Global Cannabidiol Market Size, Share, Trends & Growth Forecast Report By Type (Hemp and Marijuana), Distribution Channel (B2B and B2C), End-User (Medical, Personal Use, Pharmaceuticals and Wellness) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis (2025 to 2033)

Global Cannabidiol Market Size

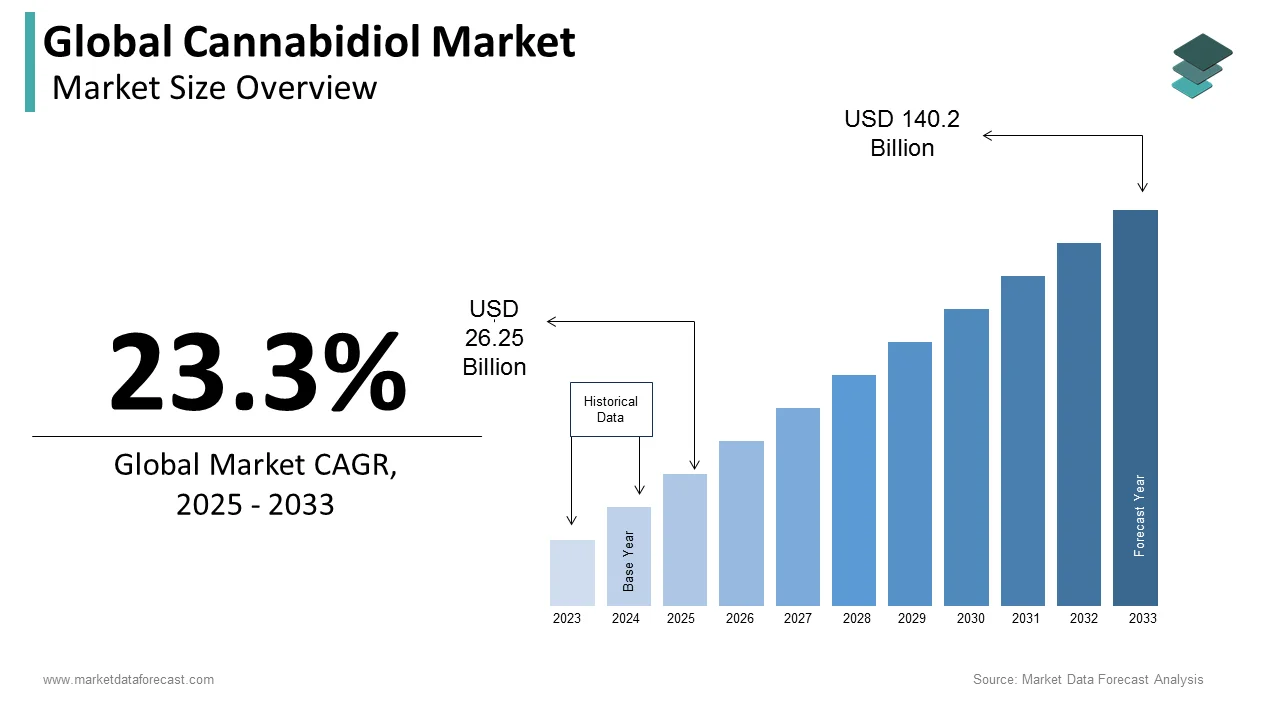

The global cannabidiol market was valued at USD 21.29 billion in 2024 and is expected to expand at a compound annual growth rate (CAGR) of 23.3% from 2025 to 2033 and be worth USD 140.2 billion by 2033 from USD 26.25 billion in 2025.

Cannabidiol, commonly referred to as CBD, represents one of the most significant components of the cannabis plant and is increasingly acknowledged worldwide for its therapeutic potential without inducing psychoactive effects. Its expanding role in healthcare, wellness, personal care, and food sectors has placed it at the centre of global discourse on plant-based remedies. Unlike tetrahydrocannabinol, CBD does not impair cognitive function, which has accelerated its acceptance across diverse consumer demographics.

MARKET DRIVERS

Regulatory Reform and Broader Legalization of Hemp-Derived CBD

The evolving legal frameworks globally have unlocked access to markets and significantly lifted barriers for cannabidiol product development and sales, which is majorly leveraging the growth of the MEA medical tourism market. Many countries have clarified or loosened laws around hemp and CBD, especially when THC content is very low. Regulatory bodies in North America, parts of Latin America, Europe, and Asia are progressively approving hemp-derived CBD for wellness, foods, cosmetics, and pharmaceuticals. Legal clarity around novel food or dietary supplement status in many jurisdictions has allowed companies to launch more mainstream CBD-infused products.

Rising Consumer Demand for Wellness Lifestyle and Alternative Therapeutic Solutions

Globally, consumers are becoming more health-conscious and seeking nonprescription, natural remedies for common ailments such as anxiety, pain, sleep disorders, inflammation, and skin conditions, which additionally leverages the growth of the cannabidiol market. Concurrently, the global market is being powered by product innovation: novel ingestible forms, edibles, topicals, beverages, skincare, and pet care are expanding rapidly. Rising online retail channels magnify that because consumers can access a wider variety of finished CBD goods conveniently. Wellness trends favor plant-based and clean label formulations, which is pushing consumers away from synthetic or high side-effect medications.

MARKET RESTRAINTS

Regulatory fragmentation and safety data gaps

Regulatory fragmentation and safety data gaps are constraining global cannabidiol adoption and raising compliance costs, which is restraining the growth of the MEA medical tourism market. NutraIngredients reported in September 2025 that EFSA’s updated analysis has led to proposed very low reference values near two milligrams per day for oral consumption pending further data. The FDA has also urged Congress to provide a clear statutory pathway because current regulatory tools are inadequate to manage long-term safety questions.

Product quality variability, contamination, and enforcement pressure

The product quality variability, contamination and intensifying are hindering the growth of the MEA medical tourism market. Independent and governmental testing programs have repeatedly found wide variability between labelled and actual cannabidiol content and frequent detections of contaminants including pesticide residues, heavy metals, and undeclared cannabinoids, which undermines consumer trust and creates recall risk, as reported in regulatory summaries and industry testing rundowns.

MARKET OPPORTUNITIES

Expansion of the CBD Pet Care Segment

The CBD pet care space is leveraging the growth of the cannabidiol market. Spending on natural supplements and wellness products for pets rises sharply. Also, regulatory environments in many countries are gradually clarifying the legality of hemp-derived CBD in pet products, which helps reduce risk for manufacturers.

Growth in Nutraceuticals and Functional Foods Incorporating CBD

The integration of cannabidiol into nutraceuticals and functional foods globally is positively impacting the growth of the cannabidiol market. Consumer interest in prevention rather than cure is driving demand for supplements that support sleep, stress management, immune health, and anti-inflammation using natural compounds. Manufacturers are now innovating with isolated CBD or broad-spectrum CBD in gummies, chewables, drink blends, and fortified snacks to meet these demands. Advances in delivery technologies, such as nanoemulsions or encapsulation,n improve bioavailability, which helps manufacturers create more effective products. Legal approvals in countries such as Canada, Australia, and several European nations for CBD in nutraceuticals are beginning to accumulate, which opens distribution channels in health food stores and mainstream retail.

MARKET CHALLENGES

Limited Clinical Evidence for Long-Term Safety and Efficacy

The lack of comprehensive clinical data supporting its long-term safety and efficacy across multiple therapeutic and wellness applications is limiting the growth of the global cannabidiol market. According to ClinicalTrials.gov, as of mid-2024, fewer than 250 registered clinical trials were investigating cannabidiol worldwide, which is relatively small compared to the number of products already available on the market. This imbalance has resulted in a gap between commercial enthusiasm and scientific validation. The absence of robust, reviewed evidence restricts medical practitioners from prescribing CBD with confidence, limits insurance coverage, and fuels regulatory hesitation.

Trade Barriers and International Supply Chain Instability

The trade restrictions and instability are additionally hindering the growth of the global cannabidiol market. Cannabidiol is derived largely from hemp, and according to the Food and Agriculture Organization, global hemp cultivation covered over 200,000 hectares in 2022. These disparities complicate international trade because hemp biomass or CBD extracts compliant in one country may be classified as illicit in another. Customs seizures and cross-border delays have become common, discouraging global suppliers from shipping to uncertain markets. Moreover, the global logistics sector continues to feel the effects of high freight rates and rising energy costs, which increase the cost of CBD product distribution.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Type, Distribution Channel, End-Users, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | |

| Market Leaders Profiled | Pharmahemp d.o.o, ENDOCA, NuLeaf Naturals LLC, Folium Biosciences, Elixinol, Cannoid LLC, Medical Marijuana Inc., and Isodiol International Inc. |

SEGMENTAL ANALYSIS

By Type Insights

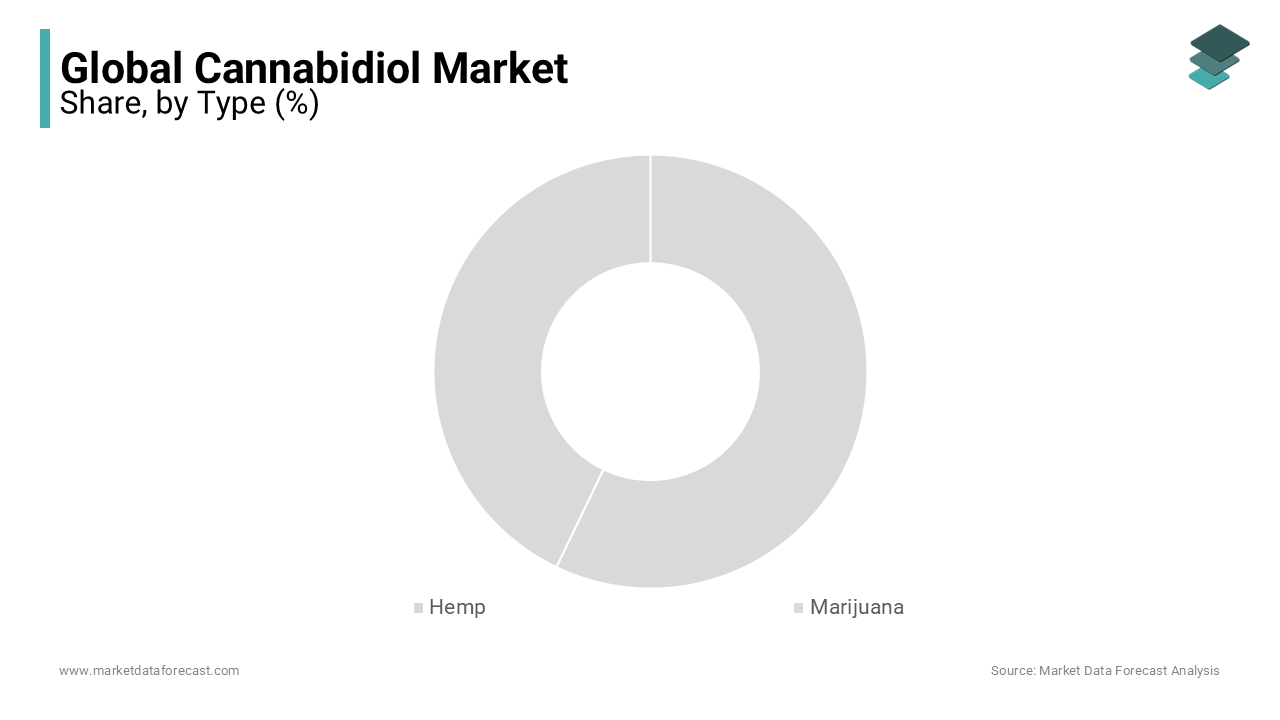

The hemp segment accounted in holding 56.8% of the global cannabidiol market share in 2024. Hemp has lower legal and regulatory barriers in many jurisdictions since it typically contains very low tetrahydrocannabinol (THC) levels. Many countries allow hemp cultivation, extraction, and sale of CBD derived from hemp under milder regulatory frameworks compared to marijuana derived CBD. The widespread use of hemp-derived isolates and broad-spectrum formulations in edible, topical, and supplement formats is supporting the segment. Also, hemp is more easily cultivated at scale in many regions, with established farming practices and supply chain logistics.

The marijuana derived CBD segment is likely to grow with an expected CAGR of 18.9% during the forecast period. Marijuana derived CBD often has higher CBD concentrations or comes as full-spectrum extracts including minor cannabinoids, which are in demand for medical and therapeutic purposes. Patients and medical researchers often prefer formulations with more potent effects or additional cannabinoids. Regulatory and clinical acceptance in some countries for such products, together with approvals of prescription CBD medicines derived from the marijuana source, are influencing this growth trajectory.

By Distribution Channel Insights

The B2B (business-to-business) segment was the largest by occupying 55.4% of the cannabidiol market share in 2024. One of the principal factors driving B2B’s dominance is the rising need among manufacturers of wellness, cosmetics, food, and pharmaceutical products to source large volumes of cannabidiol raw materials. These manufacturers purchase in bulk from CBD extractors or suppliers rather than producing in small consumer formats themselves. High volume purchases reduce cost per gram of CBD and allow manufacturers to scale product lines. Another driver contributing to B2B’s dominance is that bulk supply chains and institutional buyers are better positioned to absorb regulatory compliance, quality testing, safety certification, and supply chain inspections.

The B2C segment is projected to grow at a CAGR of 20.5% during 2025-2033. B2C growth is being driven by consumers becoming more aware of the potential health, wellness, and personal care benefits of cannabidiol. People are increasingly comfortable buying CBD oils, edibles, topicals, or cosmetics directly. Online reviews, social media, influencers, and wellness blogs are helping spread knowledge of CBD benefits.

By End-User Insights

The pharmaceuticals segment was the largest by occupying a prominent share of the cannabidiol market in 2024, with the increasing adoption in prescription therapies for serious conditions. Cannabidiol based medicines such as Epidyolex are approved in more countries, especially for rare seizure disorders. Regulatory approvals have expanded in the U.S., EU, UK, and some Asian nations. These approvals provide payers, physicians, and healthcare systems with confidence, which encourages large-scale purchases. Governments in Europe, North America, and parts of Latin America have updated rules allowing cannabinoid-based medicines to be prescribed and covered under national health systems.

The wellness segment is expected to grow with a significant CAGR during the forecast period. Wellness applications span nonprescription, preventative health, beauty, stress relief, sleep aids, and topical skincare. Producers are introducing novel wellness-oriented cannabidiol products with flavored options, cosmetic-grade purity, and broad-spectrum formulas.

REGIONAL ANALYSIS

North America Cannabidiol Market Analysis

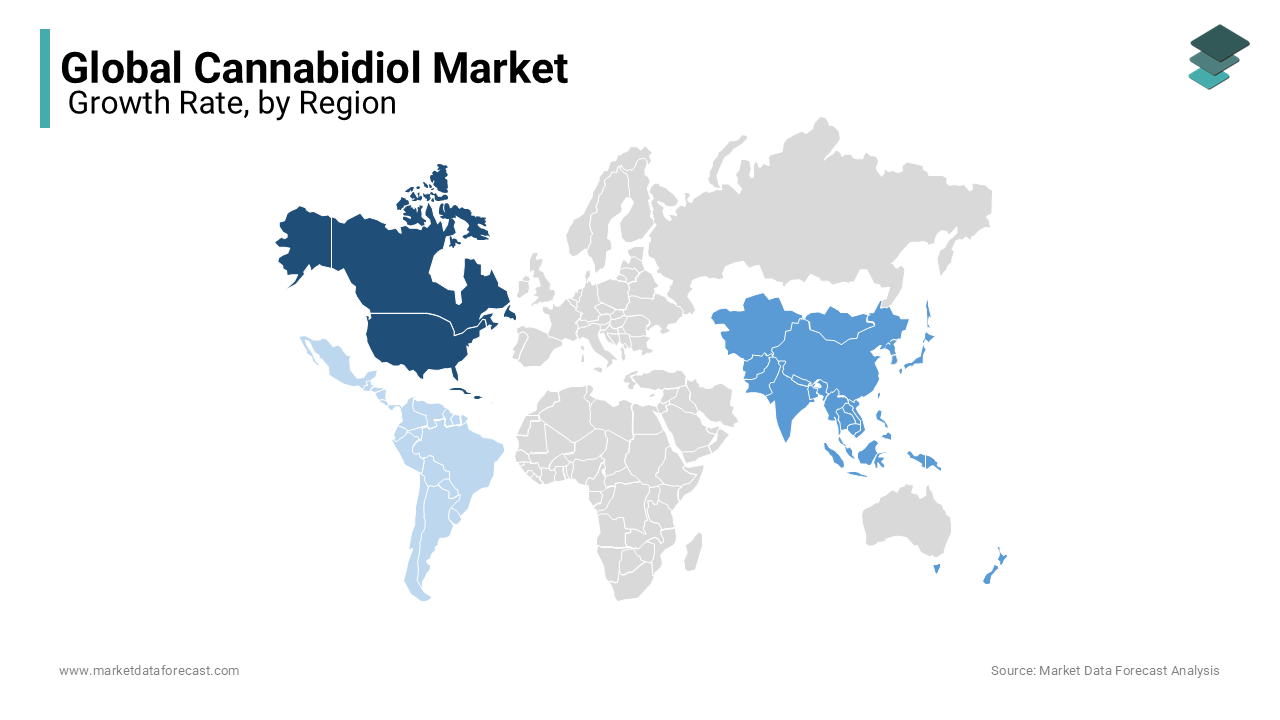

North America was the top performer of the global cannabidiol market by capturing 47.2% of the market share in 2024. The United States was the largest contributor in the North America cannabidiol market with early legal reforms that legalized industrial hemp and hemp-derived CBD under the 2018 Farm Bill. This regulatory clarity allowed widespread cultivation, processing, and sale of hemp-derived cannabidiol products. Also, strong consumer demand for wellness, pain relief, skin care, sleep aids, and anxiety support has driven growth. Regulatory frameworks in many U.S. states also allow both medical and recreational cannabis, which often include or permit cannabidiol-based products.

Europe Cannabidiol Market Analysis

Europe was positioned second by holding a prominent share of the cannabidiol market. Europe’s market status features increasing regulatory standardization around novel foods, cosmetics, and medical cannabis. Also, initiatives at the European Food Safety Authority to assess the safety of CBD as a novel food illustrate regulatory movement. Consumer demand in Europe is rising for wellness and personal care applications such as topical creams, serums, and dietary supplements. Medical cannabis adoption is increasing in countries such as Germany, the UK, Italy, and France under prescription or reimbursement settings.

Asia-Pacific Cannabidiol Market Analysis

Asia-Pacific is likely to have a significant CAGR during the forecast period. Countries like Australia, Japan, South Korea, Thailand, and others are reforming regulations to allow hemp-derived cannabidiol or medical cannabis products under strict controls. Increasing population awareness of natural wellness solutions, plus rising income levels, contribute to demand for CBD in cosmetics, sleep aids, pain relief, and stress management. Also, cross-border e-commerce and imports help bring in products where domestic supply is limited. Investments in clinical trials and research in the Asia-Pacific are on the rise to validate efficacy and safety.

Latin America Cannabidiol Market Analysis

Latin America market growth is likely to grow with prominent growth opportunities in the coming years. Rising incidence of chronic diseases and limited access to other therapies drive demand for alternative treatments, including CBD. Also, the tourism, wellness, and cosmetic industries are pushingthe incorporation of CBD in skincare and wellness spas. Trade barriers and regulatory inconsistencies still constrain full growth.

Middle East & Africa Cannabidiol Market Analysis

Middle East and Africa market is likely to grow steadily in the coming years. The status of MEA is that it is predominantly nascent, with legal restrictions generally tighter, especially regarding marijuana derived products and THC content. Certain countries are more permissive for medicinal cannabis under strict regulation. Wellness and cosmetic uses are emerging more slowly due to cultural regulatory constraints, limited product availability, and consumer awareness. However, there are signs of opportunity as governments explore medical cannabis legalisation, and demand for plant-based wellness products increases among youth and affluent consumers.

COMPETITIVE LANDSCAPE

The global cannabidiol market is highly competitive with a diverse set of players ranging from pharmaceutical giants to wellness startups. Companies are competing not only on pricing but also on quality assurance, regulatory compliance, product innovation, and consumer trust. Pharmaceutical firms such as Jazz Pharmaceuticals are building strong positions by advancing prescription-based cannabidiol medicines supported by rigorous clinical trials and regulatory approvals. Large cannabis firms, including Tilray Brands and Aurora Cannabis, are strengthening their presence through vertically integrated models that cover cultivation, processing, and distribution on a global scale. Consumer-oriented brands such as Endoca and Charlotte’s Web are differentiating through transparency, organic farming practices, and direct-to-consumer strategies across wellness and personal care categories. Market competition is also shaped by regional regulatory frameworks, which determine where companies can expand and which product formats they can legally sell.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global cannabidiol market include

- Pharmahemp d.o.o

- ENDOCA

- NuLeaf Naturals LLC

- Folium Biosciences

- Elixinol

- Cannoid LLC

- Medical Marijuana Inc.

- Isodiol International Inc.

Top Players in the Cannabidiol Market

- Jazz Pharmaceuticals is known for its cannabidiol based pharmaceutical product Epidiolex, approved for serious epilepsies. The company has recently advanced its regulatory and clinical strategy in the Asia Pacific by initiating a Phase III trial of its cannabidiol oral solution in Japan for treatment-resistant epilepsies. This demonstrates commitment to localised clinical evidence generation in APAC markets. Jazz also secured a patent in April 2024 for a cannabidiol preparation with over 90 percent CBD content designed to improve the effectiveness of combined CBD and THC therapies, which may aid future approved development in APAC jurisdictions.

- Tilray Brands has taken active steps to expand its operational footprint in the Asia Pacific by leveraging medical cannabis pathways and regulatory expertise. The company has launched pastilles in Australia under the Special Access Scheme, offering doctors options with balanced THC and CBD formulations. This indicates Tilray’s strategy of introducing products compliant with local medicinal access frameworks. It is emphasising regulatory know-how and improving gross margin performance by integrating supply chain efficiencies, quality certification, and diversifying its product offerings to meet wellness and medical demand in APAC. These actions show that Tilray is investing both in product innovation and in adapting to varying regulatory environments in the Asia Pacific.

- Endoca has long emphasised organic farming, full transparency, third-party lab testing, and seed-to-shelf production of hemp-derived CBD products. In the Asia Pacific region, Endoca expanded its portfolio of hemp-derived supplements in 2022, launching oils, capsules, and tinctures adapted to local consumer preferences and regulatory compliance standards. The company has also focused on retail distribution and e-commerce channels in countries like Australia, where wellness and natural product demand is strong. Endoca’s repeated investment in clean labels and compliance positions the firm to build trust among APAC consumers concerned about the quality, authenticity, and safety of cannabidiol products.

Top Strategies Used by the Key Market Participants

Key participants in the global cannabidiol market adopt multiple strategic approaches to maintain a competitive edge. One major strategy is investing in rigorous scientific research and clinical trials to substantiate therapeutic claims and secure regulatory approvals. Firms are engaging in double blind, controlled studies and collaborating with universities to demonstrate efficacy and safety for conditions such as epilepsy, pain, and anxiety. Another strategy revolves around focusing on quality assurance, supply chain transparency, and product standardisation. Companies emphasise seed-to-shelf traceability, good manufacturing practice,s third-party lab testing, and strict control of cannabinoid profiles. They also expand into international markets where regulation is becoming more permissive by setting up local compliance manufacturing and navigating import export rules. Product innovation is a further strategy whereby companies develop novel delivery systems such as nanotechnology-enhanced oils, topical creams, gummies, or time-release formats to improve bioavailability and consumer experience. Branding and consumer education also feature heavily as strategies.

GLOBAL CANNABIDIOL MARKET NEWS

- In September 2024, it was reported that a groundbreaking study examining the impact of cannabidiol (CBD) psychosis is planned to be introduced in late 2024. It is spearheaded by Oxford University and managed by the Prince of Wales International Centre for SANE Research. This will include one thousand patients and be conducted in 35 centers throughout North America and Europe.

- In August 2024, Vectura Fertin Pharma, Inc. and Aurora Cannabis Inc. reported that they have signed a commercial partnership with Cogent International Manufacturing Ltd., which is a fully owned subsidiary of Vectura Fertin Pharma.

MARKET SEGMENTATION

This research report on the global cannabidiol market has been segmented and sub-segmented based on the type, distribution channel, end-users, and region.

By Type

- Hemp

- Marijuana

By Distribution Channel

- B2B

- B2C

- Hospital Pharmacies

- Online

- Retail Stores

By End Users

- Medical

- Chronic Pain

- Mental Disorders

- Cancer

- Others

- Personal Use

- Pharmaceuticals

- Wellness

- Food & Beverages

- Personal Care & Cosmetics

- Nutraceuticals

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the Cannabidiol Market?

The Cannabidiol Market involves the production, distribution, and sale of CBD products derived primarily from hemp, including oils, edibles, topicals, and pharmaceuticals, used for various health and wellness applications

2. Which regions dominate the Cannabidiol Market?

North America leads with over 40% to 86% market share in 2024–2025, while Europe is expected to exhibit the fastest growth, and Asia Pacific is emerging as a promising market

3. What are the primary sources of cannabidiol in the market?

Hemp accounts for about 56% to 58% of CBD sourcing globally, dominating the market due to its legal status and high CBD content

4. What are the major product types in the Cannabidiol Market?

CBD oils dominate, followed by edibles, topicals, pet products, and pharmaceuticals targeting pain relief, anxiety, and other medical conditions

5. What factors are driving growth in the Cannabidiol Market?

Expanding legalization, rising health awareness, increased R&D investment, wider product acceptance, and growing e-commerce sales are key growth drivers

6. How is legalization affecting the Cannabidiol Market expansion?

Nearly 50 countries have legalized medical or recreational cannabis as of 2025, boosting consumer access and encouraging new market entrants worldwide

7. Who are the leading companies in the Cannabidiol Market?

Key players include Canopy Growth Corporation, Elixinol, NuLeaf Naturals, Cannoid LLC, The Cronos Group, and Medical Marijuana, Inc., among others

8. How are CBD pet products influencing the Cannabidiol Market?

The CBD pet segment is rapidly growing due to increasing adoption for pet wellness, with projected explosive revenue increases through 2035

9. What challenges does the Cannabidiol Market face?

Quality control issues, regulatory complexity, testing inconsistencies, and market fragmentation remain challenges

10. How does e-commerce impact the Cannabidiol Market?

Online sales have expanded product reach, improved consumer education, and contributed significantly to rapid market growth globally

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com