U.S. Welding Consumables Market Size, Share, Trends, and Growth Analysis Report, Segmented by Product Type, Welding Process, End-Use Industry, and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

$1.46 BnMarket Estimate, 2026

$1.52 BnMarket Forecast, 2034

$2.07 BnCAGR, 2026–2034

3.94%U.S. Welding Consumables Market Report Summary

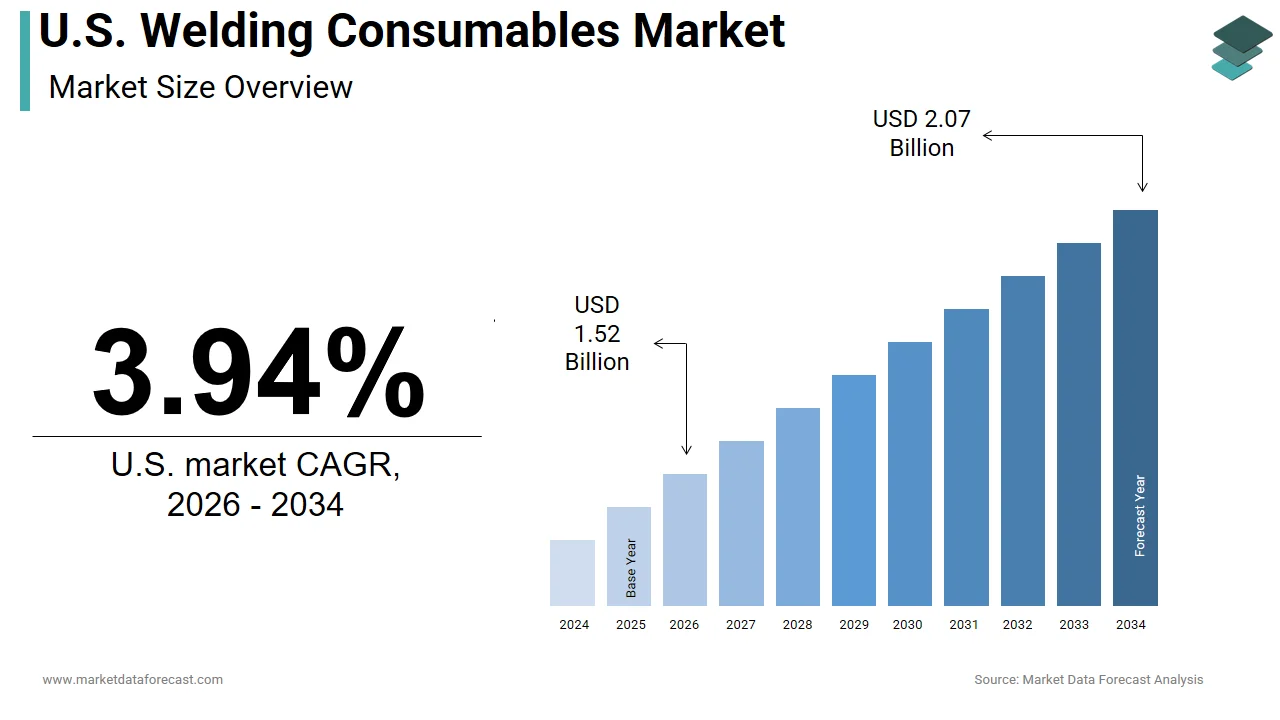

The U.S. welding consumables market was valued at USD 1.46 billion in 2025 and is projected to grow from USD 1.52 billion in 2026 to USD 2.07 billion by 2034, registering a CAGR of 3.94% from 2026 to 2034. Market growth is driven by increasing investments in construction and infrastructure projects, rising manufacturing activities, and growing demand for advanced welding technologies across industrial sectors. Welding consumables, including wires, electrodes, fluxes, and rods, are essential components in fabrication, construction, automotive, shipbuilding, and energy applications. The expansion of industrial automation, infrastructure modernization programs, and demand for high-performance welding solutions are further supporting market growth across the United States.

Key Market Trends

- Rising investments in construction, infrastructure, and industrial development projects.

- Increasing adoption of high-efficiency welding processes and consumables.

- Growing demand for automation and robotic welding solutions.

- Expansion of welding applications in the automotive, energy, and heavy equipment industries.

- Increasing focus on productivity, weld quality, and operational efficiency.

Segmental Insights

- Based on product type, the flux-cored wires segment dominated the U.S. welding consumables market in 2025 by accounting for 34.2% market share, driven by superior deposition rates, high productivity, and suitability for structural and heavy fabrication applications.

- Based on welding process, the gas metal arc welding (GMAW) segment led the market by capturing 45.3% share in 2025, supported by its versatility, efficiency, and widespread adoption across manufacturing and construction industries.

- Based on end-use industry, the construction and infrastructure segment held the dominant share of the market in 2025, driven by increasing investments in commercial buildings, transportation infrastructure, industrial facilities, and public development projects.

Regional Insights

- The United States continues to witness steady demand for welding consumables, supported by infrastructure modernization initiatives, expanding manufacturing output, and growing industrial construction activities. Increasing adoption of advanced welding technologies and automation solutions is further contributing to long-term market growth across the country.

Competitive Landscape

The U.S. welding consumables market is characterized by strong competition among leading welding equipment manufacturers and consumables suppliers focusing on product innovation, operational efficiency, and advanced welding solutions. Market participants are emphasizing the development of high-performance consumables, automation-compatible products, and application-specific welding materials to strengthen market positioning. Strategic partnerships, acquisitions, and investments in research and development are shaping competitive dynamics across the market.

Prominent companies operating in the U.S. welding consumables market include Lincoln Electric Holdings Inc., ESAB Corporation, Illinois Tool Works Inc., Kobe Steel Ltd. (Kobelco Welding of America), and voestalpine Böhler Welding USA.

U.S. Welding Consumables Market Size

The U.S. welding consumables market was valued at USD 1.46 billion in 2025. The market is anticipated to grow at a CAGR of 3.94% from 2026 to 2034, reaching USD 2.07 billion by 2034, up from USD 1.52 billion in 2026.

The welding consumables are the specialized materials essential for joining metals, including electrodes, flux-cored wires, solid wires, and submerged arc wires. These consumables serve as the critical interface in fabrication processes across aerospace, automotive, construction, and energy sectors by ensuring structural integrity and durability of assembled components. As per the American Welding Society, the nation faces a projected shortage of 400,000 skilled welders by 2030, which directly influences consumption patterns as automated welding systems utilizing specific consumables gain traction to mitigate labor gaps. The employment in metalworking occupations remains steady, yet the complexity of modern alloys requires advanced consumable formulations that offer superior arc stability and deposition rates. Regulatory bodies, such as the Occupational Safety and Health Administration, enforce strict guidelines on fume management, driving innovation in low-emission welding products. The geographic concentration of manufacturing hubs in the Midwest and South creates regional demand clusters, while infrastructure projects along the coasts stimulate localized consumption. Technological advancements in alloy development allow for the welding of high-strength steels and exotic metals, expanding application possibilities. The shift towards sustainable manufacturing practices encourages the adoption of consumables with reduced environmental footprints by aligning with corporate sustainability goals.

MARKET DRIVERS

Infrastructure Modernization Initiatives Drive Electrode and Wire Consumption

The extensive modernization of national infrastructure by generating sustained demand for various joining materials across transportation and utility sectors is majorly accelerating the growth of the United States welding consumables market. The Infrastructure Investment and Jobs Act allocates approximately 110 billion dollars for road and bridge repairs, necessitating vast quantities of welding electrodes and flux-cored wires for steel reinforcement and structural assembly. According to the Federal Highway Administration, over 45,000 bridges in the United States are structurally deficient, requiring immediate rehabilitation that relies heavily on field welding techniques using specialized consumables. These projects demand high deposition rate wires to accelerate construction timelines and minimize traffic disruptions, favoring advanced flux-cored and metal-cored products. The expansion of rail networks and transit systems further amplifies this demand, as track laying and station construction require precise and durable welds. State departments of transportation increasingly specify high-toughness consumables to withstand extreme weather conditions and heavy load stresses, driving premium product adoption. The longevity of these infrastructure assets depends on the quality of initial welds, prompting contractors to prioritize certified consumables from reputable manufacturers. This government-backed spending provides a stable baseline for consumable producers, insulating them from volatility in private sector manufacturing. The ripple effect extends to local suppliers and distributors who support these large-scale projects, creating a robust ecosystem around infrastructure-related welding activities.

Expansion of Energy Sector Fabrication Boosts Specialty Consumables Demand

The robust expansion of the energy sector in liquefied natural gas export facilities and renewable energy installations significantly boosts demand for specialty welding consumables capable of handling extreme conditions. This factor is also amplifying the growth of the United States welding consumables market. The United States has become a leading global exporter of liquefied natural gas, with multiple terminals under construction along the Gulf Coast requiring extensive piping and tank fabrication. The natural gas production reached record levels in 2025 by supporting the development of new processing plants that utilize cryogenic-resistant welding wires for nickel alloy and stainless steel components. These applications demand consumables with precise chemical compositions to prevent cracking and ensure leak-tightness at sub-zero temperatures. The wind energy sector also contributes to this growth, as offshore turbine foundations require heavy-duty submerged arc wires for thick-section steel joining. The transition towards hydrogen energy infrastructure further drives innovation in consumables designed for high-pressure and corrosive environments. Manufacturers are developing novel flux formulations that enhance arc stability and reduce hydrogen-induced cracking risks in high-strength steels. The strategic importance of energy independence ensures continued investment in these facilities, providing a lucrative market for high-value-added welding products.

MARKET RESTRAINTS

Volatility in Raw Material Prices Impacts Manufacturing Margins

The fluctuations in the costs of key raw materials, such as steel wire rod, nickel, chromium, and manganese is one of the major factors hindering the growth of the United States welding consumables market. These metals are essential components of electrode coatings and wire cores, and their prices are subject to global commodity market dynamics and geopolitical tensions. According to Trading Economics, the price of nickel experienced a 30% variance in 2025, directly affecting the production costs of stainless steel and nickel-based welding wires. Such volatility makes it difficult for manufacturers to maintain stable pricing structures, often forcing them to absorb cost increases or risk losing customers through price hikes. As per the survey, 60% of consumable producers reported margin compression due to unpredictable raw material expenses, limiting their ability to invest in research and development. The reliance on imported alloys for certain specialty grades exposes domestic manufacturers to currency exchange risks and supply chain disruptions. Tariffs on steel and aluminum imports further complicate sourcing strategies, increasing the cost base for domestic production. Smaller manufacturers lack the purchasing power to hedge against price swings effectively, making them vulnerable to market shocks. This financial instability can lead to reduced product availability or quality compromises as firms seek cheaper alternatives. Customers in price-sensitive sectors may delay purchases or switch to lower-cost competitors, exacerbating revenue fluctuations.

Stringent Environmental Regulations Increase Compliance Costs

The imposition of rigorous environmental regulations regarding welding fumes and hazardous air pollutants is another factor hindering the growth of the United States welding consumables market. The Occupational Safety and Health Administration and the Environmental Protection Agency have tightened limits on exposure to hexavalent chromium and manganese, common elements in welding fluxes and wires. The permissible exposure limits for these substances have been reduced, necessitating the development of low-fume and low-emission consumables that are often more expensive to produce. Manufacturers must invest significantly in reformulating products and conducting extensive testing to meet new safety standards by increasing research and development expenditures. Facilities using traditional consumables face higher costs for ventilation systems and personal protective equipment, discouraging the use of certain high-performance but high-fume products. The transition to cleaner technologies requires collaboration between material scientists and regulatory bodies, slowing down the introduction of new alloys. Small and medium-sized fabrication shops struggle to afford the necessary upgrades, potentially limiting their market participation. Non-compliance risks severe penalties and operational shutdowns, forcing companies to prioritize regulatory adherence over cost efficiency. The push for sustainable manufacturing also demands detailed environmental product declarations, adding administrative burdens to supply chains. These regulatory pressures create a barrier to entry for new players and consolidate market power among larger firms with greater resources for compliance.

MARKET OPPORTUNITIES

Adoption of Automated Welding Systems Creates Premium Product Opportunities

The increasing adoption of robotic and automated welding systems in manufacturing facilities is expected to significantly expand the growth of the United States welding consumables market in the coming years. Automation requires wires and fluxes with tight dimensional tolerances and uniform chemical composition to ensure reliable arc performance and minimal downtime. These systems favor spooled wires and packaged consumables that feed smoothly without tangling or jamming, creating demand for high-end products with superior surface finishes. The automated cells consume consumables at a faster rate than manual operations due to higher duty cycles, boosting overall volume sales. Manufacturers can differentiate themselves by offering technical support and customized solutions for specific robotic platforms by enhancing customer loyalty. The shift towards lights-out manufacturing further accelerates this trend, as factories seek to maximize uptime with reliable materials. The integration of sensors and artificial intelligence in welding robots allows for real-time adjustment of parameters, optimizing consumable usage and reducing waste. This technological synergy enables producers to command higher prices for specialized products that guarantee process stability.

Development of Advanced Alloys for Aerospace and Defense Applications

The continuous advancement in aerospace and defense technologies drives demand for specialized welding consumables capable of joining high-performance alloys, such as titanium, inconel, and advanced high-strength steels. The development of advanced alloys for aerospace and defense applications is set to gear up the growth of the United States welding consumables market. These sectors require materials that withstand extreme temperatures, pressures, and corrosive environments, necessitating precise metallurgical control in consumable formulation. The domestic aircraft production rates are increasing, with major manufacturers ramping up output to meet global demand, thereby boosting the consumption of exotic welding wires. The defense sector’s focus on next-generation vehicles and naval vessels further amplifies this need, as these platforms utilize complex material combinations that require specialized joining techniques. As per military specifications, welding consumables must undergo rigorous qualification processes to ensure structural integrity under combat conditions by creating high barriers to entry, but also securing long-term contracts. The development of additive manufacturing techniques using wire feed systems opens new avenues for consumable innovation, allowing for rapid prototyping and repair of critical components. Manufacturers investing in research for these niche applications can establish strong competitive advantages and brand reputation. The high-value nature of aerospace and defense projects allows for premium pricing, offsetting lower volumes compared to general industrial sectors. Collaboration with original equipment manufacturers during the design phase enables consumable producers to tailor products for specific assembly requirements.

MARKET CHALLENGES

Supply Chain Disruptions Affect Raw Material Availability

The persistent vulnerabilities in the global supply chain by impacting the timely availability of raw materials and finished products, pose a major challenge for the growth of the United States welding consumables market. Geopolitical conflicts and trade restrictions have disrupted the flow of essential alloys, such as nickel and cobalt, leading to production delays and increased lead times. The port congestion and shipping container shortages have intermittently slowed the import of critical inputs by forcing manufacturers to hold higher inventory levels and tie up working capital. These disruptions undermine the reliability of just-in-time manufacturing models with a shift towards more resilient but costly supply chain strategies. The dependence on single-source suppliers for certain rare earth elements used in specialty fluxes creates additional risk exposure, as any interruption can halt entire production lines. As per industry assessments, the lack of transparency in tier two and tier three supplier networks makes it difficult to anticipate and mitigate potential bottlenecks. Labor shortages in the transportation and warehousing sectors further exacerbate delivery delays, impacting customer satisfaction and project schedules. Fabrication shops operating on tight deadlines face penalties for late completions due to material unavailability, straining relationships with suppliers. The unpredictability of supply chain conditions complicates production planning and inventory management by leading to inefficiencies and increased operational costs. Companies are increasingly investing in digital supply chain tools to enhance visibility and responsiveness, but these technologies require significant upfront investment. The ongoing need to balance cost efficiency with supply chain resilience remains a complex strategic challenge for industry participants.

Skilled Labor Shortage Limits Effective Consumable Utilization

The acute shortage of skilled welders that limits the effective utilization of advanced welding consumables is also to impede the growth of the United States welding consumables market. An aging workforce and insufficient vocational training programs have created a gap in the availability of qualified personnel capable of executing complex welding procedures. According to the American Welding Society, the industry needs to train nearly 300,000 new welders by 2030 to meet demand, yet enrollment in trade schools remains insufficient. This labor deficit forces companies to rely on less experienced workers who may struggle with sophisticated consumables requiring precise parameter control, leading to increased rework and material waste. Many manufacturers report difficulties in filling key positions, which is leading to overtime costs and production hurdles. The lack of expertise also slows the adoption of new consumable technologies, as training requirements add to operational burdens. High turnover rates in the welding profession result in loss of institutional knowledge, further complicating quality control efforts. The skills gap impacts not only manual welding but also the operation of automated systems, which require skilled technicians for setup and maintenance. Addressing this challenge requires collaborative efforts between industry associations, educational institutions, and government agencies to develop comprehensive training programs.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Welding Process, End-Use, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Lincoln Electric Holdings Inc., ESAB Corporation, Illinois Tool Works Inc., Kobe Steel Ltd. (Kobelco Welding of America), voestalpine Böhler Welding USA, and Others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The flux-cored wires segment was the largest by holding 34.2% of the United States welding consumables market share in 2025 due to their superior deposition rates and versatility in both semi-automatic and automated welding applications. The heavy fabrication and construction industries, where productivity and weld quality are paramount. The widespread adoption of flux-cored arc welding in structural steel fabrication, which allows for continuous welding without frequent electrode changes. According to the American Welding Society, flux-cored wires account for approximately 40% of total welding wire consumption in the industrial sector, reflecting their critical role in high-volume production environments. The ability of these wires to perform well in outdoor conditions with wind exposure makes them indispensable for infrastructure projects such as bridge building and shipyard operations. Manufacturers have developed advanced formulations that offer better slag detachability and improved mechanical properties, further enhancing their appeal. The construction boom driven by federal infrastructure spending has amplified demand for these efficient consumables, as contractors seek to minimize labor hours while maintaining high standards. Additionally, the compatibility of flux-cored wires with robotic systems supports the trend towards automation in manufacturing facilities.

The metal-cored wires segment is projected to expand at a CAGR of 7.2% throughout the forecast period due to their exceptional performance in high-speed automated welding processes. These wires combine the benefits of solid and flux-cored wires, offering high deposition rates, deep penetration, and minimal post-weld cleanup. The primary growth factor is the increasing adoption of robotics in the automotive and aerospace industries, where precision and speed are critical. According to the Association for Advancing Automation, the integration of metal-cored wires in robotic cells has improved welding speeds by up to 30% compared to traditional solid wires, which is significantly boosting production throughput. The automotive manufacturers are increasingly using metal-cored wires for joining advanced high-strength steels, which require stable arcs and consistent bead profiles to ensure structural integrity. The reduced fume generation of modern metal-cored wires also aligns with stricter workplace safety regulations by making them attractive for indoor fabrication shops. The ability to weld thicker materials in a single pass reduces the number of passes required, lowering overall energy consumption and labor costs. Furthermore, advancements in wire formulation have improved feedability, reducing downtime associated with wire feeding issues in automated systems. The growing demand for lightweight vehicles and complex aerospace components necessitates joining techniques that metal-cored wires uniquely provide.

By Welding Process Insights

The gas metal arc welding segment accounted in holding 45.3% of the United States welding consumables market share in 2025 due to its versatility and ease of automation. This process is widely utilized in manufacturing, automotive, and construction sectors because it allows for continuous wire feeding, which enhances productivity and reduces operator fatigue. The process's compatibility with robotic systems has further promoted its dominance, as manufacturers seek to automate repetitive tasks to address labor shortages. The development of synergic power sources has simplified parameter selection by allowing less experienced operators to achieve high-quality welds. The availability of various shielding gases and wire diameters enables customization for specific joint configurations and material thicknesses. The construction industry relies heavily on this process for structural steel assembly, where speed and reliability are crucial. Additionally, the lower skill threshold required for basic operations compared to manual stick welding expands the pool of potential users.

The friction stir welding segment is swiftly emerging at a fastest CAGR of 8.5% during the forecast period, with its ability to join lightweight alloys without melting the base material. The increasing use of aluminum and magnesium alloys in vehicle manufacturing to improve fuel efficiency and reducing emissions. The process produces joints with superior mechanical properties and fatigue resistance compared to traditional methods, making it ideal for critical structural applications. The environmental benefits of Friction Stir Welding, including the absence of harmful fumes and radiation, align with sustainable manufacturing goals. The automotive industry is also exploring this technology for battery tray assembly in electric vehicles, where leak tightness and strength are paramount. Although initial equipment costs are higher, the long-term savings in material waste and post-weld processing justify the investment. The expansion of application areas beyond aerospace into marine and rail transport further accelerates market growth.

By End Use Industry Insights

The construction and infrastructure segment was the largest by accounting for a dominant share of the United States welding consumables market in 2025, with the extensive public and private investment in building and civil engineering projects. This sector consumes a vast quantity of electrodes and wires for structural steel erection, bridge fabrication, and reinforcement bar joining. According to the Census Bureau, construction spending on nonresidential structures reached 980 billion dollars in 2025, creating sustained demand for welding materials across commercial and industrial projects. The need for durable and code-compliant joints in high-rise buildings and large span structures ensures consistent consumption of high-quality consumables. The majority of structural steel connections are made using field welding techniques, which rely heavily on stick electrodes and flux-cored wires. The renovation of aging infrastructure, including dams and water treatment plants, further amplifies this demand. Urbanization trends continue to drive vertical construction in major metropolitan areas, requiring specialized welding solutions for complex geometries. The resilience of steel as a building material ensures its continued preference over alternatives, supporting steady market growth. Additionally, the repair and maintenance of existing structures constitute a significant portion of activity by providing a stable baseline for consumable sales.

The energy segment is likely to grow at an anticipated CAGR of 6.8% from 2026 to 2034 with the expansion of liquefied natural gas facilities and renewable energy installations. The transition towards cleaner energy sources and the strategic push for energy independence have spurred significant investment in pipeline infrastructure and processing plants. According to the Energy Information Administration, natural gas production and export capacity expansions have led to a 15% increase in welding activity for cryogenic and high-pressure piping systems in 2025. These applications require specialized consumables capable of joining nickel alloys and stainless steels that withstand extreme temperatures and corrosive environments. The construction of offshore wind farms along the Atlantic coast has created new demand for heavy-duty submerged arc wires used in foundation fabrication. The oil and gas sector continues to invest in maintenance and replacement of aging pipelines by ensuring steady consumption of repair-oriented products. The emergence of hydrogen energy infrastructure presents additional opportunities for advanced welding technologies that prevent embrittlement in high-strength steels. Regulatory mandates for safety and environmental protection drive the adoption of premium consumables that offer superior joint integrity. The geographic concentration of energy projects in specific regions creates localized spikes in demand, influencing distribution strategies.

COMPETITIVE LANDSCAPE

The competition in the United States welding consumables market is characterized by the presence of established global corporations and specialized regional manufacturers vying for dominance in diverse industrial segments. Intense rivalry exists due to the commoditized nature of standard products, prompting firms to differentiate through technical expertise, product quality, and service reliability. Major players leverage economies of scale to offer competitive pricing while investing in advanced research and development to create high-performance alloys for demanding applications. Price volatility in raw materials adds complexity to competitive dynamics by forcing companies to adopt sophisticated supply chain management strategies. Customer loyalty plays a crucial role as industrial buyers prioritize consistent quality and technical support over minor price differences. Innovation in sustainable and low-fume products provides avenues for differentiation beyond traditional metrics. The presence of imported goods creates additional pressure, leading domestic producers to emphasize local manufacturing and rapid delivery capabilities.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. welding consumables market include

- Lincoln Electric Holdings Inc.

- ESAB Corporation

- Illinois Tool Works Inc.

- Kobe Steel Ltd. (Kobelco Welding of America)

- voestalpine Böhler Welding USA

TOP PLAYERS IN THE MARKET

- Lincoln Electric Holdings Inc stands as a premier provider of welding solutions in the United States, offering a comprehensive portfolio of consumables, including electrodes, wires, and fluxes. The company leverages its extensive distribution network to serve diverse industries such as construction, automotive, and energy. Recent initiatives focus on digital integration, with the launch of advanced welding software that optimizes consumable usage and improves process efficiency. Lincoln Electric actively invests in research and development to create low-fume products that meet stringent environmental regulations.

- ITW Welding North America contributes significantly to the market through its specialized brands like Hobart and Miller Electric, which are renowned for reliability and performance. The company focuses on delivering high-value-added consumables tailored for specific industrial applications, particularly in heavy fabrication and repair sectors. Recent efforts include the development of proprietary alloy formulations that enhance arc stability and deposition rates for automated systems. ITW emphasizes customer-centric innovation by collaborating closely with end users to solve complex joining challenges. The firm also strengthens its supply chain resilience by localizing production capabilities and reducing lead times for important projects.

- ESAB Corporation plays a vital role in the United States welding consumables market by providing a wide range of filler metals and associated equipment for industrial and commercial use. The company is known for its commitment to sustainability, producing eco-friendly consumables that reduce environmental impact without compromising performance. Recent actions include the expansion of its manufacturing facilities to increase capacity for high-demand products, such as flux-cored and metal-cored wires. ESAB actively engages in strategic partnerships with technology firms to integrate smart features into welding processes by enhancing productivity and safety. The firm also prioritizes workforce development by supporting educational initiatives that train the next generation of welders.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States welding consumables market primarily employ product differentiation strategies by developing specialized alloys and low-emission formulations to meet specific industry needs. Companies invest heavily in research and development to innovate consumables that enhance welding speed and quality for automated systems. Strategic acquisitions and partnerships allow firms to expand their geographic reach and diversify their product portfolios effectively. Participants also focus on digital transformation by integrating software solutions that optimize consumable usage and provide real-time process monitoring. Sustainability initiatives are central to corporate strategies, with manufacturers adopting cleaner production methods to comply with environmental regulations. Additionally, companies prioritize customer education and training programs to address skilled labor shortages and build long-term brand loyalty. These combined approaches enable firms to maintain competitive advantages and adapt to evolving market demands while fostering innovation and operational excellence in the welding industry.

MARKET SEGMENTATION

This research report on the U.S. welding consumables market has been segmented and sub-segmented into the following categories.

By Product Type

- Stick Electrodes

- Solid Wires

- Flux-Cored Wires

- SAW Flux & Wire

- TIG Rods & Brazing Alloys

By Welding Process

- Arc

- SMAW (Stick)

- GMAW / MIG

- GTAW / TIG

- FCAW

- Resistance Welding

- Laser & Hybrid Welding

By End-Use Industry

- Construction & Infrastructure

- Automotive & Transportation

- Energy (Oil, Gas & Power)

- Shipbuilding & Offshore

- Heavy Equipment & Industrial Machinery

- Others

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. welding consumables market?

The U.S. welding consumables market includes welding electrodes, welding wire, flux, filler metals, and shielding gases used in welding processes across the United States for industrial and construction applications.

Why is the U.S. welding consumables market growing?

The U.S. welding consumables market is growing due to infrastructure development, manufacturing expansion, automotive production, construction activities, and increasing demand for reliable welding solutions nationwide.

Who uses products from the U.S. welding consumables market?

Manufacturers, construction companies, automotive plants, shipyards, pipeline contractors, repair shops, and industrial fabrication facilities use the U.S. welding consumables market for welding operations.

What types of consumables are in the U.S. welding consumables market?

The U.S. welding consumables market includes stick electrodes, MIG wire, TIG rods, flux-cored wire, submerged arc flux, filler metals, and shielding gases for various welding processes.

How does manufacturing impact the U.S. welding consumables market?

Manufacturing drives the U.S. welding consumables market through demand for fabrication, assembly, repair, automation-compatible consumables, and high-quality welding materials for industrial production.

What challenges face the U.S. welding consumables market?

Challenges in the U.S. welding consumables market include raw material price volatility, supply chain disruptions, skilled labor shortages, quality consistency, and competition from imported welding products.

Which industries drive the U.S. welding consumables market most?

Automotive, construction, oil and gas, aerospace, shipbuilding, heavy machinery, and infrastructure projects drive the largest demand in the U.S. welding consumables market.

How does automation affect the U.S. welding consumables market?

Automation shapes the U.S. welding consumables market through demand for machine-compatible wire, consistent quality consumables, high deposition rates, and materials optimized for robotic welding systems.

What role does infrastructure development play in the U.S. welding consumables market?

Infrastructure development is central to the U.S. welding consumables market, driving demand for pipeline welding, structural steel fabrication, bridge construction, and heavy equipment manufacturing.

Is the U.S. welding consumables market competitive?

Yes, the U.S. welding consumables market is highly competitive with major manufacturers, regional suppliers, private label products, quality differentiation, and pricing competition across welding material categories.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com