U.S. Home Appliance Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Distribution Channel, and Country – Industry Forecast From 2026 to 2034

U.S. Home Appliance Market Report Summary

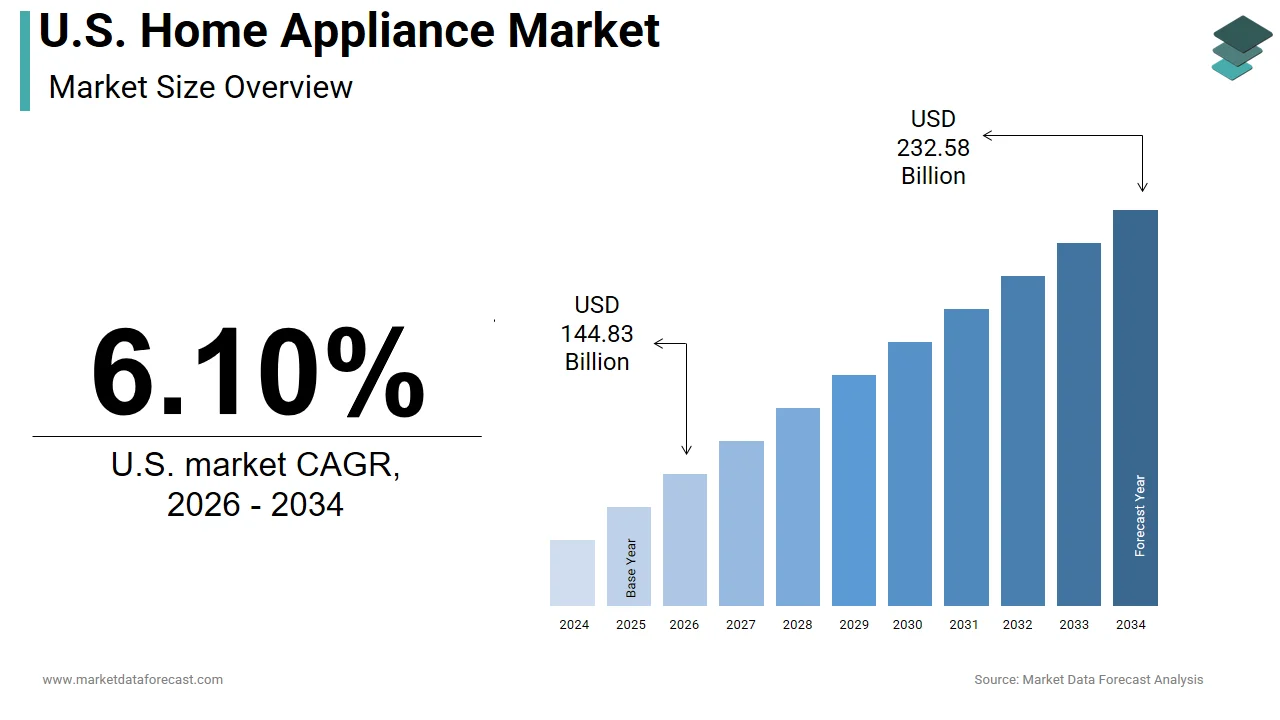

The U.S. home appliance market was valued at USD 136.10 billion in 2025, is estimated to reach USD 144.83 billion in 2026, and is projected to reach USD 232.58 billion by 2034, growing at a CAGR of 6.10% from 2026 to 2034. Market growth is driven by rising consumer demand for smart and energy-efficient appliances, increasing home renovation activities, and rapid advancements in connected home technologies. The integration of artificial intelligence, IoT-enabled functionality, and automation is transforming the home appliance industry. Additionally, growing e-commerce penetration and replacement demand for premium appliances are further supporting market expansion across the United States.

Key Market Trends

- Rising demand for smart and connected home appliances.

- Increasing focus on energy-efficient and sustainable products.

- Growth in online appliance sales and digital retail channels.

- Expansion of AI-enabled and automated household solutions.

- Increasing consumer preference for premium and multifunctional appliances.

Segmental Insights

- Based on type, the major appliances segment dominated the United States home appliance market in 2025, driven by strong demand for refrigerators, washing machines, and cooking appliances.

- Based on product category, the small appliances segment held the leading share in 2025, supported by rising adoption of kitchen and personal care appliances.

- Based on distribution channel, the online segment dominated the market in 2025, driven by growing e-commerce penetration, competitive pricing, and convenience.

Country-Level Insights

- The United States is expected to maintain its dominance in the global home appliance market over the forecast period due to increasing adoption of AI-integrated appliances and growing demand for energy-efficient replacement products. Strong technological innovation and consumer spending continue to support market growth.

Competitive Landscape

The U.S. home appliance market is highly competitive, with companies focusing on smart technologies, product innovation, and sustainability initiatives. Strategic partnerships, connected ecosystems, and expansion of digital retail channels are shaping the competitive landscape.

Prominent companies operating in the U.S. home appliance market include Whirlpool Corporation, Samsung Electronics, Haier Inc., Midea Group, Electrolux AB, Bosch, LG Electronics Inc., GE Appliances, The Maytag Corporation, and Miele & Cie. KG.

U.S. Home Appliance Market Size

The U.S. home appliance market was valued at USD 136.10 billion in 2025, is estimated to reach USD 144.83 billion in 2026, and is projected to reach USD 232.58 billion by 2034, growing at a CAGR of 6.10% from 2026 to 2034.

As per data from the U.S. Census Bureau, there are approximately 131.2 million households in the country, providing a substantial base for appliance installation and replacement. The average age of these housing units continues to increase, with many homes requiring updates to older, inefficient systems. According to the U.S. Energy Information Administration, residential buildings account for 21% of total energy consumption in the U.S., driving demand for energy-efficient models that reduce utility costs. The integration of smart technology into these devices has transformed them from simple tools into connected components of the modern smart home ecosystem. Consumers increasingly seek appliances that offer remote monitoring, automation, and connectivity with other digital devices. The shift towards sustainable living and environmental consciousness further influences purchasing decisions, with buyers prioritizing products that minimize water and energy usage. This market is not merely a reflection of consumer spending power, but also an indicator of housing market health, renovation activity, and technological adoption rates across American households.

MARKET DRIVERS

Surge in Home Renovation and Remodeling Activities

The sustained surge in home renovation and remodeling activities, as homeowners invest in upgrading their living spaces, is a key factor propelling the U.S. home appliance market growth. Following years of increased time spent at home, consumers have prioritized improving the functionality and aesthetics of their kitchens and laundry rooms. According to the Remodeling Futures Program at the Joint Center for Housing Studies of Harvard University, annual spending on home improvements and repairs in the U.S. is projected to reach $509 billion through the end of the fourth quarter of 2025. This substantial investment directly correlates with the purchase of new appliances, as renovations often involve replacing outdated units with modern, energy-efficient models. The aging housing stock in the U.S. necessitates regular updates, with many homes built before 1980 requiring significant modernization to meet current standards. Data from the National Association of Home Builders indicates that kitchen and bathroom remodels remain the most popular projects among homeowners, driving demand for high-end refrigerators, ranges, and dishwashers. Furthermore, the rise in home equity values has enabled homeowners to finance these upgrades through loans or lines of credit. The desire for customized and integrated appliances, that match contemporary interior design trends, also fuels this growth. Manufacturers are responding by offering a wider variety of finishes, sizes, and features to cater to diverse renovation needs. This continuous cycle of home improvement ensures a steady demand for both major and small appliances across the country.

Increasing Adoption of Smart Home Technology and Connectivity

The growing adoption of smart home technology and the demand for connected devices that enhance convenience and efficiency are further contributing to the U.S. home appliance market expansion. Consumers are increasingly seeking appliances that can be controlled remotely via smartphones or integrated with voice-activated assistants, such as Amazon Alexa and Google Assistant. According to the Consumer Technology Association, sales of smart home devices in the U.S. have grown consistently, with smart appliances representing a rapidly expanding category. These devices offer features, such as remote monitoring, predictive maintenance, and automated operation, which appeal to tech-savvy households. Data from rubyhome.com indicates that 77.05 million homes in the U.S. are actively using at least one smart home device as of 2026, representing 51.37% of all households. Smart refrigerators can track inventory and suggest recipes, while smart washing machines can optimize cycles based on fabric type and load size. This level of automation reduces manual effort and improves resource management, aligning with modern lifestyles that value time savings and precision. The interoperability of these appliances with broader home automation systems creates a cohesive user experience that encourages further adoption. Manufacturers are investing heavily in research and development to enhance connectivity and user interfaces, making smart appliances more accessible and user-friendly. This technological evolution drives replacement cycles, as consumers upgrade from traditional models to connected versions.

MARKET RESTRAINTS

Supply Chain Disruptions and Raw Material Volatility

The persistent supply chain disruptions and volatility in raw material prices that impact production costs and availability are primarily impeding the growth of the U.S. home appliance market. The market relies heavily on global supply chains for components, such as semiconductors, steel, aluminum, and plastics, which have experienced significant fluctuations in recent years. According to the Bureau of Labor Statistics, the producer price index for final demand rose 3.0% in 2025, after moving up 3.5% in 2024, reflecting notable increases in input costs and logistical challenges. Shortages of critical components, like microchips, have led to production delays and reduced inventory levels, affecting the ability of manufacturers to meet consumer demand. Data from the Institute for Supply Management indicates that supplier delivery times remain extended, causing uncertainty in planning and fulfillment. These disruptions force manufacturers to increase prices, which can dampen consumer demand, particularly among price-sensitive segments. Additionally, the geopolitical tensions and trade policies affecting international trade routes contribute to the instability of supply chains. The reliance on imported parts makes the industry vulnerable to external shocks, such as port congestion or labor strikes. These factors collectively constrain market growth by limiting product availability and increasing costs for both producers and consumers. Until supply chains stabilize and raw material prices normalize, the market will continue to face operational and financial pressures.

Stringent Energy Efficiency Regulations and Compliance Costs

The stringent energy efficiency regulations and the associated compliance costs that manufacturers must bear are further hindering the expansion of the U.S. home appliance market. Federal and state agencies impose strict standards on energy and water consumption for appliances to promote environmental sustainability and reduce utility bills. According to the Department of Energy, new efficiency standards for products, such as refrigerators, dishwashers, and clothes washers, require manufacturers to invest in advanced technologies and redesign processes. These regulatory requirements increase research and development expenses and production costs, which are often passed on to consumers in the form of higher prices. Data from the Appliance Standards Awareness Project indicates that compliance with evolving standards can significantly impact the affordability of appliances for low-income households. While these regulations drive innovation, they also create barriers for smaller manufacturers, who may lack the resources to adapt quickly. The complexity of navigating varying state-level regulations adds another layer of difficulty for national distributors. Additionally, the transition to more efficient technologies sometimes involves trade-offs in performance or features that may not appeal to all consumers. These regulatory pressures can slow down the adoption of new models and limit market expansion. Manufacturers must balance compliance with competitiveness, ensuring that their products remain attractive despite the added costs. This regulatory landscape poses a continuous challenge to the industry's growth trajectory.

MARKET OPPORTUNITIES

Expansion into Sustainable and Eco-Friendly Product Lines

The expansion into sustainable and eco-friendly product lines that align with growing environmental consciousness among consumers is a promising opportunity for the U.S. home appliance market. There is increasing demand for appliances that use recycled materials, reduce water consumption, and minimize carbon footprints during operation. According to the Environmental Protection Agency, consumers are increasingly prioritizing sustainability in their purchasing decisions, with many willing to pay a premium for green products. Manufacturers can capitalize on this trend by developing appliances with high Energy Star ratings and using biodegradable or recyclable components in their construction. Data from NielsenIQ indicates that sales of sustainable goods have outpaced conventional products in various categories, including home care and appliances. The introduction of heat pump technology in dryers and water heaters offers substantial energy savings and appeals to environmentally conscious buyers. Additionally, the use of smart sensors to optimize resource usage enhances the appeal of these products. Companies that transparently communicate their sustainability efforts and obtain relevant certifications can build strong brand loyalty and differentiate themselves in a crowded market. Government incentives and rebates for energy-efficient appliances further support this opportunity by reducing the upfront cost for consumers. By leading the way in sustainable innovation, manufacturers can capture a growing segment of the market and contribute to broader environmental goals.

Integration of Artificial Intelligence for Predictive Maintenance

The integration of artificial intelligence for predictive maintenance and enhanced user personalization is another notable opportunity for the U.S. home appliance market. AI-enabled appliances can monitor their own performance, detect anomalies, and alert users to potential issues before they lead to breakdowns. According to the International Data Corporation, the adoption of AI in consumer devices is accelerating, with smart appliances becoming key components of the Internet of Things ecosystem. This technology reduces the need for reactive repairs and extends the lifespan of appliances, providing value to consumers through reliability and cost savings. Data from McKinsey suggests that predictive maintenance can reduce maintenance costs by 10% to 40%, and extend equipment life by several years. Manufacturers can offer subscription-based services for ongoing monitoring and support, creating new revenue streams beyond the initial sale. AI also allows for personalized user experiences by learning household habits and optimizing appliance settings automatically. For example, smart ovens can adjust cooking times based on food type and quantity, while smart vacuums can map and clean specific areas efficiently. The ability to provide proactive service and customization enhances customer satisfaction and brand loyalty. As AI technology becomes more affordable and accessible, its integration into home appliances will drive innovation and open new markets for intelligent home solutions.

MARKET CHALLENGES

Intense Competition and Price Wars Among Market Players

The intense competition and frequent price wars among established players and emerging brands is a significant challenge to the U.S. home appliance market growth. The market is saturated with numerous manufacturers offering similar products, which leads to aggressive pricing strategies to capture market share. According to the Federal Trade Commission, high levels of competition can lead to margin compression and reduced profitability for companies unable to differentiate their offerings. Large multinational corporations often leverage economies of scale to lower prices, putting pressure on smaller domestic manufacturers, who struggle to compete on cost. Data from industry analysis shows that promotional discounts and seasonal sales have become common practices, eroding brand value and consumer perception of quality. This environment forces companies to continuously innovate and reduce costs, which can compromise product durability and service quality. Additionally, the entry of low-cost imports from international markets further intensifies the competitive landscape. Retailers also play a significant role in driving price competition by demanding lower wholesale prices from manufacturers. The resulting pressure on margins limits the resources available for research and development and marketing. Companies must find ways to distinguish their products through unique features, design, or superior customer service to avoid engaging in destructive price wars. Navigating this competitive terrain requires strategic positioning and operational efficiency to sustain long-term growth.

Cybersecurity Risks Associated with Connected Devices

The increasing connectivity of home appliances exposes the U.S. market to significant cybersecurity risks and privacy concerns that challenge consumer trust and adoption, which is another major challenge to the U.S. market. Smart appliances collect and transmit large amounts of data about household activities, which can be vulnerable to hacking and unauthorized access. According to the Federal Bureau of Investigation, cyberattacks on Internet of Things devices have risen sharply, with hackers exploiting security vulnerabilities to steal personal information or disrupt operations. Data from the National Institute of Standards and Technology highlights the lack of standardized security protocols for smart home devices, making them easy targets for malicious actors. Consumers are becoming more aware of these risks and may hesitate to purchase connected appliances if they perceive them as insecure. High-profile data breaches involving smart home devices can damage brand reputation and lead to legal liabilities for manufacturers. Ensuring robust cybersecurity requires continuous investment in encryption, software updates, and secure cloud infrastructure, which increases development costs. Additionally, the complexity of securing a diverse range of devices, with different operating systems, poses technical challenges for manufacturers. Regulatory bodies are beginning to scrutinize data privacy practices in the smart home sector, which may lead to stricter compliance requirements. Addressing these security concerns is essential for maintaining consumer confidence and sustaining the growth of the smart appliance market. Manufacturers must prioritize security by design to mitigate these risks and protect user data.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Distribution Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Whirlpool Corporation, Samsung Electronics Co. Ltd., Haier Inc., Midea Group, Electrolux AB, Bosch, LG Electronics Inc., GE Appliances, The Maytag Corporation, Miele & Cie. KG, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The major appliances segment dominated the market by holding the largest share of the U.S. market in 2025. The dominance of the major appliances segment in the U.S. market can be credited to their essential role in daily household operations and the consistent need for replacement driven by product lifecycle expiration. Items such as refrigerators, washing machines, and ovens are considered indispensable utilities in American homes, ensuring a baseline demand regardless of economic fluctuations. According to the U.S. Census Bureau, nearly 99% of occupied housing units in the country are equipped with a refrigerator, and approximately 98% have a cooking range, creating a universal market base. The average lifespan of these appliances ranges from 10 to 15 years, which creates a predictable and steady replacement cycle. Data from the Consumer Expenditure Survey indicates that households allocate a significant portion of their durable goods budget to major appliances, reflecting their priority status. When older units fail or become inefficient, consumers are compelled to purchase replacements rather than deferring the expense. This necessity-driven demand is further supported by the aging housing stock in the U.S., where older appliances are frequently upgraded during home sales or renovations. The sheer volume of transactions in this segment dwarfs other categories, because each home typically requires multiple major appliances. Furthermore, the high unit price of these items contributes significantly to overall market revenue. Manufacturers benefit from this stable demand pattern, which allows for long-term production planning and inventory management. The critical function of these devices in maintaining hygiene, food safety, and comfort ensures that they remain the cornerstone of the home appliance industry.

However, the heating and cooling appliances segment is expected to experience a promising CAGR in the U.S. market during the forecast period, owing to the increasing frequency of extreme weather events and shifting climate patterns. As temperatures become more volatile, with hotter summers and colder winters, households are investing in robust climate control systems to maintain comfort and safety. According to the National Energy Assistance Directors Association, average summer electricity expenditures for cooling are projected to reach $778 in 2026, which is an 8.5% increase from the previous year. This environmental reality drives the adoption of advanced air conditioners, heat pumps, and smart thermostats that can handle extreme conditions efficiently. Data from the Energy Information Administration indicates that residential energy consumption for space heating and cooling remains the largest component of home energy use, prompting upgrades to more efficient systems. Homeowners are replacing outdated HVAC units with modern, high-efficiency models to mitigate the impact of rising energy costs during peak weather seasons. The growing awareness of indoor air quality also contributes to this trend, as consumers seek systems with advanced filtration capabilities. The immediacy of weather-related discomfort creates a sense of urgency for purchases, accelerating the growth rate of this segment. Manufacturers are responding by developing resilient and adaptive technologies that cater to diverse climatic needs across different regions.

By Product Category Insights

The small appliances segment led the market by capturing the highest share of the U.S. market in 2025 due to their affordability and the prevalence of impulse purchase behavior among consumers. Unlike major appliances, which require significant financial planning, small appliances, such as coffee makers, blenders, and toasters, are low-cost items that can be purchased spontaneously. According to the National Retail Federation, small appliances are frequent items in promotional campaigns and holiday gift guides, driving high sales volumes throughout the year. The lower price point reduces the perceived risk for consumers, allowing them to experiment with new brands and features without a substantial commitment. Data from the Consumer Technology Association shows that small kitchen appliances are among the most commonly owned electronic devices in American households, with high penetration rates. The ease of replacement also contributes to this dominance, as consumers frequently upgrade these items to access new functionalities or aesthetic designs. Retailers strategically place small appliances in high-traffic areas to capitalize on this impulse-buying tendency. The variety of options available, from basic models to premium versions, caters to a wide range of budgets and preferences. This accessibility ensures a constant flow of transactions and keeps the segment vibrant and competitive. The ability of small appliances to serve as entry points for brand loyalty further strengthens their market position.

On the other hand, the smart home appliances segment is the fastest-growing segment due to their seamless integration with broader Internet of Things ecosystems and the desire for interconnected living experiences. Consumers are increasingly building smart homes, where appliances communicate with each other and with central hubs, to automate tasks and enhance convenience. According to Statista, global smart home device shipments are expected to approach 1.25 billion units in 2026, reflecting rapid adoption rates. Smart refrigerators, ovens, and washing machines allow users to monitor and control them remotely via smartphones, providing unparalleled flexibility and control. Data from the ASHB annual survey highlights that smart home adoption among U.S. households rose to 59% in 2025, which reflects the value tech-savvy consumers place on automation and connectivity. The ability to receive notifications, start cycles from work, or adjust settings based on real-time data appeals to busy households. Interoperability with voice assistants, like Amazon Alexa and Google Assistant, further enhances the user experience by enabling hands-free operation. As standards for connectivity improve, the ease of integrating new appliances into existing smart home setups increases. This network effect drives continuous growth, as each new device adds value to the entire system. Manufacturers are prioritizing smart features to remain competitive in this evolving landscape.

By Distribution Channel Insights

The online segment held the leading share of the U.S. home appliance market in 2025. The leading position of the online segment in the U.S. market is attributed to the unparalleled convenience it offers and the ability for consumers to extensively compare products and prices. Shoppers can browse thousands of models, read detailed specifications, and view customer reviews from the comfort of their homes, saving time and effort. According to the U.S. Census Bureau, e-commerce captured 62.52% of all smart home device sales in 2025, accounting for a significant share of total retail sales in the durable goods category. The transparency of online pricing allows consumers to find the best deals and take advantage of seasonal discounts and flash sales. Data from Adobe Analytics indicates that online spending on home appliances spikes during major shopping events, such as Black Friday and Cyber Monday, demonstrating the channel's dominance in driving volume. The ability to filter searches by features, brand, and price range helps consumers make informed decisions quickly. Additionally, the availability of detailed video demonstrations and virtual showrooms enhances the online shopping experience. Home delivery services eliminate the logistical challenges of transporting large appliances, further boosting the appeal of online purchases. The comprehensive information ecosystem available online empowers consumers and builds confidence in their buying decisions. This ease of access and information richness solidifies e-commerce as the primary channel for appliance sales.

On the other hand, the specialty stores segment is expected to exhibit the fastest CAGR in the U.S. market during the forecast period as consumers seek expert guidance and a premium customer experience for high-end and complex appliances. Unlike general retailers, specialty stores employ knowledgeable staff, who can provide detailed advice on features, installation, and maintenance, which is crucial for sophisticated smart and luxury appliances. According to the National Kitchen and Bath Association, homeowners undertaking major renovations often prefer specialty showrooms for the personalized design consultations and product expertise they offer. Data from industry surveys indicates that consumers are willing to pay more for the assurance and service provided by specialized retailers, particularly for expensive major appliances. The tactile experience of seeing and touching high-quality finishes and testing features in person builds confidence in premium purchases. Specialty stores also offer white-glove delivery and installation services, which are highly valued by customers seeking hassle-free experiences. The focus on curated selections allows these stores to showcase the latest innovations and exclusive brands. This high-touch approach differentiates them from online and mass-market competitors. As appliances become more technologically complex, the need for professional guidance increases, driving traffic to specialty outlets. This value-added service model supports the rapid growth of this channel.

COUNTRY ANALYSIS

U.S. Home Appliance Market Analysis

The U.S. is likely to continue dominating the home appliance market during the forecast period globally due to the integration of agentic artificial intelligence and a shift toward energy-efficient replacement cycles. The country serves as a global trendsetter in appliance technology and design, influencing markets worldwide. According to the U.S. Census Bureau, the vast number of housing units and high homeownership rates create a robust and stable demand base for home appliances. The market status is characterized by high saturation levels, which drive replacement sales and upgrades, rather than initial purchases. The presence of leading global manufacturers and retailers ensures a competitive and dynamic environment. Data from the Bureau of Economic Analysis indicates that consumer spending on durable goods, including appliances, remains a significant component of personal consumption expenditures. The mature nature of the market means that growth is driven by innovation, efficiency, and smart technology, rather than volume expansion. The U.S. also leads in the adoption of energy-efficient and connected appliances, setting standards for sustainability and digital integration. This leadership position ensures that the U.S. market remains the primary focus for strategic investments and product launches by major industry players. The stability and size of the market provide a foundation for long-term industry growth.

COMPETITIVE LANDSCAPE

The competition in the U.S. home appliance market is intense and characterized by the presence of established global giants and innovative niche players vying for consumer attention. Major corporations leverage their extensive distribution networks and brand recognition to maintain dominance, while smaller firms compete through specialized features and unique designs. Price sensitivity remains a key factor influencing purchasing decisions, prompting companies to offer promotional discounts and financing options. Innovation in smart technology and energy efficiency serves as a primary differentiator as consumers increasingly seek connected and sustainable solutions. Retailers play a crucial role in shaping competitive dynamics by negotiating favorable terms with manufacturers and promoting exclusive models. The rise of e-commerce has intensified price transparency and comparison shopping, forcing brands to enhance their online presence and customer service. Product longevity and reliability are critical for building brand loyalty in this mature market. Companies must continuously invest in research and development to introduce novel features that address evolving lifestyle needs. Strategic alliances with technology providers enable seamless integration into smart home ecosystems. This dynamic environment requires agility and customer-centric strategies to sustain market position and achieve long-term profitability.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. home appliance market include

- Whirlpool Corporation

- Samsung Electronics Co. Ltd.

- Haier Inc.

- Midea Group

- Electrolux AB

- Bosch

- LG Electronics Inc.

- GE Appliances

- The Maytag Corporation

- Miele & Cie. KG

TOP PLAYERS IN THE MARKET

- Whirlpool Corporation maintains a dominant presence in the U.S. home appliance market through its extensive portfolio of trusted brands, including KitchenAid, Maytag, and Amana. The company focuses on delivering innovative solutions that enhance daily household routines while prioritizing sustainability and energy efficiency. Recent strategic actions include investing heavily in smart home technology integration to connect appliances with digital ecosystems for improved user convenience. Whirlpool has also expanded its manufacturing capabilities domestically to strengthen supply chain resilience and reduce lead times for consumers. The company actively engages in product redesigns that incorporate advanced features such as remote monitoring and automated cycles. By leveraging its strong distribution network and brand loyalty, Whirlpool continues to set industry standards for quality and reliability. These efforts reinforce its position as a leading provider of essential home appliances across diverse consumer segments in the national market.

- GE Appliances contributes significantly to the US market by offering a wide range of innovative and stylish home appliances under various brand identities. The company emphasizes customer-centric design and technological advancement to meet evolving consumer preferences for connected and efficient devices. Recent initiatives include the expansion of its FirstBuild micro factory model, which allows for rapid prototyping and customization of niche products. GE Appliances has strengthened its smart home offerings through partnerships with major technology platforms, enabling seamless voice control and automation. The company also focuses on sustainability by introducing energy-efficient models that reduce environmental impact. By investing in local manufacturing and community engagement, GE Appliances builds strong brand affinity. Its commitment to innovation and quality ensures it remains a preferred choice for homeowners seeking reliable and modern solutions for their kitchens and laundry rooms.

- LG Electronics plays a vital role in the US home appliance sector by driving innovation in smart technology and premium design aesthetics. The company is known for its cutting-edge features, such as artificial intelligence-driven diagnostics and thinQ connectivity that enhance user experience. Recent actions include the launch of new product lines that integrate seamlessly with smart home ecosystems and offer personalized settings. LG has invested in expanding its service network to provide superior after-sales support and maintenance for connected devices. The company also prioritizes sustainability by developing eco-friendly materials and energy-saving technologies in its refrigerators and washing machines. By focusing on high-end innovations and sleek designs, LG appeals to tech-savvy consumers who value both functionality and style. This strategy strengthens its reputation as a leader in modern home appliance solutions across the U.S.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS IN THE MARKET

Key players in the U.S. home appliance market primarily focus on integrating smart technology and Internet of Things capabilities to enhance user convenience and operational efficiency. Companies are investing in artificial intelligence to enable predictive maintenance and personalized usage patterns for consumers. Product differentiation through sleek designs and premium finishes helps brands stand out in a saturated market. Strategic partnerships with technology firms facilitate seamless connectivity with voice assistants and mobile applications. Manufacturers are also prioritizing sustainability by developing energy-efficient models and using recycled materials to appeal to environmentally conscious buyers. Expanding direct-to-consumer sales channels allows for better customer engagement and data collection. Supply chain localization is another critical strategy to mitigate disruptions and ensure timely delivery. These approaches enable firms to maintain competitiveness and drive growth in a dynamic industry landscape.

MARKET SEGMENTATION

This research report on the U.S. home appliance market has been segmented and sub-segmented into the following categories.

By Type

- Major Appliances

- Refrigeration Equipment

- Cooking Appliances

- Washing & Drying Equipment

- Heating & Cooling Appliances

- Others

- Small Appliances

- Coffeemakers

- Food Processors

- Humidifiers

- Microwave Ovens

- Others

- Smart Home Appliances

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Stores

- Online / E-Commerce

- Others

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. home appliance market?

The U.S. home appliance market provides major and small devices for cooking, cleaning, refrigeration, and laundry serving residential consumers.

How does the U.S. home appliance market function?

The U.S. home appliance market connects manufacturers, retailers, and consumers through wholesale distribution and e-commerce sales channels.

What drives growth in the U.S. home appliance market?

The U.S. home appliance market grows from housing turnover, replacement cycles, smart technology demand, and energy efficiency preferences.

Which segments lead the U.S. home appliance market?

Major appliances like refrigerators and laundry machines dominate the U.S. home appliance market alongside growing small kitchen devices.

What role do major appliances play in the U.S. home appliance market?

Major appliances anchor the U.S. home appliance market through long replacement cycles and high-value purchases for new households.

How important are small appliances in the U.S. home appliance market?

Small appliances drive volume sales in the U.S. home appliance market with frequent replacements and impulse kitchen gadget purchases.

What is smart appliance technology in the U.S. home appliance market?

Smart appliances enhance the U.S. home appliance market with Wi-Fi connectivity, app control, and voice assistant integration.

How does energy efficiency impact the U.S. home appliance market?

Energy-efficient models gain share in the U.S. home appliance market due to utility rebates and consumer cost-saving preferences.

What channels serve the U.S. home appliance market?

The U.S. home appliance market reaches buyers through big-box retailers, online platforms, specialty stores, and home builder partnerships.

What trends shape the U.S. home appliance market?

The U.S. home appliance market follows connected devices, sustainable materials, compact designs, and integrated kitchen ecosystems.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com