Global Carbonated Soft Drinks Market Size, Share, Trends & Growth Forecast Report – Segmented By Type (Standard, Diet, Fruit Flavored Carbonates and Others), By Flavour, Distribution Channel, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis (2026 to 2034)

Global Carbonated Soft Drinks Market Summary

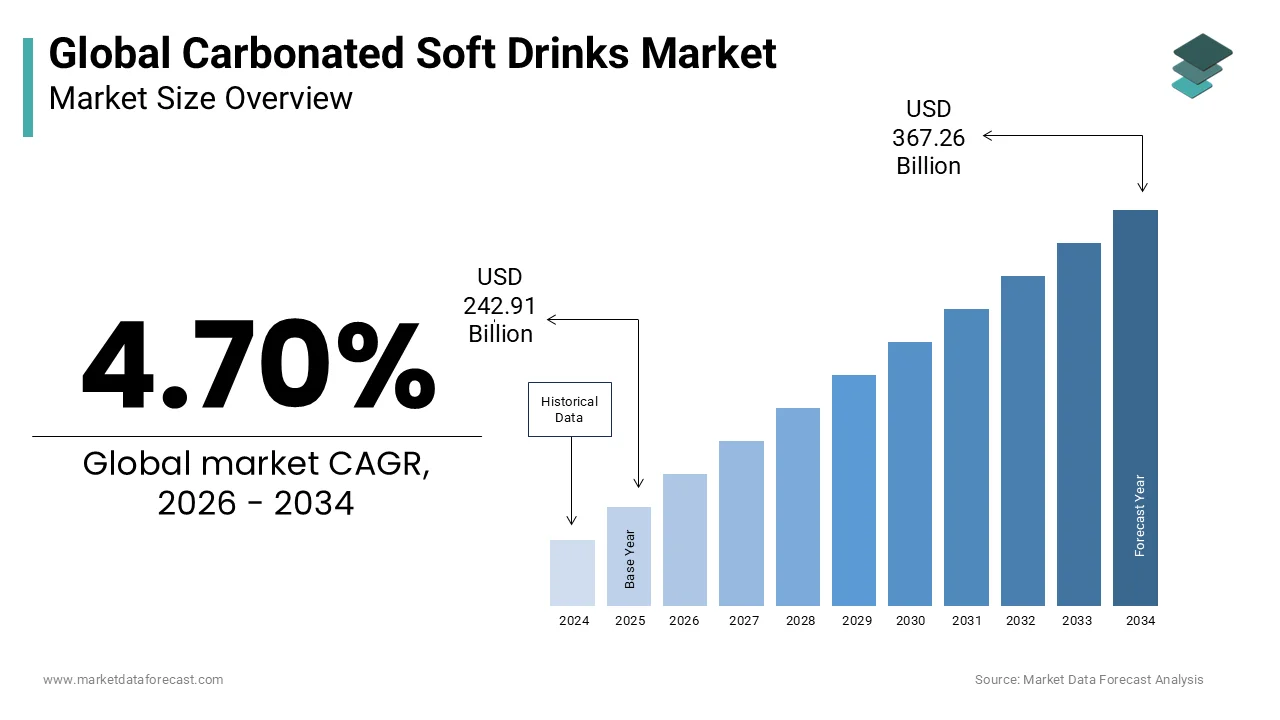

The global carbonated soft drinks market was valued at USD 242.91 billion in 2025, is projected to reach USD 254.33 billion in 2026, and is expected to grow significantly to USD 367.26 billion by 2034, registering a CAGR of 4.70% from 2026 to 2034. Market growth is driven by rising demand for flavored and sparkling beverages, strong brand presence of global beverage companies, and expanding consumption across emerging markets. Innovation in low-sugar and functional carbonated drinks, along with expanding retail penetration, continues to play a key role in market expansion. Marketing campaigns, celebrity endorsements, and new flavor launches also contribute to the market’s global momentum.

Key Market Trends

- Increasing demand for low-calorie, sugar-free, and functional carbonated beverages.

- Continuous innovation in flavors and packaging formats driven by consumer preferences.

- Expansion of store-based and online retail networks, improving product accessibility.

- Rise in consumption across emerging economies, supported by urbanization and lifestyle changes.

- Strong promotional strategies by global beverage giants boosting category awareness.

Segmental Insights

- Based on flavor, the cola segment is anticipated to maintain the highest growth rate, driven by its widespread global popularity and strong consumer loyalty.

- Based on packaging, the bottles segment has shown higher growth compared to cans and is expected to retain dominance due to convenience, portability, and strong retail presence.

- Based on distribution channel, the store-based segment held the leading share in 2023, supported by supermarkets, hypermarkets, convenience stores, and strong merchandising strategies.

Regional Insights

- Europe remains the global leader in carbonated soft drink consumption, driven by established beverage brands, strong retail infrastructure, and diverse flavor preferences.

- North America continues to show steady demand with a rising shift toward healthier and low-calorie carbonated options.

- Asia Pacific is emerging as a fast-growing market owing to young population demographics and rising disposable incomes.

Competitive Landscape

The global carbonated soft drinks market is dominated by major beverage corporations investing in flavor diversification, sustainable packaging solutions, and marketing innovations. Companies are focusing on reformulated beverages with reduced sugar content to align with health-conscious consumer trends.

Key players in the global carbonated soft drinks market include

Coca-Cola, PepsiCo, Cadbury Schweppes, Parle Agro, Postobon, Cott Corporation, Dr. Pepper Snapple Inc., and AJE Group.

Global Carbonated Soft Drinks Market Size

The global carbonated soft drinks market size was valued at USD 242.91 billion in 2025. The global market is estimated to reach USD 367.26 billion by 2034 from USD 254.33 billion in 2026, registering a CAGR of 4.70% from 2026 to 2034.

Carbonated soft drinks are a vast array of non-alcoholic beverages that are infused with carbon dioxide under pressure to create effervescence. This sector includes colas, lemon lime sodas, fruit flavored sparklers, and sparkling waters, which serve as popular refreshment options globally. The definition of this market extends beyond traditional sugary sodas to include a growing segment of low calorie and zero sugar variants that cater to health conscious consumers. The industry is deeply embedded in global consumer culture, often associated with social gatherings, dining experiences, and on the go consumption. According to the World Health Organization, the global prevalence of obesity has nearly tripled since 1975, which has significantly influenced the formulation strategies within this market. As per the Centers for Disease Control and Prevention, added sugars contribute substantially to daily caloric intake in many developed nations, prompting a shift in consumer preferences. The Environmental Protection Agency notes that beverage containers constitute a significant portion of municipal solid waste, driving innovations in recyclable packaging. Furthermore, according to the International Diabetes Federation, approximately 537 million adults were living with diabetes in 2021, highlighting the critical health context surrounding sugary beverage consumption. These societal and environmental factors shape the operational landscape, forcing manufacturers to balance taste appeal with nutritional responsibility and sustainability goals. The market dynamics are thus defined by a complex interplay of cultural habits, health awareness, and regulatory pressures that dictate product development and marketing strategies in the modern era.

MARKET DRIVERS

Innovation in Low Calorie and Zero Sugar Formulations

The rapid expansion of low calorie and zero sugar formulations is primarily boosting the global carbonated soft drinks market growth, as consumers increasingly seek healthier alternatives without sacrificing taste. Modern beverage technology has enabled the development of advanced sweeteners such as stevia, monk fruit, and erythritol, which provide sweetness with minimal or no calories. According to NielsenIQ, sales of zero sugar soft drinks have grown significantly, outpacing regular sugar variants in many key markets, including the United States and Europe. This shift is driven by rising health consciousness and the desire to manage weight and blood sugar levels effectively. The American Heart Association recommends limiting added sugar intake to no more than 6 teaspoons per day for women and 9 teaspoons for men, which has prompted many individuals to switch to diet options. According to a survey by Mintel, 45% of consumers actively look for reduced sugar options when purchasing beverages. Additionally, the introduction of premium sparkling waters with natural flavors has attracted health oriented demographics who previously avoided sodas. These innovations allow manufacturers to retain existing customers while attracting new segments who prioritize wellness. The continuous improvement in taste quality of artificial and natural sweeteners has reduced the stigma associated with diet drinks, further boosting their adoption. This strategic pivot towards healthier formulations ensures sustained relevance and growth in a market increasingly scrutinized for its health impacts.

Expansion of Premium and Craft Soda Segments

The emergence of premium and craft soda segments is another significant driver for the carbonated soft drinks market by appealing to consumers seeking unique and high quality beverage experiences. Unlike mass produced sodas, craft beverages often feature natural ingredients, exotic flavors, and artisanal production methods that differentiate them from standard offerings. According to Statista, the premium soft drink sector has experienced robust growth, as millennials and Generation Z consumers prioritize authenticity and ingredient transparency. These demographics are willing to pay a higher price for products that align with their values, such as organic sourcing and sustainable practices. According to the Specialty Food Association, sales of specialty foods and beverages, including craft sodas, have consistently outpaced overall food industry growth. Brands in this segment often use cane sugar instead of high fructose corn syrup and avoid artificial colors and preservatives, which resonates with clean label trends. Furthermore, the proliferation of independent cafes and gourmet restaurants has provided ideal distribution channels for these niche products. Consumers view craft sodas as a sophisticated alternative to alcohol or standard soft drinks suitable for social occasions. The variety of flavors, ranging from ginger beer to hibiscus and lavender, offers novelty and excitement that mass market brands struggle to replicate. This differentiation strategy allows smaller players to carve out profitable niches and challenges established giants to innovate. The emphasis on quality and uniqueness drives loyalty and word of mouth marketing, fostering a vibrant and expanding subsector within the broader market.

MARKET RESTRAINTS

Stringent Government Regulations and Sugar Taxes

The implementation of stringent government regulations and sugar taxes is impeding the expansion of the global carbonated soft drinks market by increasing production costs and altering consumer pricing structures. Many countries have introduced levies on sugary beverages to combat rising rates of obesity and diabetes, which directly impact the profitability of manufacturers. According to the World Health Organization, more than 50 countries have implemented sugar sweetened beverage taxes as a public health measure. In the United Kingdom, the Soft Drinks Industry Levy led to significant reformulation efforts but also resulted in higher retail prices for some products. According to a study published in The Lancet, sugar taxes can reduce consumption of taxed beverages by approximately 10% to 20%, depending on the tax rate. These fiscal measures discourage frequent purchase among price sensitive consumers, particularly in lower income households. Additionally, regulatory bodies are imposing stricter labeling requirements, mandating clear disclosure of sugar content and health warnings. The European Union continues to refine its regulations on food information, requiring transparent communication of nutritional values. Compliance with these diverse and evolving regulations requires substantial investment in legal counsel, reformulation, and marketing adjustments. Small and medium sized enterprises often struggle to absorb these costs, leading to market consolidation. The uncertainty surrounding future regulatory changes creates a challenging business environment where long term planning is difficult. Consequently, manufacturers face pressure to continuously adapt their portfolios while managing margin erosion caused by taxation and compliance expenses.

Growing Health Consciousness and Negative Perception of Sugary Drinks

The pervasive growth in health consciousness and the resulting negative perception of sugary drinks is also hampering the global market growth. Consumers are increasingly aware of the adverse health effects associated with excessive sugar consumption, including obesity, type 2 diabetes, and dental caries. According to the Global Burden of Disease Study, high sugar intake is a leading risk factor for disability adjusted life years lost globally. This awareness has led to a voluntary reduction in soft drink consumption among many individuals who opt for water, herbal teas, or unsweetened beverages instead. According to the Centers for Disease Control and Prevention, nearly half of US adults consume at least one sugary drink per day, but this number is declining as health education improves. Social media campaigns and public health initiatives have amplified the message against sugary beverages, influencing parental choices for children. Schools and workplaces are increasingly removing sodas from vending machines, replacing them with healthier options. This cultural shift reduces the frequency of consumption and limits the occasions where soft drinks are considered appropriate. Even among those who continue to drink sodas, there is a tendency to moderate intake rather than consume regularly. The stigma attached to sugary drinks as unhealthy indulgences undermines brand loyalty and makes it difficult for manufacturers to maintain historical sales volumes. Overcoming this deep seated negative perception requires extensive marketing efforts and product innovation, which may not always succeed in reversing the trend towards healthier lifestyles.

MARKET OPPORTUNITIES

Development of Functional and Wellness Oriented Beverages

The development of functional and wellness oriented beverages is a promising opportunity for the carbonated soft drinks market by merging refreshment with health benefits. Manufacturers are increasingly infusing sodas with vitamins, minerals, probiotics, and adaptogens to create products that offer additional physiological advantages. For instance, the global functional beverage market is expected to expand significantly as consumers seek drinks that support immunity, digestion, and mental clarity. Probiotic sodas, for example, appeal to consumers interested in gut health, a topic gaining considerable attention in nutritional science. According to the International Scientific Association for Probiotics and Prebiotics, there is growing evidence linking gut health to overall well-being, which drives demand for such products. Additionally, beverages enriched with electrolytes or caffeine cater to active individuals seeking hydration and energy without the drawbacks of traditional energy drinks. This diversification allows brands to position their products as part of a healthy lifestyle rather than an indulgent treat. Collaborations with health experts and nutritionists help validate these claims and build consumer trust. The use of natural ingredients, such as turmeric, ginger, and ashwagandha, aligns with the clean label trend and attracts health conscious buyers. By offering tangible health benefits, companies can justify premium pricing and differentiate themselves in a crowded market. This strategic expansion into functional territories opens new revenue streams and appeals to demographics that previously avoided carbonated drinks due to health concerns.

Adoption of Sustainable and Eco Friendly Packaging Solutions

The adoption of sustainable and eco-friendly packaging solutions offers a significant opportunity for the carbonated soft drinks market to enhance brand image and meet regulatory expectations. Consumers are increasingly demanding environmentally responsible practices from brands, including the use of recyclable, biodegradable, or reusable containers. According to the Ellen MacArthur Foundation, the New Plastics Economy Global Commitment has mobilized hundreds of organizations to eliminate problematic plastic packaging and increase recycling rates. Many major beverage companies have committed to using 100% recycled polyethylene terephthalate, or rPET, in their bottles by specific target dates. Aluminum cans are also gaining popularity due to their infinite recyclability and lower carbon footprint compared to plastic. According to the Aluminum Association, aluminum recycling saves 95% of the energy required to produce new metal, making it an attractive option for sustainability focused brands. Innovations such as plant based bottles and paper based containers are being explored to further reduce reliance on fossil fuels. Retailers are incentivizing sustainable packaging through preferential shelf placement and promotional support. Brands that successfully communicate their sustainability efforts can build stronger emotional connections with environmentally conscious consumers. This transition not only mitigates regulatory risks but also appeals to younger generations who prioritize corporate social responsibility. By leading the way in packaging innovation, companies can secure a competitive advantage and contribute to a circular economy while maintaining product quality and safety.

MARKET CHALLENGES

Volatility in Raw Material and Supply Chain Costs

The volatility in raw material and supply chain costs is a major challenge to the carbonated soft drinks market by impacting profit margins and pricing stability. The production of soft drinks relies on various commodities, including sugar, aluminum, steel for cans, and petroleum based plastics for bottles, all of which are subject to fluctuating global prices. According to the Food and Agriculture Organization of the United Nations, global food prices have experienced significant volatility due to climate change, geopolitical conflicts, and trade disruptions. Energy costs also play a critical role, as manufacturing and transportation require substantial power inputs. According to the International Energy Agency, energy price spikes can significantly increase operational expenses for industrial sectors, including beverage production. These cost increases are often difficult to pass on to consumers, who are sensitive to price changes and may switch to cheaper alternatives or private label brands. Supply chain disruptions caused by pandemics or logistical bottlenecks can lead to shortages of key ingredients and packaging materials, further exacerbating the situation. Manufacturers must engage in complex hedging strategies and supplier negotiations to mitigate these risks, which requires significant financial expertise and resources. Smaller companies may lack the bargaining power to secure favorable terms, leaving them vulnerable to margin compression. The unpredictability of input costs makes long term financial planning challenging and can hinder investment in innovation and expansion. Maintaining profitability in such an environment requires agile operational management and strategic cost control measures.

Intense Competition from Alternative Beverage Categories

The intense competition from alternative beverage categories, such as bottled water, ready to drink tea and coffee, and energy drinks is further challenging the global market expansion. Consumers have a wide array of choices for hydration and refreshment, many of which are perceived as healthier or more functional than traditional sodas. According to Euromonitor International, bottled water has surpassed carbonated soft drinks as the largest beverage category by volume in many regions, due to its association with health and purity. Ready to drink tea and coffee offerings have also gained traction, appealing to consumers seeking caffeine and antioxidants without the high sugar content of sodas. The energy drink segment continues to grow, particularly among younger demographics who seek performance enhancing benefits. These alternative categories benefit from strong marketing campaigns and innovative product launches that capture consumer interest and shelf space. Retailers often allocate prime positioning to these trending categories, reducing visibility for traditional soft drinks. The fragmentation of consumer preferences means that brand loyalty to sodas is eroding as shoppers experiment with new options. To remain competitive, soft drink manufacturers must diversify their portfolios to include these alternative categories, which can cannibalize their core business. The need to compete on multiple fronts stretches marketing budgets and dilutes brand focus. This dynamic landscape requires continuous adaptation and innovation to prevent further loss of market share to more agile and health aligned beverage segments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.70% |

| Segments Covered | By Type, Flavors, Packaging, Distribution Channel and Region |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Coca-Cola, PepsiCo, Cadbury Schweppes, Parle Agro, Postobon, Cott Corporation, Dr. Pepper Snapple Inc., and AJE Groups |

SEGMENTAL ANALYSIS

By Flavor Insights

The cola segment dominated the market by holding 44.7% of the global market share in 2025. The dominance of cola segment in the global market can be credited to the deep brand loyalty and the universal appeal of its distinct flavor profile, which serves as a cultural staple in many societies. The unparalleled brand loyalty cultivated by major multinational corporations over decades of strategic marketing and cultural integration is further contributing to the expansion of the global carbonated soft drinks market. Cola brands have successfully positioned themselves not merely as beverages but as symbols of happiness, sharing, and social connection. According to Interbrand, Coca Cola consistently ranks among the most valuable global brands with an estimated brand value exceeding 90 billion US dollars, which underscores the power of its identity. This emotional connection ensures that consumers often choose cola out of habit and preference rather than price sensitivity. The ubiquity of cola in fast food chains, movie theaters, and sporting events reinforces its status as the default beverage choice for many occasions. According to a study by Kantar Worldpanel, cola remains the most frequently purchased soft drink category in households across North America and Europe. The consistency in taste, regardless of geographic location, provides a sense of familiarity and comfort to consumers traveling or living abroad. Furthermore, massive advertising budgets allow these brands to maintain high visibility and recall, ensuring they remain top of mind for consumers. The ability to innovate within the core brand, such as introducing zero sugar variants while maintaining the original taste identity, helps retain traditional customers while attracting health conscious ones. This combination of emotional resonance, consistent quality, and pervasive availability solidifies the cola segment's leading position in the market.

However, the lemon and lime segment is projected to be the fastest growing flavor category in the carbonated soft drinks market and is expected to record a CAGR of 4.48% over the forecast period owing to the perception of these flavors as refreshing and lighter alternatives to heavier colas. The rapid growth of the lemon and lime segment is further attributed to the consumer perception of these flavors as refreshing, crisp, and lighter alternatives to the heavier and sweeter profile of cola. In warmer climates and during summer months, the demand for citrus flavored beverages surges as consumers seek hydration and cooling effects. According to the Beverage Marketing Corporation, citrus flavored sodas have seen a resurgence in popularity, as consumers move away from dark colas in favor of clearer and seemingly healthier options. The association of lemon and lime with natural citrus fruits enhances their appeal to health conscious individuals, who may perceive them as containing more natural ingredients, even when artificially flavored. This trend towards clean labels, as many brands are introducing sparkling lemon and lime waters with minimal additives is further boosting the expansion of the lemon and lime segment in the global market. According to a survey by Mintel, 30% of consumers prefer citrus flavors for their perceived freshness and ability to cleanse the palate. The versatility of lemon and lime sodas also allows them to be used as mixers in alcoholic and non-alcoholic cocktails, expanding their usage occasions beyond standalone consumption. The rise of craft soda brands has further revitalized this segment by offering artisanal versions with real fruit juice and organic sweeteners. These innovations attract premium seekers and differentiate the product from standard mass market offerings. The combination of refreshment appeal and perceived lightness drives the accelerated growth of this segment.

By Packaging Insights

The bottles segment led the market by holding 54.5% of the global market share in 2025. The dominance of bottles segment in the global market is attributed to the convenience of resealability, which allows consumers to consume the beverage in multiple sittings without losing carbonation or freshness. This feature is particularly valued by families and individuals who prefer larger pack sizes for cost efficiency but do not consume the entire contents at once. According to the Pet Resin Association, polyethylene terephthalate, or PET bottles, are the most widely used packaging format for soft drinks, due to their lightweight nature and shatter resistance. The ability to recap a bottle enhances portability, making it ideal for on the go consumption in schools, offices, and during travel. According to a study by Euromonitor International, single serve plastic bottles remain a popular choice for immediate consumption, due to their ease of handling and disposal. Additionally, the availability of bottles in various sizes, ranging from 200 milliliters to 2 liters, provides flexibility for different household needs and occasions. This versatility ensures that bottles cater to both individual and group consumption scenarios. The transparency of PET bottles also allows consumers to see the product, which can influence purchase decisions based on visual appeal. Furthermore, advancements in bottle design, such as ergonomic shapes and improved cap technologies, have enhanced user experience. The combination of functional benefits and consumer convenience solidifies the position of bottles as the leading packaging format in the market.

However, the cans segment is growing exponentially and is estimated to register a CAGR of 6.2% over the forecast period owing to their superior recyclability and the increasing consumer demand for environmentally sustainable packaging solutions. Aluminum cans are infinitely recyclable without loss of quality, making them a preferred choice for eco conscious buyers. According to the Aluminum Association, the recycling rate for aluminum beverage cans in the United States is approximately 50%, which is significantly higher than that of plastic bottles. In Europe, the recycling rates are even higher, with some countries achieving over 90% recovery rates, as per Metal Packaging Europe. This high recyclability aligns with global sustainability goals and regulatory pressures to reduce plastic waste. Consumers are increasingly aware of the environmental impact of their choices and are actively seeking brands that prioritize circular economy principles. The use of recycled aluminum also requires 95% less energy than producing new metal, which reduces the carbon footprint of the packaging. Major beverage companies are leveraging this advantage by promoting the green credentials of their canned products in marketing campaigns. The shift towards sustainable packaging is not just a trend but a long term structural change in consumer behavior. As governments implement stricter regulations on single use plastics, the demand for aluminum cans is expected to rise further. This environmental advantage, combined with strong consumer preference for sustainable options, drives the accelerated growth of the cans segment in the market.

By Distribution Channel Insights

The store-based segment held the highest share of 86.1% of the global market share in 2025. The leading position of store-based segment in the global market is attributed to the extensive retail network that ensures immediate availability and accessibility of carbonated soft drinks to consumers. Supermarkets, hypermarkets, and convenience stores are ubiquitous in both urban and rural areas, providing easy access to a wide variety of beverage options. According to NielsenIQ, the majority of grocery shopping still takes place in physical stores, where consumers can browse and select products based on immediate needs and preferences. The presence of soft drinks in high traffic areas, such as checkout counters and end caps, stimulates impulse purchases, which contribute significantly to sales volume. Convenience stores in particular play a crucial role in the on the go segment, offering single serve bottles and cans to commuters and travelers. The ability to physically inspect the product, check expiration dates, and choose specific pack sizes enhances consumer confidence and satisfaction. Additionally, promotional activities, such as discounts, bundle offers, and loyalty programs, are effectively executed in physical stores, driving foot traffic and sales. The established infrastructure of retail chains allows for efficient restocking and inventory management, ensuring consistent product availability. This widespread presence and operational efficiency make store based channels the primary source of carbonated soft drink purchases for the majority of consumers globally.

On the other hand, the non-store based distribution segment is the fastest growing channel for the carbonated soft drinks market and is estimated to record a CAGR of 8.8% over the forecast period owing to the expansion of e-commerce platforms and the increasing digital accessibility of beverage products. Online grocery shopping has become mainstream, as consumers appreciate the convenience of browsing and ordering from home. According to Statista, the online food and beverage market has experienced double digit growth in recent years, as internet penetration and smartphone usage increase globally. Major retailers and specialized online grocers have invested in user friendly interfaces and efficient logistics to facilitate seamless transactions. The ability to order bulk quantities of soft drinks and have them delivered to the doorstep is particularly appealing to families and office managers, who wish to avoid the hassle of carrying heavy loads. Subscription services for regular deliveries of favorite beverages offer added convenience and cost savings, encouraging customer retention. The integration of digital payment systems and real time tracking enhances the overall shopping experience, building trust and reliability. Additionally, online platforms provide access to a wider range of products, including niche and international brands that may not be available in local stores. This breadth of choice attracts diverse consumer segments and drives sales growth. The continuous improvement in digital infrastructure and consumer comfort with online transactions ensures that non store based channels will continue to expand at an accelerated pace.

REGIONAL ANALYSIS

North America Carbonated Soft Drinks Market Analysis

North America held the leading position in the global carbonated soft drinks market in 2025 with 34.3% of the global market share. The dominance of North America is majorly attributed to the high per capita consumption and a mature market landscape with strong brand presence. North America stands as the predominant force in the global carbonated soft drinks market, driven by deeply ingrained cultural habits and a highly developed retail infrastructure. The United States in particular has one of the highest per capita consumption rates of soft drinks worldwide, although recent trends show a slight decline due to health concerns. According to the Beverage Marketing Corporation, the US soft drink market remains vast, with billions of gallons consumed annually, reflecting the entrenched role of these beverages in daily life. The presence of global giants such as The Coca Cola Company and PepsiCo, headquartered in the region, ensures strong distribution networks and marketing dominance. However, the market is evolving, as consumers shift towards healthier options, prompting manufacturers to expand their portfolios of zero sugar and functional beverages. The prevalence of obesity and diabetes has led to public health initiatives and sugar taxes in certain cities, which are influencing formulation strategies. Despite these challenges, the demand for convenience and flavor variety sustains market volume. The rise of craft sodas and premium sparkling waters offers growth opportunities for niche players. Retail channels, ranging from supermarkets to vending machines, ensure widespread accessibility. The region's economic stability and high disposable income support the consumption of premium and specialized products. Consequently, North America remains a critical market, where innovation and adaptation to health trends define competitive success.

Asia Pacific Carbonated Soft Drinks Market Analysis

Asia Pacific was the second largest regional segment for carbonated soft drinks in the global market in 2025 due to its rapid urbanization and a growing middle class, which drives increased consumption. Countries such as China, India, and Indonesia are experiencing rising disposable incomes, which enable greater spending on packaged beverages. According to Euromonitor International, the Asia Pacific soft drinks market is expected to grow at a faster rate than other regions, due to the expanding middle class and urbanization. The young population in these countries is particularly receptive to global brands and new flavors, driving demand for colas and fruit flavored sodas. Local manufacturers are also gaining traction by offering affordable products tailored to regional tastes. The proliferation of modern retail formats, such as supermarkets and convenience stores, alongside traditional mom and pop shops, ensures broad distribution reach. However, the market faces challenges from increasing health awareness and government regulations aimed at reducing sugar intake. Some countries have implemented sugar taxes, which are prompting reformulation efforts. Despite these headwinds, the sheer size of the population and the ongoing shift from informal to formal retail sectors provide substantial growth potential. The adoption of digital marketing and e commerce platforms further enhances brand visibility and accessibility. As lifestyle patterns modernize, the consumption of carbonated soft drinks is expected to rise, making Asia Pacific a key engine for global market expansion.

Europe Carbonated Soft Drinks Market Analysis

Europe holds a significant position in the global carbonated soft drinks market due to a high degree of maturity and a strong focus on health and environmental sustainability. Western European countries, such as Germany, France, and the United Kingdom, have well established consumption patterns but are witnessing a shift towards low and no sugar variants. According to the European Soft Drinks Association, the industry has made substantial progress in reducing sugar content and promoting recycling initiatives. The implementation of sugar taxes in several European nations, including the United Kingdom and France, has accelerated reformulation efforts and influenced consumer choices. Consumers in Europe are increasingly prioritizing natural ingredients and clean labels, which has boosted the demand for sparkling waters and organic sodas. The region is also a leader in sustainable packaging with high recycling rates.

COMPETITIVE LANDSCAPE

The competition in the carbonated soft drinks market is intense and characterized by the dominance of a few multinational corporations alongside a growing number of niche and regional players. Established giants leverage their extensive distribution networks strong brand recognition and massive marketing budgets to maintain market leadership. However they face increasing pressure from health conscious consumers and regulatory bodies imposing sugar taxes and strict labeling requirements. This environment has forced major companies to reformulate products and diversify into healthier alternatives such as sparkling waters and functional beverages. Private label brands from large retail chains offer cost effective alternatives that challenge branded products on price. The rise of craft soda makers introduces innovation and unique flavors that appeal to discerning consumers seeking authenticity. Competitive rivalry is further heightened by the battle for shelf space in retail outlets and visibility in digital channels. Companies invest heavily in promotional activities sponsorships and celebrity endorsements to capture consumer attention. The threat of substitute products including tea coffee and juice remains significant requiring continuous innovation. Overall the market demands agility strategic foresight and a strong commitment to sustainability and health to succeed in this highly contested and evolving industry landscape.

KEY MARKET PLAYERS

The following are the key players in the global carbonated soft drinks market

- Coca-Cola

- PepsiCo

- Cadbury Schweppes

- Parle Agro

- Postobon

- Cott Corporation

- Dr. Pepper Snapple Inc.

- AJE Group

Top Players in the Market

- The Coca Cola Company remains a dominant force in the global carbonated soft drinks landscape with an extensive portfolio of sparkling beverages. The corporation continuously innovates by expanding its zero sugar offerings to align with evolving health consciousness among consumers worldwide. Recently the company has invested heavily in sustainable packaging initiatives aiming to collect and recycle a bottle or can for every one it sells. They have also diversified their flavor profiles by introducing unique regional variants that cater to local tastes in emerging markets. Strategic partnerships with major food service providers ensure widespread availability and visibility of their products. The company leverages advanced digital marketing techniques to engage younger demographics through personalized campaigns. By focusing on total beverage consumption rather than just soda volumes Coca Cola strengthens its resilience against declining traditional soda trends. Their commitment to water stewardship and community development further enhances brand reputation. These comprehensive efforts allow the company to maintain its leadership position while adapting to regulatory pressures and shifting consumer preferences in the dynamic global beverage industry.

- PepsiCo Inc holds a significant position in the carbonated soft drinks market driven by its strong brand equity and diverse product portfolio. The company actively pursues growth by reformulating its core brands to reduce sugar content and introduce natural sweeteners. PepsiCo has recently focused on enhancing its supply chain efficiency through digital transformation and automation technologies. They have expanded their presence in the premium segment by acquiring niche craft soda brands that appeal to health conscious and adventurous consumers. The company emphasizes sustainability by increasing the use of recycled materials in its packaging and reducing plastic waste. PepsiCo also leverages its powerful distribution network to ensure product accessibility in both urban and rural areas globally. Marketing campaigns featuring high profile celebrities and sports endorsements help maintain brand relevance and appeal. The integration of data analytics allows for better consumer insights and targeted marketing strategies. By balancing innovation with operational excellence PepsiCo continues to strengthen its competitive stance and drive long term value creation in the global carbonated beverage sector.

- Keurig Dr Pepper Inc is a major player in the North American carbonated soft drinks market known for its diverse brand portfolio including Dr Pepper and Seven Up. The company focuses on strategic acquisitions and partnerships to expand its reach and product offerings. Recently Keurig Dr Pepper has invested in innovative packaging solutions such as aluminum bottles and recyclable materials to meet sustainability goals. They have also enhanced their direct to consumer capabilities through e commerce platforms allowing for greater customer engagement and data collection. The company prioritizes operational efficiency by optimizing its manufacturing processes and distribution networks. Marketing efforts are centered around brand heritage and emotional connections with consumers particularly for flagship brands like Dr Pepper. Keurig Dr Pepper also explores new flavor innovations and limited edition releases to generate excitement and trial among consumers. By leveraging its strong retail relationships and agile business model the company effectively competes against larger global rivals. Their focus on profitable growth and shareholder value ensures sustained investment in brand building and product development within the competitive beverage landscape.

Top Strategies Used by the Key Market Participants

Key players in the carbonated soft drinks market predominantly employ product diversification and health oriented reformulation strategies to address changing consumer preferences. Companies are aggressively expanding their portfolios of zero sugar and low calorie options to mitigate the impact of health concerns and regulatory taxes. Strategic acquisitions of emerging brands in the sparkling water and craft soda segments allow established giants to capture niche markets and innovate rapidly. Sustainability initiatives form a core part of corporate strategy with significant investments in recyclable packaging and water conservation programs to enhance brand image and comply with environmental regulations. Digital transformation is another critical strategy where companies utilize data analytics and e commerce platforms to personalize marketing efforts and improve supply chain efficiency. Partnerships with food service providers and retailers ensure prominent shelf placement and bundled promotions that drive sales volume. Additionally manufacturers are focusing on premiumization by introducing artisanal and exotic flavors that command higher price points. These multifaceted strategies enable key participants to maintain competitiveness adapt to market dynamics and sustain growth in an increasingly health conscious and environmentally aware global marketplace.

MARKET SEGMENTATION

This research report on the global carbonated soft drinks market has been segmented and sub-segmented based on flavor, packaging, distribution, and region.

By Flavor

- Cola

- Lemon and lime

- Orange

- Others

By Packaging

- Bottles

- Cans

By Distribution Channel

- Store-based

- Non-store-based

By Region

- North America

- Europe

- Latin America

- Asia Pacific

- Middle East & Africa

Frequently Asked Questions

1. What is the global carbonated soft drinks market?

The global carbonated soft drinks market includes beverages that contain dissolved carbon dioxide, such as colas, flavored sodas, fruit-based carbonated drinks, tonic water, and sparkling beverages.

2. What factors are driving the growth of the carbonated soft drinks market worldwide?

Growth is driven by rising urbanization, strong brand marketing, product innovation in flavors, expanding retail distribution, and increasing consumption in emerging economies.

3. What types of carbonated soft drinks are available?

Major types include regular carbonated drinks, diet or zero-calorie sodas, flavored sodas, fruit-infused carbonated beverages, sparkling water, and functional carbonated drinks.

4. Which region dominates the global carbonated soft drinks market?

North America holds a significant share, while Asia-Pacific is experiencing the fastest growth due to higher disposable incomes and changing lifestyle preferences.

5. What challenges does the carbonated soft drinks market face?

Challenges include rising health concerns related to sugar intake, increasing government regulations, the shift toward healthier beverages, and competition from juices and sports drinks.

6. Why are diet and zero-sugar carbonated drinks gaining popularity?

Consumers are seeking healthier alternatives to traditional sugary sodas, driving demand for low-calorie, zero-sugar, and functional carbonated beverages.

7. How is innovation influencing the carbonated soft drinks market?

Brands are introducing new flavors, natural sweeteners, organic carbonated beverages, functional sodas with vitamins or probiotics, and sustainable packaging to attract health-conscious consumers.

8. Which distribution channels are important for carbonated soft drinks?

Key channels include supermarkets, convenience stores, hypermarkets, foodservice outlets, vending machines, and online retail platforms.

9. What role does packaging play in the carbonated soft drinks industry?

Packaging is crucial for carbonation retention, product safety, branding, portability, and sustainability, with growing adoption of recyclable bottles and cans.

10. Who are the major players in the global carbonated soft drinks market?

Leading companies include The Coca-Cola Company, PepsiCo, Keurig Dr Pepper, Suntory Beverage & Food, Asahi Group Holdings, Monster Beverage Corporation, and National Beverage Corp.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com