of Americans reported in 2024 that they are trying to limit or avoid sugars in their diet, creating a robust demand for alternative sweetening options. Manufacturers have responded by investing heavily in research and development to improve the taste profile of non-nutritive sweeteners, such as stevia, monk fruit, and allulose. These natural alternatives offer a cleaner label appeal compared to artificial sweeteners like aspartame, which many consumers perceive negatively. The introduction of these ingredients allows brands to maintain the sweetness and mouthfeel expected from carbonated beverages, while significantly reducing caloric content. This innovation has led to a surge in the popularity of zero-sugar variants of classic cola and fruit-flavored sodas. Retailers are expanding shelf space for these products, recognizing their appeal to health-conscious demographics, including diabetics and weight watchers. The ability to offer a familiar taste experience with improved nutritional metrics encourages trial and repeat purchases. Furthermore, the marketing of these products emphasizes freedom from compromise by allowing consumers to enjoy their favorite flavors without dietary regret.

Premiumization and Craft Soda Renaissance

The trend toward premiumization and the renaissance of craft sodas by appealing to consumers seeking unique and high-quality beverage experiences is also promoting the growth of the United States carbonated soft drinks market. There is a growing segment of shoppers who view soda not just as a thirst quencher but as a culinary accessory or a treat, willing to pay higher prices for artisanal and small-batch productions. Craft sodas often feature exotic flavor combinations, organic ingredients, and lower sugar content, differentiating themselves from mass market offerings. Brands are leveraging local sourcing and transparent supply chains to build trust and authenticity with consumers. The use of real fruit juices, herbal extracts, and spices creates complex flavor profiles that appeal to adventurous palates. This movement is particularly strong among millennials and Generation Z consumers, who prioritize authenticity and ethical production practices. Independent breweries and soda makers are gaining traction in urban markets, often distributing through specialty grocery stores and direct to consumers. The aesthetic appeal of premium packaging also contributes to brand loyalty, as consumers associate high-quality design with superior product quality.

MARKET RESTRAINTS

Health Concerns Related to Artificial Ingredients and Obesity

The persistent health concerns regarding artificial ingredients and the link between sugary beverages and obesity are limiting the growth of the United States carbonated soft drinks market. Despite the rise of zero-calorie options, a significant portion of the market still relies on high fructose corn syrup and artificial colors, which are increasingly viewed as detrimental to public health. The excessive consumption of free sugars is a leading contributor to tooth decay, unhealthy weight gain, and risk factors for non-communicable diseases. This scientific consensus has led to heightened scrutiny from health advocates and medical professionals by influencing consumer behavior and purchasing decisions. Many parents are actively restricting their children's access to traditional sodas by opting for water, milk, or 100% juice instead. The negative perception of artificial preservatives and colorings further dampens demand, as consumers seek clean-label products with recognizable ingredients. Regulatory bodies are also considering stricter labeling requirements and potential taxes on sugary drinks, which could increase costs and reduce consumption. The stigma associated with soda consumption as an unhealthy habit poses a long-term challenge for legacy brands that struggle to shed their image as contributors to the obesity epidemic. Even with reformulation efforts, the historical association with poor health outcomes remains a barrier to growth. Consumers are becoming more educated about the potential metabolic effects of certain sweeteners, leading to hesitation in adopting even some zero-calorie alternatives.

Environmental Impact of Single-Use Plastic Packaging

The environmental impact of single-use plastic packaging, as consumers and regulators increasingly demand sustainable solutions, is additionally declining the growth of the United States carbonated soft drinks market. The beverage industry is a major contributor to plastic pollution, with billions of bottles ending up in landfills or oceans annually. As per the Environmental Protection Agency, only 29% of plastic bottles were recycled in the United States in 2023, highlighting the inefficiency of current waste management systems. This low recycling rate has sparked public outcry and legislative action, with several states implementing extended producer responsibility laws and bans on certain single-use plastics. Consumers are actively seeking brands that demonstrate commitment to environmental stewardship, often boycotting companies perceived as negligent. The cost of transitioning to recycled materials or alternative packaging, such as aluminum cans and glass bottles, is substantially impacting profit margins. Aluminum production, while more recyclable, has a higher initial carbon footprint, creating a complex sustainability dilemma. The logistical challenges of collecting and processing recycled materials, which further complicate the supply chain. Brands face pressure to reduce plastic usage without compromising product safety or shelf life. Failure to address these environmental concerns can lead to reputational damage and loss of market share to eco-friendly competitors. The regulatory landscape is evolving rapidly, requiring companies to invest heavily in sustainable packaging innovations.

MARKET OPPORTUNITIES

Expansion into Functional and Wellness-Oriented Beverages

The integration of functional ingredients into carbonated soft drinks, as consumers increasingly seek beverages that provide health benefits beyond hydration, is certainly to expand the growth of the United States carbonated soft drink market. This trend aligns with the broader wellness movement, where individuals look for products that support digestion, immunity, and mental clarity. Manufacturers can capitalize on this by incorporating probiotics, prebiotics, vitamins, and adaptogens into sparkling beverages. Probiotic sodas, for example, appeal to consumers interested in gut health by offering a tasty alternative to traditional supplements. Adaptogenic ingredients such as ashwagandha and CBD are gaining popularity for their stress-relieving properties, attracting a demographic focused on mental well-being. These functional sodas often feature lower sugar content and natural flavors, positioning them as healthier choices. The opportunity extends to specific health claims, such as immune support or energy enhancement, which can command premium pricing. Retailers are eager to stock these innovative products, recognizing their appeal to health-conscious shoppers. Collaborations with health experts and influencers can further validate these claims and build consumer trust. By transforming soda from a mere treat into a functional tool for wellness, companies can tap into new revenue streams and differentiate their brands in a crowded market.

Growth in Direct-to-Consumer and Subscription Models

The expansion of direct-to-consumer channels and subscription models to bypass traditional retail constraints and build deeper customer relationships is expected to pose new opportunities for the growth of the United States carbonated soft drinks market. Digital platforms enable companies to reach consumers directly by offering personalized experiences and convenient delivery services. The direct-to-consumer e-commerce sales in the food and beverage sector grew by 20% in 2024, due to the shifting preferences of modern shoppers. Subscription services allow customers to receive regular shipments of their favorite sodas by ensuring consistent revenue streams and reducing churn. This model is particularly effective for craft and premium brands that may struggle for shelf space in mainstream supermarkets. Direct interaction with consumers provides valuable data on preferences and buying habits, enabling targeted marketing and product development. Brands can offer exclusive flavors or limited-edition packs to subscribers by enhancing engagement and loyalty. The ability to control the entire customer journey from discovery to delivery allows for better brand storytelling and community building. Social media integration facilitates viral marketing and user-generated content, amplifying brand reach. Additionally, direct-to-consumer models reduce reliance on retail intermediaries, improving profit margins. Companies can experiment with new products and gather immediate feedback, accelerating innovation cycles. This approach empowers brands to create a dedicated fan base that values convenience and exclusivity.

MARKET CHALLENGES

Volatility in Raw Materials and Supply Chain Costs

The volatility in raw materials and supply chain costs affecting profitability and pricing strategies is one of the major challenges for the growth of the United States carbonated soft drinks market. Key ingredients, such as sugar, aluminum, and petroleum-based plastics, are subject to fluctuating global prices driven by geopolitical tensions, climate change, and economic instability. The price of sugar has experienced significant variability in recent years, impacting production costs for beverage manufacturers. Aluminum prices are also sensitive to energy costs and trade policies, adding uncertainty to packaging expenses. These fluctuations force companies to either absorb the increased costs, reducing margins, or pass them on to consumers through price hikes, which may dampen demand. Supply chain disruptions, such as port congestion and labor shortages, further exacerbate these issues, leading to delays and inventory shortages. The complexity of global supply networks means that a disruption in one region can have cascading effects on production schedules. Companies must invest in risk management strategies and diverse sourcing options to mitigate these risks, which can be costly and operationally challenging. Smaller brands with less bargaining power are particularly vulnerable to these pressures by potentially lead to market consolidation. The need for constant adjustment to changing cost structures requires agile financial planning and operational flexibility.

Regulatory Pressure and Sugar Taxes

The increasing regulatory pressure and the implementation of sugar taxes by influencing both formulation and consumer behavior are also expected to impede the growth of the United States carbonated soft drinks market. Several cities and states have introduced taxes on sugary beverages to combat obesity and related health issues, effectively increasing the retail price of these products. As per the Rudd Center for Food Policy and Health, jurisdictions with soda taxes have seen a decline in sales of taxed beverages, indicating the effectiveness of these measures in reducing consumption. These taxes not only impact sales volume but also require companies to navigate a complex patchwork of local regulations, increasing compliance costs. The threat of broader federal legislation looms, creating uncertainty for long-term planning. Manufacturers must constantly reformulate products to reduce sugar content and avoid taxation, which can alter taste profiles and risk alienating loyal customers. The labeling requirements are also becoming stricter, with mandates for clear warning labels on high-sugar drinks. This regulatory environment creates a hostile atmosphere for traditional soda brands, forcing them to accelerate their transition to healthier alternatives. The political momentum behind public health initiatives suggests that regulatory pressures will intensify, requiring companies to proactively adapt their portfolios. Failure to comply with these regulations can result in fines and reputational damage. The challenge lies in balancing regulatory compliance with consumer satisfaction by ensuring that reformulated products remain appealing while meeting legal standards. This ongoing regulatory scrutiny restricts market freedom and drives up operational costs.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.22% |

| Segments Covered | By Product Type, Flavor, Distribution Channel, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | The Coca-Cola Company, PepsiCo, Keurig Dr Pepper, National Beverage Corp., Monster Beverage Corporation, Jones Soda Co., Refresco, Cott Corporation |

SEGMENTAL ANALYSIS

By Product Type Insights

The carbonated water segment was the largest by holding a significant share of the United States carbonated soft drinks market in 2025, owing to the profound consumer shift toward healthier hydration options that avoid added sugars and calories. Modern consumers are increasingly aware of the health risks associated with high sugar intake, prompting them to seek alternatives that provide the sensory experience of carbonation without the negative nutritional impact. The perception of carbonated water as a premium and sophisticated choice that aligns with wellness lifestyles. Brands are enhancing appeal through natural fruit essences and mineral enrichment, creating a diverse product landscape that caters to varied taste preferences. The absence of artificial sweeteners in many premium sparkling waters further attracts clean label advocates who scrutinize ingredient lists for transparency. Retailers have responded by expanding shelf space for sparkling water varieties, recognizing their high turnover rates and broad demographic appeal. The versatility of carbonated water also allows it to serve as a mixer for alcoholic and non-alcoholic beverages, increasing its usage occasions beyond simple hydration. This segment benefits from strong marketing campaigns that position sparkling water as a lifestyle essential rather than just a beverage. The continuous innovation in packaging, such as sleek cans and eco-friendly bottles, reinforces its premium image.

The sports and energy drinks segment is expected to grow at the fastest CAGR of 7.8% from 2026 to 2034, with the rising demand for functional performance beverages among active consumers. The boundary between sports nutrition and mainstream hydration is blurring, as individuals seek drinks that offer tangible benefits, such as enhanced endurance, faster recovery, and mental focus. As per the Council for Responsible Nutrition, the usage of sports nutrition supplements in the United States increased by 15% in 2024, reflecting a broader interest in performance optimization. Carbonated sports drinks are gaining traction due to their ability to provide rapid hydration and electrolyte replenishment with a refreshing mouthfeel. The integration of caffeine and B vitamins in energy drinks appeals to students, professionals, and athletes looking for sustained energy levels throughout the day. Manufacturers are innovating with natural caffeine sources such as green tea extract and guarana to appeal to health-conscious consumers who wish to avoid synthetic additives. The expansion of product lines to include zero-sugar and low-calorie options has broadened the appeal of these beverages to weight-conscious individuals. Marketing campaigns often feature professional athletes and fitness influencers, reinforcing the association between these drinks and peak physical performance. The convenience of ready-to-drink formats makes them ideal for on-the-go consumption before or after workouts. This functional positioning differentiates sports and energy drinks from traditional sodas, driving rapid adoption and loyalty among performance-oriented demographics.

By Flavor Insights

The cola flavor segment was the largest by holding 22.1% of the United States carbonated soft drinks market share in 2025 due to its iconic brand heritage and deep cultural entrenchment in American society. For decades, cola has been synonymous with refreshment and social connection, supported by massive advertising budgets and widespread availability. Major brands have built strong emotional connections with consumers through nostalgic marketing campaigns and sponsorships of major sporting events. The distinct taste profile of cola, characterized by a blend of vanilla, cinnamon, and citrus oils, has become a familiar comfort for many Americans. This familiarity reduces the risk of trial and encourages repeat purchases across generations. The versatility of cola as a standalone beverage or a mixer for alcoholic drinks further enhances its utility and consumption frequency. Retailers prioritize cola products due to their high turnover rates and consistent demand, ensuring prominent shelf placement. The strong distribution networks of leading cola manufacturers guarantee availability in virtually every retail outlet, from vending machines to supermarkets.

The fruit-flavored segment is projected to witness the fastest CAGR of 6.5% from 2026 to 2034, with the demand for natural and exotic fruit inspirations that offer vibrant and refreshing taste experiences. Consumers are increasingly seeking beverages that mimic the taste of real fruit juices while providing the effervescence of soda. As per the International Flavor and Fragrance Association, fruit flavors such as mango, passion fruit, and berry are among the top trending profiles in the beverage industry. These flavors appeal to consumers looking for a healthier and more authentic alternative to artificial-tasting sodas. Manufacturers are using real fruit purees and concentrates to enhance the authenticity of these drinks, aligning with clean label trends. The visual appeal of fruit-flavored drinks, often characterized by bright and natural colors, also attracts attention on shelves. Social media platforms play a significant role in popularizing these flavors, with influencers showcasing colorful and Instagram-worthy beverages. The variety of fruit options allows for continuous innovation and seasonal limited editions, keeping the category dynamic and exciting. Retailers are expanding their assortments of fruit-flavored sodas to cater to this growing demand, particularly among younger demographics. The perception of fruit flavors as lighter and more refreshing than cola or lemon lime also contributes to their popularity, especially during warmer months.

By Distribution Channel Insights

The supermarkets and hypermarkets segment accounted in holding 34.6% of the United States carbonated soft drinks market share in 2025 due to the convenience of one-stop shopping and the ability to purchase in bulk. Consumers prefer these large-format stores for their weekly grocery needs, allowing them to stock up on beverages alongside other household items. The wide aisle space and dedicated beverage sections allow for extensive product displays and promotions, influencing purchasing decisions. Bulk packaging options, such as multi-packs and cases, offer cost savings that appeal to families and heavy users. The ability to compare prices and brands side by side empowers consumers to make informed choices based on value and preference. Supermarkets also frequently offer loyalty discounts and digital coupons for carbonated soft drinks, incentivizing repeat purchases. The consistent availability of both mainstream and niche brands ensures that diverse consumer needs are met. The physical presence of these stores in suburban and urban areas provides easy access for a large portion of the population. The trusted environment of established supermarket chains also reassures consumers regarding product quality and freshness.

The e-commerce segment is deemed to grow at the fastest CAGR of 14.2% from 2026 to 2034 with the expansion of online grocery platforms and subscription services. The convenience of home delivery appeals to busy consumers who wish to avoid physical store visits and heavy lifting. Subscription models allow customers to automate the replenishment of staple beverages by ensuring they never run out. This model provides predictability for both consumers and manufacturers by enhancing supply chain efficiency. Online platforms offer a wider selection of niche and specialty products that may not be available in local stores, which is catering to specific taste preferences. The ability to read reviews and compare products online empowers consumers to make informed choices. Major retailers have invested heavily in last-mile delivery capabilities, reducing shipping times and costs. The integration of voice-activated ordering through smart home devices further simplifies the purchasing process. This seamless and convenient shopping experience drives repeat business and customer loyalty.

COMPETITION OVERVIEW

The competition in the United States carbonated soft drinks market is intense and characterized by the dominance of a few major players alongside a growing number of niche and craft brands. Established giants leverage their extensive distribution networks and strong brand equity to maintain market leadership while facing pressure from health-conscious consumers shifting toward healthier alternatives. Price competition remains significant, particularly in the conventional soda segment, where private label products offer cost-effective options. However, differentiation through innovation in flavors, functional benefits, and sustainable packaging drives brand loyalty and premiumization. Manufacturers continuously invest in research and development to create products that align with emerging dietary trends such as keto-friendly or plant-based formulations. Marketing strategies focus on digital engagement and personalized experiences to connect with younger demographics who value authenticity and transparency. The rise of e-commerce has lowered barriers to entry, allowing small brands to reach national audiences without traditional retail presence.

KEY MARKET PLAYERS

A few major players of the U.S carbonated soft drinks market include

- The Coca-Cola Company

- PepsiCo

- Keurig Dr Pepper

- National Beverage Corp

- Monster Beverage Corporation

- Jones Soda Co

- Refresco

- Cott Corporation

Top Strategies Used by Key Market Participants

Key players in the United States carbonated soft drinks market primarily employ product diversification and health-focused reformulation to maintain a competitive advantage. Companies frequently introduce zero-sugar and low-calorie variants to address growing health consciousness among consumers. This strategy helps retain customers who are reducing sugar intake without abandoning their favorite brands. Expansion into functional beverages with added vitamins or probiotics is another prevalent approach, as firms capitalize on wellness trends. Strategic acquisitions of niche and craft brands allow established companies to broaden their portfolios and access new market segments quickly. Sustainability initiatives, such as using recycled packaging and reducing carbon footprints, are critical for enhancing brand reputation and meeting regulatory expectations. Digital transformation and e-commerce enhancement enable manufacturers to engage directly with consumers and gather valuable data for personalized marketing. These combined strategies allow market participants to adapt to changing preferences and sustain growth in a mature industry.

Leading Players in the US Carbonated Soft Drinks Market

- The Coca-Cola Company remains a dominant force in the United States carbonated soft drinks market through its extensive portfolio of iconic brands and global distribution network. The company actively diversifies its offerings by expanding into zero-sugar variants and functional sparkling beverages to meet evolving health trends. Recent actions include significant investments in sustainable packaging initiatives, such as increasing the use of recycled materials in bottles. The company also leverages advanced data analytics to optimize supply chain efficiency and enhance consumer engagement through digital marketing campaigns.

- PepsiCo Inc plays a critical role in the United States carbonated soft drinks market with its diverse range of beverages, including Pepsi, Mountain Dew, and Sierra Mist. The company emphasizes product innovation by introducing new flavors and limited edition releases to capture consumer interest. Recent strategies involve enhancing its direct-to-consumer capabilities and expanding its presence in the e-commerce sector. PepsiCo also prioritizes sustainability by committing to reducing plastic waste and improving water stewardship across its operations. The company collaborates with retailers to optimize shelf space and promote healthier options within its portfolio. These efforts ensure that PepsiCo remains responsive to consumer preferences while maintaining strong brand visibility and market relevance in the competitive soft drink industry.

- Keurig Dr Pepper Inc contributes significantly to the United States carbonated soft drinks market through its robust portfolio featuring Dr Pepper Seven Up, and Canada Dry. The company focuses on expanding its footprint in the premium and craft soda segments to appeal to discerning consumers. Recent actions include strategic acquisitions of emerging beverage brands to diversify its product offerings and reach new demographics. Keurig Dr Pepper also invests in marketing campaigns that highlight the unique heritage and flavor profiles of its legacy brands. The company enhances operational efficiency by integrating its distribution networks and leveraging technology to improve customer service. These initiatives help Keurig Dr Pepper maintain a strong competitive position and drive growth in the dynamic carbonated soft drinks market.

MARKET SEGMENTATION

This research report on the US carbonated soft drinks market has been segmented and sub-segmented based on product type, flavor, distribution channel & region.

By Product Type

- Soft Drinks

- Carbonated Water

- Sports and Energy Drinks

- Soda

- Others

By Flavor

- Cola

- Lemon-Lime Flavored

- Fruit Flavored

- Others

By Distribution Channel

- Supermarket and Hypermarket

- Convenience Store

- E-Commerce

- Food Service

- Others

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What is driving the growth of the U.S. carbonated soft drinks market?

The market is driven by increasing demand for flavored beverages, product innovations, strong brand presence, and growing availability through retail and online channels.

2. What are the most popular carbonated soft drink flavors in the U.S.?

Cola, lemon-lime, orange, root beer, and fruit-based flavors are among the most popular choices.

3. How is consumer preference changing in the carbonated soft drinks industry?

Consumers are increasingly preferring low-calorie, sugar-free, natural ingredient, and functional beverages.

4. What role do low-sugar and zero-sugar beverages play in the market?

Low-sugar and zero-sugar drinks are becoming key growth segments due to rising health awareness and concerns about obesity and diabetes.

5. Which distribution channels dominate the U.S. carbonated soft drinks market?

Supermarkets, convenience stores, hypermarkets, vending machines, and online retail platforms are major distribution channels.

6. How does health awareness impact carbonated soft drink sales?

Growing health awareness has reduced demand for high-sugar drinks while increasing interest in healthier alternatives.

7. What are the major challenges faced by carbonated soft drink manufacturers?

Key challenges include strict sugar regulations, changing consumer preferences, rising raw material costs, and competition from healthier beverages

8. How is product innovation influencing market competition?

Companies are launching new flavors, functional beverages, and sustainable packaging solutions to attract consumers and strengthen market position.

9. What packaging trends are shaping the U.S. carbonated soft drinks market?

Recyclable cans, lightweight bottles, and eco-friendly packaging materials are becoming increasingly popular.

10. What are the future growth opportunities in the U.S. carbonated soft drinks market?

Growth opportunities include functional drinks, healthier formulations, premium beverages, and sustainable product innovations.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com