U.S. Lighting Market Size, Share, Trends, and Growth Analysis Report, Segmented by Lighting Type, Location, Connectivity, Installation Type, Distribution Channel, End-User, and Country – Industry Forecast From 2026 to 2034

U.S. Lighting Market Report Summary

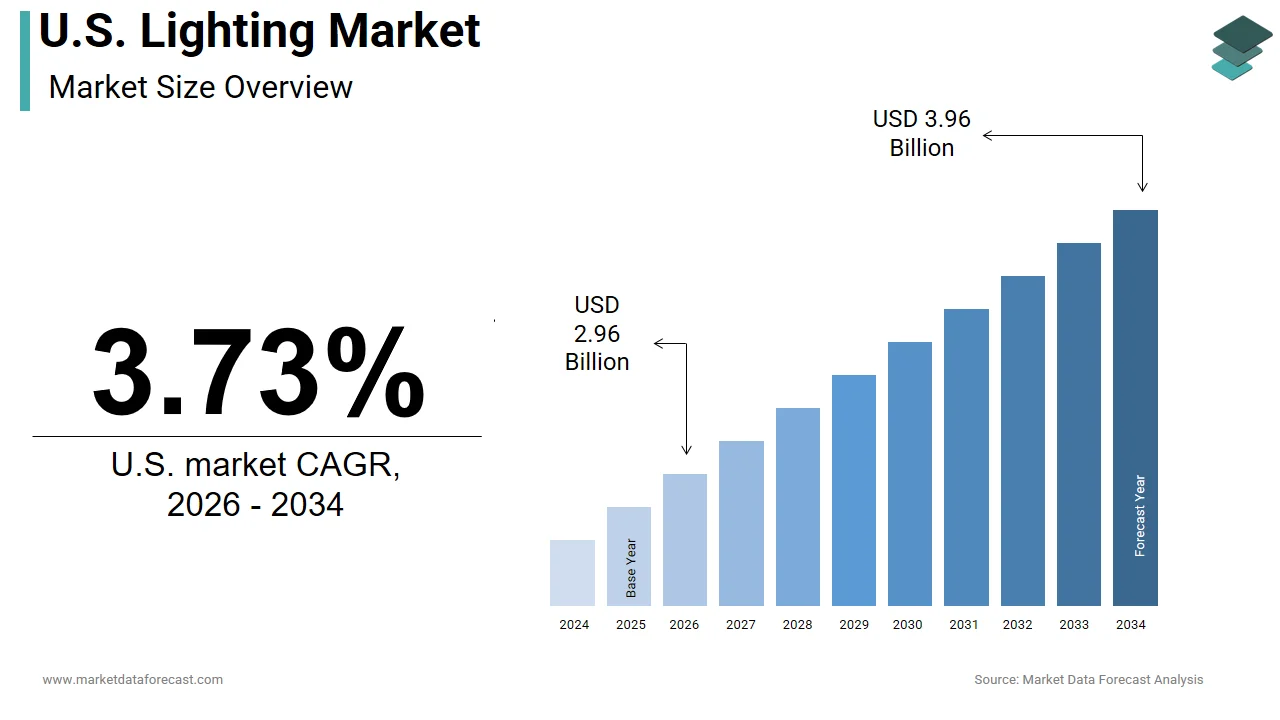

The U.S. lighting market was valued at USD 2.85 billion in 2025, is estimated to reach USD 2.96 billion in 2026, and is projected to reach USD 3.96 billion by 2034, growing at a CAGR of 3.73% from 2026 to 2034. Market growth is driven by increasing adoption of energy-efficient lighting solutions, rising demand for smart lighting systems, and ongoing residential and commercial infrastructure development. Consumers and businesses are increasingly shifting toward LED lighting and connected lighting technologies to reduce energy consumption and improve operational efficiency. Additionally, government regulations promoting sustainable lighting products, advancements in IoT-enabled lighting systems, and rising investments in smart homes and smart buildings are supporting market expansion across the United States.

Key Market Trends

- Rising adoption of energy-efficient LED lighting solutions.

- Increasing demand for smart and connected lighting systems.

- Growth in residential and commercial renovation activities.

- Expansion of IoT-enabled and automated lighting technologies.

- Increasing focus on sustainable and environmentally friendly lighting products.

Segmental Insights

- Based on lighting type, the light bulbs segment dominated the United States lighting market by accounting for 52.4% share in 2025, driven by widespread household and commercial usage.

- Based on connectivity, the wired segment held the leading share in 2025, supported by reliable infrastructure and extensive adoption across residential and commercial applications.

- Based on distribution channel, the offline segment dominated the market in 2025, driven by strong retail presence and consumer preference for in-store product evaluation.

- Based on end user, the residential segment led the market by capturing 47.6% share in 2025, supported by increasing home renovation projects and smart home adoption.

Country-Level Insights

- The United States dominated the North American lighting market by accounting for 80.5% share in 2025, supported by advanced infrastructure development, high consumer spending on smart home technologies, and increasing adoption of energy-efficient lighting systems.

U.S. Lighting Market Size

The U.S. lighting market was valued at USD 2.85 billion in 2025, is estimated to reach USD 2.96 billion in 2026, and is projected to reach USD 3.96 billion by 2034, growing at a CAGR of 3.73% from 2026 to 2034.

Lighting is the deliberate, strategic use of natural light (daylight) or artificial light sources (lamps, fixtures) to illuminate spaces, objects, or scenes to achieve practical visibility, aesthetic, or psychological effects. This market is undergoing a profound transformation driven by the rapid adoption of energy-efficient technologies and smart connectivity features rather than functioning merely as a utility domain. The fundamental necessity for artificial light in built environments ensures consistent demand across all sectors. According to the United States Energy Information Administration, lighting accounts for approximately 11% of total electricity consumption in commercial buildings and roughly 6% in residential homes, establishing a solid baseline for continuing energy savings initiatives. The aging infrastructure of the nation further amplifies the requirement for modernization as older incandescent and fluorescent systems are phased out. As per the Department of Energy, the widespread replacement of traditional bulbs with light-emitting diode (LED) technology, which uses at least 75% less energy than traditional incandescent lighting, has reduced U.S. lighting energy consumption by over 40% compared to previous baseline projections. Additionally, the proliferation of internet-connected devices has led to a steady increase in smart home adoption, with Consumer Technology Association data indicating that while general smart device ownership exceeds 80%, specialized sectors like smart lighting are rapidly expanding to capture nearly a third of American households. This phenomenon has spurred demand for integrated systems that offer remote control automation and color customization. The market is thus defined by a convergence of regulatory mandates, technological innovation, and consumer lifestyle shifts, where purchasing decisions are increasingly influenced by sustainability goals and digital convenience rather than basic illumination needs alone.

MARKET DRIVERS

Stringent Government Regulations and Energy Efficiency Mandates

The implementation of stringent government regulations and energy efficiency mandates serves as a key factor for the expansion of the LED lighting segment within the United States lighting market. Federal and state authorities have enacted policies aimed at reducing carbon emissions and minimizing energy waste in both public and private sectors. According to the Department of Energy, updated efficiency standards mandate a minimum threshold of 45 lumens per watt, effectively phasing out the manufacture and sale of standard general-service incandescent and halogen bulbs while exempting specialized specialty lighting. The Department of Energy estimates that these regulatory updates will save American consumers billions of dollars in utility bills annually while substantially mitigating carbon emissions over the next thirty years. Furthermore, many states have adopted building codes that require high-performance lighting systems in new constructions and major renovations. These legal frameworks create a compulsory market environment where compliance drives procurement decisions regardless of initial cost considerations. Utility companies also offer rebates and incentives for upgrading to certified energy-efficient products, which further accelerate adoption rates. Consequently, manufacturers are compelled to innovate and produce compliant products, ensuring that the market remains dynamic and focused on sustainability. This regulatory landscape ensures a steady and predictable demand for advanced lighting solutions.

Rapid Adoption of Smart Home and Internet of Things Technologies

The rapid adoption of smart home ecosystems and Internet of Things technologies is boosting the growth of connected lighting solutions in the country, which propels the United States lighting market. Consumers are increasingly seeking integrated home automation systems that offer convenience, security, and energy management capabilities through smartphone applications and voice assistants. According to the Consumer Technology Association, factory shipments of smart residential lighting devices continue to post steady year-over-year gains as consumers prioritize integrated home automation and energy management. The integration of lighting with platforms such as Amazon Alexa, Google Assistant, and Apple HomeKit allows for seamless interaction and personalized scheduling. The National Association of Home Builders reports that a significant and growing segment of new home buyers views smart lighting controls as a highly desirable home feature, heavily influencing modern builder configurations and automated electrical layouts. Additionally, the ability of smart lights to mimic natural circadian rhythms supports health and wellness goals by regulating sleep patterns and improving mood. This functional value proposition extends beyond mere aesthetics, driving demand in both consumer and commercial sectors. Furthermore, the decreasing cost of sensors and wireless connectivity modules has made smart lighting more accessible to mainstream audiences. As interoperability between devices improves, the appeal of holistic smart home solutions continues to rise. These technological advancements ensure that the lighting market evolves from a static utility into a dynamic component of modern digital living.

MARKET RESTRAINTS

High Initial Installation Costs for Advanced Systems

The substantial upfront investment required for installing advanced lighting systems, particularly smart and commercial-grade LED fixtures, is a significant restraint to the penetration of the United States lighting market. This is especially true among budget-conscious consumers and small businesses. While long-term operational savings are well documented, the initial purchase price of high-quality LED fixtures and smart controllers remains higher than traditional alternatives. According to the Bureau of Labor Statistics Producer Price Index data, the operational and material input costs for electrical contractors have faced inflationary pressure upward in recent years, driven by a combination of tight skilled-labor markets and fluctuating raw material costs. This financial barrier prevents a substantial segment of the population from upgrading their existing lighting infrastructure despite the potential for energy savings. Research indicates that many small enterprises operate on compressed margins, which frequently compels them to prioritize short-term operational cash flow over long-term capital investments in high-efficiency building upgrades. Consequently, these entities often delay retrofitting projects or opt for cheaper, lower-quality alternatives that may not deliver optimal performance or longevity. Additionally, the complexity of installing smart lighting systems, which may require professional configuration and network integration, adds to the total cost of ownership. The National Electrical Contractors Association indicates that labor remains a primary financial driver in commercial electrical retrofits, frequently constituting the majority share of total project expenditures during comprehensive lighting upgrades. This economic reality limits the speed of market transition and restricts the adoption of premium features. Manufacturers face the challenge of reducing production costs while maintaining quality to make these products more affordable. The high initial cost will continue to hinder widespread market expansion. This will remain true until price parity is achieved with traditional options.

Technical Complexity and Interoperability Issues

The technical complexity associated with smart lighting systems and the lack of universal interoperability standards are hampering consumer confidence and the growth of the United States lighting market. Many consumers find the setup process for connected lighting devices confusing and frustrating due to incompatible protocols and fragmented ecosystems. Studies indicate that seamless onboarding and long-term connection reliability are paramount for smart home adoption, with a significant segment of users abandoning devices that suffer from persistent pairing or network setup failures. The Consumer Technology Association underscores that configuration challenges and ecosystem interoperability problems remain leading contributors to retail return rates for smart home hardware. This fragmentation creates uncertainty for buyers who fear investing in a system that may become obsolete or incompatible with future devices. Additionally, the reliance on stable Wi Fi networks and hubs introduces points of failure that can disrupt functionality. These technical barriers deter less tech-savvy consumers from adopting smart lighting solutions. Until industry-wide standards are fully implemented and user interfaces are simplified, the market will face resistance from users seeking hassle-free experiences. This complexity limits the addressable market to early adopters and tech enthusiasts.

MARKET OPPORTUNITIES

Integration of Human Centric Lighting in Healthcare and Education

The integration of human-centric lighting systems in healthcare and educational facilities paves the way for growth in the United States lighting market. Human-centric lighting mimics the natural progression of daylight to support circadian rhythms, improve sleep quality, and enhance overall well-being. Standards published by the Illuminating Engineering Society note that peer-reviewed clinical and academic research demonstrates that exposure to optimized light spectra can significantly reduce patient recovery times and improve student concentration levels. Healthcare facility design trends show that a growing percentage of hospitals are piloting or deploying specialized circadian-supportive lighting systems to help align patient biological rhythms and foster staff alertness. This trend is driven by growing evidence linking light exposure to mental health and cognitive performance. Guidelines from the Collaborative for High Performance Schools emphasize that integrating advanced, dynamic lighting control systems creates high-quality visual environments that positively correlate with student reading comprehension and cognitive performance. These tangible benefits create a compelling value proposition for institutional buyers who prioritize health and productivity. Furthermore, government grants and funding initiatives support the modernization of public infrastructure, including schools and hospitals. Federal and state agency initiatives provide funding frameworks and guidance for modernizing school facilities, which frequently prioritize energy-efficient lighting upgrades to reduce utility overhead. As awareness of the biological impacts of light grows, the demand for tunable and adaptive lighting solutions in sensitive environments will expand. Manufacturers who specialize in high-quality spectrally tuned fixtures can capture this niche but high-value segment. This shift represents a move towards lighting as a health intervention rather than just a visual tool.

Expansion of Li Fi Technology for Data Transmission

The emergence of Light Fidelity or Li Fi technology offers a lucrative opportunity for innovation in the United States lighting market. This enables high-speed data transmission through visible light. Li Fi uses LED bulbs to transmit data at speeds comparable to or exceeding traditional Wi Fi, offering enhanced security and reduced interference. According to technical standards ratified by the Institute of Electrical and Electronics Engineers (IEEE 802.11bb), Li-Fi technology can seamlessly integrate with existing wireless infrastructure, while advanced laboratory models utilizing laser diodes have demonstrated experimental throughputs reaching 100 gigabits per second. This technology is particularly attractive for environments where radio frequency interference is a concern, such as hospitals, aircraft, and industrial facilities. Aerospace manufacturers and airlines are actively developing Li-Fi systems for in-flight entertainment and cabin connectivity, leveraging light's inherent immunity to electromagnetic and radio-frequency interference. Additionally, the inherent security of light-based transmission, which cannot pass through walls, makes it ideal for sensitive government and corporate applications. As the demand for bandwidth increases with the proliferation of Internet of Things devices, Li Fi provides a scalable solution that utilizes existing lighting infrastructure. Major telecommunications companies are partnering with lighting manufacturers to develop integrated systems. By transforming light fixtures into data access points, manufacturers can open new revenue streams and differentiate their products in a crowded market. This convergence of lighting and communications represents a frontier for technological advancement.

MARKET CHALLENGES

Supply Chain Volatility and Semiconductor Shortages

Persistent supply chain disruptions and shortages of critical semiconductors pose a significant obstacle to the manufacturing sector within the United States lighting market. Consequently, these issues threaten the stability and profitability of manufacturers. The production of LED drivers and smart lighting controllers relies heavily on chips, which are subject to global supply constraints. Research shows that lead times for critical power management integrated circuits (PMICs) extended dramatically during recent global shortages, severely disrupting manufacturing schedules across multiple electronics sectors. These delays result in inventory stockouts and an inability to meet consumer demand, particularly during peak construction seasons. Bureau of Labor Statistics Producer Price Index data reflects that domestic manufacturers faced sharp cost increases for electronic components and accessories during recent supply chain disruptions, squeezing production margins. These cost increases are often difficult to pass on to consumers in a highly competitive market, leading to compressed margins. Additionally, geopolitical tensions and trade policies affect the availability of rare earth elements used in phosphors and magnets. The United States Geological Survey reports that the nation remains heavily reliant on foreign imports for raw critical minerals and rare-earth elements, leaving domestic high-tech manufacturing chains vulnerable to upstream supply shocks. Manufacturers relying on just-in-time inventory systems have faced significant operational challenges forcing them to hold larger safety stocks, which ties up capital. Furthermore, the concentration of manufacturing in specific regions creates vulnerability to local disruptions such as natural disasters or labor strikes. These factors create uncertainty in production planning and pricing strategies, making it difficult for companies to maintain consistent product availability. Thus, the industry faces headwinds that hinder growth and customer satisfaction.

Environmental Concerns Regarding Electronic Waste

The increasing volume of electronic waste generated by discarded lighting fixtures, particularly those containing complex electronics and batteries, is a significant environmental challenge for the United States lighting market. Unlike traditional bulbs, LED fixtures and smart lights contain printed circuit boards, microcontrollers, and sometimes lithium-ion batteries, which are difficult to recycle. According to data from the Environmental Protection Agency, despite continuous improvements in electronic waste collection infrastructure, billions of pounds of consumer electronics still bypass secondary recovery systems and end up in municipal landfills annually. The presence of hazardous materials such as lead and mercury in some components poses risks to soil and water quality. State-level frameworks, particularly in California and New York, continue to evolve by expanding Extended Producer Responsibility (EPR) requirements and stricter hazardous waste rules governing the commercial lifecycle and recycling of electronic lighting products. The Resource Conservation and Recovery Act mandates strict end-to-end management of hazardous waste materials, which requires electronics manufacturers to maintain rigorous operational compliance and specialized disposal protocols. Additionally, the lack of standardized recycling infrastructure for lighting products complicates end-of-life management. Consumers are increasingly holding brands accountable for their environmental impact, which adds pressure to adopt circular economy principles. Designing products for easy disassembly and recyclability requires significant investment in research and development. Balancing regulatory compliance with cost efficiency and product performance remains a difficult task for industry participants. This environmental burden threatens the sustainability credentials of the lighting industry.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Lighting Type, Location, Connectivity, Installation Type, Distribution Channel, End-User, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Lutron Electronics Co., Inc., Koncept Inc., OttLite, Herman Miller, Inc., Acuity Brands, Inc., Cree Lighting, Hubbell Incorporated, Eaton Corporation, GE Lighting, a Savant Company, Cooper Lighting Solutions, Kichler Lighting LLC, Leviton Manufacturing Co., Inc., Progress Lighting, RAB Lighting Inc., and Others. |

SEGMENTAL ANALYSIS

By Lighting Type Insights

In 2025, the light bulbs segment dominated the United States lighting market by accounting for a 52.4% share. This dominance of the segment was driven by its universal applicability and the continuous need for replacement across residential and commercial sectors. Unlike fixed fixtures, which are installed for long periods, bulbs are consumable items that require periodic replacement due to burnout or technological upgrades. According to data from the United States Energy Information Administration, there are over 131 million households in the country, with each home utilizing an average of nearly 45 light sockets, which creates an expansive baseline market for replacement bulbs. The Department of Energy enforces strict minimum efficacy standards that have effectively transitioned the general-service market away from inefficient incandescent bulbs, driving widespread consumer adoption of energy-saving LED replacement options. Furthermore, the low unit cost of bulbs compared to fixtures makes them an accessible entry point for consumers seeking to upgrade their lighting systems without significant capital expenditure. The National Electrical Manufacturers Association shipment indices confirm that LED bulbs have long established total market dominance, commanding the overwhelming majority of consumer lamp shipments over legacy technologies. This high volume of transactions sustains the dominance of the bulb segment as manufacturers leverage economies of scale to offer competitive pricing. The ease of installation without professional assistance further encourages DIY replacements. Consequently, the bulb segment remains the backbone of the lighting industry, driven by regulatory pressure and the inherent consumable nature of the product.

In addition, the domination of the light bulb segment is further reinforced by the compelling economic argument for energy efficiency, which drives consumers to replace older bulbs with LED variants. LEDs consume less energy than incandescent bulbs and last 25 times longer, resulting in substantial cost savings for households and businesses. This financial incentive is a primary driver for procurement decisions, particularly in times of rising utility costs. Additionally, commercial entities are motivated by corporate sustainability goals and tax incentives for reducing carbon footprints. As awareness of these benefits grows, the replacement cycle accelerates, ensuring sustained demand for high-efficiency bulbs. Manufacturers continue to innovate with higher lumen outputs and better color rendering indices to meet diverse needs. These factors collectively ensure that light bulbs remain the dominant product type in the market.

But the ceiling lights segment is expected to exhibit a noteworthy CAGR of 6.5% from 2026 to 2034. This quick surge of the segment is primarily propelled by the integration of smart technology and home automation features into ceiling-mounted fixtures. Consumers are increasingly seeking centralized lighting solutions that can be controlled via smartphones, voice assistants, and automated schedules. The Consumer Technology Association indicates that shipments of smart ceiling fans and integrated LED downlights continue to see steady year-over-year growth as households expand their connected home ecosystems. Ceiling lights serve as ideal hubs for smart sensors such as motion detectors and ambient light sensors, which enhance energy efficiency and convenience. The National Association of Home Builders reports that residential developers are increasingly integrating neutral-wire electrical layouts and automated control provisions into new construction projects to satisfy consumer demand for smart-home compatibility. Additionally, the aesthetic appeal of sleek minimalist ceiling designs aligns with modern interior design trends favoring clean lines and uncluttered spaces. The ability to adjust color temperature and brightness remotely adds functional value that traditional bulbs cannot provide. Major manufacturers are investing in proprietary wireless protocols to ensure seamless connectivity with popular platforms like Alexa and Google Home. These innovations transform ceiling lights from static fixtures into dynamic components of the smart home, driving rapid adoption and revenue growth in this segment.

A further key factor driving the rapid growth of the ceiling lights segment is the ongoing trend towards home renovations and modern interior design preferences that prioritize ambient and task lighting. Homeowners are investing in upgrading outdated chandeliers and flush mounts with contemporary LED ceiling fixtures that offer better illumination and style. Ceiling lights are often the focal point of room design, influencing the overall aesthetic and perceived spaciousness. The versatility of ceiling fixtures allows for customization in kitchens, bathrooms, and living areas where functionality and mood setting are crucial. Additionally, the durability and low maintenance requirements of modern LED ceiling units appeal to busy households. Retailers are expanding their offerings of designer ceiling lights to cater to diverse tastes, from industrial to farmhouse styles. The availability of dimmable and tunable white options further enhances the appeal of ceiling fixtures for creating versatile living environments. As renovation activity remains robust, the ceiling lights segment continues to experience strong growth driven by aesthetic and functional upgrades.

By Connectivity Insights

The wired connectivity segment led the United States lighting market and captured a significant share in 2025. This leading position of the segment was driven by its unparalleled reliability and stability, which are critical for commercial and industrial applications. Wired systems, such as those using Ethernet or dedicated control wires, do not suffer from signal interference or connectivity drops associated with wireless technologies. According to life safety and building codes, dedicated emergency power circuits are mandated for safety-critical illumination in hospitals, schools, and public buildings to ensure uncompromised operation during power interruptions. International Electrotechnical Commission standards provide the rigorous technical frameworks required for resilient lighting control networks, ensuring high-reliability data transmission across mission-critical commercial and industrial infrastructure. Commercial facility managers prefer wired systems because they offer predictable performance and easier troubleshooting compared to complex wireless networks. Additionally, wired systems can support higher power loads and longer transmission distances without the need for repeaters or signal boosters. This makes them ideal for large warehouses, manufacturing plants, and outdoor street lighting applications. The initial installation cost may be higher, but the lower maintenance and higher uptime justify the investment for enterprise users. Consequently, the wired segment maintains its leadership by serving the backbone of the nation's lighting infrastructure, where reliability is paramount.

Moreover, the leadership of the wired connectivity segment is further reinforced by the established electrical infrastructure and professional installation standards that dominate the construction industry. Electricians and contractors are trained extensively in wired systems, making them the default choice for new constructions and major renovations. This familiarity reduces labor costs and installation time for wired projects. Existing buildings are already equipped with extensive wiring harnesses, which makes retrofitting with wired smart controls more feasible than deploying entirely new wireless systems. Furthermore, wired systems offer superior security as they are not vulnerable to remote hacking or unauthorized access via Wi Fi. These structural and regulatory factors ensure that wired connectivity remains the preferred solution for professional and institutional lighting applications, sustaining its market dominance.

On the contrary, the wireless connectivity segment is predicted to witness the highest CAGR of 12.8% during the forecast period. This rapid growth is fuelled by the ease of installation and the convenience it offers for retrofitting existing spaces without extensive rewiring. Wireless systems use protocols such as Zigbee, Z-Wave, and Bluetooth Mesh, which allow fixtures to communicate without physical control wires. According to the Connectivity Standards Alliance, millions of certified wireless lighting devices are deployed globally every year as commercial and residential users prioritize flexible, scalable, and interoperable control platforms. The ability to add or move lights without drilling walls or running cables appeals to renters and homeowners who want to avoid invasive construction. Research indicates that non-invasive, plug-and-play wireless smart upgrades are highly attractive to modern renters, allowing tenants to customize their living spaces without modifying permanent property infrastructure. Wireless systems also enable easy expansion, allowing users to add new fixtures to the network seamlessly. This flexibility is particularly attractive for small businesses and startups that may change layouts frequently. The reduction in labor costs associated with wireless installation makes it a cost-effective alternative to wired systems for many applications. As technology improves, the reliability of wireless connections has increased, addressing previous concerns about latency and dropouts. These advantages drive the rapid adoption of wireless lighting in both residential and commercial sectors.

A different factor accelerating the growth of wireless connectivity is its seamless integration with smart home ecosystems and mobile control platforms. Consumers increasingly demand lighting that can be controlled via smartphones, tablets, and voice assistants for enhanced convenience and personalization. Wireless lighting systems easily connect to hubs and routers, enabling remote access and automation features such as scheduling and geofencing. Users can create custom scenes, adjust colors, and monitor energy usage from anywhere in the world. This level of control appeals to tech-savvy demographics who view lighting as part of a broader digital lifestyle. Additionally, wireless systems support over-the-air updates, which allow manufacturers to add new features and improve performance without physical intervention. The data collected from wireless sensors can also be used to optimize energy consumption and enhance user experience. As artificial intelligence becomes more prevalent in home automation, wireless lighting will play a central role in creating responsive and intuitive living environments. This technological synergy ensures the continued rapid expansion of the wireless segment.

By Distribution Channel Insights

The offline distribution segment held the majority share of the United States lighting market in 2025 because of the immediate availability of products and the ability for customers to physically inspect them. Lighting is a tactile product where brightness, color temperature, and build quality are best assessed in person. Large retailers like Home Depot, Lowe's, and Ace Hardware offer extensive inventories that allow customers to take products home immediately, satisfying urgent repair or renovation needs. Additionally, professional contractors and electricians rely on local suppliers for quick access to materials during job sites, ensuring project timelines are met. The expertise of in-store staff who can provide advice on compatibility and installation further enhances the value of offline channels. Many stores also offer services such as bulb recycling and fixture assembly, which add convenience for shoppers. The trust established through face-to-face interactions and the ability to return items easily reduce perceived risk. These factors collectively sustain the dominance of offline channels as the primary source for lighting products.

Moreover, the leadership of the offline distribution segment is further reinforced by the strong relationships between retailers and professional contractors who purchase lighting in bulk for commercial and residential projects. Contractors often require specialized advice and volume discounts that are readily available through established trade counters at hardware stores. Offline retailers offer credit accounts and delivery services that facilitate large-scale procurement for construction sites. The ability to negotiate prices and secure specific brands or models in person is crucial for meeting project specifications and budgets. Additionally, trade shows and industry events hosted by offline distributors provide opportunities for professionals to discover new products and technologies. These events foster networking and education, which strengthen loyalty to specific retail partners. The personalized service and logistical support provided by offline channels create a barrier to entry for pure play online retailers in the professional segment. Consequently, the offline channel maintains its leading position by catering to the specific needs of industry professionals who drive substantial volume sales.

But the online distribution segment is estimated to register the fastest CAGR of 9.2% between 2026 and 2034 due to the convenience of shopping from home and the wide variety of products available on e-commerce platforms. Consumers can browse thousands of styles, compare prices, and read reviews without leaving their homes. Online retailers like Amazon, Wayfair, and Build.com offer niche and designer brands that may not be available in local stores. The ability to filter searches by size, color, and price helps consumers find exactly what they need quickly. Additionally, online platforms often provide detailed product descriptions and installation guides, which help users make informed decisions. The convenience of home delivery eliminates the need to transport bulky fixtures from stores. As logistics networks become more efficient, delivery times have decreased, making online shopping a viable option for urgent needs. These factors collectively fuel the rapid growth of the online channel as consumers increasingly prefer digital convenience.

The quick growth is pushed by the use of advanced visualization tools and personalized recommendations that enhance the shopping experience. Augmented reality applications allow users to visualize how lighting fixtures will look in their spaces using smartphone cameras. This innovation reduces uncertainty and lowers return rates for online lighting purchases. Artificial intelligence algorithms analyze browsing history to suggest complementary products and styles tailored to individual preferences. Online retailers also offer virtual design consultations where experts help customers plan lighting layouts remotely. These services mimic the in-store experience while leveraging digital scalability. Social media integration allows users to share ideas and get feedback from communities, further influencing purchasing decisions. The ease of comparing technical specifications and energy ratings online empowers consumers to choose efficient and suitable products. As technology advances, the online shopping experience becomes more immersive and informative, attracting a broader audience. This strategic use of digital tools ensures that online channels continue to outpace traditional retail in growth rate.

By End User Insights

The residential end-user segment was the largest by occupying a 47.6% share of the United States lighting market in 2025. This prominence of the segment was supported by the sheer volume of housing units and the frequent replacement cycles of lighting products in homes. Residential lighting includes a mix of general illumination, task lighting, and decorative fixtures, which are replaced more frequently than commercial installations due to changing trends and wear. The rise of DIY culture, encouraged by online tutorials and social media, has empowered residents to undertake lighting projects themselves, driving retail sales. Additionally, the emotional connection to home aesthetics motivates consumers to update lighting to match interior design changes. The prevalence of smart home adoption in residential settings further boosts demand for connected bulbs and fixtures. Manufacturers target this segment with affordable and stylish options that appeal to broad demographics. Consequently, the residential segment remains the largest contributor to market revenue, driven by volume and frequency of purchases.

Furthermore, the domination of the residential segment is further reinforced by the growing consumer focus on energy savings and comfort, which drives the adoption of efficient and adjustable lighting solutions. Households are increasingly aware of electricity costs and environmental impacts, leading to a shift towards LED and smart lighting. Additionally, the concept of wellness lighting, which supports circadian rhythms and mood enhancement, is gaining traction in homes. Smart lighting systems allow users to customize the ambiance for different activities such as reading, relaxing, or entertaining. This functional versatility enhances the value proposition of residential lighting products. Retailers respond by offering bundles and kits that simplify the transition to smart systems. As awareness of these benefits grows, the residential segment continues to lead the market through sustained demand for improved quality of life and cost efficiency.

However, the commercial end-user segment is anticipated to witness the fastest CAGR of 7.5% over the forecast period, owing to stringent energy regulations and corporate sustainability goals that mandate the adoption of high-efficiency lighting systems. Businesses are under pressure to reduce operational costs and carbon footprints, leading to widespread retrofitting of offices, retail spaces, and warehouses. Additionally, many states have enacted laws requiring commercial properties to meet specific energy performance standards. Corporations are also adopting Environmental, Social, and Governance criteria, which prioritize sustainable operations. This regulatory and ethical framework drives demand for smart and efficient lighting solutions in the commercial sector. Manufacturers offer tailored solutions for large-scale projects, ensuring compliance and performance. These factors collectively accelerate the growth of the commercial segment as businesses align with global sustainability trends.

A big reason for the segment’s fast growth is the adoption of smart building technologies and Internet of Things integration, which enhance operational efficiency and employee productivity. Commercial facilities are increasingly installing connected lighting systems that integrate with HVAC, security, and occupancy sensors to optimize resource use. Smart lighting allows for real-time monitoring of energy usage and maintenance needs, enabling predictive repairs and reduced downtime. Additionally, human-centric lighting in offices has been shown to improve employee well-being and performance, which is a key consideration for employers. The Illuminating Engineering Society provides guidelines for implementing these systems to maximize benefits. Commercial real estate owners are using smart lighting as a value-added feature to attract tenants and command higher rents. The scalability of IoT lighting solutions makes them suitable for large campuses and multi-site enterprises. As digital transformation accelerates in the commercial sector, the demand for intelligent lighting infrastructure continues to surge, driving robust market growth.

COUNTRY ANALYSIS

U.S. Lighting Market Analysis

The United States outperformed other countries in the North American lighting market and secured a 80.5% share in 2025. This growth of the US market was driven by the country's large population, advanced infrastructure, and strong regulatory framework promoting energy efficiency. The market status is characterized by a mature yet innovative environment where technological adoption and sustainability drive continuous evolution. According to the United States Energy Information Administration, the United States remains one of the largest consumers of electricity globally, though widespread efficiency gains have steadily reduced lighting's percentage share of total domestic energy demand. The presence of major global lighting manufacturers and technology firms fosters intense competition and innovation. High disposable income levels allow consumers and businesses to invest in premium smart and human-centric lighting solutions. The widespread adoption of smart home devices further amplifies demand for connected lighting products. Additionally, the United States has a robust construction industry with steady residential and commercial development contributing to market growth. The Federal Government offers tax incentives and rebates for energy-efficient upgrades, which stimulate market activity. These structural, economic, and regulatory factors solidify the United States as the leading market

COMPETITIVE LANDSCAPE

The competition in the United States lighting market is intense and characterized by the presence of established global giants alongside numerous regional and niche players. Market leaders compete primarily on technological innovation, product quality, and brand reputation rather than price alone. The shift towards smart and connected lighting has raised entry barriers due to the need for advanced software and hardware integration capabilities. Companies are increasingly differentiating themselves through proprietary ecosystems that offer seamless user experiences and interoperability with other smart devices. Sustainability has become a critical competitive factor as customers prefer brands that demonstrate environmental responsibility and energy efficiency. The commercial sector sees fierce rivalry in providing comprehensive building automation solutions that go beyond simple illumination. In the residential segment, branding and design aesthetics play significant roles in influencing consumer choices. Continuous investment in research and development is essential for staying ahead in this rapidly evolving landscape. Mergers and acquisitions are common strategies used to consolidate market position and acquire new technologies. The dynamic nature of consumer preferences and regulatory standards requires companies to remain agile and innovative to sustain their competitive advantage in this mature yet transforming market.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. lighting market include

- Lutron Electronics Co., Inc. (U.S.)

- Koncept Inc. (U.S.)

- Ottlite (U.S.)

- Herman Miller, Inc. (U.S.)

- Acuity Brands, Inc. (U.S.)

- Cree Lighting (U.S.)

- Hubbell Incorporated (U.S.)

- Eaton Corporation (U.S.)

- GE Lighting, a Savant Company (U.S.)

- Cooper Lighting Solutions (U.S.)

- Kichler Lighting LLC (U.S.)

- Leviton Manufacturing Co., Inc. (U.S.)

- Progress Lighting (U.S.)

- RAB Lighting Inc. (U.S.)

TOP PLAYERS IN THE MARKET

- Signify leads the United States lighting industry through its extensive portfolio of Philips Hue and Interact brands, which cater to both consumer and professional sectors. The company focuses heavily on smart lighting innovation and sustainability initiatives to maintain its competitive edge. Signify recently expanded its Interact Pro platform to support small and medium businesses with easy-to-deploy connected lighting solutions. This strategic move enhances their presence in the commercial sector by offering scalable and user-friendly systems. The company also invests significantly in research and development to improve energy efficiency and integrate advanced sensors into its fixtures. By partnering with technology firms, Signify ensures its products remain compatible with major smart home ecosystems. Their commitment to circular economy principles further strengthens brand loyalty among environmentally conscious consumers. These efforts collectively solidify their position as a primary innovator in the US market.

- Acuity Brands dominates the commercial and industrial lighting landscape in the United States with its comprehensive suite of hardware and software solutions. The company leverages its Atrius building management platform to provide integrated controls that optimize energy usage and operational efficiency. Acuity Brands recently enhanced its digital offerings by incorporating artificial intelligence capabilities into its lighting systems for predictive maintenance and space utilization analysis. This approach appeals to facility managers seeking data-driven insights to reduce costs. The company also focuses on sustainable manufacturing practices and has committed to reducing its carbon footprint across operations. By acquiring specialized technology firms, Acuity Brands expands its expertise in Internet of Things applications. Their strong distribution network ensures the wide availability of products for contractors and designers. These actions reinforce their leadership in providing holistic lighting and building automation solutions.

- GE Current, a Daintree Company, plays a pivotal role in the US lighting market by combining legacy brand recognition with advanced Internet of Things capabilities. The company focuses on delivering smart lighting solutions for cities, campuses, and industrial facilities through its Daintree Network operating system. GE Current recently launched new wireless control systems that simplify installation and improve interoperability with third-party devices. This strategy addresses the growing demand for flexible and scalable lighting infrastructure in retrofit projects. The company also emphasizes sustainability by developing products that support biodiversity and human-centric lighting applications. By leveraging its extensive partner ecosystem, GE Current provides customized solutions that meet specific client needs. Their investment in cybersecurity ensures that connected lighting networks remain secure against potential threats. These initiatives help the company maintain a strong foothold in the competitive commercial and municipal sectors.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the US lighting market employ several major strategies to maintain and enhance their competitive positions. Product innovation remains a primary focus as companies develop energy-efficient LED solutions and smart lighting systems that integrate with Internet of Things platforms. Strategic acquisitions allow firms to expand their technological capabilities and enter new market segments quickly. Partnerships with technology providers enable seamless integration with smart home and building management ecosystems. Companies also prioritize sustainability by adopting circular economy principles and reducing carbon footprints in manufacturing processes. Expanding distribution channels through online platforms helps reach broader consumer bases and improve accessibility. Investment in research and development drives continuous improvement in product performance and features. Marketing campaigns emphasize the benefits of smart controls and energy savings to attract environmentally conscious buyers. These combined efforts ensure that market participants remain agile and responsive to evolving customer demands and regulatory requirements in the dynamic lighting industry.

MARKET SEGMENTATION

This research report on the U.S. lighting market has been segmented and sub-segmented into the following categories.

By Lighting Type

- Light Bulbs

- Ceiling Light

- Lamps

- Fixtures

By Location

- Indoor

- Outdoor

By Connectivity

- Wired

- Wireless

By Installation Type

- New Installation

- Retrofit

By Distribution Channel

- Offline

- Online

By End-User

- Commercial

- Residential

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. lighting market?

The U.S. lighting market includes lamps, fixtures, LEDs, and smart lighting products used in homes, offices, stores, and outdoor spaces.

How does the U.S. lighting market function?

The U.S. lighting market works through manufacturers, distributors, retailers, and contractors that sell lighting for replacement and new builds.

What drives growth in the U.S. lighting market?

The U.S. lighting market grows from energy efficiency, smart home adoption, retrofits, and demand for modern lighting design.

Which segments lead the U.S. lighting market?

LED lighting, smart fixtures, and indoor lamps lead the U.S. lighting market because they offer savings and versatility.

Why is LED important in the U.S. lighting market?

LED is central to the U.S. lighting market because it uses less energy, lasts longer, and supports sustainability goals.

What role do smart lights play in the U.S. lighting market?

Smart lights strengthen the U.S. lighting market with app control, voice support, scheduling, and connected home convenience.

How does retrofit demand affect the U.S. lighting market?

Retrofit demand supports the U.S. lighting market as businesses and homeowners replace older fixtures with efficient LEDs.

What trends shape the U.S. lighting market?

The U.S. lighting market is shaped by smart controls, dimmable products, design-led fixtures, and energy-saving technology.

How does outdoor lighting impact the U.S. lighting market?

Outdoor lighting expands the U.S. lighting market through security, roadway, landscaping, and municipal applications.

What is the role of commercial lighting in the U.S. lighting market?

Commercial lighting is a major part of the U.S. lighting market because offices, stores, warehouses, and schools use large volumes.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com