U.S Online Dating Market Size, Share, Trends & Growth Forecast Report Segmented By Platform Type (Mobile Apps, Web-Based Platforms), Revenue Model, End User, And Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 To 2034

U.S Online Dating Market Size

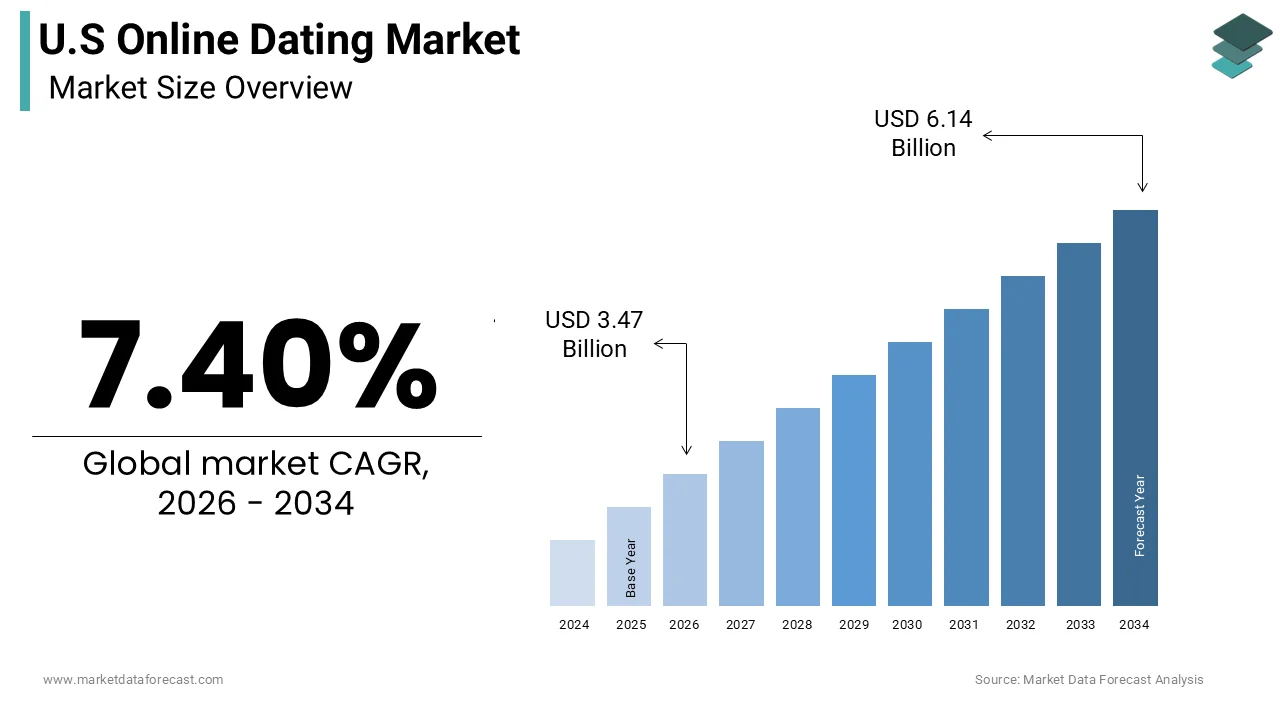

The U.S. online dating market size was calculated to be USD 3.23 billion in 2025 and is anticipated to be worth USD 6.14 billion by 2034, from USD 3.47 billion in 2026, growing at a CAGR of 7.40% during the forecast period.

Online dating is when individuals utilize internet-based platforms and mobile applications to initiate romantic connections. As per the study, approximately 30% of US adults have used a dating site or app, indicating widespread societal acceptance of digital courtship. According to the Stanford Sociological Review, nearly 40% of heterosexual couples in the United States now meet online, surpassing traditional methods such as meeting through friends or at work. This shift reflects changing social norms and the increasing reliance on digital communication for personal relationships. The consumer complaints related to online romance scams have increased, significantly amplifying the need for robust verification mechanisms. The integration of geolocation services allows for hyperlocal matching, which enhances the relevance of potential partners. This digital transformation of interpersonal connection continues to reshape the social fabric of the nation.

MARKET DRIVERS

Shifting Social Norms and Acceptance of Digital Courtship

The profound shift in social norms regarding how relationships are formed and maintained is substantially fuelling the growth of the United States online dating market. Traditional stigmas associated with meeting partners online have largely dissipated, replaced by a cultural embrace of digital convenience and efficiency. According to the study, the proportion of Americans who view online dating as a good way to meet people has risen to 53%, reflecting a majority acceptance. This normalization is particularly evident among younger people, where digital interaction is the default mode of communication. The busy lifestyles of modern professionals also contribute to this trend as individuals seek efficient ways to expand their social circles beyond immediate geographic or professional boundaries. Online platforms offer the flexibility to connect at any time, fitting seamlessly into hectic schedules. The diversity of available platforms allows users to find niche communities that align with specific interests, values, or lifestyles. This fragmentation of the market caters to varied preferences from serious long-term commitments to casual encounters. The ease of access via smartphones further accelerates adoption, making dating apps a ubiquitous part of daily life. Social media integration also plays a role by allowing users to verify identities and share common connections.

Technological Advancements in Matching Algorithms

The continuous advancement of matching algorithms and artificial intelligence, which significantly improve the user experience and success rates, is additionally bolstering the growth of the United States online dating market. Modern dating platforms utilize machine learning to analyze user behavior preferences and interaction patterns to suggest highly compatible matches. According to a study published in the Proceedings of the National Academy of Sciences, algorithms that incorporate psychological traits and behavioral data yield higher satisfaction rates than those based solely on self-reported preferences. These sophisticated systems reduce the time users spend scrolling through incompatible profiles, enhancing engagement and retention. The integration of natural language processing allows platforms to analyze message content and provide coaching tips to improve communication skills. Advances in AI have enabled real-time translation and cultural context analysis, facilitating cross-cultural connections. Video dating features powered by high-speed internet connections have become a standard offering, a safer and more authentic way to vet potential partners before meeting in person. The use of biometric verification technologies also enhances trust by confirming user identities and reducing the prevalence of fake profiles. Gamification elements such as swiping mechanics and interactive quizzes keep users engaged and make the process enjoyable. These technological innovations create a competitive advantage for platforms that can demonstrate superior matching accuracy.

MARKET RESTRAINTS

Prevalence of Online Fraud and Safety Concerns

The persistent issue of online fraud and safety concerns, which deters potential users and erodes trust, is restricting the growth of the United States online dating market. Romance scams involve fraudulent actors creating fake profiles to exploit victims emotionally and financially, causing substantial harm. According to the Federal Bureau of Investigation, the Internet Crime Complaint Center received over 24000 complaints related to romance fraud in a single year, with losses exceeding 1 billion dollars. These high-profile incidents generate negative publicity and make individuals cautious about sharing personal information on dating platforms. The anonymity provided by the internet facilitates deceptive practices by making it difficult for users to verify the authenticity of profiles. Safety concerns extend beyond financial loss to include physical risks associated with meeting strangers in person. Many users hesitate to transition from online chatting to offline meetings due to fears of harassment or violence. Platform providers face pressure to implement stricter verification processes, which can increase operational costs and friction in the user journey. The lack of standardized safety protocols across the industry creates inconsistency in user protection. High-profile data breaches also compromise user privacy, leading to reluctance in adopting new platforms.

Subscription Fatigue and Monetization Resistance

The growing resistance to subscription models and monetization strategies, which leads to user churn and reduced revenue potential, is hampering the growth of the United States online dating market. Many dating platforms operate on a freemium model, where basic features are free but premium functionalities require payment. As per the study, nearly 60% of online daters express frustration with the cost of premium subscriptions relative to the perceived value received. Users often feel that essential features, such as seeing who liked their profile or unlimited swipes, are unfairly gated behind paywalls. This perception of exploitative pricing drives users to switch between multiple apps in search of better deals or free alternatives. The average retention rate for dating apps drops significantly after the first month, indicating low long-term commitment. The abundance of free competitors exacerbates this issue, making it difficult for paid platforms to justify their fees. Subscription fatigue is a broader trend affecting digital services where consumers are overwhelmed by recurring monthly charges. Many users prefer one-time purchases or ad-supported models, which are less common in the dating sector. The pressure to convert free users to paid subscribers often results in aggressive marketing tactics that annoy users and damage brand reputation. Platforms struggle to balance profitability with user satisfaction, leading to a delicate equilibrium.

MARKET OPPORTUNITIES

Integration of Virtual Reality and Metaverse Experiences

The integration of virtual reality and metaverse experiences, which offer immersive and interactive ways to connect, is substantially creating new opportunities for the growth of the United States online dating market. These technologies allow users to interact in simulated environments, providing a deeper sense of presence and connection than traditional text or video chats. According to the International Data Corporation, the global spending on virtual reality hardware and software is projected to reach 20 billion dollars by 2025, indicating a growing infrastructure for such applications. Dating platforms can leverage this technology to host virtual dates in exotic locations or interactive games, fostering shared experiences. The virtual interactions can reduce anxiety and increase self-disclosure, leading to stronger initial bonds. The metaverse offers a space for users to express themselves through avatars and digital assets, adding a new layer of personality and creativity to dating. This innovation appeals to younger generations, who are digital natives and comfortable with virtual identities. Brands can partner with dating apps to create sponsored virtual venues or events, generating new revenue streams. The ability to test compatibility in diverse scenarios before meeting in person enhances safety and confidence. Early adopters of this technology can differentiate themselves in a crowded market.

Expansion into Niche and Community-Based Dating

The expansion into niche and community-based dating platforms that cater to specific interests, beliefs, or lifestyles is also expected to boost the growth of the United States online dating market. Generalist dating apps often fail to address the unique needs of specialized groups, leading to a demand for tailored solutions. These platforms foster a sense of community and shared values, which enhance user engagement and retention. The individuals with specific religious or political views prefer to date within their own groups to ensure compatibility. Platforms catering to pet owners, gamers, or outdoor enthusiasts provide a natural conversation starter and common ground for users. This segmentation allows for more targeted marketing and higher conversion rates as users feel understood and valued. Community features such as forums and group events further strengthen connections beyond one-on-one matching. The rise of identity-focused dating also supports marginalized communities seeking safe and inclusive spaces. By focusing on quality over quantity, niche platforms can command higher subscription fees due to the specialized value they provide. Partnerships with relevant organizations or influencers can drive user acquisition efficiently. This trend towards specialization offers a sustainable path for growth in a saturated market.

MARKET CHALLENGES

Algorithmic Bias and Ethical Concerns

The issue of algorithmic bias and ethical concerns regarding how matches are generated and presented is one of the major challenges for the growth of the United States online dating market. Algorithms may inadvertently perpetuate societal prejudices based on race, age, or appearance, leading to discriminatory outcomes. Dating apps have been found to reinforce racial stereotypes by prioritizing certain demographics in search results. This bias can alienate users and create an unequal playing field, undermining the promise of inclusive connectivity. The lack of transparency in how algorithms function makes it difficult for users to understand why they receive certain matches. Regulatory bodies are increasingly scrutinizing these practices, raising the risk of legal repercussions for non-compliant platforms. The ethical implications of using personal data for profiling also raise concerns about consent and autonomy. Users may feel manipulated by design choices that encourage addictive behaviors rather than genuine connections. The pressure to optimize for engagement metrics can conflict with fostering healthy relationships. Addressing these biases requires significant investment in ethical AI development and diverse training data. Companies must balance commercial objectives with social responsibility to maintain public trust.

Data Privacy and Regulatory Compliance Complexities

The complexity of data privacy regulations and the need for strict compliance to protect user information are also hindering the growth of the United States online dating market. Dating platforms collect vast amounts of sensitive personal data, including location, messages, and preferences, making them attractive targets for cyberattacks. Companies must provide users with greater control over their data, including the right to delete and opt out of sales. Compliance with such regulations requires robust technical infrastructure and legal expertise, increasing operational costs. The financial sector and social platforms, including dating apps, are among the most targeted industries for data breaches. A single breach can result in massive fines and loss of user trust, which is difficult to rebuild. The global nature of many dating apps means they must navigate a patchwork of international privacy laws, such as the General Data Protection Regulation in Europe. These varying requirements create logistical challenges for multinational operators. Users are becoming more aware of their privacy rights and are demanding greater transparency from platforms. The introduction of new state-level privacy laws in the US adds another layer of complexity. Companies must continuously update their policies and practices to remain compliant.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.40% |

| Segments Covered | By Platform Type, Revenue Model, End User, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Match Group, Tinder, Bumble, Hinge, OkCupid, eHarmony, Grindr, Coffee Meets Bagel, Zoosk, Plenty of Fish (POF), HER, Badoo, Happn, Taimi, The League |

SEGMENTAL ANALYSIS

By Platform Type Insights

The mobile application segment accounted for a dominant share of the United States online dating market in 2025, owing to the widespread penetration of smartphones in the United States, which serves as the primary gateway to digital services. The high level of device ownership ensures that dating platforms are accessible to users at any time and in any location, removing the barriers associated with desktop-based access. The convenience of mobile apps allows users to engage with potential matches during commutes, breaks, or leisure time, integrating dating into daily routines seamlessly. The average American spends over four hours per day on their mobile device, providing ample opportunity for app engagement. The intuitive interface of mobile apps designed for touch screens enhances user experience, making navigation and interaction effortless. Push notifications keep users engaged by alerting them to new matches or messages instantly, fostering a sense of immediacy. The portability of smartphones enables location-based services, which are crucial for hyper-local matching.

The web-based platforms segment is expected to register the fastest CAGR of 9.1% during the forecast period, with the preference of certain user segments for detailed profile management and comprehensive search functionalities that are easier to navigate on larger screens. Many professionals spend significant hours at desktop computers during work hours, providing opportunities for discreet browsing. Web platforms allow for more extensive profile creation, including long-form bios and multiple photo uploads, which appeal to users seeking serious long-term relationships. Users tend to spend more time reading and processing information on desktop interfaces compared to mobile devices. This behavior aligns with the needs of individuals who prioritize compatibility and depth over quick swiping. Web-based platforms often offer advanced filtering options that are cumbersome to use on small mobile screens. The larger display area facilitates better visualization of potential matches and their details. Users who are cautious about privacy may prefer web browsers where they can utilize incognito modes and clear history more effectively than on shared mobile devices. The stability of internet connections on desktops also supports smoother video dating experiences without the battery drain associated with mobile usage.

By Revenue Model Insights

The monthly subscription model segment accounted in holding 56.3% of the United States online dating market share in 2025. The flexibility it offers users, who are hesitant to commit to long-term financial obligations. Many Americans prefer flexible payment options that allow them to manage their cash flow effectively. Monthly subscriptions enable users to cancel or pause their memberships at any time, reducing the perceived risk of trying premium features. This model aligns with the transient nature of online dating, where users may find a partner quickly or lose interest in the platform. The low entry cost of monthly plans encourages trial among new users who are unsure about the effectiveness of the service. Platforms benefit from this model by capturing a larger volume of users who may convert to longer-term relationships later. The ease of cancellation also reduces customer acquisition friction as users feel more in control of their spending. Monthly billing allows users to align their subscription with their dating goals and activity levels. This adaptability makes monthly subscriptions the most attractive option for a diverse range of users.

The annual subscription segment is projected to register the fastest CAGR of 6.8% from 2026 to 2034. The significant cost savings offered compared to monthly billing cycles are propelling the growth of the segment. According to the study, consumers are increasingly seeking value for money in their discretionary spending amid economic uncertainties. Annual plans often provide discounts of up to 50% compared to paying monthly, which appeals to budget-conscious users. Users who are serious about finding a long-term partner view annual subscriptions as a worthwhile investment in their personal lives. The upfront payment eliminates the hassle of monthly renewals and potential price increases. This convenience factor attracts users who prefer a set-and-forget approach to their dating expenses. Platforms incentivize annual subscriptions with exclusive features or priority customer support, further enhancing the value proposition. The commitment associated with annual plans also signals seriousness to other users, potentially improving match quality.

By End User Insights

The male segment was the largest by accounting for 44.8% of the United States online dating market share in 2025 due to their higher propensity to initiate contact and engage actively on dating platforms. Men are significantly more likely than women to send the first message or swipe right on potential matches. This behavioral pattern results in higher activity levels and greater visibility for male users on these platforms. The traditional gender norms still influence online dating dynamics, with men expected to take the lead in courtship. This expectation drives men to use paid features such as boosts or super likes to stand out in a crowded market. The competitive nature of online dating for men encourages them to invest more time and money to secure matches. Male users often manage multiple conversations simultaneously, leading to higher engagement metrics. The desire to overcome the imbalance in gender ratios on some platforms further motivates active participation. Men are more likely to upgrade to premium tiers to gain advantages in visibility and communication.

The female user segment is expected to witness the fastest CAGR of 7.5% from 2026 to 2034. The rapid growth of the female user segment is primarily driven by the implementation of enhanced safety and verification features on dating platforms. Recent innovations, such as photo verification background checks and panic buttons, have addressed these concerns effectively. Women are more likely to join platforms that offer robust moderation and reporting mechanisms. The ability to control who can view their profile or send messages empowers female users. Video dating features allow women to vet potential partners safely before meeting in person. These measures build trust and encourage broader participation among women. The focus on creating respectful communities reduces harassment and inappropriate behavior. Women feel more comfortable exploring online dating when they perceive the environment as safe. Platform investments in AI-driven moderation detect and remove malicious accounts proactively. This improved safety record attracts new female users who were previously hesitant.

Leading Players in the Europe Online Dating Market

- Parship Elite is a leading premium dating service in Europe known for its scientific matching algorithm based on psychological principles. The company contributes significantly to the European market by targeting professionals seeking serious long-term relationships. Recently, Parship Elite has strengthened its position by enhancing its personality test with advanced machine learning techniques to improve match accuracy. The firm has also expanded its digital marketing campaigns across key European countries to attract younger demographics. The company continues to invest in mobile app development to provide a seamless user experience. These actions demonstrate its commitment to maintaining high standards in online matchmaking. Parship Elite remains a dominant player by adapting to changing relationship dynamics and leveraging data-driven insights. Its focus on exclusivity and compatibility distinguishes it from casual dating platforms. The brand reinforces its reputation through strategic partnerships with lifestyle brands. This approach sustains its influence in the competitive European landscape.

- Meetic is a prominent online dating platform in Europe with a strong presence in France and surrounding regions. The company offers diverse services, including video dating and event hosting, to facilitate meaningful connections. Meetic contributes to the market by providing a versatile platform that caters to various relationship goals. Recently, the company has strengthened its market position by integrating artificial intelligence to optimize user recommendations and engagement. Meetic has also launched new safety features, such as photo verification, to protect users from fraud. The platform actively organizes offline social events to bridge the gap between digital and physical interactions. These initiatives enhance user trust and community building. Meetic continues to innovate its interface to improve accessibility and usability for all age groups. The company focuses on personalized customer support to retain subscribers.

- Bumble Inc operates strongly in the European market with its unique feature requiring women to initiate conversations. The company contributes by promoting respectful and equitable online interactions. Bumble has strengthened its position in Europe by expanding its BFF and Bizz modes to support friendship and professional networking. Recently, the company has invested in robust moderation tools to combat harassment and ensure user safety. Bumble has also partnered with local organizations to promote healthy relationship education across European cities. The platform continuously updates its algorithm to prioritize active and verified profiles. These efforts enhance user satisfaction and retention. Bumble focuses on empowering users through community guidelines and inclusive policies. The company leverages social media influencers to reach younger audiences effectively.

Top Strategies Used by Key Market Participants in the US Online Dating Market

The competition in the United States online dating market is fierce and characterized by a mix of established giants and emerging niche players. Large conglomerates dominate the landscape by leveraging extensive user bases and sophisticated technology stacks to offer comprehensive dating ecosystems. These major entities compete aggressively on product innovation, user safety, and brand recognition to retain subscriber loyalty. Smaller specialized apps differentiate themselves by catering to specific communities or relationship types, such as serious marriage-minded individuals or casual daters. The barrier to entry is moderate, but scaling requires significant investment in marketing and technology development. Competition is further intensified by the low switching costs for users who can easily download multiple apps simultaneously. Firms are increasingly investing in artificial intelligence to improve match quality and reduce churn rates. The war for user attention drives continuous feature updates, including video integration and gamification elements. Strategic acquisitions are common as larger companies seek to absorb innovative startups and eliminate rivals. Pricing strategies vary widely, with some platforms offering free access supported by ads, while others rely on exclusive subscription models. Ultimately, success depends on the ability to create a safe, engaging, and effective environment for forming connections. Trust and user experience are the primary differentiators in this saturated market. Companies must constantly adapt to changing social norms and technological advancements to survive.

MARKET SEGMENTATION

This research report on the US online dating market has been segmented and sub-segmented based on platform type, revenue model, end user & region.

By Platform Type

- Mobile Apps

- Web-based Platforms

By Revenue Model

- Monthly

- Quarterly

- Annual

- Advertisement

By End User

- Male

- Female

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What factors are driving the growth of the U.S. online dating market?

Increasing digitalization, changing social lifestyles, rising use of mobile apps, and growing demand for convenient relationship platforms are major growth drivers.

2. Which segment dominates the U.S. online dating market?

Mobile dating applications dominate the market owing to their ease of use, accessibility, and growing popularity among younger consumers.

3. What is the expected CAGR of the U.S. online dating market?

The market is projected to witness steady CAGR growth during the forecast period due to rising adoption of subscription-based dating platforms.

4. How are smartphones influencing the online dating industry in the United States?

Smartphones provide instant access to dating applications, enabling users to connect anytime and anywhere, thereby increasing user engagement.

5. How is artificial intelligence impacting online dating platforms?

Artificial intelligence improves matchmaking accuracy, user recommendations, fraud detection, and personalized user experiences.

6. What are the major challenges faced by the U.S. online dating market?

Privacy concerns, fake profiles, cybersecurity risks, and user trust issues are some of the major challenges in the market.

7. Which subscription model is widely adopted in online dating platforms?

Freemium subscription models are widely adopted, allowing users to access basic services for free while paying for premium features

8. What are the emerging trends in the U.S. online dating market?

Video dating, AI-powered matchmaking, niche dating apps, virtual dating experiences, and LGBTQ+ focused platforms are emerging trends

9. Who are the key market players in the U.S. online dating market?

Major companies operating in the market include Match Group, Bumble, Grindr, eHarmony, Hinge, and OkCupid.

10. What future opportunities exist in the U.S. online dating market?

Advancements in AI, virtual reality dating, enhanced security features, and expansion of niche dating platforms are expected to create future growth opportunities.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com