U.S Cheese Market Size, Share, Trends & Growth Forecast Report Segmented By Source (Animal Type, Plant Type), Type, Product Type, And Country (California, Washington, Oregon, New York & Rest Of The United States) – Industry Analysis And Forecast, 2026 To 2034

U.S Cheese Market Size

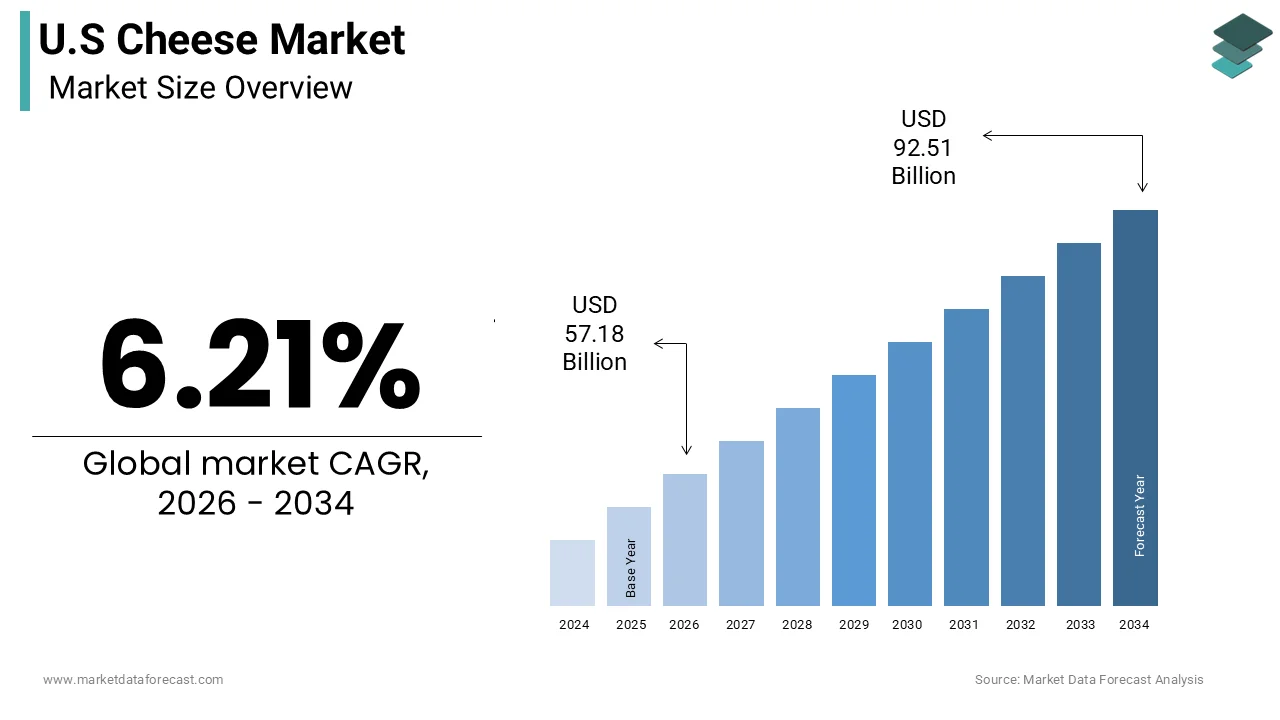

The U.S. cheese market size was calculated to be USD 53.84 billion in 2025 and is anticipated to be worth USD 92.59 billion by 2034, from USD 57.18 billion in 2026, growing at a CAGR of 6.21% during the forecast period.

The cheese is the dairy industry, characterized by diverse product offerings ranging from traditional cheddar to artisanal varieties. Cheese is defined as a dairy product derived from milk coagulation, available in numerous textures, flavors, and forms that cater to varied culinary applications. This market serves both retail consumers and industrial food manufacturers, playing a pivotal role in the national diet. According to the United States Department of Agriculture, per capita consumption of cheese in the United States has reached approximately 41 pounds annually, reflecting its entrenched status in American eating habits. The robust infrastructure of dairy farms, processing facilities, and distribution networks ensures a consistent supply across the continent. Consumer preferences are shifting toward premium and specialized products, influencing production strategies and innovation. The market encompasses various categories, including natural cheese, processed cheese, and specialty imports, each serving distinct consumer segments. Regulatory standards ensure quality and safety, maintaining consumer trust in dairy products. The integration of cheese into quick service restaurants and home cooking continues to drive volume growth.

MARKET DRIVERS

Increasing Demand for Convenience and Ready-to-Eat Foods

The increasing demand for convenience and ready-to-eat foods, as consumers seek quick and easy meal solutions, is propelling the growth of the United States cheese market. Cheese is a versatile ingredient that enhances the flavor and nutritional profile of snacks, sandwiches, and prepared meals by making it a staple in convenience food formulations. According to the research, sales of ready-to-eat and ready-to-heat meals have grown significantly, with cheese being a key component in many of these products. The packaged snacks containing cheese, such as crackers and chips, continue to see strong sales performance, driven by busy lifestyles and the need for portable nutrition. The rise of single-serve cheese packs and string cheese further supports this trend, offering convenient portion control for on-the-go consumption. Quick service restaurants also contribute to this demand by incorporating cheese into burgers, tacos, and pizzas, which remain popular menu items. The ability of cheese to melt well and provide a savory taste makes it ideal for fast food applications. Furthermore, the expansion of e-commerce grocery shopping has made it easier for consumers to purchase a wide variety of cheese products online, enhancing accessibility. This shift toward convenience-oriented consumption ensures steady demand for cheese across multiple categories.

Growing Popularity of International Cuisines and Gourmet Trends

The growing popularity of international cuisines and gourmet dining trends, by expanding consumer palates and encouraging experimentation with diverse flavors, is significantly elevating the growth of the United States cheese market. As Americans increasingly explore Mediterranean, Asian, and Latin American dishes, the demand for specific cheese varieties such as feta, mozzarella, and cotija has risen. The ethnic cuisines continue to influence menu development, with cheese playing a central role in authentic preparations. The inclusion of artisanal and imported cheeses in restaurant menus has increased, reflecting a consumer preference for high-quality and unique ingredients. This trend extends to home cooking, where individuals seek to replicate restaurant experiences using premium cheese products. Retailers have responded by expanding their specialty cheese sections, offering a wider selection of aged, flavored, and organic options. The influence of social media and food television programs further accelerates this trend by showcasing creative cheese-based recipes and pairing ideas. Consumers are becoming more knowledgeable about cheese origins and production methods, driving demand for transparent and sustainable sourcing. The willingness to pay a premium for gourmet experiences supports the growth of higher-margin cheese segments.

MARKET RESTRAINTS

Health Concerns Related to Saturated Fat and Sodium Content

The health concerns related to saturated fat and sodium content, as consumers become more conscious of their dietary intake, are limiting the growth of the United States cheese market. Cheese is often perceived as high in calories and unhealthy fats, leading some individuals to limit their consumption or seek alternatives. Heart disease remains a leading cause of death in the United States, prompting public health campaigns that advise reducing saturated fat intake. Excessive sodium consumption is linked to high blood pressure, and many cheese varieties contain significant amounts of salt. This awareness has led to a decline in consumption among health-conscious demographics, who prioritize low-fat and low-sodium options. While reduced-fat cheeses are available, they often lack the texture and flavor profile of full-fat varieties, limiting their appeal. The stigma associated with dairy fat continues to influence purchasing decisions among younger consumers who favor plant-based diets. Nutrition labels and warning signs in some jurisdictions further highlight these health risks, affecting consumer perception. Although moderate consumption is considered safe by many nutritionists, the prevailing narrative around healthy eating poses a challenge to market growth.

Volatility in Raw Milk Prices and Input Costs

The volatility in raw milk prices and input costs, by impacting production margins and pricing stability, is additionally hampering the growth of the United States cheese market. The cost of milk, which is the primary ingredient in cheese production, fluctuates due to factors such as feed costs, weather conditions, and supply chain disruptions. The milk prices have experienced considerable variability in recent years, affecting the profitability of dairy processors. The inflation in energy and transportation costs has further increased operational expenses for cheese manufacturers. These rising costs are often passed on to consumers in the form of higher retail prices, which can dampen demand, particularly for price-sensitive shoppers. Small and medium-sized producers are disproportionately affected by these fluctuations, as they lack the economies of scale to absorb cost increases. The unpredictability of input costs makes long-term planning and budgeting difficult for industry participants. Additionally, labor shortages in the dairy sector contribute to higher wages and operational challenges. The combination of volatile raw material prices and rising overheads squeezes profit margins, limiting the ability of companies to invest in innovation and expansion.

MARKET OPPORTUNITIES

Expansion of Plant-Based and Alternative Cheese Products

The expansion of plant-based and alternative cheese products by catering to the growing number of vegans and lactose-intolerant consumers is ascribed to elevating the growth of the United States cheese market. As awareness of environmental and ethical issues related to dairy farming increases, more individuals are seeking non-dairy alternatives. The sales of plant-based foods have grown substantially, with cheese alternatives representing a key category. As per Mintel, innovations in ingredient technology have improved the taste and texture of plant-based cheeses by making them more appealing to mainstream consumers. Ingredients, such as cashews, almonds, and coconut oil, are being used to create realistic dairy-free options that melt and stretch like traditional cheese. Major dairy companies are entering this space by launching their own plant-based lines, leveraging existing distribution networks to reach broader audiences. The flexibility of plant-based formulations allows for customization of flavors and nutritional profiles, attracting health-conscious buyers. Retailers are dedicating more shelf space to these products, recognizing their potential for growth. The opportunity extends beyond retail to foodservice, where restaurants are incorporating vegan cheese into menus to accommodate diverse dietary preferences.

Growth of Artisanal and Specialty Cheese Segments

The growth of artisanal and specialty cheese by appealing to consumers seeking unique and high-quality experiences is another attribute to enhance the growth of the United States cheese market. There is a rising interest in locally sourced and handcrafted cheeses that offer distinct flavors and stories behind their production. The specialty cheeses continue to outpace general cheese sales in terms of value growth, driven by consumer willingness to pay for premium quality. Farmers' markets, specialty shops, and online platforms provide direct channels for artisans to connect with customers, fostering brand loyalty and education. The trend toward experiential dining encourages consumers to explore cheese boards and pairings, boosting demand for diverse varieties. Collaborations between cheesemakers and local breweries or wineries create synergistic marketing opportunities that enhance visibility. Tourism focused on dairy farms and creameries also contributes to this growth by educating visitors about the craft of cheesemaking. The emphasis on sustainability and animal welfare in artisanal production aligns with contemporary consumer values, which is further driving preference for these products.

MARKET CHALLENGES

Supply Chain Disruptions and Logistics Constraints

The supply chain disruptions and logistics constraints, by affecting the timely delivery of products and increasing operational costs is specific challenge for the growth of the United States cheese market. The complexity of the dairy supply chain, which involves perishable goods requiring temperature-controlled transportation, makes it vulnerable to interruptions. The shortages and capacity constraints have led to delays and higher freight rates by impacting the efficiency of cheese distribution. These disruptions can result in spoilage and waste for fresh cheese varieties with short shelf lives. The reliance on just-in-time inventory systems leaves little room for error, making companies susceptible to sudden shocks. Weather events and natural disasters also threaten supply chain stability, affecting both production and transportation. The need for redundant systems and alternative sourcing strategies adds to operational complexity and cost. Manufacturers must navigate these uncertainties while maintaining product quality and meeting customer expectations. The lack of visibility into upstream and downstream processes complicates decision-making and risk management.

Regulatory Compliance and Food Safety Standards

The regulatory compliance and stringent food safety standards, by imposing rigorous requirements on production and handling processes, are another factor that limits the growth of the United States cheese market. Cheese manufacturers must adhere to regulations set by agencies, such as the Food and Drug Administration and the United States Department of Agriculture, to ensure product safety and quality. The outbreaks of foodborne illnesses linked to dairy products can lead to recalls, legal liabilities, and reputational damage by necessitating strict adherence to hygiene protocols. As per the Centers for Disease Control and Prevention, monitoring and reporting requirements for pathogens such as Listeria and Salmonella are extensive, requiring continuous testing and documentation. Compliance with these standards involves significant investment in facility upgrades, training, and quality assurance systems. Small producers may struggle to meet these requirements due to limited resources, creating barriers to entry and expansion. Changing regulations regarding labeling, additives, and environmental impact add further complexity to the compliance landscape. The need for traceability throughout the supply chain requires advanced technology and data management capabilities. Failure to comply can result in fines, shutdowns, and loss of consumer trust. Maintaining high standards while managing costs is a delicate balance that requires ongoing vigilance and adaptation. This regulatory burden acts as a constant challenge for industry participants, demanding robust governance and operational excellence to ensure safe and compliant products.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.21% |

| Segments Covered | By Source, Type, Product Type, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Kraft Heinz Company, Dairy Farmers of America, Saputo Inc., Arla Foods, Lactalis Group, Fonterra Co-operative Group, Land O'Lakes, Inc., Tillamook County Creamery Association, Bel Group, Sargento Foods Inc. |

SEGMENTAL ANALYSIS

By Source Insights

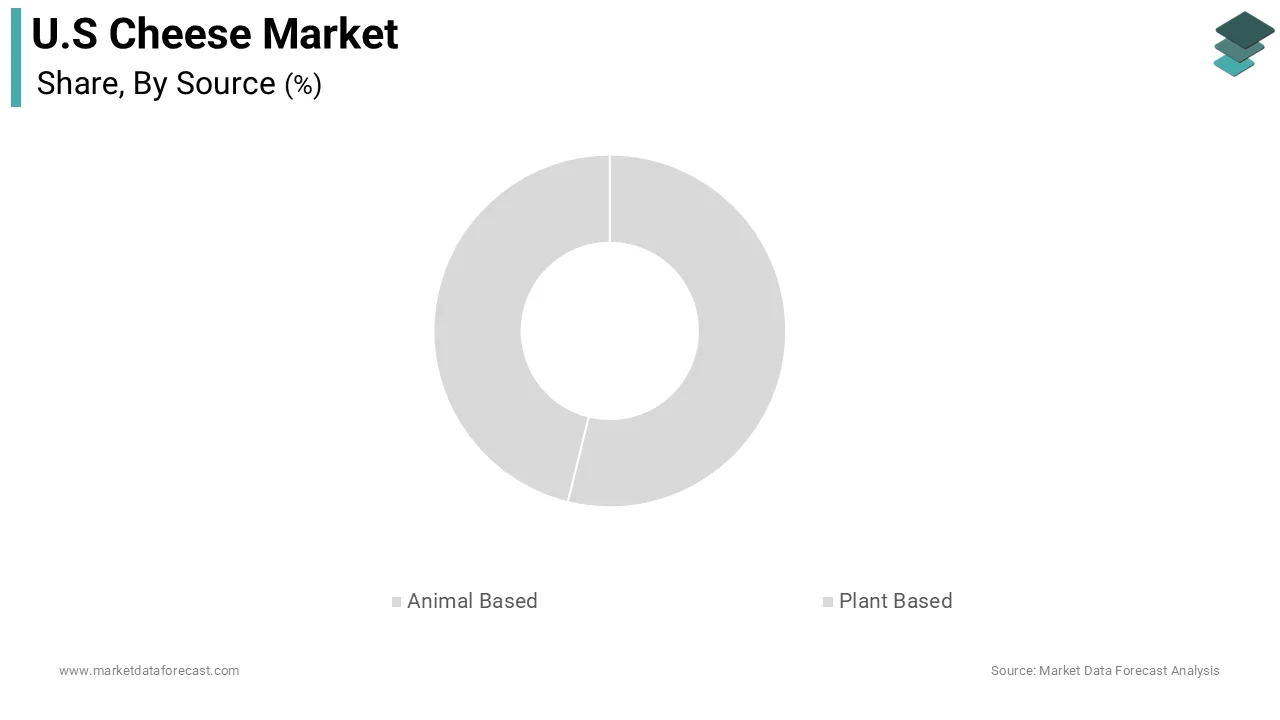

The animal-based cheese segment was the largest by holding a significant share of the United States cheese market in 2025 due to the established dairy infrastructure and deep-rooted consumer preference for traditional dairy products. The United States possesses a vast network of dairy farms and processing facilities that ensure a consistent supply and competitive pricing for cow milk cheese. According to the United States Department of Agriculture, cattle milk accounts for over 98% of total milk production in the country, providing an abundant raw material base for cheese manufacturing. As per the International Dairy Foods Association, the familiarity and versatility of animal-based cheese in cooking and snacking sustain its leading position. Consumers associate dairy cheese with high protein content and calcium benefits due to its role in daily nutrition. The widespread availability of animal-based cheese in retail stores and foodservice outlets ensures it remains the default choice for most buyers. Traditional recipes and culinary habits further cement this dominance, as many iconic American dishes rely on the melting properties and flavor profiles of dairy cheese. The industry continues to innovate within this segment by offering organic and grass-fed options that appeal to health-conscious consumers.

The plant-based segment is likely to witness the fastest CAGR of 7.6% during the forecast period, with the rise of veganism and increased awareness of lactose intolerance. A growing number of consumers are adopting plant-based diets for ethical, environmental, and health reasons, creating demand for dairy-free alternatives. The retail sales of plant-based foods have grown significantly, with plant-based cheese emerging as a key category. The prevalence of lactose intolerance affects a substantial portion of the adult population by prompting them to seek non-dairy options that do not cause digestive discomfort. The improvement in taste and texture of plant-based cheeses has made them more acceptable to mainstream consumers, who previously avoided them. Ingredients such as cashews, almonds, and coconut oil are used to mimic the creaminess and melt of dairy cheese, enhancing appeal. Retailers are expanding their plant-based offerings to meet this growing demand, providing greater visibility and accessibility.

By Type Insights

The natural segment was accounted for in holding 34.2% of the US cheese market share in 2025, with the strong consumer preference for minimally processed and clean-label foods. Shoppers are increasingly seeking products with simple ingredient lists and recognizable components, which natural cheese provides. Consumers prefer foods with fewer artificial ingredients, driving demand for natural dairy products. The natural cheeses, such as cheddar, gouda, and brie, are perceived as higher quality and more authentic than processed alternatives. This perception supports premium pricing and loyal customer bases for brands that emphasize traditional craftsmanship. The versatility of natural cheese in both cooking and snacking further enhances its appeal, as it can be used in a wide range of culinary applications. Retailers dedicate significant shelf space to natural cheese varieties, reflecting their importance in store portfolios. The trend toward home cooking and entertaining has also boosted sales of natural cheese boards and assortments. Consumers appreciate the distinct flavors and textures that come from aging and natural fermentation processes.

The processed segment in certain niches due to its convenience and extended shelf life, which appeals to busy consumers and institutional buyers. Processed cheese products are designed for easy melting and consistent performance, making them ideal for quick meals and snacks. According to the USDA Economic Research Service, the demand for convenient food options has risen, benefiting products that require minimal preparation. The processed cheese slices and spreads are popular in households with children due to their mild flavor and ease of use in sandwiches. The long shelf life of processed cheese reduces waste and allows for bulk purchasing, which is attractive to budget-conscious shoppers. Institutional sectors such as schools and hospitals rely on processed cheese for its safety and consistency in large-scale food service operations. The ability of processed cheese to remain stable at room temperature for longer periods than natural cheese adds to its logistical advantages. Manufacturers continue to innovate with packaging solutions that enhance portability and freshness.

By Product Type Insights

The mozzarella segment held a prominent share of the US cheese market in 2025 due to its central role in pizza consumption, which is a staple of the American diet. The foodservice industry, particularly quick-service restaurants, relies heavily on mozzarella for its superior melting qualities and mild flavor. The volume of mozzarella used in commercial pizza production is substantial, ensuring a steady baseline for leadership. The versatility of mozzarella extends beyond pizza to pasta dishes, salads, and sandwiches, broadening its appeal. Low-moisture mozzarella is specifically designed for industrial use by providing consistency and ease of handling for large-scale operators. The popularity of home pizza kits and frozen pizzas also contributes to retail sales of mozzarella. Consumers appreciate the mild taste that complements various toppings without overpowering them. The widespread availability of mozzarella in different forms, including shredded, sliced, and fresh, supports its dominance. The integration of mozzarella into international cuisines, such as Italian and Mediterranean, further enhances its usage.

The feta segment is likely to witness a significant CAGR of 5.4% during the forecast period, with the health-conscious trends and the adoption of the Mediterranean diet. Consumers are increasingly seeking healthier fat sources and flavorful options that align with balanced eating patterns. The Mediterranean diet, which features feta prominently, has gained popularity for its associated health benefits. Feta is perceived as a lighter alternative to heavier cheeses, appealing to those monitoring calorie intake. The tangy flavor of feta allows for smaller portions to deliver significant taste impact, supporting portion control strategies. The rise of salad bars and healthy bowl concepts in restaurants has increased the visibility and usage of feta. Retailers have expanded their feta offerings to include reduced-sodium and organic varieties, catering to specific health needs. The versatility of feta in breakfast, lunch, and dinner dishes enhances its appeal to diverse consumer groups. Social media influence has also popularized feta-based recipes, such as baked feta pasta, driving trial and adoption.

COMPETITION OVERVIEW

The competition in the United States cheese market is intense and characterized by a mix of large multinational corporations and specialized artisanal producers. Major players compete based on brand recognition, product quality, price, and distribution efficiency to secure shelf space and consumer loyalty. The market sees frequent innovation as companies strive to differentiate their offerings through unique flavors, organic certification,s and sustainable packaging. Private label brands pose a significant challenge to national brands by offering lower-priced alternatives that appeal to budget-conscious shoppers. Artisanal cheesemakers contribute to market diversity by catering to niche segments seeking high-quality and authentic products. Consolidation through mergers and acquisitions is common as larger firms seek to expand their portfolios and achieve economies of scale. Regulatory compliance and food safety standards also influence competitive dynamics, requiring continuous investment in quality assurance. The rise of plant-based alternatives adds another layer of competition, forcing traditional dairy companies to diversify their product lines.

KEY MARKET PLAYERS

A few major players of the United States cheese market include

- Kraft Heinz Company

- Dairy Farmers of America

- Saputo Inc

- Arla Foods

- Lactalis Group

- Fonterra Co-operative Group

- Land O'Lakes, Inc

- Tillamook County Creamery Association

- Bel Group

- Sargento Foods Inc

Top Strategies Used by Key Market Participants

Key players in the United States cheese market employ several major strategies to maintain competitiveness and drive growth. Product innovation is central to these efforts, with companies developing new flavors,s textures, and formats to appeal to changing consumer preferences. Expansion into plant-based alternatives allows firms to capture emerging market segments driven by health and ethical concerns. Strategic acquisitions enable larger corporations to consolidate market position and access niche brands with loyal followings. Sustainability initiatives such as reducing carbon footprints and improving animal welfare standards enhance brand reputation and meet regulatory requirements. Digital marketing and e-commerce integration help companies reach direct consumers and gather valuable data on purchasing behavior. Partnerships with foodservice providers ensure steady demand through menu inclusion and promotional activities. These combined strategies allow participants to adapt to market dynamics and sustain long-term profitability in a highly competitive environment.

Leading Players in the Market

- Lactalis Inc stands as a global leader in the dairy industry with a significant footprint in the United States cheese market. The company offers a diverse portfolio of cheese brands ranging from everyday staples to premium artisanal varieties. Lactalis leverages its extensive distribution network to ensure widespread availability across retail and foodservice channels. Recent actions include strategic acquisitions of regional cheese producers to expand its product range and geographic reach. The company invests heavily in sustainable farming practices and supply chain transparency to meet evolving consumer expectations. Lactalis also focuses on innovation by launching new flavor profiles and convenient packaging formats. These initiatives strengthen its market position by enhancing brand loyalty and operational efficiency. The organization continues to prioritize quality and safety standards to maintain consumer trust.

- Arla Foods amba is a major international dairy cooperative with a strong presence in the global cheese market. The company produces a wide array of cheese products, including chedda,r mozzarella, and specialty varieties under well-known brands. Arla emphasizes sustainability and ethical sourcing, which resonates with environmentally conscious consumers. Recent actions involve expanding its plant-based cheese offerings to cater to growing demand for dairy alternatives. The company has also invested in advanced processing technologies to improve product quality and consistency. Arla collaborates with farmers to implement best practices that reduce environmental impact. These efforts enhance its reputation for responsibility and innovation. The cooperative structure allows Arla to maintain close relationships with suppliers, ensuring stable milk supplies.

- Saputo Inc is a leading producer and distributor of cheese products with substantial operations in the United States. The company manufactures a broad spectrum of cheese types, including Italian styles and processed varieties for retail and industrial customers. Saputo focuses on operational excellence and cost efficiency to remain competitive in a dynamic market. Recent actions include the expansion of production facilities to increase capacity and meet rising demand. The company has also introduced innovative packaging solutions that extend shelf life and improve convenience for consumers. Saputo prioritizes customer collaboration to develop customized cheese solutions for foodservice clients. These strategies strengthen its market position by fostering long-term partnerships and enhancing product appeal. The organization invests in research and development to create new flavors and textures.

MARKET SEGMENTATION

This research report on the US cheese market has been segmented and sub-segmented based on Source, Type, Product Type & region.

By Source

- Animal-Based

- Cattle

- Sheep

- Goat

- Camel

- Plant-Based

- Soy

- Almond

- Cashew

- Others

By Type

- Natural

- Processed

By Product Type

- Cheddar

- Mozzarella

- Roquefort

- Stilton

- Parmesan/Parmigiano-Reggiano

- Ricotta

- Munster

- Feta

- Others

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What factors are driving the U.S. cheese market?

Key drivers include rising demand for convenience foods, growth in fast food consumption, and increasing preference for protein-rich diets.

2. Which cheese type dominates the U.S. market?

Mozzarella holds the largest share due to its widespread use in pizza and fast-food products.

3. What are the major cheese types in the U.S. market?

Major types include cheddar, mozzarella, parmesan, cream cheese, feta, and processed cheese.

4. Which distribution channel is most popular?

Supermarkets and hypermarkets dominate due to wide product availability and consumer accessibility.

5. Who are the key players in the U.S. cheese market?

Leading companies include Kraft Heinz Company, Dairy Farmers of America, Saputo Inc., Lactalis Group, and Sargento Foods Inc..

6. What trends are shaping the U.S. cheese market?

Key trends include growing demand for organic cheese, artisanal products, and plant-based cheese alternatives.

7. How is the foodservice industry impacting cheese demand?

The foodservice sector, especially pizza chains and restaurants, significantly boosts cheese consumption.

8. What role does health awareness play in the market?

Consumers are increasingly seeking low-fat, low-sodium, and organic cheese options, influencing product innovation.

9. What challenges does the U.S. cheese market face?

Challenges include fluctuating milk prices, lactose intolerance concerns, and competition from plant-based alternatives.

10. What is the future outlook for the U.S. cheese market?

The market is expected to witness steady growth with innovation in flavors, packaging, and healthier product options.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com