- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

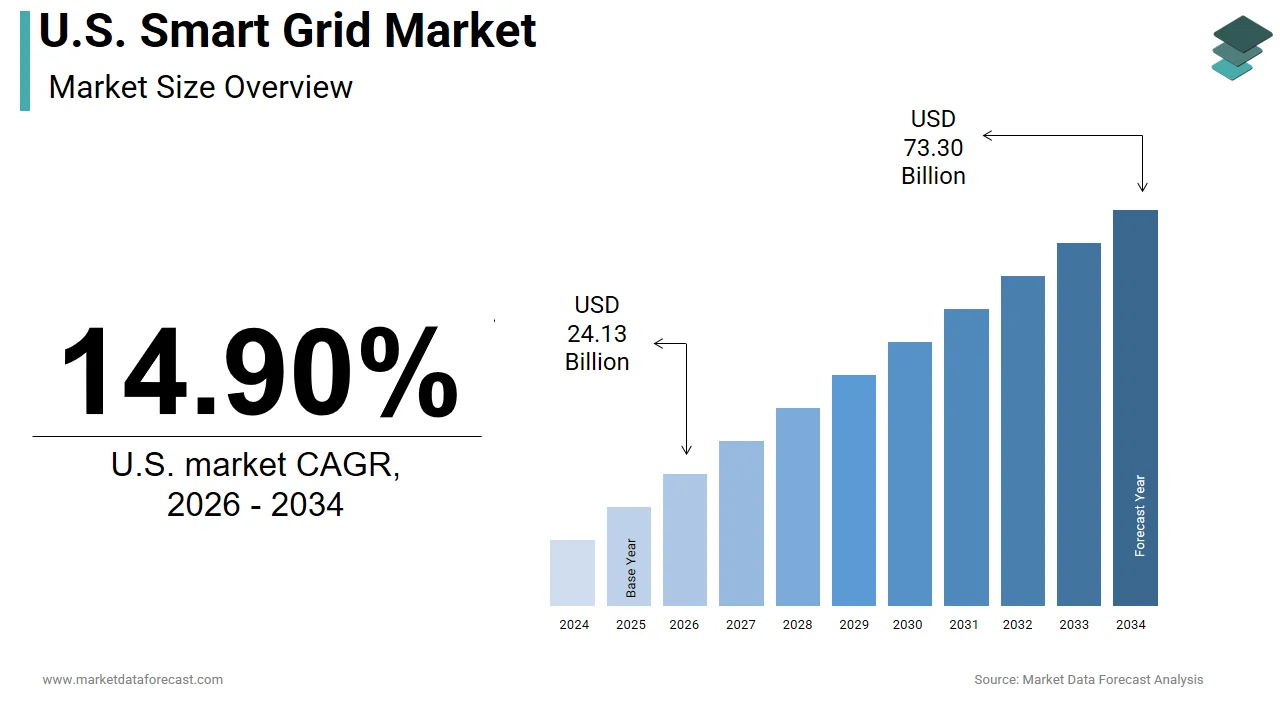

Market Size, 2025

$21 BnMarket Estimate, 2026

$24.13 BnMarket Forecast, 2034

$73.30 BnCAGR, 2026–2034

14.90%U.S. Smart Grid Market Report Summary

The U.S. smart grid market was valued at USD 21 billion in 2025, is estimated to reach USD 24.13 billion in 2026, and is projected to reach USD 73.30 billion by 2034, growing at a CAGR of 14.90% from 2026 to 2034. Market growth is driven by increasing investments in grid modernization, rising integration of renewable energy sources, and the need for efficient energy management systems. Smart grid technologies enable real-time monitoring, improved reliability, and enhanced energy efficiency across the power network. Additionally, government initiatives, regulatory mandates, and the transition toward decarbonization are accelerating the adoption of advanced grid infrastructure across the United States.

Key Market Trends

- Increasing investments in grid modernization and digital infrastructure.

- Rising integration of renewable energy sources.

- Growing adoption of IoT and advanced analytics in energy management.

- Focus on improving grid reliability and efficiency.

- Strong government support and regulatory initiatives.

Segmental Insights

- Based on end user, the utility segment dominated the United States smart grid market by capturing 35.1% share in 2025, driven by large-scale grid infrastructure deployment.

- Based on component, the hardware segment led the market with 48.6% share in 2025, supported by demand for smart meters, sensors, and communication devices.

Country-Level Insights

- The United States dominated the North American smart grid market by holding 83.7% share in 2025, driven by its extensive electrical infrastructure, ambitious modernization initiatives, and strong regulatory framework. The country continues to lead due to large-scale investments in smart energy systems and digital grid technologies.

Competitive Landscape

The U.S. smart grid market is highly competitive, with companies focusing on innovation, digital transformation, and strategic partnerships. Integration of smart technologies, data analytics, and cloud-based platforms is shaping the competitive landscape.

Prominent companies operating in the U.S. smart grid market include ABB Ltd, Siemens AG, Schneider Electric, S&C Electric Company, Eaton Corporation, General Electric, IBM, Wipro Limited, Honeywell, Cisco Systems, Aclara Technologies, Landis+Gyr, Oracle Corporation, and Itron.

U.S. Smart Grid Market Size

The U.S. smart grid market was valued at USD 21 billion in 2025. The market is anticipated to grow at a CAGR of 14.90% from 2026 to 2034 and be worth USD 73.30 billion by 2034 from USD 24.13 billion in 2026.

A smart grid is a modernized electricity network that uses digital technology, sensors, and two-way communication to monitor, manage, and optimize the generation, distribution, and consumption of electricity in real-time. This advanced network utilizes sensor control systems and automated devices to monitor, manage, and optimize the generation, distribution, and consumption of energy in real time. The transition is driven by the need for greater reliability, efficiency, and sustainability in the face of increasing energy demand and climate change pressures. As per the U.S. Energy Information Administration (April 2026), electricity consumption in the commercial sector is rising sharply, with a projected 4.5% increase in 2026 driven by data center expansion. However, residential sector sales are expected to slightly decline by 0.4% in 2026 due to milder weather. This shifting demand landscape, particularly the surge in energy-intensive commercial technologies, underscores the urgent need for responsive and flexible grid management solutions to maintain system reliability. Furthermore, the Department of Energy highlights that aging infrastructure accounts for a significant portion of power outages, emphasizing the urgent need for modernization. The integration of renewable energy sources such as wind and solar requires a grid capable of handling variable supply, which smart technologies facilitate through advanced forecasting and load balancing. Regulatory initiatives, including the Infrastructure Investment and Jobs Act, provide substantial funding for grid modernization projects, accelerating adoption. The market is characterized by the deployment of smart meters, advanced metering infrastructure and distributed energy resource management systems. This technological shift empowers consumers to participate actively in energy management while enhancing the resilience of the national power system against physical and cyber threats.

MARKET DRIVERS

Government Initiatives and Federal Funding for Infrastructure Modernization

Government initiatives and substantial federal funding serve as a primary driver for the United States smart grid market by providing the financial resources and regulatory framework necessary for large-scale infrastructure upgrades. The federal government has recognized the critical importance of modernizing the electrical grid to enhance national security, economic competitiveness, and environmental sustainability. As per the Department of Energy, the Infrastructure Investment and Jobs Act allocates billions of dollars specifically for grid resilience and smart grid technologies, enabling utilities to replace outdated equipment with intelligent systems. This financial support reduces the capital burden on utility companies, encouraging faster adoption of smart meter sensors and automation tools. Additionally, state-level mandates requiring the installation of advanced metering infrastructure create a consistent demand for smart grid components. Regulatory bodies are also implementing standards for interoperability and cybersecurity, ensuring that new technologies integrate seamlessly and securely into the existing grid. The push for decarbonization further motivates policymakers to support smart grid deployments that facilitate the integration of renewable energy sources. These coordinated efforts at the federal and state levels create a favorable environment for investment and innovation. So, the robust policy support and financial incentives accelerate the transformation of the traditional grid into a dynamic and efficient smart network.

Integration of Renewable Energy Sources and Distributed Generation

The increasing integration of renewable energy sources and distributed generation acts as a significant driver for the United States smart grid market by necessitating advanced management capabilities to handle variable power supplies. Solar and wind energy production is intermittent and decentralized, requiring a grid that can balance supply and demand in real time to maintain stability. As per the United States Energy Information Administration, renewable energy sources accounted for approximately 20 percent of total utility-scale electricity generation in recent years, a figure expected to grow substantially. Smart grid technologies such as advanced inverters, energy storage systems, and demand response programs enable utilities to manage these fluctuations effectively. Two-way communication allows for the seamless integration of rooftop solar panels and community wind farms into the main grid, preventing overloads and ensuring consistent power quality. Distributed energy resources empower consumers to become prosumers who both consume and produce electricity, requiring sophisticated metering and billing systems. The smart grid facilitates the aggregation of these dispersed resources, creating virtual power plants that enhance grid reliability. Furthermore, the ability to forecast renewable generation using artificial intelligence helps utilities plan operations more efficiently. Hence, the shift toward a decentralized and sustainable energy mix drives the adoption of smart grid solutions essential for maintaining a stable and resilient power system.

MARKET RESTRAINTS

High Initial Implementation Costs and Capital Constraints

High initial implementation costs and capital constraints pose a significant restraint to the United States smart grid market by limiting the ability of utility companies, particularly smaller municipal cooperatives, to invest in modernization. Upgrading legacy infrastructure with smart meter sensors, communication networks, and control systems requires substantial upfront expenditure that can strain financial resources. As per the Edison Electric Institute, the cost of deploying advanced metering infrastructure and associated backend systems can run into hundreds of millions of dollars for large utilities, creating a barrier to entry for smaller entities. The return on investment for smart grid technologies is often long-term and difficult to quantify immediately, making it challenging to justify expenditures to stakeholders and regulators. Additionally, the complexity of integrating new technologies with existing legacy systems increases installation and maintenance costs. Utilities may hesitate to commit to large-scale projects due to uncertainty regarding future regulatory changes and technology obsolescence. The need for specialized workforce training and cybersecurity measures further adds to the overall expense. Economic downturns or budget cuts can delay or cancel planned modernization initiatives, slowing market growth. Therefore, the significant financial burden associated with smart grid deployment acts as a brake on widespread adoption, particularly among resource-constrained utility providers.

Cybersecurity Threats and Data Privacy Concerns

Cybersecurity threats and data privacy concerns serve as a major restraint to the United States smart grid market by creating risks that deter stakeholders from fully embracing connected technologies. The increased connectivity and data exchange inherent in smart grids expand the attack surface for malicious actors seeking to disrupt power supply or steal sensitive consumer information. As per the North American Electric Reliability Corporation, cyber incidents targeting the energy sector have increased in frequency and sophistication, highlighting the vulnerability of digital grid components. Utilities must invest heavily in robust cybersecurity measures, including encryption, firewalls, and continuous monitoring to protect against breaches, which adds to operational costs. Data privacy regulations, such as state-level consumer protection laws, require strict handling of detailed usage data collected by smart meters, raising compliance challenges. Consumers may resist the installation of smart meters due to fears of surveillance or data misuse, leading to public opposition and delayed deployments. The potential for large-scale blackouts caused by cyberattacks poses a national security risk, prompting cautious adoption rates. Liability issues related to data breaches further complicate the risk landscape for utility providers. Therefore, the persistent threat of cyber vulnerabilities and privacy violations creates hesitation and slows the pace of smart grid implementation across the country.

MARKET OPPORTUNITIES

Expansion of Electric Vehicle Charging Infrastructure

The expansion of electric vehicle charging infrastructure presents a significant opportunity for the United States smart grid market by creating new demand for intelligent load management and grid integration solutions. As electric vehicle adoption accelerates, the increased electricity demand from charging stations requires a grid capable of handling peak loads and optimizing energy distribution. As per the Department of Transportation, the number of electric vehicles on US roads is projected to reach millions in the coming decade, necessitating the widespread deployment of charging networks. Smart grid technologies enable vehicle-to-grid integration, allowing electric vehicles to serve as distributed energy storage resources that can feed power back into the grid during peak demand. Smart charging solutions use real-time data to schedule charging during off-peak hours, reducing strain on the grid and lowering costs for consumers. Utilities can leverage this flexibility to balance supply and demand more effectively, enhancing overall grid stability. The development of fast charging stations in urban and highway locations requires advanced grid connections and monitoring systems, creating opportunities for smart grid component providers. Partnerships between automakers, utility companies, and technology firms foster innovation in charging infrastructure. Consequently, the synergy between electric mobility and smart grid capabilities drives growth and opens new revenue streams for market participants.

Adoption of Advanced Metering Infrastructure and Analytics

The adoption of advanced metering infrastructure and data analytics offers a substantial opportunity for the United States smart grid market by enabling utilities to gain deeper insights into consumption patterns and operational efficiency. Smart meters provide real-time data on electricity usage, allowing for accurate billing, outage detection, and demand response programs. As per the Federal Energy Regulatory Commission, the deployment of advanced metering infrastructure has reached high penetration rates in many states, creating a vast repository of data that can be leveraged for optimization. Analytics platforms process this data to identify trends, predict equipment failures, and optimize maintenance schedules, reducing operational costs and improving reliability. Utilities can offer personalized energy management services to consumers, helping them reduce consumption and save money, which enhances customer satisfaction and loyalty. The integration of artificial intelligence and machine learning enhances the predictive capabilities of these systems, enabling proactive grid management. Data-driven decision-making supports the integration of renewable energy sources and distributed resources by providing visibility into grid conditions. Furthermore, the ability to detect theft and unauthorized usage improves revenue protection for utilities. So, the value derived from data analytics and advanced metering drives continued investment and innovation in the smart grid sector.

MARKET CHALLENGES

Interoperability and Standardization Issues

Interoperability and standardization issues present a major challenge to the United States smart grid market by hindering the seamless integration of diverse technologies and systems from multiple vendors. The smart grid ecosystem comprises a wide array of devices, including smart meters, sensors, inverters, and control systems that must communicate effectively to function cohesively. As per the National Institute of Standards and Technology, the lack of universal communication protocols and data formats creates compatibility barriers that complicate system integration and increase deployment costs. Utilities often struggle to connect legacy equipment with new smart technologies, requiring custom interfaces and middleware that reduce efficiency and reliability. The absence of standardized security frameworks further exacerbates vulnerabilities, making it difficult to ensure consistent protection across the network. Vendor lock-in situations limit flexibility and increase dependence on specific suppliers, restricting competition and innovation. Regulatory bodies are working to establish common standards, but adoption remains uneven across different regions and utilities. The complexity of managing heterogeneous systems requires specialized expertise and ongoing maintenance, adding to operational burdens. Thus, the fragmentation of technology standards impedes the scalability and effectiveness of smart grid solutions, requiring concerted industry efforts to achieve true interoperability.

Workforce Skills Gap and Technical Expertise Shortage

The workforce skills gap and technical expertise shortage pose a significant challenge to the United States smart grid market by limiting the availability of qualified personnel needed to design, install, and maintain complex digital infrastructure. The transition to a smart grid requires a workforce proficient in information technology, cybersecurity, data analytics, and electrical engineering disciplines that are often distinct from traditional utility skills. As per the U.S. Bureau of Labor Statistics (BLS), employment of data scientists is projected to grow 34% from 2024 to 2034, and while there is a general talent crunch, reports from the U.S. Department of Energy (DOE) specifically cite the "hiring difficulty" within the energy transition workforce. Existing utility employees may lack the necessary training to operate and troubleshoot advanced smart grid technologies, leading to inefficiencies and increased downtime. The retirement of experienced workers further depletes the knowledge base, creating a critical gap in institutional expertise. Training programs and educational initiatives are often insufficient to meet the rapid pace of technological change, resulting in a shortage of ready-to-deploy professionals. Recruitment competition in the technology sector exacerbates the difficulty of hiring qualified candidates. Therefore, the lack of a skilled workforce hinders the effective implementation and operation of smart grid systems, requiring significant investment in education and workforce development to sustain market growth.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By End-User, Component, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | ABB Ltd., Siemens, Schneider Electric, S&C Electric Company, Eaton, General Electric Company, IBM, Wipro Limited, Honeywell, Cisco, Aclara, Landis+Gyr, Oracle, Itron, and Others. |

SEGMENTAL ANALYSIS

By End-user Insights

The utility segment held the majority share of 35.1% of the United States smart grid market in 2025. This supremacy of the segment is attributed to the critical mandate for electricity providers to modernize aging infrastructure and enhance grid reliability. Utilities are the main investors in smart grid technologies as they are responsible for the transmission and distribution of electricity to all other end users. As per the Edison Electric Institute, investor-owned utilities serve approximately 72 percent of electric customers in the United States and manage the vast majority of high-voltage transmission lines requiring robust monitoring and control systems. One of the major drivers of this domination is the need to reduce operational costs and improve outage management through automated fault detection and self-healing capabilities. Regulatory bodies such as state public utility commissions often approve rate cases that allow utilities to recover investments in advanced metering infrastructure and distribution automation. The integration of renewable energy sources into the grid requires utilities to deploy sophisticated software and hardware to balance supply and demand in real time. Furthermore, federal funding initiatives specifically target utility-scale projects to enhance national security and resilience against cyber threats and natural disasters. The sheer scale of infrastructure managed by utilities ensures that they remain the largest consumers of smart grid solutions. Thus, the regulatory, financial, and operational imperatives facing utility companies cement their position as the dominant end user in the market.

The residential segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 14% during the forecast period, owing to the increasing adoption of smart home technologies and consumer desire for energy autonomy. Homeowners are increasingly installing smart meters, solar panels, and home energy management systems to monitor consumption and reduce electricity bills. As per the United States Energy Information Administration, the number of residential solar photovoltaic installations has grown significantly, with millions of homes now generating their own power, creating a need for two-way communication with the grid. A key factor fuelling this growth is the rise of prosumers who both consume and produce electricity, requiring advanced inverters and net metering capabilities. Smart thermostats and connected appliances allow residents to participate in demand response programs, earning incentives for reducing usage during peak hours. The proliferation of electric vehicles in residential garages further drives demand for smart charging solutions that integrate with home energy systems. Government rebates and tax credits for energy-efficient upgrades encourage homeowners to invest in smart grid-compatible devices. Additionally, increased awareness of sustainability and carbon footprints motivates consumers to adopt technologies that optimize energy use. Hence, the convergence of technological affordability, environmental consciousness, and policy support accelerates the expansion of the residential smart grid segment.

By Component Insights

In 2025, the hardware segment was the largest segment in the United States smart grid market and occupied a 48.6% share. This prominence of the segment is supported by the fundamental requirement for physical devices to enable data collection, communication, and control within the electrical network. This segment includes smart meters, sensors, transformers, switches, and communication modules that form the backbone of smart grid infrastructure. As per the U.S. Energy Information Administration (EIA) and FERC (2026), advanced metering infrastructure has reached over 128 million smart meters installed across the country, representing a penetration rate of roughly 80%. The main reason behind this domination is the extensive need to replace legacy electromechanical meters and outdated grid components with digital equivalents that support real-time data exchange. Utilities must install sensors at various points in the transmission and distribution network to monitor voltage, current, and frequency, ensuring stable operations. The physical nature of these assets requires significant capital expenditure, making hardware the largest component of initial smart grid investments. Additionally, the integration of distributed energy resources such as solar inverters and battery storage systems adds to the volume of hardware required. The durability and longevity of hardware ensure a steady replacement cycle and upgrade path. So, the foundational role of physical devices in enabling smart grid functionality establishes hardware as the dominant component in the market.

The software segment is expected to exhibit a noteworthy CAGR of 16.3% over the forecast period. This quick surge of the segment is propelled by the increasing complexity of data management and the need for intelligent decision-making tools. As the volume of data generated by smart meters and sensors explodes, utilities require advanced analytics platforms to process and interpret this information effectively. As per the International Data Corporation, spending on artificial intelligence and machine learning in the energy sector is rising rapidly as companies seek to optimize grid performance and predict maintenance needs. The primary factor accelerating this growth is the shift from passive monitoring to active grid management using software-defined networks and cloud-based solutions. Advanced distribution management systems enable utilities to automate responses to fluctuations in supply and demand, integrating renewable energy sources seamlessly. Cybersecurity software is also seeing rapid adoption as utilities prioritize protection against digital threats targeting critical infrastructure. The ability to visualize grid status in real time and simulate scenarios helps operators make informed decisions quickly. Furthermore, software updates and upgrades offer a continuous revenue stream for vendors, unlike one-time hardware sales. Hence, the critical role of software in unlocking the value of smart grid data drives its exceptional growth rate.

COUNTRY LEVEL ANALYSIS

U.S. Smart Grid Market Analysis

The United States dominated the North American smart grid market and held a 83.7% share in 2025 because of its extensive electrical infrastructure, ambitious modernization goals, and strong regulatory support. The country’s market status is characterized by a mature yet evolving landscape where legacy systems are being progressively replaced by intelligent digital networks. As per the Department of Energy, the United States has one of the largest and most complex power grids in the world, necessitating significant investment in smart technologies to maintain reliability and efficiency. Federal initiatives such as the Infrastructure Investment and Jobs Act provide billions of dollars in funding for grid resilience and clean energy integration, accelerating adoption rates. The presence of leading technology companies and utility providers fosters innovation in areas such as energy storage, electric vehicle integration, and cybersecurity. State-level policies varying from California to New York drive diverse implementation strategies reflecting local energy priorities and environmental targets. High electricity consumption and the growing prevalence of distributed energy resources create a robust demand for smart grid solutions. The United States serves as a global leader in setting standards and best practices for smart grid deployment, influencing international markets. The combination of economic scale, technological expertise, and policy momentum solidifies the United States' position as the dominant force in the regional smart grid industry.

COMPETITIVE LANDSCAPE

The competition in the United States smart grid market is intense and characterized by the presence of established industrial giants, specialized technology firms, and emerging startups vying for dominance in grid modernization. Major players compete on the basis of technological innovation, system interoperability, and comprehensive service offerings. Differentiation is achieved through advanced analytics capabilities, cybersecurity features, and the ability to integrate diverse energy sources seamlessly. Price competition is moderate as utilities prioritize reliability and long-term value over initial cost savings. Strategic alliances and acquisitions are common as companies seek to expand their product portfolios and geographic reach. The market sees continuous investment in research and development to address evolving regulatory requirements and consumer demands. Customer retention relies on demonstrating tangible improvements in grid efficiency and outage reduction. Regulatory compliance and adherence to industry standards influence competitive dynamics significantly. The entry of new players with niche solutions adds pressure to incumbents to innovate continuously. Success depends on balancing technical expertise with customer-centric solutions and adapting to rapid technological changes in the energy sector.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. smart grid market include

- ABB Ltd

- Siemens

- Schneider Electric

- S&C Electric Company

- Eaton

- GE

- General Electric Company

- IBM

- Wipro Limited

- Honeywell

- Cisco

- Aclara

- Landis+Gyr

- Oracle

- Itron

TOP PLAYERS IN THE MARKET

- General Electric Company is a pivotal player in the United States smart grid market, offering comprehensive solutions for grid automation, energy management, and digital transformation. The company leverages its Grid Solutions portfolio to provide utilities with advanced hardware and software that enhance reliability and efficiency. Recent actions include the expansion of its digital twin technology, which allows utilities to simulate grid operations and predict potential failures before they occur. General Electric has also invested heavily in cybersecurity features to protect critical infrastructure from emerging threats. By integrating artificial intelligence into its platforms, the company enables real-time decision-making and optimized asset performance. These initiatives strengthen its market position by delivering innovative tools that help utilities manage complex energy flows and integrate renewable sources effectively while ensuring robust operational resilience.

- Siemens AG contributes significantly to the United States smart grid market through its extensive range of electrification products and digital grid technologies. The company provides smart meters, distribution automation systems, and grid edge solutions that facilitate the transition to a decentralized energy landscape. Recent actions involve the enhancement of its MindSphere platform, which connects physical infrastructure with the digital world to improve monitoring and maintenance capabilities. Siemens has partnered with various utility providers to deploy advanced sensor networks that increase grid visibility and responsiveness. The company focuses on sustainability by offering energy-efficient transformers and switchgear that reduce losses. Siemens strengthens its presence as a leader in modernizing electrical infrastructure by combining hardware expertise with software analytics. Furthermore, they support the integration of diverse energy resources across the nation.

- ABB Ltd plays a crucial role in the United States smart grid market by delivering cutting-edge automation and electrification technologies designed to optimize power distribution. The company offers a wide array of products, including smart substations, microgrid controllers, and electric vehicle charging infrastructure. Recent actions include the development of adaptive grid management systems that automatically adjust to fluctuations in supply and demand. ABB has expanded its collaboration with technology firms to integrate cloud-based analytics into its grid solutions, enhancing data-driven insights for operators. The company emphasizes interoperability, ensuring its devices communicate seamlessly with existing infrastructure. By focusing on resilience and flexibility, ABB helps utilities accommodate renewable energy sources and improve service quality. These strategic efforts reinforce its reputation as a key enabler of smart grid evolution and sustainable energy management in the United States.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States smart grid market primarily focus on integrating artificial intelligence and machine learning to enhance grid predictive maintenance and operational efficiency. Companies are increasingly developing interoperable platforms that allow seamless communication between diverse hardware components and software systems. Strategic partnerships with utility providers and technology firms enable the deployment of comprehensive end-to-end solutions. Investment in cybersecurity measures is prioritized to protect critical infrastructure from evolving digital threats. Expansion of distributed energy resource management systems supports the integration of renewable energy and electric vehicles. Emphasis on cloud-based analytics facilitates real-time data processing and decision making. Continuous innovation in sensor technology improves grid visibility and reliability. These strategies collectively drive growth by addressing complex grid challenges and enabling sustainable energy transitions.

MARKET SEGMENTATION

This research report on the U.S. smart grid market has been segmented and sub-segmented into the following categories.

By End-User

- Utility

- Industrial

- Residential

- Commercial

By Component

- Software

- Hardware

- Services

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.