Asia Pacific Automotive Coatings Market Size, Share, Trends & Growth Forecast Report By Resin Type (Polyurethane, Epoxy, Acrylic), By Vehicle Type (Passenger Cars, Commercial Vehicles), By Technology Type (Solvent-based, Water-based, Powder-based), By Coat Type (Clearcoat, Basecoat), and Country (India, China, Japan, South Korea, Australia, Rest of APAC) – Industry Analysis From 2026 to 2034.

Market Size, 2025

$3.97 BnMarket Estimate, 2026

$4.16 BnMarket Forecast, 2034

$6.08 BnCAGR, 2026–2034

4.85%Asia Pacific Automotive Coatings Market Size

The size of the Asia Pacific automotive coatings market was worth USD 3.97 billion in 2025. The Asia Pacific market is anticipated to grow at a CAGR of 4.85% from 2026 to 2034 and be worth USD 6.08 billion by 2034, up from USD 4.16 billion in 2026.

The Asia Pacific automotive coatings market encompasses a wide range of protective and decorative finishes applied to vehicles during manufacturing and refinish processes. These coatings include primers, basecoats, clearcoats, and functional coatings designed to enhance durability, aesthetics, and resistance to environmental factors such as UV radiation, corrosion, and abrasion.

With the region being a global hub for automotive production, countries like China, India, Japan, and South Korea are witnessing strong demand for high-performance coatings that align with evolving consumer preferences and regulatory requirements. According to the International Energy Agency, vehicle ownership rates in Southeast Asia have risen steadily, boosting both OEM and refinish coating applications.

Environmental concerns are also shaping the industry’s trajectory, with governments implementing stricter VOC (volatile organic compound) emission norms. As per the Ministry of Ecology and Environment of China, new guidelines introduced in 2023 require automotive manufacturers to adopt low-VOC and water-based coating technologies, prompting suppliers to innovate while maintaining performance standards.

In addition, the rise of electric vehicles has spurred demand for specialized coatings that protect battery enclosures and improve thermal management efficiency. The Japan Automobile Research Institute notes that advanced surface treatments are now integral to EV design strategies, reinforcing the strategic importance of automotive coatings in the Asia Pacific region.

MARKET DRIVERS

Rising Vehicle Production and Sales Across Asia Pacific

One of the primary drivers of the Asia Pacific automotive coatings market is the substantial growth in vehicle production and sales, particularly in emerging economies such as India, Indonesia, and Vietnam. According to the International Organization of Motor Vehicle Manufacturers (OICA), Asia Pacific accounted for a significant share of global automotive production in 2023, with China alone producing more than 28 million vehicles that year. This surge in automotive output directly translates into higher demand for OEM coatings, as every vehicle requires multi-layer paint systems including primer, basecoat, and clearcoat to ensure protection and aesthetic appeal. In India, the Society of Indian Automobile Manufacturers (SIAM) reported that domestic passenger car sales exceeded 3.1 million units in FY2023, reflecting sustained consumer demand for well-finished, durable vehicles. Moreover, governments in several ASEAN countries have introduced policies promoting local manufacturing and investment in automotive infrastructure. For example, Thailand’s Board of Investment recorded an influx of USD 2.5 billion in new automotive sector investments in 2023, supporting both traditional and electric vehicle assembly plants.

Growing Demand for High-Performance and Eco-Friendly Coating Solutions

The increasing adoption of high-performance and eco-friendly coatings is another significant driver influencing the Asia Pacific automotive coatings market. With growing awareness of environmental sustainability and tightening regulations on volatile organic compound (VOC) emissions, automakers and coating suppliers are transitioning toward waterborne, powder, and ultra-low VOC coating technologies.

According to the Ministry of Environment of Japan, new air quality regulations implemented in 2023 mandate a reduction in industrial solvent emissions, compelling automotive manufacturers to adopt greener alternatives.

In response, major coating companies such as PPG Industries, BASF, and Kansai Nerolac have expanded their portfolios of sustainable products tailored for the Asian market. The China Coatings Industry Association reported that in 2023, a significant share of automotive OEMs in China had transitioned to water-based painting lines, significantly reducing environmental impact while maintaining superior finish quality.

MARKET RESTRAINTS

Stringent Environmental Regulations Affecting Conventional Coating Technologies

A significant restraint affecting the Asia Pacific automotive coatings market is the tightening of environmental regulations concerning volatile organic compound (VOC) emissions from solvent-based coatings. Governments across the region are enforcing stricter limits to combat urban air pollution and reduce industrial carbon footprints. Like, several Asia Pacific countries—including China, India, and South Korea—are actively phasing out high-solvent content coatings in favor of low-VOC or waterborne alternatives. This transition necessitates extensive reformulation and process modifications for coating manufacturers, increasing development costs and implementation timelines.

Volatility in Raw Material Prices and Supply Chain Disruptions

Another critical constraint impacting the Asia Pacific automotive coatings market is the fluctuation in raw material prices and ongoing supply chain disruptions. Key materials such as resins, solvents, pigments, and additives have experienced significant price volatility in recent years, primarily due to geopolitical tensions, trade restrictions, and pandemic-related logistical bottlenecks. Such volatility increases production costs for coating manufacturers, especially smaller players who lack vertical integration or long-term supplier contracts. Furthermore, supply chain instability continues to disrupt operations across the region. Also, these constraints force companies to maintain higher inventory levels and buffer stocks, reducing operational flexibility and increasing capital expenditure.

MARKET OPPORTUNITIES

Expansion of Electric Vehicle Manufacturing Driving Specialty Coatings Demand

The rapid adoption of electric vehicles (EVs) presents a major opportunity for the Asia Pacific automotive coatings market, particularly in the development and application of specialty coatings. Unlike traditional internal combustion engine (ICE) vehicles, EVs require advanced thermal management, corrosion protection, and electrical insulation solutions, creating demand for high-performance coatings tailored to battery casings, motor housings, and charging components. China leads this transition, with the EV sales seeing a a year-on-year growth. Japanese automakers such as Toyota and Honda have also accelerated their electrification programs, incorporating heat-resistant and conductive coatings in hybrid and plug-in hybrid models. South Korea and Singapore are also witnessing strong momentum in electric mobility, prompting local suppliers to develop compact, lightweight coatings compatible with battery-powered architectures.

Growth in Refinish and Aftermarket Coating Applications

The expansion of the automotive refinish and aftermarket segments represents another promising avenue for the Asia Pacific automotive coatings market. With the rising number of registered vehicles and aging fleet ages, there is an increasing need for maintenance, repair, and repainting services, particularly in countries with large pre-owned vehicle markets. Additionally, the rise in disposable incomes and improved access to financing options in countries like Indonesia and the Philippines are encouraging vehicle owners to upgrade their existing paint finishes for better aesthetics and protection. Like, independent bodyshops and third-party service providers are increasingly sourcing high-quality, compatible refinish coatings from regional manufacturers, opening new revenue streams beyond original equipment manufacturer (OEM) contracts.

MARKET CHALLENGES

Integration of Sustainable Coatings with Cost and Performance Constraints

One of the foremost challenges facing the Asia Pacific automotive coatings market is the integration of sustainable coatings while balancing cost efficiency and performance requirements. While regulatory pressures and consumer demand are pushing automakers and suppliers toward low-VOC and waterborne formulations, these eco-friendly alternatives often come at a higher production cost and may require changes in application techniques and curing conditions. Also, the implementation of water-based coating systems in automotive OEM lines can increase energy consumption due to longer drying times and higher oven temperatures, offsetting some of the environmental benefits. Balancing environmental compliance with economic viability remains a complex challenge for stakeholders across the Asia Pacific automotive coatings industry.

Intensifying Competition from Domestic and Global Players

The Asia Pacific automotive coatings market is experiencing heightened competition from both established global players and rapidly growing domestic manufacturers. Multinational corporations such as PPG, BASF, AkzoNobel, and Axalta dominate through technological leadership and long-standing relationships with major automakers. However, local firms in China, India, and Southeast Asia are aggressively expanding their production capacities and improving product quality to capture market share.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Resin Type, Vehicle Type, Technology Type, Coat Type, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | BASF SE, PPG Industries, Inc., Axalta Coating Systems, Akzo Nobel N.V., and Kansai Paint Co., Ltd. |

SEGMENTAL ANALYSIS

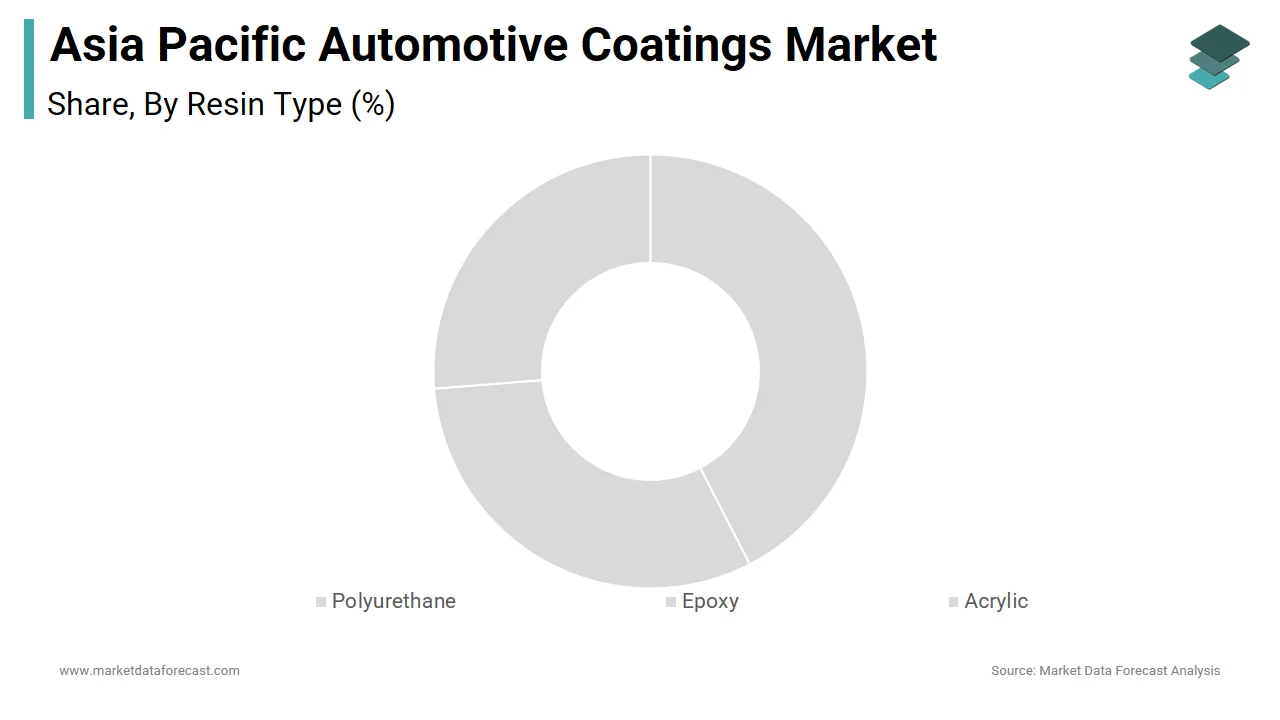

By Resin Type Insights

The polyurethane resin segment held the largest share of the Asia Pacific automotive coatings market by accounting for 42.1% of total consumption in 2025. This dominance is primarily attributed to its superior performance characteristics, such as flexibility, durability, chemical resistance, and excellent adhesion properties, making it ideal for both OEM and refinish applications. Additionally, polyurethane coatings are extensively used in automotive interiors, including instrument panels, door trims, and seating materials, where comfort and tactile feel are critical. Japanese automakers increasingly prefer polyurethane for soft-touch surfaces in premium vehicles, reinforcing its widespread usage across the region. Moreover, growing demand from commercial vehicle manufacturers for durable topcoat finishes has further strengthened polyurethane’s position in the market.

Acrylic resin is the fastest-growing segment in the Asia Pacific automotive coatings market, projected to expand at a CAGR of 7.8%. This growth is largely driven by the increasing adoption of waterborne acrylic coatings that align with stringent environmental regulations and sustainability goals across the region. Acrylic resins, particularly in aqueous form, offer low solvent content while maintaining color clarity and weather resistance, making them a preferred choice for eco-conscious manufacturers. In India, the Central Pollution Control Board mandated a phased transition toward low-VOC coating systems by 2025, prompting domestic bodyshops and OEMs to adopt acrylic formulations for basecoat applications. The Federation of Indian Chambers of Commerce and Industry (FICCI) noted a key year-on-year increase in acrylic coating procurement among Indian automotive paint suppliers in 2023.

By Vehicle Type Insights

The passenger cars dominate the Asia Pacific automotive coatings market by capturing 65.9% of total demand in 2025. This is because of the sheer volume of passenger vehicle production and sales across the region, particularly in China, India, and Southeast Asia. Rising disposable incomes and urbanization have significantly boosted vehicle ownership rates. Furthermore, governments in several countries are mandating improved aesthetic and corrosion-resistant finishes in new vehicles to enhance resale value and longevity.

The segment of commercial vehicles represented the fastest-growing segment in the Asia Pacific automotive coatings market, expanding at a CAGR of 7.2% from 2023 to 2030. This growth is primarily fueled by the rapid expansion of logistics, e-commerce, and freight transportation networks across the region. According to the ASEAN Automotive Federation, commercial vehicle production in Southeast Asia increased in 2023, driven by strong demand from transport companies seeking modern, fuel-efficient fleets. In response to evolving customer expectations, automakers are increasingly offering enhanced paint finishes even in entry-level commercial models to improve brand perception and resale value. Toyota, Isuzu, and Tata Motors launched new commercial vehicle lines in 2023 featuring high-durability coatings designed to withstand harsh operating environments. Furthermore, regulatory bodies in Australia and Japan have introduced guidelines encouraging better fleet maintenance and aesthetics, indirectly boosting the adoption of premium refinish coatings.

By Technology Type Insights

The solvent-based coatings segment held the largest share of the Asia Pacific automotive coatings market by accounting for 50.8% of total demand in 2025. Despite growing environmental concerns, solvent-based technology remains dominant due to its widespread use in refinish applications and certain OEM segments where fast drying times, ease of application, and compatibility with existing infrastructure are crucial. Similarly, in Indonesia and the Philippines, small-scale repair centers prefer solvent-based formulations for cost-effectiveness and quick turnaround.

The water-based coatings segment is emerging as the rapidly advancing segment in the Asia Pacific automotive coatings market, expected to grow at a CAGR of 9.1%. This surge is primarily driven by stringent environmental regulations and growing corporate commitments to sustainable mobility. Similar directives have been implemented in South Korea and Japan, compelling OEMs and bodyshops to upgrade their processes. Japanese automakers such as Toyota and Honda have integrated water-based painting lines into their EV and hybrid manufacturing platforms, emphasizing green credentials. In addition, Indian state pollution control boards have intensified enforcement actions against non-compliant bodyshops, accelerating the shift toward compliant coating solutions.

By Coat Type Insights

Clearcoat had the largest share of the Asia Pacific automotive coatings market by capturing 53.2% of total demand in 2025. Its dominance is attributed to its critical role in providing surface protection, gloss enhancement, and UV resistance, making it an essential component of modern automotive paint systems. Additionally, advancements in clearcoat formulations, such as scratch-resistant and self-healing technologies are driving adoption in premium and luxury vehicle segments. In India, rising consumer preference for glossy, high-durability exteriors has prompted domestic OEMs like Maruti Suzuki and Tata Motors to adopt advanced clearcoat layers even in mid-range models.

The basecoat is the fastest-growing segment in the Asia Pacific automotive coatings market, expanding at a CAGR of 8.3%. This growth is primarily driven by the increasing demand for vibrant, customizable color finishes and the shift toward environmentally friendly waterborne basecoat technologies. Korean automakers such as Hyundai and Kia have responded by incorporating low-VOC basecoat formulations in their latest model lineups.

COUNTRY LEVEL ANALYSIS

China stood at the forefront of the Asia Pacific automotive coatings market by contributing 40.7% of regional demand in 2025. As the world’s largest automotive manufacturer, China produces millions of passenger and commercial vehicles annually, each requiring multi-layer paint systems including primer, basecoat, and clearcoat to ensure protection and aesthetic appeal. Additionally, the country’s electric vehicle boom is further driving demand for specialty coatings that protect battery enclosures and improve thermal management efficiency.

India is quickly expanding. The country’s demand is driven by rising vehicle production, expanding middle-class purchasing power, and increasing penetration of high-quality paint finishes even in budget models.

Japan is a technologically advanced market with premium demand and is distinguished by its focus on high-efficiency, variable displacement, and electric compressors tailored for premium and hybrid vehicles. With one of the most mature automotive industries globally, Japan places a strong emphasis on fuel efficiency, emissions reduction, and occupant comfort. Japanese automakers such as Toyota and Honda have pioneered the integration of electric compressors in hybrid and plug-in hybrid models.

South Korea is characterized by its growing emphasis on electric mobility and high-tech thermal management solutions. With Hyundai and Kia aggressively expanding their EV portfolios, the demand for electric compressors has surged. In addition to OEM demand, South Korea is investing heavily in after-sales service infrastructure.

Thailand is serving as a key manufacturing hub for both domestic and export-oriented vehicle production. Major brands such as Toyota, Honda, and Isuzu operate large-scale plants in the country, all of which integrate air conditioning systems into their vehicle lineups.

KEY MARKET PLAYERS

Some of the noteworthy companies in the APAC automotive coatings market profiled in this report are BASF SE, PPG Industries, Inc., Axalta Coating Systems, Akzo Nobel N.V., and Kansai Paint Co., Ltd.

TOP LEADING PLAYERS IN THE MARKET

PPG Industries (USA, with major operations in China and India)

PPG is a global leader in automotive coatings and holds a dominant position in the Asia Pacific market. The company offers a comprehensive portfolio of OEM and refinish coatings, including waterborne and high-solid formulations tailored for sustainability and performance. PPG collaborates closely with major automakers across Japan, South Korea, and China to deliver innovative color technologies and protective finishes that enhance vehicle aesthetics and durability.

BASF SE (Germany, with strong presence across APAC)

BASF is a key player in the Asia Pacific automotive coatings industry, known for its advanced coating technologies and commitment to sustainable mobility. Through its Coatings division, BASF provides high-performance primers, basecoats, and clearcoats designed for both conventional and electric vehicles. The company has established strategic partnerships and R&D centers across China and India to support regional automotive growth and regulatory compliance.

Kansai Nerolac Paints Limited (India, with significant presence in Southeast Asia)

Kansai Nerolac is a leading coatings supplier in the Asia Pacific region, particularly in the Indian and ASEAN markets. The company specializes in automotive refinish coatings and industrial paint systems, offering cost-effective, environmentally compliant solutions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Expansion into High-Growth Markets through Local Manufacturing and Strategic Partnerships

Leading companies are strengthening their regional presence by setting up local production facilities and forming joint ventures with domestic players. These initiatives allow them to reduce logistics costs, comply with local regulations, and better serve growing automotive sectors in countries like India, Vietnam, and Indonesia.

Product Innovation and Customization for Diverse Applications

To meet evolving consumer and regulatory demands, key players are investing heavily in research and development to create specialized coatings that offer improved durability, aesthetic appeal, and environmental compliance. This includes developing low-VOC, fast-curing, and scratch-resistant formulations tailored for different vehicle types and usage conditions.

Focus on Sustainability and Eco-Friendly Coating Solutions

Amid rising environmental concerns, manufacturers are adopting green chemistry principles and enhancing product safety profiles. This includes reformulating solvent-based systems into waterborne alternatives and integrating circular economy practices into production processes to maintain competitiveness in environmentally conscious markets.

COMPETITION OVERVIEW

The competition in the Asia Pacific automotive coatings market is intense, characterized by a mix of global Tier-1 suppliers and rapidly growing regional manufacturers. Established players such as PPG, BASF, AkzoNobel, and Axalta dominate through technological leadership, long-standing relationships with major automakers, and continuous innovation in surface protection and aesthetic enhancement.

However, domestic firms in China, India, and Southeast Asia are aggressively expanding their capabilities, leveraging cost advantages and localized supply chains to capture market share. These regional players are increasingly matching international standards in quality and application performance, challenging traditional suppliers in mid-tier and budget vehicle segments.

Market participants are also navigating shifting regulatory landscapes, particularly concerning VOC emissions and environmental compliance, which are reshaping formulation strategies and application techniques.

RECENT MARKET DEVELOPMENTS

- In February 2024, PPG Industries opened a new technical center in Shanghai focused on developing next-generation waterborne coatings for the Chinese automotive sector, reinforcing its commitment to sustainability and regulatory alignment.

- In May 2024, BASF expanded its manufacturing facility in Maharashtra, India, to increase production capacity for high-performance automotive refinish coatings, aiming to strengthen its supply chain and customer reach in South Asia.

- In August 2024, Kansai Nerolac launched a new line of ultra-low VOC refinish coatings tailored for bodyshops across Southeast Asia, supporting the region’s shift toward eco-friendly painting solutions.

- In October 2024, Nippon Paint Automotive Coatings formed a joint venture with a leading Indonesian auto body manufacturer to develop customized paint solutions and improve after-sales service support in emerging ASEAN markets.

- In January 2025, Axalta Coating Systems partnered with a Japanese EV startup to co-develop lightweight, heat-reflective coatings for battery enclosures, aligning with the growing demand for thermal management solutions in electric vehicles across the Asia Pacific region.

MARKET SEGMENTATION

This Asia Pacific automotive coatings market research report is segmented and sub-segmented into the following categories.

By Resin Type

- Polyurethane

- Epoxy

- Acrylic

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

By Technology Type

- Solvent-based

- Water-based

- Powder-based

By Coat Type

- Clearcoat

- Basecoat

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC

Frequently Asked Questions

1. What factors are driving the Asia Pacific automotive coatings market?

The Asia Pacific automotive coatings market is driven by rapid vehicle production, rising consumer demand for durable and aesthetic finishes, technological advancements in eco-friendly coatings, and expanding automotive aftermarket services.

2. What challenges does the Asia Pacific automotive coatings market face?

The Asia Pacific automotive coatings market faces challenges such as volatile raw material prices, stringent environmental regulations, high production costs for advanced coatings, and increasing competition from local and global players.

3. What opportunities exist in the Asia Pacific automotive coatings market?

Opportunities in the Asia Pacific automotive coatings market include the growth of electric vehicles, development of water-based and low-VOC coatings, rising investments in R&D, and expanding automotive manufacturing hubs in emerging economies.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com