U.S Crackers Market Size, Share, Trends & Growth Forecast Report Segmented By Distribution Channel (Modern Trade, Traditional Trade, E-Commerce), Packing Type, Occasion, Ingredient, And Country (California, Washington, Oregon, New York & Rest of The United States) – Industry Analysis and Forecast, 2026 To 2034

U.S. Crackers Market Report Summary

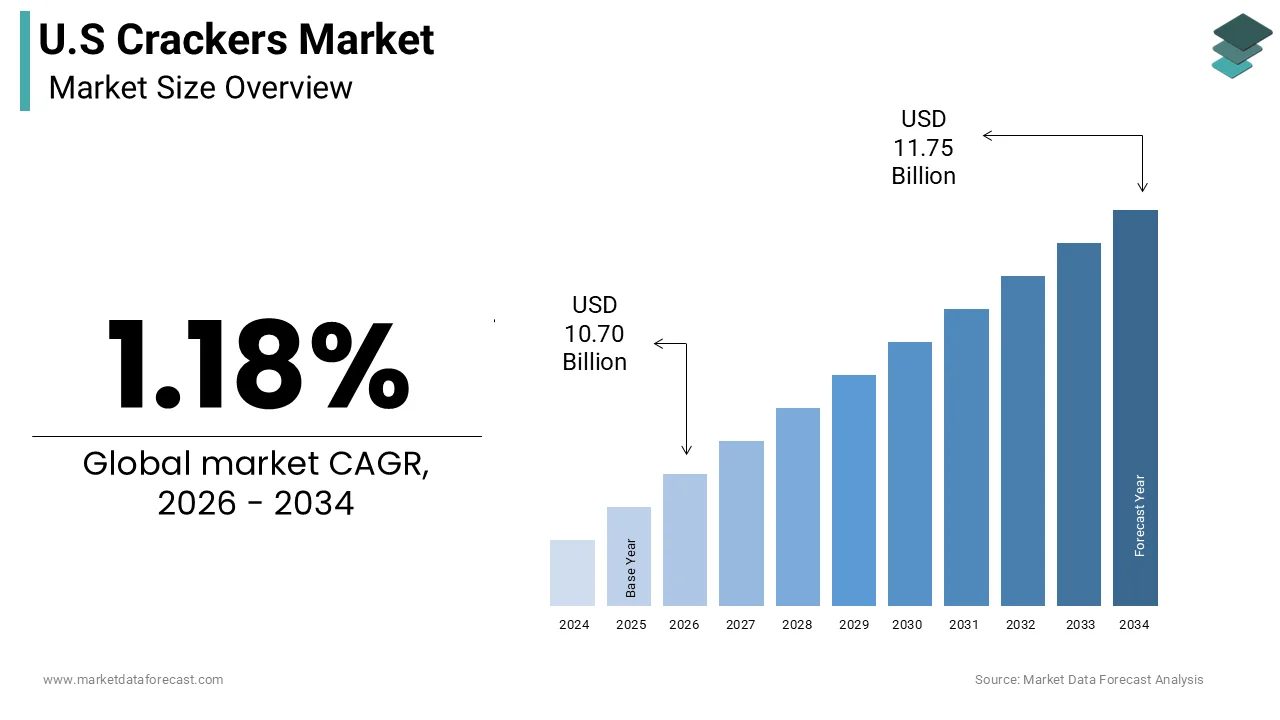

The United States crackers market was valued at USD 10.58 billion in 2025 and is projected to reach USD 11.75 billion by 2034, growing from USD 10.70 billion in 2026 at a CAGR of 1.18% during the forecast period. Market growth is driven by increasing demand for convenient snack foods, rising consumption of on-the-go snacks, and expanding product innovations in flavors and healthier ingredients. The growing popularity of whole-grain, gluten-free, and protein-enriched crackers is further supporting the growth of the U.S. crackers market.

Key Market Trends

- Rising demand for healthy and functional snack products

- Increasing popularity of gluten-free and whole-grain crackers

- Growth in premium and flavored cracker varieties

- Expansion of convenient and portable snack packaging

- Increasing consumer preference for low-calorie and baked snacks

Segmental Insights

- Based on distribution channel, the modern trade segment dominated the U.S. crackers market in 2025 by accounting for 55.5% of the market share, supported by strong supermarket and hypermarket presence

- Based on packaging type, the packets segment held the leading share in 2025 by capturing 34.2% of the market share, driven by convenience and easy portability

- Based on occasion, rthe everyday snacking segment led the market in 2025 by accounting for 45.3% of the market share, supported by rising between-meal consumption habits

- Based on ingredient, the wheat segment dominated the market in 2026 due to widespread availability, affordability, and consumer familiarity with wheat-based crackers

Competitive Landscape

- The U.S. crackers market is highly competitive, with companies focusing on healthier formulations, innovative flavors, and sustainable packaging. Market players are investing in organic ingredients, protein-enriched snacks, and premium product lines to strengthen their market presence.

- Prominent players in the U.S. crackers market include Mondelez International, Kellogg Company, Pepperidge Farm, Campbell Soup Company, General Mills, Nabisco, Lance Inc, Keebler, Snyder's-Lance, and Back to Nature Foods.

U.S Crackers Market Size

The U.S crackers market was valued at USD 10.58 billion in 2025, is estimated to reach USD 10.70 billion in 2026, and is projected to reach USD 11.75 billion by 2034, growing at a CAGR of 1.18% from 2026 to 2034.

The crackers are designed for consumption as standalone snacks or accompaniments to dips and cheeses. The definition extends beyond basic sustenance to include functional foods that cater to health-conscious lifestyles through ingredient transparency and nutritional enhancement. Consumer engagement is driven by the versatility of crackers in meal preparation and snacking routines across all age groups. The per capita consumption of grain-based snacks remains robust, with households maintaining steady inventory levels for daily use. Furthermore, data from the Bureau of Labor Statistics indicates that average annual expenditures on cereals and bakery products per consumer unit reached approximately 500 dollars, demonstrating consistent financial allocation toward these essential food items. The shift toward home entertaining and casual dining has further intensified the demand for premium and specialty cracker options that elevate social gatherings. The savory snacks account for a significant portion of impulse purchases, highlighting their role in immediate consumption scenarios. The integration of clean label practices and sustainable sourcing has become a standard expectation rather than a niche preference.

MARKET DRIVERS

Rising Demand for Healthy and Functional Snacking Options

The increasing consumer focus on health and wellness for the adoption of nutritious cracker varieties, such as whole grain, gluten-free, and high fiber options, is propelling the growth of the United States crackers market. Americans are increasingly seeking snacks that provide sustained energy and essential nutrients rather than empty calories. According to the International Food Information Council, approximately 60% of consumers follow a specific diet or eating pattern that prioritizes health benefits, driving demand for transparent ingredient lists. This behavioral shift encourages manufacturers to reformulate products using ancient grains, legumes, and seeds to enhance nutritional profiles. As per data from the Dietary Guidelines for Americans, recommendations to increase whole grain intake have influenced purchasing decisions, with many shoppers actively seeking crackers that meet these dietary standards. The prevalence of lifestyle diseases such as diabetes and obesity further motivates consumers to choose low glycemic index snacks that support blood sugar management. Brands respond by highlighting protein content and reduced sodium levels on packaging to appeal to health-conscious buyers. The rise of plant-based diets also boosts demand for vegan-friendly crackers made without animal-derived ingredients. Educational campaigns by nutritionists and healthcare providers reinforce the importance of mindful snacking in overall wellness.

Versatility and Convenience in Modern Lifestyles

The inherent versatility and convenience of crackers make them an ideal choice for busy consumers seeking quick and easy meal solutions, which is also escalating the growth of the United States crackers market. Crackers serve as a foundational element for charcuterie boards, lunchbox staples, and on-the-go snacks requiring minimal preparation time. According to the Bureau of Labor Statistics, the average American spends less than 40 minutes per day on food preparation and cleanup, increasing the reliance on ready-to-eat items. This time constraint drives demand for portable snack options that can be consumed at work, school, or during travel. The single-serve packs and resealable containers have gained popularity among commuters and students, who prioritize convenience. The ability of crackers to pair with a wide range of toppings, such as chees,e hummus, and avocado, enhances their utility in diverse culinary contexts. The trend toward casual entertaining at home has also boosted sales of premium crackers used as bases for appetizers and dips. Social media platforms showcase creative serving ideas, inspiring consumers to experiment with different combinations. Manufacturers leverage this by offering variety packs that cater to multiple taste preferences. The long shelf life of crackers reduces food waste and allows for bulk purchasing, which appeals to budget-conscious households.

MARKET RESTRAINTS

Health Concerns Regarding High Sodium and Processed Ingredients

The products high in sodium, refined flour, and artificial additives, which deter health-conscious consumers, are degrading the growth of the United States crackers market. Excessive sodium intake is linked to hypertension and cardiovascular diseases, leading to increased scrutiny of processed snack foods. According to the Centers for Disease Control and Prevention, more than 90% of Americans consume too much sodium primarily from packaged and prepared food,s including crackers. This public health concern has prompted regulatory bodies and consumer advocacy groups to call for stricter labeling and reformulation mandates. The proposed voluntary sodium reduction targets aim to lower sodium levels in commercially available products by 12% over two years. Consumers are increasingly reading nutrition labels and avoiding brands that do not meet clean label standards. The presence of preservatives and artificial flavors further erodes trust in conventional cracker brands. Negative media coverage regarding the health impacts of ultra-processed foods exacerbates consumer hesitation. Parents are particularly cautious about offering such snacks to children due to rising childhood obesity rates. This health consciousness forces manufacturers to invest in costly reformulation efforts, which can alter taste and texture.

Volatility in Raw Material Costs and Supply Chain Disruptions

The cracker manufacturing industry faces significant challenges due to fluctuations in the prices of key raw materials, such as wheat, corn oil, and packaging materials is hindering the growth of the United States crackers market. These input costs constitute a major portion of production expense,s making profitability vulnerable to market volatility. The global weather patterns and geopolitical tensions have led to unpredictable harvests, causing spikes in grain prices. Rising energy costs further inflate manufacturing expenses, as baking processes are energy-intensive. The producer price index for flour and other bakery ingredients has experienced substantial swings, creating uncertainty for long-term planning. Supply chain disruptions caused by labor shortages and logistical hurdles delay the delivery of raw materials and finished goods. The dependence on imported ingredients for specialty crackers exposes manufacturers to trade policy risks and tariff implications. Inventory management becomes challenging as businesses attempt to balance stock levels against uncertain supply conditions. Smaller producers with limited bargaining power are particularly affected by raw material scarcity. The inability to pass increased costs onto price-sensitive consumers squeezes profit margins. Retailers may reduce shelf space for higher-priced items, favoring private label alternatives. This economic instability constrains the ability of companies to maintain consistent pricing and product availability.

MARKET OPPORTUNITIES

Expansion of Plant-Based and Alternative Grain Products

The growing consumer interest in plant-based diets and alternative grains to innovate with non-traditional ingredients is ascribed to bolster the growth of the United States crackers market. Shoppers are increasingly seeking products made from chickpeas, lentils, quinoa, and almond flour, which offer superior nutritional profiles and allergen-friendly attributes. The sales of plant-based snacks have grown significantly, outpacing conventional categories as consumers prioritize sustainability and health. This shift creates a niche for companies that utilize diverse protein sources to create high fiber and high protein crackers. The innovations in gluten-free and grain-free formulations are driving growth among consumers with celiac disease or gluten sensitivity. Brands can leverage these trends by obtaining certifications such as Non-GMO Project Verified or Certified Gluten Free to build trust. Marketing campaigns that highlight the environmental benefits of plant-based agriculture resonate strongly with younger demographics. Partnerships with health influencers amplify brand credibility and reach. The introduction of savory flavors such as rosemary, sea salt, and ginger appeals to adventurous palates. Direct-to-consumer channels allow for targeted marketing of specialized lines to niche audiences.

Premiumization Through Artisanal and Gourmet Offerings

The trend toward premiumization offers substantial opportunities for manufacturers to introduce artisanal and gourmet cracker lines that emphasize quality craftsmanship and unique flavor profiles, which is another attribute to elevate the growth of the United States crackers market. Consumers are willing to pay a premium for small-batch handmade crackers that feature exotic ingredients and sophisticated tastes. The specialty food industry continues to grow, with savory biscuits and crackers being a key category driven by the desire for elevated snacking experiences. Advanced baking techniques such as stone milling and slow fermentation enable the creation of complex textures and flavors. The sales of premium crackers in independent grocery stores and specialty markets have increased as shoppers seek authentic and locally sourced products. The rise of home entertaining and wine pairing culture further fuels demand for high-end crackers that complement cheeses and charcuterie. Brands can differentiate through elegant packaging designs and storytelling that highlight heritage and artisanal methods. Collaborations with local chefs and food artisans enhance brand prestige and appeal. Subscription boxes and gift sets provide new revenue streams and enhance customer loyalty. The integration of organic and sustainably sourced ingredients aligns with ethical consumption values.

MARKET CHALLENGES

Intense Competition from Private Label Brands

The intense competition between established national brands and retailer private labels, which exerts downward pressure on prices and margins, is likely to challenge the expansion of the United States crackers market. Private label products have significantly improved in quality while maintaining a lower price point,s attracting budget-conscious consumers. This trend is exacerbated during economic downturns when shoppers actively seek cost-saving alternatives. National brands struggle to justify premium pricing without distinct functional or emotional differentiators. The retailer loyalty programs often promote private-label crackers through aggressive discounts and bundle deals. The commoditized nature of basic crackers makes it difficult for brands to sustain long-term loyalty based solely on taste. Retailers wield significant power in shelf placement and promotional support, favoring their own higher-margin brands. This dynamic forces national manufacturers to engage in frequent promotion,s eroding profitability. The ease of switching between brands means that consumers readily adopt cheaper options when available. Innovation cycles are rapid but easily replicated by competitors, limiting first-mover advantages. The saturation of the market leaves little room for volume growth without stealing share from rivals. Maintaining brand equity in a price-sensitive environment requires substantial marketing investment.

Regulatory Pressures on Labeling and Health Claims

The increasing regulatory scrutiny regarding nutritional labeling and health claims, which complicates marketing strategies and product development, is also expected to impede the growth of the United States Crackers market. Consumers and advocacy groups are demanding greater transparency regarding ingredient sourcing and nutritional content, leading to stricter compliance requirements. The updated nutrition labeling regulations require detailed disclosure of added sugars and sodium levels, impacting package design and formulation. As per data from the Center for Science in the Public Interest, misleading health claims, such as natural or wholesome, are subject to legal challenges if not substantiated by scientific evidence. Manufacturers must invest in rigorous testing and legal review to ensure compliance with federal and state guidelines. The complexity of navigating varying international standards adds operational burdens for global brands. The presence of allergens such as wheat, soy, and dairy requires clear warning labels to prevent liability issues. Failure to comply can result in recalls, fines, and reputational damage. The demand for clean-label products necessitates the removal of artificial additives, which can affect shelf life and texture. Educating consumers about regulatory changes is challenging amidst widespread misinformation. The need for third-party certifications adds another layer of complexity and expense.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 1.18% |

| Segments Covered | By Distribution Channel, Packing Type, Occasion, Ingredient, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Mondelez International, Kellogg Company, Pepperidge Farm, Campbell Soup Company, General Mills, Nabisco, Lance Inc., Kellogg's Keebler, Snyder's-Lance, Back to Nature Foods |

SEGMENTAL ANALYSIS

By Distribution Channel Insights

The modern trade segment accounted in holding 55.5% of the United States crackers market share in 2025, with its extensive reach, one-stop shopping convenience, and ability to offer competitive pricing through economies of scale. Consumers prefer these outlets for their wide variety of brands, private label options, and frequent promotional activities, which drive volume sales. According to the Food Marketing Institute, approximately 60% of grocery purchases in the United States occur in supermarkets and supercenters, reflecting the dominance of this channel for staple food items. The primary driver is the habit of weekly or biweekly bulk shopping, where households stock up on non-perishable goods like crackers. The modern trade retailers account for the majority of packaged food sales due to their strategic shelf placement and loyalty programs that incentivize repeat purchases. The presence of dedicated snack aisles and end cap displays enhances product visibility and encourages impulse buying. Retailers leverage their bargaining power to secure favorable terms from manufacturers, allowing them to pass savings to consumers. The integration of digital coupons and personalized offers through store apps further drives foot traffic and sales. The reliability of supply and consistent inventory levels build consumer trust. Additionally, the availability of diverse formats from family packs to single-serve units caters to varying household needs.

The e-commerce segment is expected to witness the fastest CAGR of 9.5% from 2026 to 2034, owing to the increasing adoption of online grocery shopping and the convenience of home delivery for heavy or bulky items. The shift in consumer behavior toward digital platforms for routine replenishment of pantry staples is also to enhance the growth of the segment. According to the United States Census Bureau, e-commerce sales for food and beverage products have grown significantly as logistics networks improve and delivery times shorten. As per data from Brick Meets Click, online grocery sales have stabilized at higher levels post-pandemic, indicating a permanent shift in shopping habits. Subscription services offered by major retailers and direct-to-consumer brands ensure automatic replenishment, reducing the effort required for regular purchases. The ability to compare prices, read reviews, and access niche or specialty brands not available in local stores appeals to discerning shoppers. Digital marketing and targeted ads drive the discovery of new products among younger demographics. The rise of quick commerce platforms offering rapid delivery further enhances the appeal of online purchasing for immediate needs. Packaging innovations that ensure product integrity during shipping have reduced damage rates and increased consumer confidence.

By Packaging Type Insights

The packets segment was the largest by occupying 34.2% of the United States crackers market share in 2025, with its cost-effectiveness, lightweight nature, and ability to preserve product freshness. Flexible packaging is the standard for most mass-market crackers due to its efficiency in manufacturing, storage, and transportation. The flexible packaging accounts for a significant share of the total packaging market due to its material efficiency and lower carbon footprint compared to rigid alternatives. The economic advantage for both manufacturers and consumers, as packets require less material and reduce shipping costs, is fuelling the growth of the segment. The flexible packaging generates less waste by weight than rigid containers, appealing to environmentally conscious stakeholders. Resealable zippers in modern packet designs enhance convenience by maintaining crispness after opening, which is a key consumer requirement. The versatility of packets allows for various sizes from single-serve snacks to family-sized bags catering to diverse consumption occasions. High-quality printing capabilities enable vibrant branding and clear nutritional labeling, which influences purchasing decisions at the point of sale. The durability of multi-layer films protects crackers from moisture and breakage during distribution. Retailers favor packets for their stackability and efficient use of shelf space.

The tins segment is likely to grow with the fastest CAGR of 7.8% from 2026 to 2034, with the premiumization trend and the demand for reusable and eco-friendly packaging solutions. Metal tins are increasingly used for gourmet artisanal and holiday-specific crackers due to their superior protection and aesthetic appeal. According to the Steel Recycling Institute, steel packaging is infinitely recyclable, making it an attractive option for brands aiming to enhance their sustainability credentials. The consumers are willing to pay a premium for products with reusable packaging that can be repurposed for storage or decoration. Tins provide excellent barrier properties against light moisture and oxygen, ensuring longer shelf life and preserved flavor quality. The tactile experience of opening a tin adds to the sensory appeal of the product, enhancing brand loyalty. Brands leverage tins to differentiate themselves in a crowded market by offering limited edition designs and collaborations. The durability of tins reduces product breakage during transit, which is a common issue with fragile crackers. Retailers display tins prominently during festive seasons, driving seasonal spikes in sales.

By Occasion Insights

The everyday snacking segment accounted in holding 45.3% of the United States crackers market share in 2025, with the habitual consumption of crackers as convenient and satisfying snacks between meals. Crackers are a staple in lunchboxes, office desks, and home pantries due to their versatility and ease of consumption. The savory snacks account for a significant portion of daily impulse purchases, reflecting their role in routine eating habits. The busy lifestyle of Americans, who seek quick and portable food options that require no preparation. Snacking has become a major part of daily caloric intake, with many consumers replacing traditional meals with snack combinations. Crackers paired with cheese dips or spreads offer a balanced mini meal that satisfies hunger and cravings. The availability of single-serve packs facilitates on-the-go consumption for students, workers, and travelers. Health-conscious consumers opt for whole-grain or high-fiber crackers as a nutritious alternative to chips and cookies. The affordability of crackers makes them an accessible option for families managing budgets. Marketing campaigns emphasize the convenience and satisfaction of snacking, reinforcing this behavior.

The party celebrations segment is expected to grow at the fastest CAGR of 6.5% during the forecast period, with the resurgence of social gatherings and the popularity of charcuterie boards and appetizers. According to the National Retail Federation, spending on party supplies and food for gatherings has increased as consumers host more dinners and events. As per data from Statista, the interest in gourmet snacking and entertaining has surged, with social media platforms showcasing elaborate cracker-based spreads. Premium and artisanal crackers are preferred for these occasions due to their sophisticated flavors and elegant presentation. The rise of wine and cheese pairing culture has further boosted demand for specialized crackers that complement specific beverages. Brands respond by launching party packs and variety boxes that cater to diverse tastes. The visual appeal of crackers on platters drives purchases for aesthetic reasons. Seasonal holidays such as Thanksgiving and Christmas see significant spikes in sales as hosts prepare for guests. The social aspect of sharing food enhances the perceived value of premium crackers.

By Ingredient Insights

The wheat segment held a dominant share of the United States crackers market in 2026, with the widespread availability of wheat flour, its established taste profile, and its role as the base for traditional cracker varieties such as saltines and butter crackers. Wheat is the most commonly used grain in baking due to its gluten content, which provides structure and texture. The wheat production remains robust, ensuring a steady and affordable supply for manufacturers. The consumer familiarity and preference for the classic taste and crunch of wheat-based crackers. The enriched wheat products are a staple in many households, providing essential nutrients, such as iron and B vitamins. The versatility of wheat flour allows for various formulations from whole wheat to refined white flour, catering to different dietary preferences. Major brands rely on wheat for their core product line,s which enjoys strong brand loyalty and recognition. The cost-effectiveness of wheat compared to alternative grains makes it an economical choice for mass production. Retailers allocate significant shelf space to wheat crackers due to their high turnover rates. The integration of wheat crackers into everyday meals and snacks reinforces their dominance.

The gluten-free segment is expected to register a CAGR of 8.6% from 2026 to 2034, with the increasing prevalence of celiac disease, gluten sensitivity, and the adoption of gluten-free diets for health reasons. According to the Celiac Disease Foundation, approximately 3 million Americans have celiac disease, while many others follow a gluten-free lifestyle by choice. As per data from Mintel, the demand for gluten-free products has expanded beyond medical necessity to include general wellness trends. Manufacturers invest in advanced formulations to improve the texture and taste of gluten-free crackers, addressing previous consumer complaints about dryness or crumbliness. Certifications such as Certified Gluten Free build trust and encourage trial among skeptical buyers. The expansion of distribution channels, including mainstream supermarkets and online platforms, has improved accessibility.

COMPETITION OVERVIEW

The competitive landscape of the United States crackers market is characterized by intense rivalry among established multinational corporations and aggressive private-label brands. Large players leverage strong brand equity and extensive distribution networks to maintain dominance while competing on price and innovation. The market is mature with steady demand driven by habitual snacking behaviors rather than discretionary spending. Price competition is fierce as retailers promote their own brands to capture margin-sensitive consumers. Private label products have improved in quality, challenging national brands on value propositions. Innovation focuses on health attributes such as whole grains and gluten-free options to differentiate offerings. Supply chain efficiency is critical for maintaining profitability amidst fluctuating raw material costs. Regulatory pressures regarding labeling and sustainability drive investments in compliant practices. Consumer loyalty is fragile, with shoppers readily switching brands for better deals or healthier options. Companies must balance cost management with product quality to sustain market position. This dynamic environment requires continuous adaptation to changing consumer preferences and retail dynamics. Success depends on operational excellence and strategic branding in a highly consolidated industry.

KEY MARKET PLAYERS

A few major players of the U.S crackers market include

- Mondelez International

- Kellogg Company

- Pepperidge Farm

- Campbell Soup Company

- General Mills

- Nabisco

- Lance Inc

- Kellogg's Keebler

- Snyder's-Lance

- Back to Nature Foods

Leading Players in the United States Crackers Market

- Mondelez International Inc is a dominant force in the United States crackers market with iconic brands such as Ritz, Triscuit, and Club. The company contributes significantly by driving innovation in flavor profiles and sustainable sourcing practices. Recent actions include expanding its portfolio of whole grain and gluten-free options to meet evolving consumer health preferences. Mondelez has invested heavily in digital marketing campaigns that highlight the versatility of crackers for snacking and entertaining. The firm focuses on supply chain efficiency to ensure consistent product availability across retail channels. Its commitment to responsible cocoa and wheat sourcing enhances its reputation. These strategies solidify its position as a leader in the savory snack sector.

- Kellogg Company, now operating as Kellanov, holds a strong position in the US crackers market through popular brands like Cheez-It, Town House, and Keebler. The company drives growth by leveraging its extensive distribution network and robust manufacturing capabilities. Recent strategies involve launching new flavors and limited edition varieties to attract younger demographics and stimulate trial. Kellanova has focused on sustainability initiatives, including reducing plastic usage in packaging and sourcing ingredients responsibly. The firm enhances its direct-to-consumer presence through e-commerce partnerships and subscription services. Investments in data analytics help optimize inventory management and predict trending flavors.

- Pepperidge Farm Incorporated, a subsidiary of Campbell Soup Company, is a key player known for premium crackers such as Goldfish, Milan,o and Distinctive. The company contributes to the market by offering high-quality artisanal products that appeal to discerning consumers. Recent actions include expanding its organic and non-GMO product lines to align with clean label trends. Pepperidge Farm has revitalized its marketing efforts by emphasizing the heritage and craftsmanship behind its brands. The firm invests in community engagement and charitable initiatives to build brand goodwill. Its focus on premium positioning allows it to command higher price points and maintain margins.

Top Strategies Used by Key Market Participants

Key players in the United States crackers market employ diverse strategies to maintain a competitive advantage and drive growth. Product innovation remains central with companies developing healthier formulations and unique flavors. Brands focus on sustainability by adopting eco-friendly packaging and responsible sourcing practices. Strategic marketing campaigns emphasize versatility and snacking occasions to boost consumption. Companies leverage digital platforms to engage directly with consumers and gather insights. Omnichannel distribution ensures widespread availability in both physical and online stores. Partnerships with retailers facilitate prominent shelf placement and promotional support. Limited edition releases create excitement and drive trial among new customers. These strategies collectively help brands differentiate themselves and capture value in a mature market.

MARKET SEGMENTATION

This research report on the US crackers market has been segmented and sub-segmented based on distribution channel, packing type, occasion, ingredient & region.

By Distribution Channel

- Modern Trade

- Traditional Trade

- E-commerce

By Packing Type

- Packets

- Boxes

- Tins

By Occasion

- Everyday Snacking

- Party Celebrations

- Gifting

By Ingredient

- Wheat

- Rice

- Corn

- Multigrain

- Gluten-Free

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What is driving the growth of the United States crackers market?

The market is growing due to rising snack consumption, demand for convenient foods, and increasing preference for healthy cracker options.

2. Which types of crackers are most popular in the United States?

Saltine crackers, cheese crackers, sandwich crackers, whole-grain crackers, and flavored crackers are among the most popular varieties.

3. Who are the major players in the United States crackers market?

Major companies include Mondelez International, Kellogg Company, and Campbell Soup Company.

4. Which distribution channels are important for cracker sales in the U.S.?

Supermarkets, hypermarkets, convenience stores, online retail platforms, and specialty stores are major distribution channels.

5. What role does product innovation play in the crackers market?

Manufacturers are launching new flavors, healthier ingredients, and premium varieties to attract more consumers.

6. What challenges are faced by the U.S. crackers market?

Challenges include fluctuating raw material prices, increasing competition, and changing consumer preferences toward fresh snacks.

7. Which age group consumes crackers the most?

Children, working professionals, and young adults are among the largest consumer groups due to convenience and portability.

8. What ingredients are commonly used in crackers?

Common ingredients include wheat flour, cheese, seeds, herbs, whole grains, and seasonings.

9. Which region in the United States has high demand for crackers?

Urban regions with busy lifestyles and high snack consumption patterns show strong demand for crackers.

10. What is the future outlook for the United States crackers market?

The market is expected to witness steady growth due to innovation, healthier snack trends, and increasing convenience food demand.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com