- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

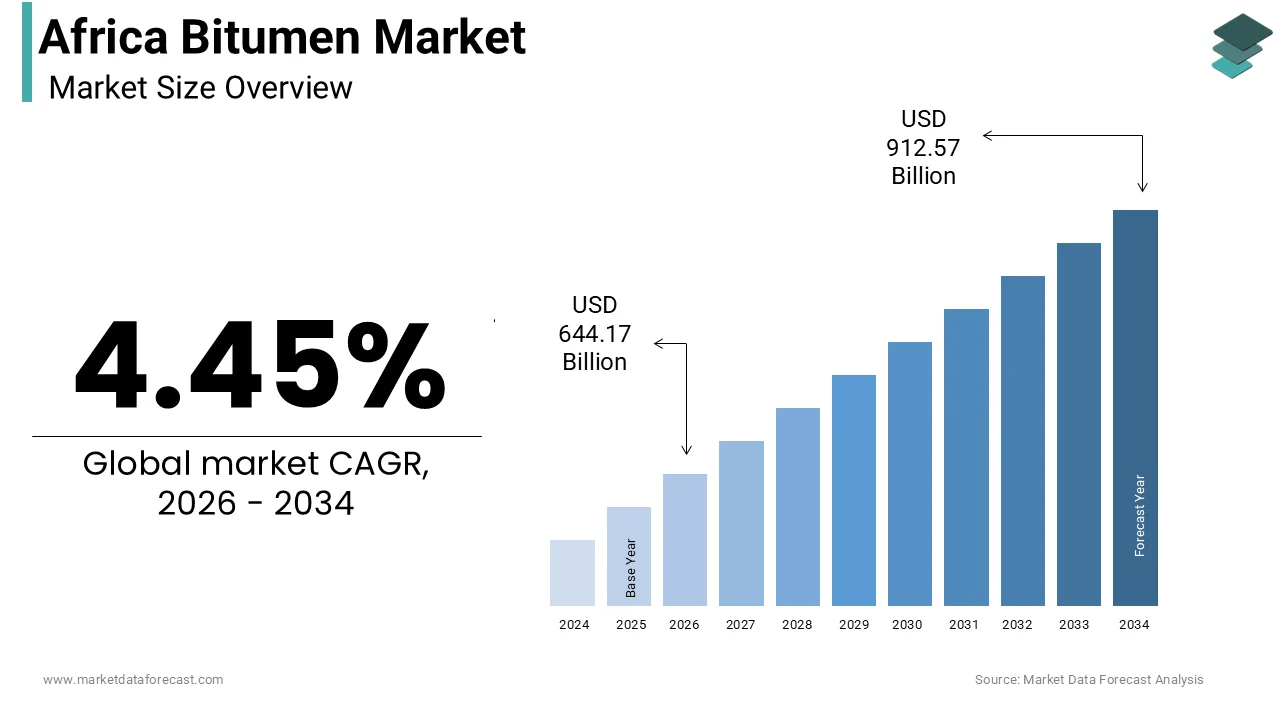

Market Size, 2025

$616.73 MnMarket Estimate, 2026

$644.17 MnMarket Forecast, 2034

$912.57 MnCAGR, 2026–2034

4.45%Executive Summary: Africa Bitumen Market

- Market Scope: Comprehensive Africa bitumen market analysis covering road infrastructure development, paving grade materials, polymer-modified bitumen, AI-enabled construction monitoring, and AfCFTA regional integration trends.

- Market Valuation: Valued at USD 616.73 million (2025), estimated at USD 644.17 million (2026), and projected to reach USD 912.57 million by 2034, registering a steady CAGR of 4.45% (2026–2034).

- Primary Growth Drivers: Accelerating road infrastructure projects, rapid urbanization requiring durable transport networks, government public works investments, polymer-modified bitumen adoption, and AfCFTA cross-border connectivity. Key challenges include supply chain disruptions and crude oil price volatility.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (Position) | Fastest-Growing Segment |

|---|---|---|

| By Segment & Application | Paving grade bitumen segment (dominated with the largest share in 2025 for road construction and asphalt applications) | Services segment (predicted significant growth) & Pharmaceutical & biotechnology end-user segment (anticipated CAGR of 33.7%) |

| By Region / Country | African continental infrastructure corridors supported by AfCFTA trade agreements and sovereign wealth initiatives | Emerging African transport networks and urban centers expanding via public works investments |

Major Market Players & Market Structure

Market Structure: Competitive regional infrastructure and construction material landscape featuring technology and industrial solution providers driving AI-enabled monitoring, surveillance, and transport connectivity enhancements.

Key Companies: Welltok Inc., Intel Corporation, Nvidia Corporation, Google Inc., IBM Corporation, Microsoft Corporation, General Vision Inc., Enlitic Inc., Next IT Corporation, iCarbonX, Siemens Healthineers, General Electric (GE) Company, Koninklijke Philips N.V., Cloudmedx Inc., Bay Labs Inc., Bosch, and Drone Shield Ltd.

Africa Bitumen Market Size

The Africa Bitumen Market Size was calculated to be USD 616.73 million in 2025 and is anticipated to be worth USD 912.57 million by 2034, from USD 644.17 million in 2026, growing at a CAGR of 4.45% during the forecast period.

Bitumen is a highly viscous petroleum-derived binding material essential for road construction, waterproofing, and industrial applications. As African countries continue to invest in infrastructure development, bitumen has become a critical component in building durable road networks that support economic growth and regional connectivity.

Africa’s increasing focus on expanding transportation infrastructure has significantly driven demand for bitumen across key economies such as Nigeria, South Africa, Kenya, Ethiopia, and Egypt. According to the African Development Bank, only about 34% of the continent's rural roads are paved, highlighting the vast potential for future road construction projects that require substantial volumes of bitumen.

Moreover, rapid urbanization is intensifying pressure on governments to improve mobility and reduce transport bottlenecks. As per the United Nations Department of Economic and Social Affairs, Africa’s urban population is expected to reach 1.3 billion by 2050. This surge necessitates extensive road network upgrades, directly boosting bitumen consumption.

Apart from these, several African nations are adopting advanced pavement technologies, including polymer-modified bitumen, to enhance road longevity and performance under extreme weather conditions. Countries like Morocco and South Africa have already begun integrating these high-performance solutions into major highway projects.

So, the need for reliable and efficient transport systems will continue to fuel demand for bitumen across the continent because of the growing foreign direct investment in infrastructure and regional integration initiatives such as the African Continental Free Trade Area (AfCFTA).

MARKET DRIVERS

Expansion of Road Infrastructure Projects

The increasing investment in road infrastructure development across the continent is one of the primary drivers of the africa bitumen market. Governments and international funding agencies are prioritizing road construction to enhance regional trade, improve access to remote communities, and support economic integration.

According to the World Bank, Africa requires an estimated $48 billion annually until 2030 to meet its infrastructure needs, with road transport accounting for the largest share of investments. In 2023 alone, over $12 billion was allocated to road construction and rehabilitation projects across Sub-Saharan Africa, many of which involved significant use of bitumen-based asphalt pavements.

A key example is the Trans-African Highway network, which aims to connect major economic hubs through an integrated road system. As per the African Development Bank, in 2023, over 20,000 km of new or upgraded roads were under construction across East and West Africa, all requiring bitumen for surfacing and paving.

Besides, national governments are accelerating efforts to improve rural connectivity. According to Ethiopia’s Ministry of Transport, in 2023, the country expanded its road network by over 5,000 km, with bitumen playing a central role in surfaced road construction.

These developments show the continued reliance on bitumen.

Growth in Urbanization and Real Estate Development

The rapid pace of urbanization and real estate development, particularly in major metropolitan centers, another key driver of the Africa bitumen market. As cities expand, the demand for internal road networks, parking lots, and residential driveways increases, directly influencing bitumen consumption.

According to the United Nations Human Settlements Programme (UN-Habitat), Africa is the world’s fastest-urbanizing continent, with nearly 40% of its population now residing in urban areas. By 2050, this figure is projected to exceed 60%, necessitating large-scale infrastructure development within city limits.

In response, municipal authorities are investing heavily in urban road construction and maintenance. For instance, Lagos has ongoing road construction projects and initiatives to improve mobility.

Similarly, Nairobi’s County Government launched a $150 million road rehabilitation program in the same year, focusing on resurfacing major thoroughfares using modified bitumen to enhance durability against heavy traffic and tropical weather conditions.

Beyond capital cities, secondary towns and peri-urban settlements are also witnessing increased road paving activity.

This trend show how urban expansion is only driving demand for bitumen but also strengthening its role in supporting economic growth through improved transport accessibility.

MARKET RESTRAINTS

High Import Dependency and Supply Chain Disruptions

The continent’s heavy reliance on imported bitumen due to limited domestic refining capacity is a significant restraint affecting the africa bitumen market. Most African countries lack sufficient oil refineries capable of producing bitumen as a by-product of crude oil processing, forcing them to depend on imports from Europe, the Middle East, and Asia.

For example, in 2023, the Red Sea shipping crisis disrupted maritime routes, causing delivery delays of up to six weeks for bitumen shipments bound for East Africa.

Furthermore, weak inland logistics infrastructure such as inadequate storage facilities and poor road connectivity complicates last-mile distribution, especially in landlocked countries like Chad, Burkina Faso, and South Sudan.

As per the estimations by Nigerian Upstream Petroleum Regulatory Authority (NUPRC), in 2023, Nigeria spent over $400 million on bitumen imports, despite being a major crude oil exporter. This dependency not only strains foreign exchange reserves but also makes pricing unpredictable for contractors and government agencies.

Price Volatility Linked to Crude Oil Markets

Price volatility remains a major challenge for the Africa bitumen market, as bitumen prices are closely tied to global crude oil markets. Since bitumen is a residual product of crude oil refining, fluctuations in oil prices directly impact the affordability and procurement planning of bitumen-dependent infrastructure projects.

According to the U.S. Energy Information Administration (EIA), global crude oil prices experienced sharp swings in 2023, peaking at over $90 per barrel before dropping below $75. These fluctuations translated into erratic bitumen pricing, making budgeting difficult for public works departments and private developers alike.

In countries like Ghana and Zambia, where road budgets are fixed and often constrained, sudden increases in bitumen costs have led to project delays. As per its 2023 annual report of the Ghanaian Ministry of Roads and Highways, the rising bitumen prices forced the postponement of several regional road upgrades, impacting rural connectivity and economic development.

Apart from these, speculative trading in international commodity markets exacerbates unpredictability.

MARKET OPPORTUNITIES

Regional Refinery Expansion and Local Bitumen Production Initiatives

The ongoing expansion of regional refineries and the establishment of local bitumen production facilities aimed at reducing import dependence and stabilizing supply chains provides a promising opportunity in the africa bitumen market.

Several African governments are investing in refinery upgrades to produce bitumen domestically rather than importing finished products. Nigeria, for instance, has been working on revamping its Port Harcourt and Warri refineries to increase bitumen output. According to the Nigerian National Petroleum Corporation (NNPC), the overhaul could boost domestic bitumen production by up to 30% by 2026, significantly reducing reliance on imports.

Similarly, South Africa’s state-owned PetroSA has partnered with private investors to establish a dedicated bitumen terminal near Durban, enhancing storage and distribution efficiency for regional road projects. As per the South African Department of Public Works and Infrastructure, this initiative is expected to streamline procurement and lower input costs for contractors.

In East Africa, Kenya’s Mombasa Refinery has initiated feasibility studies for bitumen production expansion, supported by the Kenyan Ministry of Energy. If implemented, this move would enhance regional self-sufficiency and stabilize pricing for road construction firms.

Therefore, these developments present a strong opportunity for African nations to strengthen their bitumen supply chains and support long-term infrastructure development is due the increasing emphasis on local content and import substitution policies.

Adoption of Modified Bitumen for Enhanced Road Performance

The adoption of modified bitumen represents a significant growth opportunity for the Africa bitumen market, offering enhanced durability, temperature resistance, and longer service life for road surfaces which is an essential factor given the continent’s diverse climatic conditions.

Modified bitumen, which includes polymer-modified bitumen (PMB) and rubberized bitumen, provides superior flexibility and crack resistance, making it ideal for tropical and arid regions where extreme temperatures can degrade conventional asphalt layers. As per the International Road Federation (IRF), roads constructed with modified bitumen can last up to 20 years compared to 8–10 years for standard bituminous surfaces.

Kenya has been at the forefront of this shift. Also, South Africa’s Road Traffic Management Corporation has incorporated modified bitumen specifications in national road design standards to accommodate heavy freight movement and high-temperature environments.

Private sector players are also responding to this trend.

The awareness is growing regarding the long-term economic and environmental benefits of modified bitumen, so its adoption is expected to rise across the continent, opening new avenues for market expansion.

MARKET CHALLENGES

Environmental and Health Concerns Related to Bitumen Use

The increasing scrutiny around environmental and health impacts associated with bitumen production and application is a pressing challenge for the africa bitumen market. While bitumen itself is non-toxic, emissions during heating and laying processes can release volatile organic compounds (VOCs) and fine particulate matter, raising concerns among regulators and communities.

According to the World Health Organization (WHO), exposure to fumes from hot-mix asphalt operations can cause respiratory irritation and skin sensitization, particularly in informal or poorly regulated work environments. In several African countries, safety protocols for bitumen handling remain under-enforced, leading to occupational health risks for workers.

Besides, environmental groups and urban planners are advocating for alternative road-building materials that offer lower carbon footprints. The United Nations Environment Programme (UNEP) has pointed out the need for cleaner road construction practices, prompting discussions around warm mix asphalt and cold recycling technologies that use less energy and emit fewer pollutants.

So, modified bitumen and bio-bitumen alternatives are gaining traction globally but their adoption in Africa remains limited due to higher costs and technical barriers.

Fragmented Regulatory Standards Across African Countries

Fragmented regulatory frameworks across African countries present a major challenge for the bitumen market, complicating procurement, quality assurance, and cross-border trade. Each nation maintains different specifications for bitumen grading, testing procedures, and application methods, creating inconsistencies that affect both suppliers and end-users.

According to the United Nations Economic Commission for Africa (UNECA), there are several distinct bitumen quality standards currently in use across the continent. This diversity leads to inefficiencies in sourcing, compliance, and contract bidding, particularly for multinational contractors operating in multiple African markets.

For instance, while South Africa follows the South African Bureau of Standards (SABS) classification, Nigeria adheres to the Federal Road Safety Corps (FRSC) guidelines, and Kenya implements specifications based on British and ASTM standards. This inconsistency hampers market harmonization and discourages investment in standardized production facilities.

Furthermore, customs procedures vary widely between countries, delaying shipments and increasing costs. The World Bank Logistics Performance Index (LPI) 2023 highlights that border clearance times for bitumen shipments can range from two days in North Africa to over two weeks in Central Africa, disrupting supply chains.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.45% |

| Segments Covered | By Product, Type, Application and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Sudan, Egypt, Kenya, Ethiopia, South Africa, and Rest of Africa |

| Market Leaders Profiled | Shell, TotalEnergies, ExxonMobil, Sasol Limited, Indian Oil Corporation, Nynas AB, Colas Group, Engen Petroleum Ltd, Puma Energy, TIPCO Asphalt |

SEGMENTAL ANALYSIS

By Product Type Insights

The paving grade bitumen segment was the largest segment in the Africa bitumen market by accounting for a 56.8% of total consumption in 2025. Its widespread use in road construction and asphalt pavement applications across both urban and rural areas is majorly propelling the dominance of the growth of paving grade bitumen segment. Further, the ongoing expansion of road infrastructure projects across African nations also contributes to the growth of paving grade bitumen segment. According to the African Development Bank, substantial funds was allocated to road development initiatives in Sub-Saharan Africa in 2023, with paving grade bitumen forming the core binding agent in asphalt mixtures used for surfacing and resurfacing.

Apart from these, national governments are prioritizing road connectivity to support economic growth and regional trade. As per the Ethiopia’s Ministry of Transport, in 2023, the country completed over 5,000 km of new paved roads, most of which utilized standard penetration-grade bitumen suitable for tropical climates.

Moreover, paving grade bitumen remains cost-effective compared to modified alternatives, making it the preferred choice for budget-constrained public works departments.

Hence, the continued investment in transport infrastructure and limited domestic availability of polymer-modified or cold-mix alternatives is paving grade bitumen will remain central to the continent’s road-building efforts.

The polymer modified bitumen (PMB) segment is projected to grow at the fastest CAGR of 9.4% between 2026 and 2034. The increasing demand for high-performance road surfaces that can withstand extreme weather conditions, heavy traffic loads, and temperature fluctuations is rapidly expanding the polymer modified bitumen (PMB) segment.

The rising adoption of PMB in national highway upgrades is also a major factor contributing to the growth of polymer modified bitumen (PMB) segment. In addition, South Africa has been a pioneer in PMB usage, particularly in high-traffic corridors such as Gauteng and KwaZulu-Natal.

Furthermore, foreign investors and multinational contractors operating in Africa are increasingly specifying PMB in infrastructure tenders to meet international quality benchmarks. As per the International Road Federation (IRF), PMB-based roads have an extended service life of up to 20 years, compared to 8–10 years for conventional bituminous pavements.

By Application Insights

The road construction segment dominated the Africa bitumen market with a substantial share in 2025. The massive scale of road development initiatives undertaken by African governments and multilateral agencies is the reason behind the growth of road construction segment. It is reflecting the continent's extensive need for durable transport infrastructure to support economic development and regional integration. According to the United Nations Economic Commission for Africa (UNECA), only about one-third of Africa’s rural roads are paved, prompting urgent investments in road network expansion and rehabilitation. Urbanization trends are also driving demand. The United Nations Department of Economic and Social Affairs forecasts that Africa’s urban population will reach 1.3 billion by 2050, necessitating large-scale intra-city road expansions and internal street developments that depend heavily on bitumen.

The waterproofing application segment is anticipated to grow at the highest CAGR of around 7.8% during the forecast period. The surge in commercial and residential real estate development, particularly in coastal and flood-prone regions is one significant growth driver of the waterproofing application segment. This segment includes the use of bitumen in roofing membranes, foundation coatings, and underground infrastructure protection—areas gaining attention as urban construction expands and climate-related flooding becomes more frequent. Besides, infrastructure modernization programs are fuelling demand.

Industrial facilities such as warehouses, ports, and logistics hubs are also adopting advanced bitumen-based membranes to protect concrete structures from moisture damage. The rising awareness about building durability and climate adaptation has positioned the waterproofing application segment for sustained growth which is offering new revenue streams for bitumen suppliers beyond traditional road markets.

REGIONAL ANALYSIS

Nigeria Bitumen Market Insights

Nigeria led the Africa bitumen market with an estimated 24.4% share in 2025 and is driven by its aggressive road infrastructure development agenda and growing urbanization rates. As Africa’s most populous nation, Nigeria faces significant challenges in road connectivity, prompting government-led interventions to expand and rehabilitate highways and secondary roads.

The Lagos-Ibadan Expressway and Second Niger Bridge projects were among the flagship undertakings requiring large volumes of paving grade bitumen sourced mainly through imports due to limited domestic refining capacity.

Apart from these, as per the estimations by the Nigerian Upstream Petroleum Regulatory Authority (NUPRC), the country spent over $400 million on bitumen imports in 2023, highlighting the extent of dependency on external suppliers despite being a major crude oil producer.

However, recent government initiatives to revamp the Port Harcourt and Kaduna refineries offer potential for local bitumen production, which could reduce import reliance in the coming years.

South Africa Bitumen Market Insights

South Africa is a major regional bitumen market. It is supported by its well-established road network, structured procurement processes, and early adoption of advanced bitumen technologies.

The country’s road infrastructure spans over 750,000 km, with bitumen playing a critical role in maintaining and expanding surfaced roads. South Africa also leads in the adoption of polymer-modified bitumen (PMB), which enhances road durability in high-temperature zones and high-traffic corridors. Moreover, the country benefits from PetroSA’s Sapref refinery near Durban, one of the few fully operational bitumen production units in Africa.

Despite economic headwinds, including load-shedding and inflationary pressures, South Africa remains a key hub for bitumen innovation, blending, and regional exports, positioning itself as a leader in both volume and technical advancement.

Kenya Bitumen Market Insights

Kenya commands a significant share of the Africa bitumen market and is emerging as a key player due to its strategic location, robust infrastructure development plans, and strong regional influence in East Africa.

As per the Kenya National Bureau of Statistics, GDP growth reached 4.8% in 2023, with the transport sector contributing significantly to economic output.

Mombasa, Kenya’s main port city, serves as a regional distribution center for imported bitumen destined for Uganda, Rwanda, Burundi, and South Sudan. Besides, Kenya is embracing advanced bitumen applications. This shift toward premium-grade products reflects broader trends in quality-driven infrastructure planning.

So, Kenya is poised to maintain its position as a leading consumer of bitumen in East Africa.

Egypt Bitumen Market Insights

Egypt in the Africa bitumen market is benefiting from its strategic geographic position, stable political environment, and government-backed infrastructure modernization programs.

As per Egypt’s Ministry of Transport, the country invested over EGP 150 billion ($7.7 billion) in road and transport infrastructure in 2023, focusing on expanding desert highways, urban expressways, and industrial park access roads. These initiatives require substantial quantities of bitumen for surfacing and asphalt laying.

The New Administrative Capital project, set to become Egypt’s future seat of government, incorporates extensive road networks and smart city planning, all of which rely on bitumen-based asphalt solutions. As per the Egyptian Environmental Affairs Agency (EEAA), over 3,000 km of new roads were constructed in 2023, with bitumen consumption exceeding 1.8 million tons.

Egypt also serves as a regional export hub, with Cairo-based refineries supplying bitumen to Libya, Sudan, and parts of North Africa. The General Authority for Roads, Bridges & Urban Development emphasizes quality standards aligned with European norms, ensuring compatibility with international supply chains.

Rest of Africa Bitumen Market Insights

The remaining African countries collectively account for a descent share of the regional bitumen market, with notable contributions from Ghana, Tanzania, Morocco, Algeria, and Angola. Each of these nations presents unique growth dynamics based on infrastructure spending, regulatory frameworks, and regional trade linkages.

Morocco benefits from a mature road construction industry, with according to the Moroccan Ministry of Equipment and Transport in 2023, over 1,500 km of new roads were constructed using bitumen-based asphalt, supported by local production and imports via Mediterranean ports.

Tanzania has seen a surge in bitumen demand due to its participation in regional corridor projects, including the Northern Corridor Integration Projects linking Kenya, Uganda, and Rwanda. Algeria, rich in hydrocarbon resources, produces bitumen domestically and uses it extensively in desert road construction and urban renewal projects. Meanwhile, Ghana’s Ministry of Roads and Highways launched a major road rehabilitation initiative in 2023, integrating bitumen into rural and arterial road upgrades.

LEADING PLAYERS IN THE AFRICA BITUMEN MARKET

TotalEnergies SE

TotalEnergies is a major player in the Africa bitumen market, offering high-quality paving and modified bitumen solutions tailored to the continent’s diverse climatic and road conditions. The company has a strong presence across West and East Africa through its refining and distribution networks.

Through subsidiaries and partnerships, TotalEnergies ensures consistent supply to government infrastructure projects and private contractors. Its focus on sustainable bitumen solutions, including warm mix and polymer-modified variants, aligns with evolving regional road construction standards.

By leveraging its global expertise and local logistics capabilities, TotalEnergies plays a crucial role in shaping the quality and performance expectations of bitumen applications across Africa.

Shell plc

Shell has a significant footprint in the Africa bitumen market, supplying bitumen products for road construction, industrial use, and specialty applications. Known for its technical expertise and product reliability, the company operates through a network of distributors and licensed blenders across key African markets.

In addition to conventional bitumen offerings, Shell supports innovation in asphalt technology by promoting modified and environmentally friendly formulations that enhance road longevity and reduce emissions.

The company also engages in capacity-building initiatives, working closely with road agencies and contractors to improve application techniques and maintenance practices. This commitment to value-added support strengthens Shell’s relevance in the region’s expanding infrastructure sector.

As part of its broader energy transition strategy, Shell continues to explore bio-based binders and low-carbon alternatives, positioning itself at the forefront of sustainable development in the African bitumen industry.

Nynas AB

Nynas is a leading global supplier of specialty bitumen products and holds a growing presence in the Africa bitumen market, particularly in North and Southern Africa. The company is known for its high-performance bitumen solutions designed for extreme weather conditions and heavy traffic environments.

Nynas collaborates with national road authorities and engineering firms to introduce advanced bitumen technologies such as polymer-modified and rubberized bitumen, which offer enhanced durability and reduced lifecycle costs.

Its strategic partnerships with local importers and blending facilities enable it to provide customized products suited to specific regional requirements, strengthening its competitive position.

With a focus on technical excellence and customer collaboration, Nynas continues to influence the evolution of bitumen specifications and application standards across several African countries.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by key players in the Africa bitumen market is product diversification and formulation adaptation , allowing companies to offer bitumen grades optimized for different climates, road types, and regulatory standards across African countries.

Strategic partnerships with governments and regional road agencies, enabling suppliers to align with national infrastructure priorities and secure long-term procurement contracts for large-scale road development initiatives, is another widely adopted approach.

Lastly, investment in technical training and after-sales support has become essential for differentiation. Leading companies are enhancing their value proposition by educating contractors, engineers, and road maintenance teams on best practices for bitumen application and performance optimization.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players of the Africa Bitumen Market include Shell, TotalEnergies, ExxonMobil, Sasol Limited, Indian Oil Corporation, Nynas AB, Colas Group, Engen Petroleum Ltd, Puma Energy, TIPCO Asphalt

The competition in the Africa bitumen market is shaped by a combination of global oil majors, regional traders, and emerging local blenders striving to capture a share of a rapidly expanding but highly fragmented sector. While multinational corporations like TotalEnergies, Shell, and Nynas bring brand recognition, technical expertise, and structured supply chains, regional traders often gain an edge through localized logistics and cost competitiveness.

End-users—ranging from national road agencies to private construction firms—are increasingly discerning, seeking not only reliable supply but also performance consistency and compliance with evolving environmental standards. This shift is influencing strategic moves, with companies emphasizing after-sales service, product innovation, and sustainability to build long-term relationships.

Despite logistical and regulatory challenges, the increasing need for durable transport infrastructure ensures sustained interest from both established and emerging players looking to capitalize on opportunities across diverse economic zones in Africa.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, TotalEnergies launched a new bitumen storage terminal in Lomé, Togo, aimed at improving regional supply chain efficiency and ensuring timely delivery of bitumen products to neighboring countries such as Burkina Faso and Mali.

- In July 2023, Shell initiated a technical collaboration with the Kenya National Highways Authority (KeNHA) to conduct field trials on polymer-modified bitumen applications, supporting the adoption of high-performance road surfacing materials in East Africa.

- In January 2025, Nynas AB expanded its technical advisory services into South Africa, providing free consultancy to public works departments and contractors on selecting the right bitumen grade for climate-resilient road construction.

- In May 2025, BP Plc strengthened its bitumen distribution network in Nigeria by partnering with a Lagos-based logistics firm to enhance last-mile delivery to federal and state-level road construction sites.

- In September 2025, Eni S.p.A announced a joint venture with a Tunisian refinery to blend and distribute locally adapted bitumen products across North Africa, reinforcing its regional supply chain resilience and market reach.

MARKET SEGMENTATION

This research report on the Africa Bitumen Market has been segmented and sub-segmented based on product type, application, and region.

By Product Type

- Paving Grade

- Hard Grade

- Oxidized Grade

- Bitumen Emulsions

- Polymer Modified Bitumen

- Other Product Types

By Application

- Road Construction

- Waterproofing

- Adhesives

- Other Applications

By Region

- Sudan

- Egypt

- Kenya

- Ethiopia

- South Africa

- Rest of Africa