U.S. Denim Jeans Market Size, Share, Trends & Growth Forecast Report By End Use (Men, Women, Children), Distribution Channel, and Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

$22.35 BnMarket Estimate, 2026

$23.57 BnMarket Forecast, 2034

$36.09 BnCAGR, 2026–2034

5.47%U.S. Denim Jeans Market Report Summary

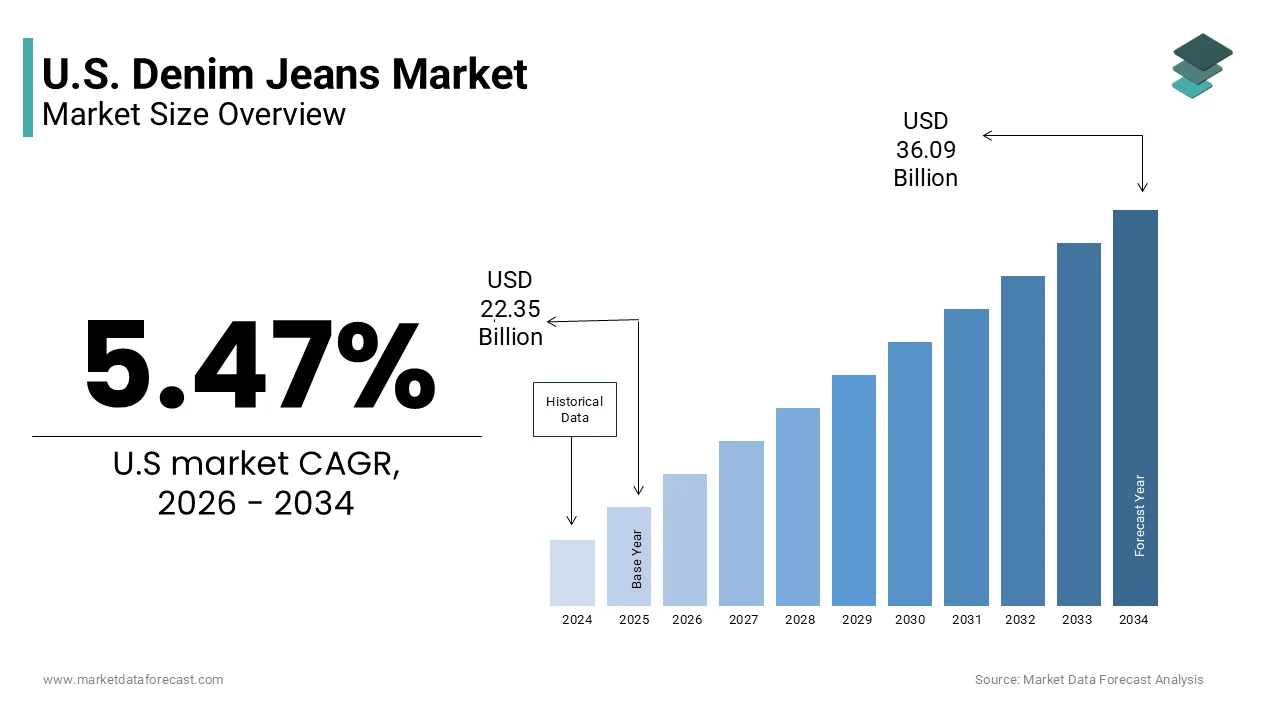

The U.S. denim jeans market was valued at USD 22.35 billion in 2025, is estimated to reach USD 23.57 billion in 2026, and is projected to reach USD 36.09 billion by 2034, growing at a CAGR of 5.47% during the forecast period. Market growth is driven by increasing consumer demand for casual apparel, evolving fashion trends, and continuous innovation in denim fabrics and designs. The popularity of versatile and comfortable clothing, combined with growing interest in sustainable and premium denim products, continues to support market expansion. Advancements in fabric technology, eco friendly manufacturing practices, and direct to consumer retail strategies are further strengthening the U.S. denim jeans industry.

Key Market Trends

- Growing demand for casual and lifestyle apparel is driving market growth.

- Increasing popularity of sustainable and environmentally responsible denim production is boosting market expansion.

- Rising consumer preference for premium, stretch, and performance denim products is supporting industry development.

- Expansion of omnichannel retail and direct to consumer sales models is enhancing market accessibility.

- Innovation in fabric technologies, fit customization, and eco friendly dyeing processes is influencing market advancement.

Segmental Insights

- Based on end use, the women segment accounted for the largest share of the U.S. denim jeans market in 2025. This dominance is attributed to broader product variety, higher fashion adoption rates, and frequent purchasing patterns.

- Based on distribution channel, the offline segment maintained the leading position in the U.S. denim jeans market in 2025. Physical retail stores continue to play a significant role as consumers prefer to assess fit, comfort, and fabric quality before making purchasing decisions.

Regional Insights

- The United States remained a major contributor to the denim jeans market in 2025 and is expected to maintain strong sales performance during the forecast period. A large consumer base, established apparel retail infrastructure, and continuous product innovation continue to support market growth.

Competitive Landscape

The U.S. denim jeans market is highly competitive, with companies focusing on sustainable production, fashion innovation, premium product offerings, and digital retail expansion to strengthen their market position. Manufacturers and brands continue investing in advanced fabric technologies, customization options, and environmentally responsible manufacturing practices.

Key companies operating in the U.S. denim jeans market include Bestseller, Pepe Jeans, United States Polo Association, PVH Corp., Kering SA, Hennes & Mauritz AB (H&M), Gap Inc., VF Corp., and Levi Strauss & Co. Class A.

U.S. Denim Jeans Market Size

The U.S. denim jeans market size was valued at USD 22.35 billion in 2025, and is projected to reach USD 36.09 billion by 2034 from USD 23.57 billion in 2026, growing at a CAGR of 5.47%.

The U.S. denim jeans market is a foundational segment of the global apparel industry characterized by the production and retail of trousers made from durable cotton twill fabric. According to the U.S. Census Bureau, the total population exceeds 349 million individuals and this provides a vast consumer base with diverse sizing and stylistic preferences. Furthermore, the prevalence of remote and hybrid work models has influenced dressing codes, leading to a sustained preference for comfortable yet presentable clothing options. As per the Bureau of Labor Statistics, Americans spend an average of 1,607 dollars annually on apparel and services, indicating consistent discretionary spending power despite economic fluctuations. The rise of e commerce has transformed distribution channels, allowing brands to reach niche demographics with specialized fits, such as athletic tapered or high waisted styles. Social media platforms amplify trends rapidly, influencing purchase decisions among younger generations who prioritize brand authenticity and environmental responsibility. The integration of stretch fabrics and moisture wicking technologies has further expanded the utility of denim beyond traditional uses. This convergence of cultural significance, technological innovation, and shifting lifestyle patterns ensures that the denim jeans market remains a dynamic and resilient component of the U.S. retail landscape.

MARKET DRIVERS

Enduring Cultural Significance and Versatility in Fashion

The enduring cultural significance and inherent versatility of denim jeans serve as a primary driver for sustained demand in the U.S. market. Denim has evolved from work wear to a universal fashion staple accepted in diverse settings ranging from casual outings to creative professional environments. According to Levi Strauss and Co historical archives, denim has been integral to American identity for over 150 years, creating deep emotional connections and brand loyalty among consumers. The adaptability of jeans allows them to be dressed up with blazers or down with t shirts, appealing to a broad demographic spectrum. As per NPD Group, data indicates that denim accounts for a significant portion of total pants sales in the U.S., reflecting its dominance in the lower body apparel category. Consumers value the durability and longevity of denim, which offers cost per wear advantages over faster fashion alternatives. The availability of various washes, cuts, and finishes enables personal expression while maintaining a classic aesthetic. Retailers continuously refresh collections with seasonal trends, such as wide leg or cropped styles, keeping the category engaging for repeat buyers. The unisex appeal of denim further expands the market potential, allowing brands to market similar styles across gender lines. This combination of historical resonance, functional utility, and stylistic flexibility ensures that denim jeans remain a cornerstone of American apparel consumption.

Innovation in Fabric Technology and Comfort Enhancements

Innovation in fabric technology and comfort enhancements drives demand by addressing consumer desires for performance and ease of movement in daily wear, which is further fuelling the expansion of the U.S. denim jeans market. Modern denim increasingly incorporates elastane, spandex, and other synthetic fibers to provide stretch and recovery properties that traditional rigid cotton lacks. According to Textile World, the adoption of advanced weaving techniques and fiber blends has revolutionized the hand feel and functionality of denim, making it suitable for active lifestyles. Consumers, particularly those in younger demographics, prioritize comfort without sacrificing style, leading to the popularity of jeggings and soft denim variants. As per the Cotton Incorporated Lifestyle Monitor Survey, a majority of U.S. consumers prefer jeans with some degree of stretch for everyday wear, citing comfort as the primary factor in purchase decisions. Brands invest in research and development to create fabrics that resist bagging out, maintain shape after washing, and offer moisture management capabilities. These technological advancements appeal to commuters, travelers, and individuals with sedentary jobs who require all day comfort. The introduction of sustainable stretch fibers derived from recycled materials also aligns with eco conscious values. Marketing campaigns highlight these technical benefits, educating consumers on the superior performance of modern denim. The ability to offer tailored fits that accommodate diverse body shapes through flexible fabrics enhances inclusivity and satisfaction. This focus on material science transforms denim from a static commodity into a dynamic performance apparel category, driving repeat purchases and brand switching.

MARKET RESTRAINTS

Shift towards Casualization and Alternative Bottom Wear

The ongoing shift towards casualization and the rising popularity of alternative bottom wear are significant restraints limiting the growth potential of the traditional denim jeans market in the U.S. Consumers are increasingly opting for leggings, sweatpants, and joggers, which offer superior comfort and ease of care compared to denim. According to the NPD Group, sales of athletic pants and leggings have grown substantially, outpacing denim in certain demographic segments, particularly among women and younger consumers. This trend is reinforced by the normalization of athleisure in social and professional contexts, reducing the occasions where jeans are considered necessary. The perception of denim as restrictive or requiring special care, such as avoiding frequent washing, deters some buyers who prioritize convenience. Additionally, the rise of remote work has diminished the need for structured office attire, including dark wash or tailored jeans. Retailers face challenges in convincing consumers to return to denim when softer alternatives dominate their wardrobes. The saturation of the market with high quality, durable jeans also means that replacement cycles are longer, reducing frequency of purchase. Brands must compete not only with each other but with entirely different categories of apparel that better align with contemporary lifestyle preferences. This substitution effect constrains volume growth and forces denim manufacturers to innovate aggressively to retain relevance.

Environmental Concerns and Water Usage in Production

Environmental concerns regarding the resource intensive nature of denim production, particularly water usage and chemical discharge is further hindering the denim jeans market expansion in the U.S. Traditional denim manufacturing involves significant water consumption for cotton cultivation, dyeing, and finishing processes, raising sustainability issues. According to the United Nations Environment Programme, the fashion industry is responsible for approximately 20% of global industrial wastewater, with denim production being a major contributor due to indigo dyeing and stone washing techniques. Consumers are increasingly aware of these impacts, leading to hesitation in purchasing new denim items frequently. As per McKinsey and Company, surveys indicate that a growing percentage of shoppers consider environmental footprint when making apparel purchases, often favoring brands with transparent and sustainable practices. The complexity of verifying sustainability claims creates skepticism and distrust among buyers who fear greenwashing. Regulatory pressures in various states regarding chemical disposal and water management increase compliance costs for manufacturers. These costs are often passed on to consumers, resulting in higher retail prices that may deter price sensitive buyers. The push for circularity and recycling is still in early stages, with limited infrastructure for large scale denim recovery. Until sustainable production methods become mainstream and affordable, the environmental baggage of denim will continue to pose a reputational and operational challenge. This restraint forces brands to invest heavily in certification and innovation, diverting resources from marketing and expansion.

MARKET OPPORTUNITIES

Expansion of Sustainable and Circular Denim Initiatives

The expansion of sustainable and circular denim initiatives presents a significant opportunity for brands to differentiate themselves and capture the growing segment of environmentally conscious consumers. Innovations such as waterless dyeing technologies, laser finishing, and recycled cotton blends allow manufacturers to reduce environmental impact while maintaining product quality. According to the Ellen MacArthur Foundation, the concept of circular fashion emphasizes keeping products and materials in use, which resonates strongly with modern consumers seeking responsible brands. Companies that implement take back programs and repair services build long term customer relationships and enhance brand loyalty. As per Business of Fashion, reports highlight that transparency in supply chains and verified sustainability credentials are becoming key drivers of purchase decisions in the apparel sector. Brands can leverage these initiatives to command premium prices and attract investors focused on environmental, social, and governance criteria. Collaborations with technology firms to develop bio based dyes and biodegradable fibers offer competitive advantages. Marketing campaigns that educate consumers on the benefits of sustainable denim foster engagement and advocacy. Retailers can create dedicated sections for eco-friendly products, simplifying the shopping experience for conscious buyers. The regulatory landscape is also shifting towards stricter environmental standards, rewarding early adopters of clean production methods. By positioning sustainability as a core value rather than a niche feature, brands can unlock new growth avenues and mitigate reputational risks. This transition aligns with global trends and ensures long term viability in a resource constrained world.

Growth of E-Commerce and Personalized Digital Shopping Experiences

The growth of e-commerce and personalized digital shopping experiences offers a lucrative opportunity for the U.S. denim jeans market. Online platforms enable retailers to showcase extensive ranges of fits, washes, and sizes that may not be available in physical stores. According to the U.S. Census Bureau, e commerce sales continue to rise, with apparel being one of the largest categories driving online revenue. Advanced technologies, such as virtual try on, augmented reality, and AI driven size recommendation tools, address the common challenge of fit uncertainty in online denim shopping. As per Harvard Business Review, personalized recommendations significantly increase customer satisfaction and reduce return rates, which are historically high in the apparel sector. Brands can utilize customer data to offer customized fits and styles, creating a unique value proposition. Direct to consumer models allow for higher margins and direct feedback loops for product improvement. Social commerce integration enables seamless purchasing from social media platforms, where denim trends are often discovered. Subscription services for denim rentals or regular replacements provide recurring revenue streams. Mobile optimized experiences ensure accessibility for on the go shoppers. By investing in digital infrastructure and user experience, brands can overcome geographical limitations and engage customers more effectively. This digital transformation opens new channels for growth and allows for agile responses to changing consumer preferences.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Volatility

Supply chain disruptions and volatility in raw material prices pose significant challenges to the expansion of the U.S. denim jeans market. The production of denim relies heavily on cotton prices, which are subject to fluctuations due to weather conditions, geopolitical tensions, and trade policies. According to the U.S. Department of Agriculture, cotton prices have experienced significant variability, impacting manufacturing costs and profit margins for denim producers. Disruptions in logistics, such as port congestion and shipping delays, affect the timely delivery of finished goods, leading to inventory imbalances. As per the National Retail Federation, supply chain inconsistencies continue to challenge retailers in maintaining optimal stock levels and meeting consumer demand. Labor shortages in manufacturing hubs further exacerbate production delays, increasing lead times and costs. The reliance on global supply chains makes the industry vulnerable to external shocks, such as pandemics or political instability. Manufacturers must navigate complex tariffs and trade agreements, which add layers of administrative burden and expense. The push for near shoring or re-shoring requires significant capital investment and time to establish new facilities. These operational challenges hinder the ability of brands to respond quickly to trends and maintain competitive pricing. Consumers may face higher prices or limited availability during periods of disruption, affecting brand loyalty. Mitigating these risks requires diversification of suppliers and investment in resilient logistics networks, which are costly and complex to implement.

Intense Competition and Market Saturation

Intense competition and market saturation are further challenging the growth in the U.S. denim jeans market as numerous brands vie for consumer attention in a mature sector. The market is crowded with established legacy brands, fast fashion retailers, and emerging direct to consumer labels offering similar products at varying price points. For instance, the apparel manufacturing industry in the U.S. is highly fragmented, with low barriers to entry for new players, leading to fierce price competition. Differentiation becomes difficult as many brands offer comparable fits and washes, forcing companies to compete primarily on price or marketing spend. Fast fashion retailers can replicate trendy styles quickly and cheaply, putting pressure on traditional denim brands to accelerate their design cycles. This rapid turnover contributes to waste and undermines sustainability efforts. Legacy brands struggle to maintain relevance among younger demographics who prioritize novelty and ethical considerations. The saturation of physical retail space limits expansion opportunities for new entrants. Digital advertising costs are rising, making customer acquisition more expensive. Brands must continuously innovate in design, technology, and sustainability to stand out, but these investments strain resources. The constant pressure to discount erodes margins and devalues the product. Navigating this competitive landscape requires strategic agility and strong brand identity, which are difficult to sustain in a saturated market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.47% |

| Segments Covered | By End Use, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Bestseller, Pepe Jeans, United States Polo Association, PVH Corp., Kering SA, Hennes & Mauritz AB (H&M), Gap Inc., VF Corp., and Levi Strauss & Co. Class A. |

SEGMENTAL ANALYSIS

By End Use Insights

The women segment dominated the market by holding the leading share of the U.S. market in 2025. The dominance of women segment in the U.S. market is majorly driven by the vast diversity of styles, fits, and fashion trends that cater to female consumers. Women’s denim encompasses a wide array of cuts, including skinny, bootcut, wide leg, high waisted, and cropped styles, which encourages frequent purchases to keep up with evolving fashion cycles. According to the NPD Group, women account for a significantly larger portion of apparel spending compared to men, with denim being a staple category that sees regular replenishment and trend driven additions. The influence of social media and celebrity culture plays a pivotal role in shaping women’s preferences, as influencers showcase new ways to style denim, creating immediate demand for specific looks. The integration of stretch fabrics and inclusive sizing further expands the addressable market, ensuring that more women can find comfortable and flattering options. Seasonal launches and collaborations with designers keep the category fresh and exciting, driving repeat visits to both online and physical stores. Women are also more likely to participate in sustainable fashion initiatives, such as buying vintage or recycled denim, which adds another layer of market activity. This combination of stylistic variety, cultural influence, and inclusive innovation solidifies the women segment as the primary revenue generator in the U.S. denim industry.

On the other side, the children segment is projected to register a promising CAGR in the U.S. market during the forecast period owing to the need for frequent replacements driven by rapid physical growth and increasing participation in school and social activities. Parents prioritize durability and comfort when purchasing jeans for children, leading to a steady demand for high quality, sturdy denim that can withstand active play. According to the U.S. Census Bureau, there are approximately 73 million children in the U.S., representing a substantial and consistent consumer base for kid’s apparel. As children grow quickly out of their clothes, parents must replace jeans every few months, ensuring recurring sales volume. The rise of mini me trends, where parents dress children in styles similar to their own, has also boosted demand for fashionable kids denim. As per the Cotton Incorporated Lifestyle Monitor Survey, parents are increasingly willing to spend on premium denim for children if it offers better fit and longevity, reducing the frequency of replacements in the long run. Retailers are expanding their children’s lines to include adaptive clothing for kids with disabilities and eco-friendly options made from organic cotton, appealing to conscientious parents. Online retailers offer convenient subscription services for kids clothing boxes, which simplifies the shopping process for busy families. The back to school season serves as a major peak period for sales, as parents outfit children for the academic year. This consistent need for replacement, combined with growing fashion awareness among younger demographics, drives the rapid expansion of the children’s denim segment.

By Distribution Channel Insights

The offline segment retained the leading position in the U.S. denim jeans market in 2025, primarily because fit and feel are critical factors in the purchase decision process for denim apparel. Consumers prefer to try on jeans in physical stores to assess comfort, waistband fit, length, and fabric texture before committing to a purchase. According to the National Retail Federation, despite the growth of e commerce, brick and mortar stores still account for the majority of apparel sales, as shoppers value the immediate gratification and tactile experience of in person shopping. Department stores, specialty retailers, and brand flagship stores provide knowledgeable staff that can assist with sizing and styling, enhancing the customer experience. For instance, physical retail locations serve as important touch points for brand building and customer engagement, allowing companies to showcase their full product range and latest collections. Many consumers use a hybrid approach known as show rooming, where they try items in store and may purchase online later, but the initial interaction often happens offline. Retailers have invested in improving store layouts, fitting room experiences, and Omni channel services, such as buy online, pick up in store, to remain competitive. The social aspect of shopping with friends or family also drives foot traffic to malls and retail districts. For premium and luxury denim brands, physical stores are essential for conveying brand heritage and quality through visual merchandising and personalized service. This enduring preference for physical interaction ensures that offline channels remain the primary driver of denim sales in the U.S.

However, the online segment is estimated to showcase a promising CAGR in the U.S. denim jeans market during the forecast period owing to the convenience, extensive selection, and advancements in digital fitting technologies. E-commerce platforms allow consumers to browse thousands of styles, sizes, and washes from the comfort of their homes, overcoming geographical limitations of physical retail. According to the U.S. Census Bureau, e commerce sales continue to grow at a robust pace, with apparel being one of the top categories for online spending. Innovations such as virtual try on tools, AI driven size recommendations, and detailed customer reviews help mitigate the risk of poor fit, which has historically been a barrier to online denim purchases. As per McKinsey and Company, digital native vertical brands have disrupted the market by offering direct to consumer models that provide higher value and personalized experiences, attracting younger shoppers. Social media integration enables seamless discovery and purchase through shoppable posts and influencer endorsements, driving impulse buys. Subscription services and easy return policies further enhance convenience, encouraging trial of new brands. The ability to compare prices and access exclusive online deals attracts budget conscious consumers. Mobile commerce has simplified the shopping process, making it accessible anytime and anywhere. Retailers are investing in logistics to ensure faster delivery times, meeting consumer expectations for immediacy. This combination of technological innovation, convenience, and expanded reach fuels the rapid expansion of the online channel, capturing an increasing share of denim sales.

COUNTRY LEVEL ANALYSIS

The U.S. held the major share of the U.S. denim jeans market in 2025 and is anticipated to experience strong sales volume and maintain its position as a highly resilient baseline market for global retail expansion over the next few years. According to Levi Strauss and Co, the birthplace of blue jeans, the U.S. remains the epicenter of denim innovation and trendsetting, influencing global fashion directions. The large population of over 349 million people provides a massive consumer base with diverse needs and preferences, driving significant volume sales. High disposable income levels allow Americans to purchase multiple pairs of jeans for different occasions, ranging from work to leisure. As per the Bureau of Labor Statistics, apparel remains a consistent category of household expenditure, reflecting the importance of clothing in American life. The presence of major global denim brands headquartered in the U.S. fosters intense competition and continuous product development. Retail networks are highly developed, with widespread availability of denim in department stores, specialty shops, and online platforms. The trend towards sustainability is gaining momentum, with U.S. consumers increasingly demanding eco-friendly production methods and transparent supply chains. Social media and celebrity culture amplify trends rapidly, creating spikes in demand for specific styles. The robust e-commerce sector facilitates easy access to a wide variety of options, enhancing market efficiency. This combination of cultural significance, economic strength, and technological adoption ensures that the U.S. maintains its dominance in the global denim jeans market, setting standards for quality, style, and innovation.

COMPETITIVE LANDSCAPE

The competition in the U.S. denim jeans market is intense and characterized by a mix of heritage brands fast fashion retailers and emerging direct to consumer labels. Major players compete on the basis of brand heritage product quality and sustainability credentials while striving to offer trendy and affordable options. The market sees continuous innovation in fabric technology such as stretch and eco friendly materials to enhance comfort and appeal. Price competition is significant in the mass market segment where value drives purchase decisions for budget conscious households. Conversely premium segments compete on exclusivity craftsmanship and unique design narratives. Retailers leverage omnichannel strategies to provide seamless shopping experiences across online and physical stores. Social media influence plays a crucial role in shaping trends and driving demand for specific styles. Direct to consumer brands disrupt traditional models by offering personalized experiences and transparent pricing. Intellectual property protection is vital for maintaining brand identity and preventing counterfeiting. Regulatory compliance regarding labor practices and environmental standards influences operational strategies. This dynamic environment fosters constant adaptation and innovation ensuring that consumers have access to diverse and high quality denim products that meet their evolving needs and values.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. denim jeans market are

- Bestseller

- Pepe Jeans

- United States Polo Association

- PVH Corp.

- Kering SA

- Hennes & Mauritz AB (H&M)

- Gap Inc.

- VF Corp.

- Levi Strauss & Co. Class A

Top Players in the Market

- Levi Strauss and Co remains a cornerstone of the U.S. denim industry with its iconic Levi s brand defining American casual wear for over a century. The company continues to lead through innovation in sustainable manufacturing and digital retail experiences. Recent actions include expanding its SecondHand resale platform and investing in waterless finishing technologies to reduce environmental impact. Levi s strengthens its market position by leveraging direct to consumer channels and personalized marketing campaigns that resonate with younger demographics. The brand actively collaborates with artists and designers to keep its product line fresh and culturally relevant. By focusing on quality durability and heritage Levi s maintains strong customer loyalty. Their commitment to social responsibility and inclusive sizing further enhances brand appeal. This strategic blend of tradition and modernization ensures Levi s remains a dominant force in the competitive U.S. denim landscape.

- VF Corporation contributes significantly to the U.S. denim market through its portfolio of premium brands including Wrangler and Lee. The company focuses on delivering high quality durable denim that appeals to both workwear and fashion conscious consumers. Recent actions involve revitalizing the Lee brand with contemporary designs and sustainable materials to attract millennial and Gen Z shoppers. VF Corporation leverages its global supply chain expertise to optimize production efficiency and reduce costs. The company invests heavily in digital transformation enhancing online shopping experiences and data analytics capabilities. By emphasizing authenticity and heritage VF Corporation builds strong emotional connections with customers. Their strategic partnerships with retailers and influencers expand brand visibility and reach. VF Corporation also prioritizes sustainability initiatives such as recycling programs and eco friendly fabrics. These efforts reinforce their reputation as a responsible and innovative leader in the denim sector ensuring continued relevance and growth in the U.S. market.

- Gap Inc plays a vital role in the U.S. denim jeans market with its flagship Gap brand offering accessible and versatile denim styles for the whole family. The company focuses on providing classic fits and trendy updates at competitive price points. Recent actions include launching specialized denim collections featuring inclusive sizing and sustainable cotton sources. Gap Inc strengthens its position by integrating omnichannel strategies that seamlessly connect online and offline shopping experiences. The brand utilizes customer data to personalize recommendations and improve inventory management. Gap Inc also engages in collaborative projects with celebrities and designers to generate buzz and attract new customers. Their commitment to quality and affordability makes denim accessible to a broad audience. By continuously refreshing its product assortment and enhancing store aesthetics Gap Inc maintains its appeal in a crowded market. This focus on accessibility style and operational efficiency solidifies Gap Inc as a key player in the U.S. denim industry.

Top Strategies Used by Key Market Participants

Key players in the U.S. denim jeans market primarily employ product differentiation strategies by introducing sustainable fabrics and innovative fits to appeal to environmentally conscious and style driven consumers. Companies invest heavily in digital transformation enhancing e commerce platforms and virtual fitting tools to improve online shopping experiences. Strategic collaborations with influencers and celebrities help build brand hype and reach younger demographics effectively. Brands emphasize direct to consumer models to capture higher margins and gather valuable customer data. Sustainability initiatives such as water conservation and recycling programs are central to corporate social responsibility efforts. Retailers optimize supply chains to ensure faster delivery and reduced environmental impact. Personalization through AI driven recommendations enhances customer engagement and loyalty. These multifaceted strategies enable participants to navigate competitive pressures and adapt to evolving consumer preferences in the dynamic apparel industry.

MARKET SEGMENTATION

This research report on the U.S. denim jeans market is segmented and sub-segmented into the following categories.

By End Use

- Men

- Women

- Children

By Distribution Channel

- Online

- Offline

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1. What is the U.S. denim jeans market?

The U.S. denim jeans market includes the production, distribution, and sale of denim jeans for men, women, and children across various price segments and styles.

2. What is driving the growth of the U.S. denim jeans market?

Market growth is driven by evolving fashion trends, increasing consumer spending on apparel, product innovation, and rising demand for comfortable and sustainable denim products.

3. Which consumer segment holds the largest share of the U.S. denim jeans market?

The women's segment holds a significant share of the market due to a wide variety of styles, fits, and fashion preferences.

4. What are the most popular types of denim jeans in the United States?

Popular styles include skinny jeans, straight leg jeans, slim fit jeans, bootcut jeans, relaxed fit jeans, and wide leg jeans.

5. How is sustainability influencing the denim jeans market?

Manufacturers are increasingly adopting sustainable materials, water saving production techniques, recycled fibers, and eco friendly dyeing processes.

6. What role does e commerce play in the U.S. denim jeans market?

Online retail platforms provide consumers with convenient shopping experiences, broader product selections, personalized recommendations, and easy product comparisons.

7. How are fashion trends affecting denim jeans sales?

Changing fashion preferences, celebrity influence, social media trends, and seasonal collections significantly impact consumer purchasing decisions.

8. Which distribution channels are important in the denim jeans market?

Department stores, specialty apparel stores, supermarkets, brand outlets, and online retail channels are major distribution channels.

9. What challenges does the U.S. denim jeans market face?

Challenges include fluctuating raw material costs, changing fashion trends, supply chain disruptions, and competition from alternative casual apparel.

10. What trends are shaping the future of the U.S. denim jeans market?

Key trends include sustainable denim production, stretch fabrics, customization options, gender inclusive designs, and digital retail expansion.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com