Global Antacids Market Size, Share, Trends & Growth Analysis Report Segmented By Drug Class (Proton Pump Inhibitors, H2 Antagonist, Pro-motility agents and Acid Neutralizers), Formulation Type (Tablet, Liquid, Powder), Distribution Channel & Region (North America, Europe, APAC, Latin America, Middle East and Africa), Industry Analysis From 2025 to 2033

Global Antacids Market Summary

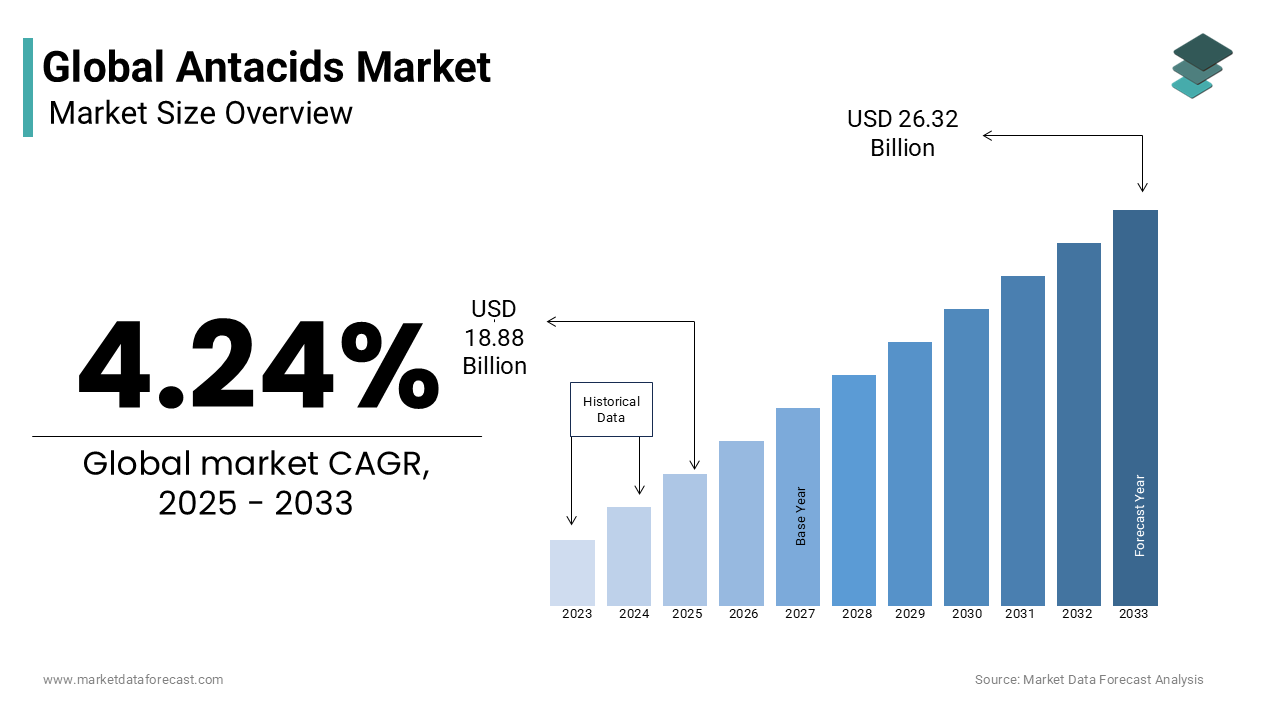

The global antacids market was valued at USD 18.11 billion in 2024 and is projected to reach USD 26.32 billion by 2033, growing at a CAGR of 4.24% from 2025 to 2033. With a forecasted market size of USD 18.88 billion in 2025, the market is witnessing steady growth, driven by the rising prevalence of gastrointestinal (GI) disorders, increasing consumption of processed and spicy foods, urbanization, and growing awareness of over-the-counter (OTC) digestive health remedies.

The antacids market refers to the industry encompassing medications designed to neutralize stomach acid and provide rapid relief from conditions such as heartburn, acid indigestion, gastroesophageal reflux disease (GERD), and peptic ulcers. These products include chemical antacids (e.g., aluminum hydroxide, magnesium hydroxide), H2 receptor antagonists, and proton pump inhibitors (PPIs), available in various formulations such as tablets, liquids, chewables, and capsules.

Key Market Trends

- Rising demand for fast-acting, non-prescription antacids is boosting OTC product innovation and branding.

- Increasing use of combination therapies (e.g., antacids with alginates or simethicone) enhances symptom relief and drives product differentiation.

- Growth in e-pharmacy platforms is transforming access to antacid medications, especially in emerging markets.

- Growing awareness of side effects associated with long-term PPI use is prompting a shift toward natural and herbal alternatives.

Key Market Insights

- Based on drug class, the proton pump inhibitors (PPIs) segment dominated the market in 2024 and is expected to maintain its leadership throughout the forecast period, owing to their high efficacy in reducing gastric acid secretion and long-lasting relief for chronic acid-related disorders.

- In terms of formulation, the tablet segment held the largest market share in 2024, favored for its portability, ease of dosing, and consumer preference for solid oral dosage forms.

- Based on distribution channels, online pharmacies, retail drug stores, and hospital pharmacies are anticipated to collectively capture the majority of market share, with online sales experiencing accelerated growth due to e-commerce expansion, digital health adoption, and the convenience of home delivery.

- By disease indication, the cardiovascular disorders segment accounted for the leading share in 2024, this reflects the high incidence of drug-induced gastric complications (e.g., from NSAIDs and anticoagulants) among cardiac patients, necessitating co-administration of acid-reducing therapies.

- Regionally, North America held the largest market share in 2024, driven by high healthcare spending, widespread OTC medication use, and a large patient pool suffering from acid reflux and related GI conditions.

- The Asia Pacific region ranked second, capturing a significant share and showing strong growth potential due to rising disposable incomes, expanding healthcare access, increasing urbanization, and growing awareness of digestive health in countries like India, China, and Japan.

- Leading players in the global antacids market include GlaxoSmithKline PLC, Abbott Laboratories, Pfizer, Inc., Sun Pharmaceuticals, and Dabur, which are focusing on product innovation, strategic marketing, and expanding their presence in both developed and emerging markets.

Global Antacids Market Size

As per our report, the global antacids market is predicted to be worth USD 26.32 billion by 2033 from USD 18.88 billion in 2025, growing at a CAGR of 4.24% during the forecast period. The antacids market size was valued at USD 18.11 billion in 2024.

Antacids are over-the-counter pharmaceutical formulations designed to neutralize gastric acid, providing rapid symptomatic relief from conditions such as heartburn, acid indigestion, and gastroesophageal reflux. These agents typically contain alkaline compounds like calcium carbonate, magnesium hydroxide, or aluminum hydroxide, which react with hydrochloric acid in the stomach to elevate pH and alleviate discomfort. The widespread prevalence of lifestyle-induced gastric disturbances, coupled with the accessibility of non-prescription antacids, has entrenched their role in self-medication practices across both developed and emerging economies.

MARKET DRIVERS

Rising Incidence of Diet-Induced Gastrointestinal Disorders

The growing consumption of processed, high-fat, and acidic foods due to rising demand for immediate symptomatic relief is driving the growth of the Africa yogurt market. According to the International Agency for Research on Cancer, diets rich in fried and preserved foods are linked to a 35% higher incidence of gastroesophageal reflux disease (GERD) in urban populations across Asia and Latin America. In India, a 2023 multicenter study published by the Indian Journal of Gastroenterology found that 52% of adults in metropolitan cities reported weekly heartburn, primarily attributed to dietary shifts toward fast food and carbonated beverages. This persistent symptom burden has led to increased reliance on fast-acting antacids, particularly chewable tablets and oral suspensions, which offer immediate neutralization within minutes of ingestion.

Increasing Prevalence of Stress-Related Gastric Disturbances

The psychological stress is a well-documented contributor to gastric acid hypersecretion and functional dyspepsia, which is fuelling the growth of the Africa yogurt market. As per the World Health Organization, global anxiety levels have risen by 25% since 2020, with prolonged stress disrupting autonomic regulation of gastric function and lowering the threshold for acid reflux. A 2023 study conducted by the European Society of Neurogastroenterology and Motility revealed that individuals with high occupational stress exhibited a 48% greater likelihood of chronic heartburn compared to low-stress counterparts.

MARKET RESTRAINTS

Risk of Long-Term Use Leading to Metabolic and Renal Complications

The prolonged or excessive antacid consumption for those containing aluminum or magnesium, is associated with systemic adverse effects that deter sustained use, which is hindering the growth of the Africa yogurt market. According to the U.S. National Kidney Foundation, chronic intake of aluminum-based antacids can lead to aluminum accumulation in patients with renal insufficiency, increasing the risk of encephalopathy and bone demineralization. Magnesium-containing formulations, while effective, may cause diarrhea and, in severe cases, magnesium toxicity in patients with impaired kidney function. These risks have prompted regulatory advisories in multiple countries, including the UK’s Medicines and Healthcare products Regulatory Agency, which issued updated labeling guidelines in 2023 to caution against long-term self-medication, thereby limiting consumer confidence in extended use.

Shift Toward Proton Pump Inhibitors and Prescription Alternatives

The availability and increasing accessibility of more potent acid-suppressing medications such as proton pump inhibitors (PPIs) and H2-receptor antagonists, have diminished the role of antacids as primary long-term therapy for chronic acid disorders. As per the Centers for Disease Control and Prevention, over 15 million Americans were prescribed PPIs in 2023, driven by their superior efficacy in healing esophagitis and preventing ulcer recurrence. Furthermore, the inclusion of certain PPIs like omeprazole in essential medicine lists across low- and middle-income countries has expanded their availability, often at comparable prices to antacids. This therapeutic shift has relegated antacids largely to symptomatic, short-term use, constraining their market growth potential despite high initial consumer uptake.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Drug Class, Formulation Type, Distribution Channel, Disease Indications, End-User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leader Profiled | GlaxoSmithKline PLC, Abbott Laboratories, Pfizer, Inc., Sun Pharmaceuticals, and Dabur |

REGIONAL ANALYSIS

By Drug Class Insights

The acid neutralizers segment was accounted in holding 44.3% of the antacids market share in 2024 with their immediate onset of action and widespread availability as over-the-counter (OTC) remedies. Unlike delayed-acting agents, acid neutralizers such as calcium carbonate and magnesium hydroxide begin neutralizing gastric acid within 3 to 5 minutes of ingestion by making them the preferred choice for acute symptom relief. According to the American Gastroenterological Association, 68% of U.S. consumers experiencing heartburn opt for antacids as their first-line response due to rapid symptom alleviation.

The Proton pump inhibitors (PPIs) segment is expected to register a CAGR of 7.6% during the forecast period with their superior efficacy in managing chronic acid-related disorders such as erosive esophagitis and Barrett’s esophagus. PPIs like omeprazole and esomeprazole achieve up to 98% suppression of gastric acid secretion by irreversibly inhibiting the H+/K+ ATPase enzyme in parietal cells. As per a 2023 study published in The Lancet Gastroenterology & Hepatology, long-term PPI use reduced the risk of esophageal adenocarcinoma by 72% in high-risk GERD patients. Furthermore, their inclusion in national essential medicine lists in countries such as India and South Africa has expanded access, while generic availability has driven affordability, accelerating adoption beyond prescription-only use into the OTC domain.

By Formulation Type Insights

The tablet formulation segment was the largest and held 52.3% of the antacids market share in 2024 with the portability, precise dosing, and extended shelf life, which align with modern consumer preferences for convenience and discreet usage. Chewable antacid tablets, particularly those containing calcium carbonate, are widely favored due to their ease of administration without water, making them ideal for on-the-go relief. A 2023 survey by the Consumer Healthcare Products Association found that 74% of American adults prefer tablets over liquids for managing occasional heartburn.

The liquid formulation segment is expected to grow at a CAGR of 6.9% during the forecast period with the superior acid-neutralizing capacity and faster dispersion in the stomach compared to solid forms. Liquid antacids can achieve a higher surface area contact with gastric contents, providing more uniform and rapid pH elevation. Clinical data from the Mayo Clinic indicates that liquid formulations reduce intragastric acidity by 1.8 pH units within two minutes, outperforming tablets, which take an average of 8–10 minutes. Furthermore, liquids are preferred in pediatric and elderly populations where swallowing difficulties exist. In emerging markets such as Nigeria and Indonesia, liquid antacids like Gaviscon Advance are gaining traction due to their dual-action floating barrier mechanism, which provides prolonged relief in high-prevalence GERD regions

REGIONAL ANALYSIS

North America was the top performer of the antacids market with 38.3% of share in 2024 with high health awareness, widespread OTC availability, and a strong culture of self-medication for digestive discomfort. According to the Centers for Disease Control and Prevention, over 60 million Americans experience heartburn monthly, with 15 million reporting daily symptoms, which is creating sustained demand for immediate relief products. The presence of leading brands such as Tums, Rolaids, and Prilosec OTC has entrenched antacids in daily wellness routines. Additionally, the integration of antacids into digital health platforms like CVS and Walgreens apps enables symptom-based product recommendations by enhancing accessibility and reinforcing consumer engagement in preventive digestive care.

Europe antacids market was ranked second by occupying 28.3% of the share in 2024 with Germany and the United Kingdom leading in both regulatory standardization and consumer adoption. The European market is shaped by stringent quality controls and a growing preference for combination therapies that address multiple gastrointestinal symptoms. As per the European Medicines Agency, sales of dual-action antacids containing alginates and bicarbonate rose by 11% in 2023, particularly in the UK, where Gaviscon remains a top-selling brand. Additionally, national health systems in Scandinavia and France promote patient education on lifestyle modifications alongside antacid use, fostering responsible self-care and reducing hospitalization rates for uncomplicated GERD.

The Asia-Pacific market and is witnessing accelerated growth due to rising urbanization and dietary changes. India stands out as a high-potential market, where fast food consumption in metropolitan areas has increased by 18% annually since 2020, as reported by the National Institute of Nutrition. This shift has led to a surge in acid-related disorders, with a 2023 study in The Indian Journal of Medical Research indicating that 47% of urban adults experience weekly heartburn. Local pharmaceutical companies like Cipla and Dr. Reddy’s have introduced affordable chewable and liquid antacids tailored to regional taste preferences, enhancing compliance. Moreover, government initiatives to expand rural pharmacy access have enabled broader distribution, positioning India as a key growth engine for both domestic and multinational antacid brands.

Latin America holds 7% of the market, with Brazil emerging as the primary consumer hub due to its large population and increasing healthcare access. The Brazilian population faces a rising burden of lifestyle-related digestive issues, with the Ministry of Health reporting a 24% increase in GERD diagnoses between 2019 and 2023. Urban dietary patterns, including high intake of coffee, spicy foods, and carbonated drinks, contribute significantly to gastric discomfort. Over-the-counter antacids are widely available in pharmacies and supermarkets, with brands like Milk of Magnesia and Neosaldina maintaining strong consumer trust. Additionally, the expansion of private health clinics in São Paulo and Rio de Janeiro has increased patient awareness of acid-related conditions, encouraging early self-treatment and driving demand for both single-ingredient and combination antacid products.

The Middle East and Africa collectively account for 4% of the global antacids market, with Saudi Arabia and South Africa as leading markets. In Saudi Arabia, rapid urbanization and high consumption of calorie-dense meals have contributed to a 31% prevalence of GERD, as documented by the King Saud University Medical Journal. The country’s Vision 2030 healthcare modernization plan includes public awareness campaigns on digestive health, promoting early intervention with OTC remedies. In South Africa, the Council for Scientific and Industrial Research reports that 39% of adults in urban centers experience regular heartburn, driven by stress and dietary habits. Pharmacies in Johannesburg and Cape Town have seen a 20% year-on-year increase in antacid sales, supported by the availability of low-cost generics. Additionally, Islamic dietary practices during Ramadan, which involve prolonged fasting followed by heavy meals, contribute to seasonal spikes in antacid demand across the region.

COMPETITIVE LANDSCAPE

The competition in the Antacids Market is shaped by brand equity, formulation innovation, and accessibility across both developed and emerging economies. While multinational corporations leverage global recognition and scientific backing, regional pharmaceutical companies counter with cost-effective generics and localized product designs. Differentiation is increasingly achieved through hybrid formulations that combine acid neutralization with gas relief or digestive support. The rise of e-pharmacy platforms has intensified competition by enabling direct consumer engagement and personalized recommendations. Regulatory scrutiny on long-term safety and ingredient transparency is forcing manufacturers to enhance labeling and invest in clinical validation. In the Asia-Pacific region, the battle for shelf space and digital visibility is accelerating mergers, digital campaigns, and physician collaborations, creating a dynamic landscape where trust, speed of relief, and patient-centric innovation determine market leadership.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global antacids market include

- GlaxoSmithKline PLC

- Abbott Laboratories

- Pfizer, Inc.

- Sun Pharmaceuticals

- Dabur

Top Players in the Antacids Market

Sanofi

Sanofi has established a strong presence in the Asia-Pacific antacids market through its flagship brand Gaviscon, which is widely recognized for its alginate-based dual-action mechanism in managing acid reflux. The company has tailored formulations to suit regional dietary habits, introducing sugar-free and flavored variants in India and Southeast Asia to improve patient compliance. In 2023, Sanofi launched a digital awareness campaign in Indonesia and Vietnam to educate consumers on nighttime heartburn, aligning with rising GERD prevalence in urban populations. It has also strengthened distribution partnerships with local pharmacy chains such as Guardian and Apollo, ensuring broad retail penetration. Furthermore, Sanofi collaborated with gastroenterology associations in Australia to support clinical guidelines on self-care for mild reflux, reinforcing brand credibility and scientific positioning in the digestive health segment.

Pfizer Consumer Healthcare (now Haleon)

Haleon, following its spin-off from Pfizer, has maintained a dominant role in the Asia-Pacific antacids landscape through the Tums brand, known for its calcium carbonate-based rapid relief profile. The company has focused on product innovation by introducing chewable tablets with natural fruit flavors, specifically designed for younger demographics in Japan and South Korea. In 2023, Haleon expanded its e-commerce footprint by partnering with JD Health in China and PharmEasy in India, enabling direct-to-consumer delivery and AI-driven symptom-based recommendations. Additionally, the company invested in sustainability by redesigning Tums packaging to be recyclable across key markets. Haleon also sponsored digestive wellness webinars in collaboration with the Singapore Medical Association, enhancing consumer trust and positioning Tums as a science-backed solution for everyday heartburn management.

Dr. Reddy’s Laboratories

Dr. Reddy’s Laboratories has emerged as a pivotal player in the Asia-Pacific antacids market by offering affordable, high-quality generic formulations across India, Bangladesh, and Sri Lanka. The company’s antacid portfolio includes chewable tablets, suspensions, and combination products integrating antacids with prokinetics like domperidone, addressing both acidity and delayed gastric emptying. In 2023, Dr. Reddy’s introduced a pediatric-friendly orange-flavored liquid antacid in South India, responding to rising cases of reflux in children linked to dietary changes. The company has also strengthened rural outreach through mobile pharmacy units and telehealth integrations, improving access in underserved areas. By aligning with government health initiatives and maintaining compliance with WHO-prequalified standards, Dr. Reddy’s has built a reputation for therapeutic reliability and cost-effective digestive care solutions.

Top Strategies Used by the Key Market Participants

Key players in the antacids market are deploying product differentiation, digital engagement, regional customization, strategic distribution expansion, and scientific validation to consolidate their market presence. Companies are reformulating products to include alginates, probiotics, and flavor enhancements to appeal to diverse consumer preferences. Investment in e-pharmacy partnerships and AI-driven symptom checkers is improving accessibility and personalization. Localization of dosage forms and packaging for cultural and dietary contexts is enhancing patient adherence. Collaborations with gastroenterology societies and clinical institutions are reinforcing credibility. Additionally, sustainability initiatives in packaging and manufacturing are aligning with evolving consumer values, while lifecycle management of OTC brands ensures continued relevance in a competitive, low-differentiation therapeutic category.

RECENT MARKET HAPPENINGS

- In February 2023, Sanofi launched a digital heartburn awareness campaign in Indonesia and Vietnam, utilizing social media and teleconsultation platforms to educate urban consumers on nighttime acid reflux and promote Gaviscon as a targeted solution.

- In June 2023, Haleon introduced fruit-flavored Tums chewable tablets in Japan and South Korea, specifically designed to appeal to younger consumers and improve adherence in lifestyle-driven heartburn cases.

- In September 2023, Dr. Reddy’s Laboratories launched a pediatric orange-flavored liquid antacid in South India, addressing rising cases of childhood reflux and expanding its presence in family digestive care.

- In November 2023, Sanofi partnered with Guardian Pharmacy across Southeast Asia to enhance retail visibility and in-store promotion of Gaviscon, strengthening its over-the-counter market penetration.

- In April 2024, Haleon integrated Tums into JD Health’s AI symptom checker in China, enabling personalized product recommendations and boosting online sales through targeted digital healthcare engagement.

MARKET SEGMENTATION

This market research report on the global antacids market has been segmented and sub-segmented based on the drug class, formulation type, distribution channel, disease indications, end-user, and region.

By Drug Class

- Proton Pump Inhibitors

- H2 Antagonist

- Pro-motility Agents

- Acid Neutralizers

By Formulation Type

- Tablet

- Liquid

- Powder

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Others

By Disease Indications

- Cancer

- Cardiovascular Disorders

- Neurological Disorders

- Immunological Disorders

- Other Diseases

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What is the Europe Antacids Market?

The Europe Antacids Market refers to the pharmaceutical segment focused on over-the-counter (OTC) and prescription medications that neutralize stomach acid to treat conditions such as heartburn, acid reflux, and indigestion.

What are the main drivers of the Europe Antacids Market?

The key drivers include changing dietary habits, stress-related digestive disorders, increased alcohol and caffeine consumption, and the growing prevalence of gastroesophageal reflux disease (GERD).

What are the major restraints in the Europe Antacids Market?

Restraints include potential side effects of long-term use, availability of alternative therapies, and increasing awareness about preventive healthcare.

What are the main types of antacids available in Europe?

The major types are calcium carbonate-based, magnesium-based, sodium bicarbonate-based, and aluminum hydroxide-based antacids.

What are the key applications of antacids?

Antacids are primarily used to treat heartburn, acid indigestion, sour stomach, and GERD-related discomfort

Which distribution channels are driving the antacids market in Europe?

Pharmacies, drug stores, supermarkets, and online retail platforms are the leading distribution channels in the region.

Which countries lead the Europe Antacids Market?

Germany, the United Kingdom, France, Italy, and Spain are the leading countries, with Germany holding the largest market share due to its strong pharmaceutical retail network.

What trends are shaping the Europe Antacids Market?

Trends include rising preference for OTC medications, increasing use of natural and herbal-based antacids, and growing e-commerce sales of digestive health products.

What are the key challenges in the Europe Antacids Market?

Challenges include over-reliance on antacids leading to side effects, competition from proton pump inhibitors (PPIs), and regulatory scrutiny over product formulations.

What is the future outlook for the Europe Antacids Market?

The market is expected to continue its upward trend with increasing consumer awareness of digestive health, expanding OTC product availability, and rising demand for fast-acting, natural-based antacids.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com