Global Aircraft Electrical Systems Market Size, Share, Trends, & Growth Forecast Report, Segmented By Platform (Fixed Wing, Rotary Wing), Component (Generators, Conversion Devices, Battery Management Systems) Application (Power Generation Management, Flight Control & Operation, Cabin System, Configuration Management) Technology (Conventional, Electric), End-User (OEM (Original Equipment Manufacturer), Aftermarket), And By Region North America, Europe, Asia-Pacific, Latin America, Middle East And Africa), Industry Forecast From 2026 to 2034

Market Size, 2025

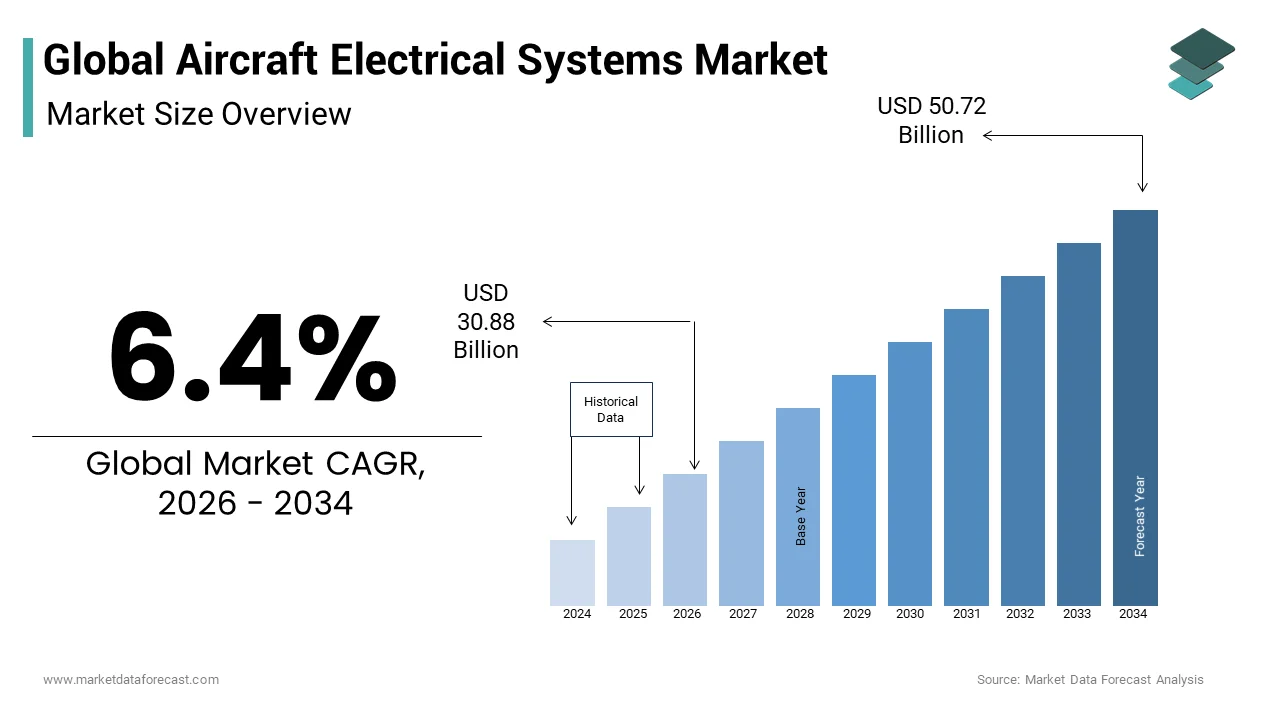

$29.02 BnMarket Estimate, 2026

$30.88 BnMarket Forecast, 2034

$50.72 BnCAGR, 2026–2034

6.4%Global Aircraft Electrical Systems Market Size

The global aircraft electrical systems market size was valued at USD 29.02 billion in 2025 and is anticipatd to reach USD 30.88 billion in 2026 to reach USD 50.72 billion by 2034, growing at an annual compound rate of 6.4% during the forecast period from 2026 to 2034.

Aircraft Electrical Systems are a broad range of components essential for powering and managing electrical functions across commercial, military, and general aviation aircraft. These systems include generators, transformers, inverters, power distribution units, circuit breakers, batteries, and advanced monitoring and control technologies. As aircraft become increasingly reliant on electrical subsystems for flight controls, navigation, communication, and in-cabin services, the demand for efficient, reliable, and high-performance electrical systems has grown significantly.

According to the International Air Transport Association (IATA), global air travel demand rebounded strongly in 2023, with passenger numbers reaching nearly 90% of pre-pandemic levels. This resurgence has driven airlines to invest in modern fleets equipped with next-generation electrical architectures that support fuel-efficient operations and digital cockpit integration. Apart from these, as per the Federal Aviation Administration (FAA), over 8,000 commercial aircraft deliveries are expected globally between 2024 and 2030, necessitating advanced electrical infrastructure.

Furthermore, the rise of electric and hybrid-electric propulsion research is reshaping the aircraft electrical systems landscape. The National Aeronautics and Space Administration (NASA) and leading aerospace firms have launched multiple initiatives aimed at developing all-electric regional aircraft, further reinforcing the strategic importance of robust and scalable electrical systems in future aviation design and performance optimization.

MARKET DRIVERS

Increasing Adoption of More Electric Aircraft (MEA) and All-Electric Platforms

The growing shift toward More Electric Aircraft (MEA) and all-electric propulsion platforms is one of the primary drivers of the Aircraft Electrical Systems Market. Traditional aircraft rely heavily on hydraulic and pneumatic systems, which are being gradually replaced by electrically powered alternatives to enhance efficiency, reduce weight, and lower maintenance costs.

This transition is particularly evident in next-generation aircraft like the Boeing 787 Dreamliner and Airbus A350, both of which feature high-voltage electrical systems capable of supporting more than 60% of onboard functions through electrical means. As reported by Rolls-Royce’s Future of Aerospace report, the electrical load in modern aircraft has increased by over 200% compared to older models, necessitating advancements in power generation, conversion, and distribution systems.

Besides, defense programs are accelerating this trend, with fighter jets such as the F-35 Lightning II integrating full-authority digital engine controls and integrated power management systems. These developments show the increasing reliance on sophisticated electrical systems, directly boosting market growth across both civil and military aviation sectors.

Rising Demand for Commercial Aircraft Fleets and Fleet Modernization

The surge in commercial aircraft orders and fleet modernization efforts undertaken by major airlines worldwide is another key driver influencing the Aircraft Electrical Systems Market. As global air traffic rebounds post-pandemic, carriers are investing heavily in newer, fuel-efficient aircraft that feature advanced electrical architectures designed for improved performance and reduced emissions. According to the International Civil Aviation Organization (ICAO), global commercial aircraft deliveries reached over 1,200 units in 2023, reflecting a strong recovery in aviation infrastructure investments.

Major aircraft manufacturers such as Boeing and Airbus have ramped up production to meet backlogged orders from airlines seeking to replace aging fleets. These new-generation aircraft incorporate extensive electrical systems to support fly-by-wire controls, in-flight entertainment, cabin climate regulation, and real-time diagnostics.

Moreover, regulatory pressures to reduce carbon footprints are prompting airlines to adopt aircraft with optimized electrical systems that support higher energy efficiency. With IATA projecting a doubling of global air passengers by 2040, the demand for technologically advanced aircraft electrical systems will continue to grow in tandem with fleet expansion and operational modernization initiatives.

MARKET RESTRAINTS

High Development and Certification Costs for Advanced Electrical Components

The high cost associated with the development, testing, and certification of advanced electrical components is a major restraint affecting the Aircraft Electrical Systems Market. Unlike consumer electronics, aircraft electrical systems must undergo rigorous safety evaluations and compliance assessments under strict regulations set by bodies such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA).

These costs are particularly burdensome for smaller suppliers and emerging players attempting to enter the market with innovative solutions. Startups focusing on solid-state power distribution or high-frequency electrical systems often struggle with financial constraints, limiting their ability to scale operations or achieve regulatory approval within competitive timeframes.

Moreover, the need for redundant and fail-safe designs increases manufacturing expenses. Military and commercial aircraft require dual or triple-redundant systems to ensure reliability under extreme conditions, further escalating costs. These economic barriers hinder rapid innovation and restrict market entry, slowing the pace of technological advancement in aircraft electrical systems.

Complexity in Integrating Electrical Systems with Existing Aircraft Architectures

The complexity involved in integrating advanced electrical systems with legacy aircraft architectures is another significant challenge impeding the Aircraft Electrical Systems Market. Many existing commercial and military aircraft were originally designed around traditional hydraulic and mechanical control systems, making retrofitting with modern electrical infrastructure both technically challenging and financially unviable.

Integration challenges extend beyond hardware compatibility to include software interoperability, thermal management, and electromagnetic interference (EMI) issues. As highlighted by NASA’s Aviation Systems Division, electromagnetic compatibility remains a critical concern when upgrading avionics and electrical wiring interconnection systems (EWIS), requiring extensive re-engineering to prevent signal disruptions or system failures.

Furthermore, the lack of standardized protocols for electrical system architecture complicates cross-manufacturer compatibility. Airlines operating mixed fleets face additional hurdles in maintaining uniformity across electrical subsystems, reducing the feasibility of widespread adoption. These technical and logistical barriers limit the scalability of advanced electrical systems, particularly in mid-life aircraft that constitute a large portion of active fleets.

MARKET OPPORTUNITIES

Growth of Urban Air Mobility and Electric Vertical Takeoff and Landing (eVTOL) Vehicles

The rapid development of Urban Air Mobility (UAM) and Electric Vertical Takeoff and Landing (eVTOL) vehicles is a promising opportunity within the Aircraft Electrical Systems Market. These next-generation aerial transport solutions rely entirely on electric propulsion systems, creating unprecedented demand for high-capacity batteries, lightweight power distribution modules, and advanced thermal management systems.

Leading aerospace firms such as Airbus, Bell Textron, and Joby Aviation are actively developing battery-powered aircraft designed for short-haul urban transportation, each requiring fully integrated electrical infrastructures. As per the Vertical Flight Society, eVTOL aircraft typically operate on 500V–1000V electrical systems, far exceeding the voltage requirements of conventional aircraft, thus driving innovation in high-density, high-efficiency electrical components.

Further, government agencies and city planners are investing in infrastructure to support eVTOL operations, including vertiports and charging stations, further accelerating market readiness. With the Federal Aviation Administration (FAA) and EASA working closely with developers to establish regulatory frameworks, the eVTOL sector presents a transformative opportunity for aircraft electrical systems providers aiming to capture early-mover advantage in this emerging mobility ecosystem.

Expansion of Onboard Power Generation and Energy Storage Technologies

The expansion of onboard power generation and energy storage technologies, driven by the need for greater autonomy and reduced dependence on fossil fuels, is an emerging opportunity in the Aircraft Electrical Systems Market. As aircraft move toward more electric and hybrid-electric configurations, the demand for compact, high-efficiency generators, supercapacitors, and advanced lithium-ion battery packs is surging.

Innovations such as variable frequency generators, solid oxide fuel cells, and regenerative braking systems are gaining traction among aircraft designers seeking to optimize power usage and reduce overall energy consumption. As per the International Council on Clean Transportation (ICCT), next-generation aircraft could reduce fuel burn by up to 20% through electrified auxiliary power units and energy recovery systems, enhancing both environmental and economic performance.

Apart from these, military aircraft programs are exploring high-energy-density batteries for stealth applications and extended mission capabilities. Companies like Safran and Honeywell are actively engaged in developing modular energy storage units compatible with both current and future aircraft platforms. These advancements open new avenues for growth in the aircraft electrical systems domain, positioning energy storage as a cornerstone of next-generation aviation technology.

MARKET CHALLENGES

Thermal Management and Overheating Risks in High-Density Electrical Systems

The issue of thermal management in high-density electrical systems is a pressing challenge confronting the Aircraft Electrical Systems Market. As aircraft integrate more electric components, ranging from high-power generators to solid-state switching devices, the risk of overheating and subsequent system failure increases significantly. Also, thermal runaway in electrical circuits is one of the leading causes of avionics malfunctions, particularly in tightly packed fuselage compartments.

Modern aircraft, especially those adopting More Electric Aircraft (MEA) architectures, generate substantial heat due to high-current loads and compact wiring harnesses. As reported by the Society of Automotive Engineers (SAE), electrical systems in next-generation aircraft can reach temperatures exceeding 200°C, necessitating advanced cooling mechanisms such as liquid cooling loops and phase-change materials. However, these solutions add weight and complexity, offsetting some of the efficiency gains sought through electrification.

Furthermore, electromagnetic interference (EMI) and insulation degradation in high-temperature environments pose additional risks to system reliability. Addressing these thermal challenges requires continuous innovation in material science, circuit design, and cooling system engineering to ensure safe and dependable aircraft electrical performance.

Cybersecurity Threats to Digitally Integrated Electrical Systems

The rising threat of cybersecurity vulnerabilities in digitally integrated electrical systems is another critical challenge impacting the Aircraft Electrical Systems Market. As aircraft electrical architectures become more interconnected and software-driven, they are increasingly exposed to potential cyber threats targeting flight controls, power distribution networks, and onboard diagnostics. According to a 2024 report by the Aerospace Industries Association (AIA), over 60% of recent aviation security audits identified potential entry points in aircraft electrical and avionics systems, emphasizing the urgent need for hardened cybersecurity measures.

Modern aircraft now feature Ethernet-based power management systems, remote diagnostics, and cloud-connected maintenance tools, expanding the attack surface for malicious actors. Also, cybersecurity researchers have demonstrated proof-of-concept attacks that could manipulate electrical system parameters via compromised in-flight entertainment networks, raising concerns about system integrity.

Regulatory bodies such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA) have mandated stricter cybersecurity standards for new aircraft certifications. Manufacturers are responding by incorporating secure boot processes, encrypted data transmission, and intrusion detection systems into electrical subsystems.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.4% |

| Segments Covered | By Technology, Components, Application, End-User, and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Boeing, Thales Group, GE Aviation, T.E Connectivity, Safran Zodiac Aerospace, Eaton, Honeywell International, Inc., Esterline Control Systems, Aircraft Spruce and Astronics Corporation |

SEGMENTAL ANALYSIS

By Platform Insights

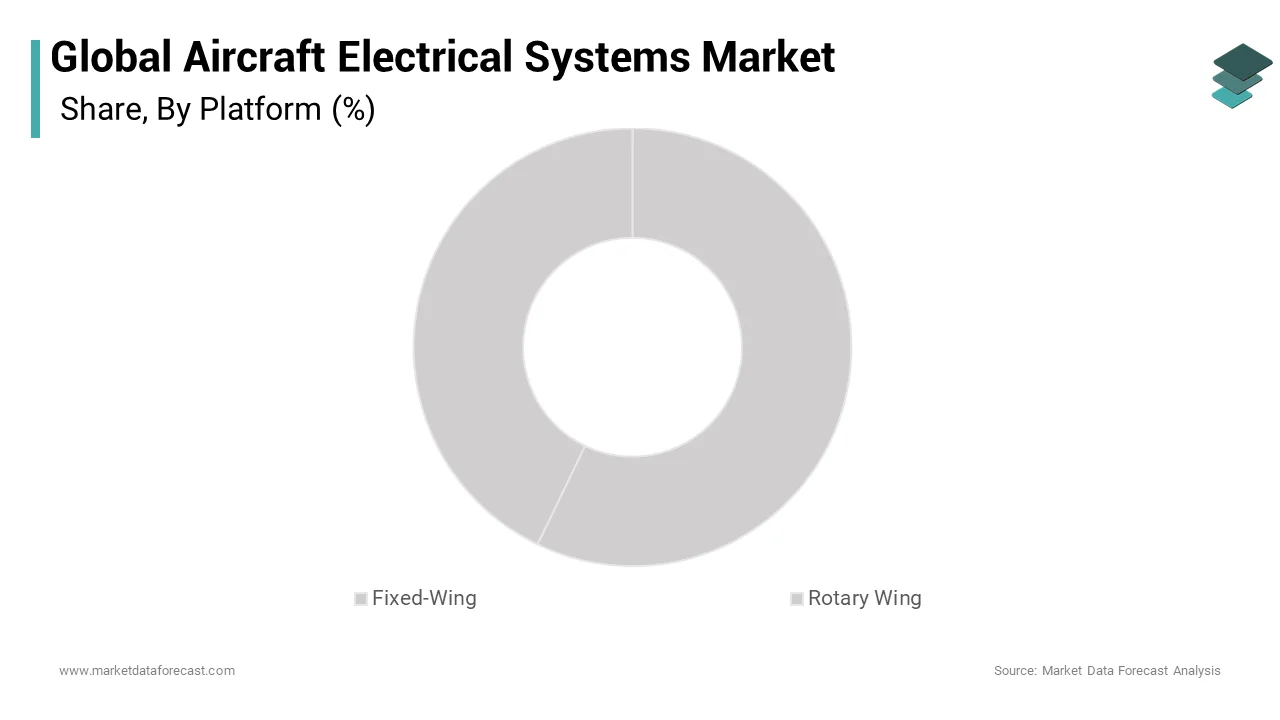

The fixed-wing aircraft segment commanded the Aircraft Electrical Systems Market by accounting for a substantial portion of total revenue in 2024. This dominance is primarily attributed to the high volume of commercial and military fixed-wing aircraft deliveries globally, which rely heavily on advanced electrical systems for power generation, distribution, and control, and is primarily credited for the dominance of the fixed-wing aircraft segment.

In addition, the increasing electrification of flight-critical systems such as fly-by-wire controls, avionics, and cabin management is also a key driver behind the growth of this segment. According to the Aerospace Industries Association (AIA), over 85% of new-generation commercial aircraft now incorporate full or partial More Electric Aircraft (MEA) architectures, significantly boosting demand for high-performance electrical components. The Boeing 787 Dreamliner and Airbus A350 are prime examples, both featuring extensive electrical subsystems that replace traditional hydraulic and pneumatic setups.

Besides, defense modernization programs have further strengthened the market position of fixed-wing platforms. As per the U.S. Department of Defense, over 1,200 military fixed-wing aircraft are expected to be procured between 2024 and 2030, each requiring sophisticated electrical infrastructure for radar, electronic warfare, and autonomous operations. These factors collectively reinforce the fixed-wing platform's dominant role in shaping the future of aircraft electrical systems.

The rotary-wing aircraft segment is projected to be the fastest-growing within the Aircraft Electrical Systems Market, with a CAGR of 9.4% between 2025 and 2033.

The rising adoption of electric propulsion systems in next-generation rotorcraft is a major factor fueling the growth of the rotary-wing aircraft segment. While currently holding a smaller share compared to fixed-wing aircraft, rotary-wing platforms—comprising helicopters and emerging eVTOL (electric Vertical Takeoff and Landing) vehicles—are experiencing rapid technological evolution and increased electrification. According to the Vertical Flight Society, over 60 eVTOL development programs were actively underway globally in 2024, many of which are based on fully electric or hybrid-electric configurations. These aircraft require high-capacity batteries, advanced power conversion units, and integrated energy management systems, all of which drive demand for next-gen electrical components.

Moreover, urban air mobility (UAM) initiatives are accelerating investment in rotary-wing electrical systems. As per McKinsey & Company’s 2024 Urban Air Mobility Outlook, urban air taxi services could become commercially viable by 2027, contingent upon robust onboard electrical infrastructure. Moreover, military and emergency response sectors are adopting more electric helicopter designs to reduce maintenance costs and improve operational efficiency, further strengthening the outlook for this high-growth segment.

By Component Insights

The generators segment maintained the top-performing category in the Aircraft Electrical Systems Market by capturing 34.5% of total component sales in 2024.

The increasing electrification of aircraft systems, particularly in More Electric Aircraft (MEA) and all-electric propulsion platforms, is one primary driver behind the strong position of the generators segment. Generators are essential for converting mechanical energy from engines or auxiliary power units into electrical energy, powering critical aircraft functions ranging from avionics to cabin systems. According to Rolls-Royce’s Future of Aerospace report, the electrical load in modern commercial aircraft has grown by over 200% compared to older models, necessitating higher-capacity generators capable of supporting these demands. The Boeing 787 Dreamliner, for instance, utilizes six integrated drive generators to supply power across its digital cockpit and distributed electrical architecture.

Furthermore, military aircraft upgrades are reinforcing generator demand. As per the U.S. Air Force Research Laboratory, next-generation fighter jets such as the F-35 Lightning II incorporate variable frequency generators to support high-energy weapon systems and sensor arrays, enhancing mission capabilities.

The battery management systems (BMS) segment is emerging as the fastest-growing within the Aircraft Electrical Systems Market, with a CAGR of 11.2% forecasted between 2024 and 2030. This rapid expansion is driven by the Growing reliance on lithium-ion and solid-state batteries in both commercial and military aircraft, especially in More Electric Aircraft (MEA) and electric propulsion systems, which is largely contributing to the rapid growth of the battery management systems (BMS) segment.

The increasing deployment of high-density battery packs in next-generation aircraft is another key factor fueling this growth. Battery management systems are essential for monitoring voltage, temperature, and charge levels to prevent thermal runaway and optimize performance.

Further, regulatory mandates and industry standards are pushing aerospace firms to adopt advanced BMS solutions. With the rise of electric vertical takeoff and landing (eVTOL) vehicles and hybrid-electric regional aircraft, the demand for sophisticated battery management systems is set to accelerate even further.

By Application Insights

The power generation management segment commanded the Aircraft Electrical Systems Market by capturing 38.5% of total application-based demand in 2024. This dominance of the segment is due to the critical need for reliable and efficient power generation across all aircraft types, particularly as electrical loads increase due to digitization and automation.

An additional major driver behind this segment’s leadership is the integration of high-output generators and auxiliary power units (APUs) in next-generation aircraft. According to the Aerospace Industries Association (AIA), the electrical load in modern commercial aircraft has surged by over 200% compared to legacy models, necessitating advanced power generation and regulation technologies. The Boeing 787 Dreamliner, for example, features six variable-speed generators to support its fully integrated electrical architecture.

A further contributing factor is the adoption of hybrid-electric propulsion research programs, which require highly efficient power generation systems to support onboard energy needs. As per NASA’s Glenn Research Center, hybrid-electric aircraft under development feature multi-megawatt-class generators to support propulsion and avionics, highlighting the growing complexity of power generation systems. These advancements ensure that power generation management remains a cornerstone of aircraft electrical system design and development.

The flight control & operation segment is projected to grow at the fastest rate within the Aircraft Electrical Systems Market, with a CAGR of 10.8%. The increasing reliance on electrical systems for primary and secondary flight control functions, replacing traditional hydraulic and mechanical systems, is driving the acceleration of the flight control & operation segment.

The widespread adoption of fly-by-wire (FBW) technology in modern aircraft also contributes to the rise of this segment. These systems enhance fuel efficiency, reduce weight, and improve responsiveness, making them indispensable in next-generation aircraft.

Apart from these, the push toward autonomous and semi-autonomous flight operations is intensifying demand for advanced electrical control modules. These developments underscore the expanding role of electrical systems in flight control, positioning this segment for sustained growth across civil and military aviation.

REGIONAL ANALYSIS

North America Aircraft Electrical Systems Market Insights

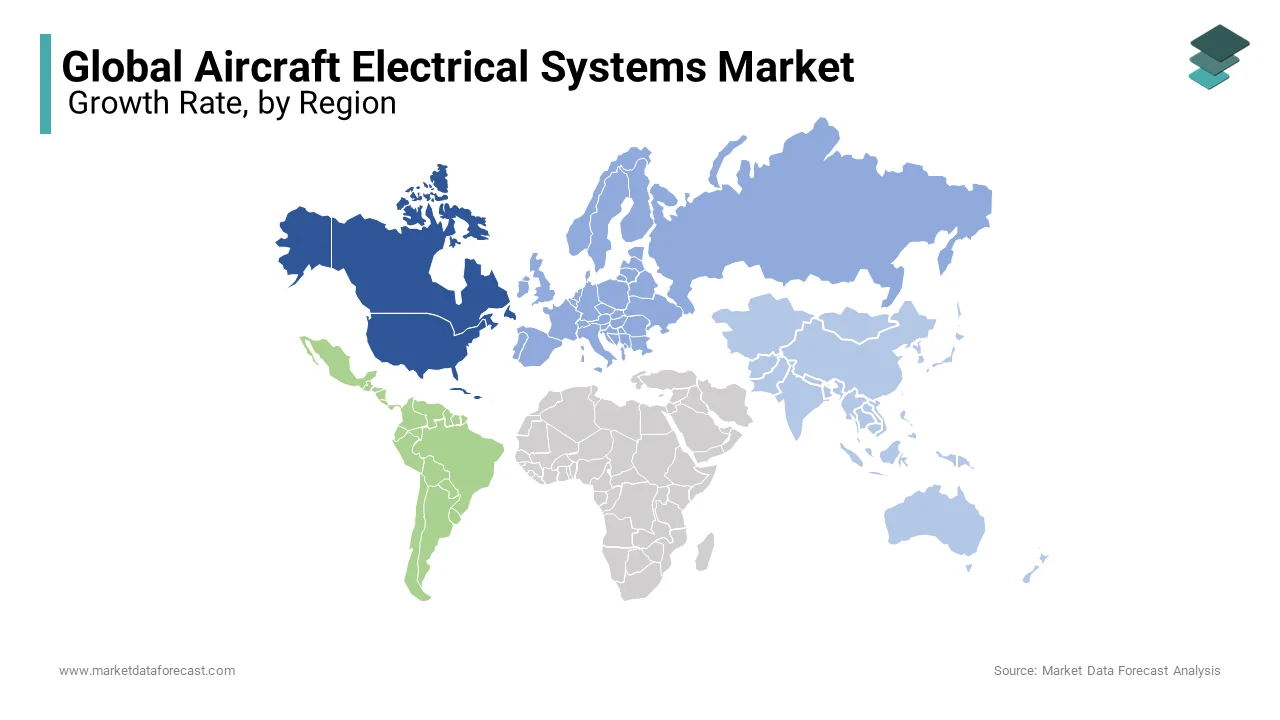

North America maintained a dominant position in the global Aircraft Electrical Systems Market by capturing an estimated share of 39.6% in 2024. The region’s leading position is underpinned by the presence of major aerospace manufacturers, extensive defense spending, and a strong commercial aviation sector.

A key growth driver is the high level of investment in next-generation aircraft development. According to the Aerospace Industries Association (AIA), over 1,200 commercial aircraft deliveries were made by North American manufacturers in 2023, each incorporating advanced electrical systems for power management, avionics, and digital cockpits. Besides, the U.S. Department of Defense continues to fund modernization programs involving stealth fighters, unmanned aerial vehicles (UAVs), and next-generation transport aircraft, all of which integrate cutting-edge electrical architectures.

Moreover, the region leads in the development of More Electric Aircraft (MEA) and electric propulsion technologies. NASA and leading firms like Boeing and General Electric are actively engaged in R&D initiatives aimed at reducing reliance on hydraulic systems and optimizing onboard electrical networks.

Europe Aircraft Electrical Systems Market Insights

Europe holds a significant share of the Aircraft Electrical Systems Market. The region benefits from a well-established aerospace industry, led by companies such as Airbus, Safran, and Leonardo, which are driving the adoption of advanced electrical systems in commercial and military aircraft.

A key growth factor is the increasing integration of More Electric Aircraft (MEA) technologies in the latest Airbus A320neo and A350 series.

Moreover, government-backed initiatives to decarbonize aviation are accelerating the shift toward electric propulsion systems. These efforts, combined with strong collaboration between academic institutions and industry players, position Europe as a key contributor to the global aircraft electrical systems landscape.

Asia-Pacific Aircraft Electrical Systems Market Insights

Asia-Pacific is a lucrative region in the global Aircraft Electrical Systems Market. The region’s growth is driven by expanding commercial airline fleets, rising defense budgets, and increasing investments in indigenous aircraft manufacturing.

China and India are emerging as key markets due to their ambitious aviation modernization programs. According to the Civil Aviation Administration of China (CAAC), domestic airlines placed orders for over 400 new aircraft in 2023, many of which feature advanced electrical architectures designed for improved efficiency and connectivity.

Japan and South Korea are also contributing to market expansion through partnerships with global aerospace firms. As per the Japan Aerospace Industries Association (JAIA), Japanese companies have secured contracts worth over USD 1.2 billion in 2023 to supply electrical components for international aircraft programs, reinforcing the country’s strategic role in the value chain. With continued fleet expansion and growing interest in urban air mobility, Asia-Pacific presents substantial opportunities for aircraft electrical systems providers seeking long-term growth.

Middle East and Africa Aircraft Electrical Systems Market Insights

Middle East and Africa are gaining momentum due to expanding air travel demand and strategic defense procurement initiatives.

The Middle East, particularly the Gulf Cooperation Council (GCC) countries, is a key growth engine. According to the Arab Air Carriers Organization (AACO), Gulf airlines accounted for nearly 15% of global wide-body aircraft deliveries in 2023, with carriers like Emirates and Qatar Airways investing in ultra-modern fleets equipped with advanced electrical architectures. Dubai Airports and Riyadh Airports Authority have also initiated smart airport projects that align with onboard digitalization trends, reinforcing demand for upgraded aircraft electrical systems.

In Africa, the Nigerian and South African aviation sectors are witnessing gradual modernization, supported by government-backed infrastructure upgrades and foreign investments. As per the African Airlines Association (AFRAA), regional airlines are increasingly leasing modern aircraft with enhanced electrical capabilities, signaling a shift away from aging fleets. These developments indicate growing potential for aircraft electrical systems in the Middle East and Africa, despite ongoing economic and logistical challenges.

Latin America Aircraft Electrical Systems Market Insights

Latin America is showing steady progress due to fleet modernization efforts and the expansion of low-cost carriers.

Brazil is the leading market in the region, benefiting from Embraer’s presence and its growing focus on regional jet exports equipped with advanced electrical systems.

Mexico is also emerging as a hub for aircraft component manufacturing, attracting foreign direct investment from U.S. and European suppliers. While limited by budget constraints and infrastructure limitations, Latin America’s evolving aviation ecosystem offers long-term potential for aircraft electrical systems providers aiming to diversify beyond traditional markets.

COMPETITIVE LANDSCAPE

The competition in the Aircraft Electrical Systems Market is intense, driven by rapid technological evolution, increasing electrification of aircraft functions, and stringent safety and performance standards. Established aerospace giants such as Honeywell, Collins Aerospace, and Safran dominate the landscape due to their deep engineering expertise, broad product portfolios, and long-standing relationships with major aircraft manufacturers. However, they face growing competition from specialized firms and emerging startups focused on niche areas like solid-state power distribution, high-density energy storage, and smart electrical monitoring systems.

Market leaders differentiate themselves through innovation, regulatory compliance, and system integration capabilities, particularly as the industry moves toward More Electric Aircraft (MEA) and fully electric propulsion systems. Smaller players are leveraging agility and disruptive technologies to carve out market space, often partnering with larger firms to scale their solutions. Further, the rise of urban air mobility (UAM) and eVTOL vehicles has introduced new entrants seeking to redefine electrical system architecture.

Competition is also intensifying around cybersecurity, weight reduction, and thermal management, as aircraft designers demand more robust and efficient electrical infrastructures. As the industry shifts toward sustainability and digitalization, differentiation through reliability, modularity, and compatibility with future aircraft platforms will be critical in determining long-term market leadership.

KEY MARKET PLAYERS

The global aircraft electrical system market is concentrated with well-established players. Key players in the market included

- Boeing

- Thales Group

- GE Aviation

- T.E Connectivity

- Safra Zodiaccc Aerospace

- Eaton

- Honeywell International, Inc.

- Esterline Control Systems

- Aircraft Spruce

- Astronics Corporation.

Top Players In The Market

- Honeywell Aerospace is a leading global supplier of aircraft electrical systems, known for its innovative power generation, distribution, and energy storage solutions. The company plays a crucial role in advancing More Electric Aircraft (MEA) technologies by offering high-efficiency generators, solid-state power controllers, and advanced battery management systems. Honeywell’s contributions to next-generation aircraft such as the Boeing 787 and Airbus A350 have positioned it as a key player in shaping the future of aircraft electrification.

- Collins Aerospace, a Raytheon Technologies company, is a major force in the Aircraft Electrical Systems Market, providing integrated power solutions for commercial, military, and business aviation platforms. The company's expertise lies in developing scalable electrical architectures that support fly-by-wire controls, avionics integration, and onboard energy optimization. Collins Aerospace has been instrumental in enabling hybrid-electric propulsion research through strategic partnerships with aerospace agencies and defense organizations.

- Safran Electrical & Power Systems specializes in designing and manufacturing high-performance electrical systems tailored for modern aircraft requirements. With a strong focus on lightweight, compact, and high-efficiency components, Safran supports the transition toward electric and hybrid-electric aircraft. Its innovations in power conversion and thermal management have made it a preferred partner for both civil and military aviation programs worldwide.

Top Strategies Used By Key Market Participants

A primary strategy employed by leading players in the Aircraft Electrical Systems Market is continuous investment in R&D to develop next-generation electrical architectures. Companies are focusing on high-voltage DC systems, solid-state circuit protection, and modular power electronics to meet evolving aircraft design demands and improve system efficiency.

Another key approach is strategic collaborations with airframers, propulsion developers, and regulatory bodies. By working closely with original equipment manufacturers (OEMs) and government agencies, companies ensure alignment with industry standards while accelerating the certification and deployment of new electrical technologies.

Lastly, expanding into emerging markets and forming joint ventures with regional suppliers has become essential for maintaining a competitive advantage. This enables companies to strengthen their supply chains, enhance local service capabilities, and capture growth opportunities in fast-developing aviation sectors across Asia-Pacific and the Middle East.

RECENT MARKET NEWS

- In January 2024, Honeywell Aerospace unveiled a new line of variable frequency generators designed specifically for next-generation narrow-body aircraft, aiming to enhance power efficiency and reduce overall system weight in collaboration with major OEMs.

- In March 2024, Collins Aerospace announced a strategic partnership with a European battery technology firm to co-develop advanced lithium-ion battery packs and integrated management systems tailored for hybrid-electric regional aircraft development.

- In June 2024, Safran Electrical & Power Systems launched an ultra-compact solid-state power distribution unit for military and commercial applications, emphasizing reduced maintenance costs and improved fault tolerance under extreme operating conditions.

- In September 2024, Raytheon Technologies, parent company of Collins Aerospace, acquired a startup specializing in AI-driven electrical diagnostics, signaling a move toward smarter, predictive maintenance-enabled aircraft electrical networks.

- In November 2024, GE Aerospace introduced a modular electrical power conversion system aimed at supporting future all-electric propulsion demonstrators, aligning with ongoing efforts to decarbonize regional aviation and urban air mobility platforms.

MARKET SEGMENTATION

This research report on the global aircraft electrical systems market has been segmented and sub-segmented based on the component, technology, application, and region.

By Platform

- Fixed-Wing

- Rotary Wing

By Component

- Generators

- Conversion Devices

- Battery Management Systems

By Application

- Power Generation Management

- Flight Control & Operation

- Cabin System

- Configuration Management

By Technology

- Conventional

- Electric

By End User

- OEM (Original Equipment Manufacturer)

- Aftermarket

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What is the aircraft electrical systems market?

The aircraft electrical systems market includes systems and components used to generate, distribute, and manage electrical power in aircraft.

Why is the aircraft electrical systems market growing rapidly?

The market is growing due to increasing aircraft production and rising demand for advanced aviation technologies.

What types of aircraft electrical systems are commonly used?

Common systems include power generation systems, lighting systems, wiring systems, and flight control electrical systems.

Which aircraft electrical systems segment leads the market?

Power generation systems dominate the market due to their critical role in aircraft operations and onboard functionality.

Who are the primary users of aircraft electrical systems?

Aircraft manufacturers, airlines, defense organizations, and maintenance service providers are the main users.

How do aircraft electrical systems improve aircraft performance?

They support efficient power management, improve operational reliability, and enhance flight safety.

Why is the more electric aircraft concept increasing demand for aircraft electrical systems?

More electric aircraft require advanced electrical technologies to reduce fuel consumption and improve efficiency.

What challenges does the aircraft electrical systems market face?

High development costs and strict aviation safety regulations can affect market growth.

How is technology influencing the aircraft electrical systems market?

Advanced power electronics, lightweight materials, and smart monitoring systems are improving electrical system performance.

What is the future outlook for the aircraft electrical systems market?

The market is expected to grow steadily with increasing aircraft modernization and demand for energy-efficient aviation systems.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com