U.S. Hospitality Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Accommodation Class, Booking Channel, and Country – Industry Forecast From 2026 to 2034

U.S. Hospitality Market Report Summary

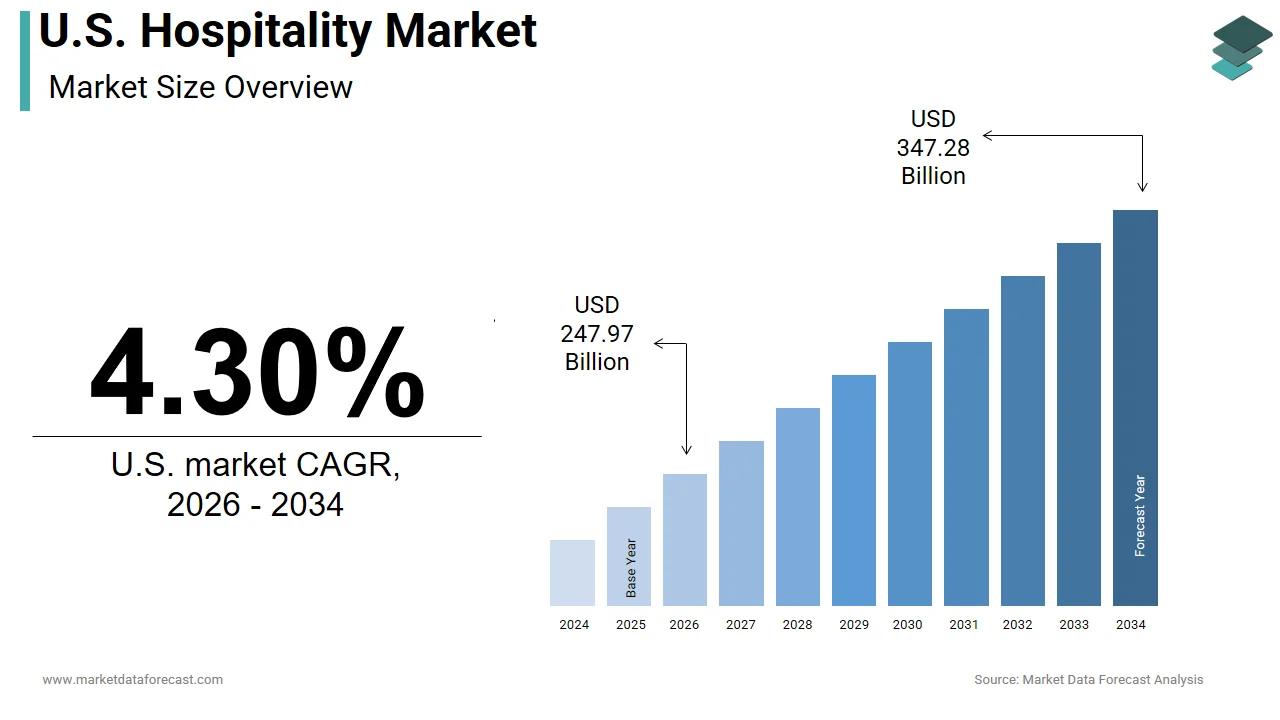

The U.S. hospitality market was valued at USD 237.75 billion in 2025, is estimated to reach USD 247.97 billion in 2026, and is projected to reach USD 347.28 billion by 2034, growing at a CAGR of 4.30% from 2026 to 2034. Market growth is driven by rising domestic and international tourism, increasing business travel, and growing demand for premium travel experiences. The hospitality industry is witnessing significant transformation through digital booking platforms, personalized guest experiences, and smart hospitality technologies. Additionally, the recovery of global travel and the hosting of major international sporting and entertainment events are expected to further boost market expansion across the United States.

Key Market Trends

- Rising demand for personalized and premium travel experiences.

- Increasing adoption of digital booking and contactless hospitality solutions.

- Growth in business and leisure travel activities.

- Expansion of midscale and upper-midscale hotel segments.

- Increasing investments in smart hospitality technologies and guest experience enhancement.

Segmental Insights

- Based on type, the chain hotels segment dominated the United States hospitality market in 2025, driven by strong brand presence, loyalty programs, and extensive property networks.

- Based on accommodation class, the mid and upper-midscale hotels segment held the leading share in 2025, supported by affordability, convenience, and growing consumer preference for value-driven stays.

Country-Level Insights

The United States hospitality market is expected to witness significant growth over the forecast period, supported by increasing visitor spending and expansion in room supply ahead of major international sporting and entertainment events. Strong tourism infrastructure and rising travel demand continue to support market expansion.

Competitive Landscape

The U.S. hospitality market is highly competitive, with companies focusing on customer experience, digital transformation, and expansion of hotel portfolios. Loyalty programs, technology integration, and strategic partnerships are key competitive strategies shaping the market.

Prominent companies operating in the U.S. hospitality market include Marriott International, Hilton Worldwide, Wyndham Hotels & Resorts, Hyatt Hotels Corporation, InterContinental Hotels Group, and Choice Hotels International Inc..

U.S. Hospitality Market Size

The size of the U.S. hospitality market was worth USD 237.75 billion in 2025. The market is anticipated to grow at a CAGR of 4.30% from 2026 to 2034 and be worth USD 347.28 billion by 2034 from USD 247.97 billion in 2026.

As per data from the Bureau of Labor Statistics, the leisure and hospitality sector employed 16.9 million individuals as of March 2026, representing a significant portion of the total workforce in the country. The industry's recovery and growth are closely tied to mobility trends and consumer behavior shifts following global disruptions. According to the U.S. Census Bureau, there are over 1 million restaurants and more than 50,000 lodging establishments operating across the nation, providing a vast infrastructure for service delivery. The integration of digital technologies has transformed operational efficiencies and customer engagement strategies, with mobile check-ins and contactless payments becoming standard practices. Consumer preferences have evolved towards experiential travel and personalized dining, which drives innovation in service offerings. The Federal Reserve Bank of St. Louis notes that personal consumption expenditures on services, particularly in recreation and hospitality, remain robust, indicating sustained demand. These market dynamics reflect a complex interplay between supply chain capabilities, labor availability, and evolving consumer expectations for quality and convenience in service interactions.

MARKET DRIVERS

Resilient Consumer Spending and Pent Up Demand for Experiential Travel

The resilient consumer spending, coupled with a strong pent-up demand for experiential travel and social dining, is primarily driving the expansion of the U.S. hospitality market. After periods of restricted mobility, consumers have prioritized spending on experiences over material goods, seeking to reconnect with family and friends through travel and dining out. According to the Bureau of Economic Analysis, personal consumption expenditures on services, including hospitality, increased by 0.6% in February 2026, reflecting a shift in household budget allocations. Data from the American Hotel and Lodging Association indicates that leisure travel demand has surpassed pre-pandemic levels in many regions, driven by a desire for unique and memorable experiences. Consumers are willing to pay premium prices for high-quality accommodations and gourmet dining, which boosts revenue per available room and average check sizes. The rise of bleisure travel, where business trips are extended for leisure purposes, further amplifies demand for hotel stays and local attractions. Additionally, the proliferation of social media platforms fuels the desire for Instagrammable destinations and culinary experiences, creating viral trends that drive immediate booking spikes. This behavioral shift towards valuing experiences ensures a steady flow of customers into hotels, restaurants, and entertainment venues. The willingness to spend on discretionary activities, despite economic uncertainties, underscores the emotional and social importance of hospitality services in modern American life.

Expansion of Business Travel and Corporate Event Recovery

A significant driver of the U.S. hospitality market is the gradual, but steady, recovery of business travel and corporate events, which traditionally account for a substantial portion of industry revenue. As companies resume in-person meetings, conferences, and team-building activities, the demand for conference facilities, business-class accommodations, and corporate dining has increased. According to the Global Business Travel Association, corporate travel spending in the U.S. reached $1.48 trillion in 2025, which represents a full recovery to pre-pandemic levels as organizations recognize the value of face-to-face interactions for negotiation and collaboration. Data from the Convention Industry Council shows that the meetings and conventions sector generates billions of dollars in economic impact, supporting hotels and catering services nationwide. The return of large-scale trade shows and professional associations provides a stable base of occupancy for urban hotels and convention centers. Furthermore, the hybrid work model has led to new forms of corporate travel, where employees gather periodically for strategic planning and networking. This structured demand helps stabilize occupancy rates during weekdays, which were previously impacted by remote work trends. Hotels are adapting by offering flexible meeting spaces and technology-enabled conferencing solutions to meet evolving corporate needs. The resurgence of business travel complements leisure demand, ensuring a balanced revenue stream for hospitality providers across different segments and geographies.

MARKET RESTRAINTS

Labor Shortages and Workforce Retention Challenges

The persistent labor shortage and difficulties in retaining skilled workforce members across various service roles are a major impediment to the U.S. hospitality market growth. The U.S. market has struggled to replenish staff levels following widespread departures during recent global disruptions, leading to operational constraints and reduced service capacity. According to the Bureau of Labor Statistics, the job openings rate for the leisure and hospitality sector remained high at 7.6% as of early 2026, indicating a significant gap between demand for workers and available supply. Data from the National Restaurant Association reveals that many establishments are operating at reduced hours or limiting menu options due to insufficient staffing levels. The high turnover rate inherent in the industry exacerbates this issue, requiring constant recruitment and training efforts, which increase operational costs. Wage pressures have intensified as businesses compete for limited talent, leading to higher labor expenses that squeeze profit margins. Additionally, the perception of hospitality work as unstable or demanding discourages new entrants from joining the workforce. This labor crunch affects service quality and customer satisfaction, as remaining staff face increased workloads and burnout. The inability to fully staff operations limits the ability of hotels and restaurants to maximize revenue potential during peak demand periods. Addressing these workforce challenges requires long-term strategies in compensation, benefits, and career development, which remain difficult to implement in a low-margin environment.

Inflationary Pressures and Rising Operational Costs

The inflationary pressures and rising operational costs that impact profitability and pricing strategies are further hindering the expansion of the U.S. hospitality market. The cost of essential inputs, such as food ingredients, energy, utilities, and maintenance supplies, has increased significantly, forcing businesses to raise prices for consumers. According to the Bureau of Labor Statistics, the Consumer Price Index for food away from home rose 4.5% year-over-year in February 2026, affecting restaurant margins and hotel food and beverage operations. Data from the American Hotel and Lodging Association indicates that energy costs for heating, cooling, and lighting have risen sharply, adding to the overhead burden for property owners. These increased costs are often passed on to customers in the form of higher room rates and menu prices, which can dampen demand among price-sensitive consumers. Inflation also affects disposable income, reducing the frequency of discretionary dining and travel occasions for middle- and lower-income households. Supply chain disruptions continue to cause volatility in ingredient availability and pricing, making budgeting and inventory management challenging for operators. The cumulative effect of these cost increases compresses profit margins and limits the ability of businesses to invest in improvements or expansions. Hospitality providers must balance price increases with value perception to maintain customer loyalty, while managing tight financial constraints. This economic environment creates a precarious operating landscape where cost control is critical for survival.

MARKET OPPORTUNITIES

Integration of Sustainable Practices and Eco Tourism

The integration of sustainable practices and the development of eco-tourism offerings that appeal to environmentally conscious consumers is a notable opportunity for the U.S. hospitality market. Travelers are increasingly prioritizing brands that demonstrate commitment to environmental stewardship, such as reducing waste, conserving water, and sourcing local, organic ingredients. According to the U.S. Environmental Protection Agency, a typical hotel can reduce its energy use by 20% by implementing energy efficiency measures, creating ample opportunity for improvement and differentiation through green initiatives. Data from Booking.com indicates that 80% of global travelers confirm that traveling more sustainably is important to them, with many willing to pay more for sustainable options. Hotels and resorts can capitalize on this trend by obtaining certifications, such as LEED or Green Key, which validate their sustainability efforts. Implementing energy-efficient systems, solar power, and zero-waste programs not only reduces operational costs but also enhances brand reputation. Restaurants can attract patrons by featuring farm-to-table menus that support local agriculture and reduce carbon emissions from transportation. Eco-tourism destinations that offer nature-based experiences, such as hiking, wildlife viewing, and conservation education, are gaining popularity. By aligning with consumer values and regulatory trends towards sustainability, hospitality businesses can unlock new market segments and build long-term loyalty. This strategic focus on environmental responsibility offers a competitive advantage in an increasingly discerning marketplace.

Adoption of Artificial Intelligence and Personalization Technologies

The adoption of artificial intelligence and advanced personalization technologies to enhance customer experience and operational efficiency is another prominent opportunity in the U.S. hospitality market. AI-driven tools can analyze guest preferences to offer tailored recommendations for dining, activities, and amenities, creating a highly personalized stay. According to the International Data Corporation, 60% of hospitality leaders plan to prioritize AI-driven personalization in 2026, as businesses seek to automate routine tasks and improve decision-making. Data from McKinsey suggests that personalization can deliver five to eight times the ROI on marketing spend, and lift sales by 10% or more. Hospitality providers can use chatbots for instant customer service, dynamic pricing algorithms to optimize revenue, and predictive analytics to manage inventory and staffing. Smart room technologies that allow guests to control lighting, temperature, and entertainment via voice or mobile apps enhance convenience and comfort. These innovations reduce friction in the guest journey and create memorable experiences that encourage repeat visits. Furthermore, AI can help identify high-value customers and target them with specific promotions, improving marketing return on investment. The ability to leverage data for real-time customization distinguishes brands in a crowded market. As technology becomes more accessible, smaller operators can also benefit from these tools, leveling the playing field. Embracing digital transformation positions hospitality businesses to meet the expectations of tech-savvy consumers.

MARKET CHALLENGES

Cybersecurity Threats and Data Privacy Concerns

The growing risk of cybersecurity threats and data privacy breaches that can severely damage brand reputation and customer trust is primarily challenging the expansion of the U.S. hospitality market. Hospitality businesses collect vast amounts of sensitive personal and financial information from guests, making them attractive targets for cybercriminals. According to the Federal Trade Commission, the number of consumer fraud reports reached 2.6 million in 2023, with hotels and restaurants being frequent victims of ransomware and phishing attacks. Data from the 2024 IBM Cost of a Data Breach Report indicates that the average cost of a data breach in the hospitality industry reached $3.36 million, driven by the volume of records compromised and regulatory penalties. A single security incident can lead to loss of customer confidence, legal liabilities, and substantial remediation costs. Compliance with data protection regulations, such as the California Consumer Privacy Act, requires a robust security infrastructure and continuous monitoring, which can be costly for smaller operators. The integration of third-party vendors and Internet of Things devices expands the attack surface, creating additional vulnerabilities. Guests are becoming more aware of privacy risks and may hesitate to share personal information or use digital services if they perceive inadequate security measures. Protecting data integrity requires ongoing investment in encryption, employee training, and incident response plans. Failure to address these security challenges can result in long-term reputational damage and loss of market share.

Regulatory Complexity and Compliance Burdens

The U.S. hospitality market faces significant challenges due to regulatory complexity and the burden of complying with diverse local, state, and federal laws. Operators must navigate a patchwork of regulations covering health and safety, labor standards, alcohol licensing, and zoning, which vary significantly across jurisdictions. According to the National Restaurant Association, labor costs represent approximately 33% of a typical restaurant's sales, and compliance with changing labor laws, including minimum wage increases and overtime rules, adds administrative complexity and cost to operations. Data from the American Hotel and Lodging Association highlights that varying short-term rental regulations in different cities create uncertainty for property owners and platform operators. Health codes and sanitation requirements require rigorous adherence and regular inspections, which can disrupt operations if violations occur. The introduction of new taxes, such as tourism levies or soda taxes, further impacts pricing strategies and profitability. Keeping abreast of legislative changes requires dedicated legal and compliance resources, which strain small- and medium-sized businesses. Inconsistent enforcement of regulations across regions creates an uneven playing field and operational inefficiencies. Additionally, environmental regulations regarding waste disposal and energy usage impose additional compliance costs. The dynamic nature of the regulatory landscape requires constant adaptation and vigilance. Failure to comply can result in fines, closures, or legal action, posing a serious threat to business continuity. Managing these regulatory demands is a persistent challenge for hospitality providers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Accommodation Class, Booking Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Marriott International, Hilton Worldwide, Wyndham Hotels & Resorts, Hyatt Hotels Corporation, InterContinental Hotels Group (IHG), Choice Hotels International Inc., and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The chain hotels segment dominated the market by holding the highest share of the U.S. hospitality market in 2025. The dominance of the chain hotels segment in the U.S. market is driven by their ability to cultivate strong brand loyalty through sophisticated, integrated loyalty programs. Major hotel groups, such as Marriott International, Hilton Worldwide, and Hyatt Hotels Corporation, have developed extensive rewards ecosystems that incentivize repeat business by offering points, free nights, and exclusive perks. According to the American Hotel and Lodging Association, 60% of all hotel room nights in the U.S. are booked at branded chain properties, reducing reliance on third-party distribution channels and lowering acquisition costs. Data from McKinsey indicates that members of hotel loyalty programs generate substantially higher revenue per available room compared to non-members, as they tend to stay more frequently and spend more on ancillary services. The consistency of service quality and amenities across different locations provides travelers with a sense of security and predictability, which is highly valued in both leisure and business travel. Chain hotels leverage their scale to negotiate better rates with suppliers and invest in technology enhancements that improve the guest experience. The widespread recognition of these brands also simplifies the decision-making process for consumers, who prefer familiar environments. This strategic advantage in customer retention and operational efficiency solidifies the dominance of chain hotels in the competitive U.S. landscape.

On the other side, the independent hotels segment is estimated to showcase a promising CAGR in the U.S. market during the forecast period owing to the increasing consumer demand for unique and authentic local experiences that differ from standardized chain offerings. Modern travelers, particularly Millennials and Generation Z, seek accommodations that reflect the culture and character of their destination, rather than generic corporate environments. According to a survey by Booking.com, 75% of travelers look for authentic experiences that are representative of the local culture, and many express a desire to stay in properties that offer a distinct local flavor and personalized service. Data from the Independent Hotel Show indicates that independent boutiques are gaining market share by curating bespoke experiences, such as locally sourced dining, art installations, and community-guided tours. These hotels often occupy historic buildings or unique architectural structures that provide a memorable aesthetic appeal. The rise of social media has amplified this trend, as guests share images of distinctive interiors and localized amenities, creating organic marketing buzz. Independent operators can adapt quickly to emerging trends and customize their services to niche markets, without the constraints of corporate branding guidelines. This flexibility allows them to cater to specific interests, such as wellness, sustainability, or culinary tourism. As travelers prioritize authenticity and emotional connection over uniformity, independent hotels are well-positioned to capture this growing segment of the market.

By Accommodation Class Insights

The mid and upper-midscale hotels segment led the market with the largest share of the U.S. hospitality market in 2025 because they offer an optimal balance of affordability and quality that appeals to the broadest segment of travelers. This category includes well-known brands, such as Holiday Inn, Hampton Inn, and Courtyard by Marriott, which provide consistent comfort and essential amenities without the premium price tag of luxury properties. According to the American Hotel and Lodging Association, midscale and upper-midscale segments account for 51% of total room inventory and occupancy in the U.S.. Data from STR indicates that these segments demonstrate resilience during economic fluctuations, as they attract both cost-conscious leisure travelers and budget-aware business professionals. The value proposition of clean, comfortable rooms, complimentary breakfast, and reliable Wi-Fi meets the core needs of most guests. Family travelers often prefer these hotels for their spacious layouts and family-friendly policies, which are less common in budget or luxury tiers. Corporate travel policies also favor midscale options for standard employee trips, ensuring steady demand throughout the week. The widespread geographic presence of these brands ensures accessibility in both urban and suburban locations. This combination of practical amenities, reasonable pricing, and broad appeal sustains the dominance of the mid and upper-midscale segment in the U.S. market.

However, the luxury hotels segment is estimated to be the fastest-growing segment in the U.S. hospitality market during the forecast period, owing to the rise in high-net-worth individuals and a shifting definition of luxury towards experiential travel. Affluent travelers are increasingly seeking exclusive, personalized, and immersive experiences, rather than just opulent surroundings. According to the Federal Reserve, the net worth of the top 1% of U.S. households reached a record $44.6 trillion at the end of 2023, providing higher disposable income for premium travel services. Data from Bain and Company indicates that the luxury travel sector is recovering faster than other segments, as high-end consumers prioritize unique memories and privacy. Luxury hotels are responding by offering bespoke services, such as private chefs, curated cultural tours, and wellness retreats, that cater to individual preferences. The demand for secluded resorts and boutique luxury properties in natural settings has surged, as travelers seek escape and rejuvenation. Social status and the desire for Instagrammable moments also drive spending on high-end accommodations. Luxury brands are investing in exceptional staff-to-guest ratios to ensure attentive and anticipatory service. This focus on exclusivity and personalization attracts wealthy domestic and international tourists, who are less sensitive to price increases. The resilience of this demographic during economic downturns further supports the robust growth of the luxury segment.

COUNTRY ANALYSIS

U.S. Hospitality Market Analysis

The U.S. is expected to see a significant rise in visitor spending and a 4.2% expansion in room supply as major international sporting events approach over the next few years. The country stands as the largest and most mature hospitality market in North America, accounting for the majority of regional revenue and employment. The country serves as a global leader in hospitality innovation, setting trends in technology, service standards, and sustainability practices. According to the World Travel and Tourism Council, the travel and tourism sector contributed $2.36 trillion to the U.S. GDP in 2023, highlighting its economic significance. The market status is characterized by a diverse mix of urban resorts, rural retreats, and business hubs that cater to varied traveler segments. The presence of major global hotel chains and iconic independent properties ensures a competitive and dynamic environment. Data from the Department of Commerce indicates that international visitor spending remains a crucial component of the industry, driving demand in gateway cities and tourist destinations. The mature nature of the market means that growth is driven by experience enhancement, technological integration, and sustainable practices, rather than simple capacity expansion. The U.S. also leads in the adoption of digital booking platforms and contactless services, influencing global operational standards. This leadership position ensures that the U.S. market remains the primary focus for strategic investments and product launches by international hospitality groups. The stability and size of the market provide a foundation for long-term industry resilience.

COMPETITIVE LANDSCAPE

The competition in the U.S. hospitality market is intense and characterized by the presence of global chains, independent boutiques, and alternative accommodation providers vying for traveler attention. Major hotel groups leverage their scale, brand recognition, and loyalty programs to maintain dominance while independent properties compete through unique experiences and personalized service. Price sensitivity fluctuates with economic conditions, prompting dynamic pricing strategies and promotional offers to attract guests. Innovation in technology and sustainability serves as a key differentiator as consumers seek seamless digital experiences and eco-friendly options. The rise of short-term rental platforms has intensified competition by offering diverse and often cheaper alternatives to traditional hotels. Retailers and online travel agencies influence competitive dynamics by controlling visibility and distribution channels. Product quality and service excellence are critical for building brand loyalty in this mature market. Companies must continuously invest in property renovations and staff training to meet evolving expectations. Strategic alliances with airlines and credit card companies enhance value propositions. This dynamic environment requires agility and customer-centric strategies to sustain market position and achieve long-term profitability.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. hospitality market include

- Marriott International

- Hilton Worldwide

- Wyndham Hotels & Resorts

- Hyatt Hotels Corporation

- InterContinental Hotels Group (IHG)

- Choice Hotels International Inc.

TOP PLAYERS IN THE MARKET

- Marriott International maintains a dominant presence in the U.S. hospitality landscape through its extensive portfolio of thirty distinct brands, ranging from luxury to budget segments. The company leverages its massive Bonvoy loyalty program to drive direct bookings and foster deep customer engagement across its properties. Recent strategic actions include expanding its footprint in key urban markets and resort destinations while investing heavily in digital transformation initiatives. Marriott has enhanced its mobile app capabilities to offer seamless contactless check-in and personalized guest experiences. The company actively pursues asset-light growth models by focusing on management and franchise agreements rather than ownership. By prioritizing sustainable tourism practices and diverse travel options, Marriott strengthens its appeal to modern travelers. These efforts reinforce its position as a leader in delivering consistent quality and innovative service solutions throughout the nation.

- Hilton Worldwide Holdings contributes significantly to the US market by operating a diverse collection of hospitality brands that cater to various traveler needs and preferences. The company focuses on delivering exceptional guest experiences through its award-winning Hilton Honors loyalty program, which drives repeat business and brand loyalty. Recent initiatives involve accelerating development in high-growth leisure destinations and enhancing digital tools for streamlined stays. Hilton has invested in smart room technologies and mobile key features to improve convenience and safety for guests. The company also emphasizes sustainability through its Travel with Purpose strategy, aiming to reduce environmental impact across its operations. By expanding its mid-scale and extended stay offerings, Hilton captures broader market segments. These strategic moves ensure Hilton remains a preferred choice for both leisure and corporate travelers seeking reliable and modern accommodations.

- Hyatt Hotels Corporation plays a vital role in the US hospitality sector by focusing on premium and luxury segments with a strong emphasis on personal care and unique experiences. The company distinguishes itself through its World of Hyatt loyalty program, which offers valuable rewards and exclusive member benefits. Recent actions include aggressive expansion into the all-inclusive resort market and lifestyle hotel segments to diversify its portfolio. Hyatt has strengthened its presence in key gateway cities and vacation destinations through strategic acquisitions and organic growth. The company prioritizes employee well-being and an inclusive culture, which translates into superior guest service standards. Hyatt also integrates advanced technology to enhance booking processes and personalize guest interactions. By focusing on high-touch service and distinctive property designs, Hyatt attracts discerning travelers. This approach solidifies its reputation for quality and innovation in the competitive US hospitality environment.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS IN THE MARKET

Key players in the U.S. hospitality market primarily focus on expanding their loyalty programs to drive direct bookings and enhance customer retention. Companies are investing heavily in digital transformation, including mobile apps and contactless technologies to improve guest convenience and operational efficiency. Strategic acquisitions of boutique brands and lifestyle hotels help diversify portfolios and attract younger demographics. Sustainability initiatives are increasingly central to corporate strategies as brands aim to reduce environmental impact and appeal to eco-conscious travelers. Partnerships with technology firms enable personalized experiences through data analytics and artificial intelligence. Franchise models are preferred for rapid expansion with lower capital risk. Enhancing food and beverage offerings with local and healthy options differentiates brands. These approaches enable firms to maintain competitiveness and drive growth in a dynamic industry landscape.

MARKET SEGMENTATION

This research report on the U.S. hospitality market has been segmented and sub-segmented into the following categories.

By Type

- Chain Hotels

- Independent Hotels

By Accommodation Class

- Luxury

- Mid & Upper-Midscale Hotels

- Budget & Economy

- Service Apartments

By Booking Channel

- Direct Digital

- OTAs

- Corporate/MICE

- Wholesale & Traditional Agents

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. hospitality market?

The U.S. hospitality market includes hotels, restaurants, resorts, and venues providing lodging, dining, and events for leisure and business travelers.

How does the U.S. hospitality market operate?

The U.S. hospitality market functions through property owners, management companies, and brands delivering guest services, bookings, and operations.

What drives demand in the U.S. hospitality market?

The U.S. hospitality market grows from domestic travel, business meetings, tourism recovery, and consumer spending on experiences and dining.

Which sectors lead the U.S. hospitality market?

Hotels and restaurants dominate the U.S. hospitality market, followed by resorts, event spaces, and foodservice operations nationwide.

What role do hotels play in the U.S. hospitality market?

Hotels form the core of the U.S. hospitality market by offering rooms, conference facilities, dining, and loyalty programs to diverse guests.

How important are restaurants in the U.S. hospitality market?

Restaurants drive revenue in the U.S. hospitality market through daily dining, catering services, and integration with hotel properties.

What trends shape the U.S. hospitality market?

The U.S. hospitality market embraces contactless services, sustainability practices, personalized guest experiences, and digital booking platforms.

How does technology impact the U.S. hospitality market?

Technology transforms the U.S. hospitality market with mobile check-ins, revenue management software, and AI-driven guest personalization.

What challenges face the U.S. hospitality market?

Labor shortages, rising operational costs, and shifting travel patterns challenge profitability across the U.S. hospitality market.

How do resorts contribute to the U.S. hospitality market?

Resorts expand the U.S. hospitality market by offering leisure destinations, spas, activities, and all-inclusive guest packages.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com