U.S Liability Insurance Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Employer's Liability Insurance, Product Liability Insurance, Commercial Liability Insurance, Professional Liability Insurance, Others), Distribution Channel, End User, And Country (California, Washington, Oregon, New York & Rest Of The United States) – Industry Analysis And Forecast, 2026 To 2034

U.S Liability Insurance Market Size

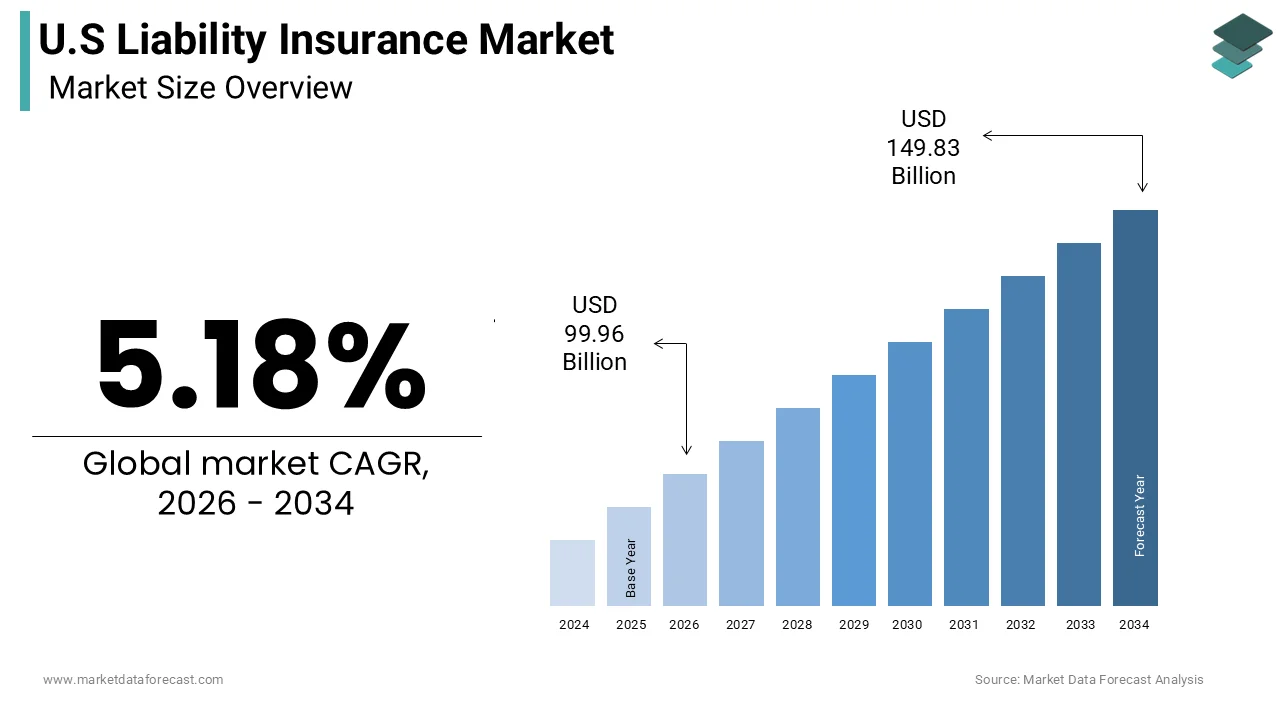

The U.S. liability insurance market size was calculated to be USD 95.02 billion in 2025 and is anticipated to be worth USD 149.83 billion by 2034, from USD 99.96 billion in 2026, growing at a CAGR of 5.18% during the forecast period.

Liability insurance is a type of policy that protects individuals and businesses from financial losses arising from legal claims of negligence, bodily injury, or property damage caused to third parties. It covers legal defense costs and payouts, serving as a safety net against lawsuits. This sector encompasses various forms of coverage, including general liability, professional liability, product liability, and directors and officers insurance. These instruments are essential for risk management in a litigious society where legal claims can result in substantial financial losses. According to the Insurance Information Institute, liability claims constitute a significant portion of commercial insurance losses, reflecting the persistent exposure faced by enterprises across diverse industries. The regulatory environment mandates certain types of liability coverage for specific professions and business operations, ensuring a baseline level of protection for the public. As per the National Association of Insurance Commissioners, premium writings for liability lines have shown consistent growth, driven by increasing awareness of legal risks and expanding business activities. The complexity of modern commerce, characterized by global supply chains and digital interactions, has amplified the need for comprehensive liability solutions. Courts continue to interpret laws in ways that expand the scope of potential liabilities, prompting organizations to seek broader coverage limits. This dynamic landscape requires insurers to continuously adapt their underwriting criteria and policy structures. The market functions not only as a mechanism for loss transfer but also as a stabilizer that enables economic activity by mitigating the uncertainty associated with legal disputes and compensatory awards.

MARKET DRIVERS

Escalating Litigation Costs and Legal Judgments

The rising cost of litigation and increasingly large legal judgments contribute to the growth of the United States liability insurance market. As legal fees and settlement amounts increase, businesses and professionals recognize the necessity of robust insurance coverage to protect their assets. According to the U.S. Chamber Institute for Legal Reform, the total cost of the tort system in the United States reached approximately 2.4 percent of the gross domestic product, indicating a substantial financial burden on the economy. This high-cost environment compels entities to secure higher liability limits to cover potential exposures. As per VerdictSearch data, median jury awards in personal injury and commercial liability cases have trended upward over the past decade, with some verdicts exceeding millions of dollars. The phenomenon of nuclear verdicts, where awards are disproportionately large compared to the actual damages, has heightened anxiety among corporate risk managers. Consequently, organizations are more willing to invest in comprehensive liability policies that include defense cost coverage and extended reporting periods. The frequency of class action lawsuits also contributes to this demand, as seen in sectors such as consumer products and healthcare. As per Law360, the number of class action filings has remained elevated, creating a persistent need for insurance mechanisms that can handle complex multi-plaintiff claims. This legal landscape ensures that liability insurance remains a non-negotiable component of corporate risk management strategies.

Regulatory Compliance and Mandatory Coverage Requirements

Stringent regulatory compliance standards and mandatory coverage requirements further drive the expansion of the United States liability insurance market. Federal and state laws impose specific liability insurance obligations on various industries to ensure public safety and financial responsibility. According to the Occupational Safety and Health Administration, businesses must adhere to strict safety regulations, and failure to do so can result in significant liabilities that necessitate insurance coverage. Many states require contractors, healthcare providers, and transportation companies to maintain minimum levels of liability insurance as a condition of licensure. As per the National Council on Compensation Insurance, workers' compensation and employer liability insurance are mandatory in most jurisdictions, creating a stable base of demand for these products. The healthcare sector faces particularly rigorous requirements due to the High Cost of medical malpractice claims. As per the American Medical Association, nearly all physicians carry medical malpractice insurance, often mandated by hospitals and state boards. Environmental regulations also drive demand for pollution liability coverage, as companies must demonstrate financial responsibility for potential cleanup costs. The Securities and Exchange Commission imposes fiduciary duties on corporate directors, leading to increased uptake of directors and officers liability insurance. These regulatory frameworks create a compulsory market segment where insurance is not optional but a legal prerequisite for operation. This structural demand ensures consistent premium growth and market stability regardless of broader economic fluctuations.

MARKET RESTRAINTS

Volatility in Investment Income and Interest Rates

Volatility in investment income and fluctuating interest rates are major limiting factors to the United States liability insurance market. This impacts insurer profitability and pricing strategies. Insurance companies rely heavily on investment returns from premiums collected before claims are paid out, known as the float. According to the Federal Reserve, changes in interest rates directly affect the value of fixed income portfolios, which constitute a large portion of insurer assets. When interest rates are low or volatile, insurers may struggle to generate sufficient investment income to subsidize underwriting losses. As per the National Association of Insurance Commissioners (NAIC) 2024 Mid-Year Outlook, a decline in investment yields pressures insurers’ net income, but premium adjustments are more directly correlated with rising loss ratios and social inflation; despite these increases, demand for mandatory liability coverage remains resilient. The uncertainty surrounding monetary policy makes long-term financial planning difficult for carriers, leading to more conservative underwriting practices. This caution can result in reduced capacity for certain high-risk lines of business, limiting availability for consumers. Furthermore, inflationary pressures erode the real value of future claim payments, requiring insurers to hold larger reserves. As per the Bureau of Labor Statistics, persistent inflation increases the cost of settling claims, particularly in liability lines where medical and repair costs are significant. These financial headwinds constrain the ability of insurers to offer competitive pricing and broad coverage terms. The resulting market hardening can discourage smaller businesses from purchasing adequate coverage, thereby exposing them to greater financial risk and limiting overall market growth potential.

Complexity of Emerging Risks and Data Privacy Laws

The complexity of emerging risks and evolving data privacy laws hampers the expansion of the United States liability insurance market. This creates uncertainty in underwriting and claims assessment. Rapid technological advancements introduce new liabilities such as cyber breaches and artificial intelligence errors that are difficult to quantify and price. According to a study, while earlier studies showed 64% experienced breaches, current data shows 81% of Americans feel they have little control over data collection, highlighting a pervasive cyber risk environment that traditional general liability policies (which often contain "silent cyber" exclusions) may not cover. The lack of historical data for these novel risks makes it challenging for insurers to develop accurate actuarial models. As per the National Conference of State Legislatures, numerous states have enacted distinct data privacy laws, creating a fragmented regulatory landscape that complicates compliance and liability determination. Insurers face difficulties in defining exclusions and coverage boundaries for cyber liability, leading to gaps in protection and potential disputes. The rapid pace of legislative change means that policies can become obsolete quickly, requiring frequent updates and adjustments. This uncertainty increases administrative costs and slows down the issuance of new products. Additionally, the interplay between general liability and cyber liability creates coverage overlaps and ambiguities that confuse buyers. As per the Insurance Information Institute, the ambiguity surrounding cyber coverage limits market expansion as businesses hesitate to purchase policies without a clear understanding of protections. This regulatory and technological complexity restrains market efficiency and slows the adoption of comprehensive liability solutions.

MARKET OPPORTUNITIES

Expansion of Cyber Liability Insurance Products

The expansion of cyber liability insurance products offers a significant opportunity for the United States liability insurance market. This growth is driven by accelerated digital transformation across all sectors. Businesses are increasingly dependent on digital infrastructure, making them vulnerable to cyberattacks, data breaches, and ransomware demands. According to the 2024 IBM Cost of a Data Breach Report, the average cost of a data breach in the United States reached $9.36 million, which remains the highest in the world and underscores the severe financial impact of cyber incidents on U.S. enterprises. This high cost drives demand for specialized cyber liability coverage that includes incident response, legal fees, and notification costs. As per the Cybersecurity and Infrastructure Security Agency, small and medium-sized enterprises are increasingly targeted by cybercriminals, expanding the potential customer base for insurers. Insurers have the opportunity to develop tailored policies that address specific industry needs, such as healthcare, finance, and retail. The integration of risk management services with insurance coverage, such as security audits and employee training, adds value for clients and reduces claim frequency. As per Marsh McLennan, the placement of cyber insurance has become a priority for risk managers, with many organizations seeking higher limits and broader terms. The evolving nature of cyber threats encourages continuous innovation in policy design, allowing insurers to differentiate their offerings. Furthermore, regulatory requirements for data protection are becoming stricter, mandating certain levels of cybersecurity preparedness that insurance can support. This growing awareness and regulatory pressure create a fertile environment for insurers to expand their cyber liability portfolios and capture new revenue streams in a rapidly developing segment of the market.

Growth in Professional Liability for Healthcare and Technology

The growth in professional liability insurance for the healthcare and technology sectors provides a promising prospect for the United States liability insurance market expansion. This is due to increasing specialization and regulatory scrutiny. In the healthcare industry, the rise of telemedicine and complex medical procedures has increased the potential for professional errors and subsequent lawsuits. According to the American Telemedicine Association, the adoption of telehealth services has surged, creating new liability exposures related to remote diagnosis and treatment. Insurers can develop specialized policies that address these unique risks, attracting healthcare providers who seek comprehensive protection. In the technology sector, the proliferation of software as a service and cloud computing has increased the demand for errors and omissions insurance. As per sources, global spending on IT services is projected to grow significantly, driving the need for coverage against service interruptions and data loss. Technology firms face liabilities related to intellectual property infringement and contract breaches, which require tailored insurance solutions. The increasing complexity of professional services in both sectors creates a need for higher coverage limits and broader definitions of covered acts. Insurers who can provide expertise in these niche areas can command premium pricing and build long-term client relationships. As per the Healthcare Financial Management Association, the cost of medical malpractice continues to rise, prompting hospitals and clinics to seek more robust insurance programs. This trend provides insurers with the opportunity to innovate and capture market share in high-value professional liability segments.

MARKET CHALLENGES

Social Inflation and Nuclear Verdicts

Social inflation and the emergence of nuclear verdicts hinder the growth of the United States liability insurance market. This drives up claim costs and creates unpredictability in loss forecasting. Social inflation refers to the increasing costs of insurance claims resulting from broader societal trends such as litigation funding and changing jury attitudes. As per Marathon Strategies (or Swiss Re), the frequency of large verdicts has increased, with some 'thermonuclear' awards reaching hundreds of millions of dollars. These nuclear verdicts distort the historical data used for pricing, making it difficult for insurers to set accurate premiums. As per the American Tort Reform Association, third-party litigation funding has contributed to this trend by enabling plaintiffs to pursue prolonged and aggressive legal strategies. Insurers face the challenge of reserving adequately for these potential outliers, which ties up capital and reduces profitability. The unpredictability of jury decisions in certain jurisdictions forces insurers to withdraw from markets or restrict coverage terms. This reduction in capacity can leave businesses underinsured and vulnerable to financial ruin. As per Swiss Re, social inflation is a global phenomenon, but is particularly pronounced in the United States due to its legal system. The challenge is compounded by the difficulty in quantifying the impact of social media and public sentiment on jury decisions. Insurers must invest in advanced analytics and legal expertise to navigate this complex environment. Failure to adapt to these trends can result in significant underwriting losses and destabilize the market, posing a persistent challenge to long-term sustainability.

Talent Shortage and Underwriting Expertise Gap

A talent shortage and the gap in underwriting expertise are key barriers to the United States liability insurance market. This hinders the ability to assess and price complex risks accurately. The insurance industry faces an aging workforce, with many experienced underwriters approaching retirement age. According to The Institutes (or Free Partners LLP), the industry struggles to attract younger talent due to perceptions of the sector as 'boring' or 'traditional. This demographic shift results in a loss of institutional knowledge and expertise in niche liability lines. As per Deloitte, the complexity of emerging risks, such as cyber and environmental liabilities, requires specialized skills that are in short supply. The lack of qualified underwriters leads to slower policy issuance and potential mispricing of risks, which can result in adverse selection and losses. Insurers must invest heavily in training and development to bridge this gap, which increases operational costs. The competition for talent in the technology and finance sectors further exacerbates the shortage, driving up compensation costs. As per The Jacobson Group and Aon, the demand for experienced insurance underwriters remains high, and they are among the most difficult roles to fill due to a limited pool of qualified candidates. This challenge is particularly acute for smaller insurers who lack the resources to compete for top talent. The inability to secure skilled underwriters limits the capacity of the market to write new business and innovate. Addressing this human capital challenge is critical for the industry to maintain its competitiveness and ability to manage evolving liability exposures effectively.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.18% |

| Segments Covered | By Type, Distribution Channel, End User, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | The Travelers Companies Inc., The Hartford Financial Services Group Inc., Chubb Limited, American International Group Inc., Liberty Mutual Insurance, Zurich Insurance Group, Allianz SE, AXA SA, CNA Financial Corporation, Berkshire Hathaway Inc., The Progressive Corporation, Nationwide Mutual Insurance Company, State Farm Insurance, Tokio Marine Holdings Inc., Sompo Holdings Inc... |

SEGMENTAL ANALYSIS

By Type Insights

The commercial general liability insurance segment dominated the United States market and accounted for a substantial share in 2025. This dominance of the segment is driven by the fact that it is a fundamental requirement for business operations and contractual agreements across nearly all industries. Most commercial leases, client contracts, and government permits mandate that businesses carry this coverage to protect against third-party bodily injury and property damage claims. According to a survey by Next Insurance, 90 percent of small business owners lack confidence that they are adequately insured, despite general liability being a core coverage need. This widespread necessity ensures a consistent and broad demand base that sustains the segment's leading position. As per the Insurance Information Institute, general liability premiums constitute a significant portion of commercial multiline packages, reflecting their status as a foundational risk management tool. The versatility of this coverage allows it to apply to diverse scenarios such as slip and fall accidents in retail stores or accidental damage caused by contractors at client sites. Because almost every physical business operation faces these basic risks, the penetration rate of commercial general liability insurance is exceptionally high. Furthermore, lenders often require proof of this insurance before approving business loans, adding another layer of compulsory demand. This structural integration into the fabric of American commerce ensures that commercial general liability remains the largest segment by premium volume. The universal applicability of the coverage means that even during economic downturns, businesses prioritize maintaining this essential protection to remain operational and compliant with legal and contractual obligations. The broad scope of coverage provided by commercial general liability insurance contributes significantly to its market dominance by addressing a wide array of common business risks. This policy type covers legal costs and settlements arising from allegations of negligence, advertising injury, and personal injury, which are frequent occurrences in daily business activities. The comprehensive nature of general liability policies makes them an attractive first line of defense for business owners who seek to mitigate multiple risks under a single premium. As per Chubb, the flexibility of these policies allows for customization through endorsements that address specific industry needs, further enhancing their appeal. For instance, restaurants can add coverage for foodborne illness, while retailers can include protection for product completion operations. This adaptability ensures that the policy remains relevant across various sectors, including construction, healthcare, and professional services. The ability to bundle general liability with other coverages, such as property insurance, in a business owner’s policy also drives adoption by simplifying the purchasing process and reducing administrative burdens. Insurers benefit from the economies of scale associated with writing these standardized policies, which allows them to offer competitive pricing. The combination of broad protection and cost efficiency solidifies commercial general liability as the cornerstone of the US liability insurance market.

The cyber liability insurance segment is predicted to witness the highest CAGR of 16.4% from 2026 to 2034 due to the surging frequency and severity of cyberattacks that threaten businesses of all sizes. As digital transformation accelerates, organizations become increasingly vulnerable to data breaches, ransomware, and phishing schemes that can result in substantial financial losses. According to the IBM Cost of a Data Breach Report 2024, the average cost of a data breach in the United States was $9.36 million in 2024, decreasing slightly from $9.48 million in 2023 but remaining the highest in the world. This escalating financial impact compels companies to seek insurance solutions that can cover incident response, legal fees, and regulatory fines. As per the Verizon 2024 Data Breach Investigations Report, 68 percent of breaches involved the non-malicious human element, such as error or social engineering, holding steady as a primary driver of incidents. The rising sophistication of cybercriminals means that traditional security measures are often insufficient, making insurance a critical component of risk management. High-profile attacks on major corporations have raised awareness among board members and executives about the potential reputational and financial damage of cyber incidents. Consequently, businesses are prioritizing cyber liability policies to ensure they have the resources to recover quickly from such events. The growth in remote work has further expanded the attack surface, creating new vulnerabilities that insurers are addressing through specialized products. This heightened threat landscape ensures that cyber liability insurance continues to experience robust growth as organizations seek to transfer the financial risk associated with digital threats. Stringent regulatory pressure and evolving compliance requirements are key drivers fueling the rapid expansion of the cyber liability insurance segment. Governments at both the federal and state levels are implementing stricter data privacy laws that impose heavy penalties for non-compliance and data mishandling. According to the National Conference of State Legislatures, over 100 data privacy and security bills were introduced across various states in recent years, creating a complex regulatory environment for businesses. The California Consumer Privacy Act and similar legislation in other states require companies to implement robust data protection measures and notify individuals of breaches, processes that are costly and legally complex. As per the Federal Trade Commission, enforcement actions related to data privacy have increased, resulting in significant fines for companies that fail to protect consumer information. Cyber liability insurance helps organizations manage these compliance costs by covering legal defense expenses and regulatory fines where permitted by law. The uncertainty surrounding liability in the event of a breach makes insurance an attractive option for risk mitigation. Additionally, industry-specific regulations such as HIPAA for healthcare and GLBA for finance mandate strict data security standards, further driving demand for specialized cyber coverage. Insurers are responding by offering policies that include compliance support and regulatory defense coverage. This regulatory tailwind ensures that cyber liability insurance remains a high-growth area as businesses strive to navigate the intricate landscape of data privacy laws and avoid severe financial penalties.

By Distribution Channel Insights

The brokers and intermediaries segment led the US liability insurance market and captured a significant share in 2025. This leading position of the segment is attributed to its specialized expertise in assessing complex risks and placing coverage with appropriate carriers. Liability insurance often involves nuanced policy terms and exclusions that require professional interpretation to ensure adequate protection. According to The Council of Insurance Agents & Brokers' Q4 2025 Commercial Property/Casualty Market Survey, average premium increases moderated to 0.2%, reflecting a softening market rather than specific client preference data, which is typically tracked by separate consumer satisfaction studies. This preference is particularly strong in sectors such as construction, healthcare, and manufacturing, where risks are highly specialized. As per Marsh McLennan, brokers provide valuable risk management services that go beyond simple policy placement, including loss control analysis and claims advocacy. These added services enhance the value proposition for clients who seek comprehensive support in managing their liability exposures. The ability of brokers to access multiple markets allows them to compare options and secure competitive pricing for their clients, which is difficult to achieve through direct channels. Furthermore, the relationships between brokers and insurers facilitate smoother underwriting processes and faster policy issuance. In an environment where social inflation and nuclear verdicts are increasing claim costs, the guidance of experienced brokers is crucial for ensuring that coverage limits are sufficient. This reliance on professional advice sustains the dominant position of brokers in the liability insurance distribution landscape. The establishment of trust and long-term client relationships is a fundamental factor driving the dominance of brokers in the liability insurance distribution channel. Liability insurance is a critical component of business continuity, and companies prefer to work with trusted advisors who understand their unique operational risks and history. According to a study by J.D. Power, customer satisfaction in commercial insurance is heavily influenced by the quality of the relationship with the agent or broker. Clients value the personalized service and consistent support that brokers provide, especially during the claims process when timely assistance is vital. As per Applied Systems, agencies that focus on building strong client relationships experience higher retention rates and increased cross-selling opportunities. The complexity of liability claims often requires ongoing communication and negotiation, roles that brokers are well-suited to fulfill. Businesses appreciate having a dedicated point of contact who can advocate for their interests with insurers. This level of service is difficult to replicate through automated or direct sales channels, particularly for mid-sized and large enterprises. The trust built over time also allows brokers to proactively advise clients on emerging risks and coverage gaps, further cementing their role as essential partners in risk management. This relational dynamic ensures that brokers remain the preferred distribution channel for liability insurance, maintaining their market leadership despite the rise of digital alternatives.

The online platforms and digital direct channels segment is estimated to register the fastest CAGR of 9.2% during the forecast period, owing to the convenience and speed they offer in policy procurement. Small business owners and freelancers increasingly prefer the ability to purchase insurance instantly without the need for lengthy consultations or paperwork. These platforms allow users to obtain quotes, customize coverage, and bind policies in minutes, significantly reducing the time and effort required compared to traditional methods. The automation of underwriting processes enables insurers to offer competitive pricing by reducing administrative costs. This efficiency appeals to price-sensitive customers who value quick transactions. The integration of artificial intelligence and data analytics allows online platforms to assess risks accurately and provide instant decisions, enhancing the customer experience. Furthermore, the availability of these platforms on mobile devices enables users to manage their policies on the go, adding to the convenience. As digital natives enter the business world, their preference for online interactions further accelerates the growth of this channel. The ability to scale rapidly and reach a broad audience makes online platforms a powerful driver of market expansion. Transparency and comparative shopping capabilities inherent in online platforms are significant drivers of their rapid growth in the liability insurance market. Digital aggregators and direct insurer websites provide clear information about coverage options, exclusions, and pricing, empowering consumers to make informed decisions. Online platforms allow users to compare multiple quotes side by side, ensuring they receive the best value for their needs. This clarity is particularly important for liability insurance, where terms can be complex and misleading. The elimination of information asymmetry encourages competition among insurers, leading to more innovative and affordable products. Customers appreciate the ability to review policy documents digitally and access support through chatbots or online resources. This self-service model appeals to independent professionals and small business owners who prefer to manage their own insurance needs. The data collected through these platforms also enables insurers to refine their offerings and target specific customer segments more effectively. The combination of transparency and empowerment ensures that online platforms continue to gain market share as a preferred distribution channel.

By End User Insights

The corporate sector held the majority share of 48.1% of the US liability insurance market in 2025. This supremacy of the segment is credited to its extensive operational exposures and the critical need for asset protection. Large corporations face a wide range of liability risks, including product liability, environmental damage, and employment practices issues that can result in substantial financial losses. The scale of corporate operations means that even minor incidents can escalate into major lawsuits, necessitating high-limit policies. The presence of valuable assets and brand reputation makes corporations targets for litigation, further increasing the demand for comprehensive coverage. Directors and officers liability insurance is also a major driver within this segment, as corporate leaders seek protection against personal liability for management decisions. The regulatory scrutiny faced by large companies in sectors such as finance and healthcare adds to the need for robust liability protection. Corporations also engage in mergers and acquisitions, which require specialized liability coverage for transaction-related risks. The sheer size and complexity of corporate entities ensure that they remain the largest consumers of liability insurance. Their ability to absorb higher premiums in exchange for broader coverage and specialized services sustains the dominance of this segment in the market. Regulatory mandates and stakeholder expectations significantly drive the dominance of the corporate sector in the liability insurance market. Publicly traded companies are subject to strict regulatory requirements that necessitate certain types of liability coverage to protect shareholders and stakeholders. Investors and boards of directors expect companies to have adequate insurance in place to mitigate potential financial shocks from legal claims. Customers and partners also expect corporations to carry sufficient liability coverage as a sign of financial stability and reliability. This expectation is particularly strong in supply chains where contractors and vendors require proof of insurance before engaging in business. The pressure to maintain corporate social responsibility leads companies to invest in coverage for issues such as pollution and employment practices. These external pressures create a consistent demand for liability insurance among corporate entities. The need to comply with international regulations further expands the scope of coverage required by multinational corporations. This combination of regulatory compliance and stakeholder assurance ensures that the corporate sector remains the primary driver of the liability insurance market.

The non-profit organizations segment is anticipated to witness the fastest CAGR of 6.3% between 2026 and 2034. This quick surge of the segment is propelled by increasing litigation risks and the specific liabilities associated with volunteer activities. As nonprofits expand their services and community engagement, they face greater exposure to claims related to bodily injury, property damage, and professional errors. Volunteers, while essential, may lack the training and experience of paid employees, raising the potential for accidents and mistakes. Directors and officers of nonprofits are also facing increased personal liability, prompting organizations to purchase protection for their leadership teams. The reliance on public donations and grants means that non-profits must demonstrate prudent risk management to maintain funding, further encouraging insurance adoption. High-profile cases involving nonprofits have raised awareness about the importance of liability protection. Insurers are responding by developing tailored policies that address the unique needs of charities, educational institutions, and religious organizations. This growing recognition of risk among non-profit leaders ensures that this segment continues to expand at a rapid pace. Grant requirements and funding compliance are key factors driving the rapid growth of liability insurance among non-profit organizations. Many government agencies and private foundations require nonprofits to carry specific types and levels of liability insurance as a condition for receiving grants and contracts. This financial imperative compels non-profits to prioritize insurance purchases even when budgets are tight. The complexity of grant requirements often necessitates specialized coverage, such as abuse and molestation insurance or event liability. Nonprofits operating in multiple states or countries must navigate varying regulatory landscapes, further driving the need for comprehensive policies. The desire to protect restricted funds and assets from legal claims also motivates nonprofits to secure robust liability coverage. Insurers are offering flexible payment options and bundled packages to accommodate the budget constraints of non-profits. The alignment of insurance coverage with funding requirements ensures that this segment experiences sustained growth. The non-profit sector is becoming more professionalized and regulated. As a result, the demand for liability insurance will continue to rise.

REGIONAL ANALYSIS

The United States remained the top performer in the global liability insurance market and occupied a 45.6% share in 2025. This leading position of the segment is driven by the country’s highly litigious legal environment, complex regulatory framework, and advanced insurance infrastructure. According to OECD-referenced data from the World Justice Project's 2024 Rule of Law Index, the United States ranks 26th globally in civil justice, reflecting a system where significant litigation costs in specific sectors drive demand for liability coverage, despite not having the highest overall rate of civil litigation among developed nations. The market status is characterized by a mature and competitive landscape with numerous domestic and international insurers offering a wide range of products. As per the National Association of Insurance Commissioners, the US liability insurance sector demonstrates resilience and adaptability, consistently innovating to address emerging risks such as cyber threats and climate change. The presence of major reinsurance hubs and legal centers further strengthens the market’s global influence. The depth of the capital markets allows US insurers to secure substantial capacity for large and complex liability risks. Regulatory oversight by state insurance departments ensures consumer protection and market stability. The cultural emphasis on individual rights and accountability fuels the continuous evolution of liability laws, which in turn drives insurance demand. The United States serves as a trendsetter for global liability insurance practices, with innovations in policy wording and risk management often originating in this market. The strong economic foundation and diverse industrial base provide a steady stream of premium income. This combination of legal, economic, and structural factors ensures that the United States remains the central pillar of the global liability insurance industry.

COMPETITION OVERVIEW

The competition in the United States liability insurance market is intense and characterized by a mix of large multinational carriers and specialized niche providers. Major insurers compete based on financial strength, underwriting expertise, and product diversity to attract corporate and individual clients. The market sees frequent innovation as companies strive to address emerging risks such as cyber liability and environmental damage. Price competition is significant but often secondary to the quality of service and claims handling efficiency. Insurers are increasingly differentiating themselves through digital capabilities, offering seamless online experiences and rapid policy issuance. Strategic partnerships with technology firms are common as carriers seek to leverage data analytics for better risk assessment. The presence of insurtech startups adds pressure on traditional players to modernize their operations and improve customer engagement. Regulatory compliance also plays a crucial role in shaping competitive dynamics, with companies investing heavily in adherence to state and federal laws. Mergers and acquisitions are frequent as larger firms seek to consolidate market position and acquire specialized expertise. This dynamic environment requires continuous adaptation and investment to maintain relevance and profitability in the face of evolving customer expectations and legal landscapes.

KEY MARKET PLAYERS

A few major players of the United States liability insurance market include

- The Travelers Companies Inc.

- The Hartford Financial Services Group Inc

- Chubb Limited

- American International Group Inc

- Liberty Mutual Insurance

- Zurich Insurance Group

- Allianz SE

- AXA SA

- CNA Financial Corporation

- Berkshire Hathaway Inc

- The Progressive Corporation

- Nationwide Mutual Insurance Company

- State Farm Insurance

- Tokio Marine Holdings Inc

- Sompo Holdings Inc

Top Strategies Used by Key Market Participants

Key players in the United States liability insurance market employ several major strategies to maintain competitiveness and drive growth. Product innovation is central to these efforts, with insurers developing specialized coverage for emerging risks such as cyber threats and climate change. Digital transformation is another critical strategy involving the adoption of artificial intelligence and machine learning to enhance underwriting accuracy and claims efficiency. Companies are also focusing on customer experience by creating user-friendly online platforms that simplify policy purchase and management. Strategic mergers and acquisitions allow insurers to expand their capabilities and enter new market segments rapidly. Additionally, firms are investing in risk management services to help clients prevent losses and reduce claim frequency. Partnerships with technology providers enable the integration of real-time data into risk assessment models. These combined strategies ensure that insurers can adapt to evolving market dynamics and meet the diverse needs of policyholders effectively.

Leading Players in the Market

- Chubb Limited stands as a premier provider of liability insurance solutions globally with a strong presence in the United States market. The company offers comprehensive coverage options, including general professional and cyber liability, tailored to diverse industry needs. Chubb leverages its extensive underwriting expertise to assess complex risks accurately and provide customized policies for corporate and individual clients. Recent actions include the expansion of its cyber insurance capabilities through enhanced digital tools and risk management services. The company has also invested in artificial intelligence to streamline claims processing and improve customer experience. Chubb actively engages in strategic partnerships with technology firms to develop innovative products that address emerging liabilities. These initiatives strengthen its market position by delivering superior value and responsiveness to clients. The organization continues to focus on sustainable growth by maintaining disciplined underwriting standards while expanding its product portfolio. This approach ensures long-term stability and competitiveness in the evolving liability insurance landscape.

- Allianz SE is a global financial services leader with a significant footprint in the United States liability insurance sector. The company provides a wide array of liability products ranging from commercial general liability to specialized professional indemnity coverage. Allianz utilizes its vast global network to support multinational corporations with cross-border risk management solutions. Recent efforts involve the integration of advanced data analytics to enhance risk assessment and pricing accuracy. The company has launched new digital platforms that simplify policy administration and claims handling for business customers. Allianz also focuses on sustainability by offering insurance products that support environmental, social, and governance goals. These actions reinforce its reputation for innovation and reliability in the market. By prioritizing customer-centric services and technological advancement, Allianz strengthens its competitive edge. The company continues to invest in talent and infrastructure to meet the changing needs of policyholders. This commitment ensures sustained growth and leadership in the global liability insurance industry.

- AXA SA is a major international insurer with a robust presence in the United States liability insurance market. The company delivers comprehensive liability solutions, including directors and officers coverage and cyber liability protection for businesses of all sizes. AXA emphasizes customer engagement through digital transformation initiatives that enhance accessibility and service efficiency. Recent actions include the acquisition of specialized insurance firms to expand its niche capabilities in professional and financial lines. The company has also developed proprietary risk modeling tools to better predict and manage liability exposures. AXA collaborates with industry partners to create holistic risk management frameworks that address complex client needs. These strategies bolster its market position by offering differentiated products and superior service quality. The organization remains committed to innovation by investing in technology and data science. This focus enables AXA to adapt quickly to market changes and regulatory developments. Through continuous improvement and strategic expansion, AXA maintains its status as a key player in the global liability insurance sector.

MARKET SEGMENTATION

This research report on the US liability insurance market has been segmented and sub-segmented based on type, distribution channel, end user & region.

By Type

- Employer's Liability Insurance

- Product liability insurance

- Commercial liability insurance

- Professional Liability Insurance

- Others

By Distribution Channel

- Broker

- Online Platform

- Insurance Agents

- Direct Sales

- Others

By End User

- Corporate

- Government Entities

- Non-Profit Organization

- Others

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What does the U.S. liability insurance market include?

It includes various policies such as general liability, professional liability, product liability, and employer liability insurance.

2. What are the key drivers of the U.S. liability insurance market?

Rising litigation rates, increasing awareness of risk management, and strict regulatory requirements are major growth drivers.

3. Who are the major players in the U.S. liability insurance market?

Leading companies include The Travelers Companies, Chubb, AIG, Liberty Mutual, and The Hartford.

4. What is general liability insurance?

General liability insurance covers claims related to bodily injury, property damage, and advertising injury caused by business operations.

5. What is professional liability insurance?

Also known as errors and omissions (E&O) insurance, it protects professionals against claims of negligence or inadequate service.

6. What industries commonly use liability insurance?

Industries such as healthcare, construction, manufacturing, IT, and finance widely use liability insurance.

7. What are the challenges in the U.S. liability insurance market?

Challenges include increasing claim severity, fraud, regulatory changes, and pricing pressures.

8. What role does regulation play in this market?

Regulations ensure compliance, protect policyholders, and influence coverage requirements and pricing.

9. How is technology impacting liability insurance?

Technologies like AI, big data, and automation improve underwriting, claims processing, and risk assessment.

10. What is the future outlook of the U.S. liability insurance market?

The market is expected to grow steadily due to evolving risks, digital transformation, and increasing demand for specialized coverage.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com