- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

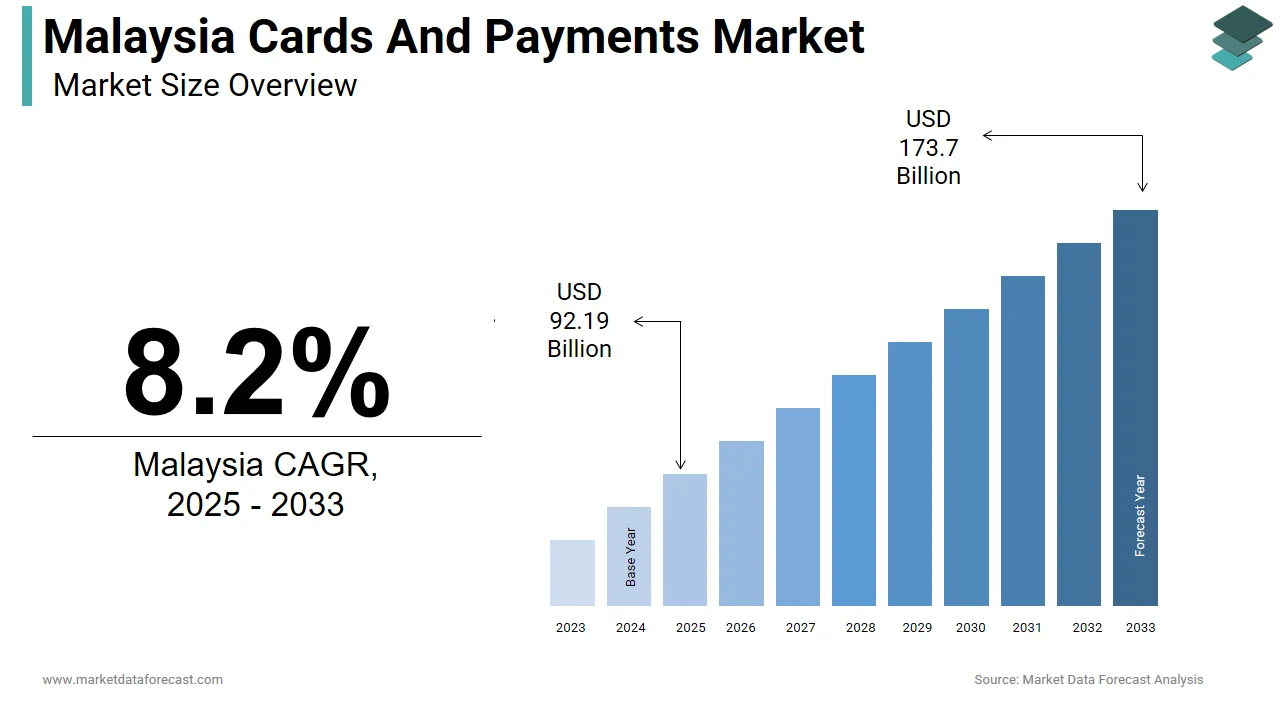

Malaysia Cards and Payments Market Size

The Malaysia cards and payments market size was valued at USD 85.2 billion in 2024. This market is expected to grow at a CAGR of 8.2% from 2025 to 2033 and be worth USD 173.17 billion by 2033 from USD 92.19 billion in 2025.

MARKET DRIVERS

Surge in Digital Payment Adoption Driven by E-Commerce Growth

One of the primary drivers of Malaysia’s cards and payments market is the rapid growth of e-commerce, which has significantly accelerated digital payment adoption across the country. This surge has fueled demand for secure and convenient card-based and mobile wallet transactions. The Central Bank of Malaysia (Bank Negara Malaysia) reported that electronic money (e-money) transaction value grew by 28% year-on-year, reaching RM 196 billion (approximately US$44 billion). Also, credit and debit card usage increased during the same period, driven by online platforms such as Shopee, Lazada, and Zalora. With smartphone penetration high among internet users and mobile banking adoption on the rise, consumers are increasingly shifting away from cash-based transactions, reinforcing sustained growth in the cards and payments sector.

Government Initiatives to Promote Cashless Transactions and Financial Inclusion

Another key driver of Malaysia’s cards and payments market is the government’s proactive push to promote financial inclusion and reduce reliance on cash through national digital payment initiatives. Under Bank Negara Malaysia’s Financial Inclusion Strategic Framework, access to formal financial services expanded significantly, with financial inclusion reaching 88% in 2023, up from 68% in 2015, according to the World Bank’s Global Findex Database. To support this transition, the Malaysian government launched the National Digital Payment Framework (NDPF) in 2018, followed by the introduction of DuitNow, a real-time interbank fund transfer system that supports QR code payments, mobile apps, and linked identification numbers. By December 2023, DuitNow had processed over RM 380 billion in transactions, with more than 12 million QR codes registered nationwide, according to Bank Negara Malaysia. These efforts have not only boosted consumer confidence in digital payments but also encouraged banks and fintech firms to innovate and expand their offerings across urban and rural areas.

MARKET RESTRAINTS

Persistent Cash Preference in Rural and Informal Economies

Despite growing digital adoption in cities, a significant restraint on Malaysia’s cards and payments market is the continued dominance of cash in rural areas and informal sectors. According to the Department of Statistics Malaysia (DOSM), approximately 14% of adults remained unbanked as of 2023, many of whom operate within micro-economies such as small-scale trading, agriculture, and street vending. Bank Negara Malaysia noted that cash-in-circulation still accounted for around 40% of total retail transactions by volume in 2023. This behavioral inertia slows the transition to a fully integrated digital payments ecosystem and requires targeted education campaigns and infrastructure development to overcome.

Limited Merchant Acquiring Infrastructure outside Urban Centers

Another key constraint in Malaysia’s cards and payments market is the uneven distribution of merchant acquiring infrastructure, especially outside major cities like Kuala Lumpur, Penang, and Johor Bahru. As of 2023, the Malaysian POS terminal business had a relatively low installed base compared to other regions. In contrast, Thailand and Singapore each have more POS devices per capita despite smaller populations. This infrastructure gap limits the ability of digital payment providers to scale and hampers broader financial inclusion goals.

MARKET OPPORTUNITIES

Expansion of Buy Now, Pay Later (BNPL) Services Across Retail and E-Commerce

A growing opportunity in Malaysia’s cards and payments market is the expansion of Buy Now, Pay Later (BNPL) services, which are gaining traction among young, digitally savvy consumers and e-commerce platforms. Local players such as Atome, Hoolah, and PayLater by Touch'n Go have seen rapid user growth, with Atome reporting over 3 million registered users by mid-2023. The Credit Counselling and Debt Management Agency (AKPK) observed that BNPL adoption is particularly strong among millennials and Gen Z, who account for a major share of all BNPL users. As consumer credit demand expands and regulatory clarity improves, BNPL services offer a viable alternative to traditional credit cards, enabling greater financial access and stimulating higher spending in both online and offline retail environments.

Rise of Super App Ecosystems Integrating Financial and Payment Services

The proliferation of super apps in Malaysia presents a transformative opportunity for the cards and payments industry, as these platforms integrate multiple financial services—including digital wallets, lending, insurance, and investment—into a single interface. Touch'n Go e-Wallet, GrabPay, and Boost are leading this trend, offering comprehensive financial ecosystems that serve tens of millions of users daily. These super apps are not only enhancing financial inclusion but also driving card-linked payments, QR code transactions, and peer-to-peer transfers. With their deep integration into everyday life—from ride-hailing to food delivery—super apps are reshaping consumer behavior and accelerating the shift toward a cashless society in Malaysia.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Expanding Digital Payment Systems

As Malaysia’s digital payment landscape expands rapidly, cybersecurity vulnerabilities pose a growing challenge to the stability and trustworthiness of the cards and payments market. The increasing number of digital transactions has attracted cybercriminals, leading to a rise in fraud incidents and data breaches. According to the Malaysian Computer Emergency Response Team (MyCERT), the number of reported cyberattacks targeting financial institutions surged by 42% in 2023 compared to the previous year. Smaller fintech firms and regional banks often lack the resources to invest in advanced threat detection and encryption technologies, making them particularly vulnerable. Strengthening digital infrastructure, enforcing stricter compliance standards, and improving consumer awareness are essential to mitigating these risks and ensuring sustainable growth in Malaysia’s evolving payments ecosystem.

Regulatory Complexity and Compliance Burden for Emerging Fintech Innovations

Regulatory complexity remains a major challenge for Malaysia’s cards and payments market, particularly for fintech startups aiming to introduce innovative payment solutions. While Bank Negara Malaysia has implemented progressive policies to support digital finance, the approval process for new products and services can be lengthy and cumbersome. Furthermore, the requirement for local data storage and restrictions on cross-border fund flows complicate international expansion plans for many companies. Streamlining oversight while maintaining consumer protection and financial stability is crucial to fostering innovation and attracting further investment in Malaysia’s fast-growing digital payments sector.

MARKET KEY HIGHLIGHTS

The sevenfold increase in the use of contactless cards in the country owing to the distribution of such cards from all major banks like Maybank, Bank Simpanan Nasional (BSN), CIMB Bank, Public Bank, and Hong Leong Bank is forcing financial institutions to develop innovative products like NFC Wristband, Maybank Visa Payband providing payment convenience at a wave of the wrist.

The launch of alternative payments like mobile wallets by Samsung Electronics, CIMB Bank, and Maybank was due to the growing preference for secure electronic payments, growth in the young population, and deeper smartphone penetration between 2016-2017.

The government implemented DFTZ as part of the National E-commerce Strategic Roadmap in partnership of Alibaba and Malaysia Digital Economy Corporation to support digital services, worldwide online business, and push the e-commerce market.

KEY MARKET PLAYERS

Top players in the Malaysia cards and payments market include

- Malayan Banking Berhad

- National Savings Bank

- Public Bank

- CIMB Bank

- Islamic Bank

- Citibank

- Hong Leong Bank

- HSBC

- AmBank

MARKET SEGMENTATION

This research report on the Malaysia cards and payments market has been segmented and sub-segmented based on the following categories.

By Cards

- Debit Cards

- Credit Cards

- Prepaid Cards

By Payment Terminals

- POS

- ATM's

By Payment Instruments

- Credit Transfers

- Direct Debit

- Cheques

- Payment Cards