Global Vascular Access Devices Market Size, Share, Trends & Growth Forecast Report By Type, By Application, By End User, and By Region (North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa) – Industry Analysis and Forecast, 2026 to 2034

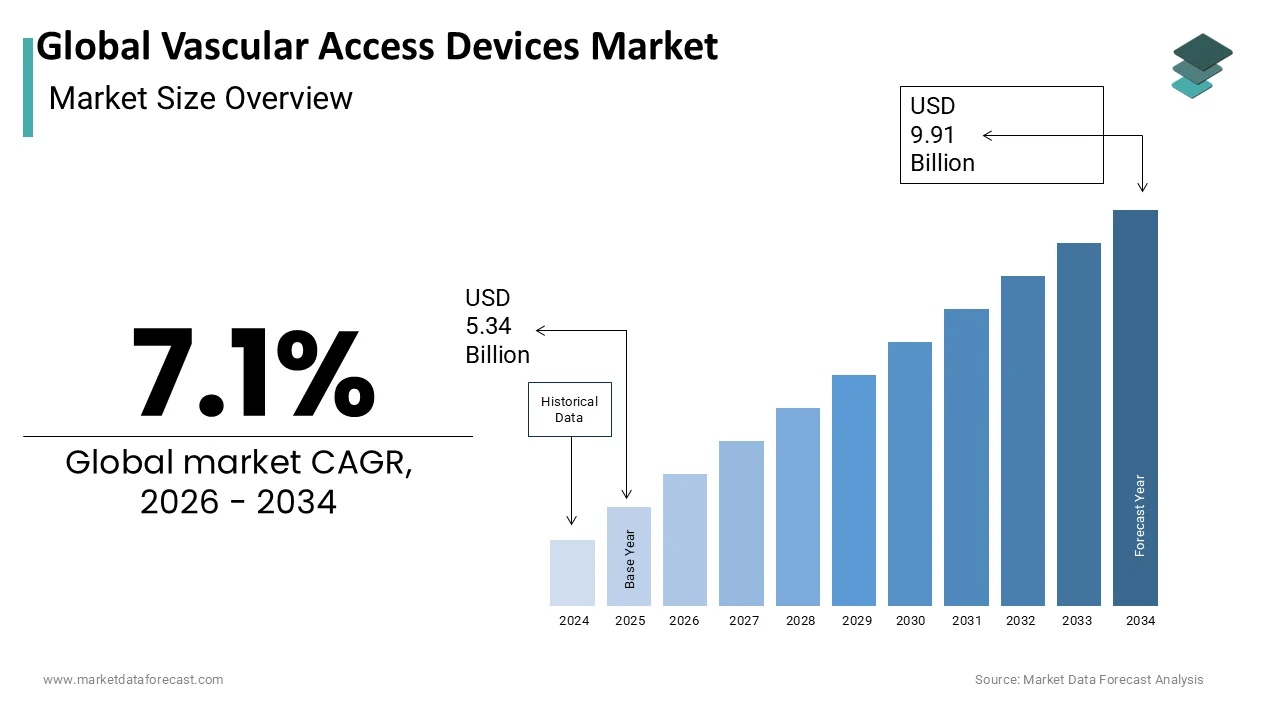

Market Size, 2025

$5.34 BnMarket Estimate, 2026

$5.72 BnMarket Forecast, 2034

$9.91 BnCAGR, 2026–2034

7.1%Global Vascular Access Devices Market Size

The Global Vascular Access Devices Market was valued at USD 5.34 billion in 2025, is estimated to reach USD 5.72 billion in 2026, and is projected to reach USD 9.91 billion by 2034, growing at a CAGR of 7.1% from 2026 to 2034.

Vascular access devices (VADs) are medical tools used to gain entry into the vascular system for the administration of fluids, medications, blood products, and nutritional support. These devices range from peripheral intravenous catheters to more complex central venous and arterial lines, including implantable ports and dialysis catheters. Their use is essential in both acute and chronic care settings, particularly in oncology, critical care, nephrology, and home healthcare.

The global shift toward minimally invasive procedures and the rising prevalence of chronic diseases have significantly increased the demand for vascular access solutions. According to the Centers for Disease Control and Prevention (CDC), approximately 15 million patients in the United States receive central venous catheters annually, underscoring the widespread reliance on these devices across hospital environments.

Technological advancements, including antimicrobial-coated catheters and ultrasound-guided insertion techniques, have enhanced safety and efficiency in vascular access procedures. As healthcare systems emphasize infection control and improved patient outcomes, the role of advanced vascular access devices has become increasingly vital. This evolving clinical landscape continues to shape the trajectory of the VAD market, setting the stage for deeper exploration of its growth drivers.

MARKET DRIVERS

Increasing Prevalence of Chronic Diseases

One of the primary drivers of the Vascular Access Devices Market is the growing prevalence of chronic diseases such as cancer, diabetes, cardiovascular disorders, and end-stage renal disease (ESRD). These conditions often necessitate frequent intravenous therapies, chemotherapy, or hemodialysis, all of which rely heavily on vascular access devices.

According to the World Health Organization (WHO), non-communicable diseases accounted for 71% of all global deaths in 2023 , with a significant proportion requiring long-term vascular access for treatment. In the U.S., the American Cancer Society estimated that nearly 2 million new cancer cases were diagnosed in 2023 , many of which required central venous catheters for chemotherapy delivery.

The increasing geriatric population, which is more prone to such chronic illnesses, further amplifies demand. With life expectancy rising globally and comorbidities becoming more common, the need for reliable vascular access solutions is expected to grow steadily, reinforcing the expansion of this market segment.

Expansion of Home Healthcare and Ambulatory Care Settings

Another key driver of the Vascular Access Devices Market is the rapid expansion of home healthcare and ambulatory care services. Patients increasingly prefer receiving treatment in less restrictive environments, leading to a surge in outpatient procedures and home-based infusion therapies.

As per data published by the Agency for Healthcare Research and Quality (AHRQ), home infusion therapy utilization in the U.S. grew by nearly 40% between 2020 and 2023 , driven by cost savings, convenience, and technological advancements that enable safe vascular access outside hospitals. The trend is particularly evident in oncology and chronic disease management, where patients require ongoing intravenous treatments without extended hospital stays.

Apart from these, the rise in ambulatory surgical centers (ASCs) has contributed to higher adoption rates of short-term vascular access devices. This shift toward decentralized care models is reshaping vascular device usage patterns and fostering market growth.

MARKET RESTRAINTS

Risk of Catheter-Related Bloodstream Infections

A major restraint affecting the Vascular Access Devices Market is the persistent risk of catheter-related bloodstream infections (CRBSIs), which pose serious health threats and increase healthcare costs. Despite advances in device design and infection control protocols, CRBSIs remain a significant clinical challenge.

According to the Centers for Disease Control and Prevention (CDC), approximately 30,000 cases of central line-associated bloodstream infections (CLABSIs) occur annually in U.S. hospitals , contributing to prolonged hospitalization, increased mortality, and added financial burden.

These complications have prompted regulatory agencies and healthcare institutions to adopt stricter guidelines on vascular access hygiene and device selection. While these measures improve patient safety, they also slow down device adoption due to heightened scrutiny and training requirements. Furthermore, legal liabilities associated with infection outbreaks discourage some healthcare providers from using certain types of vascular access devices, limiting market expansion despite high underlying demand.

High Cost of Advanced Vascular Access Devices

Another significant restraint in the Vascular Access Devices Market is the high cost associated with technologically advanced devices, which limits their accessibility—particularly in low- and mid-tier healthcare facilities. Devices equipped with antimicrobial coatings, anti-thrombotic properties, or real-time monitoring capabilities come at a premium, making them less affordable for budget-constrained institutions.

These pricing disparities affect purchasing decisions, especially among smaller hospitals and clinics that prioritize cost-efficiency over innovation.

In addition, reimbursement policies in several regions do not fully cover the cost of premium vascular access devices. Consequently, despite proven clinical benefits, the economic barriers associated with advanced vascular access technology hinder broader market penetration.

MARKET OPPORTUNITIES

Integration of Smart and Connected Vascular Access Technologies

An emerging opportunity in the Vascular Access Devices Market lies in the integration of smart and connected technologies that enhance device functionality and improve patient monitoring. Innovations such as wireless sensors, real-time flow monitoring, and antimicrobial detection systems are being incorporated into vascular access devices to reduce complications and streamline clinical workflows.

For instance, companies like BD (Becton, Dickinson and Company) and B. Braun have introduced smart infusion systems that integrate with electronic health records (EHRs) to provide clinicians with real-time feedback on vascular access performance. According to a 2023 study published in Critical Care Medicine , hospitals utilizing smart infusion pumps experienced a 25% reduction in medication errors and a 30% decline in catheter-related complications , demonstrating the potential of digital integration in vascular care.

Furthermore, wearable vascular access monitors are gaining traction in home healthcare settings, allowing remote tracking of catheter function and early detection of blockages or infections. The increasing adoption of telehealth platforms and the push for personalized medicine create a favorable environment for the commercialization of next-generation vascular access technologies, offering substantial growth potential for market participants.

Growth in Oncology and Dialysis Treatments

The expanding scope of oncology and dialysis treatments presents a significant opportunity for the Vascular Access Devices Market. With rising cancer incidence and chronic kidney disease prevalence, the demand for durable, long-term vascular access solutions is surging.

According to the American Society of Clinical Oncology (ASCO), chemotherapy remains a cornerstone of cancer treatment, with over 65% of patients undergoing some form of systemic therapy , most of which requires central venous access.

To meet this demand, manufacturers are developing specialized vascular access products tailored for oncology and nephrology applications. For example, implantable ports designed for frequent chemotherapy infusions and dialysis-specific catheters with reduced thrombogenicity are witnessing strong uptake.

MARKET CHALLENGES

Regulatory Complexity and Compliance Requirements

One of the major challenges facing the Vascular Access Devices Market is the increasing complexity of regulatory frameworks governing medical device approvals and compliance standards. Manufacturers must navigate stringent regulations imposed by agencies such as the U.S. Food and Drug Administration (FDA), European Medicines Agency (EMA), and other national bodies to ensure product safety and efficacy.

The FDA’s Medical Device Reporting (MDR) program mandates rigorous post-market surveillance, requiring companies to submit detailed reports on adverse events and device malfunctions. In 2023, the FDA issued over 120 warning letters related to medical device quality violations , many of which pertained to vascular access products. Such regulatory scrutiny increases time-to-market and development costs, particularly for smaller firms lacking robust compliance infrastructure.

Moreover, international expansion is complicated by varying regional requirements. As regulatory landscapes evolve, manufacturers face heightened pressure to invest in quality assurance and clinical validation, impacting overall market agility.

Shortage of Skilled Healthcare Professionals

Another pressing challenge in the Vascular Access Devices Market is the shortage of skilled healthcare professionals trained in proper device insertion, maintenance, and complication management. Effective vascular access requires technical expertise, particularly for complex procedures such as central line placement and dialysis catheter management.

According to the American Association of Critical-Care Nurses (AACN), nearly 40% of ICU nurses reported insufficient training in advanced vascular access techniques , leading to variability in clinical outcomes.

This skills gap is exacerbated by workforce shortages in nursing and allied health professions. Without adequate training and staffing, even the most advanced vascular access devices may fail to deliver their intended clinical benefits, posing a barrier to market growth.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, End-User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leader Profiled | Becton Dickinson and Company, C.R.Bard Inc., Smiths Medical, Inc., Teleflex Incorporated, B Braun Melsungen Ag |

SEGMENTAL ANALYSIS

By Type Insights

Based on vascular access devices, the central vascular access devices segment is expected to occupy most of the share in the global market due to its practical use in chemotherapy treatment. These are specific devices inserted into the body through a vein, like subclavian or jugular vein by ports, or inserted into one of the peripheral veins by PICCs, to allow delivery of fluids, blood products, medications, and other therapies into the blood flow.

Peripheral catheters are also expected to grow over the forecast period owing to their nature of most widely accepted catheters in the world due to their various benefits of ease of insertion, cost-effectiveness, high profitability, much shorter duration of use, reduced risk of complications, and mostly, its ease of administration over central catheters.

By Application Insights

The Drug Administration application segment commanded the Vascular Access Devices Market, capturing nearly 45% of total market share in 2024. This segment's overwhelming dominance is directly linked to the essential role vascular access plays in delivering medications, especially in oncology, infectious disease management, and chronic condition treatments.

A major contributing factor is the high frequency of intravenous (IV) drug delivery in modern healthcare. According to the Centers for Disease Control and Prevention (CDC), more than 90% of hospitalized patients receive at least one IV medication during their stay , highlighting the indispensable nature of vascular access in clinical settings.

In addition, the rise in antibiotic-resistant infections has led to an increase in long-term IV antibiotic therapy, further fueling demand. With pharmaceutical advancements continuing to favor IV formulations for potency and bioavailability, the vascular access market remains closely tied to the expanding scope of parenteral drug delivery.

The Diagnostics Testing application segment is anticipated to grow at the fastest CAGR of 9.3%. This rapid expansion is fueled by the increasing reliance on blood sampling and real-time monitoring through vascular access points, particularly in intensive care units, emergency departments, and chronic disease management programs.

A key driver is the growing integration of vascular access devices in point-of-care diagnostics and continuous blood monitoring systems. According to the Society of Critical Care Medicine (SCCM), critically ill patients in ICUs undergo an average of 4–6 blood draws daily , necessitating dedicated arterial or venous access lines for efficient sample collection. The emergence of smart vascular access technologies that allow simultaneous infusion and blood withdrawal without line contamination is accelerating adoption.

Furthermore, the rise in chronic diseases such as diabetes and cardiovascular disorders has increased the need for regular biomarker testing, including glucose, lactate, and electrolyte levels. As healthcare moves toward more integrated and data-driven models, vascular access for diagnostics is set to expand rapidly.

By End User Insights

Based on end-user, the hospitals are regarded to account for the largest share due to the hospitals' major vascular access devices, advanced healthcare infrastructure, high traffic environment, presence of experienced medical professionals, and availability of various medical machines as a result of growing demand for minimally invasive procedures leading to increase in the number of surgeries for vascular diseases.

The clinics and ambulatory care centers, on the other hand, are the fastest growing healthcare facilities and are proving it by gaining patients' satisfaction with the outcome of the surgery, low cost, and quality of care they receive and also impressed with the way the facility is run, which is why the ambulatory care centers are also expected to grow over the forecast period.

REGIONAL ANALYSIS

North America held the largest share of the global Vascular Access Devices Market. The region maintains its dominant position due to a well-established healthcare infrastructure, high prevalence of chronic diseases, and robust investment in medical device innovation.

One key driver is the substantial burden of cancer and kidney disease, which necessitates frequent vascular access interventions. Besides, North America leads in the adoption of advanced vascular access technologies, including antimicrobial-coated catheters and smart infusion systems. With strong regulatory support and increasing focus on infection control, North America remains at the forefront of vascular access device utilization and development.

Europe accounts for a notable share of the global Vascular Access Devices Market. The region’s market strength is underpinned by its mature healthcare systems, stringent regulatory standards, and growing emphasis on patient safety and infection prevention.

Germany stands out as a key contributor, hosting several leading manufacturers and research institutions focused on vascular access technology.

The United Kingdom also plays a pivotal role, particularly in the field of home-based vascular access care.

The Asia-Pacific region is emerging as a high-growth area in the Vascular Access Devices Market. This expansion is primarily driven by rising healthcare expenditure, growing prevalence of chronic illnesses, and improving medical infrastructure across countries like China, India, and Japan.

India, in particular, has witnessed a surge in demand for vascular access solutions due to increasing cancer incidence and diabetic complications. Additionally, the country’s burgeoning private healthcare sector is investing in advanced vascular access technologies to meet international standards.

China, on the other hand, is leveraging domestic manufacturing capabilities to reduce dependency on imported devices. With rising disposable incomes and expanding insurance coverage, the Asia-Pacific region is expected to continue its upward trajectory in vascular access device adoption over the next decade.

Latin America is still a smaller player compared to North America and Europe, the region is experiencing gradual growth due to increasing healthcare investments and rising awareness of advanced vascular care practices.

Brazil leads the regional market, driven by government initiatives aimed at improving public healthcare services. Besides, partnerships between multinational device manufacturers and local distributors have facilitated better availability of high-quality vascular access products.

Mexico is also showing promise, particularly in urban centers where private healthcare facilities are adopting newer vascular technologies. Despite economic fluctuations and limited reimbursement structures, Latin America presents untapped potential for market expansion as healthcare systems continue to evolve.

The Middle East and Africa remains relatively underdeveloped, certain Gulf Cooperation Council (GCC) countries are driving progress through healthcare modernization efforts and increased foreign investment.

The United Arab Emirates (UAE) leads the region in terms of healthcare spending and infrastructure development. The country’s growing expatriate population and rising prevalence of lifestyle-related diseases have also contributed to increased demand for intravenous therapies and dialysis access.

South Africa, despite economic challenges, is another focal point for vascular access device adoption. With ongoing improvements in healthcare policy and increasing private sector participation, the Middle East and Africa offer promising yet nascent opportunities for future market growth.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Some of the notable participants dominating the global vascular access devices market profiled in this report are Becton Dickinson and Company, C.R.Bard Inc., Smiths Medical, Inc., Teleflex Incorporated, B Braun Melsungen Ag, AngioDynamics, Terumo Corporation, Nipro Medical Corporation, Edwards Lifesciences Corporation, Ameco Medical, Romsons Scientific & Surgical Pvt. Ltd and Prodimed.

The competition in the vascular access devices market is highly dynamic, shaped by continuous technological advancements, evolving clinical guidelines, and increasing demand for safer, more efficient vascular access solutions. Established multinational corporations dominate the landscape, leveraging their extensive distribution networks, brand recognition, and R&D capabilities to maintain leadership positions. However, regional players and emerging startups are gaining traction by offering cost-effective alternatives and niche innovations tailored to specific clinical applications.

Market participants are increasingly focusing on differentiation through product design enhancements, integration of smart technologies, and improved safety features that reduce infection risks and enhance ease of use for healthcare professionals. Strategic collaborations between device manufacturers and healthcare providers are also playing a crucial role in shaping clinical adoption patterns and influencing purchasing decisions. Additionally, regulatory scrutiny and reimbursement policies significantly impact market dynamics, prompting companies to align their offerings with evolving compliance requirements while maintaining affordability and accessibility across different healthcare settings. As demand for minimally invasive and long-term vascular access continues to grow, the industry remains poised for sustained innovation and competitive evolution.

Top Players in the Market

Becton, Dickinson and Company (BD)

BD is a global leader in medical technology, with a strong presence in the vascular access devices market. The company offers a comprehensive portfolio of peripheral and central venous access products, including safety-engineered catheters, PICCs, and implantable ports. BD’s commitment to innovation is evident through its continuous development of antimicrobial-coated and needle-free vascular access solutions aimed at reducing healthcare-associated infections and improving patient outcomes.

B. Braun Melsungen AG

B. Braun is a major player known for its high-quality vascular access devices tailored for acute care, oncology, and home infusion settings. The company emphasizes patient and clinician safety by integrating advanced features such as anti-reflux valves and antimicrobial protection into its catheter designs. B. Braun also collaborates closely with healthcare institutions to develop evidence-based vascular access protocols that enhance clinical efficiency and reduce complications associated with intravenous therapy.

Teleflex Incorporated

Teleflex has established itself as a key innovator in vascular access with a focus on specialty catheters and ultrasound-guided insertion systems. Its product lines include Arrow-branded vascular access devices, which are widely used in critical care and dialysis applications. Teleflex prioritizes research and development to introduce technologically advanced solutions that improve accuracy, reduce infection risks, and support better clinical decision-making in vascular care across diverse healthcare environments.

Top Strategies Used by Key Market Participants

Product Innovation and Technological Advancement

Leading companies in the vascular access devices market prioritize continuous product innovation to meet evolving clinical needs. They invest heavily in R&D to develop next-generation devices featuring antimicrobial coatings, real-time monitoring capabilities, and enhanced safety mechanisms designed to minimize complications and improve patient outcomes.

Strategic Acquisitions and Partnerships

To expand their market reach and strengthen product portfolios, key players engage in strategic acquisitions and collaborative partnerships with smaller firms and research institutions. These moves allow them to integrate cutting-edge technologies, accelerate time-to-market for new products, and enhance their competitive positioning across global healthcare sectors.

Focus on Global Expansion and Regulatory Compliance

Major market participants actively pursue geographic expansion, particularly in emerging markets with growing healthcare infrastructure. Simultaneously, they ensure compliance with international regulatory standards to facilitate smoother market entry and maintain product credibility across diverse healthcare ecosystems.

RECENT HAPPENINGS IN THE MARKET

In January 2025, BD launched a new line of antimicrobial-coated central venous catheters designed specifically for intensive care units, aiming to reduce catheter-related bloodstream infections and reinforce its leadership in hospital infection control.

In March 2025, B. Braun expanded its manufacturing facility in Tuttlingen, Germany, to increase production capacity for safety-engineered vascular access devices, supporting rising global demand and strengthening supply chain resilience.

In June 2025, Teleflex introduced an integrated ultrasound guidance system for vascular access procedures, enhancing precision and reducing complications in difficult insertions, particularly in emergency and ambulatory care settings.

In August 2025, Smiths Medical announced a strategic partnership with a digital health platform provider to develop connected vascular access devices capable of real-time flow monitoring and remote data transmission for home healthcare applications.

In October 2025, ICU Medical unveiled a redesigned range of closed-system IV connectors intended to prevent contamination and streamline fluid administration, reinforcing its position in the ambulatory and oncology infusion markets.

MARKET SEGMENTATION

This research report on the global vascular access devices market has been segmented and sub-segmented based on the type, application, end-user, and region.

By Type

- Peripheral Vascular Access Devices

- Implanted Ports

By Application

- Drug Administration

- Diagnostics Testing

By End- User

- hospitals

- clinics and ambulatory care centers

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

How much is the global Vascular Access Devices Market going to be worth by 2033?

As per our research report, the global Vascular Access Devices Market size is projected to be USD 9.25 billion by 2033.

Which region is growing the fastest in the global Vascular Access Devices Market ?

Geographically, the North American Vascular Access Devices Market accounted for the largest share of the global market in 2024.

At What CAGR, the global Vascular Access Devices Market is expected to grow from 2024 to 2033?

The global Vascular Access Devices Market is estimated to grow at a CAGR of 7.1% from 2024 to 2033.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com