Global Artificial Intelligence (AI) In Transportation Market Size, Share, Trends, & Growth Forecast Report By Type (Machine Learning Technology, Process) Application (Autonomous Trucks, HMI Trucks, Semi-Autonomous Trucks) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Global Artificial Intelligence (AI) in Transportation Market Report Summary

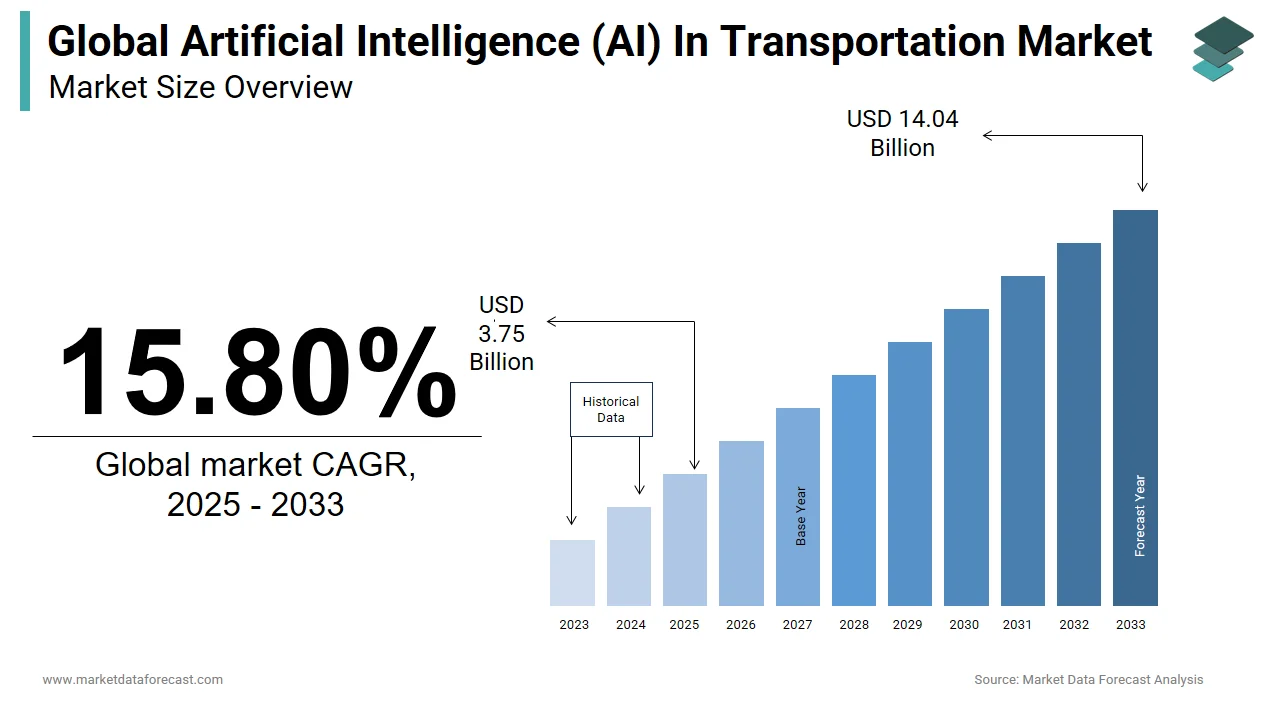

The global artificial intelligence (AI) in transportation market was valued at USD 4.34 billion in 2025 and is projected to grow from USD 5.03 billion in 2026 to USD 16.25 billion by 2034, registering a CAGR of 15.80% from 2026 to 2034. Market growth is driven by the increasing adoption of autonomous and connected vehicles, rising demand for intelligent traffic management systems, and growing investments in smart transportation infrastructure. AI technologies are transforming transportation by enhancing route optimization, predictive maintenance, fleet management, driver assistance systems, and autonomous mobility solutions. The expansion of smart cities, advancements in machine learning algorithms, and increasing focus on transportation safety and efficiency are further accelerating market growth worldwide.

Key Market Trends

- Rising adoption of autonomous and semi-autonomous vehicle technologies.

- Increasing deployment of AI-powered traffic management and mobility solutions.

- Growing use of predictive analytics for fleet management and maintenance.

- Expansion of smart city and intelligent transportation system (ITS) initiatives.

- Advancements in machine learning, computer vision, and real-time data processing technologies.

Segmental Insights

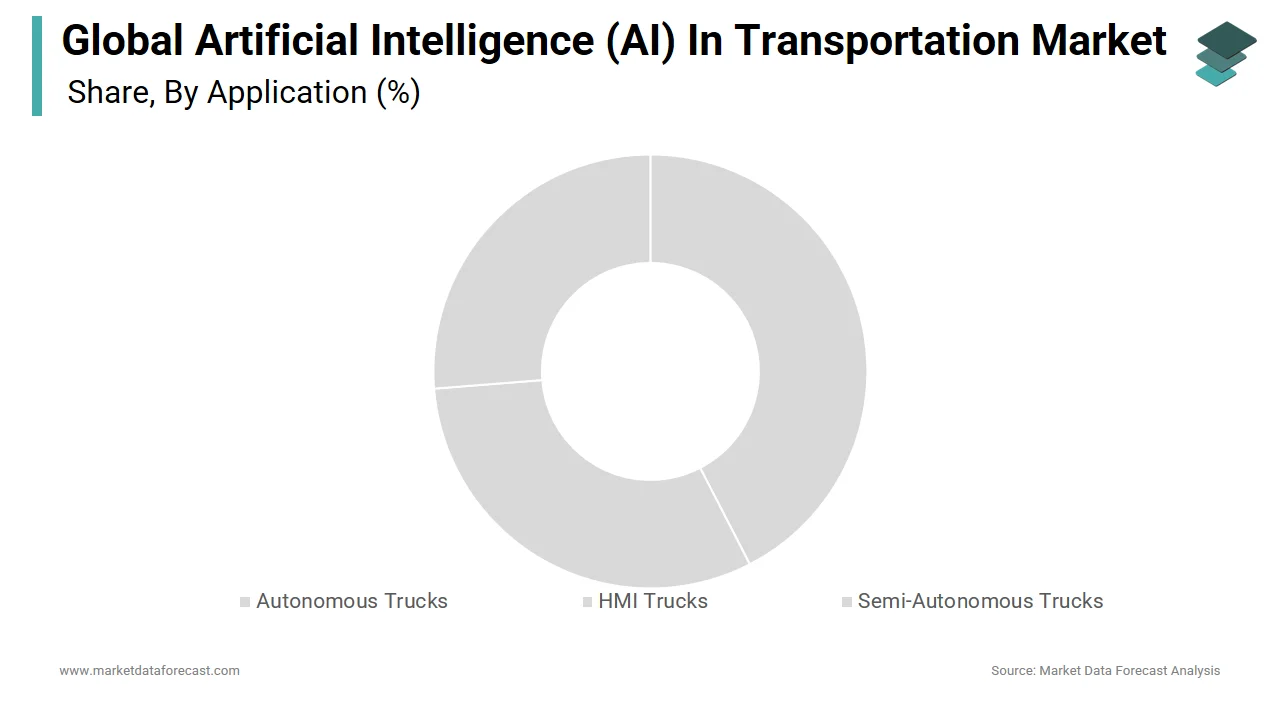

- Based on application, the semi-autonomous trucks segment dominated the global artificial intelligence in transportation market by accounting for 45.3% share in 2025, driven by increasing demand for enhanced driver assistance systems, improved logistics efficiency, and reduced operational costs.

- Based on type, the machine learning technology segment held the largest share of the market with 62.6% in 2025, supported by its extensive use in predictive analytics, route optimization, autonomous navigation, traffic forecasting, and intelligent decision-making applications.

Regional Insights

The global artificial intelligence in transportation market is witnessing rapid growth across major regions due to increasing investments in intelligent mobility solutions and transportation modernization.

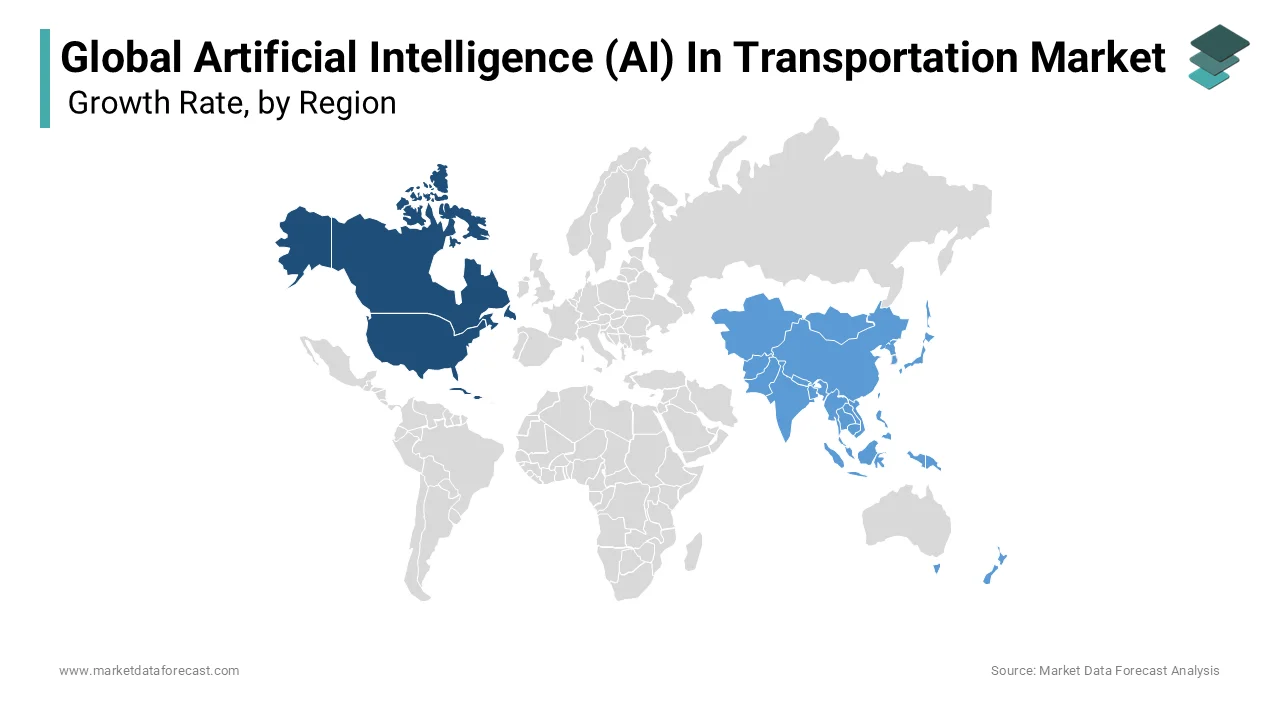

- North America dominated the global market in 2025 with 38.1% share, driven by strong technological innovation, widespread adoption of autonomous vehicle technologies, and significant investments in smart transportation infrastructure.

- Europe held the second-largest position with 28.4% share in 2025, supported by stringent transportation safety regulations, smart mobility initiatives, and growing investments in connected vehicle ecosystems.

- Asia-Pacific is projected to register the fastest growth during the forecast period, fueled by large-scale government investments in smart transportation projects, rapid urbanization, expanding logistics networks, and increasing adoption of AI-powered mobility solutions.

Competitive Landscape

The global artificial intelligence in transportation market is characterized by the presence of leading automotive manufacturers, semiconductor companies, and technology providers focusing on autonomous mobility, intelligent transportation systems, and advanced driver assistance technologies. Market participants are investing heavily in AI research, machine learning platforms, vehicle automation, and strategic partnerships to strengthen their competitive position. Continuous innovation in autonomous driving technologies, fleet intelligence, and transportation analytics is shaping the competitive landscape.

Prominent companies operating in the global artificial intelligence (AI) in transportation market include Daimler AG, MAN SE, PACCAR Inc., Qualcomm, NVIDIA, Scania Group, ZF Friedrichshafen AG, Intel Corporation, and Valeo SA.

Global Artificial Intelligence (AI) in Transportation Market Size

The global artificial intelligence (AI) in transportation market was worth USD 4.34 billion in 2025. The global market is expected to reach USD 16.25 billion by 2034 from USD 5.03 billion in 2026, growing at a CAGR of 15.80% from 2026 to 2034.

Artificial Intelligence (AI) in transportation refers to using technologies like machine learning, computer vision, and predictive analytics to make the movement of people and goods safer, faster, and more efficient. It transforms traditional, rigid transport systems into smart networks that can perceive their surroundings, predict disruptions, and make autonomous decisions. This technological paradigm transforms traditional transit infrastructure into intelligent, responsive ecosystems capable of optimizing traffic flow and enhancing passenger safety. According to the World Health Organization, road traffic crashes claim approximately 1.19 million lives each year globally, ranking as the leading cause of death for children and young adults aged 5–29. Furthermore, the World Economic Forum (WEF) and global transit data engines indicate that severe traffic congestion costs the global economy more than $500 billion every year in wasted time, gridlock inefficiencies, and excess fuel consumption. Also, the International Energy Agency (IEA) establishes that the transport sector is a dominant driver of climate impact, accounting for approximately 25% of global energy-related carbon dioxide emissions, with road vehicles comprising the vast majority of that footprint. The integration of deep learning models into public transit networks allows for dynamic scheduling and predictive maintenance, ensuring higher operational reliability. Additionally, the International Road Transport Union (IRU) and regional transport networks show that "empty running" (vehicles driving with zero paying cargo) averages over 20% across regional road freight corridors, introducing severe structural waste and unnecessary overhead into the global logistics market. This foundational shift toward cognitive mobility is absolutely indispensable for modernizing global supply chains and creating sustainable, efficient urban environments.

MARKET DRIVERS

Escalating Imperative for Road Safety and Accident Reduction.

The absolute necessity to mitigate human error and reduce catastrophic road accidents is a key factor driving the growth of artificial intelligence (AI) in the transportation market. This accelerates the integration of cognitive algorithms into vehicular systems. A historic NHTSA field survey indicated that the final critical action in 94% of evaluated crashes was linked to the driver. Nevertheless, federal safety officials emphasize that systemic improvements—combining advanced vehicle safety features with safer road infrastructure—are required to reduce traffic accidents. Artificial intelligence-powered features like automatic emergency braking, lane keeping assist, and driver fatigue monitoring continuously analyze the driving environment to prevent collisions before they occur. In addition, the World Health Organization states that road traffic injuries are the leading cause of death for children and young adults aged 5 to 29 years, prompting governments worldwide to mandate the inclusion of active safety technologies in new vehicle registrations. Research from the European Transport Safety Council (ETSC) indicates that mass adoption of Intelligent Speed Assistance (ISA) software can reduce overall traffic collisions by up to 30% and cut road deaths by 20% across Europe. This profound societal and regulatory demand for zero fatality transit networks forces automotive manufacturers to embed sophisticated neural networks and sensor fusion technologies into their platforms, thereby driving massive and sustained procurement of artificial intelligence solutions across the global transportation sector.

Surging Demand for Supply Chain Optimization and Freight Efficiency.

The exponential growth of global electronic commerce and the corresponding need for rapid, cost-effective logistics fulfillment further boost the expansion of artificial intelligence (AI) in the transportation market. This serves as a critical demand driver propelling the adoption of machine learning in freight operations. Modern supply chains require dynamic route optimization and predictive fleet maintenance to minimize downtime and reduce fuel expenditure. Multiple studies show that advanced economies typically keep logistics overhead below 8% of GDP, whereas structural bottlenecks cause logistics costs in developing regions to hover between 11 percent and 15 percent of GDP. Furthermore, research indicates that heavy-duty commercial trucks travel without cargo for roughly 20 percent of their total mileage, presenting a substantial economic inefficiency that fleet operations attempt to mitigate through integrated freight network coordination. The American Transportation Research Institute (ATRI) outlines that fleet repair and maintenance represent one of the fastest-growing operational costs per mile, pushing carriers to explore preventative vehicle management solutions. This relentless commercial pressure to maximize cargo throughput while minimizing transit times and carbon footprints guarantees a robust and continuous demand for intelligent transportation management systems across the global logistics and freight forwarding industry.

MARKET RESTRAINTS

Prohibitive Implementation Costs and Complex Infrastructure Requirements.

The massive capital expenditure required for deploying advanced sensor arrays, edge computing hardware, and vehicle-to-infrastructure communication networks hampers the growth of artificial intelligence (AI) in the transportation market. This severely restricts the rapid commercialization of intelligent transit systems. Equipping urban environments with the necessary smart traffic lights, high-definition cameras, and low-latency communication towers demands unprecedented financial investment from municipal governments. The International Transport Forum (ITF) emphasizes that preparing legacy physical road infrastructure for automated vehicles introduces high fiscal uncertainty, requiring municipal planners to focus on vehicle-to-city communication standards. Apart from this, global capital expenditure forums recognize that scaling nationwide vehicle connectivity requires massive physical-to-digital infrastructure investments, necessitating coordinated public-private financing frameworks. Enterprise IT cost analysis confirms that software maintenance, cloud processing pipelines, and data storage account for significant ongoing operational expenditure (OpEx) margins after initial hardware deployments. For small and medium-sized logistics operators, the inability to justify these exorbitant upfront technology costs forces them to delay the integration of artificial intelligence, thereby acting as a significant restraint on the overall market expansion and limiting the technology primarily to well-capitalized enterprise fleets and wealthy urban centers.

Severe Data Privacy Concerns and Regulatory Fragmentation.

The extensive collection of sensitive location data, biometric passenger information, and continuous vehicular telemetry raises profound privacy concerns, which impede the expansion of artificial intelligence (AI) in the transportation market. These issues significantly hinder the seamless deployment of artificial intelligence in public and commercial transit. Intelligent transportation systems rely on massive datasets to train predictive models, but this constant surveillance creates severe vulnerabilities regarding user anonymity and data security. Enforced under frameworks coordinated by the European Data Protection Board (EDPB), cross-border privacy mandates impose heavy penalties for generalized data misuse, forcing mobility firms to implement rigorous data anonymization protocols for vehicle telemetry. Furthermore, the United Nations Conference on Trade and Development (UNCTAD) notes that fragmented digital governance and mismatched electronic commerce regulations present operational hurdles for international data-dependent supply chains. Global consumer privacy index indicators compiled via privacy regulatory groups highlight that user trust remains a significant barrier for location-based services, with a large majority of consumers demanding clear data opt-out mechanisms for geolocation tracking. This pervasive consumer skepticism and the labyrinth of conflicting regional privacy laws force developers to invest heavily in anonymization protocols and legal compliance, thereby slowing down the rapid scaling of intelligent mobility solutions.

MARKET OPPORTUNITIES

Proliferation of Smart City Initiatives and Urban Mobility Hubs.

Aggressive global initiatives to build intelligent cities and mobility hubs have created massive commercial opportunities for artificial intelligence (AI) in the transportation market. Consequently, there is a strong demand to deploy cognitive traffic management and public transit optimization algorithms. As urban populations swell, municipal governments are heavily investing in digital infrastructure to alleviate congestion and reduce local pollution levels. According to the United Nations Department of Economic and Social Affairs, the global urban population is projected to reach 6 billion by the year 2045, necessitating the immediate modernization of metropolitan transit networks to handle unprecedented passenger volumes. Moreover, research indicates that smart city technology spending is scaling significantly, with municipal authorities prioritizing capital expenditures on intelligent transit frameworks and synchronized vehicle management technologies. The C40 Cities Network emphasizes that optimizing public mass transit routes and prioritizing zero-emission vehicle lanes are critical tactics for lowering localized municipal greenhouse gases and curbing gridlock. Technology providers can secure long-term, high-value municipal contracts by building the foundational software architecture for futuristic urban ecosystems. This strategy establishes a highly lucrative and sustainable revenue stream across the global transportation sector.

Emergence of Mobility as a Service and Autonomous Fleets.

The rapid transition from private vehicle ownership to shared, on-demand mobility platforms creates an unprecedented opportunity for artificial intelligence (AI) in the transportation market. This helps AI to orchestrate complex, multimodal transportation networks. Mobility as a Service applications rely entirely on sophisticated machine learning models to predict passenger demand, dynamically price rides, and optimize the routing of shared autonomous fleets in real time. The International Transport Forum (ITF) demonstrates that in a theoretical urban ecosystem where all private transport is replaced by shared autonomous mobility on demand, the total number of vehicles on city streets could drop significantly. In addition, studies suggest that autonomous passenger fleets and digital on-demand transit services will unlock substantial revenue streams as commercial ride-hailing networks transition to driverless technologies. This paradigm shift toward software-defined mobility ecosystems allows technology companies to monetize continuous data streams and operational management services, unlocking vast new financial frontiers in the transportation industry.

MARKET CHALLENGES

Extreme Environmental Variability and Sensor Degradation.

The absolute reliance of autonomous systems on optical and radar sensors is a formidable technical barrier to artificial intelligence (AI) in the transportation market. This is because severe weather conditions drastically degrade their operational reliability. Heavy rain, dense fog, snow accumulation, and blinding glare can obscure camera lenses and scatter light detection and ranging signals, rendering the artificial intelligence algorithms blind to critical obstacles. The U.S. Federal Highway Administration (FHWA) confirms that approximately 21% of all vehicle crashes are weather-related, driven primarily by rain, snow, and wet pavement conditions. Furthermore, research confirms that heavy rain, thick fog, and airborne particles scatter laser beams, reducing the operational range and depth-perception accuracy of light detection and ranging (LiDAR) units during adverse atmospheric conditions. This persistent vulnerability to environmental interference severely limits the all-weather operational capability of intelligent vehicles, creating a massive engineering hurdle that delays the widespread commercial deployment of fully autonomous transportation networks.

Acute Shortage of Specialized Artificial Intelligence Talent.

There is a severe deficit of highly skilled engineers who can design, train, and deploy complex machine learning models for vehicular applications, which challenges the expansion of artificial intelligence (AI) in the transportation market. As a result, this talent shortage acts as a critical barrier that slows down innovation in the sector. Developing safe and reliable autonomous systems requires niche expertise in computer vision, edge computing, and robotic sensor fusion, disciplines where qualified professionals are exceptionally rare. The definitive Global Talent Crunch assessment published by Korn Ferry estimates that if left unaddressed, a skilled talent deficit of more than 85 million workers could occur by 2030, causing trillions of dollars in unrealized revenue across global economies. Intense global demand for software engineers specializing in deep learning networks has driven significant salary inflation across tech markets, escalating the operational expenses of autonomous vehicle development programs. This profound human resource constraint forces companies to delay critical project milestones, outsource essential development work to third-party agencies, and struggle to maintain the rigorous testing standards required for regulatory approval, thereby stifling the rapid advancement of intelligent mobility solutions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Application, Type, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Daimler AG, MAN SEPACCAR Inc., Qualcomm, NVIDIA, Scania Group, ZF Friedrichshafen AG, Intel Corporation, and Valeo SA. |

SEGMENTAL ANALYSIS

By Application Insights

The semi-autonomous trucks segment dominated the global artificial intelligence (AI) in transportation market and accounted for a 45.3% share in 2025. This dominance of the segment was driven by stringent government regulations mandating the integration of advanced driver assistance systems. Regulatory bodies worldwide are aggressively implementing safety protocols to minimize catastrophic road accidents and protect vulnerable pedestrians. Joint regulatory rules finalized by NHTSA and the FMCSA mandate that all new heavy commercial vehicles must be equipped with Automatic Emergency Braking (AEB) systems to dramatically minimize rear-end commercial crashes. Furthermore, the European Commission enforces rigorous General Safety Regulations that require all newly registered heavy-duty vehicles to be equipped with intelligent speed assistance and advanced distraction warning systems. This profound regulatory pressure forces commercial fleet operators to upgrade their existing vehicle inventories with semi-autonomous capabilities to ensure strict legal compliance. Consequently, the uncompromising legal requirements for enhanced vehicular safety guarantee the continuous and overwhelming market leadership of semi-autonomous trucks across the international transportation sector.

Also, a key reason supporting the top spot for this segment is the relentless commercial demand for enhanced fuel efficiency and optimized fleet management. Modern logistics companies operate on extremely thin profit margins, reducing operational expenditures to an absolute strategic priority. Semi-autonomous systems utilize predictive cruise control and dynamic route optimization algorithms to maintain optimal driving speeds and minimize unnecessary braking or acceleration. The American Transportation Research Institute (ATRI) highlights that fuel remains one of the highest marginal costs for carriers, making tech-driven optimizations like adaptive cruise control and aerodynamic fuel-saving measures a high priority. Assessments outline that integrating intelligent dispatch platforms and driver-assist safety suites can enhance fleet asset deployment and minimize unscheduled vehicle downtime. This compelling combination of massive cost reductions and operational efficiency ensures that semi-autonomous trucks remain the undisputed leaders in the global market.

The autonomous trucks segment is expected to exhibit a noteworthy CAGR of 22.4% from 2026 to 2034 due to the severe and escalating global shortage of commercial truck drivers. The logistics and freight industry is currently facing an unprecedented demographic crisis as veteran drivers retire and younger generations show declining interest in pursuing long haul driving careers. According to the American Trucking Associations, the United States alone faces a deficit of over 80000 commercial drivers, a number projected to exceed 160000 by the end of the decade. This massive labor shortfall severely disrupts supply chains and delays critical freight deliveries across continental networks. Autonomous trucks offer a definitive technological solution to this crisis by enabling continuous, round-the-clock operations without the legal rest periods mandated for human drivers. Furthermore, studies indicate that the deployment of autonomous hub-to-hub trucking operations can increase daily asset runtime by removing human hours-of-service (HOS) restrictions, significantly extending the operating window of long-haul vehicles. This absolute necessity to maintain uninterrupted supply chain velocity and overcome insurmountable labor deficits propels the autonomous trucks segment to the forefront of rapid market expansion.

The rapid proliferation of advanced sensor fusion technologies and exponential improvements in edge computing capabilities further drive the explosive growth of this segment. Modern autonomous vehicles rely on a complex array of light detection and ranging sensors, high definition cameras, and radar systems to perceive their surrounding environment with absolute precision. The IEEE outlines that transitioning toward high-level driving automation requires an exponential increase in compute performance to handle high-bandwidth multimodal sensor data streaming. In addition, research emphasizes that autonomous vehicle safety architectures require localized edge computing infrastructure to process obstacle perception and safety-critical brake commands with near-zero latency, avoiding reliance on remote cloud networks. These monumental technological breakthroughs eliminate previous performance bottlenecks, driving rapid commercial adoption.

By Type Insights

The machine learning technology segment led the global market and captured a 62.6% share in 2025. This leading position of the segment was attributed to the massive proliferation of predictive maintenance applications across global transit networks. Transportation operators are increasingly deploying machine learning algorithms to analyze continuous streams of telematics data from vehicle engines, braking systems, and tire pressure sensors to predict component failures before they occur. The International Association of Public Transport (UITP) emphasizes transitioning toward condition-based predictive maintenance to monitor real-time equipment status and optimize urban rail transit reliability. Moreover, the Federal Railroad Administration (FRA) promotes the deployment of automated track geometry inspection vehicles and wayside rolling stock sensors to identify infrastructure flaws before they lead to structural failures. This profound ability to maximize asset uptime and drastically reduce maintenance expenditures ensures that machine learning technology remains the undisputed foundation of the global market.

A different factor securing the dominance of machine learning technology is its seamless integration with natural language processing systems to create highly intuitive in-cabin voice assistants for drivers and passengers. Modern transportation environments require operators to maintain constant visual attention on the road, making hands-free interaction with vehicle infotainment and navigation systems an absolute safety necessity. Research indicates that outfitting flight compartments with voice-activated technology requires specialized acoustic noise-canceling hardware and narrow-band filtering to differentiate pilot vocals from ambient turbine frequencies. This critical enhancement in user experience and operational safety guarantees the continuous and overwhelming market leadership of machine learning technology across all transportation domains.

The deep learning segment is predicted to witness the highest CAGR of 28.7% during the forecast period, owing to the exponential growth in massive training datasets required for advanced computer vision and object detection applications. Autonomous vehicles and advanced driver assistance systems rely entirely on deep learning neural networks to accurately identify pedestrians, other vehicles, traffic signs, and unexpected road obstacles in highly complex environments. Global connected vehicle ecosystems and automotive embedded telematics data pipelines are projected to generate upwards of 500 petabytes of time-series data annually as fleets scale up camera and radar telemetry inputs. Furthermore, IEEE libraries documents that applying convolutional neural networks (CNNs) to thermal and infrared imagery significantly enhances obstacle and pedestrian classification compared to legacy edge-detection computer vision. As per sources, continuous advancements in deep learning architectures allow vehicles to predict the future trajectories of moving objects with millisecond precision. This relentless improvement in visual perception capabilities drives the rapid expansion of the deep learning segment.

The rapid development of sophisticated neural networks capable of executing complex decision-making in highly unpredictable and dynamic environments further accelerates the explosive growth of the deep learning segment. Unlike traditional rule-based programming, deep learning models can autonomously navigate ambiguous traffic scenarios, interpret the subtle gestures of human pedestrians, and adapt to sudden changes in weather conditions without explicit human intervention. Urban traffic engineering field studies demonstrate that upgrading legacy timed traffic signals to adaptive, data-informed signal control platforms can significantly reduce intersection idling delays and peak-hour vehicle congestion. This unparalleled ability to master complex cognitive tasks ensures the rapid expansion of deep learning.

REGIONAL ANALYSIS

North America Artificial Intelligence (AI) In Transportation Market Analysis

North America was the top performer in the global artificial intelligence (AI) in transportation market and occupied a 38.1% share in 2025. This supremacy of the North American market was mainly propelled by the aggressive deployment of artificial intelligence solutions by major technology conglomerates and established automotive manufacturers seeking to dominate the future of mobility. The region functions as the primary hub for technological innovation, autonomous vehicle testing, and massive venture capital investments. The federal National Highway Traffic Safety Administration outlines generalized regulatory guidelines for automated driving safety. Building on this, individual state departments of transportation, such as in Texas, have established physical smart freight corridors along major highways to enable industry-led autonomous vehicle testing and validation. Furthermore, sources reveal that North American logistics corporations are scaling up capital allocations toward intelligent freight management platforms, focusing heavily on cross-border customs clearances and IoT fleet asset tracking. The presence of world-class semiconductor designers and artificial intelligence research institutions ensures a continuous pipeline of cutting-edge computational hardware. This robust ecosystem of innovation, substantial financial backing, and progressive regulatory frameworks cements North America as the undisputed leader in the global artificial intelligence in transportation market.

Europe Artificial Intelligence (AI) In Transportation Market Analysis

Europe was the next prominent region in the artificial intelligence (AI) in transportation market and held a 28.4% share in 2025 because of its world-renowned automotive manufacturing heritage and stringent environmental mandates. The core driving force behind this market strength is the aggressive implementation of the European Green Deal, which mandates significant reductions in transportation-related carbon emissions, compelling fleet operators to adopt artificial intelligence for route optimization and fuel efficiency. Europe functions as a highly progressive and strictly regulated territory within the global ecosystem, guiding the development of safe, sustainable, and highly integrated intelligent transit networks. The European Commission supports the widespread roll-out of Cooperative Intelligent Transport Systems (C-ITS) to cut transit delays and greenhouse gases across the Single European Transport Area. In addition, state-level train operators across Europe are modernizing infrastructure, utilizing advanced digital signaling and centralized traffic management algorithms to optimize cross-border track capacity within the European Union Agency for Railways (ERA) unified safety framework. The region features highly robust digital infrastructure and clear legal guidelines regarding data privacy, which allows mobility providers to deploy connected vehicle technologies with high consumer trust. This profound commitment to sustainable mobility and technological excellence ensures Europe remains a critical and highly influential territory.

Asia Pacific Artificial Intelligence (AI) In Transportation Market Analysis

The Asia Pacific regional market is expanding at the highest rate globally. This quick surge is primarily fueled by unprecedented government investments in urban infrastructure and the urgent need to manage the mobility requirements of massive, densely populated metropolitan areas. It functions as the main driver of rapid smart city adoption and massive public transit modernization. The Asian Development Bank (ADB) actively finances municipal upgrades toward sustainable, low-carbon public transit systems across Asia, with urban development projects emphasizing smart traffic management and electrified mass transport networks. Moreover, the World Bank Group stresses that the massive boom of e-commerce across developing Asian nations has exacerbated urban logistics friction, forcing private freight providers to invest heavily in smart dispatch and routing optimization systems. The region benefits from a massive domestic consumer base that is highly receptive to digital mobility applications and shared transportation services. This immense scale of urbanization and aggressive government backing guarantees that the Asia Pacific will dominate global market growth trajectories.

Latin America Artificial Intelligence (AI) In Transportation Market Analysis

Latin America is also an emerging region in the global market. The region's success depends heavily on modernizing commercial freight logistics and optimizing public bus networks. This growth is driven primarily by the urgent need to improve supply chain efficiency and reduce the high operational costs associated with aging transportation infrastructure. The dominant factor for technology adoption in this region is the massive expansion of agricultural and mining exports, which requires highly sophisticated fleet management systems to navigate vast and often challenging geographical terrains. Also, the Inter-American Development Bank (IDB) indicates that systemic inefficiencies drive logistics costs to between 18% and 35% of the total value of goods in Latin America, leaving a wide margin for tech-driven route and freight optimizations Furthermore, Project assessments from the World Resources Institute (WRI) spotlight how cities like Bogota and Santiago prioritize the physical expansion of Bus Rapid Transit (BRT) corridors and dedicated transit lanes to combat severe urban congestion and guarantee public transit reliability. This critical focus on operational efficiency and urban mobility improvement ensures steady growth for the market.

Middle East and Africa Artificial Intelligence (AI) In Transportation Market Analysis

The Middle East and Africa region is predicted to expand notably in the artificial intelligence (AI) in transportation market from 2026 to 2034. It focuses heavily on leveraging artificial intelligence to build futuristic smart cities and modernize legacy transit infrastructure. The regional market status is characterized by massive sovereign wealth investments in advanced mobility technologies, particularly within the Gulf Cooperation Council nations. The primary driver of adoption is the aggressive execution of national economic diversification strategies that prioritize the development of autonomous logistics and intelligent public transportation networks. Enforced directly by the Dubai Roads and Transport Authority (RTA), the Dubai Autonomous Transportation Strategy formally targets transforming 25% of all individual transport journeys into autonomous trips by the year 2030. Apart from this, strategic infrastructure funding from the African Development Bank (AfDB) focuses heavily on upgrading physical transnational transport corridors, cross-border rail links, and port connections to lower logistics costs and improve long-haul trade safety. This dual focus on building world-class smart city infrastructure in the Middle East and optimizing critical freight logistics in Africa ensures steady and targeted growth for the regional market.

COMPETITIVE LANDSCAPE

The competitive landscape of the market is characterized by intense technological rivalry among multinational automotive conglomerates, specialized semiconductor manufacturers, and agile software startups. These organizations continuously strive to outpace their rivals by integrating advanced neural networks, sensor fusion algorithms, and high-performance edge computing into their core mobility platforms. The industry exhibits a highly consolidated structure at the hardware tier, where a few dominant corporations control the majority of global revenue through extensive computational portfolios and robust manufacturing networks. However, the software development segment remains highly dynamic, featuring numerous innovative enterprises that introduce disruptive machine learning models and novel navigation techniques. To maintain their competitive edge, industry leaders heavily prioritize continuous scientific research, ensuring their platforms meet the evolving demands of autonomous safety and operational efficiency. Strategic joint ventures also play a pivotal role, allowing established players to rapidly access specialized artificial intelligence expertise and secure favorable regulatory approvals. Furthermore, companies are increasingly focusing on developing customized software solutions that cater specifically to the unique logistical requirements of commercial freight operators. This relentless pursuit of technological innovation ensures that the competitive environment remains highly dynamic, forcing all participants to continuously upgrade their computational capabilities to secure long term contracts globally.

KEY MARKET PLAYERS

The major companies operating in the global artificial intelligence (AI) in transportation market include

- Daimler AG

- MAN SE

- PACCAR Inc.

- Qualcomm

- NVIDIA

- Scania Group

- ZF Friedrichshafen AG

- Intel Corporation

- Valeo SA

TOP PLAYERS IN THE MARKET

- NVIDIA operates as a vital contributor to the global transportation landscape by providing cutting-edge computational hardware and comprehensive software platforms for autonomous vehicle development. The company focuses heavily on leveraging its advanced graphics processing units to accelerate the training of complex deep learning models required for self-driving cars. To strengthen its position, the enterprise recently introduced its next-generation automotive system on a chip, which delivers unprecedented processing power for real-time sensor fusion. This strategic hardware advancement enables automotive manufacturers to achieve higher levels of vehicle autonomy while significantly reducing the physical footprint and power consumption of onboard computing systems.

- Intel contributes extensively to the market through the engineering of specialized microprocessors and advanced mapping technologies designed to support safe autonomous navigation. The company focuses on bridging the gap between vehicle sensors and cloud-based infrastructure to optimize fleet management and traffic coordination. To expand its footprint, the organization recently launched a highly advanced visual perception system that utilizes artificial intelligence to create precise, lane-level three-dimensional maps in real time. This architectural enhancement allows autonomous vehicles to navigate complex urban environments with absolute confidence, significantly improving passenger safety and enabling the widespread deployment of robotic taxi services across diverse global markets.

- Qualcomm significantly impacts the market by merging its dominant mobile communication expertise with highly specialized automotive digital chassis architectures. The company works to transform modern vehicles into fully connected, software-defined mobility platforms capable of continuous over-the-air updates. The enterprise has recently expanded its technological ecosystem by integrating advanced artificial intelligence accelerators directly into its vehicle connectivity modules. These sophisticated pipelines assist automotive developers in creating highly responsive digital cockpit experiences and robust vehicle-to-everything communication networks. This deep integration of connectivity and computational power makes the firm a central coordinator for the future of intelligent and autonomous transportation ecosystems.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key participants in the market primarily focus on strategic collaborations and extensive research partnerships to accelerate the development of safe and reliable autonomous systems. By partnering with specialized semiconductor manufacturers, these corporations integrate advanced computational hardware directly into their core vehicular platforms. Furthermore, industry leaders heavily invest in acquiring innovative artificial intelligence startups to rapidly expand their proprietary software capabilities and secure critical intellectual property. Collaborative testing agreements with municipal governments also form a crucial strategy, enabling companies to validate their technologies in complex real-world urban environments. Finally, organizations are increasingly prioritizing the development of open source software architectures to encourage widespread industry adoption and establish universal standards for intelligent mobility.

MARKET SEGMENTATION

This research report on the global AI in transportation market has been segmented and sub-segmented based on the application, type, and region.

By Application

- Autonomous Trucks

- HMI Trucks

- Semi-Autonomous Trucks

By Type

- Machine Learning Technology

- Computer Vision

- Context Awareness

- Deep Learning

- Natural Language Processing

- Process

- Data Mining

- Image Recognition

- Signal Recognition

By Region

- North America

- The United States

- Canada

- Rest of North America

- Europe

- The United Kingdom

- Spain

- Germany

- Italy

- France

- Rest of Europe

- The Asia Pacific

- India

- Japan

- China

- Australia

- Singapore

- Malaysia

- South Korea

- New Zealand

- Southeast Asia

- Latin America

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- The Middle East and Africa

- Saudi Arabia

- UAE

- Lebanon

- Jordan

- Cyprus

Frequently Asked Questions

What is the global artificial intelligence in transportation market?

The global artificial intelligence in transportation market involves AI application in autonomous vehicles traffic management and logistics to improve safety reduce accidents congestion and minimize carbon emissions.

Why is the global artificial intelligence in transportation market growing?

The global artificial intelligence in transportation market is growing due to increasing adoption of autonomous vehicles by automakers and technology companies plus demand for safer roads and improved logistical efficiency.

What are the key drivers of the global artificial intelligence in transportation market?

The global artificial intelligence in transportation market is driven by autonomous vehicle adoption predictive analytics for logistics smart traffic systems reducing urban congestion and improving passenger safety standards worldwide.

What technologies are used in the global artificial intelligence in transportation market?

The global artificial intelligence in transportation market uses machine learning computer vision and data analytics to predict traffic patterns reduce fuel consumption and enhance overall transportation system efficiency globally.

How does autonomous vehicles impact the global artificial intelligence in transportation market?

The global artificial intelligence in transportation market sees major trend in increasing autonomous vehicle adoption by automakers and technology companies making safer roads a key opportunity for market growth.

What are the benefits of the global artificial intelligence in transportation market?

The global artificial intelligence in transportation market provides benefits including reduced waiting time parking management road condition monitoring safety improvement and fewer road accidents in cities and smart cities.

How does the global artificial intelligence in transportation market reduce congestion?

The global artificial intelligence in transportation market collects traffic patterns minimizes road congestion and enhances public transportation schedules through AI-driven traffic management and smart systems deployment.

What opportunities exist in the global artificial intelligence in transportation market?

The global artificial intelligence in transportation market includes key opportunities in advancing autonomous vehicle technologies for safer roads improving logistical efficiency via predictive analytics and deploying smart traffic systems.

Why is predictive analytics important for the global artificial intelligence in transportation market?

The global artificial intelligence in transportation market uses predictive analytics to improve logistical efficiency optimize routes and reduce fuel consumption making it crucial for transportation operations worldwide.

How does the global artificial intelligence in transportation market improve safety?

The global artificial intelligence in transportation market improves passenger safety reducing accidents and traffic congestion while ensuring compliance with law and order in cities towns and smart cities globally.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com